PFAS-free Coatings Market Size and Overview

The global PFAS-free coatings market reached USD 1,587 million in 2025 and is expected to reach USD 2,788 million by 2035, growing with a CAGR of 5.8% during the forecast period 2026-2035. The market is experiencing steady growth as regulatory authorities across North America and Europe accelerate restrictions on per- and polyfluoroalkyl substances (PFAS), prompting manufacturers to transition toward fluorine-free coating technologies. Increasing adoption of PFAS-free formulations in food-contact packaging, cookware, construction materials, automotive components, electronics, and industrial equipment is strengthening market demand as end users seek compliance with evolving environmental standards while maintaining high-performance surface properties. Continuous advancements in silicone, ceramic, epoxy, polyurethane-, and bio-based coating chemistries are enabling manufacturers to deliver corrosion resistance, chemical durability, and barrier performance without relying on PFAS compounds. Major coatings producers are expanding research and commercialization of fluorine-free technologies to align with sustainability commitments and anticipated regulatory requirements. However, performance validation for highly demanding applications, reformulation costs, and qualification timelines continue to moderate the pace of market adoption.

The updated ECHA PFAS restriction proposal would enhance the regulatory pressure on coating producers, forcing them to invest in fluorine-free coatings and eco-friendly technology. In August 2025, European Coatings reported that the European Chemicals Agency (ECHA) proposed the revision to restrict the use of per- and polyfluoroalkyl substances (PFAS) through the EU REACH framework based on a thorough evaluation of over 5,600 stakeholder comments collected in the consultation process. The revised proposal favors the EU-wide PFAS restriction that will promote the use of PFAS-free coatings.

PFAS-free coatings Market Key Takeaways

- Europe dominated the global landscape by capturing a 36.8% market share in 2025, a position heavily supported by strict regional chemical restriction frameworks.

- Stringent global regulations serve as the primary market driver with a 40% positive impact on growth, forcing rapid adoption across sectors like food packaging and automotive components.

- Growing commercial interest in eco-friendly surface technologies contributes a substantial 30% positive impact to market expansion, accelerating corporate shifts toward bio-based and silicone platforms.

- Continuous advancements in alternative fluorine-free coating chemistries provide a 25% positive impact on market development, successfully improving properties like corrosion and abrasion resistance.

- Functional performance limitations compared to traditional fluoropolymers exert an 18% negative drag on market growth, temporarily restricting substitution in highly demanding technical use cases.

PFAS-free Coatings Market Industry Trends and Strategic Insight

- Europe dominated the global landscape by capturing a 36.8% market share in 2025, a position heavily supported by strict regional chemical restriction frameworks.

- Stringent global regulations serve as the primary market driver with a 40% positive impact on growth, forcing rapid adoption across sectors like food packaging and automotive components.

- Growing commercial interest in eco-friendly surface technologies contributes a substantial 30% positive impact to market expansion, accelerating corporate shifts toward bio-based and silicone platforms.

- Continuous advancements in alternative fluorine-free coating chemistries provide a 25% positive impact on market development, successfully improving properties like corrosion and abrasion resistance.

- Functional performance limitations compared to traditional fluoropolymers exert an 18% negative drag on market growth, temporarily restricting substitution in highly demanding technical use cases.

PFAS-free coatings Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 1,587 Million | |

| 2035 Projected Market Size | USD 2,788 Million | |

| CAGR (2026-2035) | 5.8% | |

| Largest Market | Europe | |

| Fastest Growing Market | Asia-Pacific | |

| By Coating Type | Silicone-Based, Wax-Based, Bio-Based, Others | |

| By Substrate | Textile, Paper & Cardboard, Metal, Concrete & Masonry, Others | |

| By End User | Industrial Manufacturing, Automotive & Transportation, Building & Construction, Packaging, Electronics & Electrical, Aerospace & Defense, Healthcare, Consumer Goods, Textile Industry, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

