Printed Circuit Board PCB Market Overview

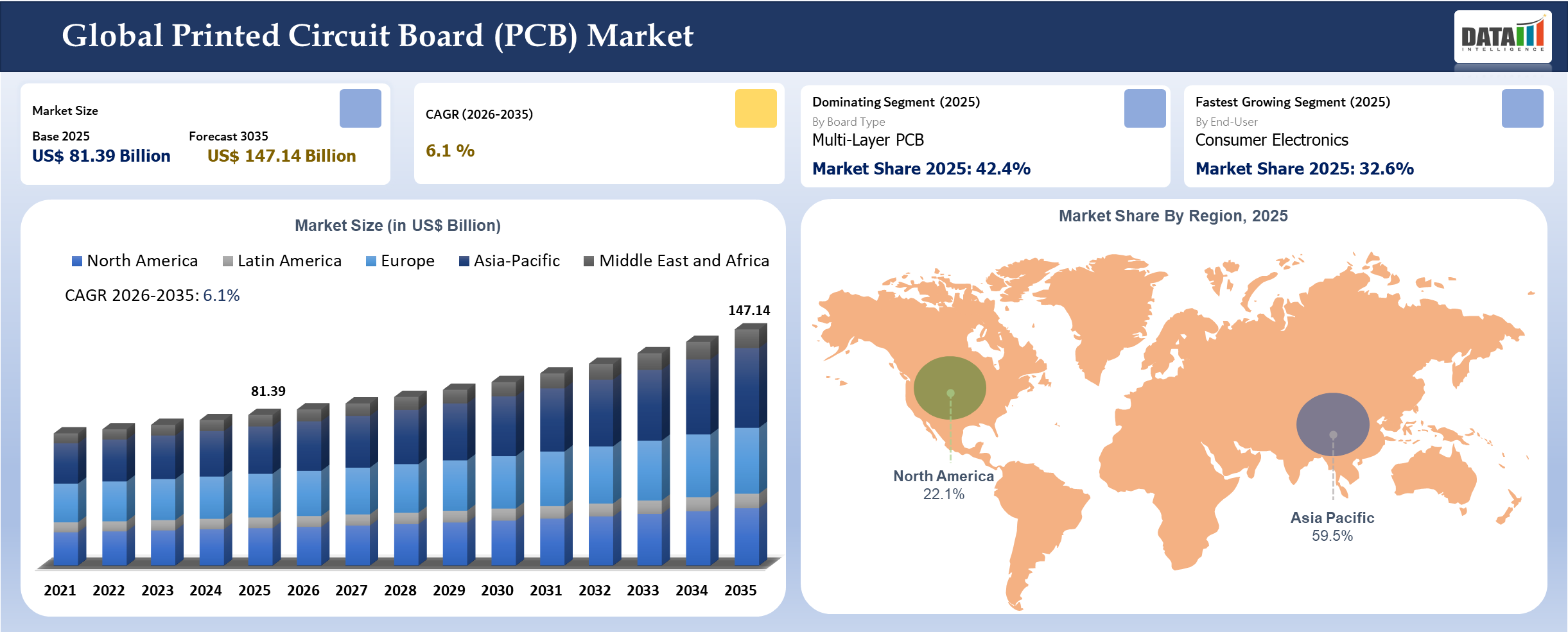

The global printed circuit board (PCB) market reached US$ 81.39 billion in 2025 and is expected to reach US$ 147.14 billion by 2035, growing with a CAGR of 6.1% during the forecast period 2026-2035. The increasing demand for highly advanced electronics in the form of electronic products that are applicable in various industries, such as consumer electronics, automotive industry, telecommunication and industrial automation. Increased digitization process, high penetration rates of intelligent gadgets and integration have greatly contributed to the growth of global demand for PCBs. According to the Japan Electronics and Information Technology Industries Association, there is an increasing production of electronics globally because of semiconductors, telecommunication equipment and electronic components.

The swift advancement in technology, which includes 5G, Electric Vehicle (EV), artificial intelligence and Internet of Things (IoT), continues to add more complexity and demand for higher volumes of PCB design. For example, according to the International Telecommunication Union, the worldwide internet usage surpassed 65%. It indicates an increase in demand for communication networks, including high-frequency PCB designs used in 5G base stations and networking equipment. In addition, the rise of electric cars has been documented by the International Energy Agency; the sales of electric cars have risen above 14 million per year. Due to the nature of their design, EVs require far more PCB than conventional cars.

