PFAS Filtration Technologies Market Overview

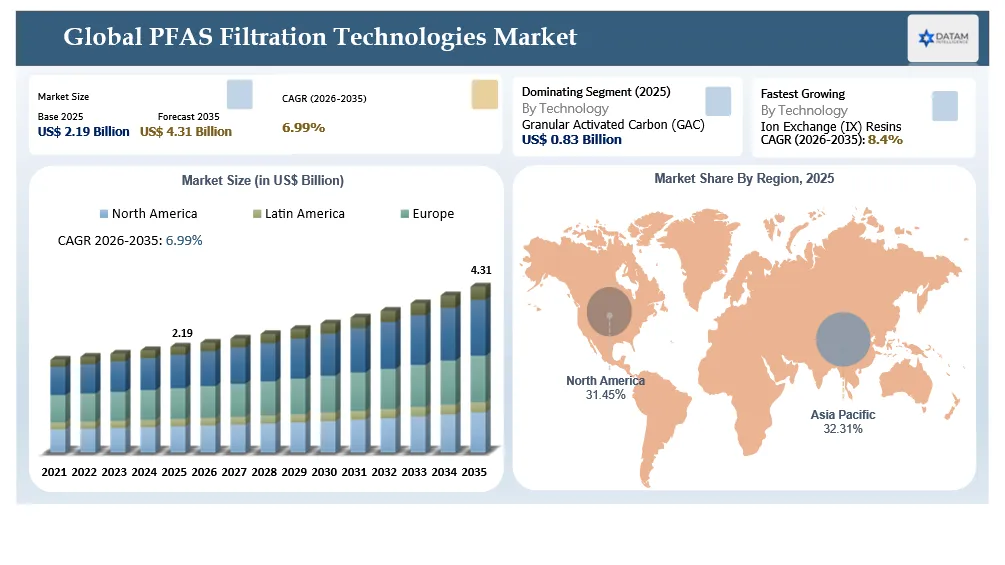

The global PFAS Filtration Technologies market reached US$ 2.19 billion in 2025 and is expected to reach US$ 4.31 billion by 2035, growing with a CAGR of 6.99% during the forecast period 2026-2035.

The evolution of the PFAS filtration technology sector is influenced by the transition from the detection of PFAS to the necessity of treatment due to the enforcement of drinking water regulations covering key substances such as PFOA and PFOS. In contrast to conventional water filtration markets, the PFAS filtration technology sector finds demand mainly in pollution areas including water supply systems, military bases, airports, chemical industry facilities, semiconductor production locations and waste treatment sites. Municipal drinking water treatment accounts for more than 45% of global demand, reflecting large-scale investments in centralized treatment systems, while industrial wastewater treatment contributes approximately 30%, driven by stricter discharge limits and corporate sustainability commitments. Granular Activated Carbon (GAC) remains the leader in large municipal projects due to its reliability and profitability, while ion exchange resins significantly gain popularity due to their efficiency in the treatment of short-chain PFAS compounds that effectively adsorb on GAC.

In today's market, competition is evolving from the sale of equipment to providing lifecycle services that include media replacement, regeneration of filtration media, monitoring of performance and long-term operation & maintenance (O&M) contracts of the equipment/system. Through regeneration and replacement media, which are responsible for about 40% to 45% of the lifetime value of PFAS systems, suppliers have the opportunity for growth of revenues from recurring services. Technology selection is driven by treatment objectives, water chemistry and lifespan economics, not a one-size-fits-all strategy. Granular Activated Carbon (GAC) remains the treatment technology of choice for major municipal drinking water projects, given its proven operating performance and comparatively moderate treatment cost for long-chain PFAS. Ion exchange resins are being increasingly employed in industrial wastewater and groundwater cleanup due to their better adsorption capacity and longer service life for short-chain PFAS, which allows for less frequent media replacement. RO and NF are mostly used in high value industrial applications, such as semiconductor manufacturing and water reuse, where PFAS removal, in addition to dissolved salt, heavy metals and other micropollutants, justifies the higher capital and operating costs. This is leading utilities and industrial operators to invest more in hybrid treatment.

PFAS Filtration Technologies Market Key Takeaways

- Granular Activated Carbon (GAC) continues to be the leading technology, representing around 35–40% of worldwide market revenue by 2025, bolstered by its extensive use in municipal drinking water treatment and advantageous lifecycle economics.

- Municipal water utilities account for the largest end-user segment, making up over 45% of overall market demand, fueled by stricter PFAS drinking water regulations and infrastructure upgrade initiatives.

- Industrial wastewater treatment represents almost 30% of market revenue, with semiconductor, chemical production and landfill leachate treatment identified as the quickest-growing application sectors.