PFAS-free coatings Market Disruption Analysis

Shift Toward Fluorine-Free Material Platforms Reshaping the Coatings Industry

There is structural disruption in the PFAS-free coatings market, due to the shift from fluoropolymer coating systems to silicone-, polyurethane-, epoxy-, acrylic-, polysiloxane-, and ceramic-based coating systems that could offer the same level of protection from corrosion, weathering, abrasion, and chemical degradation without using PFAS. The development of such products, replacement of materials used, and qualification process has been greatly accelerated due to the development of OECD's 2025-2026 PFAS program, which published additional technical reports about fluoropolymers and their PFAS-free analogs and continues to expand the number of recommendations for industrial substitution of PFAS with other substances. The other important change in the industry caused by the growing trend of substituting fluoropolymers with PFAS-free alternatives is an increased investment in the validation of coatings in specific applications.

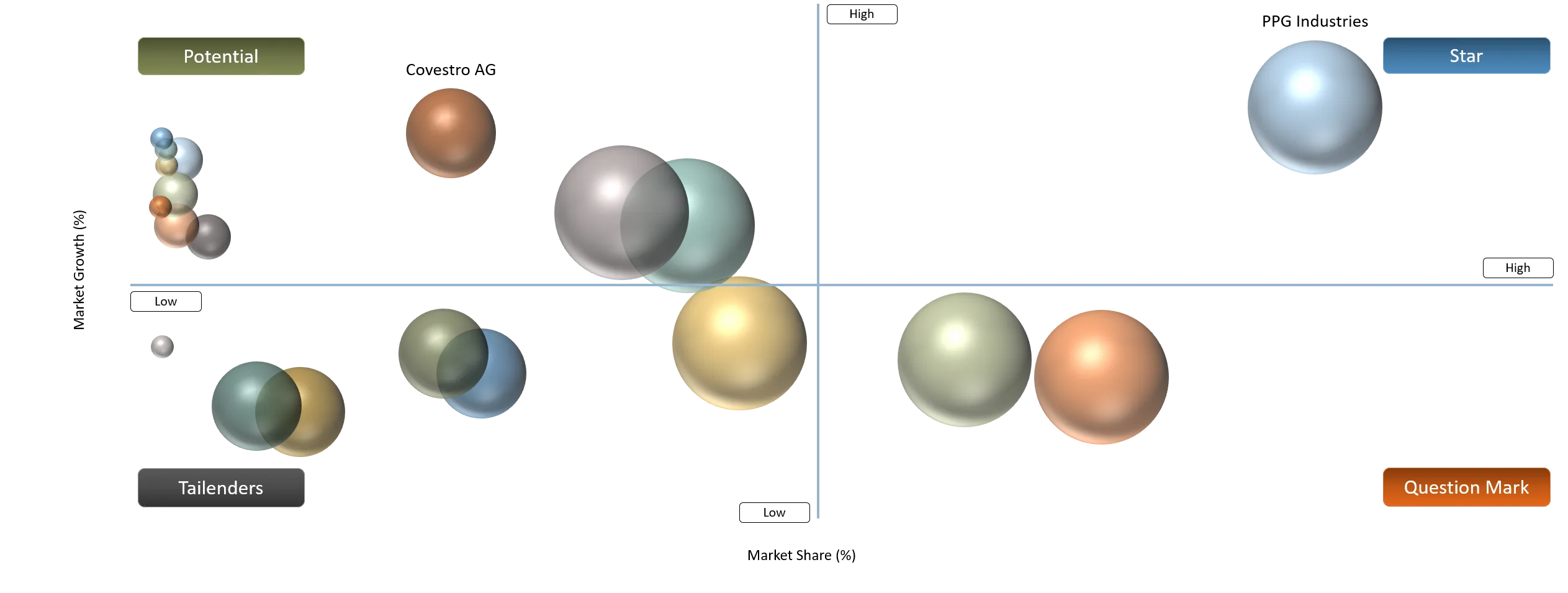

PFAS-free Coatings Market BCG Matrix: Company Evaluation

Stars include PPG Industries, AkzoNobel, Sherwin-Williams, and BASF Coatings GmbH because of their extensive global coatings portfolios, strong R&D capabilities, and active commercialization of PFAS-free and fluorine-free coating technologies across industrial, packaging, automotive, and architectural applications. Question Marks include Nippon Paint Holdings, Kansai Paint Co., Ltd., Jotun A/S, and Berger Paints India Ltd. as they are expanding sustainable and fluorine-free coating portfolios while strengthening their presence in high-growth regional markets.

