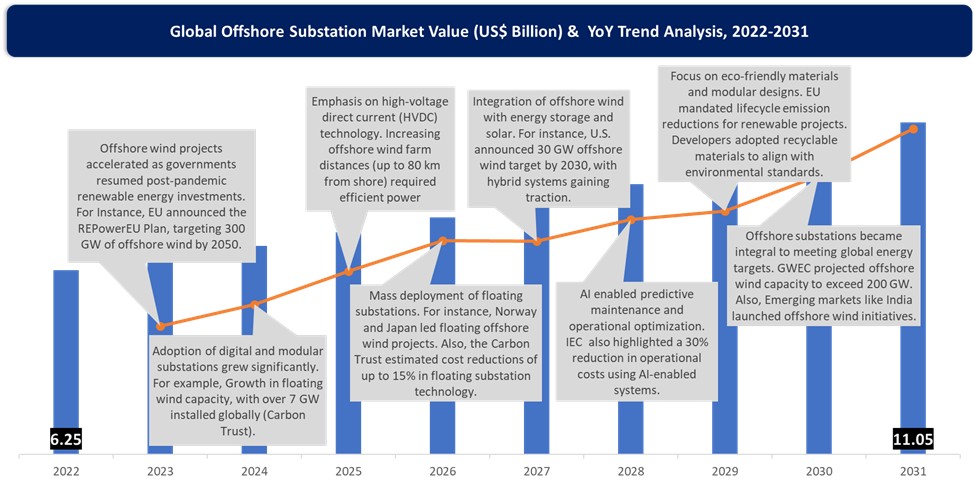

Offshore Substation Market Overview

The global offshore substation market relates to the renewable energy infrastructure, making it possible for the power produced by offshore wind farms to be efficiently transmitted to an onshore electrical grid. Offshore substations are increasing their demand in light of governments pushing for achieving net-zero emissions, as it is estimated from Global Wind Energy Council (GWEC) that the installed offshore wind capacity reached around 75 GW by 2023, with projections to be more than 200 GWs by 2030 biennially plotted. The development is an avenue attracting investments in advanced substations.

Key Takeaways

- Europe accounted for the largest market share in 2025, estimated at around 41.8%, driven by aggressive offshore wind expansion targets, grid modernization initiatives, and strong government support across countries such as the United Kingdom, Germany, the Netherlands, and Denmark. The region continues to lead global offshore renewable energy deployment, creating sustained demand for HVAC and HVDC offshore substations.

- Asia-Pacific is projected to register the fastest growth rate through 2030, supported by large-scale offshore wind projects in China, South Korea, Japan, Taiwan, and Vietnam. China remains the dominant growth engine, with significant investments in deep-water offshore wind farms and ultra-high-voltage transmission infrastructure designed to connect offshore generation assets to coastal demand centers.

- North America is emerging as a high-potential market, led by the rapid development of offshore wind projects along the U.S. East Coast. Federal leasing programs, clean energy incentives, and state-level renewable energy mandates are accelerating investments in offshore transmission infrastructure and offshore substations.

- HVDC offshore substations are gaining strategic importance as offshore wind farms move farther from shore and increase in capacity. HVDC technology enables efficient long-distance power transmission with lower energy losses, making it the preferred solution for next-generation gigawatt-scale offshore wind developments.

- Floating offshore wind projects are creating new opportunities for innovative substation designs. As developers target deeper waters where fixed-bottom foundations are impractical, demand is increasing for compact, lightweight, and floating-compatible offshore electrical infrastructure.

- Digitalization is transforming offshore substation operations. Asset owners are increasingly integrating AI-based monitoring systems, predictive maintenance platforms, digital twins, and remote-control technologies to improve reliability, reduce downtime, and optimize maintenance costs in harsh marine environments.

- Supply chain localization is becoming a major industry trend. Governments and developers are encouraging domestic manufacturing of transformers, switchgear, cables, and substation components to reduce project risks, strengthen energy security, and support local economic development.

- The competitive landscape is shifting toward large EPC and grid technology partnerships. Companies are increasingly forming strategic alliances to deliver integrated offshore transmission solutions that combine substations, export cables, grid connections, and advanced power conversion technologies.

