PFAS Remediation Market Definition and Overview

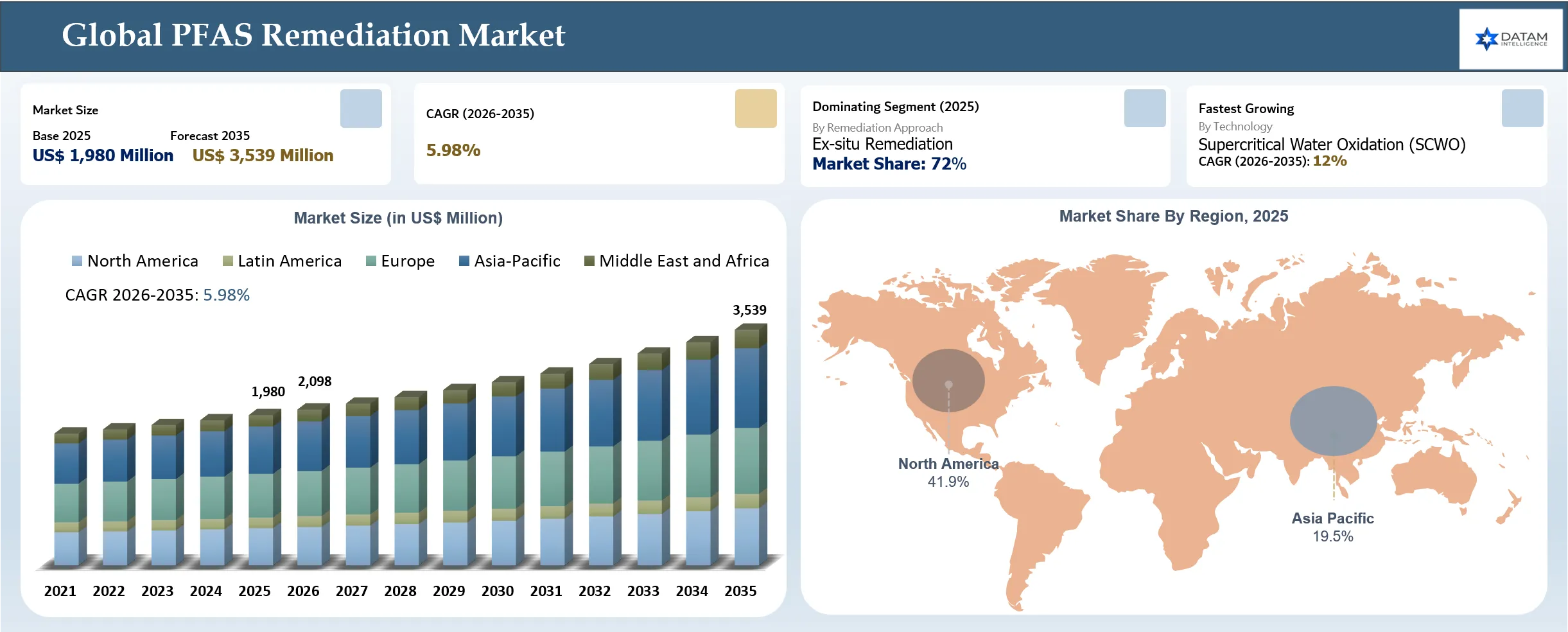

The global PFAS Remediation market reached USD 1,980 million in 2025 and is expected to reach USD 3,539 million by 2035, growing with a CAGR of 5.98% during the forecast period 2026-2035. The market expansion is supported by the rapid rise in PFAS contamination investigations and remediation programs across municipal water supplies, industries, airports, military facilities, and landfills. In 2026, the U.S. Environmental Protection Agency (EPA) provided an additional budget of nearly USD 1 billion in support of state programs on PFAS contamination in drinking water, along with the enforcement of a 4 parts per trillion (ppt) standard for drinking water concerning PFOA and PFOS, which will further stimulate the investments in PFAS treatment equipment. Moreover, the EPA released USD 945 million for PFAS drinking water projects and developed methods that are able to identify 40 different types of PFAS compounds in wastewater, groundwater, surface water, soil, sludge, sediment, landfill leachate, and fish tissue, thereby boosting the demand for innovative remediation solutions. Such companies as Battelle, Cyclopure, Aclarity, Aquagga, and 374Water offer advanced destruction and separation technologies for efficient PFAS remediation and reduction of the total treatment cost. Although the regulation is highly active, the costly remediation, site-specific treatment needs, and the difficulty in destroying various types of PFAS limit the widespread adoption of the technology.

These developments indicate the rapid adoption of PFAS remediation technologies, driven by increasingly stringent policies and increased spending, leading to more frequent deployments of these solutions. In April 2026, the PFAS Treatment Europe Summit article, "the EU Drinking Water Directive, which established legal limits on PFAS beginning January 2026, is helping municipalities and industries procure remediation technologies." Moreover, it mentions that reverse osmosis and nanofiltration technologies will continue to increase at an annual rate of 7.7% until 2031, fueled by growing requirements for groundwater remediation and industrial wastewater treatment.

