Real-Time Infection Detection Devices market Overview

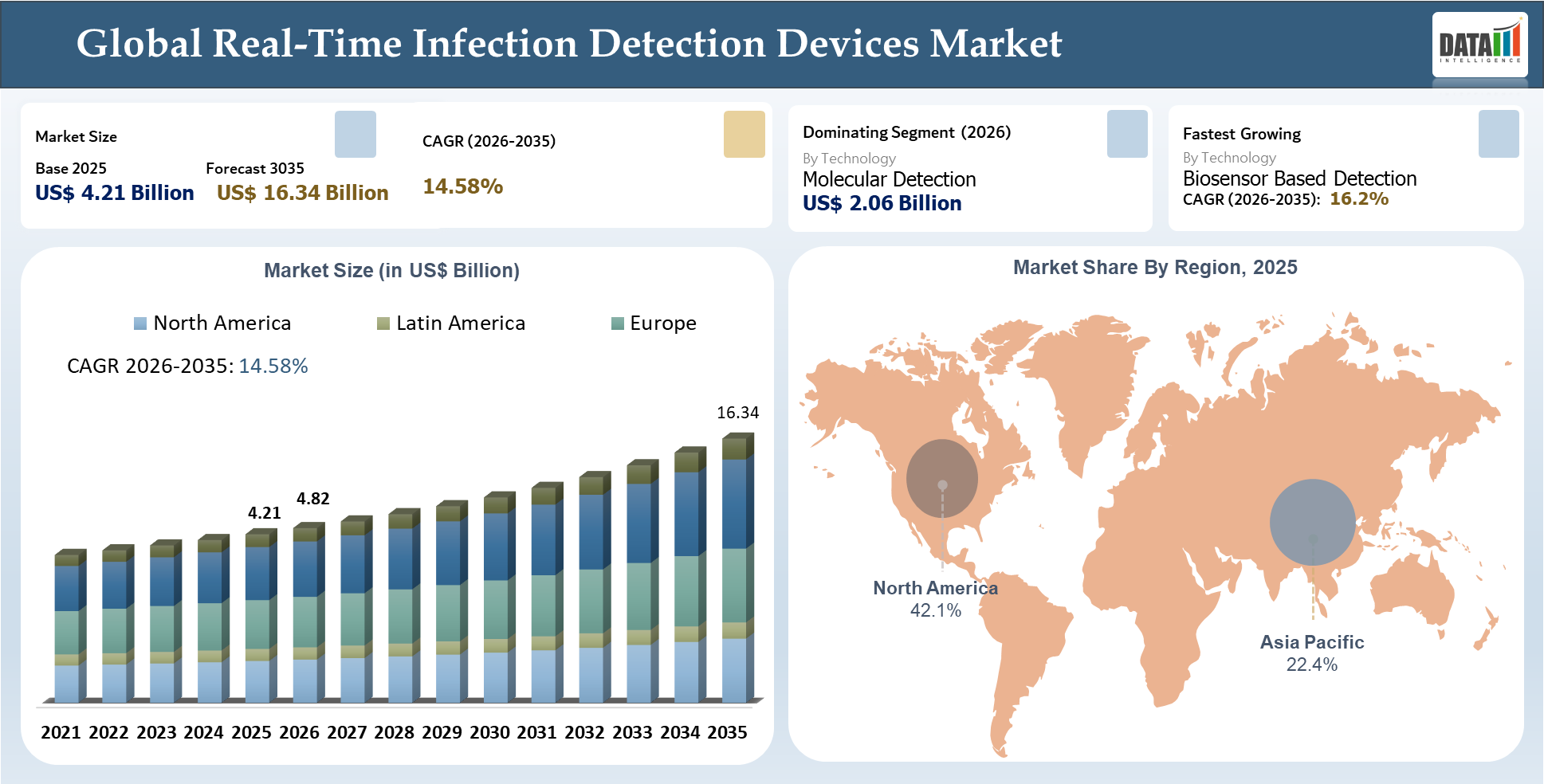

Real-Time Infection Detection Devices market size recorded $4.21 billion globally in 2025 and projected to grow to $16.34 billion by 2035, expanding at a CAGR of 14.58% throughout 2026–2035. With the increasing momentum in the global RTIDD industry, the need for prompt detection of infections, which allows for earlier diagnosis and treatment, continues to emerge among healthcare practitioners who recognize the potential for more effective patient management through real-time detection technology. The greatest demand will come from ICU, perioperative, emergency, and sepsis-prone patients whose clinical status can deteriorate if there is a time delay in infection verification.