- Grid integration has become a critical challenge for offshore wind expansion. Many countries are investing in coordinated offshore transmission networks and multi-terminal HVDC systems to efficiently connect multiple wind farms while ensuring long-term grid stability.

The Offshore Substation market in the Asia-Pacific region is experiencing rapid growth, primarily due to investments in renewable energy. The Global Wind Energy Council (GWEC) estimates that Asia-Pacific is expected to account for up to 61% of the new additions to be constructed globally in the 2024-2030 period. As of the end of 2023, it already accounted for over half (51%) of the global total wind power installations. Government initiatives, including Japan's offshore wind roadmap for 10 GW by 2030 and South Korea's Green New Deal, emphasize offshore infrastructure. These developments ignite regional demand for high-capacity technologically advanced substations, thereby positioning the Asia-Pacific region as a significant growth contributor.

Offshore Substation Market Scope

| Metrics | Details |

| CAGR | 5.9% |

| Size Available for Years | 2023-2033 |

| Forecast Period | 2026-2033 |

| Data Availability | Value (US$) |

| Segments Covered | Type, Voltage Type, Installation, End-User and Region |

| Regions Covered | North America, Europe, Asia-Pacific, South America and Middle East & Africa |

| Fastest Growing Region | Asia-Pacific |

| Largest Region | Asia-Pacific |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth, Demand, Recent Developments, Mergers and Acquisitions, New Product Launches, Growth Strategies, Revenue Analysis, Porter’s Analysis, Pricing Analysis, Regulatory Analysis, Supply-Chain Analysis and Other key Insights. |

