Psilocybin Market Snapshot

| Metric | Details |

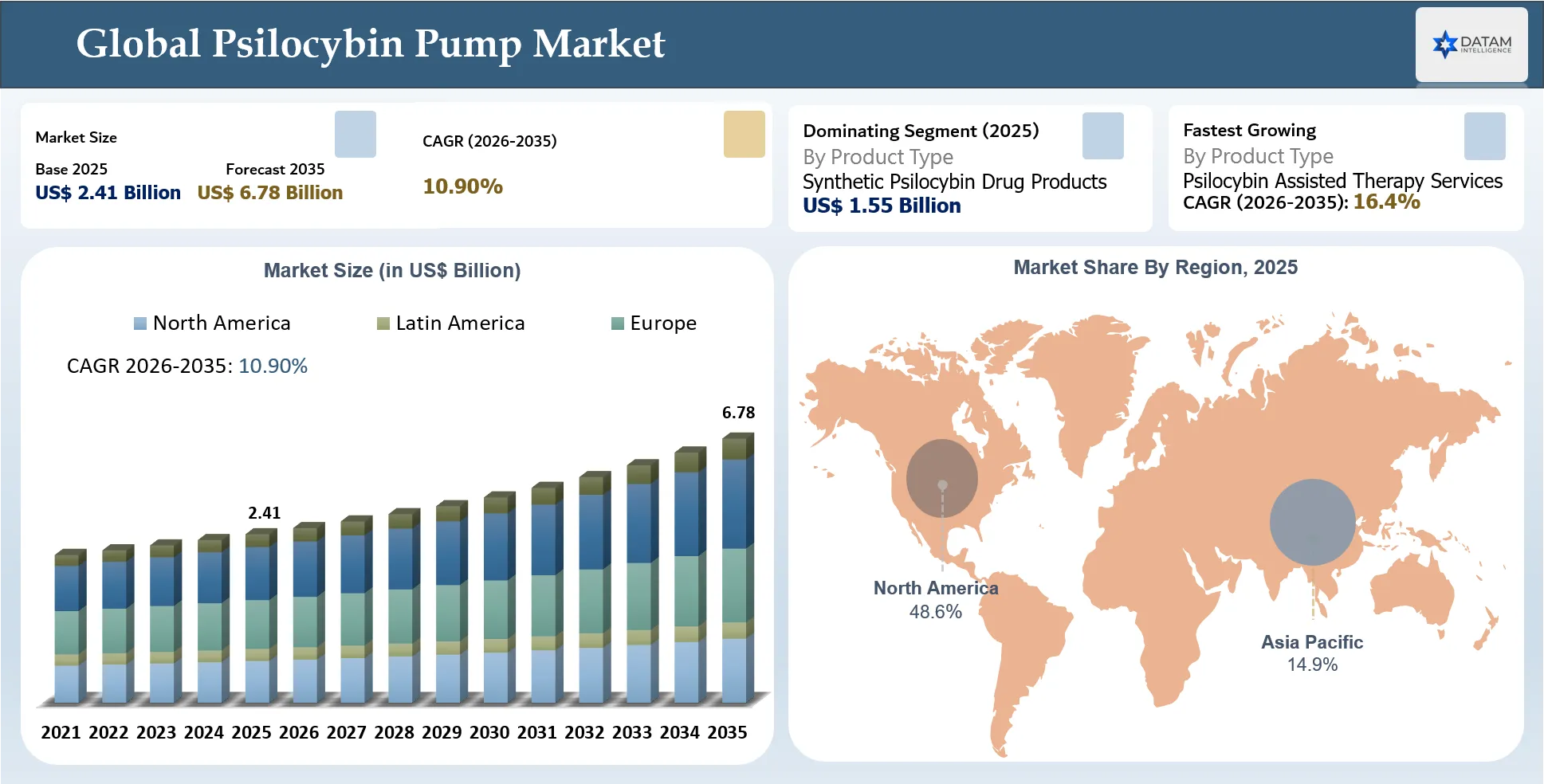

| Global Market Size (2025) | USD $2.41 Billion |

| Projected Market Size (2035) | USD $6.78 Billion |

| CAGR (2026–2035) | 10.90% |

| Largest Segment Name | Synthetic Psilocybin Drug Products |

| Largest Segment Share | 64.20% |

| Fastest Growing Segment Name | Psilocybin Assisted Therapy Services |

| Fastest Growing Segment Share / CAGR | 16.40% |

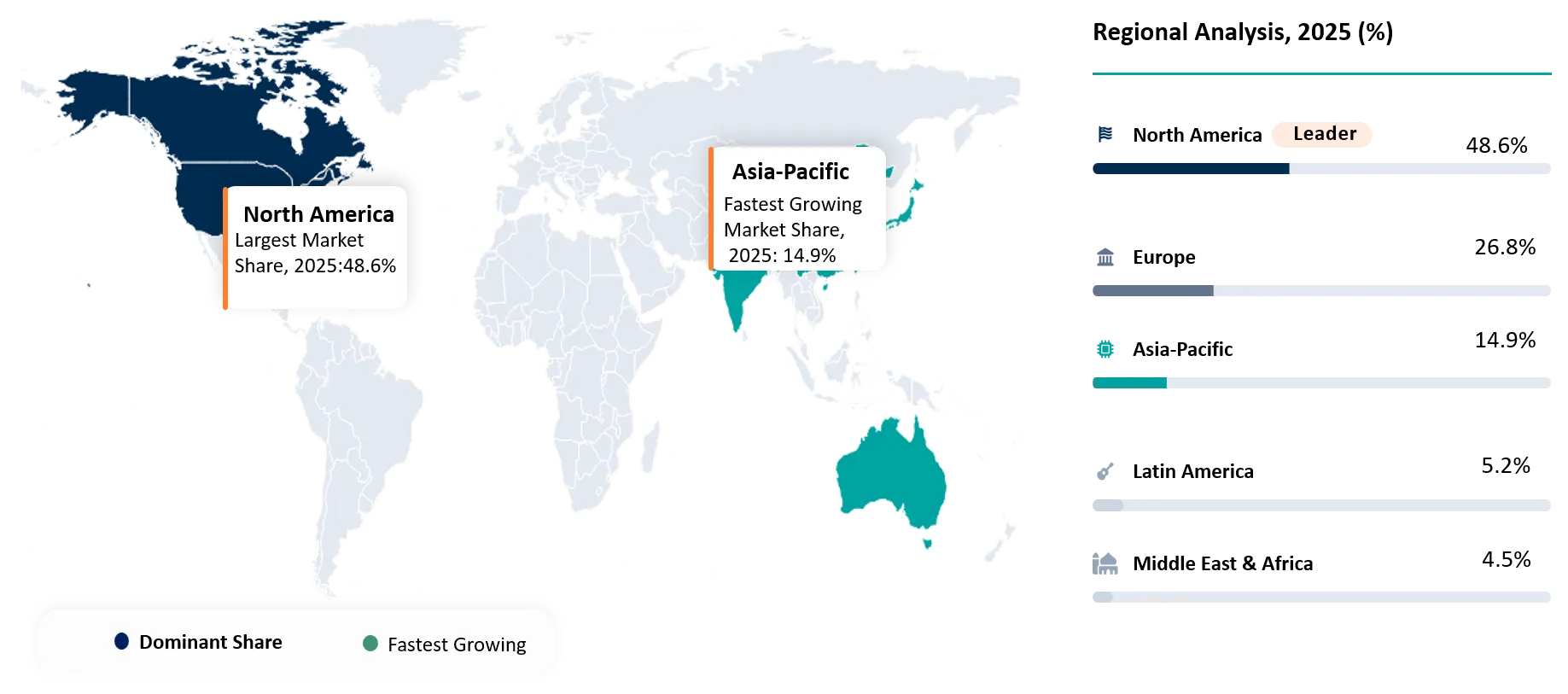

| Largest Region Name | North America |

| Largest Region Share | 48.60% |

| Fastest Growing Region Name | Asia Pacific |

| Fastest Growing Region Share / CAGR | 14.20% |

| Geographic Market Share for the 5 Regions | North America: 48.6%, Europe: 26.8%, Asia Pacific: 14.9%, Latin America: 5.2%, Middle East & Africa: 4.5% |

| Top Companies | The Psilocybin Market competitive landscape is led by clinical stage biopharma firms, psychedelic therapy infrastructure providers, GMP manufacturers and regulated service operators building evidence based access pathways. • Compass Pathways • Cybin Inc. • AtaiBeckley • MindMed • Usona Institute • GH Research • Filament Health • Psyence Biomedical • Numinus Wellness • Silo Pharma |

Psilocybin Market Definition & Overview

What is the Psilocybin Market?

The Psilocybin Market covers the development, supply, clinical administration, regulatory access and supporting infrastructure for psilocybin based products and psilocybin assisted therapy. It includes synthetic psilocybin active pharmaceutical ingredients, naturally derived or biosynthesized psilocybin inputs, finished investigational medicines, therapy protocols, clinical trial services, specialized treatment centers, training programs, analytical testing and digital support tools. The market is currently led by clinical stage pharmaceutical use in treatment resistant depression and major depressive disorder, while regulated service models in select jurisdictions are creating early commercial pathways. Long term value depends on FDA/EMA style approvals, controlled substance rescheduling, payer coverage, therapist capacity, safety monitoring and scalable clinic delivery models.

Psilocybin Market Industry Background & Evolution