Printed Circuit Board (PCB) Industry Trends and Strategic Insights

- Board type remains the most commercially useful lens because it explains how buyers allocate budgets, compare suppliers and frame performance trade-offs inside the printed circuit board market.

- Demand is shifting toward solutions that can prove measurable value in HDI PCB and Multi Layer PCB rather than relying on broad platform claims.

- Asia-Pacific is setting the competitive pace, with China and Taiwan shaping product design, supply decisions and go-to-market priorities.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 81.39 Billion | |

| 2035 Projected Market Size | US$ 147.14 Billion | |

| CAGR (2026-2035) | 6.1% | |

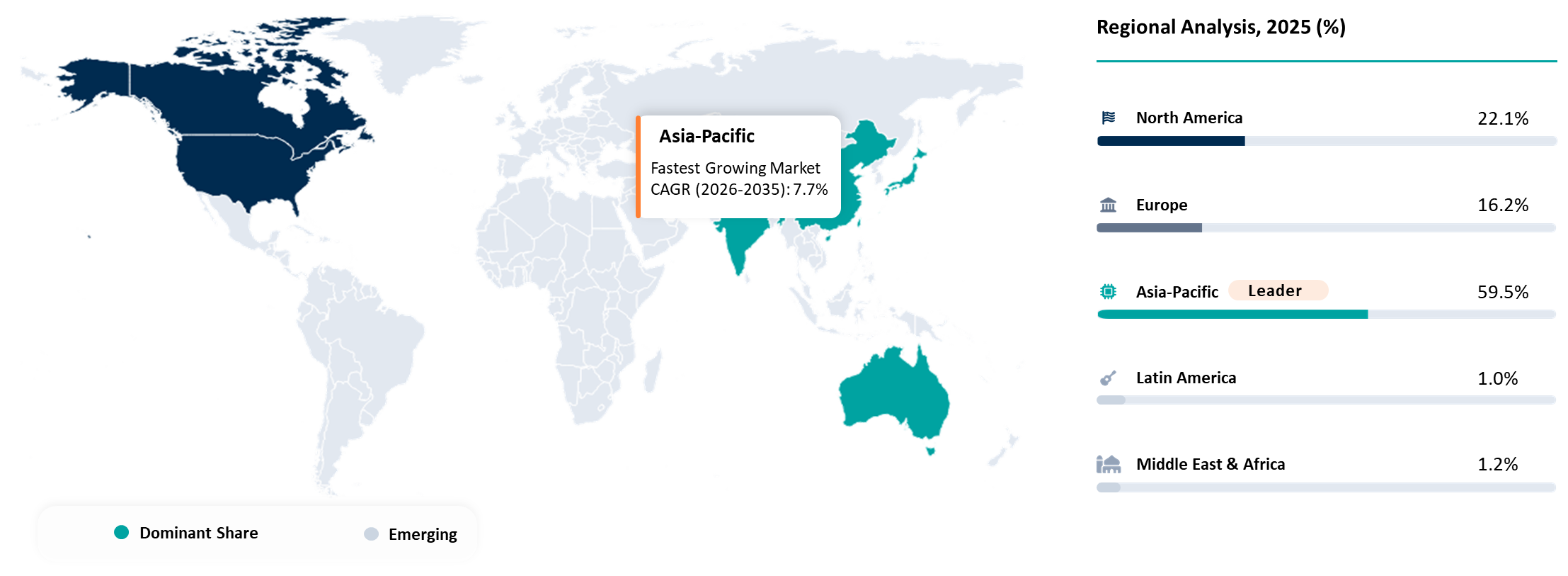

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Board Type | Single Sided PCB, Double Sided PCB, Multi-Layer PCB, HDI PCB, Rigid Flex PCB | |

| By Material | FR 4, High Speed Materials, Metal Core, Ceramic and Specialty Materials | |

| By End-User | Consumer Electronics, Automotive, Telecom, Industrial, Aerospace and Defense, Healthcare | |

| By Layer Count | 1 to 4 Layer, 6 to 8 Layer, 10 Layer and Above | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

