PFAS Testing Market Overview

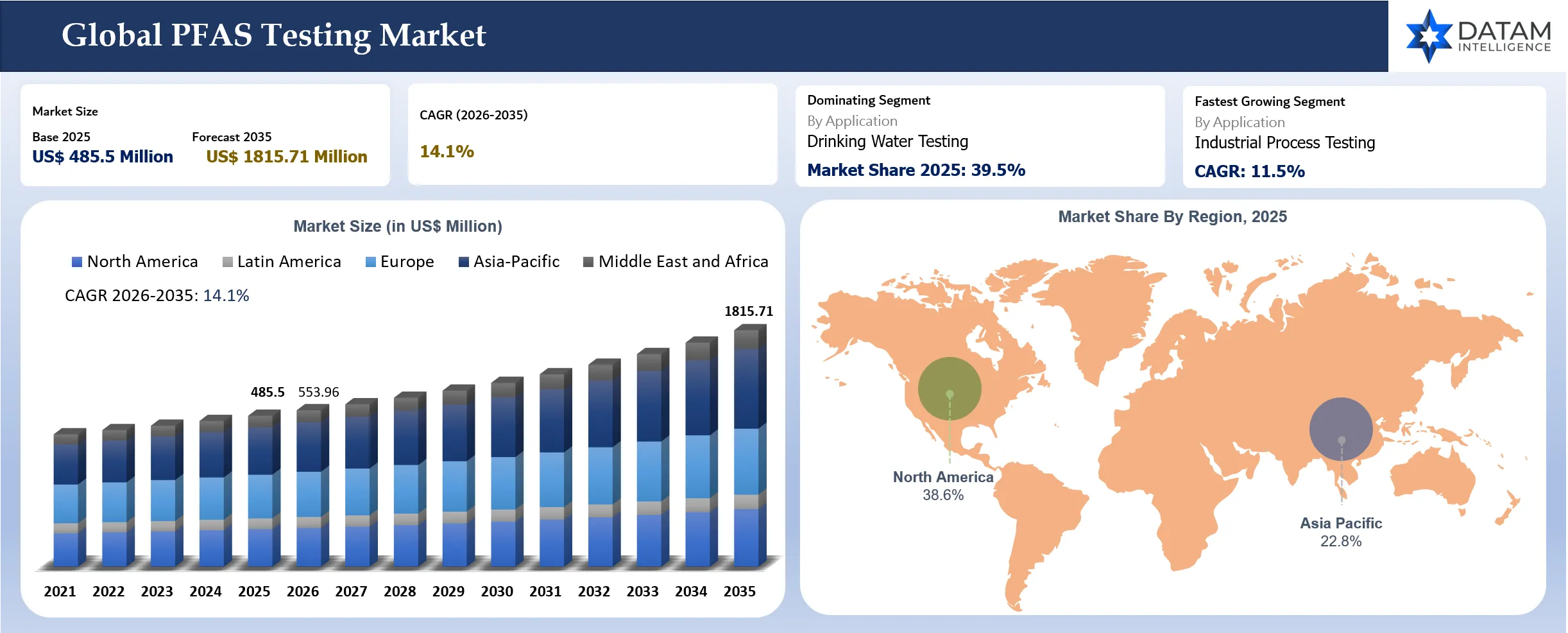

The global PFAS Testing Market reached US$ 485.5 million in 2025 and is expected to reach US$ 1815.71 billion by 2035, growing with a CAGR of 14.1% during the forecast period 2026-2035. Witnessing strong market growth owing to increasing regulatory scrutiny on per- and polyfluoroalkyl substances (PFAS) contamination across water sources, industrial emissions, food products, and consumer goods globally. Rising public health concerns and growing environmental monitoring initiatives are accelerating demand for advanced PFAS analytical services with ultra-trace detection capabilities. Increasing adoption of LC-MS/MS and high-resolution mass spectrometry technologies is further supporting testing accuracy and operational efficiency across laboratories. Expansion of remediation projects, wastewater treatment investments, and industrial compliance programs are additionally contributing to market expansion. Companies including Eurofins Scientific, SGS, Intertek, Agilent Technologies, and Thermo Fisher Scientific are strengthening their PFAS testing portfolios through laboratory expansion, advanced analytical solutions, and regulatory support services.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 485.5 Million | |