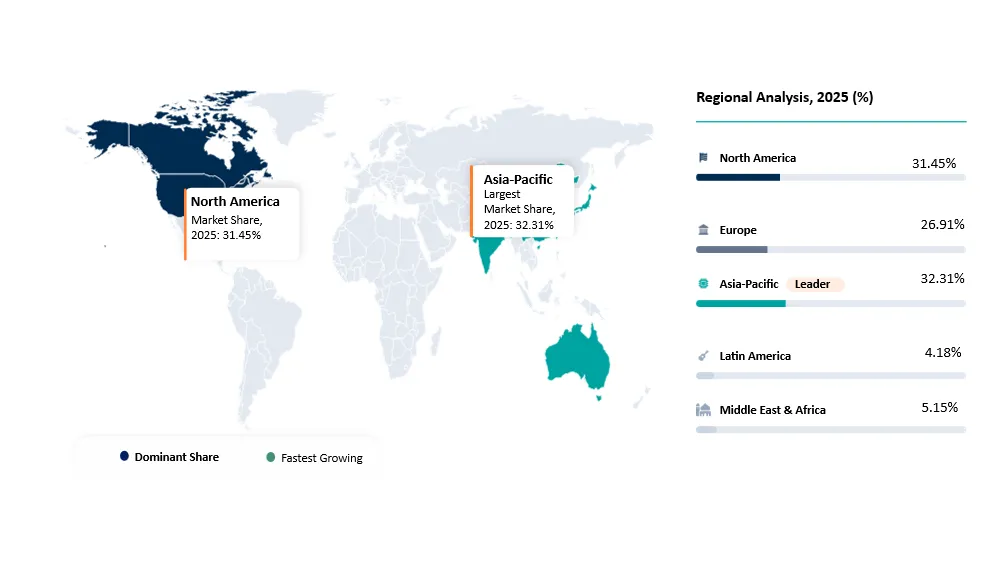

- The Asia-Pacific region accounts for the largest share at 32.31%, driven by growing industrial operations, rising investments in advanced water treatment systems and enhanced environmental regulations.

- The market is transitioning to recurring revenue models, with media replacement, regeneration services and long-term operation & maintenance (O&M) contracts accounting for about 40–45% of the lifetime value of PFAS treatment systems, prompting suppliers to emphasize integrated treatment solutions instead of individual equipment sales.

PFAS Filtration Technologies Industry Trends and Strategic Insights

- Utilities are progressively adopting regenerable filtration media to lower lifecycle treatment expenses, decrease media replacement intervals and enhance operational sustainability.

- The demand for ion exchange resins is increasing as utilities and industrial users aim for effective elimination of short-chain PFAS compounds, which are not as effectively addressed by traditional activated carbon.

- Hybrid treatment systems that integrate GAC, ion exchange and membrane technologies are emerging as the favored approach for intricate water matrices that demand high efficiency in PFAS removal.

- Management of PFAS concentrate and spent media is becoming a crucial investment focus, enhancing the combination of regeneration and destruction technologies with traditional filtration systems.

- Performance-based procurement is becoming more prevalent, as purchasers assess technologies according to PFAS removal effectiveness, longevity of media, operational expenses and adherence to regulations instead of focusing solely on the price of equipment.

PFAS Filtration Technologies Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.19 Billion | |

| 2035 Projected Market Size | US$ 4.31 Billion | |

| CAGR (2026-2035) | 6.99% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Technology | Granular Activated Carbon (GAC), Powdered Activated Carbon (PAC), Activated Carbon Block Filters, Ion Exchange Resins, Reverse Osmosis (RO), Nanofiltration (NF), Ultrafiltration (UF), Foam Fractionation, Electrochemical Treatment, Advanced Oxidation Processes (AOP), Plasma-Based PFAS Destruction, Emerging Adsorbent Technologies and Others | |

| By PFAS Type | Long-Chain PFAS, Short-Chain PFAS, Ultra-Short Chain PFAS and Mixed PFAS Contamination | |

| By Treatment Process | Adsorption, Membrane Separation, Ion Exchange, Chemical Oxidation, Electrochemical Oxidation, Thermal Treatment and Hybrid Treatment Systems | |

| By Regeneration Method | Single Use (Disposable), Thermal Regeneration, Chemical Regeneration and Solvent Regeneration | |

| By Waste Stream Management | Destructive Treatment, Non-Destructive Treatment and Hybrid Treatment | |

| By Product Type | Filtration Media and Filtration Skids | |

| By Application | Drinking Water Treatment, Industrial Wastewater Treatment, Groundwater Remediation, Surface Water Treatment, Landfill Leachate Treatment, Firefighting Foam (AFFF) Waste Treatment, Process Water Treatment, Wastewater Reuse & Recycling and Others | |

| By End-User | Municipal Water Utilities, Industrial Manufacturing, Semiconductor & Electronics, Aerospace & Defense, Oil & Gas, Mining, Commercial Buildings, Environmental Remediation Contractors,Research Institutes & Laboratories and Others | |

| By Installation Type | Centralized Treatment Systems, Point-of-Entry (POE) Systems, Point-of-Use (POU) Systems, Mobile Treatment Units and Containerized Treatment Systems | |

| By Capacity | Small Capacity (<100 m³/day), Medium Capacity (100–1,000 m³/day), Large Capacity (1,000–10,000 m³/day) and Very Large Capacity (>10,000 m³/day) | |

| By Deployment Mode | Permanent Installations, Temporary Installations and Emergency Response Systems | |

| By Component | Filtration Media, Membranes, Pressure Vessels, Pumps, Monitoring & Control Systems, Valves & Piping and Chemical Dosing Systems | |

| By Sales Channel | Direct Sales, Engineering, Procurement & Construction (EPC), Water Treatment Integrators, Distributors, OEMs and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia, Singapore, Vietnam, Thailand, Philippines, Taiwan | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why does this report matter in 2026?