For more details on this report – Request for Sample

Offshore Substation Market Dynamics

Growing Ambitious Renewable Energy Targets

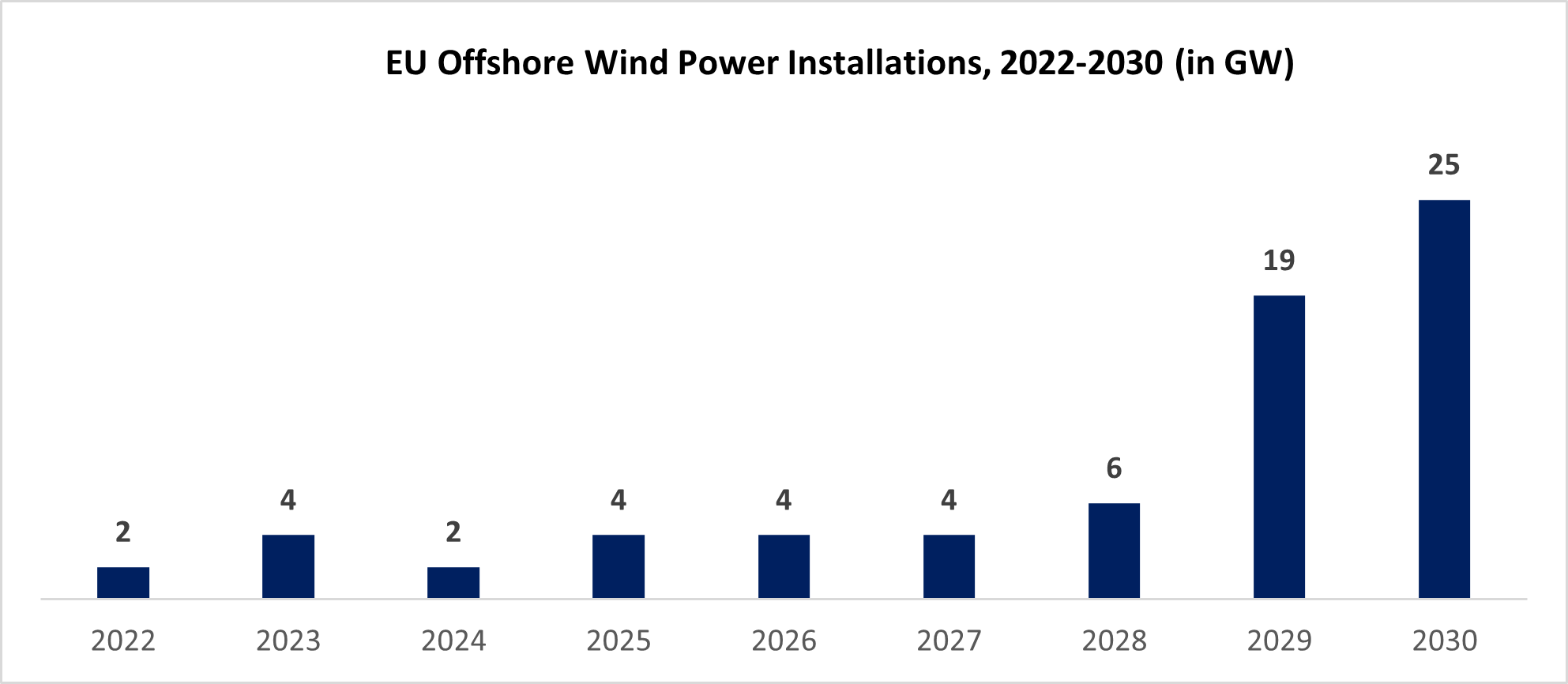

Given the increasing ambition of government renewable energy targets worldwide, it is reasonable to assume that the offshore substation market would be stimulated. In fact, the Renewable Energy Directive of the EU is going to require member states to attain a 42.5% renewable energy share by 2030. This necessitates the construction of offshore wind farms with substantial capacity. Their offshore substations will play a critical role in the incorporation of the grid and the transmission of power.

The U.S. Department of Energy (DOE) aims to achieve 30 GW by 2030 and establish a roadmap for attaining 110 GW or more by 2050. This would necessitate an investment of approximately $12 billion in offshore substations and associated infrastructure, as per the report published by the American Clean Power Association (ACPA). Similarly, the British Energy Security Strategy (BESS) established an ambitious goal of producing 50 GW of offshore wind by 2030, which includes 5 GW of innovative floating technology, at the beginning of April.

Source: WindEurope

The floating offshore wind farms, which can also be deployed in deeper waters, are gathering momentum. In this instance, they necessitate novel substation designs, specifically floating substations, to optimize operational efficiency. The market for next-generation substation solutions is rapidly expanding as Norway's Floating Offshore Wind Strategy aims to achieve 30 GW of capacity by 2040. These substations are important in the global renewable energy targets and are regarded as a component of the integration of wind power within national grids while maintaining grid stability. Substation technologies, including high-voltage direct current (HVDC) systems, are receiving increased investment as developers prioritize reliability and efficiency.

Rise of Digital And Smart Substations

The offshore substation development market is significantly influenced by the ongoing technological advancements in substation design and operation. The modern operating efficiency dimension is transformed by digital and smart substations that feature real-time monitoring and advanced communication systems. Digital substations are more reliable and reduce operational costs by up to 30%, according to the International Electrotechnical Commission (IEC). In order to optimize costs and expedite installation, modular substations are preassembled and pretested prior to their delivery to the site. Additionally, the International Atomic Energy Agency (IAEA) has demonstrated that modular designs can reduce deployment timelines, making them an ideal choice for rapid-track energy initiatives.