The competition within the RTIDD market still exists as innovation and diversity continue to thrive in technologies. In addition, the growth within the market comes from developments in molecular detection, biosensors, wearable sensors, and point-of-care testing that facilitate quick detection, faster turnaround, and creation of actionable alerts. While decision-makers assess the devices according to their ability to detect pathogens, other areas of concern have started to appear, such as false alarm minimization, stability of the calibration process, and value to clinical workflow. Leading vendors include diagnostic firms, specialized infection monitoring companies, and platform suppliers.

AI Impact Analysis

Several subtle applications of artificial intelligence have a commercially valuable impact in the market for real-time infection detection devices. These include AI in design engineering, process automation, predictive maintenance, quality analysis, and demand sensing. It does not necessarily create a new market category; however, it enables performance augmentation of all stages in the existing value chain.

From the buyer’s perspective, the tangible impact of AI will be experienced in such areas as the reduction of waste, acceleration of cycle times, improvement in diagnostic accuracy, or facilitation of operations by reducing mistakes in system handling. Suppliers who successfully combine smart products with their service data are gaining a competitive advantage over companies that are selling pure products based only on hardware specifications.

Artificial intelligence has an impact on the commercialization activities of both sales and after-sales departments. On the sales side, customers can receive assistance in simulation, configuration, and usage analysis from sales reps, while after-sales can use the performance information for better management of renewals, parts, and service activities.

Key Takeaways

- The Real-Time Infection Detection Devices market was valued at USD 4.21 billion in 2025 and is projected to reach USD 16.34 billion by 2035, growing at a CAGR of 14.58%.

- Molecular Detection leads the technology segment, while Biosensor-Based Detection is witnessing strong adoption in high-value clinical applications.

- North America holds the largest market share, supported by advanced healthcare infrastructure, while Asia-Pacific is expected to register the fastest growth through 2035.

- Hospitals and diagnostic laboratories remain the leading end users, driven by increasing demand for rapid detection of sepsis, respiratory infections, and hospital-acquired infections.

