Power Flow Controller Market Overview

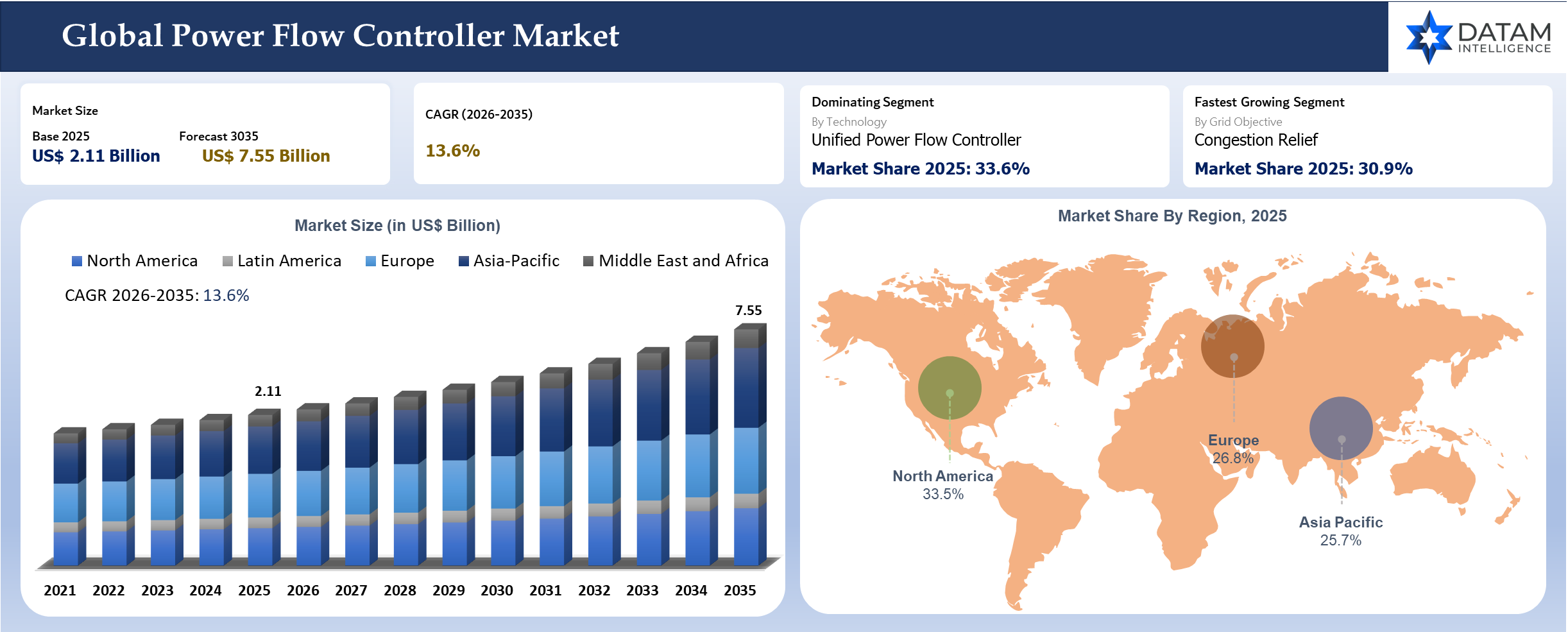

The global power flow controller market reached US$ 2.11 billion in 2025 and is expected to reach US$ 7.55 billion by 2035, growing with a CAGR of 13.6% during the forecast period 2026-2035. The rising instances of power grid congestion, loop flows and voltage instability have been attributed to the unpredictable behavior of renewables, especially solar and wind energy. A greater need for FACTS technology is to use advanced power flow controllers to manage the power flows, optimize the use of assets and avoid expensive additions to the grid.

The need for cross-border electricity trade, as well as the trend towards meshed grids, is expected to stimulate demand for power flow controllers that enable the optimization of electricity trading as well as ensuring system stability in line with measures undertaken by ENTSO-E to strengthen grid coordination amid rising levels of renewables. Additionally, technological advances are also expected to drive market growth as technologies such as high voltage power electronics, wider bandgap semiconductors (SiC) and digital control become widely available. The development will boost performance characteristics of power flow controllers, making them feasible for new installations as well as retrofitting applications.