Source: Global Wind Energy Council

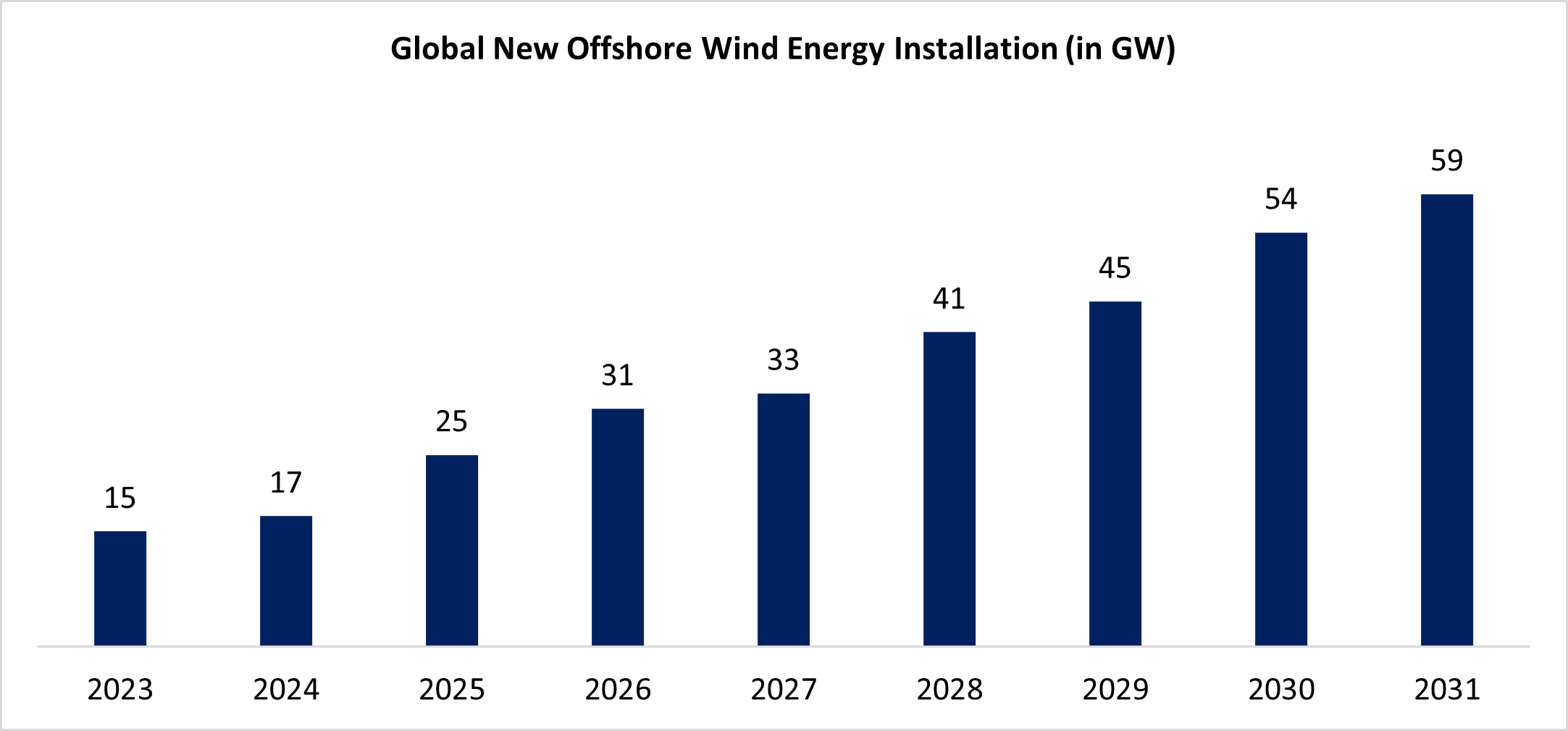

Another breakthrough is the development of floating substations, which support offshore wind farms located in deeper waters. Norway and Japan are pioneering floating substation deployment to leverage deeper offshore wind potential. Additionally, HVDC technology is gaining prominence for its ability to efficiently transmit power over long distances. Substations incorporating HVDC systems are increasingly being used in large-scale offshore wind projects. The Global Wind Energy Council reports that in 2023, the industry connected 11 GW of offshore wind to the grid representing a 24% year-on-year (YoY) increase across the world.

High Initial Investment Costs

Despite significant growth prospects, high initial investment costs remain a major restraint for the offshore substation market. The construction of offshore substations involves substantial capital expenditure, encompassing advanced equipment, underwater cabling and installation in harsh marine environments. According to the International Renewable Energy Agency (IRENA), the average cost of building an offshore substation is $2-3 lakhs per MW of capacity. The financial burden is particularly challenging for emerging markets, where developers often face limited access to capital. The World Bank reports that financing constraints delay offshore wind projects in regions like Africa and Southeast Asia, impeding substation market growth.

Additionally, the complexity of offshore substation design and installation contributes to cost escalation. Projects located in deeper waters or areas with harsh environmental conditions require specialized equipment and expertise, further inflating costs. For instance, floating substations, while innovative, entail higher initial costs due to the use of advanced materials and technologies. Grid integration challenges also add to the financial burden. Establishing connectivity between offshore substations and onshore grids requires extensive infrastructure investments. The European Commission’s Wind Energy The Fact highlight that grid integration costs account for up to 10% of total project expenditures.