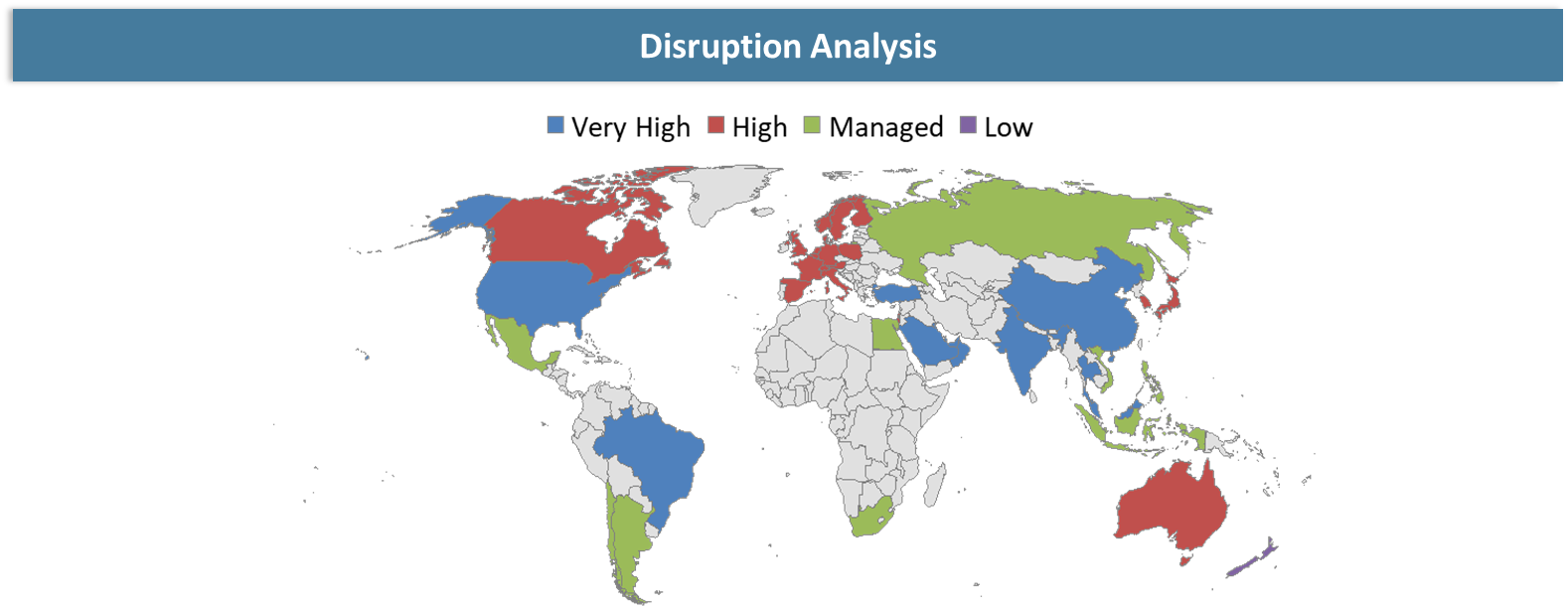

Disruption Analysis

Disruption within the PCB industry cannot be considered an individual launch but rather a shift within the market itself, from a competition based upon generic features to one focused upon actual operational value. Suppliers cannot continue depending on specifications or buzzwords related to innovative performance while buyers ask questions about how quickly and easily their product will fit into existing systems, its reliability and how fast it will pay off its initial cost.

New models for sales channels, alliances and bundling are leading consumers to consider the surrounding services layer or ecosystem along with core technological products. As a result, it is common for a supplier with better management of its surroundings to take control of a contract even if the competing product has equally advanced technology. The PCB market also faces the challenge of disruption due to increased demand for accountability and resilience of solutions.