| 2035 Projected Market Size | US$ 1815.71 Million | |

| CAGR (2026-2035) | 14.1% | |

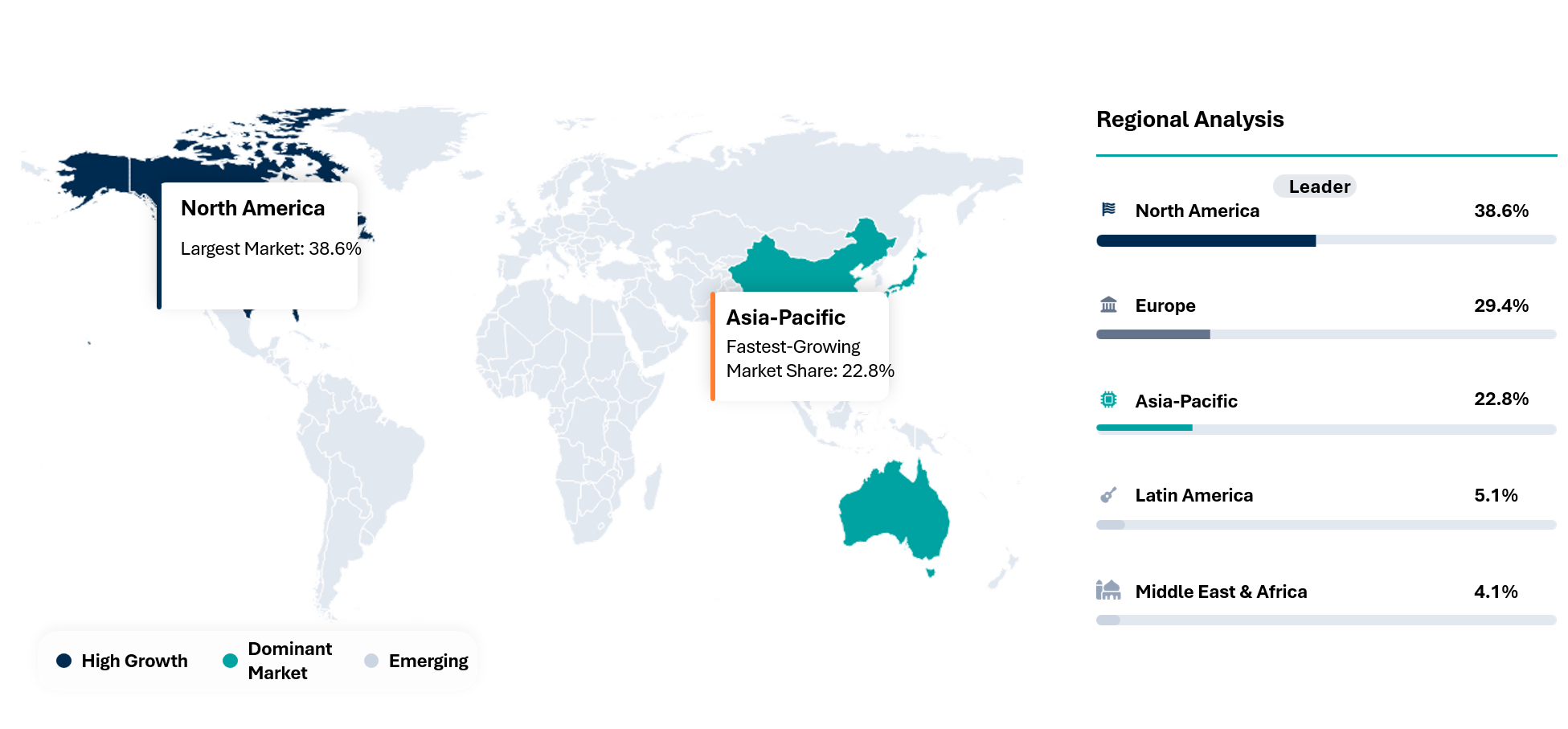

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Offering | PFAS Testing Services, Certified Reference Materials and Standards, Sample Preparation Products, Laboratory Consumables, Software and Data Management Solutions, Regulatory and Consulting Services, Others | |

| By Testing Method | EPA 533, EPA 537 / 537.1, EPA 1633, ASTM Methods, ISO Methods, Proprietary/In-House Methods, Others | |

| By Technology | LC-MS/MS, High-Resolution Mass Spectrometry (HRMS), Gas Chromatography-Mass Spectrometry (GC-MS), Combustion Ion Chromatography (CIC), Total Organic Fluorine (TOF) Analysis, Non-Targeted Analysis (NTA), Others | |

| By PFAS Type | Long-Chain PFAS, Short-Chain PFAS, Ultra-Short-Chain PFAS, Fluoropolymers, Others | |

| By Sample Type | Drinking Water, Groundwater, Wastewater, Soil & Sediment, Air Emissions, Biosolids & Sludge, Food & Beverage, Biological Samples, Industrial Effluents, Consumer Products, Others | |

| By Application | Drinking Water Testing, Wastewater and Industrial Effluent Testing, Environmental Testing, Food and Consumer Product Testing, Biological and Healthcare Testing, Industrial Process Testing, Research and Development, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Key Takeaways