U.S. EPA's USD 1 Billion PFAS Investment Unlocks Wide-Scale Opportunities Across the Remediation Value Chain

In May 2026, the U.S. Environmental Protection Agency (EPA) allocated nearly USD 1 billion in supplemental funding through state drinking water programs to strengthen PFAS mitigation and compliance infrastructure rather than providing direct grants to remediation technology companies. The largest portion of the funding is directed toward upgrading municipal drinking water treatment facilities through the installation of granular activated carbon (GAC), ion exchange resins, reverse osmosis (RO), and other PFAS treatment technologies, while additional funding supports water infrastructure improvements in small and disadvantaged communities. The investment also covers engineering design, site characterization, treatment system construction, laboratory testing, regulatory monitoring, and long-term compliance activities. As part of the funding rollout, the EPA announced USD 77.3 million for California, USD 33.6 million for New Jersey, USD 15.7 million for seven PFAS treatment projects across Southern California, USD 9.46 million for Kansas, and USD 9.5 million for New Hampshire to accelerate PFAS drinking water treatment and infrastructure modernization.

The funding is expected to create significant procurement opportunities across the PFAS remediation value chain. Engineering and environmental service providers such as Veolia, AECOM, Jacobs, Tetra Tech, WSP Global, Stantec, and TRC Companies are well-positioned to secure contracts for site investigation, remediation design, construction management, and system operation. Treatment equipment and technology manufacturers, including Xylem, Evoqua Water Technologies, Calgon Carbon Corporation, Purolite, Kurita Water Industries, and Pentair, are expected to benefit from increasing demand for advanced PFAS treatment systems and media. PFAS destruction technology developers such as 374Water, Aquagga, Aclarity, and Revive Environmental are likely to gain opportunities through pilot-scale and commercial deployment projects. In addition, environmental laboratories and analytical service providers, including Eurofins Scientific, SGS, Bureau Veritas, and ALS Limited, are expected to experience higher demand for PFAS sampling, analytical testing, compliance monitoring, and environmental reporting as funded projects progress from site assessment through long-term remediation and regulatory verification.

PFAS Remediation Market Key Takeaways

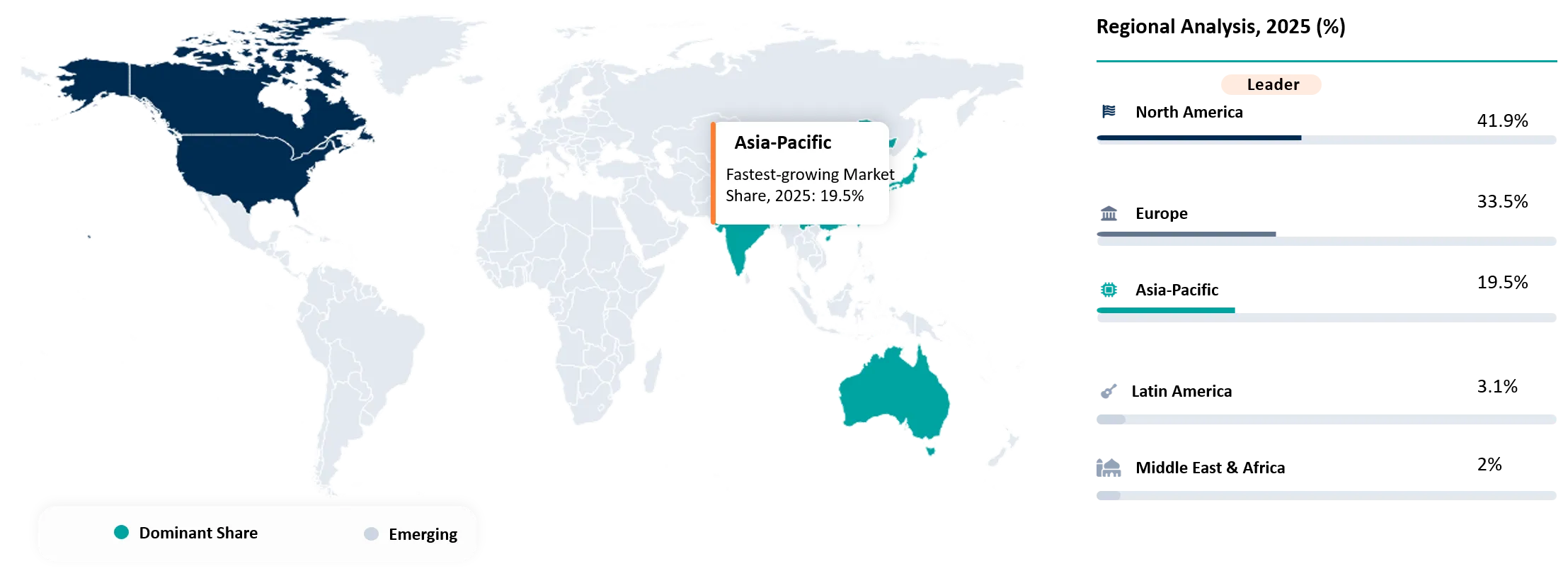

- North America led the global marketplace by commanding a substantial 41.9% of the total market share in 2025. This leading position is sustained by widespread contamination testing alongside aggressive government-led environmental cleanup programs.