Offshore Substation Market Segment Analysis

The global offshore substation market is segmented based on type, voltage type, installation, end-user and region.

Rising Deep-Water Wind Farms Drive the Demand for Floating Offshore Substations

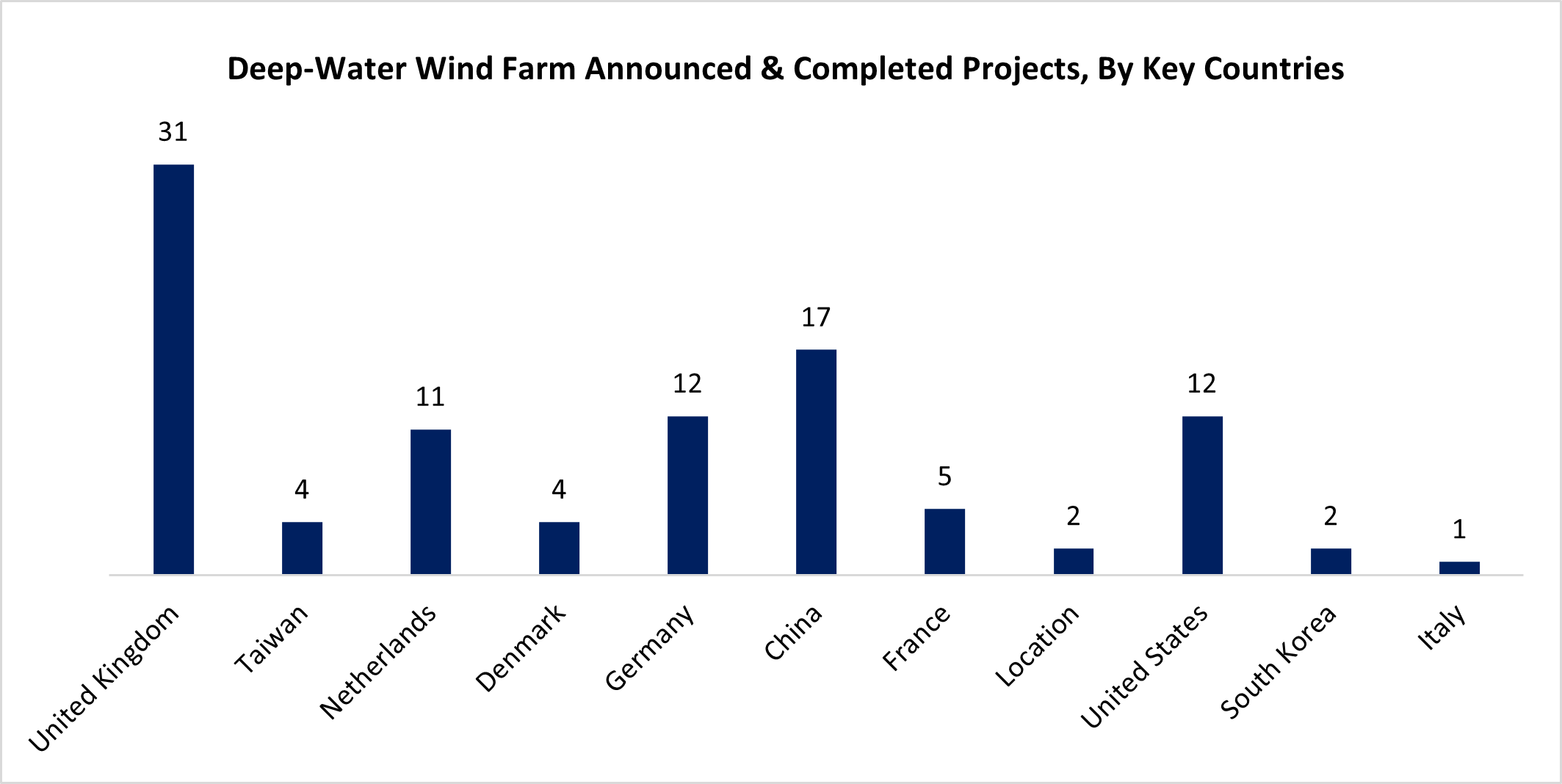

The floating substation segment is emerging as the fastest-growing segment in the offshore substation market. With offshore wind farms increasingly moving to deeper waters, traditional fixed-bottom substations are becoming less viable. Floating substations provide a practical alternative, enabling efficient power transmission from remote locations. According to the Carbon Trust, floating wind projects accounted for 7 GW of global offshore wind capacity in 2023, with projections to reach 70 GW by 2040. This exponential growth is driving demand for floating substations.