- North America is dominating the global PFAS testing market, accounting for a share of 38.6% in 2025.

- In 2025, drinking water testing application and use cases led the market with a share of approximately 39.5%.

- Industrial process testing is the fastest-growing application and use cases in 2025, with a CAGR 11.5%.

- PFAS regulations introduced by the United States Environmental Protection Agency (EPA) and global environmental agencies are major drivers accelerating demand for PFAS testing services due to increasing mandatory monitoring requirements across drinking water systems, industrial facilities, wastewater treatment plants, and environmental remediation projects.

- Eurofins Scientific, SGS SA, Intertek Group plc, Thermo Fisher Scientific, and Agilent Technologies are strengthening market growth through expansion of advanced analytical laboratory networks, adoption of LC-MS/MS and high-resolution mass spectrometry technologies, and development of ultra-trace PFAS detection capabilities for environmental, industrial, and public health compliance applications.

PFAS Testing Industry Trends and Strategic Insight

- The PFAS testing market is undergoing rapid transformation into ultra-trace analytical techniques like LC-MS/MS, HRMS, and non-target analysis due to growing regulatory pressures and demands for extensive PFAS analytes. Firms such as SGS SA, Eurofins Scientific, and Intertek Group Plc have been enhancing their analytical capacities and laboratories for various applications of drinking water, industry, and the environment.

- The PFAS testing industry is seeing an increasing shift towards extensive multi-matrix testing services such as testing in drinking water, waste water, biosolids, food packaging materials, healthcare products, and semiconductor manufacturing facilities. The firms that are making significant progress in terms of EPA 1633 compliant testing, contamination risk assessment, and automation of analysis include SGS and Eurofins.

- Growing environmental remediation projects, stringent contaminant concentration limits, and higher compliance in industries are driving the demand for scalable PFAS testing solutions from leading firms such as ALS Limited, Montrose Environmental Group, and Pace Analytical Services.

Disruption Analysis

Rapid regulatory changes continuously alter laboratory testing requirements

The disruptive nature in the PFAS testing industry can be largely attributed to evolving regulations and the ongoing increase in the number of regulated PFAS substances in various jurisdictions around the world. The environmental bodies continue updating the acceptable exposure levels as well as new testing methodologies for drinking water, wastewater, soil, emission gases, and industrial products. The process is creating disruptions for the traditional processes employed by laboratories, which are being pushed to constantly improve their abilities to test for these substances, including compliance mechanisms.

Technological disruption is also evident in the PFAS testing industry through the shift in focus from targeted tests to NTA, HRMS, and ultra-trace detection. The older testing techniques that were used to detect legacy PFAS chemicals have become inadequate given the demands for wider analyte screening capabilities and faster turnaround times for results. Testing facilities as well as instrumental makers are thus rethinking how they operate, incorporating innovations such as automation and AI-powered analytics.