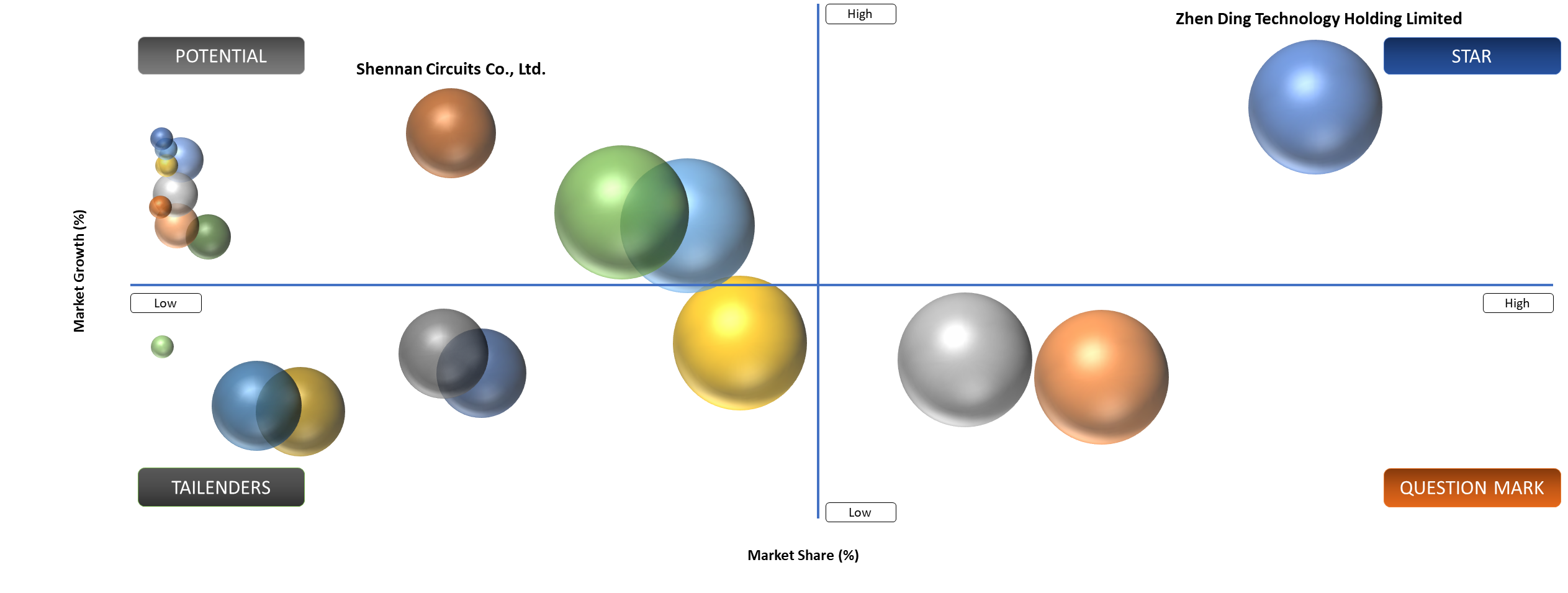

BCG Matrix: Company Evaluation

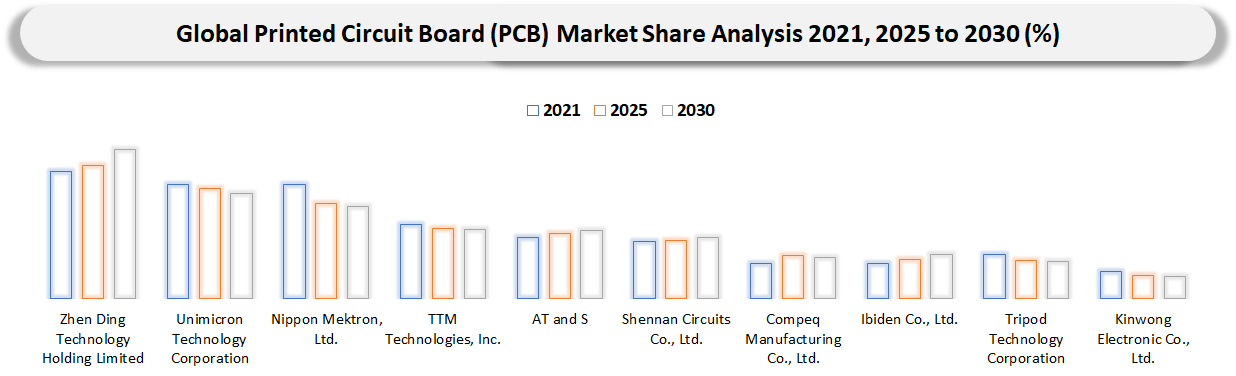

In BCG terms, the Stars in the global printed circuit board (PCB) market are usually the suppliers combining visible demand momentum with ecosystem control. Companies such as Zhen Ding Technology Holding Limited, Unimicron Technology Corporation and Nippon Mektron, Ltd. tend to sit in this zone when they can link product depth with distribution reach, integration credibility and recurring account expansion. The advantage is not only sharing; it is the ability to shape customer expectations about what a complete solution should include.

Market Dynamics

The rapid expansion of electric vehicles is increasing multilayer PCB adoption rates.