The Potential category includes Covestro AG, Allnex GmbH, Plasmalex Group, and Plasmatreat GmbH, which provide enabling technologies such as coating resins, specialty polymers, and plasma-based surface treatment solutions supporting the development of PFAS-free coatings. Tailenders include Sichem S.A. and Fraunhofer IFAM, whose involvement is primarily concentrated in specialized non-stick coatings, plasma-assisted coating technologies, and technology transfer activities.

PFAS-free Coatings Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Stringent Global Regulations Accelerating the Transition to PFAS-free Coatings across multiple end-use industries. | 40% | High concentration | Food-contact packaging, cookware, textiles, industrial coatings, electronics, automotive components, and consumer products | Accelerates replacement of PFAS-based coating systems, increases demand for compliant fluorine-free formulations, and creates competitive advantage for companies investing in regulatory-ready coating technologies |

Rising Demand for Sustainable and Safer Surface Technologies. | 30% | Strong demand | Packaging materials, consumer goods, architectural coatings, industrial equipment, and household applications | Drives investment in bio-based, silicone-based, ceramic, and water-based coating solutions while enabling manufacturers to differentiate through sustainability performance |

Continuous Advancements in Fluorine-Free Coating technologies is improving corrosion resistance, abrasion resistance, chemical durability, and barrier performance. | 25% | Concentrated in high-performance industries | Protective coatings, automotive parts, aerospace components, electronic devices, machinery, and specialty industrial applications | Reduces performance limitations of PFAS alternatives, expands commercialization opportunities, and supports adoption of next-generation coating chemistries |

Increasing Demand from Automotive and Industrial Manufacturing to meet customer sustainability targets while maintaining corrosion protection, weatherability, and mechanical durability. | 20% | High demand | Automotive coatings, machinery, renewable energy equipment, transportation components, and industrial infrastructure | Encourages OEM-driven material substitution, strengthens supplier partnerships, and accelerates integration of PFAS-free coatings into industrial supply chains |

Stringent Global Regulations Accelerating the Transition to PFAS-free Coatings across multiple end-use industries

The PFAS-free coatings market is being reshaped by increasingly stringent regulations that have been formulated regarding the use of intentionally added PFAS in various industrial and consumer goods. Such regulation is pressuring coating producers to switch to alternative formulations that do not contain fluoropolymers, but fluorine-free ones instead in packaging, cookware, textiles, construction, automotive, and industrial use applications. Under Minnesota's Amara's Law, which came into effect on January 1, 2025, the use of intentionally added PFAS in 11 categories of consumer products was banned.

The increased regulatory restrictions on the application of PFAS chemicals in major markets, there is a push for coating product manufacturers to come up with PFAS-free coatings. In January 2026, according to TÜV SÜD, Canada has issued new regulations on Prohibition of Certain Toxic Substances Regulations, which involve tougher control of certain toxic substances, among them, PFAS substances such as PFOS, PFOA, and long-chain perfluorocarboxylic acids (LC-PFCAs). The updated regulation that will come into effect on June 30, 2026 will restrict further the use of PFAS substances in products and industrial processes due to reduced exemptions.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Higher Formulation Costs and Complex Development Requirements for PFAS-free Coatings to achieve comparable properties to fluoropolymer-based coatings. | 20% | R&D investment, raw material costs, product commercialization timelines | Food packaging coatings, automotive coatings, electronics coatings, industrial protective coatings | Increases development costs and delays large-scale adoption; favors established coating manufacturers with strong formulation expertise and testing capabilities |