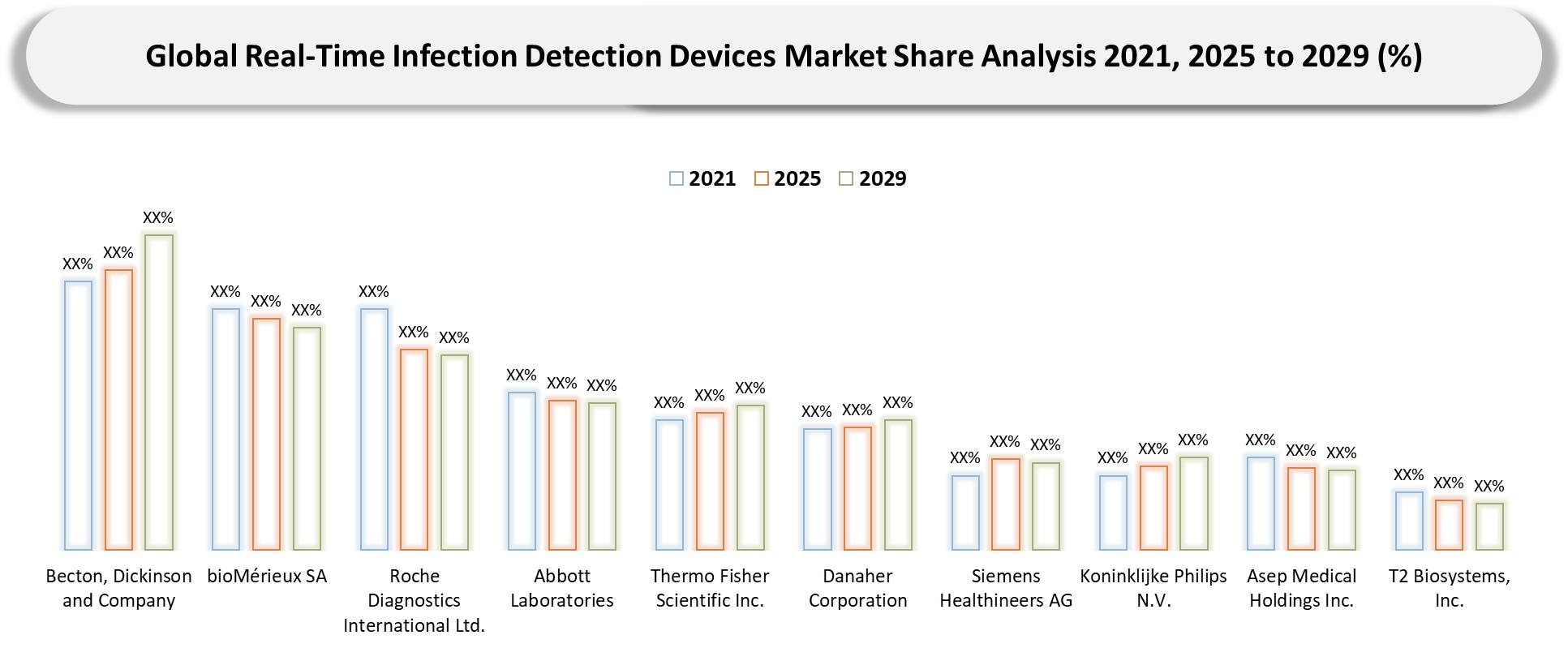

- Major players including Becton, Dickinson and Company, bioMérieux SA, Roche Diagnostics International Ltd., Abbott Laboratories, and Thermo Fisher Scientific Inc. are expanding their portfolios through product innovation and regulatory approvals.

Market Scope

| Metrics | Details |

| Market Size (2025) | USD 4.21 Billion |

| Market Size (2035) | USD 16.34 Billion |

| CAGR (2026-2035) | 14.58% |

| Historic Years | 2023-2024 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Segments Covered | Technology, Care Setting, Product Format, Application, End User, Region |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

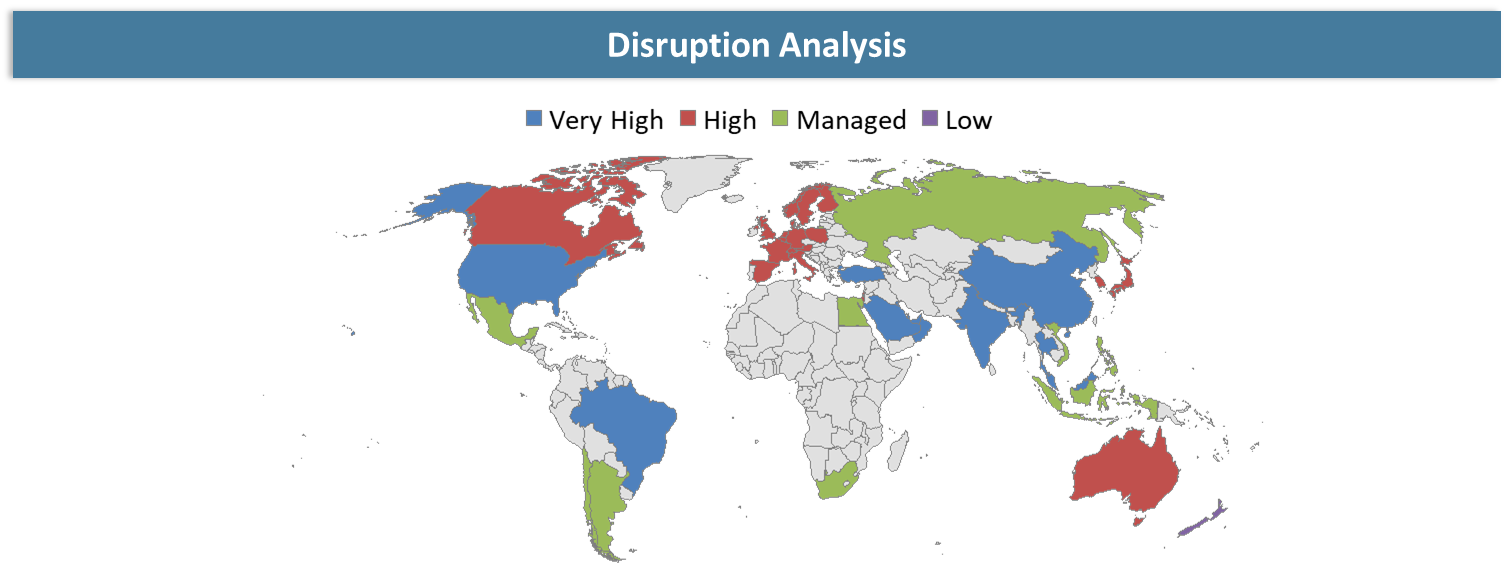

Disruption Analysis

Shift from Feature-Centric Innovation to Ecosystem-Driven, Outcome-Based Value Realization