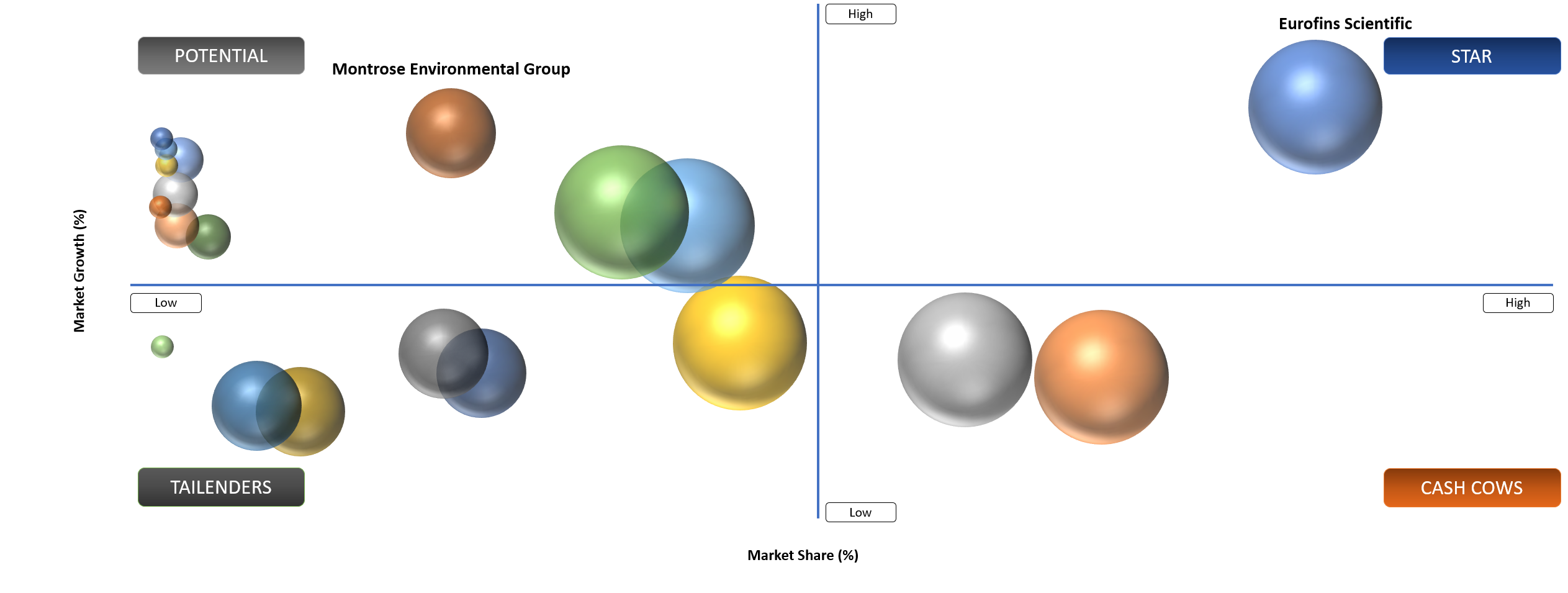

BCG Matrix: Company Evaluation

Stars companies like Eurofins Scientific, SGS SA, and Intertek Group plc due to the robust international presence of their laboratories, PFAS analysis expertise, and comprehensive compliance portfolios. Question Marks category are ALS Limited, Bureau Veritas, and Pace Analytical Services because they are building PFAS testing capabilities to enhance their position in the market through increased investments in new analysis technologies.

Potential companies such as Montrose Environmental Group, GEL Laboratories, and Battelle Memorial Institute due to their increasing role in environmental remediation services and testing contracts as well as their analysis for contaminants in the environment. Enthalpy Analytical is among the Tailenders because its PFAS testing services are more specialized and limited to a particular region than multinational companies engaged in environmental testing and inspections.

Market Dynamics

Driver Impact Analysis

| Driver | Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Stringent PFAS regulations by the United States Environmental Protection Agency and global regulatory agencies are increasing mandatory testing requirements | 5.4% | North America environmental agencies, European regulatory ecosystem, municipal water authorities | Drinking water testing, wastewater compliance monitoring, industrial discharge assessment | Accelerates adoption of PFAS analytical services and expands regulatory-driven testing infrastructure globally |

Increasing adoption of LC-MS/MS technologies for trace-level PFAS detection is supporting market growth | 4.9% | Advanced analytical laboratories, environmental research institutes, industrial compliance facilities | Ultra-trace PFAS detection, food safety analysis, biological sample testing | Strengthens analytical precision and improves multi-compound detection capabilities across testing laboratories |

Rising contamination concerns associated with groundwater, soil, and landfill sites are increasing environmental monitoring activities | 4.7% | Environmental remediation contractors, industrial zones, contaminated site management programs | Soil testing, groundwater analysis, remediation monitoring | Expands long-term environmental assessment contracts and increases recurring testing demand |

Increasing PFAS testing demand from semiconductor, electronics, and advanced manufacturing industries | 4.5% | Asia-Pacific electronics manufacturing hubs, semiconductor fabrication clusters, industrial process facilities | Ultra-pure water testing, industrial process monitoring, contamination control | Supports expansion of specialized high-sensitivity testing solutions for advanced manufacturing applications |

Stringent PFAS regulations by the United States Environmental Protection Agency and global regulatory agencies are increasing mandatory testing requirements