Performance Gap Compared with Conventional PFAS-based Coatings in High-demand Applications. | 18% | Functional performance, durability, chemical resistance, long-term reliability | High-performance textiles, aerospace components, semiconductor/electronics surfaces, automotive applications | Limits replacement of fluoropolymer coatings in critical applications; requires continuous innovation in hybrid and advanced coating technologies |

Limited Availability of High-performance PFAS-free Raw Materials and Supply Chain Constraints. | 15% | Manufacturing complexity, process optimization, scalability | Sustainable packaging, textile finishing, industrial coatings, construction protection coatings | Creates supply uncertainty and increases procurement costs; encourages manufacturers to develop diversified supplier networks and alternative formulations |

Technical Challenges in Achieving Multi-functional Coating Performance often requires hybrid formulations and additional processing steps, increasing complexity for coating manufacturers. | 15% |

Manufacturing complexity, process optimization, scalability | Anti-stain coatings, oil/water-resistant coatings, anti-corrosion coatings, release coatings | Increases production complexity and quality-control requirements; may slow commercialization and adoption among small and medium-sized coating producers |

Higher Formulation Costs and Complex Development Requirements for PFAS-free Coatings to achieve comparable properties to fluoropolymer-based coatings

One of the major challenges limiting the widespread adoption of PFAS-free coatings is the high cost of formulation involved in developing coating technologies that are comparable in their properties to conventional fluoropolymer coatings. During 2025-2026, coating developers have been witnessing an increase in research and development costs due to the development of alternative chemistries, including silicone coatings, polyurethane coatings, ceramic coatings, and bio-based coatings. This is attributed to the need for advanced and costly ingredients used in their formulations.

The technical challenge of producing equivalent coatings that can match the excellent performance of fluoropolymer coating without PFAS is difficult for manufacturers. For instance, in April 2026, according to PatSnap, the shift to PFAS-free coating technology poses significant technical difficulties for manufacturers since they have to produce alternatives to fluoropolymer coating. This article indicates that PFAS-free coating technologies, which include silicone-based, polyurethane-based, sol-gel, and hybrid coating technologies, need to meet the same performance criteria, such as water resistance, oil resistance, chemical resistance, and low friction among others.

PFAS-free coatings Market Segment Analysis

The global PFAS-free coatings market is segmented based on coating type, substrate, end user, and region.

Silicone-Based Coatings Leading Market Adoption Due to High Performance and Broad Application Compatibility

The silicone-based coatings segment dominates the PFAS-free coatings market, with the market share of 40% in 2025, by coating type due to its ability to offer low surface energy, water resistance, chemical resistance, heat resistance, and durability without using any fluorinated chemicals. Increasing efforts towards the removal of PFAS chemicals from industrial applications and consumer goods during 2025-2026 have led to the rising popularity of the use of silicone coatings in various applications, including those in which fluoropolymers were widely used before.

Manufacturers across multiple industries increasingly shifted toward silicone elastomer and silicone resin coating technologies as PFAS-free solutions for achieving anti-fouling, anti-fingerprint, abrasion resistance, and easy-clean properties. The demand was particularly strong in automotive displays, consumer electronics, and high-performance textiles, where companies sought sustainable coatings that could maintain performance requirements while complying with evolving PFAS restrictions in North America and Europe.

PFAS-free coatings Market Geographical Penetration

Stringent PFAS Regulations and Sustainable Coating Transition Driving Market Leadership in Europe

The Europe region dominates the PFAS-free coatings market, supported by strong regulatory initiatives, rapid adoption of sustainable coating technologies, and increasing demand for environmentally compliant alternatives across industrial and consumer applications. The region accounted for 36.8% of the global PFAS-free coatings market share in 2025, driven by strict restrictions on per- and polyfluoroalkyl substances (PFAS), growing sustainability commitments from manufacturers, and accelerated replacement of fluorinated coatings in sectors such as textiles, automotive, electronics, packaging, and industrial equipment.