The biggest disruption in the real-time infection detection devices market isn’t one launch or another. It’s the shift in the market itself away from generic functionality comparison toward measurable operational value. The old days of relying on a specification sheet or impressive innovation-speak are gone, as buyers want to know how quickly the device integrates, how well it operates at scale, and how rapidly it validates its budgetary impact.

There’s also a commercial disruption, whereby channel structures, integrations, and bundling opportunities drive customer evaluations. Indeed, in some instances, the vendor who can orchestrate the ecosystem around the technology wins out even when there is an equal player with superior core technology.

Further disruptions are occurring in the area of operational excellence. Customers want to know where the device comes from, who provides local support, how it behaves during a supply crisis, and what metrics are used post-deployment to measure success.

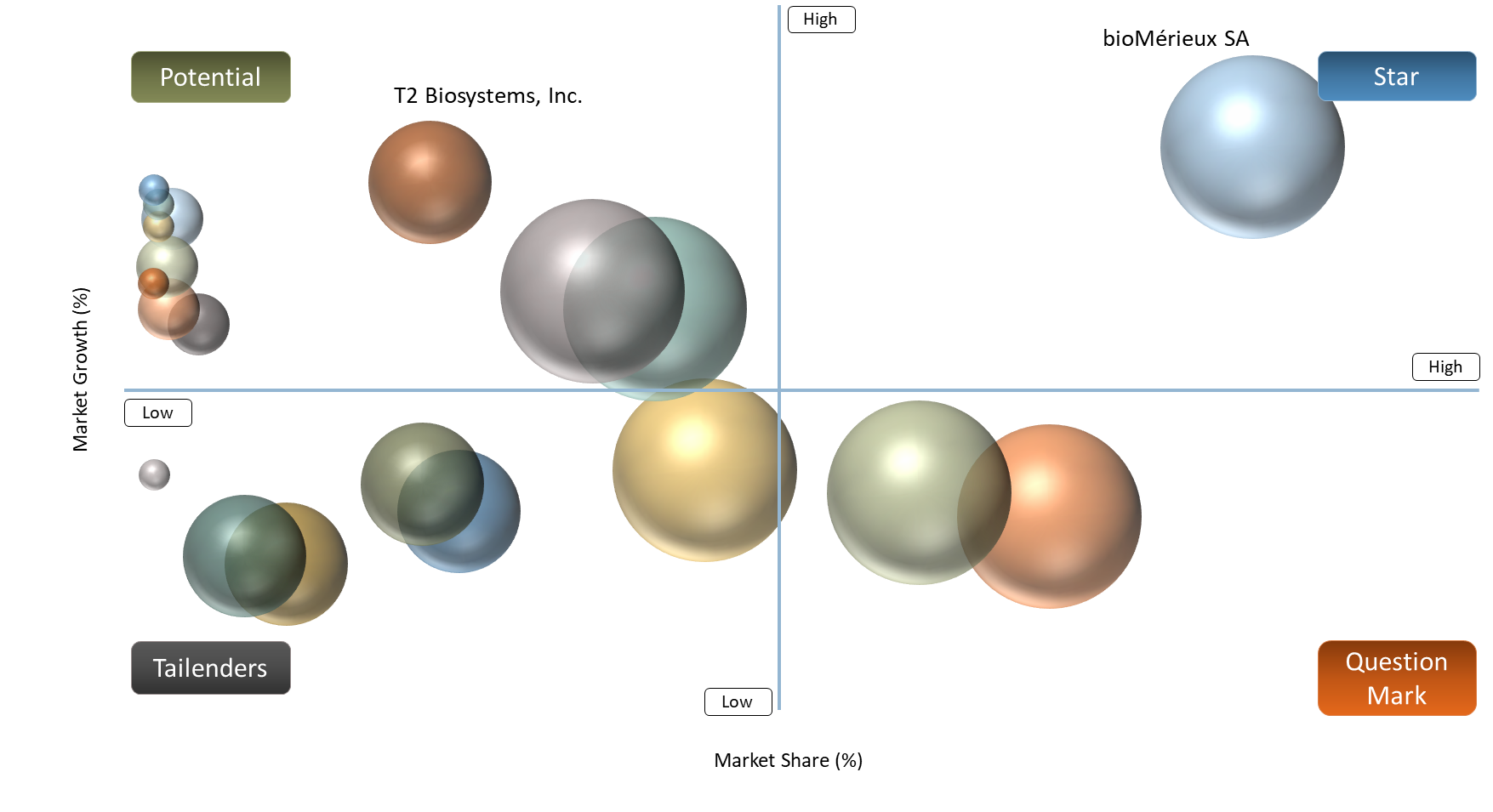

BCG Matrix: Company Evaluation

From a BCG perspective, the Stars in the real-time infection detection devices industry will be the vendors that have both demand momentum and control of the ecosystem. Firms such as Becton, Dickinson and Company, bioMérieux SA, and Roche Diagnostics International Ltd. will fit into this category if they can couple the product depth and distribution width with credibility of integration and ongoing expansion of accounts. It is not just that they have the majority share but also that they set customers’ expectations of a total solution package.

It is more likely that the incumbents with a strong existing installed base, wide geographic coverage, or enduring channels will occupy the Cash Cow space, regardless of how conservative they might be in comparison to the most aggressive rivals.

Question marks in this market can be newer specialists or even suppliers in adjacent markets that come into the market through a very narrow niche, like molecular detection or biosensor detection. They can have great potential if they can demonstrate differentiating results, but they may still require scale, partnering strength, or commercial validation. Dogs are often suppliers who continue to be too vulnerable to volume, ecosystem, or delivery concerns.

Market Dynamics