- The ex-situ remediation segment established absolute market leadership with a dominant 72% share in 2025. Its commercial maturity and capability to treat contaminated fluids under controlled conditions reinforce its operational preference.

- The U.S. EPA provided an additional budget of nearly USD 1 billion for state programs and USD 945 million for drinking water projects. These massive financial allocations are designed to fast-track the procurement and deployment of specialized treatment infrastructure.

- Reverse osmosis and nanofiltration technologies are projected to increase at a steady annual rate of 7.7% until 2031. This growth is driven by escalating municipal demands for deep groundwater remediation and heavy industrial wastewater purification.

- The EU Drinking Water Directive enforced limits of 0.10 µg/L for 20 combined PFAS and 0.50 µg/L for total PFAS. Effective from January 2026, these strict limits legally compel regional municipalities and industries to rapidly procure remediation technologies.

PFAS Remediation Market Industry Trends and Strategic Insights

- Transition from PFAS removal to irreversible destruction technologies. The industry is shifting from adsorption processes for PFAS treatment and adopting destructive techniques like electrochemical oxidation, plasma oxidation, supercritical water oxidation (SCWO), hydrothermal alkali destruction, and advanced oxidation using UV to permanently cleave carbon-fluorine bonds and produce less secondary waste.

- Integrated “capture-and-destroy” treatment system training is becoming the favored option for deployment. Municipal utility companies and industrial firms are starting to pair granular activated carbon (GAC), ion exchange resins, or membrane filtration with the destruction of PFAS.

- Regulatory frameworks are accelerating technology qualification and performance benchmarking. The environmental agencies have been setting up technology evaluation systems, standard analysis procedures, and annual guidance revisions that facilitate the assessment of efficiency of destruction, byproduct production, and long-term environmental performance.

- Digital monitoring tools and PFAS analysis are becoming strategic differentiators. Highly sophisticated analytical techniques that can detect more than two dozen PFAS compounds in various media such as groundwater, wastewater, sediments, landfill leachate, and biosolids can help plan for remediation and optimize process operations.

- Lifecycle remediation economics are emerging as one of the primary criteria for purchasing. End-users are progressively using total costs of treatment, power consumption, production of residual waste, regeneration needs of media, and destruction effectiveness in evaluating technologies and not simply equipment costs.

PFAS Remediation Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 1,980 Million | |

| 2035 Projected Market Size | USD 3,539 Million | |

| CAGR (2026-2035) | 5.98% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Technology | Granular Activated Carbon (GAC), Ion Exchange Resins, Reverse Osmosis (RO), Nanofiltration (NF), Foam Fractionation, Electrochemical Oxidation, Plasma Treatment, Supercritical Water Oxidation (SCWO), Thermal Treatment, Other Emerging Destruction Technologies | |

| By Contaminated Media | Groundwater, Surface Water, Drinking Water, Industrial Wastewater, Municipal Wastewater, Soil, Landfill Leachate, Others | |

| By Remediation Approach | In-situ Remediation, Ex-situ Remediation, Others | |

| By PFAS Type Treated | Long-Chain PFAS, Short-Chain PFAS, PFAS Mixtures | |

| By End User | Municipal Water Utilities, Defense & Military Installations, Airports, Oil & Gas, Chemical & Petrochemical, Semiconductor & Electronics Manufacturing, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

