Pallet Packaging Market Overview

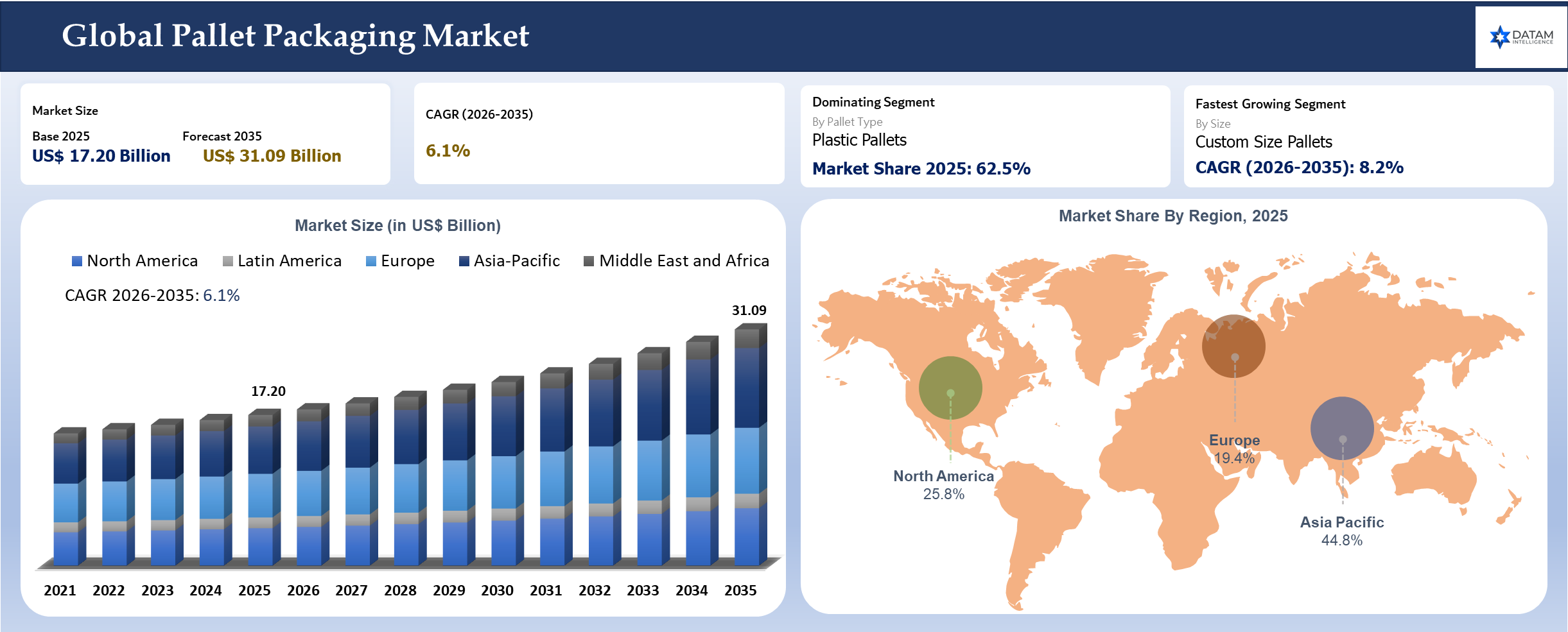

The global pallet packaging market reached US$ 17.20 billion in 2025 and is expected to reach US$ 31.09 billion by 2035, growing with a CAGR of 6.1% during the forecast period 2026-2035. Pallet packaging demand comes from the needs of warehouses, producers, exporters, retailers, logistic companies and temperature-controlled supply chains for protecting cargo from damage, ensuring stability during handling operations and maintaining handling efficiency. The main categories of products in the market include stretch films, shrink films, pallet wraps, straps, corner boards, edge protection and automatic film wrap machines.

Market growth depends on growing palletized freight volumes, growing online retail sales, improving warehouse performance and better control over cargo losses from transport. Companies operating in sectors including foods and beverages, chemicals, pharmaceuticals, consumer goods, construction materials and industrial products seek packaging solutions which provide protection without significant costs for material or additional handling time.