Shift toward measurable operating value and application-specific buying criteria

One of the key drivers of growth within the real-time infection detection devices market is the evolution of interest in the category into purchasing behavior motivated by quantifiable results. Increasingly, buyers are looking for a solution that will enable them to increase capacity, improve performance, decrease time to results, lessen labor costs, or create an entirely new revenue model. This evolution is critical since it places a premium on those companies that know the buyer's process well enough to make a business case for their solution.

A second dimension of demand involves the selection process followed by procurement groups. It no longer revolves exclusively around technical capabilities; rather, it considers ease of deployment, quality of vendor support, regulatory compliance, integration requirements, and even the validity of cost savings claims. This creates an additional incentive for buyers to concentrate their budgets on products like molecular detection and biosensor-based detection devices.

Ecosystem maturity is also helping drive further market expansion. With more customers able to rely on surrounding tools, service partners, connectivity layers, or manufacturing services that reduce risk from their initial decision, the decision itself can be better justified. This makes the addressable market larger.

End users also show less patience with solutions that generate unnecessary overhead post-installation. End users demand solutions that integrate seamlessly into their current environment and don’t require a redesign at each scale point. The resulting need for greater value is driving demand for more valuable suppliers.

Integration burden, compliance friction, and longer enterprise decision cycles

The main constraint within the market for real-time infection detectors is that sometimes the customer’s interest may not be directly related to the rapid adoption of the solution. Buyers encounter challenges related to implementation, validation, data or process limitations, and purchasing control.

Such barriers are especially common if the technology interferes with regulatory processes, involves large sums of money, interacts with existing legacy infrastructure, or involves multiple stakeholders. Manufacturers of such products often overestimate their ability to rapidly turn pilots into sales.