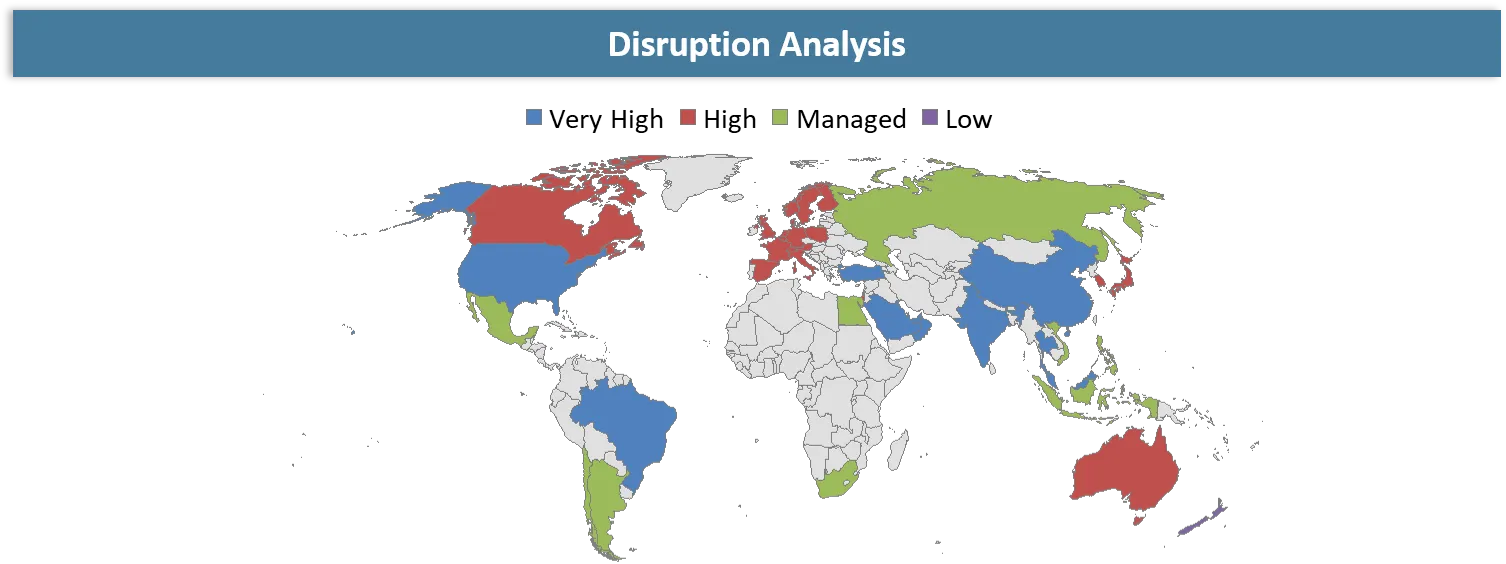

PFAS Remediation Market Disruption Analysis

Commercialization of Modular and Mobile PFAS Remediation Systems Transforming On-Site Treatment Strategies

The PFAS remediation market is undergoing a significant transformation with the commercialization of the modular and mobile treatment systems that enable rapid deployment at contaminated sites without requiring permanent treatment infrastructure. While most traditional remediation efforts take longer to implement through the design, engineering, permitting, and construction process, modular and skid-mounted systems can be brought into service much quicker for groundwater, landfill leachate, industrial wastewater, and emergency contamination incidents. As a result, procurement processes are being impacted as municipalities, industries, airports, military bases, and environmental companies seek out modular systems that are faster to install, easier to expand, and less costly to operate than conventional treatment facilities.

Equipment makers are therefore adapting to the needs of these changing conditions by developing standardized and portable treatment systems that utilize adsorption and membrane filtering systems as well as new methods of PFAS destruction. According to the U.S. EPA report "Technical Overview of PFAS National Primary Drinking Water Regulation (NPDWR)," that the agency expects an estimated cost of about $1.548 billion for the implementation each year, involving 66,000 public water systems in monitoring of PFAS and between 4,100 to 6,700 water systems needing to take remediation steps through use of technology such as granular activated carbon, ion exchange, and reverse osmosis.