Parent market background: The psilocybin market sits within the broader neuropsychiatry, central nervous system therapeutics and behavioral health services markets, where unmet need remains high because depression, anxiety, addiction and trauma related disorders often have incomplete response to conventional drugs and psychotherapy. Evolution roadmap: 1950s 1960s: early academic psychedelic research explored psilocybin for psychiatric conditions before regulatory restrictions halted mainstream development. 1970s 1990s: Schedule I controls shifted activity toward limited academic and underground research. 2000s 2015: university led safety and efficacy studies restarted controlled clinical investigation. 2016 2020: breakthrough therapy designations, decriminalization movements and venture funding revived commercial pipelines. 2021 2024: Phase 2 data, Oregon services and Australia access programs moved the sector from research to structured delivery. 2025 2026: pivotal Phase 3 readouts, clinical trial expansion and regulated access models accelerated commercialization planning. 2027 2035: expected transformation centers on approved medicines, specialty clinic networks, reimbursement pathways and evidence based integration into mental health care.

Historical Psilocybin Market Trend Analysis

During 2021 to 2025, the psilocybin market moved from early enthusiasm toward evidence gated institutionalization. The most important shift was the separation between pharmaceutical grade psilocybin development and loosely regulated wellness use. Investors became more selective after the first psychedelic funding cycle, redirecting capital toward companies with controlled IP, GMP manufacturing, dose optimization and late stage clinical assets. Oregon’s regulated service center framework created a non prescription access model, while Australia introduced psychiatrist led access for treatment resistant depression, proving that commercial pathways can emerge before broad global approval. At the same time, clinical protocols matured from generic psychedelic therapy toward standardized screening, preparation, administration, integration and adverse event monitoring. The impact has been a more credible but slower growth market: fewer speculative operators, stronger clinical governance, more emphasis on payer evidence and greater demand for trained facilitators, controlled environments and scalable safety infrastructure.