Technological advancements are playing a key role in the segment’s expansion. Floating substations are leveraging HVDC technology for efficient power transmission and incorporating digital systems for enhanced operational control. These innovations align with the International Renewable Energy Agency’s (IRENA) emphasis on cost reduction and efficiency improvement in offshore wind infrastructure. The segment’s growth is also supported by partnerships and collaborations. For example, in 2023, Siemens Energy and ABB announced a joint venture to develop next-generation floating substations, aiming to reduce costs and improve scalability.

Source: European Wind Energy Association

Why Offshore Substation Market Matters in 2026

The global energy industry is undergoing a significant transformation as countries accelerate the transition toward renewable power generation and offshore wind deployment.

Offshore substations are becoming a critical component of modern offshore wind infrastructure by enabling efficient power collection, voltage transformation, grid integration, and long-distance electricity transmission from offshore wind farms to onshore grids.

Several macroeconomic and industry-specific factors are driving market growth:

- Increasing government investments in renewable energy infrastructure

- Growing electricity demand and grid modernization initiatives

- Net-zero carbon emission targets across major economies

- Advancements in High Voltage Direct Current (HVDC) transmission technology

- Increasing offshore wind farm sizes and transmission distances

- Strong policy support and renewable energy auctions

- Growing investments in floating offshore wind projects

- Expansion of interconnection networks and offshore power hubs

Analyst View

DataM Intelligence Analyst Perspective

The offshore substation market is transitioning from a supporting infrastructure segment into a strategic enabler of global renewable energy expansion.

The long-term success of the offshore substation market will depend on:

- Offshore wind project pipeline growth

- Grid integration capabilities

- HVDC technology adoption

- Cost optimization and project efficiency

- Reliability in harsh marine environments

- Supply chain resilience

- Regulatory and permitting frameworks

- Digital monitoring and predictive maintenance solutions

- Expansion of floating wind infrastructure

- Strategic partnerships between utilities, EPC contractors, and technology providers

Europe continues to lead the global offshore substation market due to its mature offshore wind sector and ambitious renewable energy targets. China dominates project deployment volume through large-scale offshore wind investments and strong government support. The United States is accelerating offshore wind development along its Atlantic coast, while Japan and South Korea are expanding offshore renewable energy capacity to strengthen energy security. India is emerging as a promising future market supported by renewable energy commitments, coastal infrastructure development, and increasing investments in offshore wind projects.

Market Geographical Share

Robust Renewable Energy Policies and Significant Offshore Wind Capacity Expansions in Asia-Pacific

Asia-Pacific holds the distinction of being the largest region in the offshore substation market, driven by aggressive renewable energy policies and significant offshore wind capacity expansions. According to the Asia Wind Energy Association (AWEA), the region accounted for over 60% of global offshore wind installations in 2023, with China leading the charge. China’s National Energy Administration (NEA) has set a target of achieving 50 GW of offshore wind capacity by 2030, requiring substantial investments in substations to support these projects.

Japan and South Korea are also key players in the region. Japan’s offshore wind roadmap outlines a target of 10 GW by 2030 and 30-45 GW by 2040, emphasizing the development of floating wind farms and advanced substations. Similarly, South Korea’s Green New Deal includes plans for 12 GW of offshore wind capacity by 2030, accompanied by significant investments in high-voltage substations and grid infrastructure.

Technological advancements in substation designs, such as modular and floating substations, are gaining traction in Asia-Pacific. The Carbon Trust highlights that these designs are particularly suitable for the region’s deep-water projects, enhancing efficiency and reducing costs. Additionally, the integration of energy storage systems with offshore substations is becoming a key trend, addressing grid stability challenges associated with renewable energy.

Major Global Players

The major global players in the market include General Electric Company, Aker Solutions, Envision Group, Petrofac Limited, Burns & McDonnell, Hitachi Energy, HSM Offshore Energy BV, SLPE, Hollandia and Siemens. The key players are focusing on strategic partnerships, product innovation and expanding their global presence to increase their market share. The following recent developments highlight the strategies that enhance their competitiveness in the market.