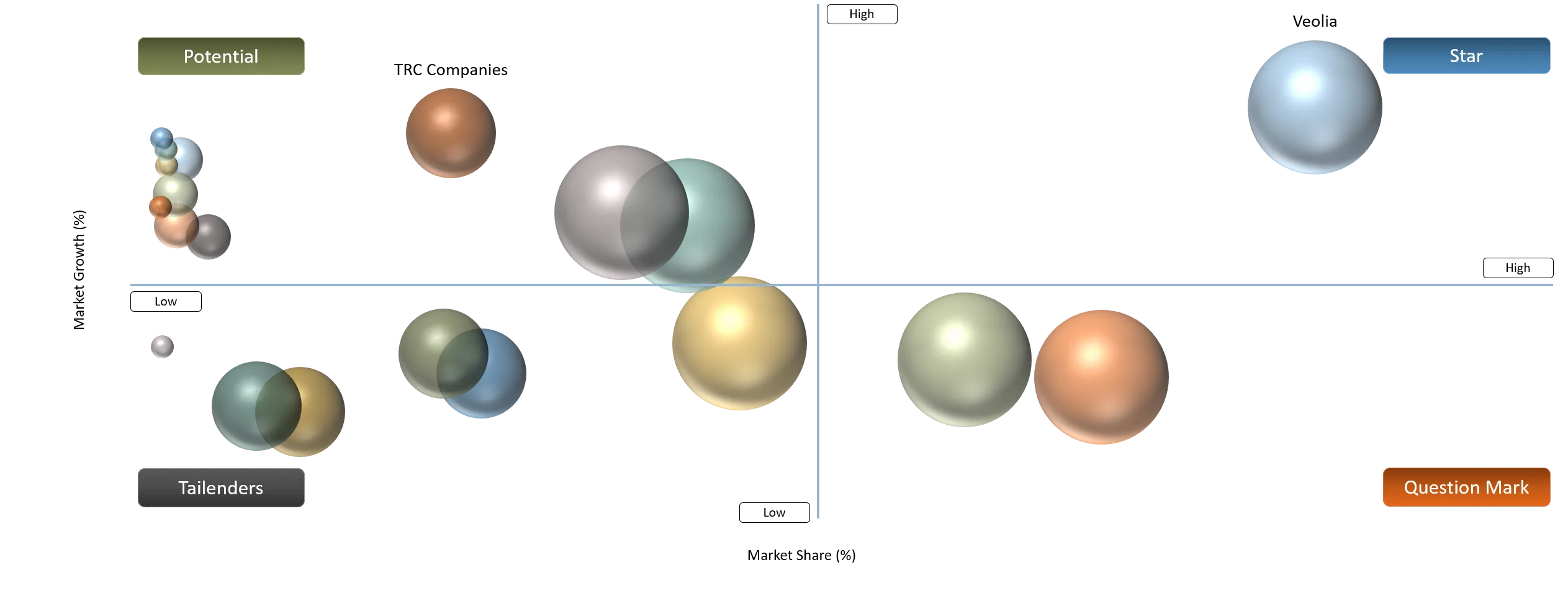

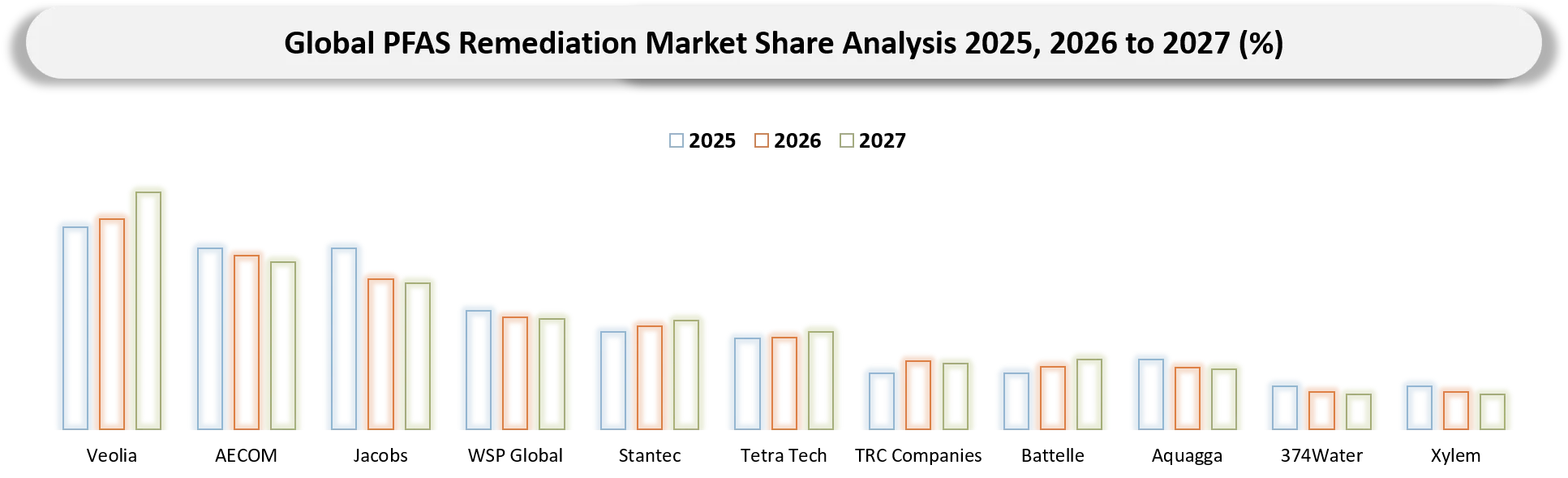

PFAS Remediation Market BCG Matrix: Company Evaluation

Stars include Veolia, AECOM, and Tetra Tech, due to their broad international environmental remediation experience, engineering strengths, and demonstrated proficiency in undertaking major PFAS remediation projects at municipalities, industries, military bases, and government agencies. Question Marks include Jacobs, WSP Global, and Stantec, which have quickly gained PFAS remediation consulting, engineering, and environmental restoration capacities via technology partnerships and increased project participation.

Potential categories include TRC Companies, Battelle, and Xylem owing to their rising investment in PFAS treatment and destruction technologies. Battelle keeps on developing new PFAS destruction technologies, while Xylem is working on new water treatment technologies, and TRC Companies keeps improving its remediation engineering portfolio due to PFAS cleanup projects. Tailenders are composed of Aquagga, 374Water, and Calgon Carbon Corporation. Although Aquagga and 374Water have revolutionary destruction technologies that are commercializable, these are still at the early stages of their worldwide implementation.

PFAS Remediation Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

The expansion of legally enforceable PFAS cleanup obligations is transforming remediation from a voluntary environmental initiative into a mandatory compliance requirement. | 2.4% | Very High | Municipal drinking water treatment, groundwater remediation, industrial wastewater treatment, contaminated site restoration | Expands long-term remediation contracts and accelerates deployment of advanced PFAS treatment and destruction technologies across regulated sectors. |

Progressive tightening of drinking water, groundwater, and contaminated land standards is compelling asset owners to deploy advanced PFAS remediation technologies to meet regulatory thresholds. | 1.9% | High | Public water utilities, industrial manufacturing, landfill leachate treatment, environmental compliance projects | Drives replacement of conventional treatment systems with high-efficiency adsorption, membrane filtration, and destruction technologies to achieve regulatory compliance. |