Segmentation Analysis

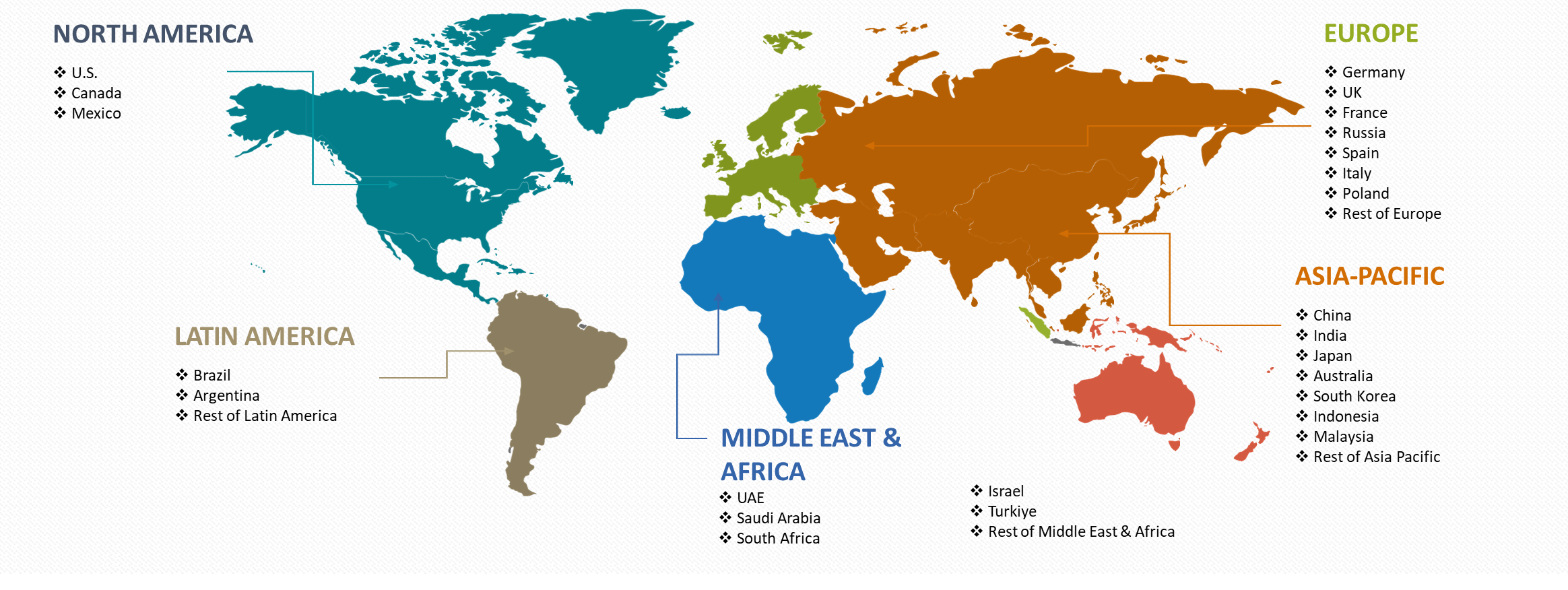

The global real-time infection detection devices market is segmented based on technology, care setting, product format, application, end-user, and region.

Technology Segment as the Core Lens for Market Economics and Strategic Positioning

The technology perspective offers the strongest foundation for evaluating the real-time infection detection devices market since it provides an accurate depiction of how the buying process truly takes place, namely with respect to feasibility, workflow compatibility, scalability, price rationale, and quantifiable ROI. In addition, it offers one of the most financially viable perspectives for segmenting the market to size it. This is because product offerings, demand trends, and applicability are easier to assess than in other, more overarching strategic perspectives.

From this perspective, the molecular detection and biosensor-based detection categories offer the greatest strategic value. Molecular detection usually enjoys greater and faster adoption owing to better compatibility with current clinical practices, higher institutional awareness levels, and less disruption within organizations. The financial attractiveness of the segment is further enhanced by the addition of service packages offered by vendors.

On the other hand, biosensor-based detection is more suited for high-value applications, where the importance of sensitivity, accuracy, and differentiation outweighs the advantages of ease of use. Even if uptake may be slower, the category typically carries higher account value, deeper strategic integration, and greater pricing flexibility.

This market does not follow a clear winner-take-all model. The realistic scenario is that of a two-tracked approach, where Molecular Detection leads the charge in terms of volume growth, and Biosensor Based Detection handles the premium and strategic opportunities. Companies capable of competing on both fronts have the upper hand in market leadership.

Geographical Penetration

North America Accelerating Real-Time Infection Detection Devices Adoption Through Clinical Integration, Procurement Sophistication, and Outcome-Driven Commercialization

North America represents the most impactful geographical market in the real-time infection detection device market due to its ability to capture how the category is developing in actual care environments as opposed to mere demand numbers. It increasingly serves as the driving force in how suppliers consider the issues of commercialization, integration, and positioning in the market. Buyers are no longer looking at how suppliers' technology solves infection detection as standalone diagnostics.