As per DataM analysis, pallet packaging suppliers are no longer competing only on film gauge, strap strength or unit price. Buyers are comparing packaging performance against load containment force, puncture resistance, film yield, packaging waste, machine compatibility, wrapping consistency and total packaging cost per pallet. Suppliers that help customers reduce film usage while maintaining load security are gaining stronger commercial relevance.

Sustainability is also changing purchasing behavior. Recyclable films, downgauged stretch films, bio-based films, PCR content, reusable pallet covers and packaging designs that reduce excess plastic are gaining attention. However, buyers remain practical. Sustainability claims must be supported by load performance, cost control and supply reliability, otherwise adoption remains limited.

Pallet Packaging Industry Trends and Strategic Insights

- Stretch film continues to dominate owing to its extensive applicability in warehousing, manufacturing and logistics.

- Wrapping automation is increasing as organizations lessen their reliance on manual labor while simultaneously enhancing the quality of the wrapping process.

- Innovation driven by sustainability principles is fueling a shift towards sustainable films, thin gauge films, PCR films, and efficient utilization of materials.

- Supplier differentiation depends on load stability performance, packaging cost savings, machine compatibility and technical support.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 17.20 Billion | |

| 2035 Projected Market Size | US$ 31.09 Billion | |

| CAGR (2026-2035) | 6.1% | |

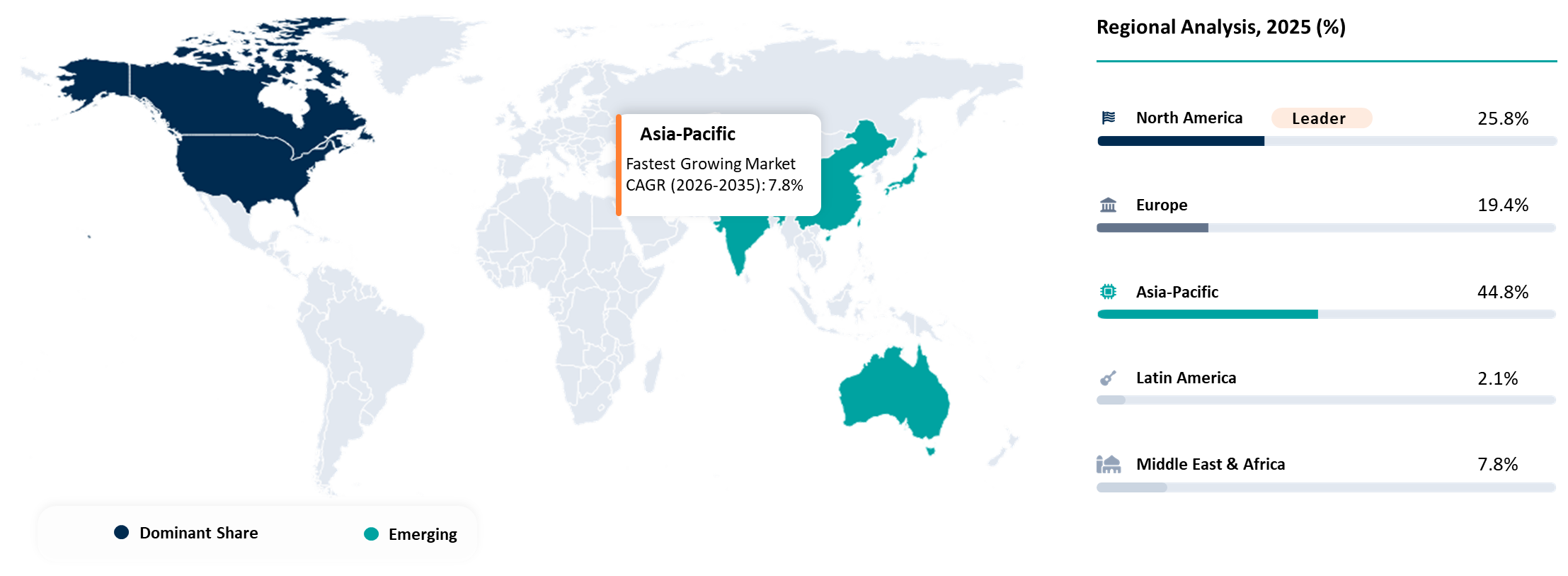

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Pallet Type | Wooden Pallets, Plastic Pallets, Metal Pallets, Paper and Corrugated Pallets, Presswood Pallets, Composite Pallets and Others. | |