Increasing designation of PFAS-contaminated sites under national and regional environmental programs is generating a sustained pipeline. | 1.6% | Medium to High | Site investigation, groundwater cleanup, soil remediation, military bases, airports, chemical manufacturing facilities | Strengthens recurring demand for engineering services, environmental monitoring, pilot testing, and full-scale remediation projects while expanding the addressable market. |

Regulatory emphasis on permanent contaminant reduction is accelerating the adoption of high-performance remediation technologies. | 1.4% | High | Electrochemical oxidation, plasma treatment, supercritical water oxidation (SCWO), integrated capture-and-destroy systems | Accelerates commercialization of next-generation PFAS destruction technologies and shifts procurement toward permanent contaminant elimination instead of contaminant transfer. |

The expansion of legally enforceable PFAS cleanup obligations is transforming remediation from a voluntary environmental initiative into a mandatory compliance requirement

The rapid expansion of legally enforceable PFAS clean-up obligations is transforming the paradigm of environmental remediation from an elective action to a mandatory process, thus accelerating the development of PFAS remediation and destruction technology. Drinking water quality, groundwater quality, and contaminated sites are being regulated more and more strongly by governments, thus obliging municipalities, industries, airports, military bases, and environmental contractors to implement PFAS remediation systems. This trend of strict regulatory obligations is accelerating investments in GAC, ion exchange, and membrane filtration systems for PFAS remediation, as well as novel PFAS destruction technology.

These legally enforceable limits are accelerating the investment in state-of-the-art PFAS treatment technology and infrastructure improvements in the municipal water supply system. In January 2026, as stated by the European Commission, the amended EU Drinking Water Directive brought about mandatory restrictions on the combined total of 20 PFAS at 0.10 µg/L and total PFAS at 0.50 µg/L in drinking water.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Advanced PFAS destruction technologies remain capital-intensive and have limited full-scale commercial deployment. | 2.2% | Capital investment and technology commercialization | Supercritical Water Oxidation (SCWO), electrochemical oxidation, plasma treatment, hydrothermal destruction | Delays large-scale commercialization, limiting adoption to pilot projects, government-funded programs, and high-priority remediation sites. |

The chemical stability of PFAS compounds makes complete destruction technically challenging, often requiring high energy input and specialized treatment conditions. | 1.7% | Treatment efficiency and operational complexity | High-concentration industrial wastewater, landfill leachate, mixed PFAS contamination | Increases operating costs and restricts widespread deployment of permanent PFAS destruction technologies, encouraging continued reliance on separation methods. |

Conventional technologies such as granular activated carbon (GAC) remove PFAS but generate secondary waste streams that require additional treatment or disposal, increasing lifecycle remediation costs. | 1.5% | Lifecycle cost and waste management | Municipal drinking water treatment, groundwater remediation, industrial water treatment | Raises total cost of ownership through media replacement, regeneration, concentrate management, and disposal, reducing project cost-effectiveness. |

Uncertainty regarding the long-term performance and regulatory acceptance of emerging PFAS destruction technologies delays investment decisions and large-scale commercialization. | 1.3% | Technology validation and regulatory approval | Commercial-scale PFAS destruction projects, municipal infrastructure upgrades | Slows private-sector investment, extends technology qualification timelines, and delays procurement of next-generation remediation systems until long-term performance is validated. |

Advanced PFAS destruction technologies remain capital-intensive and have limited full-scale commercial deployment

Commercialization of the advanced PFAS destruction technology remains hindered due to the high cost involved, complex technology integration, and lack of experience in large-scale operations. In comparison to conventional treatment technologies like granular activated carbon (GAC), ion exchange, and reverse osmosis, destructive technologies that include SCWO, electrochemical oxidation, plasma treatment, hydrothermal alkaline treatment, and mechanochemical destruction entail specialized equipment, high temperature/high pressure, advanced control systems, and considerable energy input. This makes the cost higher and restricts the application mainly to pilot testing, government-funded demonstrations, and high-profile remediation projects only.

Although these technological improvements have been made, the commercialization of advanced PFAS destruction technologies still faces challenges from high initial cost, strict permit conditions, and a lack of large-scale applications in the end-user market. In September 2025, Revive Environmental, the company's PFAS Annihilator® Supercritical Water Oxidation (SCWO) technology, was awarded the 2025 WEF Innovative Technology Award with more than 99.99% PFAS destruction efficiency, which is the first commercial-scale PFAS destruction SCWO technology in North America.

PFAS Remediation Market Segment Analysis

The global PFAS Remediation market is segmented based on technology, contaminated media, remediation approach, PFAS type treated, end user, and region.

Ex-situ Remediation Dominates the PFAS Remediation Market Due to Proven Commercial Deployment and Regulatory Acceptance

The Ex-Situ Remediation segment continues to dominate the PFAS remediation market, with a market share of 72% in 2025, owing to its proven efficiency, regulation acceptance, and ability to work well with available PFAS removal technology, such as granulated activated carbon (GAC), ion exchange resins, reverse osmosis (RO), nanofiltration (NF), and destruction technology. The application of ex-situ remediation provides the chance of pumping out and treating contaminated groundwater, drinking water, industrial wastewater, and landfill leachate under controllable operational conditions, thus ensuring efficient treatment of contaminants. Consequently, there will be a preference for ex-situ treatment systems in large-scale PFAS remediation operations.