Psilocybin Growth Outlook Summary

The Psilocybin Market growth outlook is strongest where clinical efficacy, regulated access and delivery infrastructure converge. In the short term, 2026 to 2028 growth will be shaped by Phase 3 trial outcomes, possible regulatory submissions, controlled substance review and preparation by specialty mental health clinics. Revenue will remain concentrated in clinical trials, APIs, service centers, training and early access programs. In the mid term, 2029 to 2032, the market should broaden if approved psilocybin medicines enter treatment resistant depression and if payer pilots validate durable outcomes relative to chronic antidepressant therapy. Demand will shift from isolated treatment centers to integrated psychiatric networks supported by digital intake, monitoring and integration platforms. In the long term, 2033 to 2035, the market is expected to become more segmented, with pharmaceutical products, clinic services, analytics and manufacturing each forming distinct revenue pools. Growth will depend less on legalization narratives and more on operational capacity, affordability, clinical standardization, risk management and country specific reimbursement frameworks.

Key Takeaways

- Synthetic psilocybin drug products are expected to hold the largest segment position because regulators, hospitals and payers prefer GMP grade dosing consistency, validated purity and controlled clinical documentation over variable natural product formats.

- North America remains the largest region because the U.S. has the deepest clinical pipeline, strongest venture backed company base, active state level access experiments and the largest pool of treatment resistant depression patients with commercial reimbursement potential.

- Psilocybin assisted therapy services are expected to be the fastest growing segment as drug approval alone will not create market adoption without trained therapists, screening workflows, integration sessions and specialized treatment settings.

- Asia Pacific is expected to be the fastest growing region as Australia’s controlled prescribing framework creates an early national access model and regional healthcare systems begin evaluating psychedelic assisted therapy within specialist psychiatry.

- The market is moving from product only valuation toward system level commercialization, where companies that control molecule supply, clinical protocol, therapist training, real world evidence and payer engagement will command higher strategic value.

Psilocybin Market White Space & Investment Opportunities

White space opportunities highlight where investment can create defensible advantage, especially across compliant clinics, GMP supply, outcome tracking and payer linked service models as psilocybin commercialization matures globally.

- Clinic integrated psychedelic assisted therapy networks are a major white space because most mental health providers lack controlled drug infrastructure, specialized rooms and trained staff. Networks that combine compliance, treatment protocols and referral partnerships can scale faster.

- Employer and veteran’s mental health programs could become high value channels if clinical evidence supports durable functional recovery. These buyers may fund care outside traditional reimbursement when productivity, disability and suicide prevention outcomes are compelling.

Psilocybin Market Procurement & Buyer Behavior Analysis

Psilocybin Market Buyer Decision Making Criteria

Buyers of psilocybin products and services are prioritizing safety, evidence, compliance and operational practicality. Hospitals, clinics, trial sponsors and service networks are not simply buying a compound, they are procuring a regulated treatment capability that must withstand medical, legal and payer scrutiny.

- GMP grade product quality and validated purity

- Controlled substance licensing and secure logistics

- Clinical evidence strength by indication

- Protocol standardization and therapist training support

- Adverse event management and patient screening tools

- Integration workflow and outcomes tracking

- Compatibility with psychiatric referral pathways

- Cost per treatment episode and facility throughput

- Payer evidence and health economic documentation

- Supplier continuity, stability data and regulatory documentation

Psilocybin Market Economic & Investment Analysis

Psilocybin Market Macroeconomic Impact Factors

Macroeconomic conditions are shaping the Psilocybin Market through healthcare budgets, investor risk appetite, labor shortages and payer cost control pressure. Higher interest rates and biotech funding selectivity have reduced speculative financing, pushing capital toward late-stage clinical assets, defensible IP and clear regulatory paths. Mental health burden remains economically significant because depression and anxiety drive absenteeism, disability, emergency care and productivity losses. This supports long term demand for treatments that can show durable functional improvement. Inflation and wage pressure increase clinic operating costs, especially because psilocybin therapy requires trained staff and long treatment sessions. At the same time, healthcare systems are seeking alternatives to chronic medication escalation and under capacity psychotherapy. The market therefore benefits from macro pressure on mental health outcomes but faces near term constraints from capital discipline and payer scrutiny. Companies that can demonstrate total cost savings, workforce recovery and scalable delivery economics will be best positioned.

Psilocybin Investment Trends in the Market

Investment is becoming more disciplined, moving away from broad psychedelic branding toward late-stage assets, GMP supply, digital evidence tools and clinic infrastructure. Investors are prioritizing companies that can survive long regulatory timelines and prove reimbursement logic.

- Late-stage psilocybin and analog clinical trials

- GMP API manufacturing and biosynthetic production

- Psychedelic assisted therapy clinic networks and outcomes platforms

Psilocybin Market Funding & M&A Activity

Funding and M&A activity is expected to focus on consolidation, late-stage clinical readiness and infrastructure ownership. Investors are favoring companies with regulatory catalysts, credible clinical endpoints and scalable care models instead of early wellness concepts.

- November 2025: Atai Life Sciences and Beckley Psytech completed a strategic combination to form AtaiBeckley, creating a larger psychedelic mental health pipeline and stronger development platform.

- November 2025: MindMed reported a $258.9 million financing, strengthening capital reserves for pivotal psychedelic therapy programs and signaling investor preference for late-stage CNS assets.

- April 2025: Beckley Psytech was reported to be seeking up to $20 million in new funding at a $200 million pre money valuation, showing continued investor interest in differentiated psychedelic treatment platforms.

Psilocybin Market Regulatory & Policy Analysis

Psilocybin Market Regulatory Framework Overview

The psilocybin regulatory framework is defined by a split between drug approval systems and controlled substance laws. In the U.S., psilocybin remains federally controlled, requiring DEA compliant research, storage and handling until any rescheduling follows potential medical approval. Australia permits psychiatrist led access for specific conditions under strict authorized prescriber pathways. Oregon regulates adult psilocybin services through licensed manufacturers, service centers, facilitators and laboratories. Europe remains largely clinical trial focused, with future commercialization dependent on medicines approval and national narcotics rules.

- January 2025: Oregon implemented rule updates linked to SB 303, increasing program structure and data oversight for psilocybin services.

