PFAS Water Treatment Market Size and Overview

The global PFAS water treatment market reached USD 3.4 billion in 2025 and is expected to reach USD 16.2 billion by 2035, growing with a CAGR of 16.9% during the forecast period 2026-2035. The market is witnessing increased investments being made by governments and water utilities in PFAS remediation in response to stricter drinking water regulations and increasing identification of water sources affected by contamination. In 2025, the U.S. EPA indicated that its drinking water treatment research encompasses 76 types of PFAS and reviews 35 treatment methods, among which GAC, ion exchange resins, and membrane-based technology are still the predominant commercially available options. U.S. Government Accountability Office (GAO) pointed out in 2025 that the federal PFAS drinking water regulation would cause thousands of public water systems to monitor and upgrade their water treatment facilities, resulting in a massive investment in the water infrastructure of municipalities. Major players such as Veolia, Xylem Inc., Calgon Carbon Corporation, AECOM, and Evoqua Water Technologies are developing advanced adsorption, filtration, and PFAS destruction technologies in response to the increased demand from municipal and industrial customers. Nevertheless, the issue of concentrate disposal, media replacement, and the capital-intensive nature of advanced destruction technologies hamper wider market adoption.

In October 2025, Chemical Processing published a report on PFAS Destruction and Removal Technologies, as the chemical industry is accelerating to address growing regulatory requirements for water and wastewater treatment. The report highlights that Lummus Technology's modular ZEO (Zimpro Electro Oxidation) system successfully demonstrated complete destruction of all identified PFAS compounds across industrial wastewater, drinking water, and landfill leachate applications. Additionally, reactivating spent granular activated carbon (GAC) can reduce treatment costs by 20–40% compared to purchasing virgin GAC, while AI-driven material discovery is helping develop more efficient PFAS treatment materials.

PFAS Water Treatment Market Key Takeaways

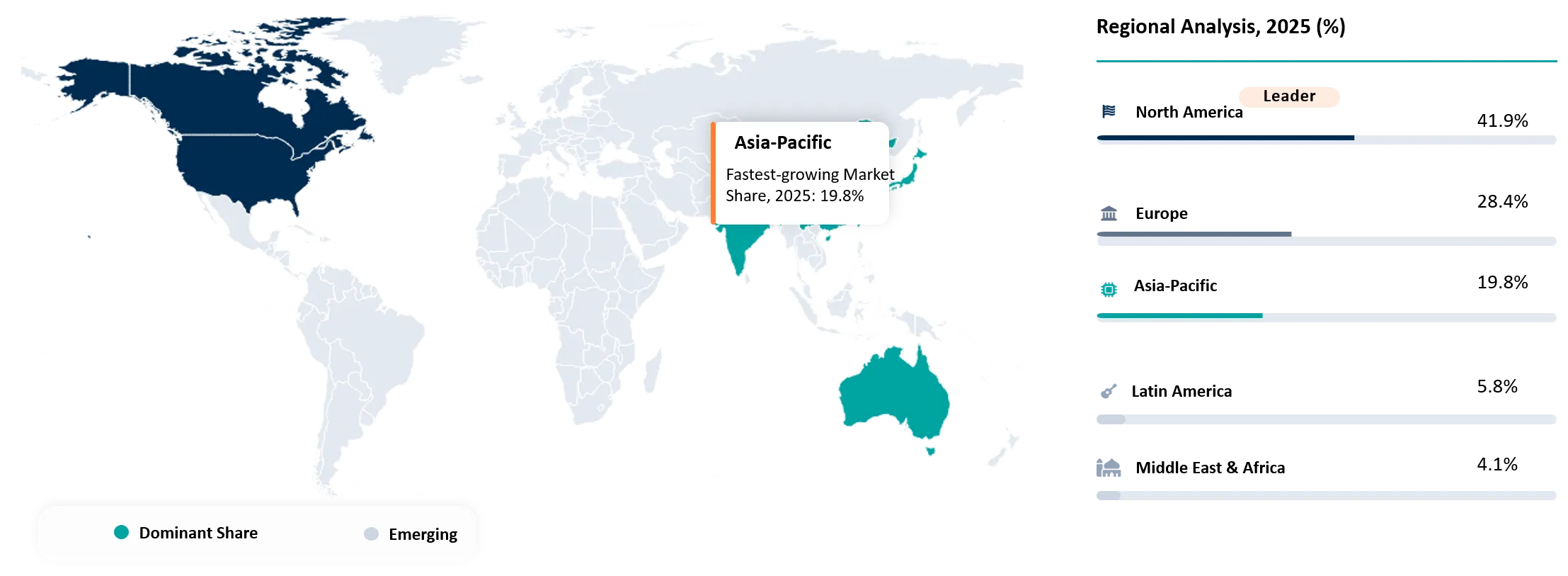

- North America led the global landscape by capturing a dominant 41.9% market share in 2025. Widespread regulatory frameworks and government-funded cleanups across municipal utilities maintain its leading position.