2026 signifies the transition phase of PFAS filtration technologies landscape from voluntary assessment to obligatory treatment and enforcement of compliance. Municipal water supplying organizations, factories, airports, military entities and landfill managers are going to invest in PFAS treatment frameworks due to stricter regulations regarding drinking and waste disposal water. Such changes will contribute to the purchase of new filtering media, treatment systems and O&M services thus opening up excellent prospects for tech companies and investors.

The report provides important information to decision-makers about the competitiveness of technology, trends in adoption by application, regional demand trends and changes in the competitive environment. It provides an assessment of the economic prospects of GAC, ion exchange resins, membrane filtration technologies and the new methods of destroying PFAS substances, while paying special attention to methods of procurement and making sure that the costs of products during their life cycle and the income generated by replacing and recycling these substances are taken into consideration. These insights provide producers, corporations, investors and public authorities with the data necessary for creating strategies in a market where compliance with regulations, effectiveness of technologies and economic factors become the key to success.

PFAS Filtration Technologies Market White Space & Investment Opportunities

- Selective short-chain PFAS treatment media presents a significant growth opportunity since traditional GAC shows reduced adsorption effectiveness for substances like PFBS, PFHxA and GenX. Investment in advanced ion exchange resins and specialized adsorbents is anticipated to rise.

- Many areas still lack advanced infrastructure for the regeneration of used filtration media. Firms providing thermal regeneration, resin recovery and media recycling services can benefit from the increasing number of PFAS treatment systems and escalating disposal expenses.

- Modular and containerized PFAS remediation systems provide considerable advantages for small towns, industrial sites, airports and urgent cleanup efforts that need quick implementation with reduced initial capital costs.

- Integrated PFAS treatment and destruction solutions represent a significant opportunity, as end users are increasingly looking for technologies that merge contaminant removal with electrochemical, plasma, or thermal destruction to minimize secondary waste streams and lessen long-term environmental risks.

- Digital tracking and anticipatory media management is a developing investment sector. AI-driven advanced forecasting, immediate PFAS tracking and predictive upkeep systems can enhance media usage, lower operational expenses and strengthen regulatory adherence for substantial municipal and industrial treatment plants.

PFAS Filtration Technologies Future Market Transformation

The PFAS filtration technologies market is projected to evolve from using separate filtration machines to having complete treatment systems that involve PFAS removal, media regeneration, concentrating management and destroying technologies. Since regulatory bodies consider PFAS compounds rather than just PFOA and PFOS, end users are going to choose technologies that can work with long and short-chain PFAS, at the same time generating less secondary waste. This change may push the use of hybrid treatment systems and reusable filtration media in municipal and industrial facilities to increase significantly.

Within the next ten years, competition will be more about economics related to lifecycle treatment rather than solely about removal efficiency. Those suppliers providing long-lasting filter media, packaged treatment plants, regeneration services and contracts based on performance will benefit from the fact that utilities want predictable costs and sustainable compliance with the regulations. In addition, more investments in modular treatment plants and technologies of PFAS destruction should be expected, educing dependence on landfill disposal and creating a more circular treatment model.

PFAS Filtration Technologies Market Buyer Decision-Making Criteria

When purchasing PFAS filtration solutions, buyers in the sector analyze systems based on their compliance to regulations as well as cost-effectiveness throughout the lifespan of the system. Municipal wastewater treatment plants and industrial users readily prefer solutions that are effective in removing both long and short-chain PFAS in different water quality conditions while favoring systems that minimize media change intervals and energy consumption and waste disposal expenses. Apart from technology functioning procurement decisions are influenced by scalability and ease of integration with other treatment solutions used by customers, as well as media availability and O&M support. Since PFAS regulations are expected to change in the future, buyers pay more attention to suppliers that have already proven their systems are efficient in practice, as well as their capability to provide pilot testing and performance guarantees.

PFAS Filtration Technologies Market Economic & Investment Analysis

The PFAS filtration technologies sector is seeing continued capital investments as governments, municipal agencies and industrial operators are improving water treatment systems. Companies are investing more in high-capacity adsorption media, modular treatment solutions and long-term regeneration services rather than traditional filtration devices, emphasizing the importance of the economics of life cycle treatment. Granular Activated Carbon (GAC) is the most economical solution when it comes to large municipal projects, but more investment is directed to more expensive ion exchange resins and hybrid treatment systems for applications where effective removal of short-chain PFAS and complex contaminant mixtures is required.

When it comes to investing, the market has shifted towards more recurring revenue rather than equipment sales. The revenue of the PFAS treatment business includes revenue made from filtration media replacement, regeneration, O&M and performance monitoring (PM). In addition, the recent wave of venture capital and strategic investments in selective adsorbents, technologies for PFAS destruction and treatment systems in containers comes on the heels of utilities and businesses looking for methods to decrease costs of operations, cut down secondary waste and comply with the laws concerning PFAS.

PFAS Filtration Technologies Investment Trends in the Market

- Municipal capital spending is progressively aimed at centralized PFAS treatment enhancements, with utilities favoring GAC and ion exchange systems rather than traditional treatment methods to comply with new drinking water regulations.