Stringent PFAS regulations imposed by the US EPA and other international agencies are rapidly leading to mandatory testing requirements in drinking water systems, industry, and environmental monitoring programs. As per EPA in May 2025, the EPA is ensuring the continued existence of National Primary Drinking Water Regulations (NPDWRs) for PFOA and PFOS while allowing additional time for compliance, emphasizing the long-term requirement for public water systems and laboratories to conduct ongoing monitoring. The EPA has further provided guidelines on implementation, laboratory testing requirements, and analytical methods, which include EPA Method 537.1, as part of PFAS monitoring programs. Additionally, the EPA requires public water systems to implement initial PFAS monitoring before 2027 and subsequent compliance monitoring programs thereafter.

With the emergence of increasingly strict regulations, there is a substantial push towards investments in laboratory facilities, technology, and environmental compliance programs. For instance, as per the report by the EPA, the final rule on the PFAS drinking water regulation will be able to protect more than 100 million individuals from exposure to PFAS chemicals, and prevent several deaths and severe illnesses as well. Additionally, it was reported that the EPA will fund USD 1 billion under the Infrastructure Investment and Jobs Act to help out with the implementation of PFAS testing and treatments in public water systems. With increasing regulations, there will be growing adoption of cutting-edge technology, including LC-MS/MS and high resolution mass spectrometry, which will help in attaining ultra-trace detection limits for regulated PFAS. As regulations keep evolving and contamination limits are lowered further, lab reports become more stringent, and there are stricter restrictions on the industry’s discharges; PFAS testing has become a crucial obligation in the long run.

Restraint Impact Analysis

| Restraint | Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

Extremely low detection limit requirements increase quality control complexity | 4.2% | Laboratory quality assurance systems and analytical validation processes | Ultra-trace PFAS analysis, regulatory compliance testing | Increases operational complexity and extends validation timelines for testing laboratories |

High capital investment requirements for advanced analytical instruments limit adoption among small and mid-sized laboratories | 4.5% | Laboratory infrastructure expansion and technology procurement | LC-MS/MS deployment, HRMS-based analytical testing | Restricts market entry and slows advanced testing capability expansion in emerging laboratories |

Limited availability of standardized global testing protocols creates operational inconsistencies | 3.8% | Cross-border laboratory harmonization and regulatory alignment | International compliance testing, multi-region environmental monitoring | Complicates result comparability and increases procedural adaptation requirements across laboratories |

Risk of sample contamination during collection and preparation affects testing reliability | 3.9% | Sample handling procedures and laboratory workflow management | Water sampling, soil testing, biological sample preparation | Raises re-testing requirements and increases overall operational costs for PFAS analytical services |

Extremely low detection limit requirements increase quality control complexity

Ultra-low detection limits present significant operational and quality control challenges for laboratories analyzing PFAS worldwide. Modern PFAS regulation often calls for ultra-low detection limits, which necessitate the use of ultra-clean analytical spaces and sensitive testing. Laboratory contamination, whether through tubing, solvents, gloves, protective clothing, or sample containers, may lead to inaccurate results and false positives. This leads to an increase in re-tests, quality control difficulties, and operational costs for testing laboratories.

Furthermore, laboratories are forced to ensure calibration verifications, duplication tests, blank analyses, and intricate sample preparations to stay up to date with regulatory standards. The growing trend in terms of expanding analyte lists from traditional PFAS substances to short-chain and novel fluorine-containing substances has been leading to a growing need for advanced testing. Testing laboratories are therefore under pressure to acquire liquid chromatography mass spectrometry systems, cleanrooms, automation, and train their staff. This operational and capital cost burden poses a challenge when scaling up operations, especially for small and medium-sized laboratories that wish to expand PFAS testing facilities.

Segmentation Analysis

The global PFAS testing market is segmented based on offering, testing method, technology, PFAS type, sample type, application, and region.

Increasing Regulatory Monitoring Requirements for Drinking Water Safety are Driving Demand for PFAS Drinking Water Testing

The drinking water testing segment is the leading application area in the PFAS testing market with a substantial market share owing to the factors such as stringent regulations, rising contamination concerns, and public health monitoring programs. Rising contamination of PFAS compounds in municipal water systems, groundwater reservoirs, and public water distribution network is driving the demand for ultra-trace analysis that will detect contaminants in parts per trillion level. Increasing adoption of advanced analytical methods like liquid chromatography-mass spectrometry (LC-MS/MS), and high-resolution mass spectrometry among others to ensure regulatory compliance and water quality is contributing to the growth of this segment.