Sustainability Analysis

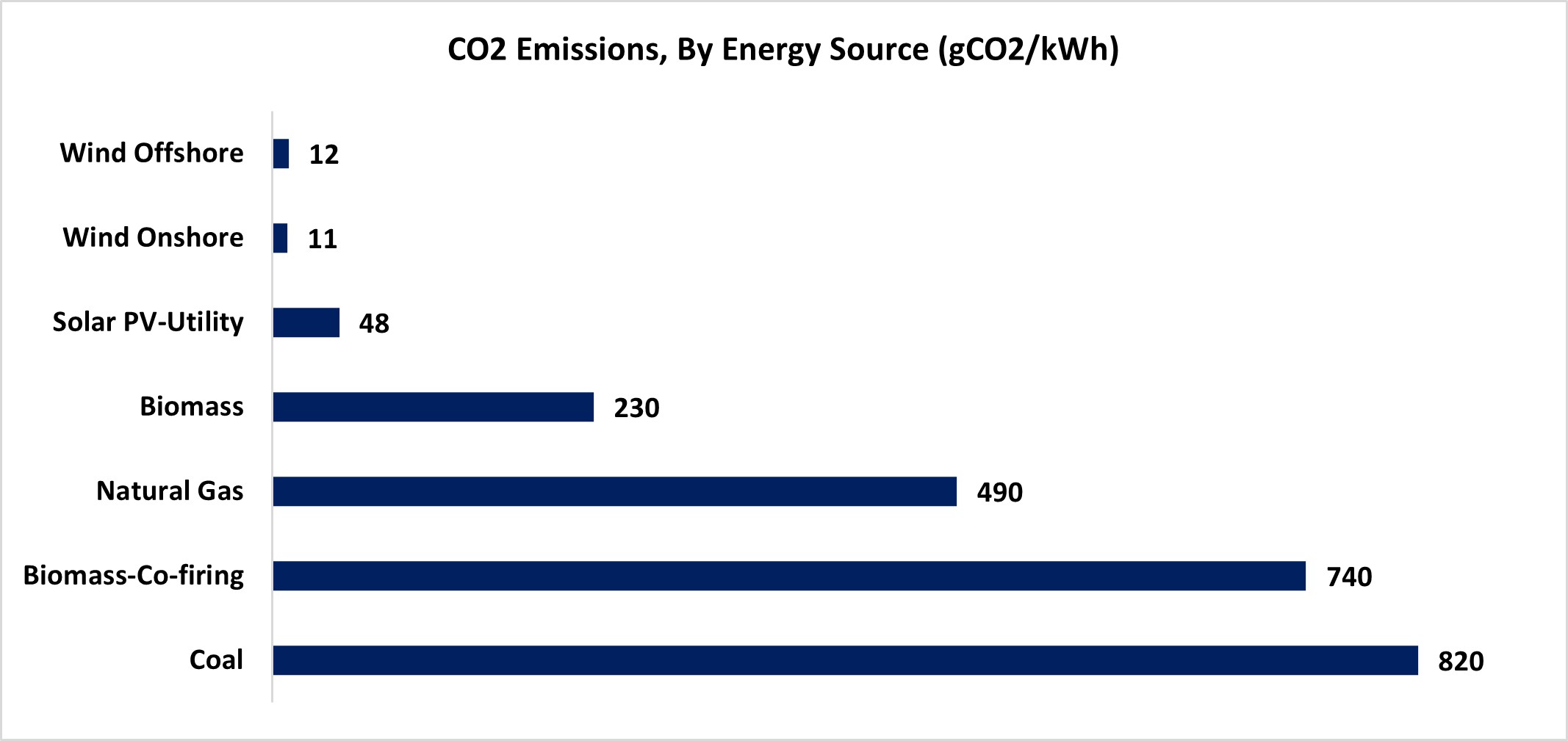

Sustainability is a cornerstone of the offshore substation market, with trends emphasizing eco-friendly practices and technologies. Offshore substations contribute to decarbonization by facilitating the integration of renewable energy into grids. According to the International Renewable Energy Agency (IRENA), offshore wind farms can reduce CO2 emissions by up to 500 grams per kWh compared to fossil fuels. Sustainable materials and designs are gaining traction. Developers are adopting corrosion-resistant and recyclable materials to enhance substation longevity and minimize environmental impact. The European Commission’s Horizon 2020 program has funded several projects focusing on sustainable substation designs, including modular systems that reduce material usage.