- Long-chain compounds represented the largest treated category by holding a 60% market share in 2025. Decades of historical usage in manufacturing and firefighting foams make these specific contaminants highly persistent.

- Enforceable regulatory limits act as the single strongest market driver, holding a 35% growth impact score. Under these rules, the U.S. EPA sets strict maximum contaminant limits at 4.0 parts per trillion (ppt) for PFOA and PFOS.

- Europe implemented strict new harmonized directive limits to monitor chemical presence across member nations. The regulations enforce explicit caps of 0.1 µg/L for the "Sum of PFAS" and 0.5 µg/L for "PFAS Total."

- The U.S. EPA significantly boosted advanced system deployment by unveiling funding worth almost US$1 billion in 2026. This financial injection targets state-level drinking water initiatives to fast-track cutting-edge destruction systems.

PFAS Water Treatment Market Industry Trends and Strategic Insight

- Municipal water infrastructure is becoming the largest investment segment. Utilities are accelerating capital expenditure on PFAS treatment systems as drinking water standards become more stringent.

- Rather than providing separate equipment to filter PFAS, suppliers are developing integrated PFAS concentration techniques along with subsequent destruction methods. Such a system will help reduce the disposal costs of used carbon, ion exchange resin, and RO concentrate.

- Source-point treatment of PFAS for the semiconductor industry, chemicals industry, electroplating, textile industry, airport operations, military installations, and landfill management is gaining popularity as a way of reducing PFAS contamination in discharges before they enter into the municipal water system.

- PFAS water treatment systems are implementing online monitoring, process control, predictive maintenance, and digital water management systems to ensure efficient treatment, improved regulation reporting, and reduced downtime at PFAS water treatment systems.

- With increased PFAS removal capacity expands focus on the proper disposal of spent PFAS removal media. The technology providers that offer closed loop systems for their PFAS removal media have an increasingly strong competitive edge.

PFAS Water Treatment Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 3.4 Billion | |

| 2035 Projected Market Size | USD 16.2 Billion | |

| CAGR (2026-2035) | 16.9% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Technology | Granular Activated Carbon (GAC), Ion Exchange Resins, Reverse Osmosis (RO), Nanofiltration (NF), Advanced Oxidation Processes (AOP), Electrochemical Oxidation, Plasma-Based PFAS Destruction, Foam Fractionation, Other Emerging PFAS Treatment Technologies | |

| By PFAS Type Treated | Long-Chain PFAS, Short-Chain PFAS, PFAS Mixtures | |

| By End User | Municipal Water Utilities, Industrial Facilities, Environmental Remediation Contractors, Defense & Military Facilities, Airports, Commercial & Institutional Facilities, Groundwater Remediation, Wastewater Treatment, Landfill Leachate Treatment, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

