Reagent Grade Gases Market Overview

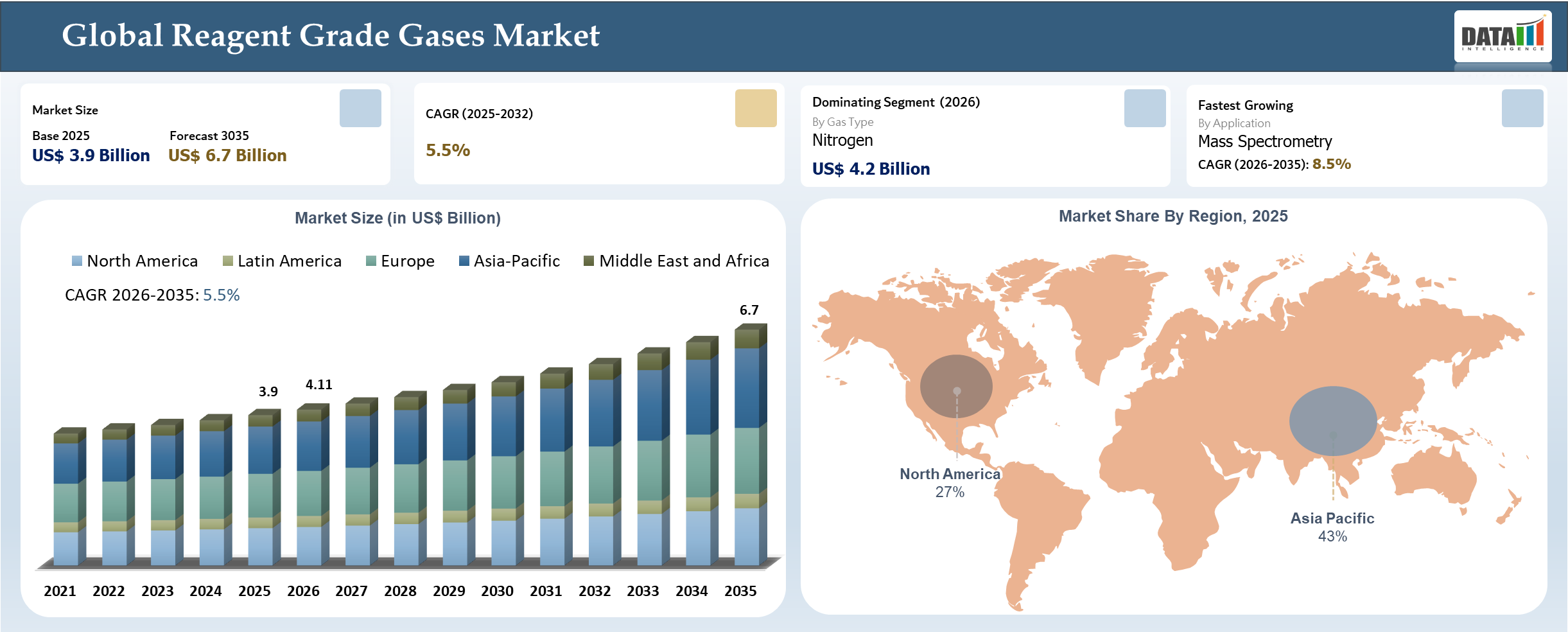

The global Reagent Grade Gases Market reached US$ 3.9 billion in 2025 and is expected to reach US$ 6.7 billion by 2035, growing with a CAGR of 5.5% during the forecast period 2026-2035. Reagent Grade Gases Market involves the key offerings, distribution systems, and services impacting the commercial purchasing decisions and preferences of buyers for such products. The structural makeup of the market involves the classification of gases on the basis of various factors including their type, purity, mode of delivery, packaging method, applications and users; and the earning potential of companies depends highly upon how well they adhere to performance benchmarks.

It can be said that the market is gradually shifting from pricing and availability towards a performance-based approach for evaluating vendors and suppliers in this industry. Buyers are now concerned with efficiency and risk minimization and other factors which have forced the suppliers to make changes in their product portfolios and services offering them according to different applications and localizing their distribution capabilities.

AI Impact Analysis

AI appears to be that of an enabling layer rather than that of a stand-alone driver in terms of its influence on decision-making in the reagent grade gases industry. It is used by firms in improving their demand forecasting and portfolio management efforts as well as focusing on high value accounts where they can tailor their offerings in accordance with customer needs. Given the nature of this market in terms of fragmentation and varied purchasing patterns, such a step could have an important impact in terms of maximizing sales revenue potential.