- February 2026: Positive Phase 3 psilocybin data strengthened the case for regulatory submission discussions in treatment resistant depression.

- June 2026: Australia updated access guidance for prescribing psychiatrists, reinforcing controlled clinical protocol expectations.

Psilocybin Market Trends & Innovation Landscape

Psilocybin Key Market Trends

Psilocybin market trends are increasingly evidence led instead of hype led. Investors, regulators and healthcare buyers are focusing on clinical durability, delivery scalability, patient safety and reimbursement readiness instead of broad wellness claims.

- The market is shifting toward pharmaceutical grade synthetic psilocybin because reproducible dosing, impurity control and regulatory documentation are essential for approved mental health treatments. This favors GMP suppliers and sponsors with strong clinical quality systems.

- Integrated therapy protocols are becoming as important as the molecule itself. Screening, preparation, administration, integration and long-term outcome tracking are now competitive differentiators because they determine real world safety, payer confidence and treatment durability.

Psilocybin Market Technology Advancements

Technology advancement in psilocybin is concentrated around better pharmacokinetics, lower delivery cost and stronger clinical data capture. The goal is only to create a psychedelic experience while to make treatment predictable, safe and scalable.

- February 2026: COMP360 Phase 3 success strengthened confidence in fixed dose synthetic psilocybin for treatment resistant depression. The market impact is improved regulatory credibility and clearer benchmarks for efficacy, durability and safety.

- December 2025: CYB003 Phase 3 activity for major depressive disorder highlighted deuterated psilocin analog innovation. The impact is a second-generation pathway focused on shorter, more predictable clinical sessions and potentially stronger clinic economics.

Psilocybin Industry Transformation Trends

The industry is transforming from a fragmented psychedelic wellness ecosystem into a medicalized specialty care market. Pharmaceutical companies are prioritizing proprietary molecules, controlled manufacturing and regulatory submissions, while clinics are professionalizing around patient screening, protocol fidelity and outcomes measurement. Capital is moving away from broad recreational or lifestyle positioning and toward late-stage assets, regulated access and infrastructure. This structural transition favors companies that can operate across drug development, care delivery and evidence generation instead of single point consumer brands.

Psilocybin Market Disruption & Structural Shift Analysis

Psilocybin Market Technology Disruption Impact

Technology disruption in psilocybin is changing both the product and care delivery model. New formulations, analogs and digital infrastructure are lowering barriers that historically made psychedelic therapy difficult to standardize and scale.

- Shorter duration analogs disrupt the market by targeting clinic throughput and cost per treatment. If efficacy is maintained, they could shift value from long session classical psilocybin to operationally efficient second-generation molecules.

- Real world evidence platforms disrupt payer engagement by turning psychedelic sessions into measurable treatment episodes. Clinics that document symptom response, durability, safety and integration adherence will be more attractive to insurers and pharmaceutical partners.

Psilocybin Future Market Transformation

By 2035, the Psilocybin Market business model is likely to transform from private pay niche access into a regulated specialty care pathway. Approved medicines will be paired with certified administration sites, standardized preparation and integration protocols, digital outcomes tracking and payer reviewed treatment bundles. Manufacturers will sell more than a drug: they will support training, risk management and evidence generation. Clinics will move from isolated wellness sessions to accredited psychiatric service lines. The most durable businesses will combine pharmaceutical margins, care delivery revenue, data assets and partnerships with hospitals, employers and insurers.

Psilocybin Policy Impact on Market Growth

Government policy is shifting from blanket prohibition toward controlled medical evaluation and regulated access. Market growth will be strongest where policy supports research, specialist prescribing and real-world safety data without opening uncontrolled consumer channels.

- Authorized prescriber pathways in Australia support early demand for medical psilocybin while requiring specialist governance, which strengthens clinical credibility.

- U.S. state level service frameworks create operating data on training, licensing and patient demand, informing future national policy.

- Public mental health pressure is encouraging governments to evaluate new treatments for refractory depression, addiction and trauma related disorders.

Psilocybin Market Disruption Analysis

Rapid clinical validation and regulatory experimentation are disrupting the psilocybin market. The first disruption is the shift from chronic daily psychiatric medication toward episodic, supervised therapy with potentially durable outcomes after limited dosing. The second disruption is the rise of regulated non traditional access models, such as Oregon service centers and Australia’s psychiatrist led prescribing pathway. Together, these changes challenge conventional pharmaceutical commercialization because value is created through both molecule performance and the service environment. Companies must therefore build hybrid capabilities across drug supply, clinical protocols, therapist training, digital monitoring and compliance management.

Psilocybin Market Growth Dynamics

Psilocybin Market Drivers

- Positive late-stage clinical evidence in treatment resistant depression is improving confidence among regulators, investors and psychiatric providers. The market impact is strongest in pharmaceutical grade psilocybin because pivotal data can unlock approval planning, payer modeling and specialty clinic preparation.

- Rising unmet need in depression, anxiety and substance use disorders is driving demand for therapies with rapid onset and durable outcomes. Psilocybin benefits from dissatisfaction with chronic pharmacotherapy, but adoption depends on demonstrating repeatable, supervised and economically defensible outcomes.

Psilocybin Market Driver Impact Assessment

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Positive Phase 3 and late stage clinical evidence | 5.8% | U.S. and Europe clinical stage pharmaceutical ecosystem, academic psychiatry centers, specialty clinics | Treatment resistant depression, major depressive disorder, clinical trial services | Accelerates regulatory submissions, payer discussions, clinic readiness and manufacturing scale up. |

Regulated access and service center models | 4.6% | Oregon, Colorado, Australia, early adopter psychiatry networks | Supervised administration, facilitator training, integration therapy | Creates early commercial learning loops before broad drug approval. |

Mental health treatment gap and antidepressant non response | 4.3% | High income countries with large depression burden and under capacity psychiatry systems | TRD, anxiety, substance use disorder, palliative care distress | Supports demand for rapid acting, episodic, specialist administered treatment models. |

Psilocybin Market Restraints

- Psilocybin remains highly restricted in many countries, which limits prescribing, manufacturing, transport, research access and commercial distribution. This slows market growth because companies must navigate controlled substance licensing, local approvals and narrow patient access pathways.