| By Design | Stringer Pallets, Block Pallets, Deck Based Pallets, Nestable Pallets, Rackable Pallets, Stackable Pallets and Specialty Design Pallets. | |

| By Load Capacity | Light Duty Pallets, Medium Duty Pallets and Heavy Duty Pallets. | |

| By Size | Standard Pallets and Custom Size Pallets. | |

| By Ownership Model | Purchased Pallets, Rental Pallets and Pooling Pallets. | |

| By Sales Channel | Direct Sales, Pallet Pooling Companies, Distributors and Wholesalers and Online Sales. | |

| By Application | Export Pallets, Hygienic Pallets, Retail Display Pallets, Industrial Storage Pallets, Warehouse Handling Pallets, Cold Chain Pallets, Spill Control Pallets and Others. | |

| By End-User | Food and Beverage, Pharmaceuticals and Healthcare, Chemicals, Consumer Goods, Automotive and Industrial Goods, Building Materials, Agriculture, Retail and E Commerce, Logistics and Warehousing and Others. | |

| By Region | North America | USA, Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

AI Impact

AI Improves Wrap Settings and Material Planning

AI has a limited but growing role in the pallet packaging market. The most significant applications of AI would be through warehouse and packaging line optimization through analyzing machine data for wrappers, load movement, and records of load transportation damage that will indicate unnecessary film consumption, faulty wrap specifications, and load failure.

Through the use of AI-powered monitoring tools, adjustments can be made in relation to wrapping parameters according to pallet height, load weight, load configuration, and product fragility. This will help in avoiding over-wrapping and film wastage while maintaining proper container force. Automated large logistics facilities or warehouses are likely to adopt such tools due to their existing connected systems and volume of pallet loads.

AI technology can also aid in demand forecasting and inventory planning related to packaging materials. Historical purchase behavior, seasonal purchasing patterns, and shipments by customers can be leveraged by manufacturers and distributors to better plan for packaging materials including stretch film, straps, pallet cover and protection film. The lack of stockouts will be particularly beneficial for customers involved in food/beverages, pharmaceuticals, and exports.

While AI may be beneficial in many ways, it does not play a significant role in the growth of the pallet packaging industry. Most purchasing decisions will revolve around packaging effectiveness, pallet cost, environmental compliance, machine suitability, and continuity of supply. While artificial intelligence could increase efficiencies in more advanced processes, it is just a complementary technology.

Disruption Analysis

Downgauging and Automation Reshape Pallet Protection

The industry is undergoing significant disruptions caused by the transition from traditional packaging to performance packaging. Consumers are looking to cut back on plastic utilization, decrease packaging costs while ensuring pallet stability. The trend will be towards thinner high-performance films, advanced pre-stretch systems, more sustainable materials, and wrapping solutions that require minimal film for each pallet.

Automation is the other disruptor in the pallet packaging market. While manual pallet wrapping remains prevalent in small operations, semi-automation and automation have become more widespread in large warehouses and manufacturing plants. Pallet wrapping automation enhances wrap uniformity, minimizes operator fatigue, prevents unnecessary film waste, and improves pallet throughput speed. Companies capable of offering films, machinery, and technical assistance have an advantage over pure-play packaging product suppliers.

Regulatory pressures and customer packaging goals are also disrupting the competitive landscape. Retailers, brand holders, and logistics organizations have begun requesting suppliers to minimize the use of virgin plastics, enhance material recyclability, and facilitate packaging waste reduction. Film providers who offer certified recyclable films, PCR films, and assistance with downgauging initiatives receive greater recognition among buyers.