Through the use of performance data and information gathered through field-level interactions with customers as well as from other sources, AI is helping reduce the need for companies to make use of trial-and-error strategies when developing new products and services. The result could be an acceleration in product cycles along with solutions for particular applications being developed. Competitive advantage for suppliers could also depend on making use of installed base data and field operations information.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 3.9 Billion | |

| 2035 Projected Market Size | US$ 6.7 Billion | |

| CAGR (2026-2035) | 5.5% | |

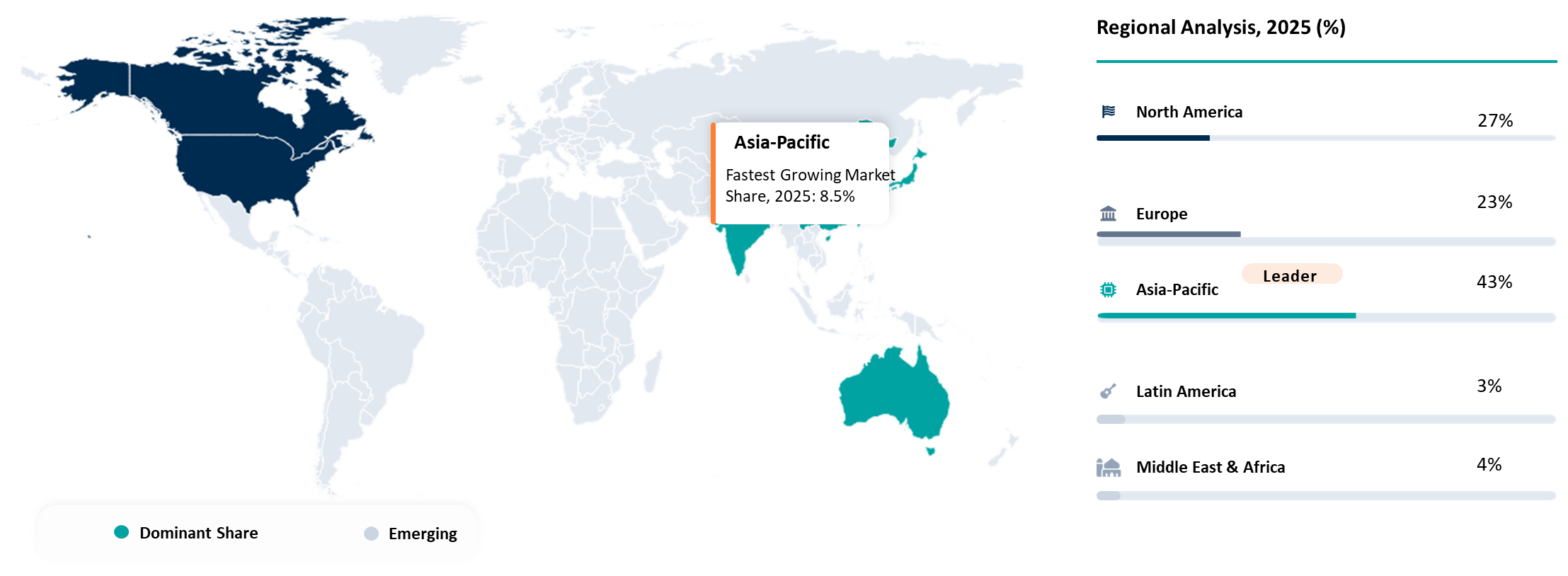

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By GasType | Nitrogen, Hydrogen, Helium, Argon, Oxygen, Carbon Dioxide, Specialty Gas Mixtures | |

| By Purity Grade | Ultra High Purity, Research Grade, Analytical Grade, Calibration Grade | |

| By Supply Mode | Cylinders, Bulk and Microbulk, On Site Generation, Portable Canisters | |

| By Packaging | Returnable Cylinders, Non Returnable Cylinders, Tube Trailers, Cryogenic Containers | |

| By Application | Analytical Instruments, Laboratory Research, Semiconductor and Electronics Testing, Environmental Testing, Pharmaceutical and Biotech, Calibration and Validation | |

| By End-User | Academic and Research Institutes, Testing Laboratories, Pharmaceutical and Biotech Companies, Semiconductor Manufacturers, Hospitals and Clinical Labs | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Value Redefinition and Ecosystem Convergence Reshaping Competitive Advantage in Reagent Grade Gases

The major disturbance in the market for reagent grade gases is a shift in the value definition from traditional performance specifications to metrics such as uptime, compliance, yield, and total cost of ownership. The resulting increase in buyer demand for performance will drive suppliers to focus on value creation and innovative products rather than commodity offerings, as they try to meet the rising buyer expectations.

