Next-Gen Cloud 3.0 Market Overview

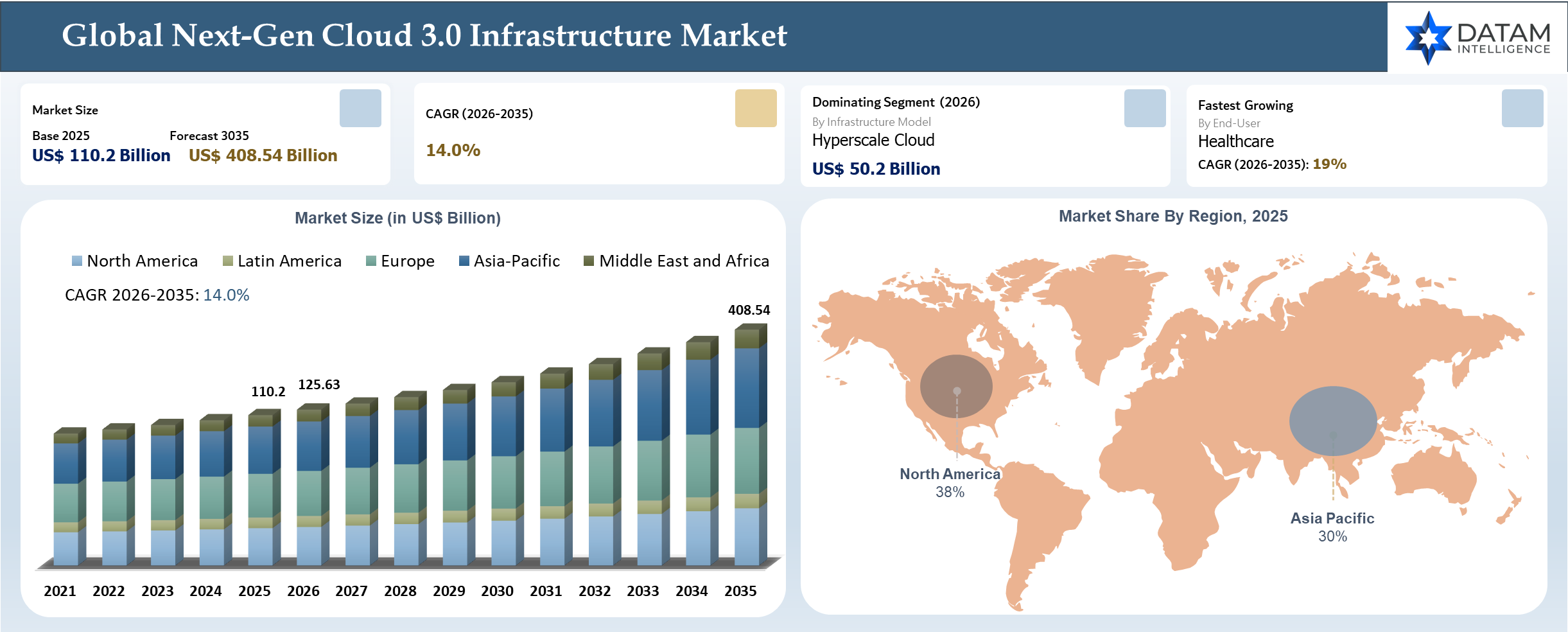

The global Next-Gen Cloud 3.0 Infrastructure market reached US$ 110.2 billion in 2025 and is expected to reach US$ 408.54 billion by 2035, growing with a CAGR of 14% during the forecast period 2026-2035. The Next-Gen Cloud 3.0 Infrastructure market is undergoing a shift in terms of needs for certain operations like AI clusters, sovereign cloud, and low-latency edge deployments that are impacting the design of infrastructure, the location of workloads, and the creation of value propositions. Network optimization, hierarchy of storage, and performance reliability are having an impact on customer evaluation of products as well as areas in which pricing will remain high. The competition is becoming one of implementation with consumers valuing clear unit economics, resilience, and security above all else.