Price competition is still fierce, particularly within the realms of regular stretch film and strapping. While low-cost vendors can capture volumes where customers are highly sensitive to price, buyers who face considerable risk associated with damage typically favor vendors who have the ability to offer load stability and reduced costs per pallet.

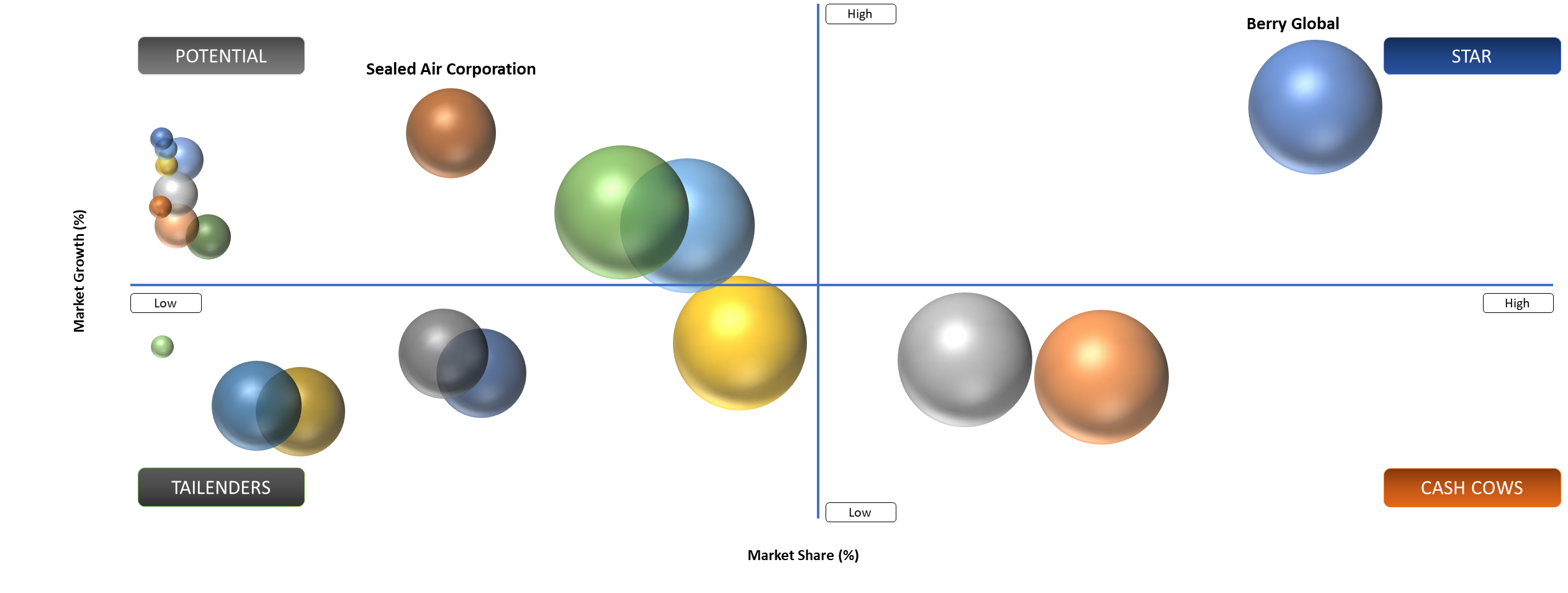

BCG Matrix: Company Evaluation

Load Securement Leaders Gain From Scale and Technical Depth

Stars in the pallet packaging market include Signode Industrial Group LLC and Berry Global Group, Inc. Signode has strong positioning in strapping, stretch wrapping systems, protective packaging and load securement solutions, making it relevant across industrial and logistics-heavy applications. Berry Global benefits from scale, polymer film expertise and broad packaging capabilities, especially in flexible packaging and stretch film-related applications.