- Investment is moving toward sustainable filtration media, as utilities aim to lower lifecycle operating expenses linked to regular media replacement, transport and disposal of PFAS-contaminated adsorbents.

- Producers are increasing output capabilities for activated carbon, ion exchange resins and membrane modules to meet growing demand from municipal water suppliers, industrial wastewater treatment plants and remediation service providers.

- Strategic investments are speeding up in PFAS concentrate handling and destruction methods, allowing treatment providers to enhance traditional filtration with options that diminish secondary waste and long-term disposal responsibilities.

- Technology vendors are boosting investments in service-oriented business models, encompassing media revitalization, extended supply contracts and operation & maintenance (O&M) agreements, creating ongoing revenue in addition to initial equipment sales.

Strategic Indicators For PFAS Filtration Technologies Market

High Regulation Impact

The market for PFAS filtration technologies depends heavily on regulation because the adoption of technology is closely linked to measurable regulations regarding drinking water and industrial discharge, rather than voluntary sustainability initiatives. As regulators continue to expand the list of regulated PFAS compounds and reduce permissible concentration levels, it forces municipal utilities, industries, airports, military posts and landfills to invest in dedicated PFAS treatment systems. Thus, regulations dictate the timing of capital investments, as well as the choice of technologies, meaning that only technologies such as ion exchange resins, advanced activated carbon and hybrid treatment systems that provide high-level solutions can meet ever-tightening compliance requirements.

High Investment Activity

Currently, the PFAS filtration technologies industry experiences an increased investment activity, since municipalities, corporations and individuals are expanding their treatment technology infrastructure to comply with PFAS regulations. Capital is increasingly directed towards development of various advanced filtration media, modular treatment systems and PFAS destructing technologies, while manufacturers of activated carbon, ion exchange resins and membranes expand their production. Investment is also shifting toward service-based business models, including long-term media supply, regeneration and operation & maintenance (O&M) contracts, reflecting the market's transition from one-time equipment sales to recurring revenue streams.

Supply Chain Disruption

The PFAS filtration technologies industry is encountering moderate supply chain constraints, since production capabilities of activated carbon, ion exchange resins and advanced membrane materials cannot keep up with the growing needs of various municipalities and industries. In addition, the longer delivery times for various types of media for high-performance filtration, limited local regeneration facilities and reliance on specialized raw materials are driving up costs and lengthening lead times. In tacking these challenges, the manufacturers are increasing production capabilities of media, localizing supply chains and building long-term relationships with suppliers of raw materials and filtration media.

Pricing Volatility

The PFAS filtration technologies market displays moderate variability in pricing, which is mainly due to price variations in activated carbon, ion exchange resins, specialty polymers and membranes. Activated carbon prices and prices for ion exchange media fluctuated by 10–20% in the past years, subject to raw material availability, energy prices, prices of transport and change of environmental policies. Furthermore, high-performance PFAS-selective resins typically command a 20–40% price premium over conventional ion exchange resins. Consequently, now municipal utility companies and industrial consumers prefer entering multi-year supply contracts, as well as evaluating technologies of treatment not just according to initial procurement prices but total treatment costs over time.

Procurement Pressure

The market for PFAS filtration technologies is under significant procurement pressure since municipal utilities and industrial facilities are sourcing activated carbon, ion exchange resins, membrane systems and packaged treatment skids promptly to meet the stricter PFAS regulations. The spur of compliance-driven projects has led to a surge in competition for high-performance filtration media causing procurement lead times to increase to about 3–9 months for particular activated carbon and specialty resin supplies. Nonetheless, the process of completion of projects has become easier as buyers now prefer multi-year supply agreements, frameworks contracts and dual-sourcing practices.

New Technology Adoption

The market for PFAS filtration technology is seeing quick uptake, with PFAS-specific ion exchange resins and advanced activated carbon types being adopted as part of more effective systems to remove both long- and short-chain PFAS from water. Certain ways of working with PFAS decontamination products, including foam fractionation, electrochemical oxidation and plasma destruction technology, are also slowly becoming more popular. Such developments help businesses to comply with stricter environmental regulations while continuing getting good results from the media they use in their operations.

Regional Expansion Opportunity

Asia-Pacific represents an excellent regional growth potential owing to growing industrialization, stricter environmental regulations and investment in municipal water infrastructure contributing to the proliferation of PFAS treatment technologies. The countries like China, Japan, South Korea and Australia are expanding their modern water treatment capabilities to tackle industrial pollution and PFAS rules. At the same time, North America and Europe provide good chances for technology suppliers in terms of new media, regeneration service and modernization of the existing treatment systems as utility companies move from pilot schemes to a full-scale establishment of PFAS treatment facilities. The developing markets of the Middle East and Latin America are rich in the long-term potential for growth due to the increasing focus of their governments on water quality.

Government Policy Support

The development of filteration technologies in the industry of PFAS dependent on government policies, as new regulations enhancing standards of the quality of drinking water, standards of discharging substances into the water basins and rules of remediation of PFAS polluted sites have been introduced. Participation of state financing and investments into water management spheres allowed local governments to improve their filtration plants. Due to the demand provoked by regulations industries like chemical, semi-conductor and aviation industries have to introduce PFAS systems according to regulators` duties. As far as authorities add new compounds with PFAS status and decrease allowable concentration levels, it can be stated that policy support will lead to further investments into filteration technologies, regeneration of media and solutions used for compliance with laws and regulations.