Power Flow Controller Industry Trends and Strategic Insights

- Advanced power flow control solutions have emerged as viable alternatives to transmission line upgrades that take time and cost a lot.

- Successful projects will be those whose success can be proven by achieving congestion alleviation, renewables integration and contingency management goals.

- Uptake of such solutions is increasing rapidly since their recognition as grid-enhancing technologies in the planning process.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.11 Billion | |

| 2035 Projected Market Size | US$ 7.55 Billion | |

| CAGR (2026-2035) | 13.6% | |

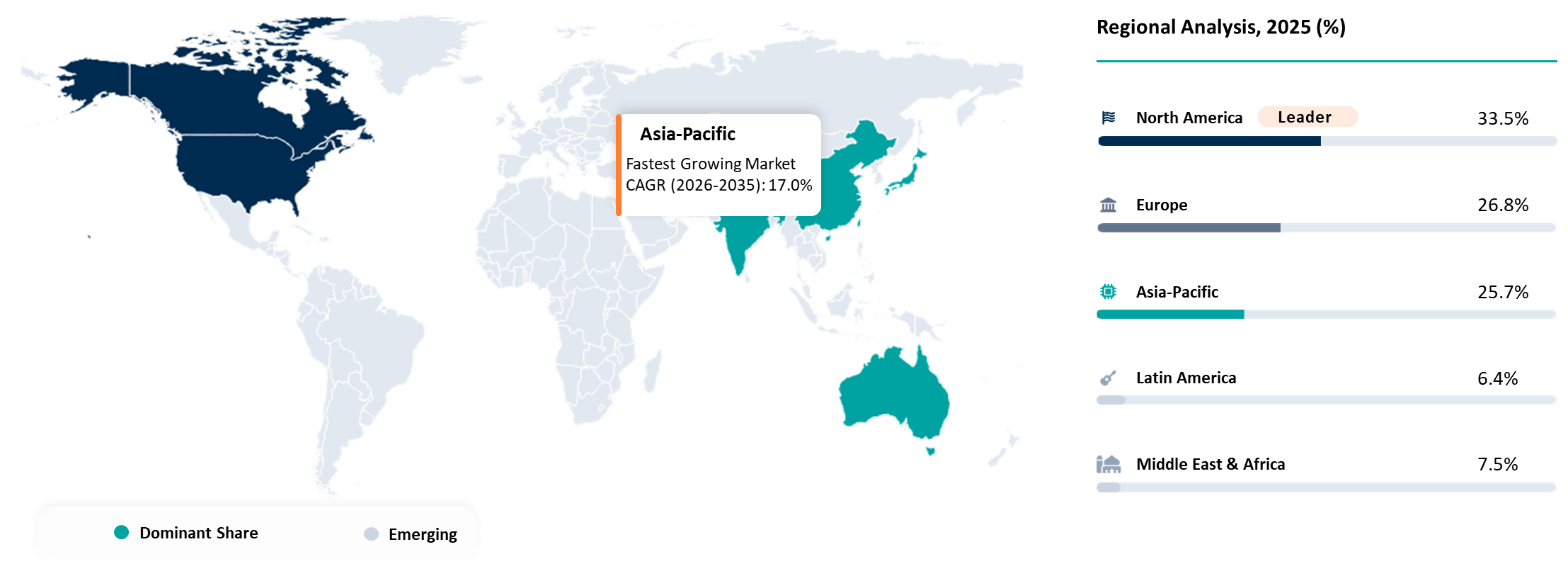

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Technology | Series Power Flow Controller, Parallel Power Flow Controller, Unified Power Flow Controller, Distributed Power Flow Controller, Modular Advanced Power Flow Controller | |

| By Voltage Level | Below 132 kV, 132 kV to 220 kV, 221 kV to 400 kV, above 400 kV | |

| By Grid Objective | Congestion Relief, Renewable Integration, N-1 Reliability Support, Interconnector Optimization, Loss Reduction | |

| By Deployment Model | Utility Owned, Transmission System Operator Deployment, Third Party Grid Enhancement Deployment | |

| By Installation Environment | New Substation or Corridor Build, Brownfield Retrofit, Dynamic Congestion Hotspot Deployment | |