Potential players include Trioworld Group and Sealed Air Corporation. Trioworld has relevance in stretch film, industrial films and sustainable film development, while Sealed Air has strong protective packaging expertise and customer reach. Both companies can gain share in specialized applications where sustainability, protection and performance optimization influence buying decisions.

White Space Opportunities

White-space opportunity is strongest where the current market offer remains too broad for the problem the buyer is actually trying to solve inside the pallet packaging market. A large part of the market still packages value at a category level even though revenue is shifting toward narrower use cases with stronger consequences for quality uptime route stability or premium output. Suppliers that design propositions around those exact pain points can create defensible share faster than vendors pushing average-market language.

Mid-market and retrofit environments remain under-served across many of these markets. Large flagship projects receive the most attention while a meaningful pool of profitable demand sits inside existing assets regional operators and buyers that need practical upgrades rather than full replacement. Better modularity, stronger advisory support and lower implementation friction can unlock value that is still poorly captured.

Service layers offer another open opportunity. Buyers increasingly want lower risk clearer validation and stronger lifetime economics rather than just a product transaction. Testing support optimization training modernization traceability and co-development can therefore generate stickier revenue than one-time selling in many of these segments.

Geographic localization is still weak in many offers. Country-level operating conditions differ more than many vendors admit. Players that localize specification strategy without fragmenting their platform will gain more share in the next phase of market development.

Market Dynamics

Rising Demand for Load Stability and Packaging Cost Optimization

As palletized logistics grow, more need arises for packaging systems that can stop movement, product breakage, and any other damage during transit. This is because pallets pass through many points such as warehouses, trucks, ports, distribution centers, and back rooms within stores. Improperly wrapped pallet loads are likely to cause damage to products, rejected loads, safety hazards, and increased reverse logistics expenses.

Stretch films, shrink films, straps, pallet covers and edge protection products are gaining importance because companies need predictable pallet performance under real shipping conditions. Food and beverage companies require stable loads for bottled products, cartons and canned goods. Chemical companies need secure pallet packaging to reduce leakage and handling risk. Pharmaceutical and healthcare products require clean, consistent and damage-resistant pallet protection across controlled supply chains.

Cost optimization is also supporting adoption of better pallet packaging. Buyers are calculating cost per secured pallet rather than only price per roll or price per strap. A higher-performance stretch film can become attractive when it reduces film layers, lowers breakage, improves wrapping speed or prevents product loss. Packaging suppliers that provide load testing, film audits and wrapping parameter recommendations can help customers reduce total packaging cost.

As per DataM analysis, the strongest growth opportunities are in high-volume operations where small packaging improvements create large annual savings. Warehouses, distribution centers, beverage plants, FMCG manufacturers and export-focused industries are more likely to invest in optimized pallet packaging because damaged pallets directly affect margins, delivery reliability and customer satisfaction.

Volatility in Polymer Prices and Recycling Limitations

Price fluctuations in polymers continue to be a significant barrier in the pallet packaging industry since many products such as stretch films, shrink films, straps, and other forms of pallet protection require plastic resins. Variations in the prices of materials such as polyethylene (PE), polypropylene (PP), and polyethylene terephthalate (PET) have an impact on cost and pricing challenges. Price-conscious clients may resist using high-performing or sustainable materials during periods of high resin prices. The inability to recycle pallet packaging materials also acts as a barrier in adopting sustainable pallet packaging solutions. While stretch films can be recycled, the process can be difficult due to issues such as contamination, mixed materials, ineffective collection processes, and non-separation after use.

Sustainable alternatives also present technical and economic challenges. Films based on PCR, biodegradable materials, and down-gauged films need to be able to offer puncture resistance, clinginess, flexibility, and load retention. Consumers are not going to accept any sustainability benefits that lead to a higher incidence of damaged goods or disrupt logistics operations. Thus, the uptake is more limited in areas where there are no established recycling processes, unpredictable resin prices, and consumers who prioritize upfront costs in their decision-making process.