Pricing Intelligence

In the PFAS filtration technologies market, pricing is increasingly determined by lifecycle treatment costs, as opposed to equipment costs only. A standard municipal PFAS treatment project generally falls in the range of US$1 million to over US$50 million, depending on the treatment technology and capacity of the system. A more recent way of PFAS treatment is the use of containerized/mobile systems with prices typically reaching US$250,000 - US$2 million. The O&M costs usually account for around 60-75% of the lifecycle cost of the PFAS treatment system mainly due to replacement/regeneration of the filtration medium, the energy expenditure and handling of waste. As a result, the utilities tend to award contracts based on the cost per cubic meter of water treated as well as the long-term service agreement instead of capital cost only.

| HS Code | Reporter | Trade Flow | 2025 Trade Value | Interpretation |

| 842121 | China | Exports | US$ 9.0 Billion | China remains the largest exporter of water filtration and purification equipment, supporting the global supply of PFAS treatment systems. |

| 842121 | United States | Imports | US$ 4.5 Billion | High import volumes reflect strong demand for advanced water treatment equipment driven by tightening PFAS regulations. |

| 842121 | Germany | Exports | US$ 3.0 Billion | Germany is a major supplier of premium industrial filtration and membrane systems for municipal and industrial water treatment. |

| 842121 | India | Imports | US$ 1.0 Billion | Rising imports indicate increasing investments in water infrastructure, industrial wastewater treatment and adoption of advanced filtration technologies. |

AI Impact Analysis of PFAS Filtration Technologies Market

AI assists the PFAS filtration technology industry with regards to its operational efficiency and not its filtration technology. Utility companies and manufacturers use AI systems to perform analytics in monitoring treatment performance, predicting breakthrough of filtration media, optimizing regeneration schedules and lessening energy consumption. Based on these capabilities, costs incurred towards PFAS operations are lowered and PFAS regulations are complied with effectively.

AI is most valued in asset management and process optimization processes that include predictive maintenance, real-time water quality monitoring and the optimization of treatment systems. However, it does not participate in PFAS removal because this process relies on innovations of adsorbent materials, membrane technologies and destruction processes.

Disruption Analysis of PFAS Filtration Technologies Market

The transition from capture-based treatment of PFAS to complete PFAS lifecycle management is disrupting the PFAS filtration technologies market. Conventional technologies like granular activated carbon (GAC), ion exchange resins and reverse osmosis practically eliminate PFAS from water but produce spent media or concentrate streams that have to be treated or disposed of. As environmental regulations turn to the management of PFAS waste, utilities and industrial entities are looking for treatment solutions that are based on the amount of waste produced, regeneration options and overall lifecycle costs instead of removal of contaminants only.

Commercialization of the PFAS destruction technology is another significant breakthrough in the industry aside from traditional filtration. The use of electrochemical oxidation, plasma-based treatment and supercritical water oxidation technologies is being integrated with adsorptive and membrane methods to destroy PFAS in an effective way. This is modifying the competitive landscape of the industry as the manufacturers of the filtration equipment are also beginning to engage in regeneration, concentrate management and destruction through partnerships and products. This is because the customer increasingly requires the overall PFAS treatment as opposed to just filtering capabilities.

