Polypropylene Terpolymer Market Size

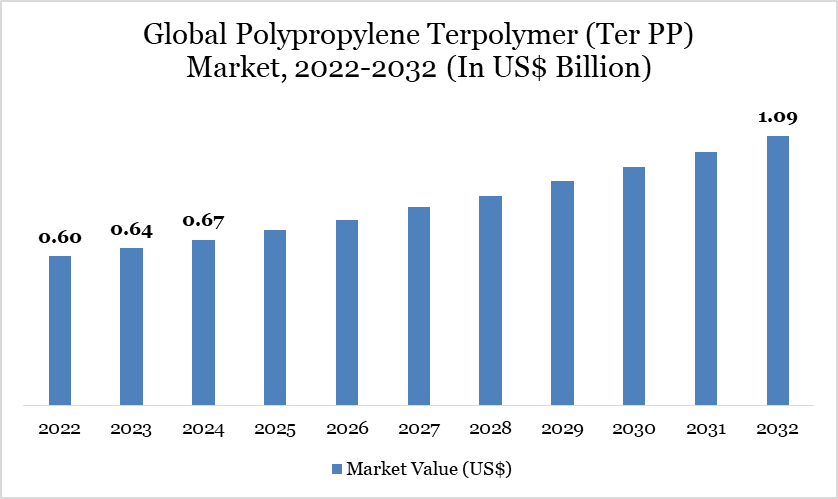

Global Polypropylene Terpolymer (Ter PP) Market reached US$ 710.96 Million in 2025 and is expected to reach US$ 1.09 billion by 2032, growing with a CAGR of 6.3% during the forecast period 2026-2033.

The global polypropylene terpolymer (Ter PP) market is experiencing robust expansion driven by escalating demand for high-performance, lightweight polymer solutions across key end-use industries such as packaging, automotive, healthcare, and consumer goods.

The packaging sector remains the largest segment, driven by heightened consumption of flexible films for food, pharmaceutical, and industrial packaging. Innovations in high-clarity and low-temperature seal films tailored to expanding global cold chain logistics further reinforce this trend.

The automotive industry is increasing its use of terpolymers for interior trim, battery components, and lightweight structural parts, aligning with broader industry efforts to reduce vehicle weight and emissions. The shift toward electric and hybrid vehicles amplifies this demand, as polymers contribute to improved energy efficiency without compromising performance.

Despite these strong tailwinds, the market faces notable headwinds, principally raw material price volatility related to propylene feedstock and ongoing supply chain uncertainties.

Polypropylene Terpolymer (Ter PP) Market Trend

Advancements in packaging solutions is a key trend which is increasing the adoption of Ter PP, contributing significantly to market growth. Polypropylene Terpolymer (Ter PP) has been adopted by a growing number of packaging industries due to its properties, including exceptional clarity, flexibility and resistance to a variety of environmental factors. It is evident from these factors that Ter PP has the potential to develop novel applications in the fields of industrial, pharmaceutical and food packaging.

The recyclable property of Ter PP will be perceived as a competitive advantage in the market by consumers who are becoming more aware of sustainable packaging. Ter PP's significance for the cause is underscored by the fact that 81% of consumers in the UK were already requesting sustainable packaging in 2023.

Source- DataM Intelligence

For more details on this report, Request for Sample

Market Scope

| Metrics | Details |

| By Processing Technology | Injection Molding, Extrusion, Blow Molding, Thermoforming, Others |

| By Sealing Temperature | Below 105°C, 105°C -115°C, Above 115°C |

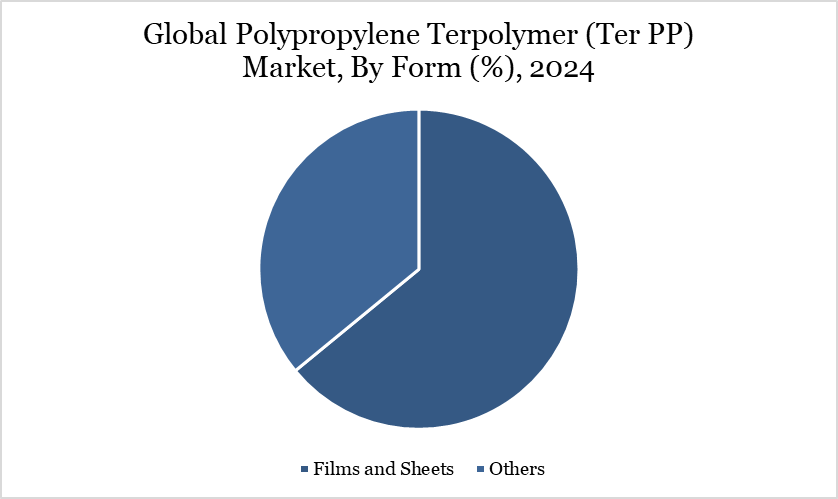

| By Form | Films and Sheets, Others |

| By End-User | Automotive Industry, Packaging Industry, Electrical and Electronics Industry, Building and Construction Industry, Healthcare Industry, Others |

| By Region | North America, South America, Europe, Asia-Pacific, Middle East and Africa |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Polypropylene Terpolymer Market Dynamics