Innovations assist the manufacturers in fulfilling the changing regulatory standards as well as retaining the toughness and performance levels of conventional fluoropolymer-based coating systems. In April 2026, Henkel, a Germany-based has launched its new range of PFAS-free anti-fingerprint coatings for automotive displays, consisting of products such as Loctite AF 8810 and Loctite AF 8812, which are free from PFAS and fluorine-containing compounds. The coatings are developed using silicon-based low surface energy technology that ensures characteristics like optical clarity, low coefficient of friction, toughness, and cleanliness. Loctite AF 8812 demonstrated the toughness level after 5,000 abrasions and can be used for glass display with a 9H hardness rating.

Germany PFAS-free coatings Market Trends

Germany dominates the European PFAS-free coatings market, supported by its strong specialty chemicals industry, advanced automotive manufacturing base, and early adoption of sustainable material regulations. The country’s leadership is driven by high demand for PFAS-free coatings from key industries such as automotive, industrial machinery, electronics, textiles, and packaging, where manufacturers are actively replacing fluorinated coatings with silicone-based, bio-based, and other non-fluorinated alternatives during 2025–2026.

The commercialization of PFAS-free low-pressure plasma coating technologies highlights Germany’s growing innovation in sustainable surface treatment solutions. In May 2026, Plasmatreat GmbH, a Germany-based surface treatment technology company, in collaboration with Fraunhofer Institute for Manufacturing Technology and Advanced Materials IFAM, scaled up PFAS-free low-pressure plasma coating technologies for industrial applications. The collaboration focuses on advancing fluorine-free coating solutions, including PLASLON® and UltraPLAS® technologies, which provide non-stick and functional surface properties without the use of PFAS chemicals.

France PFAS-free coatings Market Outlook

France is the fastest-growing country in the Europe PFAS-free coatings market, driven by increasing regulatory focus on PFAS reduction, rising investments in sustainable materials, and growing adoption of environmentally friendly coating solutions across textiles, packaging, aerospace, and consumer goods industries. During 2025–2026, French manufacturers and brands increasingly shifted toward PFAS-free alternatives to align with European sustainability objectives and upcoming restrictions on fluorinated substances.

Innovations enable manufacturers to adopt fluorine-free coating technologies while maintaining the protective properties required for advanced applications. In March 2025, Plasmalex, a France-based advanced coating technology company, launched PlasmaGuard® X, a 100% PFAS-free conformal barrier coating designed to replace traditional fluorinated coating solutions. The coating technology provides high-performance protection against moisture, corrosion, and environmental exposure while maintaining barrier properties required for applications such as medical devices, consumer electronics, printed circuit board assemblies (PCBAs), and advanced materials.