- Therapy delivery is capacity constrained because administration requires screening, supervised dosing, psychological support and integration. The market impact is material because treatment cannot scale like a conventional pill without trained clinicians and dedicated facilities.

Psilocybin Market Restraint Impact Assessment

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Regulatory scheduling and controlled substance licensing | 5.1% | Manufacturing, logistics, clinical sites, commercial prescribing | Approved medicine launch, clinical trials, service center access | Slows geographic expansion and raises compliance costs. |

Therapist and clinic capacity constraints | 4.4% | Care delivery infrastructure and workforce training | Supervised dosing, preparation, integration | Limits patient throughput and raises treatment cost. |

Reimbursement and affordability uncertainty | 4.0% | Payer adoption, patient access, clinic economics | TRD therapy, private pay services, mental health networks | Delays mass adoption despite clinical demand. |

Emerging Psilocybin Growth Factors

Emerging growth factors show where psilocybin adoption can accelerate beyond clinical trials, linking science, regulation, delivery capacity and payer readiness into scalable commercial pathways for the next decade globally ahead.

- Shorter-acting analogs and optimized formulations are emerging because traditional psilocybin sessions require long supervision windows. Molecules or delivery models that reduce session time while preserving efficacy could expand clinic throughput and lower total treatment cost.

- Biosynthetic production is gaining attention as companies seek scalable, consistent, lower cost active ingredient supply. Fermentation-based routes could reduce dependence on controlled cultivation and improve pharmaceutical quality control.

Psilocybin Market Segmentation Analysis

Psilocybin Market by Product Type Trends

Synthetic psilocybin is the major product segment because pharmaceutical sponsors, regulators and medical buyers require consistent dose strength, validated purity, GMP documentation and scalable stability data. The major trend is the movement from natural mushroom-derived material toward proprietary synthetic formulations and analogs with tighter pharmacokinetic control. The market is headed toward a dual structure: approved synthetic medicines for psychiatric indications and smaller regulated natural product channels in service center or wellness-adjacent frameworks. Synthetic products will continue attracting premium investment because they support IP protection, clinical trial replication, payer evidence and controlled global distribution.

Psilocybin Market by Application Trends

Treatment-resistant depression is the major application because it has high unmet need, defined clinical endpoints and the most advanced late-stage evidence base. The major trend is movement from exploratory depression studies toward pivotal trials, regulatory dossiers and commercial launch planning. The market is headed toward specialist psychiatry adoption first, with expansion into major depressive disorder, anxiety, substance use disorder, palliative care distress and neurological conditions after additional evidence. TRD will remain the proof of concept indication because payers can compare high treatment burden, relapse risk and medication cycling against supervised psilocybin-assisted therapy outcomes.

Psilocybin Market by End User Trends

Pharmaceutical and biotechnology companies are the major end user segment because they control clinical development, IP, regulatory filings and manufacturing partnerships. The major trend is consolidation around late stage assets and platform capabilities instead of broad psychedelic portfolios. The market is headed toward tighter partnerships between drug sponsors, CROs, specialty clinics, contract manufacturers and digital outcome vendors. Specialty clinics will grow fastest after approval, but biopharma firms will remain the value anchor because they determine approved indications, dosing protocols, label restrictions, commercial education and payer-facing evidence packages.

Psilocybin Market Regional Market Analysis

North America Psilocybin Market

North America is the largest Psilocybin Market region because the U.S. combines the deepest clinical pipeline, strongest investor base, active state level access models and large unmet demand in depression, addiction and trauma related disorders. The region’s demand profile is shifting from consumer curiosity toward regulated psychiatric use, supported by Phase 3 clinical progress and specialized clinic preparation. Production capacity is focused on synthetic API, GMP drug product, analytical testing and controlled substance logistics instead of agricultural mushroom supply. Oregon provides a live service center model, while Colorado and other jurisdictions are shaping future access structures. Canada remains important through research activity, early psychedelic clinic networks and public debate around special access. From 2026 to 2035, North America growth will depend on federal scheduling outcomes, insurer reimbursement, clinical workforce expansion and integration with existing psychiatric referral channels. If approval occurs, the region will likely set global benchmarks for treatment protocols, adverse event management, payer dossiers and real world evidence collection.

Europe Psilocybin Market

Europe is a strategically important psilocybin region because it combines advanced mental health research, established pharmaceutical regulation and strong academic psychiatry networks. The UK, Netherlands, Germany, Switzerland and Nordic countries are central to clinical trials, therapist training and scientific legitimacy. Demand is led by treatment resistant depression and broader unmet needs in mental health systems facing long waiting lists and high antidepressant use. Production capacity is concentrated in GMP manufacturing, clinical trial supply and specialist research sites instead of broad commercial access. Europe’s market is expected to grow steadily but cautiously because EMA style approval, national reimbursement negotiations and controlled substance rules can vary by country. By 2035, Europe is likely to become a high quality medical market with slower consumer access but stronger institutional adoption.

Asia Pacific Psilocybin Market

Asia Pacific is the fastest growing region because Australia created an early psychiatrist led access pathway for psilocybine in treatment resistant depression, giving the region a practical regulatory learning advantage. Demand is emerging from specialist psychiatry, private mental health clinics and research centers seeking alternatives for refractory depression and trauma related disorders. Japan, China, India, South Korea and Singapore are still cautious due to controlled substance concerns, but large mental health treatment gaps and expanding clinical research infrastructure create long term potential. Production capacity is likely to develop through pharmaceutical outsourcing, analytical testing and regional clinical trial support. Growth through 2035 will depend on evidence acceptance, cultural stigma reduction and country specific medical access frameworks.