PFAS Filtration Technologies Market BCG Matrix: Company Evaluation

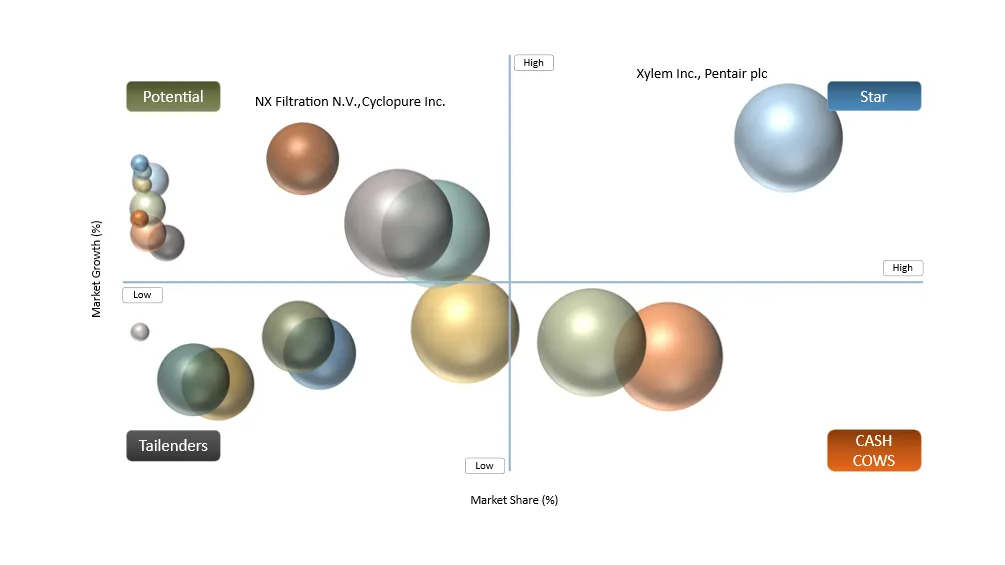

STAR

Xylem Inc., Pentair plc, DuPont Water Solutions, Kuraray Co. Ltd. (Calgon Carbon), Ecolab Inc. (Purolite), Toray Industries, Inc., LANXESS AG and Kurita Water Industries Ltd are held in high esteem as Star companies on account of their extensive PFAS filtration products. These companies have made their mark in municipal as well as industrial water treatment and powerful technology at their disposal. These companies offer a combination of activated carbon, ion exchange resins, membrane-based technologies and integrated treatment systems with a good supply chain network. With more investment being made into media regeneration, high-capacity adsorption materials and packaged PFAS treatment solutions the position of these companies gets stronger as demand for projects increases.

POTENTIAL

NX Filtration N.V., Cyclopure Inc., Jacobi Carbons Group, Koch Separation Solutions, Amiad Water Systems Ltd., Pall Corporation, Hydranautics, Applied Membranes, Inc., Microdyn-Nadir GmbH and LG Chem are acknowledged as Potential companies because they make use of their innovative technologies to create footholds in the PFAS treatment sphere. They are enhancing their competitive position by means of innovations related to membrane filtration, efficient efforts in adsorption media development and modular treatment applications.

PFAS Filtration Technologies Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Stringent PFAS Drinking Water Regulations | 34% | North America, Europe | Municipal drinking water treatment | Accelerates deployment of GAC, ion exchange and membrane filtration systems to meet regulatory compliance. |

Rising Groundwater Remediation Projects | 28% | United States, Australia, Western Europe | Groundwater remediation at military bases, airports and industrial sites | Increases demand for mobile and permanent PFAS treatment systems and remediation services. |

Growing Industrial Compliance Requirements | 22% | Chemical, Semiconductor, Manufacturing Industries | Industrial wastewater treatment | Encourages adoption of advanced PFAS filtration technologies to comply with discharge standards and reduce environmental liabilities. |

Increasing Investments in Water Infrastructure Modernization | 16% | Global, particularly Asia-Pacific and North America | Municipal and industrial water treatment facilities | Supports long-term upgrades of aging infrastructure and adoption of next-generation PFAS filtration technologies. |

Driver: Stringent PFAS Drinking Water and Wastewater Regulations

The market for PFAS filtration technologies is predominantly influenced by the development of strict regulations concerning PFAS. As a result, the treatment process for PFAS is no longer considered an optional environment protection step, but rather an obligatory action for compliance. Governments reduce the PFAS levels permitted in water and increase the scope of their regulation to involve more PFAS chemicals, which makes the regulators require municipal water companies, industrial plants, airports, militaries, waste disposal companies, etc., to use more advanced technologies such as GAC, ion-exchange resins and RO. Consequently, regulatory compliance has turned into the leading factor of investment, long contracts for servicing and demand for more media in the PFAS treatment industry.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

High Capital and Operating Costs of Advanced Filtration Systems | 33% | Municipal Utilities & Industrial Facilities | Large-scale PFAS treatment installations | Delays adoption among budget-constrained utilities and small-to-medium industrial users, increasing project payback periods. |

Complex Disposal of PFAS-Contaminated Filter Media and Concentrates | 27% | Waste Management & Environmental Compliance | Spent GAC, ion exchange resins and RO concentrate disposal | Raises lifecycle costs and drives demand for PFAS destruction and media regeneration technologies. |

Variable Removal Efficiency Across Different PFAS Compounds | 22% | Technology Performance | Treatment of short-chain and emerging PFAS | Necessitates hybrid treatment systems, increasing system complexity and procurement costs. |

Limited Standardized Regulations in Developing Regions | 18% | Emerging Markets | Municipal and industrial water treatment projects | Slows investment decisions and delays widespread adoption until stronger regulatory frameworks are established. |

Restraint: High Lifecycle Treatment and Waste Management Costs

Although usage of these solutions is growing, high treatment cost over the lifetime of the solution makes them most problematic for the market. The end users will still have little expenses for filtration media replacement and regeneration, costs of energy and costs of disposal of spent PFAS-laden activated carbon, exhausted ion exchange resins and reverse osmosis concentrate, in addition to expenses for purchasing the equipment needed for filtration. Thus, the cost is especially high for some large municipal companies in their processes. Hence, the issue of costs makes clients put off their intentions to spend large investments in filters.

PFAS Filtration Technologies Market Segment Analysis

The global PFAS Filtration Technologies market is segmented based on the Technology, PFAS Type, Treatment Process, Regeneration Method , Waste Stream Management , Product Type , Application, End-User, Installation Type, Capacity, Deployment Mode, Component, Sales Channel and region.

By Technology: Granular Activated Carbon (GAC) Dominates the PFAS Filtration Technologies MarketSegment

Granular Activated Carbon (GAC) was estimated to contribute nearly 38% of the global PFAS filtration technologies market share in 2025, thereby becoming the foremost segment in the technology segment. This segment has achieved success due to its reputation for being able to effectively eliminate long-chain PFAS compounds, large-scale use in municipal water treatment plants and lower costs of treatment during the entire lifecycle of the technology in comparison with advanced membrane technologies. The significance of availability of regenerated activated carbon, vast experience of using the carbon and compatibility of GAC with existent technical facilities will boost the popularity of GAC among the stakeholders.