At the same time, ecosystem convergence changes the competition dynamic, requiring suppliers to develop comprehensive solutions or strategic collaborations to compete effectively, as well as making it difficult for customers to switch suppliers. In this environment, companies are unlikely to succeed through large product portfolios alone, unless their efforts are accompanied by relevant innovations. On the other hand, new entrants can gain competitive advantage by concentrating on specific high value segments or through more commercially-oriented approaches.

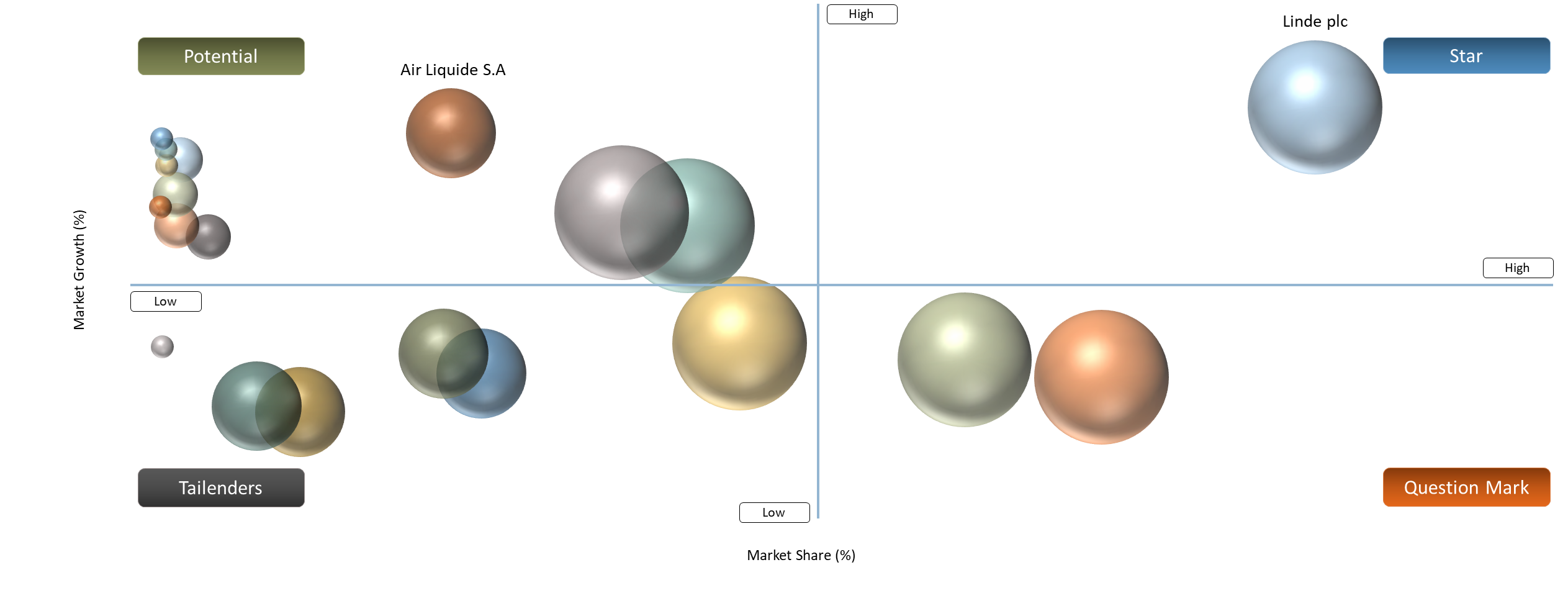

BCG Matrix: Company Evaluation

The market leadership quadrant is spearheaded by Linde plc, Air Liquide S.A., and Air Products and Chemicals, Inc., backed by excellent global market shares and sophisticated technology in ultra-high purity and reagent-grade gases manufacturing. Messer SE and Co. KGaA and Nippon Sanso Holdings Corporation provide robust support to this segment with innovations in semiconductors and specialty gases. Established Performance Quadrant is occupied by Matheson Tri-Gas, Inc. and Air Water Inc., who benefit from consistent demand for their products across healthcare, laboratory, and electronics industries. Iwatani Corporation and SOL S.p.A. perform consistently due to the diverse range of applications.