PFAS-free coatings Market Competitive Landscape

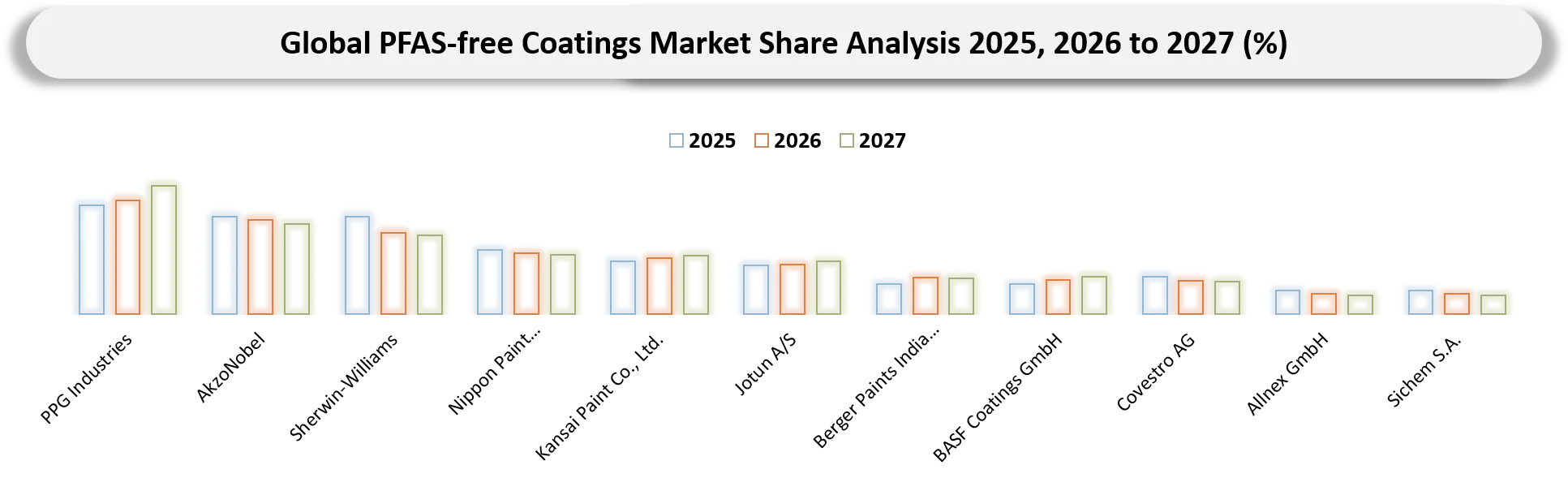

- The PFAS-free coatings market is characterized by three major participant groups: global coatings manufacturers, specialty chemical and resin suppliers, and advanced surface-treatment technology providers. Leading coatings companies such as PPG Industries, AkzoNobel, Sherwin-Williams, Nippon Paint Holdings, Kansai Paint Co., Ltd., Jotun A/S, and Berger Paints India Ltd. focus on developing sustainable coating portfolios by replacing fluorinated chemistries with silicone-based, bio-based, wax-based, and other environmentally compliant formulations. Specialty chemical and material innovation companies, including BASF Coatings GmbH, Covestro AG, and Allnex GmbH, contribute through the development of advanced binders, resins, and coating technologies that enable PFAS-free alternatives with comparable durability, chemical resistance, and surface performance. Surface-treatment technology providers and research organizations, including Sichem S.A., Plasmalex Group, Plasmatreat GmbH, and Fraunhofer IFAM, support market development through plasma-based surface modification, functional coatings, and industrial-scale PFAS-free treatment technologies.

- Key players in the PFAS-free coatings market include PPG Industries, AkzoNobel, Sherwin-Williams, Nippon Paint Holdings, Kansai Paint Co., Ltd., Jotun A/S, Berger Paints India Ltd., BASF Coatings GmbH, Covestro AG, Allnex GmbH, Sichem S.A., Plasmalex Group, Plasmatreat GmbH, and Fraunhofer IFAM.

Key Developments

- August 2025: Wolverhampton Electro Plating (WEP), a UK-based metal finishing specialist and part of the Anochrome Group, partnered with a major automotive fastener manufacturer to test PFAS-free coating systems for automotive components supplied to leading OEMs. The collaboration focuses on evaluating PFAS-free zinc flake coatings from GEOMET NOF, Magni, and Dörken, along with PFAS-free electroplated topcoats from MacDermid.

- December 2025: Xampla, a UK-based biomaterials company, partnered with DIC Corporation, a Japan-based specialty chemicals manufacturer, to introduce a PFAS-free and plastic-free coating solution for the Asian market. The coating technology is based on Xampla’s plant-based Morro™ materials and is designed as a sustainable alternative to conventional PFAS-containing barrier coatings used in packaging applications.

- January 2026: Nordson Corporation, a United States-based precision technology solutions provider, integrated PFAS-free coating technologies into its advanced coating solutions portfolio to support industries transitioning away from fluorinated surface treatments.

- January 2026: the PLASRECO project, a European research initiative focused on sustainable coating technologies, developed PFAS-free functional coating solutions for packaging, leather, and textile applications. The project focuses on silicon-based coatings applied through atmospheric plasma technology to replace conventional PFAS-containing surface treatments.