During 2025–2026, regulatory developments further reinforced the dominance of ex-situ remediation. In addition, the Australian Government released the National PFAS Environmental Management Plan (NEMP) Version 3.0 in 2025, strengthening national guidance for the investigation and remediation of PFAS-contaminated sites. These regulatory initiatives are accelerating investment in centralized treatment infrastructure where ex-situ technologies provide the most commercially mature and operationally reliable remediation solution, reinforcing the segment's leadership in the global PFAS remediation market.

PFAS Remediation Market Geographical Penetration

North America Leadership Driven by Stringent PFAS Regulations and Large-Scale Remediation Investments

The North America region is dominating the global PFAS Remediation market, contributing to 41.9% of the global market share in 2025, owing to stringent regulations related to the environment, widespread contamination testing programs, and increasing investment in sophisticated treatment techniques. A high number of contaminated sites due to industrial activities, use of firefighting foams, and manufacturing activities have boosted the demand for treatment processes like activated carbon treatment, ion exchange, membrane filtration, and destruction methods. The regulatory efforts taken by the government organizations through stringent standards for drinking water and cleanup have boosted PFAS remediation initiatives in the region.

This development highlights the increased adoption of advanced PFAS destruction solutions across North America, as more communities have been investing in large-scale treatment facilities to deal with PFAS-contaminated waste streams and also comply with new regulations. In June 2026, 374Water Inc., a U.S.-based Environmental Services / Cleantech Company, announced an expanded partnership with the City of Orlando, Florida, USA to develop a full-scale PFAS waste destruction and manufacturing facility at Iron Bridge Regional Water Reclamation Facility. In the expanded facility, 88,000 gallons of on-site tank storage will be added, the airSCWO™ system will be upgraded, and a 35,000+ square-foot manufacturing and assembly facility will be created. The projected first-year annual revenues of the WDS hub are expected to be about US$3-5 million.

U.S. PFAS Remediation Market Trends

The U.S. has a dominant position in the North American PFAS Remediation Market due to the country's high levels of contamination, good regulation, and investments in technological advancements. By the thousands of contaminated sites from the military, air force bases, industrial manufacturing, firefighting foams, and the use of municipal water systems, the need for PFAS destruction and removal services has increased considerably. In 2025, the US is expected to be a major shareholder in the North American PFAS Remediation market due to federal financial support, stringent water rules, and adoption of technologies such as GAC, ion exchange, reverse osmosis, and destruction of PFAS.

This advancement highlights the growing adoption of innovative PFAS destruction technology in the U.S. because both industries and municipal authorities want to use viable options to tackle the problem of PFAS contamination. In December 2025, Claros Technologies, Inc., which is a U.S.-based company dealing in environmental technology/PFAS remediation, succeeded in the commercial-scale validation of its ClarosTechUV™ PFAS destruction technology. It successfully destroyed more than 99.99% of targeted PFAS chemicals in long, short, and ultra-short chain PFAS. This has been done in cooperation with some industries, and it has involved the treatment of over 170,000 gallons of PFAS-laden industrial process water.

Canada PFAS Remediation Market Outlook

Canada is emerging as the fastest-growing country in the North American PFAS Remediation market, owing to the growing concern over PFAS contamination, an increase in environmental monitoring initiatives, and investments being made in remediation infrastructures of water and soil. There has been an increasing need for PFAS remediation products across municipal water plants, industries, airports, and firefighting training grounds owing to awareness regarding the long-term effects of contaminants in the environment. There has been a rise in the uptake of advanced technologies such as activated carbon adsorption, ion exchange, membrane filtration, and novel destruction technologies.

This development strengthens the process of PFAS remediation in Canada by increasing the speed of the detection of contamination and allowing site characterization before implementing the process of treatment. In September 2025, Fredsense Technologies Inc., a Canada-based Environmental Technology / Water Monitoring Company, launched the Fredsense PFAS Analyzer, which is the first field-based PFAS detection system that allows for laboratory-quality results on-site in a single day.

PFAS Remediation Market Competitive Landscape

- The Global PFAS Remediation market can be characterized by three major types of players in the market segment. First, there are environmental engineering and consultancy companies; secondly, companies that deal with water treatment technologies; thirdly, there are companies that develop PFAS destruction technologies. Among the environmental service providers are companies like Veolia, AECOM, Jacobs, WSP Global, Stantec, and Tetra Tech, which enhance their market presence by offering comprehensive remediation, regulatory compliance, assessment, and water treatment solutions. The technology companies like Xylem and Calgon Carbon Corporation offer advanced solutions for PFAS removal through activated carbon adsorption, filtration, and water treatment systems. The innovation-based companies include Battelle, Aquagga, and 374Water, which deal with new PFAS destruction technologies such as electrochemical treatment, hydrothermal oxidation, and supercritical water oxidation.