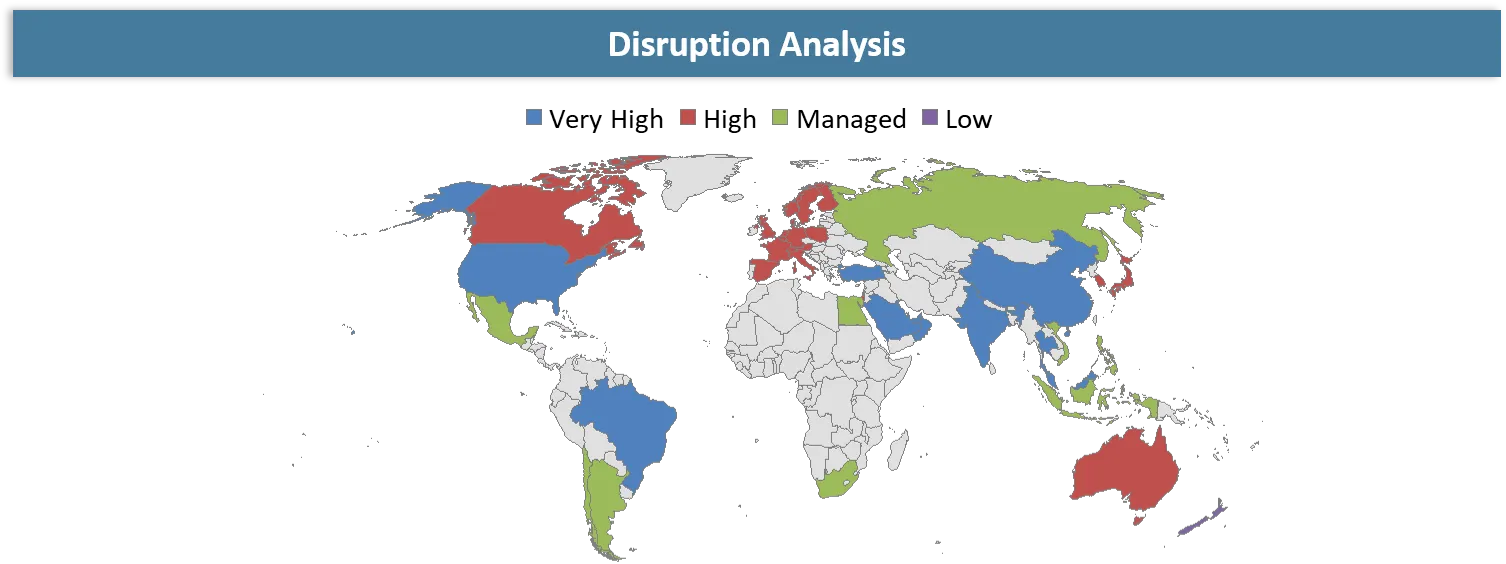

PFAS Water Treatment Market Disruption Analysis

Transition from PFAS Removal to PFAS Destruction Technologies Reshaping the Water Treatment Landscape

The primary disruption in the PFAS Water Treatment market is the transition from conventional PFAS separation technologies to PFAS destruction technologies. GAC, ion exchange resins, and RO are the most commonly used technologies for removing PFAS, but the problem is that they produce PFAS-containing waste that has to be disposed of or treated. This is pushing the development of PFAS destruction technologies, such as electrochemical oxidation, plasma treatment, SCWO, and hydrothermal alkaline treatment technologies, that can help shift from PFAS transfer to PFAS destruction. This disruption is compounded by the growing trend of regulatory backing and infrastructure development. In 2026, the U.S. Environmental Protection Agency (EPA) unveiled funding totaling almost US$1 billion in support of drinking water initiatives involving PFAS at the state level and with an emphasis on cutting-edge treatment and destruction systems.

Additionally, the organization issued an annual update to its Guidance for the Destruction and Disposal of PFAS, shifting from a three-year revision timeline in order to speed up the development and implementation of destruction technologies. The change is forcing the procurement strategy away from focusing exclusively on removal efficacy toward incorporating considerations like life-cycle cost, reduced residual waste, and destruction capability.