Growing Demand in Automotive Applications

The automotive industry has experienced an increase in fuel efficiency and a decrease in emissions as a result of the current trend toward lightweight materials. Polypropylene Terpolymer (Ter PP) is essential for the production of a variety of automobile components, including bumpers, consoles and interior trims, due to its exceptional thermal stability and high impact resistance. Light polymers can result in a 50% reduction in a vehicle's weight and a 35% increase in fuel efficiency.

Manufacturers are making substantial enhancements to their operations in order to mitigate environmental regulations and maintain the production of their products. The global move toward electric vehicles has bolstered the argument for lightweight materials, which are essential for enhancing battery performance and overall vehicle efficiency. In fact, the International Energy Agency observed that electric car sales in 2023 were 3.5 million higher than in 2022, resulting in a 35% year-over-year increase. This increase will stimulate development in the Ter PP market.

Fluctuating Raw Material Prices

The fluctuating cost of raw materials, particularly propylene, presents a significant challenge to the Polypropylene Terpolymer (Ter PP) market. Propylene prices are closely tied to crude oil prices, which are subject to volatility due to factors such as geopolitical tensions, production cuts and economic fluctuations. In 2023, crude oil prices surged by 15%, directly impacting the production costs of propylene and, consequently, Ter PP.

This price increase can strain manufacturers who rely on stable raw material costs to maintain profitability and competitive pricing. Additionally, supply chain disruptions, notably those stemming from the Russia-Ukraine war, have further exacerbated the volatility of raw material prices. High raw material costs can deter companies from adopting Ter PP, especially in price-sensitive markets where alternatives may be more economically viable.

Polypropylene Terpolymer Market Segment Analysis

The global Polypropylene Terpolymer (Ter PP) market is segmented based on offering, sealing temperature, form, end-user and region.

Source- DataM Intelligence

Superior Quality of Films and Sheets Drives the Segment Growth

Films and sheets is expected to hold about 62% of the global market valuing about US$ 0.42 billion in 2024. The segment of Ter PP is highly valued for its superior properties such as high clarity, rigidity, excellent impact resistance and good chemical resistance, making it ideal for a wide range of industries. Films and sheets made from Ter PP are increasingly used in packaging, especially for food and consumer goods, due to their durability and barrier properties. These materials offer an alternative to traditional plastic films, providing lightweight and cost-effective solutions.

Ter PP films and sheets are used in automotive and electronics industries for protective coatings and insulation. Their ability to be easily processed into various shapes and sizes enhances their versatility, driving demand across multiple sectors. The Polyolefin Company offers COSMOPLENE Terpolymer grades which are available in film form and cater to a wide range of film extrusion processing technologies. These grades are ideal for various applications such as food packaging, overwrapping, cigarette/tobacco packaging, lamination etc.

Injection Molding

The injection molding segment accounts for a substantial share of Ter PP consumption globally, supported by rising demand for lightweight, durable, and aesthetically versatile plastic parts.

Injection molding represents one of the most commercially significant processing technologies within the global polypropylene terpolymer (Ter PP) market, driven by its ability to deliver complex geometries, high dimensional stability, and cost-efficient mass production.

Ter PP, with its enhanced impact resistance, improved transparency, and superior low-temperature performance compared to homopolymer and random copolymer PP grades, is increasingly preferred for precision-molded components across automotive, consumer goods, medical, and packaging applications.

Technological advancements in high-flow Ter PP grades are further enhancing process efficiency in injection molding by enabling shorter cycle times, reduced warpage, and improved surface finish.

Polypropylene Terpolymer Market Geographical Share

North America

The North America polypropylene terpolymer (Ter PP) market is witnessing steady expansion, driven by rising demand for high-performance, impact-modified polymers across packaging, automotive, and medical applications.

North America’s flexible and rigid packaging demand continues to expand in line with changing consumer lifestyles, e-commerce penetration, and convenience-driven product formats.