By Application: Industrial Wastewater Treatment Expected to Register the Highest Growth

Industrial Wastewater Treatment is expected to be the fastest-growing segment of the industry, with a high compound annual growth rate (CAGR) of about 8.1% during the forecast period. The high rate of investment in concentration treatment infrastructure is due to the strict PFAS discharge regulations being implemented in chemical, semiconductor, metal manufacturing, textile and landfill leachate industry sectors. Manufacturing industries require treatment solutions to treat the high concentration of PFAS in wastewater which are complex in nature, leading to increasing adoption of ion exchange resins, reverse osmosis and hybrid systems that are efficient in removing PFAS while being cost effective.

PFAS Filtration Technologies Market Geographical Penetration

U.S. PFAS Filtration Technologies Market Landscape

The U.S. is the biggest and most advanced PFAS filtration technologies market with the implementation of enforced federal and state drinking water regulations with respect to PFAS, a wide range of groundwater cleaning programs and massive investments in municipal water networks. The main buyers in the market are municipal water suppliers, the Department of Defense, airports and industries, which leads to the stable demand for GAC (granular activated carbon), ion-exchange resins and reverse osmosis systems. The latter have come into the market nowadays as well as the technologies related to regenerable filtration media, packaged water treatment technology and O&M contracts, which confirm the trend to the life-cycle-based procurement.

Japan PFAS Filtration Technologies Market Outlook

Japan is enhancing its position in the market for PFAS filtration technologies with constant investments in the updated water purification process and high-efficiency filtration materials. The demand is fueled by the semiconductor, electronics, chemical production and public water supply industries, where strict requirements for water quality and growing PFAS monitoring encourage the use of membrane filtration, ion-exchange resins and advanced adsorption technologies. The country’s state-of-the-art production of membranes and specialized filtration materials gives the opportunity for local manufacturers to take advantage of the increasing demand in both domestic and overseas markets.

EU PFAS Filtration Technologies Market Trends

The European marketplace is changing fast as the area approaches tougher PFAS regulations and broader environmental sustainability targets. The investments are going into municipal drinking water improvements, industrial wastewater treatment facilities, landfill leachate disposal and environmental remediation. There is also growing demand for regenerable activated carbon, ion-exchange resins and membranes due to the search for technologies that have low lifecycle cost and produce low secondary waste. The market is shifting towards advanced hybrid solutions that combine filtration and media regeneration as businesses try to lower secondary waste and comply with stricter regulations.

PFAS Filtration Technologies Market Competitive Landscape

- Xylem Inc., Pentair plc, Kuraray Co., Ltd. (Calgon Carbon), DuPont Water Solutions and Ecolab Inc. (Purolite) consistently rank among market leaders thanks to their extensive offerings in activated carbon, ion exchange resins, membrane technologies and complete PFAS treatment.

- While Kuraray is consolidating its leadership in activated carbon business, DuPont Water Solutions, Ecolab (Purolite) and LANXESS AG are enhancing their footprint with specialist ion exchange resins capable to remove PFAS.

- Membrane Technology companies such as Toray Industries, LG Chem, Hydranautics and Koch Separation Solutions are growing their portfolio focusing on industrial wastewater treatment, water reuse and applications requiring advanced PFAS removal technologies.

- Businesses are now venturing into other areas such as regeneration, package treatment systems and long-term operation & maintenance (O&M) agreements, thus generating recurring revenue streams and enhancing customer retention.

- Acquisitions and integration are shaking the competitive landscape, paving the way for manufacturers to provide full PFAS treatment solutions combining filtration, media replacement, regeneration and new PFAS destruction techniques.

- Manufacturers are ramping up investments in capacities, tailored product offerings and creating pilot projects to wrestle lucrative municipal and industrial contracts.

Key Companies

- Xylem Inc. (USA)

- Pentair plc (United Kingdom)

- DuPont Water Solutions (USA)

- Kuraray Co., Ltd. (Japan)

- Ecolab Inc. (USA)

- Toray Industries, Inc. (Japan)

- LANXESS AG (Germany)

- Kurita Water Industries Ltd. (Japan)

- Jacobi Carbons Group (Sweden)

- Pall Corporation (USA)

- Koch Separation Solutions (USA)

- NX Filtration N.V. (Netherlands)

- Amiad Water Systems Ltd. (Israel)

- Cyclopure Inc. (USA)

- Membranium (Russia)

- Hydranautics (USA)

- LG Chem (South Korea)

- Microdyn-Nadir GmbH (Germany)

- Applied Membranes, Inc. (USA)

- Veolia Water Technologies (France)

PFAS Filtration Technologies Market Major Pain Points

- The expensive life cycle treatment cost is due to expenses incurred in replacing filtration media, regenerating cartridges, energy use and disposing of PFAS-contaminated activated carbon and spent ion exchange resin media.

- Conventional adsorption technologies are not effective in treating short-chain PFAS, resulting in the need for use of expensive alternative high-performance ion exchange resins as well as advanced membrane technologies.