PFAS Water Treatment Market BCG Matrix: Company Evaluation

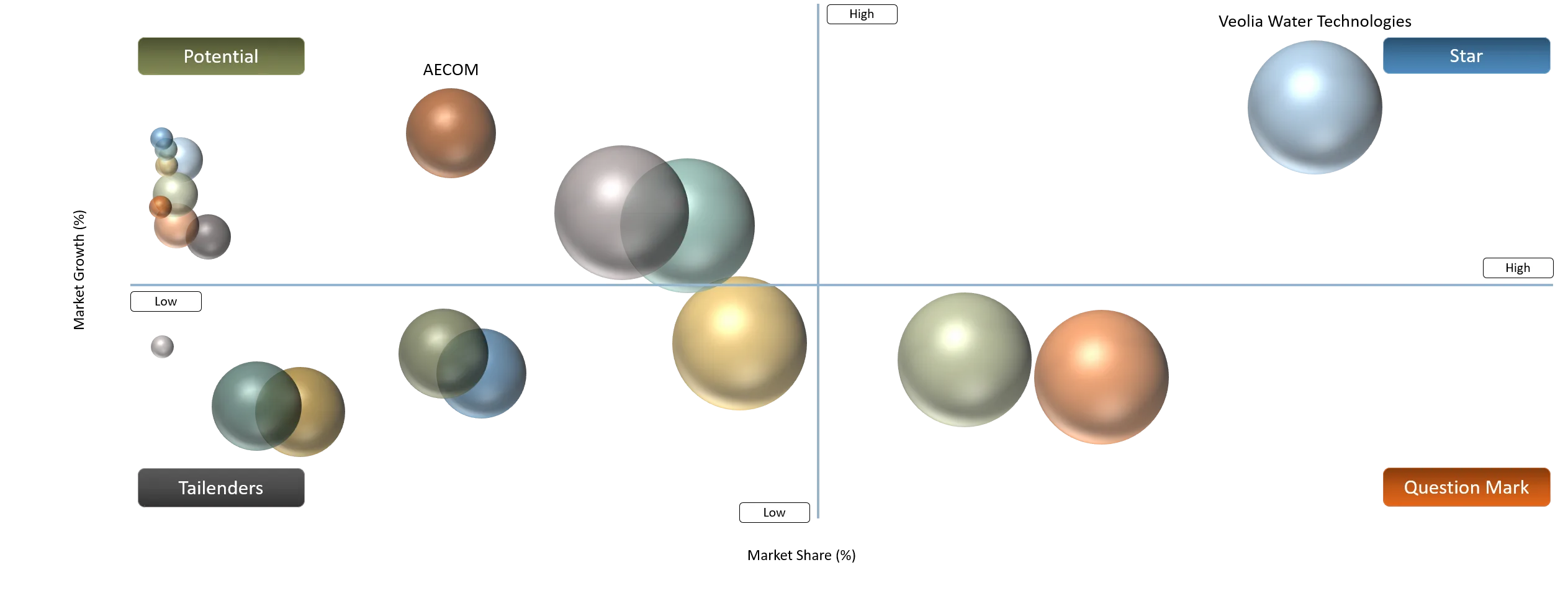

Stars include Veolia Water Technologies, Xylem Inc., and Calgon Carbon Corporation, which have been chosen since they are already widely utilizing PFAS removal technologies commercially in water infrastructures. The reason behind their inclusion is that they have significant global market presence, wide-ranging portfolios in terms of granular activated carbon (GAC), ion exchange, membranes, and combined systems, and they are further growing via technological advancements and acquisitions. Question Mark players include DuPont Water Solutions, Kurita Water Industries Ltd., and Aqua-Aerobic Systems, Inc. These companies possess high levels of expertise in membrane technology, ion exchange resin technology, and industrial water treatment, while constantly developing solutions for PFAS.

The potential includes AECOM, Jacobs Solutions Inc., and Black & Veatch. These are famous engineering and environmental infrastructure companies that have considerable experience working with PFAS remediation and treatment system design and municipal water infrastructure projects. Their competitive strength lies in EPC (Engineering Procurement Construction) and remediation work, instead of the technology they use. Tailenders consist of WSP Global Inc., Stantec Inc., and CDM Smith. These firms retain strong environmental consulting and water engineering competencies and are involved in projects relating to PFAS testing and remediation in several regions.

PFAS Water Treatment Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

The introduction of legally enforceable PFAS limits for drinking water is driving the market.

| 35% | Municipal water utilities, public drinking water systems, regulatory agencies | Drinking water treatment, municipal water infrastructure upgrades | Accelerates deployment of GAC, ion exchange, RO, and PFAS destruction technologies while driving long-term compliance investments. |

Rising Identification of PFAS-Contaminated Water Sources is expanding the number of remediation projects worldwide. | 27% | Environmental remediation firms, groundwater authorities, industrial site owners, landfill operators | Groundwater remediation, contaminated site cleanup, landfill leachate treatment | Expands remediation project pipeline and increases demand for mobile and permanent PFAS treatment systems. |

Expansion of Municipal Water Infrastructure Investments to comply with PFAS regulations. | 23% | Municipal utilities, engineering contractors, EPC companies | Water treatment plant modernization, new PFAS treatment facilities | Increases capital expenditure on advanced treatment systems, engineering services, and long-term operation & maintenance contracts. |

Growing Industrial Demand for PFAS Treatment are investing in on-site PFAS treatment systems to reduce contaminant discharge, meet environmental permits, and lower remediation liabilities. | 21% | Chemical manufacturing, semiconductor, metal finishing, textile, airports, defense facilities

| Industrial wastewater treatment, process water treatment, source-point PFAS removal | Drives adoption of decentralized treatment systems and creates demand for high-performance industrial PFAS treatment technologies. |

The introduction of legally enforceable PFAS limits for drinking water is driving the market

The implementation of enforceable PFAS limits for drinking water is the most important driver contributing to faster adoption of PFAS treatment technologies around the world. Since the regulatory bodies have started to enforce PFAS requirements on municipalities, water utilities, and industries, the investments made in granular activated carbon (GAC), ion exchange resins, RO, and PFAS destruction are growing to ensure regulatory compliance. According to the Environmental Protection Agency, it will ensure that the maximum contaminant levels (MCL) for perfluorooctanoic acid (PFOA) and perfluoro octane sulfonic acid (PFOS) are maintained at the federal level in relation to drinking water. Drinking water regulations, the MCL of PFOA and PFOS is 4.0 parts per trillion (ppt) each. This will help utilities comply with the standards by upgrading their existing infrastructure over a period of time. Moreover, public water systems must conduct PFAS monitoring and provide treatment in case of contamination beyond regulatory limits.