Segmentation Analysis

Stretch Film Leads While Automation Raises Packaging Efficiency

Stretch film is the most important product segment in the pallet packaging market because it is widely used to secure pallet loads across manufacturing, warehousing, distribution and retail logistics. Demand is supported by its flexibility, relatively low cost, compatibility with manual and machine wrapping and ability to stabilize different load shapes. High-performance stretch films are gaining share as customers reduce film thickness while maintaining containment force.

Shrink film serves applications that require tighter product bundling, improved tamper resistance or additional protection during transport and storage. It is used in selected industrial, beverage, consumer goods and distribution applications where product visibility and load protection are both important. Shrink film adoption is more selective than stretch film because it often requires heat application and specific equipment.

Strapping and banding remain important for heavy, rigid or high-risk palletized goods. Steel, PP and PET straps are commonly used in building materials, metals, paper, chemicals, appliances and industrial goods. PET strapping is gaining preference in many applications due to strength, safety and handling advantages over steel in selected load types.

Pallet covers, top sheets and liners are used where dust, moisture, contamination or outdoor exposure needs to be reduced. Food ingredients, chemicals, pharmaceuticals, agriculture products and export shipments often require added protection beyond basic stretch wrapping. Demand is strongest where palletized goods face storage exposure or longer transport cycles.

Manual packaging still finds its applications in smaller warehouses, lower volume shippers and cost-conscious consumers. Semi-automatic packaging is becoming increasingly common in mid-sized facilities that require improved consistency and reduced labor but do not need complete automation. Automatic packaging is gaining acceptance in larger manufacturing facilities, logistics centers and distribution centers, which demand increased efficiency and material savings.

Geographical Penetration

Asia-Pacific Growth Rises With Manufacturing and Logistics Expansion

Asia-Pacific is expected to maintain dominance in terms of growth rate due to industrialization, export, organized retail, e-commerce, and automation in warehouse management systems. Some of the notable regions in Asia-Pacific are China, India, Japan, South Korea, Indonesia, Vietnam, and Thailand.

North America Pallet Packaging Market Outlook

The North American presents a huge market for pallet packaging owing to efficient warehousing, retail logistics, production of food and beverages, and ecommerce logistics operations. The massive distribution network in the United States and Canada creates constant demand for stretch films, machine films, pallet covers, strapping, and automated packaging machines. Labor costs have forced many manufacturers to purchase semi-automatic and fully automatic pallet wrapping machinery.

Europe Pallet Packaging Market Trends

Europe (Germany, France, UK, Italy, Spain, Poland, and Netherlands) represents substantial demand for sustainable and recyclable pallet packaging. The European customers generally evaluate pallet packaging material according to their recycling, downgauging properties, recycled content of post-consumer, and packaging waste management methods.

Latin America and Middle East and Africa display an increasing demand for food exports, agriculture, chemical products, building supplies, and retail distribution. Although the adoption of state-of-the-art pallet packaging varies from country to country, there seems to be increasing demand owing to improvements in logistics and loss prevention in exportation packaging.

Competitive Landscape

Suppliers Compete on Film Performance, Service and Sustainability Data

- Pallet packaging is a competitive market with a variety of players like global packaging firms, industrial packaging firms, film makers, strapping firms, and regional converters. The main competitors include those who differentiate themselves with extensive product range, availability, technical support, sustainability efforts, and relationships with multinationals.

- Product differentiation occurs in high performance stretch films, machine films, recyclable films, PET strapping, automation technology, and load security solutions. Firms which offer services of auditing packaging lines of their customers, recommending film specification, and securing loads command higher prices than those supplying commodity film or straps.

- Sustainability has become an important element in competitive strategy, with companies offering thin films, recyclable films, PCR material, lighter packaging, and so forth. Nonetheless, success in the market is dependent upon ability to convince customers that sustainable packaging works in challenging transport and storage environments. Buyers are increasingly asking for data on load containment, film usage reduction and recycling compatibility.