- Disposal of PFAS waste is a major issue since the disposal of spent media and reverse osmosis concentrate involves either specialized disposal or specialized destruction processes to avoid further pollution risks.

- Long procurement times as well as lack of availability of high-performance filtration media (in particular PFAS-specific ion exchange resins and some specialty membranes) may delay the implementation of large municipal and industrial treatment operations.

- Changes in regulations and updating regulated lists of PFAS compounds create uncertainties while choosing technology and bring the risk of additional investments into the project.

PFAS Filtration Technologies Market Recent Developments

- February 2026: NX Filtration N.V. has announced that its revenues for the fiscal year 2025 have increased by 28% due to the increased application of their hollow fiber direct nanofiltration (dNF) technology in the areas of drinking water, water reuse and PFAS removal.

- February 2026: NX Filtration N.V. disclosed the signing of a partnership agreement with Applied Membranes, Inc. for the utilization of the direct nanofiltration membrane in the processes of the pharmaceutical wastewater recycling project in the USA.

- April 2026: LANXESS AG expanded its portfolio for PFAS treatment during IFAT 2026 by exhibiting its Lewatit ion exchange resins for the elimination of long, short and ultra-short chain PFAS from drinking water and wastewater applications.

- March 2026: Veolia Water Technologies enhanced its PFAS treatment capability in Australia through the acquisition of the soil remediation business of Orica at AUD 220 million.

- August 2025: NX Filtration N.V. has reported a 26% revenue rise in the first half of 2025 while emphasizing the growing application of its direct nanofiltration technology for drinking, industrial wastewater and PFAS treatment processes.

Analyst View / Opinion on PFAS Filtration Technologies Market

- Leadership in the future marketplace will be shaped by the provision of holistic treatment solutions for PFAS, consisting of treatment techniques such as filtration, media regeneration and PFAS destruction rather than independent types of filtration. Companies that have all facilities are likely to be competitive.

- Ion-exchange resin technology should be widely accepted as a good option for the elimination of short-chain PFAS, while GAC technology will still maintain its supremacy within major municipal water supply operations, as it has achieved accepted of proven efficiency and has already created efficient infrastructures for its implementation.

- The market is slowly moving towards offering services rather than selling equipment, with media replacements, media regeneration and operations and maintenance agreements playing a vital role in generating revenues for vendors.

- The ability to commercialize treatment technologies for short-chain PFAS will be an important differentiator over the next ten years since activated carbon technologies, which have been traditionally used to treat such contamination, may not be as efficient when it comes to some emerging PFAS.

- Technologies for PFAS destruction can serve as a supplement to the traditional filter systems, since the growing regulations can serve as a motivation for various agencies and manufacturers to get rid of secondary wastes and to stay compliant with the regulations in the long run.

PFAS Filtration Technologies Market Target Audience

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Municipal Water Utilities | Water Utility Operators, Infrastructure Managers | Evaluate PFAS treatment technologies, regulatory compliance strategies and infrastructure investment opportunities. |

| Water Treatment Equipment | Filtration System Manufacturers, OEMs, Technology Providers | Understand market trends, competitive landscape, technology adoption and growth opportunities. |

| Environmental Remediation | Remediation Contractors, Environmental Consultants | Identify emerging remediation projects, technology demand and regional market opportunities. |

| Chemical & Specialty Materials | Activated Carbon, Ion Exchange Resin and Adsorbent Manufacturers | Track demand for filtration media and develop next-generation PFAS removal solutions. |

| Industrial Manufacturing | Chemical, Semiconductor, Electronics, Textile and Industrial Plant Operators | Benchmark compliance strategies and select optimal PFAS treatment technologies for wastewater management. |

| Engineering & EPC | Engineering Firms, EPC Contractors, System Integrators | Assess upcoming water infrastructure projects and technology integration opportunities. |

| Government & Regulatory Agencies | Environmental Protection Agencies, Water Authorities | Support policy formulation, compliance monitoring and investment planning for PFAS mitigation. |

| Research & Academia | Universities, Research Institutes, Innovation Centers | Analyze technology developments, research trends and commercialization opportunities in PFAS treatment. |

| Investment & Financial Services | Private Equity Firms, Venture Capitalists, Institutional Investors | Identify high-growth companies, emerging technologies and investment opportunities in the PFAS filtration sector. |

| Healthcare & Commercial Facilities | Hospitals, Laboratories, Commercial Building Operators | Evaluate point-of-use and point-of-entry PFAS filtration systems to ensure safe water quality and regulatory compliance. |

Why Choose DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

What DATAM Uniquely Provides

- Thorough investigation of the PFAS filtration supply chain, including filtering materials, membrane technologies, regeneration methods and new approaches to destroying PFAS.

- Comprehensive assessment of competitiveness in different technologies such as GAC, ion exchange resins, reverse osmosis, nanofiltration and advanced adsorbents along with their potential of implementation.

- Clear recommendations on the tendencies in regulations, procurement, prices and opportunities for investment.

- Extensive analysis of market demands for technology application in treatment processes in municipal and industrial sector.

- Actionable forecasts of new lucrative segments and new opportunities for manufacturers and water utilities.