These stricter regulatory standards are expected to accelerate investments in new PFAS treatment technology solutions such as GAC, ion exchange resins, membranes, and new PFAS destruction technologies. On January 12, 2026, in accordance with the European Commission (Directorate-General for Environment), the new European Union-wide regulation on drinking water was adopted on 12 January 2026, mandating all Member States to monitor for the presence of PFAS in drinking water for the first time and to respect harmonized limit values within the recast Drinking Water Directive. The Directive sets out limit values of 0.1 µg/L for "Sum of PFAS" and 0.5 µg/L for "PFAS Total".

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

High Capital and Operating Costs of Advanced PFAS Treatment Systems such as reverse osmosis (RO), ion exchange resins, plasma treatment, electrochemical oxidation. | 22% | Municipal water utilities, industrial wastewater treatment facilities, remediation projects | Drinking water purification, semiconductor manufacturing wastewater, chemical processing, landfill leachate treatment | High installation costs, energy requirements, replacement of membranes/resins, and PFAS concentrate disposal expenses slow adoption, particularly among small and medium-sized utilities. Life-cycle studies published in 2025 identified capital and operational expenditure as major decision factors when selecting PFAS treatment technologies. |

Limited Commercial Maturity of PFAS Destruction Technologies. | 16% | Advanced destruction technologies including plasma treatment, electrochemical oxidation, supercritical water oxidation | Permanent PFAS destruction and concentrated waste treatment after separation processes | Emerging destruction technologies face challenges related to pilot-to-commercial scale transition, reactor complexity, energy consumption, and limited long-term operational data. This delays large-scale adoption compared with established separation technologies such as activated carbon and ion exchange. |

High Analytical Testing and Continuous Monitoring are increasing the overall cost of compliance for municipalities and industrial operators. | 14% | Water quality monitoring, regulatory compliance, laboratory testing infrastructure | Drinking water compliance monitoring, industrial discharge monitoring, environmental remediation sites | Continuous PFAS testing requires advanced analytical methods such as LC-MS/MS, skilled laboratory personnel, and frequent sampling programs, increasing the total cost burden for operators. Regulatory compliance cost assessments by the U.S. GAO in 2025 highlighted treatment, monitoring, and administrative expenses as major components of PFAS regulation implementation. |

Integrating PFAS treatment technologies into existing municipal and industrial treatment plants often requires significant infrastructure modifications. | 18% | Water treatment infrastructure, wastewater facilities, industrial processing plants | Municipal drinking water systems, chemical plants, manufacturing facilities, airports, military sites | Existing facilities often require additional land, process redesign, hydraulic modifications, and new waste handling systems to incorporate PFAS treatment units. These retrofit requirements increase project timelines and capital expenditure, limiting rapid deployment. EPA treatment cost models highlight that PFAS treatment costs vary significantly based on system design, flow capacity, site conditions, and technology configuration. |

High Capital and Operating Costs of Advanced PFAS Treatment Systems, such as reverse osmosis (RO), ion exchange resins, plasma treatment, and electrochemical oxidation

One of the major challenges restricting the widespread adoption of advanced PFAS water treatment technologies like reverse osmosis (RO), ion exchange resins, plasma treatment, and electrochemical oxidation is the high capital costs and operational costs related to their implementation. The installation of the system for PFAS removal involves the need to use special treatment devices, high-pressure membranes, chemically resistant installations, advanced measurement tools, and even waste treatment plants, resulting in an increased cost of the project for both local governments and industry representatives. High-pressure RO systems can remove up to 95% of PFAS from water, according to the ampacwatersystems, but at the same time, they create concentrated streams that have to be further removed or treated. According to EPA data, membrane-based technologies can remove more than 90% of PFAS, but 20% of the treated water remains high-strength waste.

Technical and economic problems associated with advanced PFAS treatment technology can affect its use, especially by smaller utilities and industry players who have limited budgets. In October 2025, Springer Nature published a report that scientists examined the advanced filtration techniques and electric membrane techniques used to clean PFAS-contaminated water, which included adsorption, nanofiltration (NF), reverse osmosis (RO), electrodialysis, and membrane-assisted decomposition. From this study, it is clear that approximately 70% of all membrane-based PFAS treatment research papers written in the years 2016 to 2025 were about filtration processes, and the existing commercial NF and RO membranes can remove about 99% of PFAS from water. However, the problem of the high cost of operation was mentioned as a significant obstacle in the review.