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

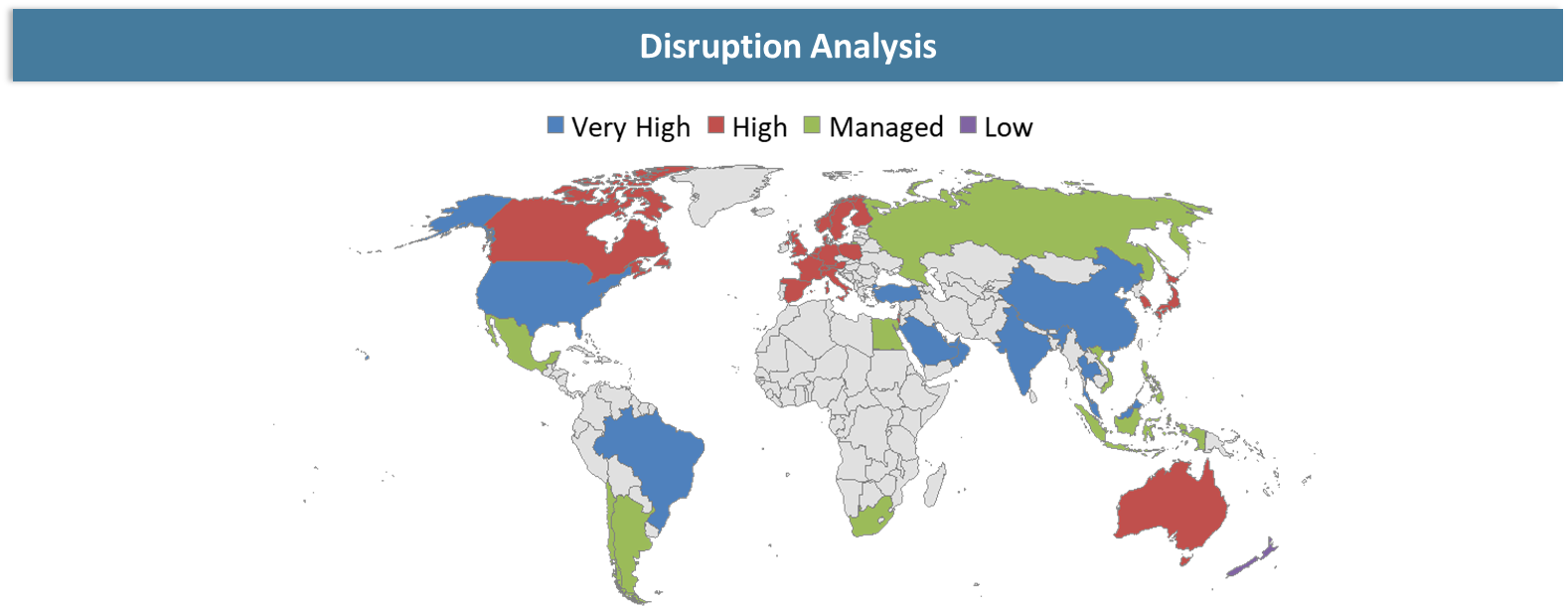

Disruption Analysis

Power flow control devices are an integral part of a wider shift in transmission approach, wherein system operators are now faced with greater pressure to utilize their current systems better before getting clearance for any big investments. It not only changes the purchasing dynamics but also gives rise to a different competitive landscape. Previous installations of FACTS were usually considered major substation projects, while the newer solutions were packaged as quick-fix solutions to congestion bottlenecks in transmission networks.

It allows the market to become more open to those utilities that need a small step-by-step improvement rather than a complete rebuilding of the entire corridor. The market can be further disrupted by new policy language that will classify certain grid enhancement technologies. As soon as regulatory bodies, planners and even market players recognize GETs within the framework of planning documents, it becomes easier for controller manufacturers to find their way into budget documents.