Psilocybin Market Country-Level Market Analysis

United States Psilocybin Market Size/Forecast

The United States Psilocybin Market is the largest country level opportunity because it combines large depression prevalence, high therapy spending, extensive clinical trials, investor backed companies and active state policy experimentation. Demand is shifting toward treatment resistant depression, where approved psilocybin could fit into specialty psychiatry pathways. Production capacity is centered on synthetic API, GMP drug product, controlled substance storage, trial logistics and specialty clinic networks. The market forecast is highly sensitive to FDA approval timing, DEA scheduling decisions, payer coverage and state level service models. By 2035, the U.S. could become the global reference market for regulated psilocybin assisted therapy commercialization.

Japan Psilocybin Market Size/Forecast

Japan’s Psilocybin Market is currently cautious but strategically relevant because of high unmet need in depression, an aging population and strong pharmaceutical quality standards. Demand is likely to emerge first through academic research, multinational clinical trials and carefully controlled psychiatric use instead of broad access. Production capacity would probably rely on domestic pharmaceutical partners, imported GMP API and strict narcotics compliance. Adoption may be slower than in Australia or the U.S., but Japan could become a premium medical market if regulators accept global clinical data and local psychiatrists see durable outcomes. By 2035, growth is expected to remain evidence led and institutionally controlled.

China Psilocybin Market Size/Forecast

China’s Psilocybin Market is at an early stage due to strict controlled substance policies and limited commercial openness for psychedelic therapies. However, the country has large mental health treatment demand, growing neuroscience research capability and strong pharmaceutical manufacturing capacity. Near term demand will likely remain in research, analytical chemistry and potential collaboration with global drug developers instead of direct patient access. Production capacity could become significant if policy permits GMP synthesis or contract manufacturing under controlled licenses. By 2035, China’s role may be more manufacturing and research oriented than patient access led unless regulatory attitudes toward psychedelic medicines materially change.

India Psilocybin Market Size/Forecast

India’s Psilocybin Market is nascent but long term potential is supported by high depression burden, expanding private psychiatry, clinical trial capabilities and pharmaceutical manufacturing strength. Current demand is constrained by strict narcotics controls and low mainstream clinical acceptance. Production capacity could develop through API manufacturing and contract research if global sponsors seek compliant partners. Market growth will depend on regulatory clarity, hospital ethics approvals, safety training and willingness of private mental health providers to adopt evidence based psychedelic assisted care. By 2035, India could become a cost efficient clinical research and manufacturing hub before becoming a broad treatment market.

Psilocybin Market Other Key Countries

- Australia Psilocybin Market: Australia is a leading early access country because authorised psychiatrists can prescribe psilocybine for treatment resistant depression under strict conditions. This creates demand for clinical protocols, specialist training and compliant product supply.

- Canada Psilocybin Market: Canada is important for research, special access discussions and psychedelic clinic networks. Growth depends on federal controlled drug policy and stronger reimbursement evidence.

- United Kingdom Psilocybin Market: The UK has strong clinical research activity and company presence, making it a key development hub even before broad commercial approval.

- Germany Psilocybin Market: Germany offers strong reimbursement potential and psychiatric infrastructure, but adoption will require EU level approval, national assessment and strict evidence standards.

- Netherlands Psilocybin Market: The Netherlands benefits from an established psychedelic services ecosystem and research openness, but medical market growth depends on formal clinical regulation.

Psilocybin Market Competitive Landscape

Psilocybin Market Competitive Benchmarking

Competitive benchmarking in psilocybin is shifting from broad pipeline claims to proof of late stage clinical execution, controlled manufacturing, protocol scalability and payer readiness. The strongest companies are those able to connect molecule differentiation with real world therapy delivery.

- Compass Pathways: Portfolio focus is COMP360 synthetic psilocybin for treatment resistant depression. Target strategy centers on regulatory approval, fixed dose standardization and specialist psychiatry adoption. Use case focus is TRD with potential expansion into adjacent mood disorders.

- Cybin: Portfolio focus is CYB003, a deuterated psilocin analog. Target strategy emphasizes shorter, predictable sessions and adjunctive major depressive disorder treatment. Use case focus is MDD and clinic throughput improvement.

- AtaiBeckley: Portfolio focus includes next generation psychedelic assets and a diversified mental health pipeline. Target strategy is platform consolidation and global clinical development. Use case focus extends beyond psilocybin into rapid acting neuropsychiatric medicines.

- Usona Institute: Portfolio focus is non profit psilocybin research and pharmaceutical grade development. Target strategy emphasizes public benefit science, investigator networks and regulatory quality evidence. Use case focus includes major depressive disorder.

- Numinus Wellness: Portfolio focus is clinic operations, therapist training and psychedelic assisted care infrastructure. Target strategy is care delivery and protocol implementation. Use case focus is patient access and integration services.