Laboratory facilities continue to enhance their drinking water testing capabilities and analytical capacities in response to increased demand. For instance, in July 2025, SGS, which is a Swiss-based company, introduced enhanced PFAS testing and analysis capabilities that enable testing and analysis of samples from drinking water, groundwater, wastewater, biosolids, and other environmental samples using EPA-compliant analysis techniques such as EPA 1633. SGS also provided PFAS sampling kits and non-targeted analysis services to assist its customers in ensuring proper compliance with relevant regulations. This demonstrates the trend toward enhancing analytical capabilities for long-term monitoring of drinking water.

Geographical Penetration

Expanding Regulatory Compliance and Advanced Analytical Infrastructure are Strengthening North America’s Leadership

North America remains the key regional market for PFAS testing owing to strict environmental regulations, strong presence of testing laboratories, and an increase in drinking water monitoring programs in the US and Canada. Growing concerns regarding PFAS contamination are driving demand for high-end analytical solutions in municipalities, industries, the healthcare sector, and consumer products companies in the region. North America is also seeing increased uptake of technologies such as liquid chromatography-tandem mass spectrometry (LC-MS/MS) and high-resolution mass spectrometry for the detection of ultra-trace PFAS. Increasing remediation efforts and regulatory compliance are further boosting the growth of the market in North America.

For example, in December 2025, Eurofins Scientific introduced the first-ever GMP PFAS testing and screening solution for the medical devices industry to address regulatory compliance issues. The solution consisted of combustion ion chromatography, extractables & leachables testing, toxicological risk assessment, and contamination pathways identification for detecting PFAS in medical applications. The development reflects the growing trend of investment by the industry in extending the scope of PFAS analysis beyond environmental testing to highly regulated industries including healthcare. Increasing investments in PFAS-specific testing solutions will ensure continued leadership of North America in the regulatory-driven contamination monitoring and compliance tests market.

U.S PFAS Testing Market Trends

The U.S dominates the PFAS testing market in North America due to strict EPA guidelines and large-scale initiatives to monitor drinking water, coupled with the growth of remediation in the industries and municipal settings. Increasing concerns about the presence of PFAS in groundwater systems, wastewater treatment plants, and manufacturing processes are driving demands for advanced analytical techniques such as LC-MS/MS and high-resolution mass spectrometry.

For instance , in February 2025, SGS extended its PFAS testing capacity in the U.S through the acquisition of RTI Laboratories located in Detroit, Michigan, becoming the firm's eighth dedicated PFAS lab. This move reflects the growing commitment of companies to enhance their laboratory capacities amid increased PFAS monitoring requirements in the country.

Canada PFAS Testing Market Outlook

The PFAS testing market in Canada is experiencing growing momentum on account of escalating contamination control standards, extensive environmental testing initiatives, and strict regulations in the healthcare, pharmaceutical, and water treatment sectors. Heightened awareness about PFAS contamination in the water supply, biosolids, and industrial effluents is driving demand for more sophisticated testing solutions.

For instance, in May 2025, SGS announced the extension of ISO 17025 accreditation at its pharmaceutical lab in Mississauga, Canada, enabling better extractables and leachable testing solutions to serve the needs of pharmaceutical, biopharmaceutical, and medical device makers.

Regulatory Analysis

The global regulatory regime on PFAS substances is increasingly stringent, with governments now seeking to impose very tight restrictions on detectability, measurement, and safe exposure limits in drinking water, soils, wastewater, food packaging materials, and industrial effluents. In the U.S., the EPA has established binding drinking water standards for specific PFAS chemicals and increased nationwide testing requirements for all public water systems. In Europe, the European Chemicals Agency (ECHA) is working towards proposing a wide-ranging PFAS restriction under REACH legislation, which would seek to limit its use both industrially and consumer-wise.

In the Asia-Pacific region, countries like Japan, South Korea, China, and Australia are enhancing their environmental monitoring policies and aligning themselves with global standards regarding PFAS limits, especially when it comes to water and industrial waste discharges. At the same time, countries like Canada have introduced more stringent regulations with respect to the PFAS monitoring program and environmental protection. The OECD and other global organizations are advocating for standardized PFAS test methods and risk assessments, thus contributing to a harmonized approach toward PFAS testing. All these regulatory initiatives continue to spur the growth of the analytical testing market and drive the use of innovative technologies such as EPA 1633 and LC-MS/MS.