- As per DataM analysis, competitive advantage will belong to suppliers that combine material performance, equipment compatibility, packaging engineering and sustainability support. Companies that help customers reduce damage, lower plastic use and improve cost per pallet will be better positioned than suppliers competing only on material price.

Key Developments

- May 2026: Amcor plc reinforced its role through a launch collaboration or segment-specific initiative tied to more selective demand pockets. Market impact is meaningful because premium projects increasingly favor suppliers that can pair product depth with stronger support.

- March 2026: Berry Global Group, Inc. highlighted market activity linked to premium segments and commercially demanding customers. Strategic importance comes from the way such moves signal where capital and technical effort are being directed as buying criteria become stricter.

- January 2026: Signode Industrial Group LLC strengthened its strategic position through product capacity or program activity that improved visibility in higher-value specifications. Commercial relevance is high because buyers are rewarding suppliers that remove operating risk and can scale without service disruption.

- November 2025: Mosca GmbH showcased capability enhancements relevant to more selective buying criteria. Market significance is tied to the growing premium on implementation confidence and practical field performance.

- September 2025: FROMM Holding AG advanced commercial reach through project modernization technical-support or channel activity linked to customer requirements in this market. Importance lies in stronger access to recurring and defensible demand pools.

- July 2025: Mondi plc reported progress that improved competitiveness in targeted programs specialty applications or lifecycle-driven work. Development matters because revenue quality is shifting toward segments where validation and service matter more than simple volume.

- February 2025: Lantech, LLC expanded regional or segment activity in a way that improved its standing with customers looking for local support and faster response. Strategic value comes from the fact that regional execution now affects supplier choice more strongly.

- October 2024: Sealed Air Corporation signaled stronger competitive intent through capability-building channel expansion or targeted project engagement. Market importance rests in the shift toward differentiated and high-fit opportunities.

- August 2024: Trioworld Group increased visibility in emerging or specialized subsegments that are drawing stronger buyer interest. Such moves matter because small premium niches often shape future share gains before they become large-volume categories.

- June 2024: Aetna Group S.p.A. strengthened its offering through product refinement digital support or route-to-market action aligned with present customer pain points. Development is notable because established players are defending share through deeper value delivery.

DMI Opinion

According to DataM, the pallet packaging market will reward precision more than breadth over the next cycle. Buyers are not short of alternatives. Buyers are short of suppliers that can prove why a specific solution is the right one under a defined operating constraint. Markets of this kind rarely reward generic category language for long because the customer can see where failure really happens.

Strong long-term positions will belong to companies that combine technical credibility commercial patience and execution quality. Technical credibility gets the supplier onto the shortlist. Commercial patience keeps the supplier close to the customer through testing validation or planning cycles. Execution quality turns that first decision into repeat business and stronger pricing power.

Premium value is also likely to migrate toward subsegments that still look narrow today. Smaller segments with higher switching barriers or stronger visibility around failure often shape margin more than large segments built on easy substitution. Companies that understand those pockets early can create a more durable market position than volume-led competitors.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience

- Manufacturers and OEMs: Companies producing systems materials ingredients or components linked to pallet packaging market and evaluating product strategy expansion priorities and competitive positioning.

- Distributors and Channel Partners: Firms managing regional sales specification support dealer networks or value-added services in this market.

- Asset Owners and Commercial Buyers: Operators processors building owners utilities farms or industrial users procuring solutions based on lifecycle economics uptime quality or compliance needs.

- Engineering and Technical Teams: Consultants plant managers formulation experts project developers or maintenance leads responsible for validating performance and implementation fit.

- Investors and Private Equity Firms: Financial stakeholders assessing margin structure consolidation potential and growth pockets in premium or underpenetrated subsegments.

- Government Regulators and Standards Bodies: Institutions shaping safety environmental trade building agricultural or quality frameworks that affect demand formation.

- Technology and Service Providers: Companies offering analytics testing retrofit support digital tools or system-integration capabilities that complement the core market.

- Strategic Procurement and Supply Chain Leaders: Decision-makers monitoring sourcing resilience feedstock risk regional supply concentration and long-term supplier reliability