Rapid proliferation of electric vehicles (EVs) is driving up the uptake of multilayer printed circuit boards (PCBs) across the global PCB industry. EVs need an advanced electronic architecture to control the batteries, distribute power, enable ADAS (advanced driver assistance systems), infotainment features and even thermal management. With their capabilities of integrating more components in a small space with high signal integrity, multilayer PCBs are indispensable to cater to such requirements. EVs have many more electronic control units (ECUs) than internal combustion engine-based cars; hence, there are many more PCBs needed for each car. With more developments being made towards connected, autonomous vehicles, there is a significant increase in the need for high-performance multilayer PCBs. With governments around the world promoting the cause of electrification through various policies and incentives, automakers are mass-producing EVs, resulting in steady growth in the use of multilayer PCBs.

Supply chain disruptions are affecting timely availability of critical electronic components.

Disruptions in the supply chain have emerged as one of the most important problems concerning the availability of electronic components in the Global Printed Circuit Board (PCB) Market. The process of PCB manufacturing is largely reliant upon an intricate and interconnected worldwide supply chain that includes semiconductors, capacitors, resistors, laminates and other specific materials. Disruption in any form, whether because of geopolitical problems, trade barriers, natural calamities or logistical challenges, can result in the delayed procurement of these components. For example, scarcity of materials like copper foil, fiberglass and laminates has raised the lead times for the acquisition of these components from the usual 8-10 weeks to 16-20 weeks, while some advanced material types take as long as 140 days to be delivered. Also, over 80 percent of electronics companies have had to deal with delayed deliveries because of insufficient supply of components in recent years. With the growing demands coming from various emerging industries like electric cars, 5G networks and artificial intelligence devices, the supply chain issue becomes even more pronounced.

Segmentation Analysis

The global printed circuit board (PCB) market is segmented based on the board type, material, end-user, layer count and region.

HDI PCB Adoption Accelerates in Printed Circuit Board (PCB) Market Driven by Cost Efficiency and Low Integration Disruption

HDI PCB holds its place because consumers will be able to embrace it without the need to alter other aspects of their business process. Moreover, it may fit within the budget, ecosystem of partners and skill level of the company, making it a much easier purchase decision. In most instances, it will be where the initial growth of the market will take place, as it is less disruptive for consumers to implement it into their business process. In addition, HDI PCB receives a commercial advantage in cases where suppliers provide implementation assistance and other services alongside the product. It allows buyers to feel more comfortable with the purchasing process and sign off on it sooner. On the contrary, HDI PCB will come under pressure once buyers seek greater control over performance or function.

Geographical Penetration

Asia-Pacific Leadership and Innovation Discipline Reshape Strategic Direction in the Printed Circuit Board (PCB) Market

The dynamics of procurement practices, distribution channel configurations, regulatory compliance and product offerings are trending in a manner that makes the region a source of insight into future revenue concentrations and strategic direction. The prominence of Asia-Pacific comes down to the fact that the production of PCBs is dependent on electronics manufacturing concentration, material supply chains, assembly operations and the rate of new product introductions. Market leadership is now dependent on the ability of the vendors to manage scales, HDI capabilities, automotive standards and rapid turnaround times within diverse board structures. Another factor behind the importance of the region is the rising sophistication in customers’ demands for validation. Procurement teams want to know how quickly the solution can be rolled out, its performance in actual situations and the capability to scale through local partners.

China Printed Circuit Board (PCB) Market Insights

The Chinese market indicates which vendors can meet tougher customer needs compared to their global positioning strategy. One of the noticeable trends emerging in China is that consumers no longer reward general offers. Instead, they want solutions aligned with the specific costs, compliance, integration capabilities and performance of the local environment. It impacts how vendors position themselves in the market locally, choose channel partners and decide on product variants. The market also becomes significant because success requires more from vendors than just being interesting. The vendors offering an integrated approach and ecosystem-level coordination of implementation, services, compliance and adjacent technologies tend to outpace competitors whose focus is just on products.

Taiwan Printed Circuit Board (PCB) Industry Growth

Taiwan emphasizes the areas of specialization that could help to develop additional segments that have more value in the bigger picture. In this way, it represents another good indicator of premiumization and competitive position. Meanwhile, China offers itself the largest platform for manufacturing, not only because of the scale. The importance of China lies in its ability to rapidly enter segments of higher complexity boards needed by the sectors of telecommunications, automobile and computing industries. Meanwhile, Taiwan plays a strategic role because of its proximity to the segment of computing hardware and servers with advanced electronics programs that require more precision and perfection. Overall, both countries demonstrate that regional growth is uneven and revenue growth is dependent on the fit between segment mix and commercial and supplier capability.