Competitive Landscape

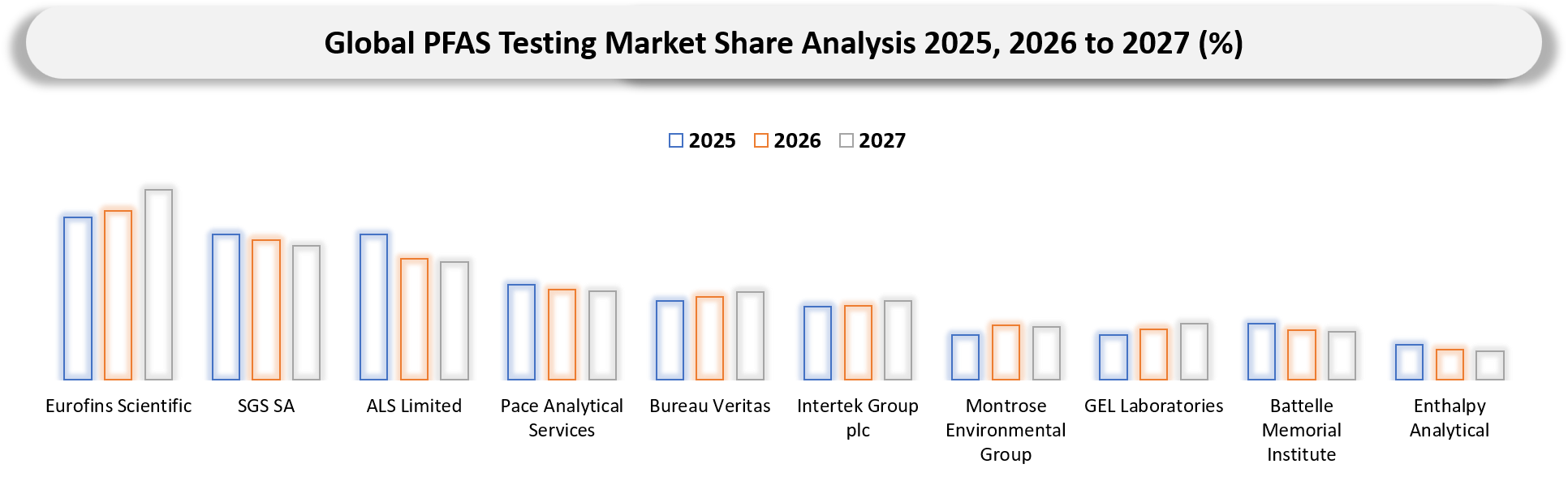

- The market is characterized by three key participant groups: global environmental and analytical testing companies, specialized environmental monitoring and remediation providers, and research-focused analytical laboratories. Eurofins Scientific, SGS SA, Intertek Group plc, Bureau Veritas, ALS Limited, and Pace Analytical Services lead through extensive laboratory networks, regulatory compliance services, and advanced PFAS analytical capabilities; Montrose Environmental Group and GEL Laboratories focus on environmental remediation, contamination assessment, and specialized PFAS monitoring solutions; while Battelle Memorial Institute and Enthalpy Analytical strengthen the market through research-driven analytical expertise and advanced environmental testing services. This creates a highly regulation-driven and technology-intensive competitive landscape where laboratory scale, analytical sensitivity, accreditation capabilities, and compliance expertise define market competitiveness.

- Key players include Eurofins Scientific, SGS SA, ALS Limited, Pace Analytical Services, Bureau Veritas, Intertek Group plc, Montrose Environmental Group, GEL Laboratories, Battelle Memorial Institute, and Enthalpy Analytical.

Key Developments

- April 2025: Pace Analytical received U.S. Department of Defense accreditation for multiple PFAS analytical methods including ASTM D8421, ASTM D8535, and EPA 8327, strengthening support for environmental remediation and compliance projects.

- February 2025: Perma-Fix Environmental Services expanded its proprietary PFAS treatment technology to support additional contaminated waste streams including wastewater concentrate and industrial leachate applications.

- October 2025: LGC Standards launched new 13C-labelled PFAS reference materials designed for EPA Method 1633 workflows to improve calibration accuracy and analytical data quality for environmental laboratories.

- May 2025: The U.S. Environmental Protection Agency confirmed continued implementation of national drinking water standards for PFOA and PFOS, accelerating long-term demand for advanced PFAS laboratory testing and compliance monitoring services.