- April 2026: KYMC (Kuen Yuh Machinery Engineering Co., Ltd.), a Taiwan-based coating and printing equipment manufacturer, collaborated with PuriBlood and FT International to introduce PFK Bio-Med Barrier Coating Technology, a PFAS-free and plastic-free coating solution for sustainable packaging applications.

Key Procurement Priorities and Buyer Evaluation Criteria

- Organizations investing in PFAS-free coatings solutions are increasingly selecting suppliers based on their ability to provide high-performance, environmentally compliant coating technologies that can replace traditional fluorinated coatings while maintaining critical properties such as water repellency, chemical resistance, durability, low friction, and surface protection across multiple applications.

- The procurement decision-making process is increasingly influenced by tightening PFAS regulations, sustainability commitments, circular economy initiatives, and customer demand for safer material alternatives across industries such as textiles, automotive, packaging, electronics, industrial equipment, and consumer products. Buyers are prioritizing suppliers that can support regulatory compliance with evolving restrictions in Europe and North America during 2025–2026.

- Buyers evaluate factors such as coating performance consistency, PFAS-free certification, durability, adhesion strength, thermal and chemical resistance, environmental footprint, and compatibility with existing manufacturing processes when selecting coating technology providers. The ability to achieve comparable performance to fluorinated coatings while maintaining cost competitiveness is a key purchasing consideration.

Why Choose DataM?

- Technological Innovations: Explores advancements in PFAS-free coating technologies, including silicone-based coatings, bio-based formulations, wax-based alternatives, plasma surface treatments, and next-generation water-repellent technologies, enabling industries to achieve comparable performance to fluorinated coatings while improving environmental compliance and sustainability across textiles, automotive, packaging, electronics, and industrial applications.

- Product Performance & Market Positioning: Evaluates how leading coating manufacturers differentiate their solutions based on water repellency, chemical resistance, durability, abrasion resistance, low surface energy, thermal stability, and substrate compatibility. The analysis highlights competitive positioning of companies developing high-performance PFAS alternatives for demanding applications while balancing sustainability, cost efficiency, and regulatory requirements.

- Real-World Evidence: Highlights commercial adoption of PFAS-free coatings across outdoor textiles, automotive components, consumer electronics, food packaging, industrial equipment, and medical applications, demonstrating benefits such as reduced environmental impact, compliance with PFAS restrictions, improved product sustainability profiles, and maintained functional performance.

- Market Updates & Industry Changes: Tracks key industry developments including PFAS regulatory actions, sustainable coating launches, investments in fluorine-free technologies, expansion of green chemistry initiatives, and strategic collaborations among coating manufacturers, chemical suppliers, and research organizations across Europe, North America, and Asia-Pacific.

- Competitive Strategies: Analyzes how leading players strengthen their market presence through sustainable product innovation, R&D investments, acquisitions, partnerships, and expansion of PFAS-free coating portfolios. The report evaluates strategies adopted by global coating companies and specialty material providers to capture demand from industries transitioning away from fluorinated surface treatments.

- Pricing & Market Access: Examines pricing variations based on coating chemistry, formulation complexity, substrate requirements, application method, and performance specifications. The analysis evaluates market access through global coating manufacturers, specialty chemical suppliers, contract coating providers, and advanced surface-treatment technology companies supporting adoption across diverse industries.

- Market Entry & Expansion: Identifies growth opportunities driven by increasing PFAS restrictions, sustainability targets, demand for eco-friendly materials, and replacement of traditional fluoropolymer coatings. The report outlines expansion strategies including development of application-specific formulations, regional manufacturing investments, technology partnerships, and collaboration with end-use industries to accelerate global adoption of PFAS-free coating solutions.

Target Audience

- Coating Manufacturers and Technology Developers

- Specialty Chemical and Material Suppliers

- Automotive and Transportation Companies

- Textile and Apparel Manufacturers

- Packaging and Food Contact Material Companies

- Electronics and Semiconductor Industry Participants

- Chemical and Coatings Distributors