PFAS Water Treatment Market Segment Analysis

The global PFAS Water Treatment market is segmented based on technology, PFAS type treated, end user, and region.

Long-Chain PFAS Dominating Demand Due to Regulatory Focus and Historical Contamination Burden

The long-chain PFAS segment continues to dominate the PFAS water treatment market, with a 60% market share in 2025, driven by the historical prevalence of compounds such as PFOA and PFOS, their extreme environmental persistence, and the increasing requirement for removal from drinking water and industrial wastewater streams. In 2025, long-chain PFAS accounted for the majority share of PFAS remediation demand, as these compounds remain the primary contaminants detected in municipal water systems, groundwater, and industrial discharge sites due to decades of usage in applications such as firefighting foams, metal plating, textiles, and chemical manufacturing.

The widespread presence of PFAS contamination in U.S. drinking water supplies is increasing pressure on municipalities and water utilities to adopt effective PFAS removal technologies. According to Environment America in July 2025, citing the latest data from the U.S. Environmental Protection Agency (EPA), approximately 158 million people in the United States are at risk of exposure to PFAS-contaminated drinking water. Additionally, estimates indicate that PFOS and PFOA contamination may have affected the drinking water supplies of nearly 200 million people across the country, highlighting the widespread impact of legacy PFAS pollution and the increasing need for advanced water treatment solutions.

PFAS Water Treatment Market Geographical Penetration

Regulatory Enforcement and Large-Scale Remediation Investments Driving North America PFAS Water Treatment Market Leadership

The North American market dominates the PFAS water treatment market, supported by strict regulatory frameworks, widespread PFAS contamination across municipal and industrial water systems, and increasing investments in advanced remediation technologies. North America accounted for 41.9% of the global PFAS water treatment market share in 2025, making it the leading regional market due to early adoption of PFAS monitoring programs, government-funded cleanup initiatives, and strong demand from municipal utilities, industrial facilities, military sites, and airports. The presence of established environmental regulations and significant public awareness regarding PFAS health risks has accelerated the deployment of activated carbon, ion exchange, and membrane filtration technologies across the region.

As regulatory pressure on PFAS handling continues to increase, integrated environmental service providers are expected to play a larger role in supporting end-to-end PFAS treatment solutions. In November 2025, Veolia announced a $3 billion acquisition of Clean Earth, a U.S.-based hazardous waste management and remediation company, to expand its environmental services capabilities in North America. The transaction is expected to double Veolia’s U.S. hazardous waste footprint, add 2,600 employees, and strengthen treatment, storage, and disposal capabilities across more than 150 locations, including facilities supporting the management of emerging contaminants such as PFAS. The acquisition is valued at 9.8x 2026 estimated EBITDA and is expected to generate approximately $120 million in synergies by the fourth year.

U.S. PFAS Water Treatment Market Trends

The United States holds the dominant position in the North American PFAS water treatment market owing to its extensive legacy PFAS contamination, stringent federal and state regulatory framework, and significant investments in drinking water infrastructure and environmental remediation. The country has the largest concentration of municipal water utilities, industrial facilities, military bases, and airports requiring PFAS treatment, driving strong demand for advanced technologies such as granular activated carbon (GAC), ion exchange resins, reverse osmosis, and high-pressure membrane filtration.

The acquisition enhances Parsons' ability to deliver comprehensive PFAS remediation services by integrating advanced treatment technologies for contaminated water and environmental media. In February 2025, Parsons Corporation acquired TRS Group, Inc. in an all-cash transaction valued at $36 million to strengthen its environmental remediation capabilities across the U.S. TRS Group, founded in 2000, specializes in PFAS, thermal, and holistic remediation technologies and has completed more than 160 in-situ thermal remediation projects for treating hazardous contaminants, including PFAS, in soil, groundwater, and bedrock.

Canada PFAS Water Treatment Market Outlook

Canada is becoming a significant growth market in the North American PFAS water treatment industry due to increasing regulatory attention toward persistent chemical contamination, rising PFAS monitoring activities, and growing investments in municipal and industrial water treatment infrastructure. Although the United States remains the dominant market in the region, Canada is witnessing faster adoption of PFAS removal technologies as federal and provincial authorities strengthen controls on PFAS substances and address contamination risks in drinking water sources, industrial sites, airports, and firefighting training areas.