Key Procurement Priorities and Buyer Evaluation Criteria

- Firms that are making investments within the market for PFAS testing services are opting for vendors that can offer ultra-trace contamination testing, compliance-based analytical services, and scalable environmental testing infrastructure for water, soil, food, and industrial uses.

- Some aspects related to the procurement process of PFAS test service providers are being influenced by PFAS regulation changes, increased use of EPA 1633 and EPA 537.1 testing techniques, expansion of drinking water monitoring initiatives, and increased demand for advanced analytical instruments in the industrial sector (LC-MS/MS and High-resolution Mass Spectrometry).

- Among several aspects of consideration in the procurement process are the level of analytical sensitivity, the status of laboratory accreditation, turnaround time, contamination controls, multi-matrix testing capabilities, and compliance with environmental and public health regulations.

- Other important factors considered include laboratory network size, non-targeted analysis services, automated sample preparation technology, analytical data quality, and the capability of working with complex applications like wastewater monitoring, remediation programs, industrial process verification, healthcare testing, and consumer product contamination studies.

Why Choose DataM?

- Technological Innovations: Explores advancements in PFAS analytical technologies including LC-MS/MS, high-resolution mass spectrometry (HRMS), combustion ion chromatography (CIC), and non-targeted analysis (NTA), enabling ultra-trace contamination detection, broader analyte coverage, and improved regulatory compliance across drinking water, environmental, industrial, and healthcare applications.

- Product Performance & Market Positioning: Evaluates how different market participants deliver PFAS testing solutions based on analytical sensitivity, turnaround time, contamination-control capability, multi-matrix testing expertise, and regulatory accreditation, highlighting how leading companies differentiate through advanced laboratory infrastructure and scalable analytical services.

- Real-World Evidence: Highlights increasing adoption of PFAS testing across drinking water systems, wastewater treatment plants, semiconductor manufacturing facilities, food packaging, healthcare products, and environmental remediation projects, demonstrating benefits such as improved contamination monitoring, regulatory compliance, public health protection, and industrial risk management.

- Market Updates & Industry Changes: Tracks key developments including laboratory expansions, EPA Method 1633 adoption, non-targeted PFAS screening advancements, accreditation upgrades, and increasing investments in environmental testing infrastructure across North America, Europe, and Asia-Pacific markets.

- Competitive Strategies: Analyzes how leading companies expand through laboratory acquisitions, advanced analytical technology adoption, regulatory-compliance partnerships, automation integration, and expansion of PFAS analyte coverage to address rising global testing demand from environmental and industrial sectors.

- Pricing & Market Access: Explains pricing variations based on detection limits, sample complexity, testing methodology, accreditation requirements, and turnaround time, along with market access through environmental laboratories, industrial testing providers, regulatory agencies, and specialized analytical service companies.

- Market Entry & Expansion: Identifies growth opportunities driven by tightening PFAS regulations, expanding drinking water monitoring programs, rising remediation projects, and increasing industrial compliance requirements, while outlining strategies such as laboratory network expansion, technology differentiation, and advanced analytical capability development to strengthen market presence globally.

Target Audience

- Environmental Testing Laboratories: Commercial, government, and independent laboratories providing PFAS analytical, contamination monitoring, and regulatory compliance testing services.

- Water Utilities & Municipal Authorities: Public water systems, wastewater treatment operators, and municipal agencies implementing PFAS monitoring and drinking water compliance programs.

- Industrial Manufacturers: Chemical, semiconductor, electronics, aerospace, food processing, textile, and industrial manufacturing companies conducting PFAS contamination assessment and process monitoring activities.

- Healthcare & Pharmaceutical Companies: Medical device manufacturers, pharmaceutical companies, and healthcare organizations performing PFAS screening, extractables and leachables testing, and contamination-risk assessments.

- Government & Regulatory Bodies: Environmental protection agencies, public health authorities, defense organizations, and policymakers strengthening PFAS regulations, remediation programs, and environmental monitoring frameworks.

- Investors & Private Equity Firms: Stakeholders monitoring growth opportunities in environmental testing, laboratory infrastructure, analytical instrumentation, water treatment, and contamination remediation markets.

- Analytical Instrumentation & Supply Chain Providers: Companies supplying LC-MS/MS systems, HRMS platforms, laboratory consumables, reference materials, sample preparation products, and environmental analytical software solutions.