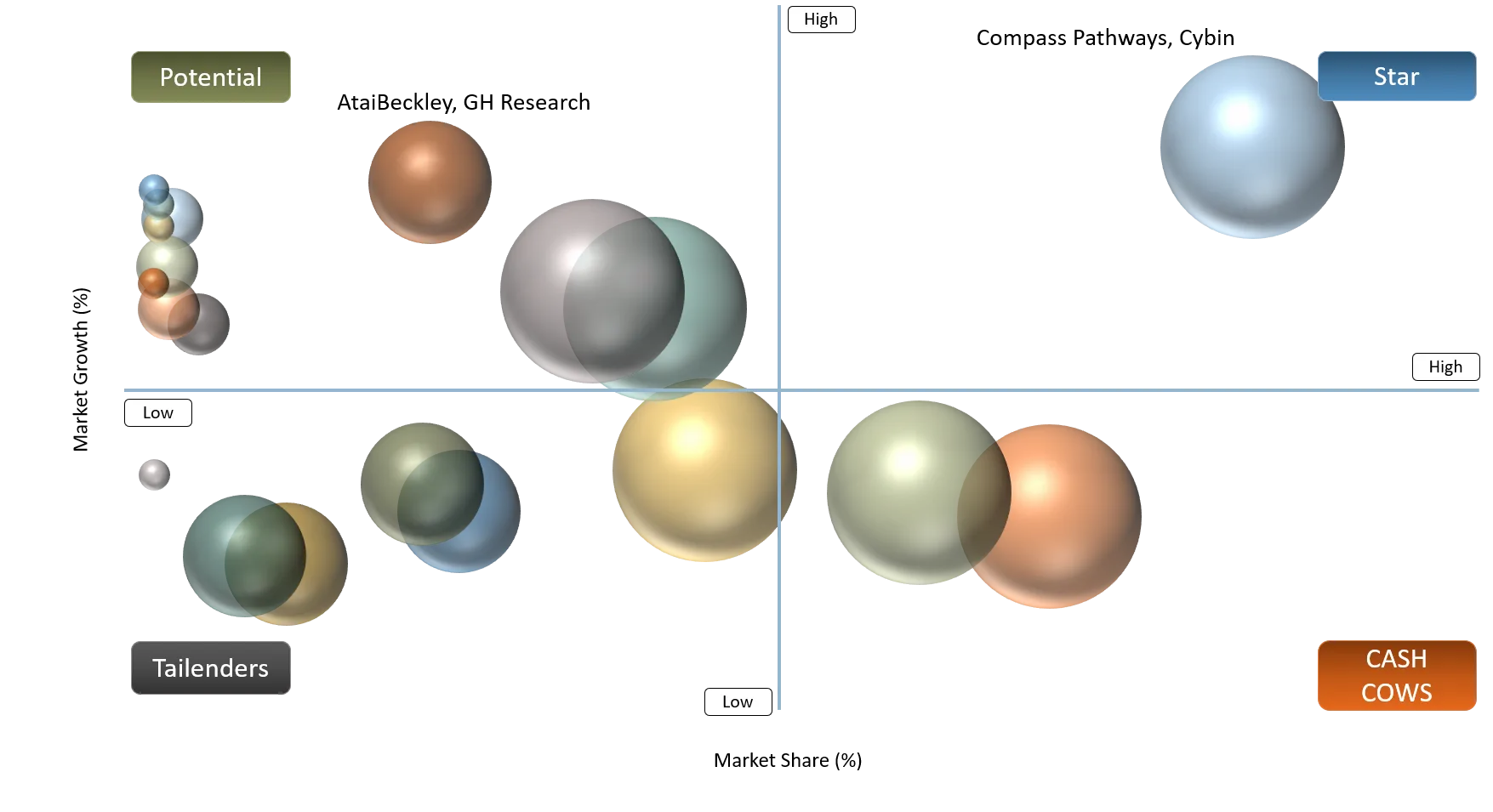

Psilocybin Market BCG Matrix List

- Stars: Compass Pathways, Cybin

- Question Marks: AtaiBeckley, GH Research

- Cash Cows: Numinus Wellness, Usona Institute

- Tailenders: Smaller retreat style operators, undercapitalized early stage psychedelic startups

Psilocybin Market BCG Matrix Analysis

The BCG matrix for the Psilocybin Market reflects a sector moving from speculation to clinical execution. Compass Pathways and Cybin fit the Stars category because they have late stage clinical assets, strong regulatory relevance and high growth potential if pivotal data translate into approvals. AtaiBeckley and GH Research are Question Marks because they hold differentiated psychedelic pipelines and investor attention, but some lead assets are broader tryptamine or adjacent psychedelic therapies instead of pure psilocybin commercialization. Numinus Wellness and Usona Institute are Cash Cows in a strategic clinical replacing high profit sense: they provide protocol, training, or research infrastructure that supports market formation, though revenue scaling may be slower. Tailenders include retreat style or undercapitalized startups that lack clinical grade evidence, GMP supply, payer pathways and compliance infrastructure. Their market position is vulnerable as regulators and healthcare buyers increasingly demand safety, reproducibility and measurable outcomes.

Psilocybin Market Company Profiles & Strategy Analysis

Psilocybin Market Expansion & Partnership Strategy

- February 2026: Compass Pathways reported that COMP360 met the primary endpoint in its second Phase 3 TRD trial. The impact is stronger confidence in FDA submission planning and commercial readiness for synthetic psilocybin therapy.

- November 2025: atai Life Sciences and Beckley Psytech completed their strategic combination to form AtaiBeckley. The impact is consolidation of psychedelic mental health pipelines and stronger late stage development capability.

Psilocybin Market Key Developments (2025–2026)

Psilocybin Major Industry Developments

Major industry developments are being led by clinical data, regulatory access models and consolidation. These events show the market moving toward medical credibility and operational readiness.

- June 2025: Compass Pathways reported positive Phase 3 COMP005 results for COMP360 in treatment resistant depression, strengthening confidence in pivotal psilocybin development.

- November 2025: Atai Life Sciences and Beckley Psytech completed their strategic combination to form AtaiBeckley, signaling consolidation around diversified psychedelic mental health pipelines.

- December 2025: Cybin’s CYB003 Phase 3 program activity expanded, highlighting next generation psilocybin analog competition in major depressive disorder.

- January 2025: Oregon implemented updated psilocybin service rules, increasing structure around licensed access and data oversight.

- February 2026: Compass Pathways reported positive second Phase 3 COMP006 results, creating a stronger basis for regulatory submission planning.

Psilocybin Recent Market Announcements

February 2026: Compass Pathways announced that COMP360 achieved the primary endpoint in the second Phase 3 trial for treatment resistant depression. This is the most important recent market announcement because it strengthens the probability that psilocybin could move from experimental therapy toward regulated medicine. The impact extends across the value chain: GMP manufacturers gain future demand visibility, specialty clinics can plan administration capacity, investors can reassess late-stage psychedelic assets and payers can begin evaluating health economic models. The announcement also raises competitive pressure on second generation analog developers to prove shorter duration, better tolerability, or broader indication value.

