Ophthalmic Sutures Market Size

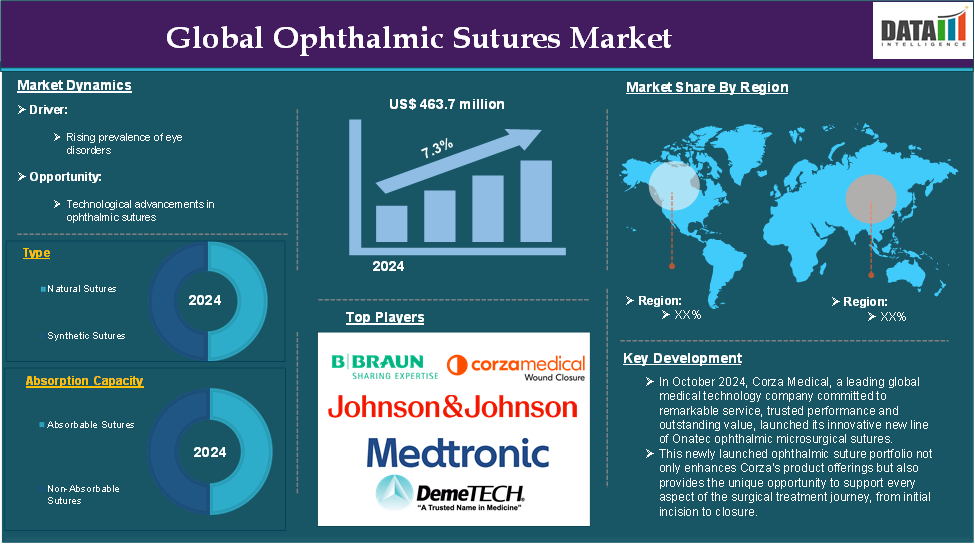

The Global Ophthalmic Sutures Market reached US$ 463.7 million in 2024 and is expected to reach US$ 871.5 million by 2033, growing at a CAGR of 7.3% during the forecast period 2025-2033.

Ophthalmic sutures are specialized medical threads or strands used to close surgical incisions or wounds in the eye or surrounding ocular tissues. These sutures are designed to provide precise tissue approximation, support healing, and minimize trauma to delicate ocular structures. They are crucial in ophthalmic surgeries, including procedures on the cornea, sclera, iris, eyelids, and orbital tissues. Ophthalmic sutures are extremely thin and delicate to match the sensitive and intricate nature of eye tissues.

The ophthalmic sutures market experiencing consistent growth, driven by factors such as the increasing prevalence of eye disorders and advancements in surgical techniques. For instance, in October 2024, Corza Medical launched its innovative new line of Onatec ophthalmic microsurgical sutures, unveiled at the American Academy of Ophthalmology (AAO) conference in Chicago.

Executive Summary

For more details on this report – Request for Sample

Market Dynamics: Drivers & Restraints

Rising prevalence of eye disorders

The rising prevalence of eye disorders is significantly driving the growth of the ophthalmic sutures market and is expected to drive the market over the forecast period. Cataracts are one of the most common eye conditions worldwide, particularly in the aging population. As people age, the likelihood of developing cataracts increases. Cataract surgery is one of the most common procedures performed worldwide.

For instance, the WK Eye Institute estimates that around 15% of the approximately 28 million cataract procedures carried out annually globally take place in the US. The number of cataract surgeries is projected to rise further, consequently increasing the demand for ophthalmic sutures.

Diabetic retinopathy, a complication of diabetes that affects the retina, is a growing concern. According to the International Diabetes Federation (IDF), up to 28% of the 463 million persons with diabetes worldwide are at risk for developing diabetic retinopathy. Treatment for advanced stages of diabetic retinopathy often involves vitrectomy (removal of the vitreous gel from the eye), which requires specialized sutures to repair and close incisions made during surgery.

Age-related macular degeneration (AMD) is another eye disorder that is becoming more common with aging. By 2040, 288 million people are expected to suffer from AMD, according to the American Academy of Ophthalmology. While AMD typically requires medical treatments like injections, advanced cases may need surgical interventions, such as retinal surgeries, where ophthalmic sutures are essential for tissue repair and closure.