The emerging growth quadrant consists of SIAD S.p.A., Westfalen AG, and Yingde Gases Group Company Limited, who are gradually increasing their presence in high purity and specialty gases but have not yet achieved global presence. Gulf Cryo Holding C.S.C. and Coregas Pty Ltd. have gained momentum by expanding regionally. The niche and specialized quadrant consists of Bhuruka Gases Limited, Ellenbarrie Industrial Gases Ltd., Resonac Holdings Corporation, Norco, Inc., and Taiyo Gases Co., Ltd.

Market Dynamics

Expansion of Installed Analytical Base and Regulated Testing Demand Driving Certified Gas Consumption

The main growth factor in the reagent grade gases industry is the growing number of analyzers in combination with the complexity of regulations governing the processes of testing, which necessitate using purified gases. In the decision-making process, an emphasis is placed on value factors like reliability, return on investment, and operational effectiveness. Therefore, this growth factor plays a key role for both new system purchases and reorders.

Another benefit of this growth factor is improved demand visibility through tying consumption rates to operational metrics such as number of analyzers, volume of testing, and production volume. From the perspective of suppliers, this growth factor promotes the development of business models that can provide standardization in combination with customized offerings, which allows them to scale their operations while remaining relevant to applications.

High Logistics Complexity and Helium Tightness Constraining Market Scalability

One major restraint on the reagent grade gases market is the availability of helium supplies and expensive delivery of specialty gases. These two conditions can cause delays in product qualification and limit the volume of production available and its pricing power. The challenge is experienced even in cases of high demand since the above limitations can hinder the ability of producers to generate sustainable order volumes, especially those demanding high levels of purity.

The problem becomes even more relevant in markets where there is a lack of established standards and an ever-changing regulatory landscape or inefficient delivery systems. In such cases, proper commercialization of these products becomes difficult due to poor implementation strategies and inadequate spending visibility. Consequently, proper sizing of the market is done based on segments with better spending visibility.

Segmentation Analysis

The global reagent grade gases market is segmented based on gas type, purity grade, supply mode, packaging, application, end user and region.

Nitrogen Solidifying Its Position as the Core Enabler of Purity-Critical Operations and Long-Term Supplier Lock-In

Nitrogen remains the primary utility gas used in the reagent grade gases industry owing to its extensive application in inerting, purging, instrumentation, and decontamination. In high-end settings, the decision making regarding procurement is no longer guided by its economic attributes but rather its performance characteristics such as moisture control, particulate stability, and transportation efficiency, which have direct implications on the production process.

Reagent grade gases are becoming increasingly significant for semiconductor and analytical applications in scenarios that require constant purity and process stability. Modes of supply, including on-site manufacturing, cylinder, and micro bulk, are progressively determined by their level of contamination and suitability to the workflow processes. Economically, nitrogen also provides an entry into long-term vendor relationships, since qualification through purity and logistics results in a high cost of switching, enabling recurrent revenue streams from reagent gases.

Geographical Penetration

Asia-Pacific as the Strategic Hub for High-Purity Gas Demand and Supply Chain Localization

The Asia-Pacific region is the most important geographical area in the reagent grade gases market, it is witnessing significant commercial activities, as well as some changes in operations and future demands. The main reason behind the importance of the region is the presence of many electronic manufacturers, as well as analytical labs and industrial processes, which requires more sophistication to meet their needs in terms of packaging and service applications.

Moreover, there are several reasons for raising demand in the region, which includes increasing investments in the semiconductors industry, along with focusing on meeting higher quality standards for the process. Another significant trend for reagent grade gases and their precursors is the emergence of localization, since it is the answer to the disruptions in the global supply chain.

South Korea Reagent Grade Gases Market Trends

As far as its significance within the reagent grade gases sector is concerned, South Korea occupies a very important place because its demand for reagents depends on the semiconductor production capacity build-up and increased concerns about materials safety issues. Deals on ultra-high purity gas supply that are related to major semiconductor fabrication facilities contribute to setting standards higher within the whole sector.

The main competitive factors in South Korea’s market have shifted from volume to reliability, purity level, and integration capability within the fab facilities. As a result, adjacent segments such as laboratory gases and specialty gases are impacted by the trends as well. On the other hand, there is an evident tendency towards localization within the market, which makes it even more relevant when discussing the topic of premium gases strategies.