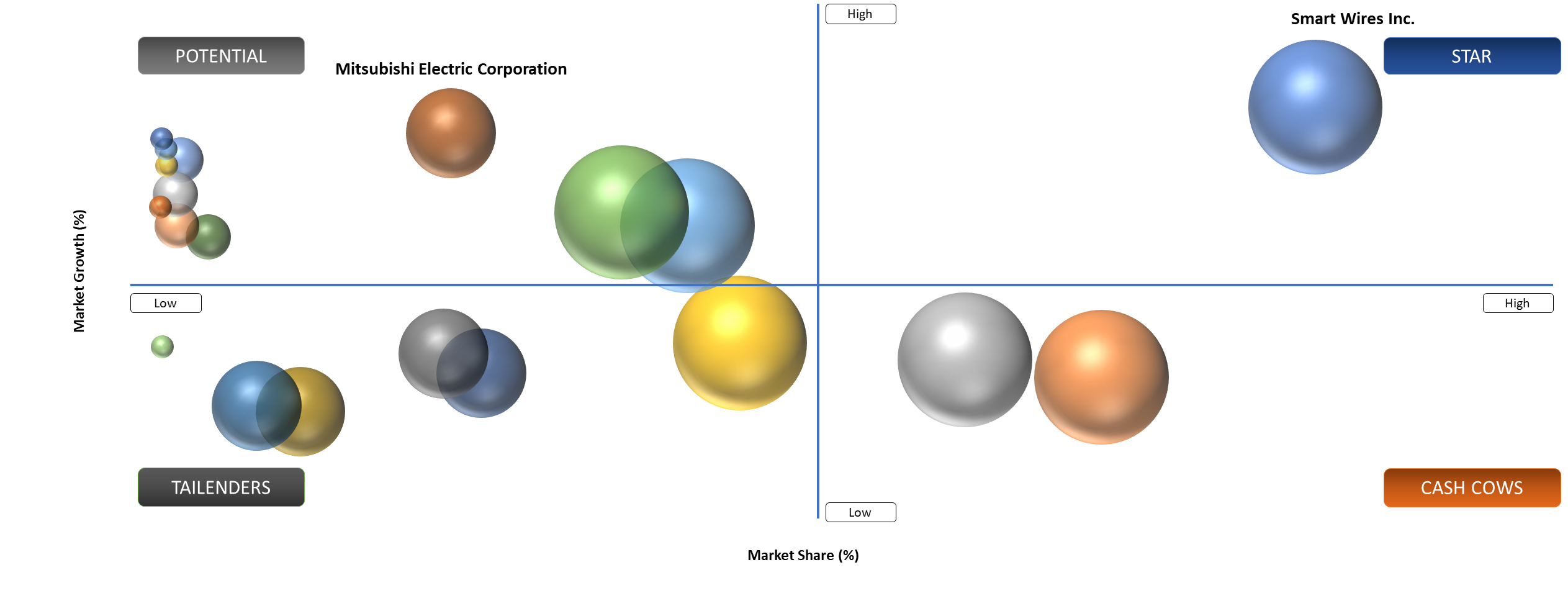

BCG Matrix: Company Evaluation

Star players balance technical legitimacy with grid flexibility discussions on a utility-grade level. Smart Wires is particularly well-placed for modular advanced power flow control solutions that serve as grid upgrades rather than single-substation improvements. Potential players have established grid experience, strong engineering backgrounds and legitimate procurement networks for utilities, even though power flow controllers contribute to just one aspect of a company's larger grid portfolio. Question Mark players have potential in cases when utilities seek alternatives, although they should enhance their visibility in specific advanced power flow applications.

Market Dynamics

Utilities are using controllability as a faster answer to transmission congestion than waiting for new line builds

Many power grids face increased congestion due to the rate at which power generation is increasing faster than the development of networks. The power flow controller provides utilities and grid managers with a mechanism for recovering their viable capacity and re-routing loads without first having to go through the process of sitting and permitting that might take several years.

It allows utilities to deal with congested lines, minimize thermal issues and make their N-1 operation comfortable in certain areas. Controllability becomes economically viable because of congestion, load curtailment, penalties for reliability and deferred interconnection. Vendors who convert these cost savings to utility-level metrics are helping the market evolve past pilot stories to budgetable projects.