Shift towards sutureless surgical techniques

Shift towards sutureless surgical techniques is expected to hamper the growth of the ophthalmic sutures market. While ophthalmic sutures are essential for many eye surgeries, the development and adoption of sutureless techniques are reducing the dependency on traditional sutures in various surgical procedures. For instance, in cataract surgeries, adopting femtosecond laser technology has reduced the need for sutures. This technology enables surgeons to perform precise corneal incisions that often do not require sutures for closure.

Surgeons are increasingly utilizing self-sealing corneal incisions in cataract and refractive surgeries. These incisions naturally close without requiring sutures, reducing the need for suturing altogether. This trend is particularly evident in refractive surgeries (e.g., LASIK, PRK) where small, precise incisions are made, often without sutures, leading to faster recovery times and minimal scarring.

Tissue adhesives or cyanoacrylate-based glues are gaining popularity as alternatives to sutures in many ophthalmic surgeries, especially for procedures like corneal wound repair and retinal surgeries. These adhesives provide a quicker and more efficient closure for certain types of eye surgeries, offering several advantages over traditional sutures, such as ease of application, reduced surgical time, and fewer complications. For instance, in retinal detachment surgeries, cyanoacrylate tissue adhesives are sometimes used to seal retinal tears, eliminating the need for sutures.

Market Segment Analysis

The global ophthalmic sutures market is segmented based on type, absorption capacity, application, end-user and region.

Absorption Capacity:

The non-absorbable sutures segment is expected to dominate the ophthalmic sutures market share

Non-absorbable sutures are preferred in surgeries where long-term tissue support is crucial, such as scleral or corneal repairs, retinal surgeries, and glaucoma surgeries. These surgeries often involve tissues that take a longer time to heal or need sustained support. For instance, in glaucoma surgeries like trabeculectomy, non-absorbable sutures are used to ensure that the incision remains closed until the wound fully heals. Their ability to provide durable support is essential for reducing the risk of postoperative complications like wound dehiscence (wound opening).

Nylon and polypropylene, the two most common materials used for non-absorbable sutures, offer superior tensile strength and durability compared to absorbable sutures. This makes them ideal for use in areas that experience high mechanical stress or require precise closure. For instance, in corneal surgeries, such as penetrating keratoplasty (corneal transplants), where precise wound closure is critical to prevent infection and ensure proper healing, non-absorbable sutures ensure that the incision site is securely closed for a prolonged period.

Non-absorbable sutures do not dissolve over time, which makes them suitable for applications where the removal of sutures is not necessary. For instance, in cataract surgeries, retinal procedures, or glaucoma surgeries, non-absorbable sutures can remain in place indefinitely without causing issues, reducing the need for follow-up procedures. In cases like eyelid surgeries, the sutures may remain permanently in place, providing lasting structural support to the eyelids.

Market Geographical Share

North America is expected to hold a significant position in the ophthalmic sutures market share

Ophthalmic diseases such as cataracts, glaucoma, age-related macular degeneration (AMD), diabetic retinopathy, and other vision-related disorders are more prevalent in North America especially in the United States and Canada, particularly due to an aging population and increasing lifestyle-related factors like diabetes. For instance, according to the American Academy of Ophthalmology (AAO), 14.6 million Americans are predicted to have diabetic retinopathy by 2050, increasing the demand for procedures involving ocular sutures.

The ophthalmic sutures market in North America benefits from a well-established healthcare market, with high adoption rates of ophthalmic procedures. In particular, cataract surgeries in the U.S. are expected to increase due to the country’s aging population and advancements in surgical techniques.

For instance, according to the National Eye Institute (NEI), the number of cataract surgeries performed in the United States alone is expected to increase significantly over the next several decades, from about 3.6 million in 2020 to 5.7 million by 2050. Sutures are frequently needed to close the incision during cataract surgeries, and as more procedures are performed, there is a growing need for ophthalmic sutures.

Asia-Pacific is growing at the fastest pace in the ophthalmic sutures market

The Asia-Pacific region has a large and growing population that is increasingly affected by a range of eye disorders. Conditions such as cataracts, glaucoma, age-related macular degeneration (AMD), diabetic retinopathy, and corneal diseases are becoming more prevalent due to an aging population, lifestyle changes, and rising diabetes rates. For instance, Cataracts are a major concern in Asia. According to World Health Organization (WHO) predictions, cataracts will continue to be the major cause of blindness in the region, affecting over 50 million people by 2030.