Energy efficiency is another focus area. Advanced cooling systems and energy storage integration are being incorporated into substations to optimize performance and reduce energy loss. For example, the German Offshore Wind Energy Foundation highlights that integrating battery storage with offshore substations can improve grid stability and reduce reliance on fossil fuel backup systems. Environmental impact assessments are becoming mandatory for substation projects, ensuring compliance with regulations. UK’s Marine Management Organization (MMO) requires offshore wind developers to conduct environmental impact studies, addressing concerns like marine biodiversity and ecosystem disruption.

Source: World Nuclear Association

Offshore Substation Market Recent Developments

- In May 2026, Hitachi Energy expanded its offshore substation solutions with advanced HVDC technology for large-scale wind projects. The initiative focuses on efficient long-distance power transmission. This supports offshore wind expansion.

- In April 2026, Siemens Energy introduced next-generation offshore substations with modular and digitalized designs. The development enhances installation efficiency and operational reliability. This benefits offshore wind farms.

- In March 2026, GE Vernova strengthened its offshore grid solutions with high-capacity substations and advanced control systems. The innovation focuses on grid stability and integration. This supports renewable energy projects.

Offshore Substation Market Investment & Funding Analysis

Global investments in offshore wind infrastructure continue to rise significantly, driven by expanding renewable energy targets and large-scale offshore wind farm developments.

Major Funding Areas Include:

- Offshore wind transmission infrastructure

- High-voltage substations (HVAC & HVDC)

- Grid integration technologies

- Digital monitoring and control systems

- Floating offshore wind support infrastructure

- Subsea cable networks

- Smart grid connectivity solutions

- Offshore electrification projects

Strategic Recommendations

For Offshore Wind Developers

- Invest in advanced offshore substation technologies

- Strengthen grid connection capabilities

- Expand partnerships with EPC contractors

- Accelerate deployment of digital asset management systems

For Investors

- Focus on high-growth offshore wind infrastructure projects

- Monitor government renewable energy incentives

- Evaluate long-term grid modernization opportunities

- Assess emerging floating wind developments

For Governments

- Streamline offshore permitting processes

- Strengthen renewable energy transmission networks

- Encourage public-private infrastructure investments

- Support offshore wind capacity expansion targets

Why Buy This Offshore Substation Report?

This report helps organizations:

- Understand future offshore energy infrastructure trends

- Identify high-growth investment opportunities

- Benchmark competitors effectively

- Analyze evolving regulatory frameworks

- Optimize market entry strategies

- Evaluate technology advancements

- Assess regional growth opportunities

- Track offshore wind deployment developments

What's Included in the Offshore Substation Report?

The report provides:

- Market size & forecast analysis

- Regional growth outlook

- Competitive intelligence

- Technology benchmarking

- Pricing analysis

- Regulatory assessment

- Supply chain insights

- Market share analysis

- Investment landscape analysis

- Strategic recommendations

- Emerging trends analysis

- Company profiling

Who Should Buy This Report?

This Offshore Substation Market report is ideal for:

- Offshore wind farm developers

- Power transmission companies

- Renewable energy companies

- EPC contractors

- Utility providers

- Grid operators

- Infrastructure investors

- Private equity firms

- Engineering consultancies

- Government agencies

- Energy technology providers

- Market intelligence teams

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies

Key Benefits for Stakeholders

Gain actionable market intelligence:

- Understand offshore energy infrastructure trends

- Analyze global project development strategies

- Evaluate grid modernization initiatives

- Identify strategic growth opportunities

- Benchmark leading market participants

- Improve investment decision-making

- Assess emerging technology adoption

- Track renewable energy expansion opportunities

- Strengthen long-term business planning

- Enhance competitive positioning in the offshore power sector

The global offshore substation market report would provide approximately 70 tables, 65 figures and 250 pages.