- Key players include Veolia, AECOM, Jacobs, WSP Global, Stantec, Tetra Tech, TRC Companies, Battelle, Aquagga, 374Water, Xylem, and Calgon Carbon Corporation.

Key Developments

- February 2025: Parsons Corporation, a United States-based Engineering, Environmental, and Infrastructure Solutions Company, acquired TRS Group, Inc., a United States-based Environmental Remediation Company specializing in in-situ groundwater remediation technologies, including PFAS treatment solutions, to strengthen its capabilities in contaminated site assessment and remediation services.

- August 2025: Chemours Company, DuPont de Nemours, Inc., and Corteva, Inc., United States-based chemical and specialty materials companies, reached a comprehensive agreement with the State of New Jersey to resolve environmental claims, including PFAS-related liabilities, reinforcing their commitment to funding environmental investigation, remediation, and restoration activities at contaminated sites across the state.

- June 2026: EnSafe Inc., a United States-based environmental engineering and consulting company, acquired Porewater Solutions Inc., a Canada-based hydrogeology and environmental consulting company, to expand its expertise in contaminated site investigation, groundwater assessment, and PFAS-related environmental remediation services across North America.

- June 2026: Reworld, a United States-based sustainable waste solutions and environmental services company, launched ReAssure™, a full-scale PFAS destruction service designed to safely manage and destroy PFAS-containing materials, expanding commercial treatment capacity for contaminated wastes generated from industrial, municipal, and environmental cleanup activities.

- March 2026: Veolia Environnement S.A., a France-based environmental services company, agreed to acquire Enviropacific Services Limited, an Australia-based environmental remediation and contaminated land management company, for an enterprise value of AUD 220 million to strengthen its capabilities in PFAS treatment, soil remediation, and hazardous waste management across Australia.

Key Procurement Priorities and Buyer Evaluation Criteria

- Organizations investing in the Global PFAS Remediation Market increasingly select suppliers based on their ability to deliver proven PFAS removal and destruction technologies that achieve stringent regulatory compliance, high contaminant removal efficiency, and scalable treatment performance for water, soil, and industrial waste streams.

- Procurement decisions are increasingly influenced by evolving PFAS regulations, lower drinking water limits, growing adoption of destructive treatment technologies, sustainability objectives, and the supplier's capability to manage both short-chain and long-chain PFAS while minimizing secondary waste generation and lifecycle treatment costs.

- Buyers evaluate vendors based on PFAS removal efficiency, destruction rates, regulatory compliance, treatment capacity, technology maturity (TRL), operational reliability, energy and chemical consumption, waste management requirements, and total cost of ownership when selecting remediation solutions.

Why Choose DataM?

- Technological Innovations: Explores advancements in PFAS remediation technologies, including granular activated carbon (GAC), ion exchange resins, reverse osmosis, nanofiltration, electrochemical oxidation, plasma treatment, supercritical water oxidation (SCWO), and hydrothermal destruction, enabling higher PFAS removal efficiencies and permanent destruction of both short-chain and long-chain PFAS compounds.

- Technology Performance & Market Positioning: Evaluates how technology providers differentiate based on PFAS removal efficiency, destruction effectiveness, treatment capacity, energy consumption, operational costs, secondary waste generation, and regulatory compliance, highlighting competitive advantages across municipal, industrial, landfill leachate, and defense remediation applications.

- Real-World Evidence: Highlights commercial deployment of PFAS remediation solutions across drinking water utilities, industrial wastewater treatment facilities, military bases, airports, chemical manufacturing sites, and contaminated groundwater projects, demonstrating measurable improvements in regulatory compliance, contaminant removal, and long-term environmental sustainability.

- Market Updates & Industry Changes: Tracks major industry developments, including evolving PFAS regulations, drinking water standards, remediation funding programs, commercialization of PFAS destruction technologies, strategic partnerships, facility expansions, and government-led cleanup initiatives across North America, Europe, and Asia-Pacific.

- Competitive Strategies: Analyzes how leading companies strengthen their market positions through technology innovation, acquisitions, engineering and remediation contracts, strategic collaborations, pilot-scale demonstrations, and commercialization of next-generation PFAS destruction solutions to address increasing global remediation demand.

- Pricing & Market Access: Explains pricing variations based on treatment technology, contaminant concentration, project scale, media replacement requirements, operational complexity, and lifecycle costs, while assessing market access through environmental engineering firms, water treatment solution providers, technology licensors, EPC contractors, and government procurement programs.

- Market Entry & Expansion: Identifies growth opportunities driven by tightening environmental regulations, increasing PFAS contamination assessments, rising municipal and industrial treatment investments, defense and airport remediation projects, and commercialization of destructive treatment technologies, while outlining strategies such as regional expansion, technology partnerships, regulatory certifications, and integrated remediation service offerings.

Target Audience

- Municipal Water Utilities and Drinking Water Authorities

- Industrial Water and Wastewater Treatment Companies

- Environmental Remediation Service Providers

- Environmental Engineering, Procurement & Construction (EPC) Firms

- Chemical and Petrochemical Manufacturers

- Oil & Gas and Energy Companies

- Semiconductor and Electronics Manufacturing Companies