In countries like India, China, and Japan, where the aging population is rapidly increasing, the demand for cataract surgeries and related ophthalmic treatments is soaring. Cataract surgery often involves the use of ophthalmic sutures for wound closure, driving the demand for sutures.

For instance, the significant accomplishments of the Cataract Blindness project in India are detailed in the World Bank's Implementation Completion Report. An estimated 320,000 people are prevented from becoming blind each year, based on an estimated 3.5 million cataract procedures. During the program period, the overall prevalence of cataract blindness decreased by 26%, from 1.5 percent at baseline to 1.1 percent. These rising cataract surgeries boost the demand for ophthalmic sutures in the region.

Competitive Landscape

The major global players in the ophthalmic sutures market include B. Braun SE, Johnson & Johnson Medical NV., Medtronic plc, DemeTECH Corporation, Corza Medical, KATSAN Katgut Industry and Trade Inc., Golnit, Accutome Inc. Aurolab, Dolphin Sutures and among others.

Scope

| Metrics | Details | |

| CAGR | 7.3% | |

| Market Size Available for Years | 2018-2033 | |

| Estimation Forecast Period | 2025-2033 | |

| Revenue Units | Value (US$ Mn) | |

| Segments Covered | Type | Natural Sutures and Synthetic Sutures |

| Absorption Capacity | Absorbable Sutures and Non-Absorbable Sutures | |

| Application | Cataract Surgery, Corneal Transplantation Surgery, Vitrectomy Surgery, Iridectomy Surgery, Oculoplastic Surgery and Others | |

| End-User | Hospitals, Ophthalmic Clinics, Ambulatory Surgical Centers and Others | |

| Regions Covered | North America, Europe, Asia-Pacific, South America, and Middle East & Africa | |

Why Purchase the Report?

- Pipeline & Innovations: Reviews ongoing clinical trials, product pipelines, and forecasts upcoming advancements in medical devices and pharmaceuticals.

- Product Performance & Market Positioning: Analyzes product performance, market positioning, and growth potential to optimize strategies.

- Real-World Evidence: Integrates patient feedback and data into product development for improved outcomes.

- Physician Preferences & Health System Impact: Examines healthcare provider behaviors and the impact of health system mergers on adoption strategies.

- Market Updates & Industry Changes: Covers recent regulatory changes, new policies, and emerging technologies.

- Competitive Strategies: Analyzes competitor strategies, market share, and emerging players.

- Pricing & Market Access: Reviews pricing models, reimbursement trends, and market access strategies.

- Market Entry & Expansion: Identifies optimal strategies for entering new markets and partnerships.

- Regional Growth & Investment: Highlights high-growth regions and investment opportunities.

- Supply Chain Optimization: Assesses supply chain risks and distribution strategies for efficient product delivery.

- Sustainability & Regulatory Impact: Focuses on eco-friendly practices and evolving regulations in healthcare.

- Post-market Surveillance: Uses post-market data to enhance product safety and access.

- Pharmacoeconomics & Value-Based Pricing: Analyzes the shift to value-based pricing and data-driven decision-making in R&D.

The global Ophthalmic Sutures market report delivers a detailed analysis with 70 key tables, more than 64 visually impactful figures, and 159 pages of expert insights, providing a complete view of the market landscape.

Target Audience 2024

- Manufacturers: Pharmaceutical, Medical Device, Biotech Companies, Contract Manufacturers, Distributors, Hospitals.

- Regulatory & Policy: Compliance Officers, Government, Health Economists, Market Access Specialists.

- Technology & Innovation: AI/Robotics Providers, R&D Professionals, Clinical Trial Managers, Pharmacovigilance Experts.

- Investors: Healthcare Investors, Venture Fund Investors, Pharma Marketing & Sales.

- Consulting & Advisory: Healthcare Consultants, Industry Associations, Analysts.

- Supply Chain: Distribution and Supply Chain Managers.

- Consumers & Advocacy: Patients, Advocacy Groups, Insurance Companies.

- Academic & Research: Academic Institutions.