Japan Reagent Grade Gases Market Outlook

The Japanese market continues to be an important player in the reagent grade gases market due to its high standards in terms of analysis and its strength in electronics, advanced materials, and precision engineering applications. The Japanese market is known for favoring suppliers that have the capability to provide consistent performance reliability rather than those who offer cheaper products.

In the Japanese market, customer requirements have much to do with process discipline, which means that documentation processes, cylinder handling procedures, and contamination control play a role in decision-making. In terms of capital expenditures in the semiconductor and advanced manufacturing industries, the Japanese market becomes a benchmark in terms of the supply of packaged gas of higher quality.

Competitive Landscape

- The competitive landscape is led by a mix of global leaders and focused specialists, with Linde plc, Air Liquide S.A., Air Products and Chemicals, Inc., and Messer SE and Co. KGaA shaping category standards. Market positioning depends on portfolio breadth, application depth, route to market strength, and the ability to support customers after the initial sale.

The strongest companies are using product upgrades, partnerships, regional manufacturing, and selective vertical focus to defend share. As the market matures, leadership is likely to concentrate further around suppliers that can translate technical capability into faster commercialization and stronger customer retention.

Key Developments

- August 2025: Air Liquide acquired DIG Airgas to strengthen its semiconductor-grade and high-purity gas portfolio in Asia, supporting advanced electronics manufacturing demand.

- April 2026: Air Liquide invested in Japan to expand ultra-high purity gas production for next-generation semiconductor fabrication and AI chip manufacturing.

- April 2026: Linde plc announced a new air separation unit in the U.S. to increase supply of high-purity oxygen, nitrogen, and argon for electronics, healthcare, and analytical applications.

- July 2025: Linde plc expanded its industrial gas infrastructure in Texas to support aerospace and high-spec manufacturing requiring ultra-high purity gases.

- March 2026: INOX Air Products planned a $1 billion IPO to fund expansion of production and distribution of specialty and high-purity gases for pharma, healthcare, and laboratory applications.

- March 2026: Air Liquide opened a helium production facility in Taiwan to address semiconductor-grade gas shortages and strengthen supply of high-purity gases for chip fabrication.

- April 2026: Linde plc announced a new air separation plant in North Carolina to expand production of high-purity oxygen, nitrogen, and argon for industrial and analytical applications.

Why Choose DataM?

- Technological Innovations: Focuses on advancements in reagent grade gases, including ultra-high purity refinement techniques, advanced gas handling and delivery systems, real-time monitoring and analytics integration, improved cylinder and micro-bulk packaging, and application-specific gas mixtures, all of which enhance process accuracy, regulatory compliance, and operational efficiency across laboratory, semiconductor, and specialty manufacturing environments.

- Product Performance & Market Positioning: Assesses how suppliers perform across laboratory, semiconductor, pharmaceutical, and specialty manufacturing environments by comparing parameters such as purity consistency, contamination control, supply reliability, packaging formats, and application compatibility, highlighting how leading players differentiate through technical precision and service capability.

- Real-World Evidence: Highlights practical use cases of reagent grade gases in analytical testing, semiconductor fabrication, calibration processes, and controlled manufacturing environments, demonstrating measurable improvements in process accuracy, compliance adherence, yield stability, and operational efficiency.

- Market Updates & Industry Changes: Tracks key developments including capacity expansions, purification technology upgrades, new specialty gas introductions, localization initiatives, evolving regulatory standards, and shifts in demand across major regions such as North America, Asia-Pacific, China, and India.

- Competitive Strategies: Analyzes how leading suppliers strengthen market position through distribution network expansion, localized production, strategic partnerships, application-specific solutions, and differentiation based on purity assurance, delivery reliability, and integrated service offerings.

- Pricing & Market Access: Explains pricing dynamics across bulk, cylinder, and micro-bulk supply modes, factoring in purity grades, logistics complexity, and service requirements, while also evaluating distribution reach, contract structures, and supply agreements that influence market accessibility.

- Market Entry & Expansion: Identifies growth opportunities driven by increasing analytical intensity, semiconductor investments, and regulatory-driven testing demand, while outlining strategies for scaling through regional supply infrastructure, partnerships, and enhanced after-sales and technical support capabilities.

Target Audience 2026

- OEMs and product developers active across the reagent-grade gases value chain

- Distributors, channel partners, and regional aggregators

- Strategy teams, product managers, and corporate development leaders

- Procurement heads and technical buyers at key end users

- Investors, consultants, and market intelligence teams tracking emerging growth pockets