OEMs and Tier-1 suppliers are increasingly adopting Ter PP for interior trims, soft-touch components, and impact-resistant parts, as manufacturers prioritize weight reduction to meet fuel efficiency and emission standards.

North America benefits from strong feedstock availability and integrated polypropylene production capacity, particularly along the U.S. Gulf Coast. However, price volatility linked to propylene monomer fluctuations and competitive pressure from alternative polymers such as polyethylene and PET remain key challenges.

Sustainability Analysis

Polypropylene Terpolymer (Ter PP), like other polyolefins, is derived from fossil fuels primarily through the polymerization of propylene and other olefins. As such, its production contributes to carbon emissions and resource depletion. However, Ter PP's lightweight nature and durability enable manufacturers to use less material per product, reducing overall environmental footprint compared to heavier plastics or alternative materials. Moreover, the recyclability of Ter PP supports circular economy models, although global recycling rates remain suboptimal due to inadequate infrastructure and contamination issues.

Increasing global regulations on single-use plastics and carbon emissions are pushing the polymer industry to innovate. In response, several chemical companies are investing in bio-based or chemically recycled Ter PP variants to reduce environmental impact. Regulatory pressures, especially in the EU and North America, are accelerating demand for recycled-content plastics, with Ter PP being explored as a viable material for both mechanical and chemical recycling initiatives.

Polypropylene Terpolymer Market Major Players

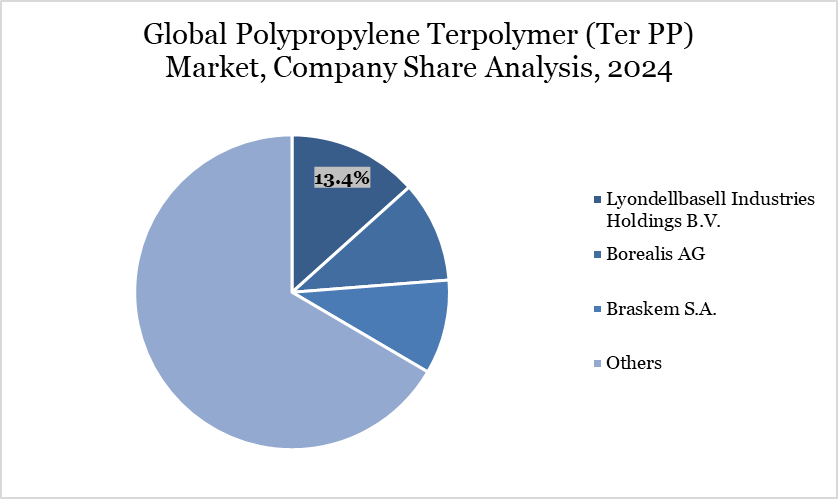

The major global players in the market include Lyondellbasell Industries Holdings B.V., The Polyolefin Company (Singapore) Pte Ltd., Borealis AG, W. R. GRACE & CO., HMC Polymers Company Limited, INEOS Group Holdings S.A., Braskem S.A., Jam Polypropylene Co. (JPPC), Mitsui Chemicals, Inc. and Hanwha TotalEnergies Petrochemical Co., Ltd.

Source- DataM Intelligence

Key Developments

Company Name Strategy Month & Year Development LyondellBasell Vertical Integration January 2024 Acquired a 35% stake in NATPET (Saudi Arabia) to secure feedstock for high-end PP grades. ExxonMobil Efficiency Optimization December 2025 Completed historical range review (2021–2024) to pivot toward 7.1% CAGR growth for bulk chemical resilience. SABIC Healthcare Localization January 2026 Full commercialization of medical-grade PP for syringes in Saudi Arabia to reduce import dependency. Borealis AG Capacity Expansion H2 2026 (Planned) Scheduled start-up of a new $100M+ High Melt Strength PP line in Germany for recyclable

foam solutions.

Sinopec Advanced Catalysis March 2023 Partnered with W. R. Grace to use UNIPOL PP and CONSISTA catalysts for advanced Ter PP grades. INEOS Decarbonization January 2025 Received giant prefabricated furnaces for Project ONE to modernize low-cost upstream production. HMC Polymers Sustainable Innovation February 2025 Launched the "NEVER STOP INNOVATING" vision targeting 31 billion Baht revenue through

Bio-Circular PP.

W. R. Grace & Co. Technology Licensing Ongoing 2024/25 Expanded UNIPOL PP licensing globally to enable regional producers to manufacture

high-clarity Ter PP.

Braskem S.A. Circular Economy July 2025 Integrated bio-attributed and recycled polymers into the Brazil high-performance PP

market strategy.