Competitive Landscape

- Competition in the global printed circuit board (PCB) market is defined by a split between scale players and focused specialists. Large vendors such as Zhen Ding Technology Holding Limited, Unimicron Technology Corporation and Nippon Mektron, Ltd. use portfolio breadth, channel reach and account access to shape category expectations, while specialist vendors try to win through product depth, faster implementation or sharper use case alignment.

Market positioning is increasingly influenced by how well suppliers defend the full customer journey. Product quality still matters, but so do onboarding friction, integration capability, data or workflow control, application engineering and lifecycle support. Vendors anchoring around high-value segments such as HDI PCB and Multi-Layer PCB are generally in a better position to protect pricing and expand share.

Key Developments

- March 2026: Tripod Technology Corporation is strengthening its multilayer and HDI PCB manufacturing capabilities for automotive, industrial electronics and high-reliability applications across global OEM partnerships.

- March 2026: Kinwong Electronic Co., Ltd. is expanding PCB manufacturing capabilities in China, focusing on telecom, automotive electronics and industrial applications with advanced multilayer board technologies.

- March 2026: WUS Printed Circuit Co., Ltd. is expanding PCB manufacturing capabilities in China, targeting telecom infrastructure, automotive electronics and industrial applications with advanced multilayer technologies.

- January 2026: Unimicron Technology Corporation increased investments in HDI and IC substrate technologies to support advanced semiconductor packaging and high-performance electronics manufacturing demand.

- January 2026: Nippon Mektron, Ltd. expanded investments in flexible circuits and HDI technologies to support EV electronics, miniaturization and next-generation semiconductor packaging demand growth.

- January 2026: AT&S Austria Technologie & Systemtechnik AG is strengthening its advanced PCB and IC substrate production capabilities to support high-performance computing, automotive electronics and aerospace applications.

- January 2026: Shennan Circuits Co., Ltd. is investing in advanced multilayer and high-density PCB production capacity to support telecom infrastructure, automotive electronics and data communication systems.

- October 2025: COFCO Biochemical (Anhui) Co., Ltd. enhanced corn-based lactic acid production, strengthening vertical integration for PLA bioplastics targeting food packaging applications.

- September 2025: Henan Jindan Lactic Acid Technology Co., Ltd. strengthened lactic acid integration for PLA production, improving upstream efficiency and supporting biodegradable plastics market expansion.

August 2025: Hisun Biomaterials Co., Ltd. increased PLA production capacity in China, focusing on cost competitiveness and large-scale supply for packaging and 3D printing industries.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Electronics & Consumer Device Manufacturers: OEMs producing smartphones, laptops, wearables, home appliances and IoT devices that rely heavily on advanced PCB architectures for miniaturization and performance optimization.

- Automotive & Electric Vehicle (EV) Manufacturers: Automotive OEMs, EV startups and Tier-1 suppliers integrating PCBs into ADAS systems, battery management systems, infotainment and power electronics.

- Telecommunications & Networking Companies: Telecom operators, 5G infrastructure providers and networking equipment manufacturers deploying high-frequency and high-density interconnect (HDI) PCBs for faster data transmission and connectivity.

- Industrial Electronics & Automation Providers: Companies engaged in industrial automation, robotics and smart manufacturing systems utilizing rugged and high-reliability PCBs for control systems and embedded applications.

- Aerospace & Defense Organizations: Defense contractors and aerospace firms requiring high-performance, mission-critical PCBs with stringent quality, durability and reliability standards.

- Healthcare & Medical Device Manufacturers: Producers of diagnostic equipment, wearable health monitors, imaging systems and life-support devices leveraging compact and high-precision PCB solutions.

- PCB Manufacturers & OEM Suppliers: Global and regional PCB fabricators, material suppliers and assembly service providers focusing on innovation, cost optimization and scaling production capabilities.

- Semiconductor & Component Manufacturers: Chipmakers and electronic component suppliers aligning PCB designs with advanced semiconductor packaging, integration and system-on-chip (SoC) developments.

- Investors & Private Equity Firms: Investment entities monitoring growth in electronics manufacturing, semiconductor ecosystems and emerging PCB technologies such as flexible, rigid-flex and substrate-like PCBs.

- Distributors & Supply Chain Stakeholders: Authorized distributors, EMS (Electronics Manufacturing Services) providers and logistics partners involved in PCB sourcing, assembly, testing and aftermarket services.