Utility procurement still moves more slowly than the technical case for controllable power flow.

The problem is whether utilities can integrate effectively within the framework of their planning, regulatory and purchasing policies. Many utilities find themselves still more at ease investing in traditional transmission infrastructure because all the frameworks for this are already in place. It is true even when congestion economics favor a quicker move forward. Projects may get stuck among planning, operations and regulatory authorities if none take ownership.

Segmentation Analysis

The global power flow controller market is segmented based on the technology, voltage level, grid objective, deployment model, installation environment and region.

Modular Solutions Challenge UPFC Dominance as Utilities Prioritize Speed and Targeted Grid Optimization

The unified power flow controller continues to serve as a benchmark for high-level controllability in transmission system applications where operators seek broad flexibility in controlling voltage and line power characteristics. It will be most useful in situations where sophisticated utility grids are willing to invest heavily in advanced devices capable of being deeply engineered into their systems. Such systems typically favor it if they require sophisticated solutions to network problems and have patience for extended cycles of project development.

The problem with the classic implementation of UPFC technology is that it may sometimes feel bulky, given the context of the problem. It is because customers may not need such a robust feature set to solve their immediate problem. The other emerging trend in the industry is advanced modular power flow controllers because they suit today’s utility requirements for fast results and target solutions to corridor congestion. It suits customers who want quick wins and a focused approach to solving congestion problems without building new substations from scratch.

Geographical Penetration

North America Accelerates Power Flow Controller Market Growth Amid Rising Grid Congestion and Data Center Power Demand

The power flow controller market in North America is rapidly evolving on the back of growing power consumption, power congestion and the need for upgrade and replacement of outdated electrical grids. According to the U.S. Department of Energy, transmission congestion is one of the biggest problems that must be overcome to ensure that growing electricity requirements are met. It is especially important, since just the data centers in 2023 consumed almost 4.4% of all U.S. electricity and are expected to consume as much as 12% of all power generated by 2028. Grid modernization investments and funding through federal and utility programs have been making strides towards implementing digital control mechanisms and power electronics.

USA Power Flow Controller Market Trends

Utility companies and grids within the U.S. are incorporating FACTS, such as UPFC, to increase efficiency within the grid. The need for power flow controllers in North America is largely dictated by the requirements of grid development, renewable energy integration and managing congestion within the existing transmission networks. For example, utility companies like American Electric Power and PJM Interconnection have been actively working on FACTS implementation.

Canada Power Flow Controller Market Trends

The power flow controller market in Canada is witnessing a steady growth trajectory due to various factors such as electricity trade across borders, dominance of hydro power and need for grid balancing. Grids in provinces like Quebec and British Columbia have started implementing advanced grid technologies that would help to overcome the fluctuations related to the generation of hydro power and transmit power over long distances. Also, the Smart Renewables and Electrification Pathways Program of Natural Resources Canada is investing more than US$960 million to update their grid technology.