Psilocybin Market Technology Launches & Partnerships

Technology launches and partnerships are increasingly focused on clinical validation, pipeline consolidation and delivery efficiency. The most important developments are those that reduce regulatory risk or improve treatment scalability.

- February 2026: COMP360 Phase 3 data strengthened fixed dose synthetic psilocybin as a leading regulatory grade technology platform for TRD.

- November 2025: AtaiBeckley formation combined complementary psychedelic assets and development capabilities, improving portfolio depth and partnership optionality.

- December 2025: CYB003 Phase 3 activity advanced the next generation analog pathway, supporting innovation in treatment duration and clinic economics.

Psilocybin Market Strategic Insights & Analyst Perspective

Analyst Insights for Psilocybin Market

From a DataM Intelligence perspective, the Psilocybin Market is entering its most important transition phase: moving from science led promise to regulated healthcare commercialization. The market’s long term growth potential is meaningful, but it will not scale like a conventional pharmaceutical category. Psilocybin requires a combined product and service model, where value depends on clinical evidence, controlled manufacturing, trained therapists, appropriate patient selection, safe administration sites and post treatment outcome tracking. The strongest signal is late stage progress in treatment resistant depression, which can provide a medically credible entry point into mainstream psychiatry. However, the market remains constrained by controlled substance status, reimbursement uncertainty, therapy session economics and uneven regional regulation. DataM Intelligence expects market share to concentrate among companies that can align molecule differentiation with implementation infrastructure. Synthetic psilocybin will remain the largest product segment because it meets regulatory and payer expectations for dose consistency. Psilocybin assisted therapy services will grow fastest because approved drugs cannot generate revenue without scalable delivery capacity. By 2035, the market will likely be less about psychedelic novelty and more about measurable outcomes, safety governance, care pathway integration and country specific access models.

Strategic Recommendations for Psilocybin Market

- Recommendation 1: Companies should build launch strategy around evidence based specialty care instead of broad wellness demand. The best path is to focus on one or two high need indications, develop standardized screening and administration protocols, train certified therapy teams and create payer ready evidence packages. Partnerships with psychiatric hospitals, academic centers and outcomes platforms will reduce commercialization risk and improve clinical credibility.

- Recommendation 2: Companies should invest early in operational scalability because therapy delivery will determine market share after approval. This means securing GMP supply, controlled substance logistics, site accreditation, digital monitoring and workforce training before broad commercial launch. Firms that reduce treatment time, document durability and lower cost per response will have stronger pricing power and better payer acceptance.

Psilocybin Future Market Outlook (2035 Vision)

In 2025, the Psilocybin Market is still largely a clinical stage and regulated access market. Revenue is concentrated in trials, research supply, service center activity, training, consulting and early access programs. Adoption is limited by legal controls, private pay economics and incomplete reimbursement. By 2035, the market is expected to look substantially more institutionalized. Approved synthetic psilocybin products may be available for treatment resistant depression and potentially broader depressive disorders, with specialist clinics delivering standardized therapy episodes. Digital platforms will track patient selection, symptom response, durability and safety. Manufacturing will be more scalable through GMP synthesis and biosynthetic methods. Regional differences will remain: North America will lead commercialization, Europe will emphasize regulated medical quality, Asia Pacific will grow through controlled specialist access and emerging regions will develop selectively. The major difference between 2025 and 2035 will be trust: the market will shift from experimental promise to an evidence backed psychiatric treatment ecosystem.

Psilocybin Market Target Audience

- Pharmaceutical and biotechnology companies: To understand clinical pipelines, competitive positioning, regulatory pathways and partnership opportunities in psilocybin based medicines.

- Mental health clinics and hospital systems: To assess treatment delivery models, therapist capacity, safety protocols and future reimbursement opportunities.

- Contract manufacturers and API suppliers: To identify GMP production demand, controlled substance supply requirements and formulation opportunities.

- CROs and clinical trial sites: To evaluate trial activity, patient recruitment needs and site readiness requirements.

- Investors and private equity firms: To assess late stage assets, infrastructure opportunities, consolidation targets and risk adjusted market growth.

- Digital health and outcomes platforms: To understand demand for screening, monitoring, integration and payer evidence tools.

- Regulators and policymakers: To benchmark access models, safety controls and clinical governance frameworks.

Who Should Buy this Report?

This report is designed for organizations that need more than a basic market overview. It helps buyers understand where psilocybin commercialization is headed, which segments will scale and how regulation, clinical evidence and delivery infrastructure affect investment decisions.

- Biopharma strategy teams evaluating psilocybin pipelines and indication priorities

- Specialty mental health providers planning psychedelic assisted therapy services

- Investors assessing market size, share, growth and forecast assumptions

- CROs and trial networks targeting psychedelic clinical research

- GMP manufacturers evaluating controlled substance production opportunities

- Digital health vendors building outcome and integration platforms

- Policy and market access teams studying country specific market size and share potential

Why Choose DataM Intelligence?

- DataM Intelligence supports clients with business outcome focused market sizing, helping teams understand where revenue pools will form across products, services, regions and end users.

- The report connects clinical evidence, regulatory pathways and commercial adoption to identify practical growth opportunities instead of broad hype driven assumptions.

- DataM helps clients benchmark competitors by pipeline maturity, target strategy, product positioning and partnership readiness.

- The analysis supports market entry decisions by clarifying country specific regulation, access models and demand concentration.

- Procurement and buyer behavior insights help suppliers design offerings aligned with clinic, payer, manufacturer and trial sponsor needs.

- Strategic recommendations translate market data into actions for partnerships, investment prioritization, positioning and long term forecast planning.