Rather, the focus has shifted to how it helps in improving triaging time, promoting antimicrobial stewardship, lowering the risk of escalation, and supporting the flow of the process in ICU and emergency settings. North America becomes particularly important when trying to identify areas with a concentration of revenue generation. What sets North America apart from other geographies is its need for evidence on what kind of value a particular solution brings to the buyer. The evidence is sought not only in terms of the ability to implement the solution fast and perform under pressure, but also in terms of the supplier's reliability in servicing and training users.

U.S. Real-Time Infection Detection Devices Market Trends

The United States represents a market worth special consideration in real-time infection detection devices for a variety of reasons. Firstly, the U.S. is a significant market when it comes to setting the direction in this category, supplier strategies, and commercial opportunities. While there is no shortage of buyers, the market is becoming less about demand and more about the increasing complexity of evaluations that hospitals use to assess new products. Instead of simply listing features, buyers are now asking questions about speed of adoption, ease of interoperability, workflow fit, and overall clinical and economic impact.

Infection detection devices are now being evaluated for how effectively they help patients be identified and prioritized for intervention, for their impact on reducing sepsis and improving antimicrobial stewardship, and for their potential to speed up critical decisions in acute environments. The United States becomes an especially relevant market in identifying what companies are able to deliver on the operational outcomes of technology. Finally, in recent years, success in this space has increasingly required ecosystem collaboration. Companies that are able to complement outstanding device performance with a solution approach are winning more often than those focused only on the device.

Canada Real-Time Infection Detection Devices Market Outlook

The Canadian market is one such example of a strategic and selective market in the real-time infection detection devices sector since the adoption process in this market is primarily driven by clinical utility, system integration, and applicability to patient care pathways rather than simply size considerations. The Canadian market is particularly relevant to evaluate infection detection solutions in publicly funded health systems where end users consider factors such as system integration, ease of implementation, and clinical benefits during their purchasing decisions. Additionally, the Canadian market illustrates the need for infection detection solutions in decentralized healthcare systems in which timely detection can make a substantial difference in care planning and resource utilization. Furthermore, Canada is also a relevant market in which premium niches and opportunities may be identified. This market would allow us to assess infection detection solutions in markets where product reliability, localized support, and integration outweigh commercial aspects such as pricing and promotion.

Competitive Landscape

- The competitive environment within the real-time infection detection devices industry is characterized by the distinct separation of large diagnostics companies and specialists in this sphere. For instance, the most successful market participants in terms of competitive advantage can include Becton, Dickinson and Company, bioMérieux SA, Roche Diagnostics International Ltd., Abbott Laboratories, and Thermo Fisher Scientific Inc., who enjoy the benefits of diverse portfolios, existing customer base, wide geographical presence, and higher level of influence on the purchase decisions made by hospitals and laboratories.

- Nevertheless, specialists and medium-sized companies in turn can be able to win their place within this industry through the provision of more focused products, quick deployment of the systems, precise targeting of their solutions at niche clinical needs, and more efficient customer service. In today's market, competition can be viewed not as a question of technical superiority of the solution provided by vendors, but as buyers' assessment of its integration into clinical practice, ease of use, support, interoperability, and overall value delivery in practice.

- With time, competitive positions can be obtained by those vendors who combine technological know-how with partner relations and commercial efficiency in high-value areas, including molecular detection and biosensor-based solutions.

Key Developments

- February 2026: bioMérieux received IVDR CE-marking for the BIOFIRE SPOTFIRE R/ST plus Panel and R/ST plus Panel Mini, expanding near-patient real-time detection of respiratory and sore throat infections in Europe.

- March 2026: QIAGEN received U.S. clearance for Gastrointestinal Panels on the QIAstat-Dx Rise system, strengthening higher-throughput syndromic infection testing for gastrointestinal pathogens.

- January 2026: Roche’s 2025 annual reporting confirmed continued expansion of its cobas liat point-of-care infectious disease testing portfolio, including STI and Bordetella infection detection offerings launched and cleared across 2025.

- September 2025: QIAGEN gained U.S. clearance for the higher-throughput QIAstat-Dx Rise platform, expanding automated rapid syndromic testing capacity for infectious disease diagnostics.

- August 2025: bioMérieux received U.S. FDA 510(k) clearance and CLIA waiver for Anterior Nasal Swab use with the BIOFIRE SPOTFIRE R/ST Panel Mini, improving flexibility in respiratory infection testing.

- March 2025: QIAGEN received U.S. clearance for the QIAstat-Dx Gastrointestinal Panel 2 Mini B, expanding outpatient-focused rapid detection of gastrointestinal infections.