Competitive Landscape

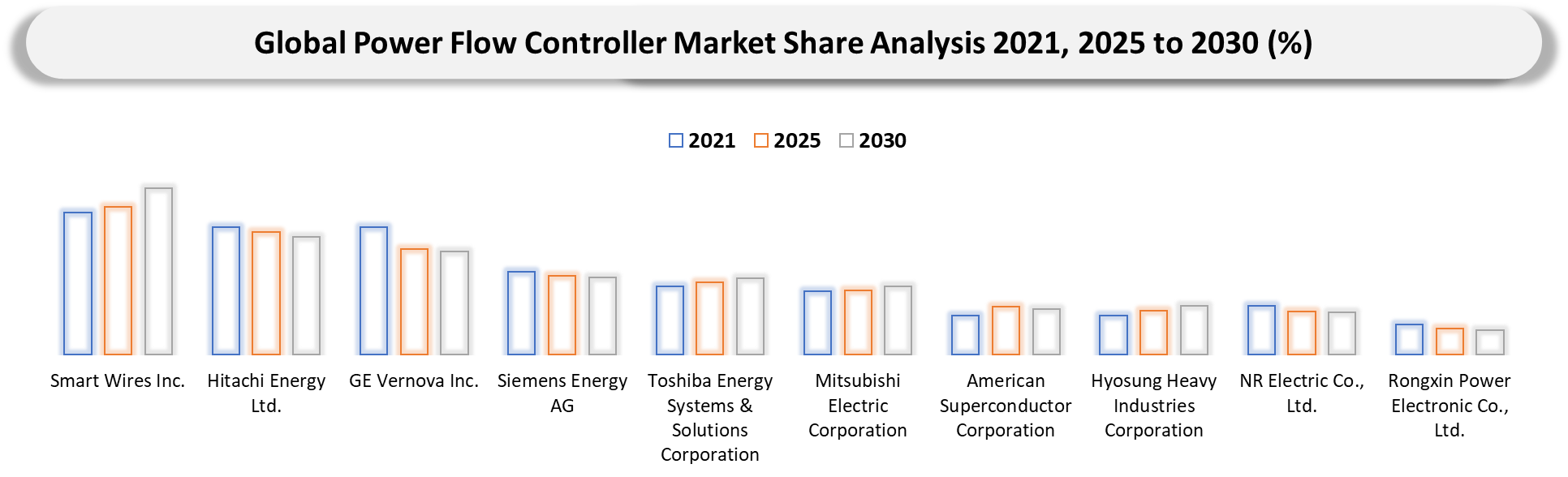

- The competition revolves around firms that can integrate power-electronic engineering knowledge with utility planning language. Firms such as Smart Wires Inc., Hitachi Energy Ltd., GE Vernova Inc. and Siemens Energy AG carry significant weight due to their ability to link controller technology with congestion control, reliability and implementation capabilities.

The competitive advantage is shifting toward firms that can integrate controllers as part of a broader grid enhancement or flexibility strategy. Companies with close ties to utilities but unclear positioning may be at a disadvantage to those that provide compelling applications, modular installations and accurate project valuations. The market is still nascent, meaning that successful demonstration projects can define a vendor's reputation for years to come.

Key Developments

- December 2025: Hyosung Heavy Industries Corporation expanded U.S. manufacturing investments to address rising grid equipment demand driven by renewable integration and power flow control requirements.

- November 2025: Siemens Energy AG announced a €2 billion global investment in transformer and grid infrastructure manufacturing, strengthening capabilities supporting advanced power flow control deployment.

- June 2025: GE Vernova Inc. signed an MoU with Smart Wires to enhance grid performance using advanced power flow control and digital grid optimization technologies.

- May 2025: Smart Wires Inc. partnered with PG&E, deploying SmartValve APFC devices, boosting substation capacity over 100 MW for data center-driven demand growth.

April 2025: Hitachi Energy Ltd. awarded a 6 GW, 950 km HVDC project in India, enabling bi-directional power flow control supporting renewable integration and grid stability.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Transmission System Operators and Independent System Operators: Grid operators evaluating controllable transmission capacity, congestion relief and reliability improvement across stressed corridors.

- Investor-Owned Utilities and Public Power Utilities: Transmission planners and grid-modernization teams comparing controller deployment against line rebuilds, reconductoring and substation expansion.

- Renewable Project Developers and Interconnection Sponsors: Companies affected by queue delays and constrained evacuation paths that benefit when grid operators unlock more usable transfer capability.

- Grid Planning and Power System Engineering Firms: Consultants and technical advisors modeling corridor stress, contingency support and power-electronics integration in transmission studies.

- Regulators and Energy Policy Institutions: Stakeholders shaping the treatment of grid-enhancing technologies within planning, cost recovery and reliability frameworks.

- Equipment EPCs and Grid Integrators: Contractors responsible for installation, systems integration and commissioning of advanced controllability solutions in live utility environments.

- Utility Digitalization and Control Room Teams: Operators assessing how controlled data, dynamic ratings and dispatch tools can work together in a more flexible transmission environment.

- Infrastructure Investors and Strategic Capital Providers: Investors evaluating GET-aligned technologies that can scale with transmission constraints and rising power demand.