The development of advanced PFAS filtration technologies by Canadian companies is supporting the expansion of local treatment capabilities to address emerging water contamination challenges. In November 2025, Radio-Canada, Quebec-based Ecofilter Tek is developing an innovative PFAS removal solution for drinking water using advanced filtration technology based on ion-exchange resins and membrane systems. The company’s technology, designed to target persistent contaminants such as PFAS, aims to improve the efficiency and sustainability of water purification by providing high-performance filtration solutions for municipal and industrial applications.

PFAS Water Treatment Market Competitive Landscape

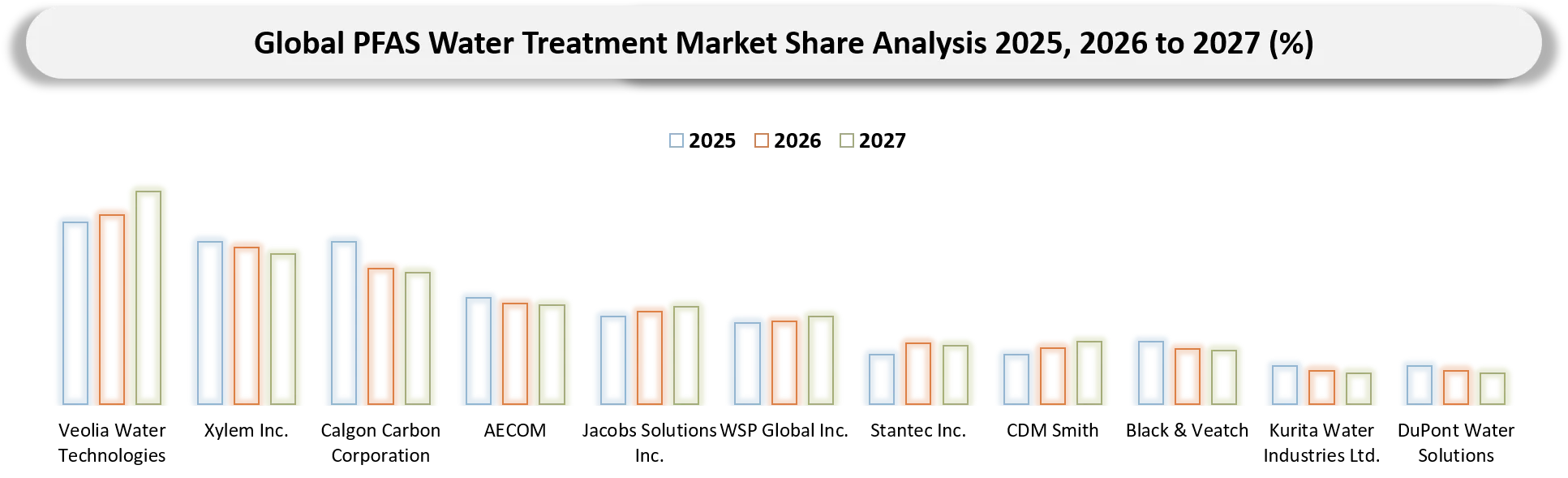

- The PFAS water treatment market is characterized by a mix of water technology providers, environmental engineering firms, remediation specialists, and advanced filtration solution companies competing across municipal water treatment, industrial wastewater, groundwater remediation, and PFAS destruction applications. The competitive landscape is highly fragmented, with leading players differentiating through treatment technology portfolios, project execution capabilities, regulatory expertise, and large-scale remediation experience. Companies such as Veolia Water Technologies, Xylem Inc., Calgon Carbon Corporation, and DuPont Water Solutions maintain strong positions through activated carbon adsorption, ion exchange, membrane filtration, and integrated PFAS removal systems. Engineering and environmental consulting firms, including AECOM, Jacobs Solutions Inc., WSP Global Inc., Stantec Inc., CDM Smith, and Black & Veatch, strengthen the market through PFAS assessment, remediation planning, and large-scale water infrastructure projects.

- Key players in the PFAS water treatment market include Veolia Water Technologies, Xylem Inc., Calgon Carbon Corporation, AECOM, Jacobs Solutions Inc., WSP Global Inc., Stantec Inc., CDM Smith, Black & Veatch, Kurita Water Industries Ltd., DuPont Water Solutions, and Aqua-Aerobic Systems, Inc.

Key Developments

- April 2025: Hawkins, Inc., completed the acquisition of WaterSurplus (Surplus Management, Inc.) to expand its U.S. water treatment capabilities and strengthen its portfolio of sustainable treatment solutions. WaterSurplus provides membrane separation systems, engineering and design services, media filtration systems, equipment manufacturing, rental units, and rapid-response PFAS removal solutions for “forever chemicals.”