- January 2025: Roche received FDA clearance with CLIA waiver for cobas liat CT/NG and CT/NG/MG assays, strengthening point-of-care molecular infection detection for sexually transmitted infections.

- November 2024: QIAGEN received FDA clearance for the QIAstat-Dx Meningitis/Encephalitis Panel, extending real-time molecular infection detection into central nervous system infections.

- October 2024: QIAGEN received FDA clearance for the QIAstat-Dx Respiratory Panel Mini, supporting faster outpatient respiratory infection diagnosis.

- June 2024: bioMérieux received U.S. FDA 510(k) clearance and CLIA waiver for the BIOFIRE SPOTFIRE R/ST Panel Mini, strengthening decentralized respiratory and sore throat infection detection at the point of care.

DMI Opinion

As per DataM, the key challenge for real-time infection detection devices will be proving that there is demand for the solution, and not who is able to fulfill it first. It is increasingly clear that vendors with solutions that are operationally feasible in deployment in hospitals, ICU settings, and point-of-care locations will be preferred over those that are still at the pilot evaluation phase. Buyers have evolved from pilots to using real-time infection detection devices only for specific purposes like sepsis testing, respiratory infections, and antimicrobial stewardship.

However, DataM notes that a large number of vendors are overly optimistic about their capabilities in terms of product accuracy and underrate other aspects of product development, like workflow suitability, ease of use, integration ability, and service support after deployment.

Hence, it can be concluded that the focus of competition has shifted to use cases where there is significant value rather than broad-spectrum offerings.

Why Choose DataM?

- Innovation in Technology: Reviews innovative developments in the area of technology related to real-time detection of infections, such as molecular detection technology, biosensor-based systems, POC technology, artificial intelligence algorithms, connectivity, and diagnostic workflow solutions.

- Supplier Performance and Positioning Analysis: Provides a review of various supplier performance and their positioning in the context of hospitals, ICUs, ERs, laboratories, and other decentralized care environments. This evaluation focuses on comparing the suppliers in terms of speed, sensitivity, specificity, integrability, and other aspects of performance.

- Real-World Evidence: Illustrates case studies and practical examples from hospitals regarding the use of real-time infection detection devices in the management of sepsis, respiratory infection screening, antimicrobial stewardship, bed-side triaging, and more.

- Market Update and Industry Evolution: Follows industry updates in terms of the launch of new products/services, regulatory clearance, shift in reimbursement, hospital IT evolution, infection monitoring priorities, and geographical adoption trends in North America, Europe, Asia Pacific, the U.S., and Canada.

- Competitive Strategy: Examines the strategy of key players in consolidating their positions via platform extension, service offering integration, channeling, menu extension, commercialization in specific geographies, and differentiation based on ecosystems.

- Pricing and Market Access: Details about price competition among competitors on molecular, biosensor, and point-of-care platforms, pricing models such as instrument/consumables model, bundled services, and enterprise agreements, in addition to market access strategy impacting adoption.

- Market Entry & Growth: Growth opportunities in acute care, decentralized diagnostics, and infection monitoring, along with approaches for vendors to capitalize on by way of partnerships, fit in workflows, regulatory preparedness, and other factors.

Target Audience 2026

- Corporate Strategy and Market Intelligence Teams: Teams evaluating market attractiveness, competitive dynamics, regional opportunities, pricing trends, and long-term growth potential in real-time infection detection devices.

- Business Development Leaders: Leaders identifying new growth avenues, strategic partnerships, expansion opportunities, and entry into new clinical or geographic markets.

- Sales and Channel Leaders: Teams focused on customer acquisition, key account management, distributor strategy, and improving market access across hospitals, diagnostics networks, and care settings.

- Investors and Private Equity Firms: Stakeholders tracking investment opportunities, market consolidation, technology differentiation, and long-term value creation in infection detection technologies.

- Procurement and Sourcing Teams: Decision-makers assessing supplier reliability, cost structures, service capabilities, and supply chain resilience for infection detection devices and related solutions.

- Technology and Operations Leaders: Healthcare and lab operations leaders evaluating deployment feasibility, workflow integration, system interoperability, and real-world performance.

- Consulting and Advisory Teams: Firms supporting clients with market entry strategies, competitive benchmarking, growth planning, and investment due diligence in the infection detection devices market.