- November 2025: Nijhuis Saur Industries (NSI), part of Saur Group, acquired a majority stake in Coldep, a French water treatment technology company, to strengthen its capabilities in advanced water treatment and emerging contaminant removal.

- September 2025: Kurita America company partnered with Cyclopure to deliver advanced PFAS removal and regeneration solutions by combining Cyclopure’s DEXSORB® regenerable adsorbent technology with Kurita’s water treatment engineering expertise.

- December 2025: Fermi National Accelerator Laboratory (Fermilab) partnered with Proficio Consultancy to develop an advanced PFAS water treatment system that uses electron beam accelerator technology to destroy PFAS contaminants in water.

- November 2025: Saur Group launched PFAS Resolve, an integrated PFAS water treatment solution designed to detect, concentrate, treat, and destroy PFAS contaminants across municipal and industrial water systems.

Key Procurement Priorities and Buyer Evaluation Criteria

- Organizations investing in the PFAS water treatment market increasingly prioritize suppliers based on their ability to provide high-efficiency PFAS removal solutions with proven performance across municipal drinking water, industrial wastewater, and groundwater remediation applications. Buyers evaluate treatment providers on their capability to remove persistent PFAS compounds such as PFOA and PFOS while meeting evolving regulatory requirements and ensuring long-term operational reliability.

- The procurement decision-making process is increasingly influenced by stricter PFAS regulations, rising contamination monitoring requirements, government-funded water infrastructure upgrades, and growing demand for sustainable remediation solutions. Utilities and industrial operators are prioritizing technology partners that can deliver scalable PFAS treatment systems capable of handling varying contamination levels while reducing lifecycle costs.

- Buyers consider factors such as PFAS removal efficiency, treatment capacity, operating cost, media replacement requirements, waste management capabilities, and compliance with regulatory standards when selecting PFAS water treatment providers. The ability to achieve low detection limits, minimize secondary waste generation, and provide reliable performance under different water conditions has become a critical evaluation criterion.

Why Choose DataM?

- Regulatory Landscape & Treatment Innovation: Explores advancements in PFAS water treatment technologies, including granular activated carbon (GAC), ion exchange systems, membrane filtration, electrochemical oxidation, and PFAS destruction technologies, highlighting how these solutions help utilities and industries comply with tightening PFAS regulations and achieve effective contaminant removal.

- Technology Performance & Market Positioning: Evaluates how treatment providers differentiate based on PFAS removal efficiency, treatment capacity, operating cost, scalability, waste management capabilities, and regulatory compliance. The analysis highlights the competitive positioning of companies offering solutions for municipal drinking water, industrial wastewater, groundwater remediation, and complex contamination sites.

- Real-World Evidence: Highlights real-world adoption of PFAS treatment solutions across municipal water facilities, manufacturing industries, airports, military installations, and firefighting foam-contaminated sites, demonstrating benefits such as reduced PFAS concentration levels, improved water safety, regulatory compliance, and long-term environmental risk reduction.

- Market Updates & Industry Changes: Tracks key developments such as new PFAS regulations, government funding initiatives, remediation projects, technology launches, partnerships, and infrastructure investments across North America, Europe, and Asia-Pacific. The report provides insights into how evolving environmental policies and increasing contamination awareness are reshaping the PFAS treatment ecosystem.

- Competitive Strategies: Analyzes how leading companies expand through advanced treatment technology development, strategic partnerships, project acquisitions, service expansion, and integrated water management solutions. The study evaluates competitive approaches adopted by water technology providers, engineering firms, and environmental remediation companies to capture increasing PFAS treatment demand.

- Pricing & Market Access: Explains cost variations based on contamination levels, treatment technology selection, system capacity, operational requirements, and lifecycle management needs. The analysis covers procurement models involving municipal utilities, industrial operators, engineering contractors, and remediation service providers to understand market accessibility and adoption barriers.

- Market Entry & Expansion: Identifies growth opportunities driven by stricter PFAS regulations, increasing drinking water safety requirements, industrial wastewater treatment demand, and large-scale remediation programs. The report outlines expansion strategies such as regional project execution, technology partnerships, customized treatment solutions, and investment in next-generation PFAS removal and destruction technologies.

Target Audience

- Water Treatment Technology Providers

- Municipal Water Utilities & Public Water Suppliers

- Industrial Wastewater Treatment Operators

- Environmental Engineering & Remediation Companies

- Government Agencies & Regulatory Bodies

- Investors, Private Equity Firms & Venture Capital Companies

- Chemical & Filtration Material Manufacturers