Next-Gen Cloud 3.0 Infrastructure Industry Trends and Strategic Insights

- Demand is shifting toward solutions that can prove measurable value in Hyperscale Cloud and Sovereign Cloud rather than relying on broad platform claims.

- Europe is setting the competitive pace, with Germany and France shaping product design, supply decisions, and go to market priorities.

- Winning suppliers are combining product depth, application know how, and ecosystem partnerships to defend pricing and shorten customer decision cycles.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 110.2 Billion | |

| 2035 Projected Market Size | US$ 408.54 Billion | |

| CAGR (2026-2035) | 14% | |

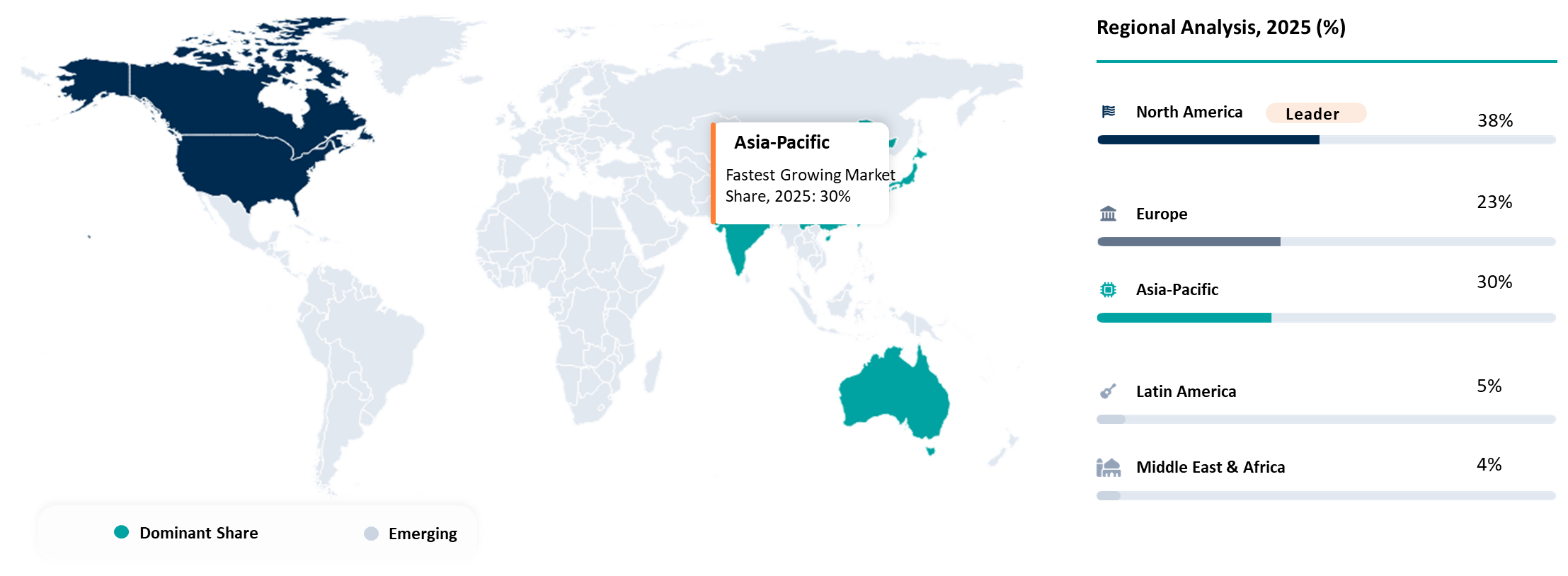

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Infrastructure Model | Hyperscale Cloud, Sovereign Cloud, Distributed Edge Cloud, Hybrid Cloud | |

| By Workload | AI Training, AI Inference, Analytics, Enterprise Applications, Content Delivery | |

| By Hardware Layer | GPU Dense Compute, CPU Compute, High Speed Networking, Storage and Data Fabric, Cooling and Power Systems | |

| By Deployment Environment | Centralized Data Centers, Regional Availability Zones, Edge Facilities, Private Cloud | |

| By End-User | BFSI, Healthcare, Manufacturing, Telecom, Retail and E-commerce, Public Sector | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

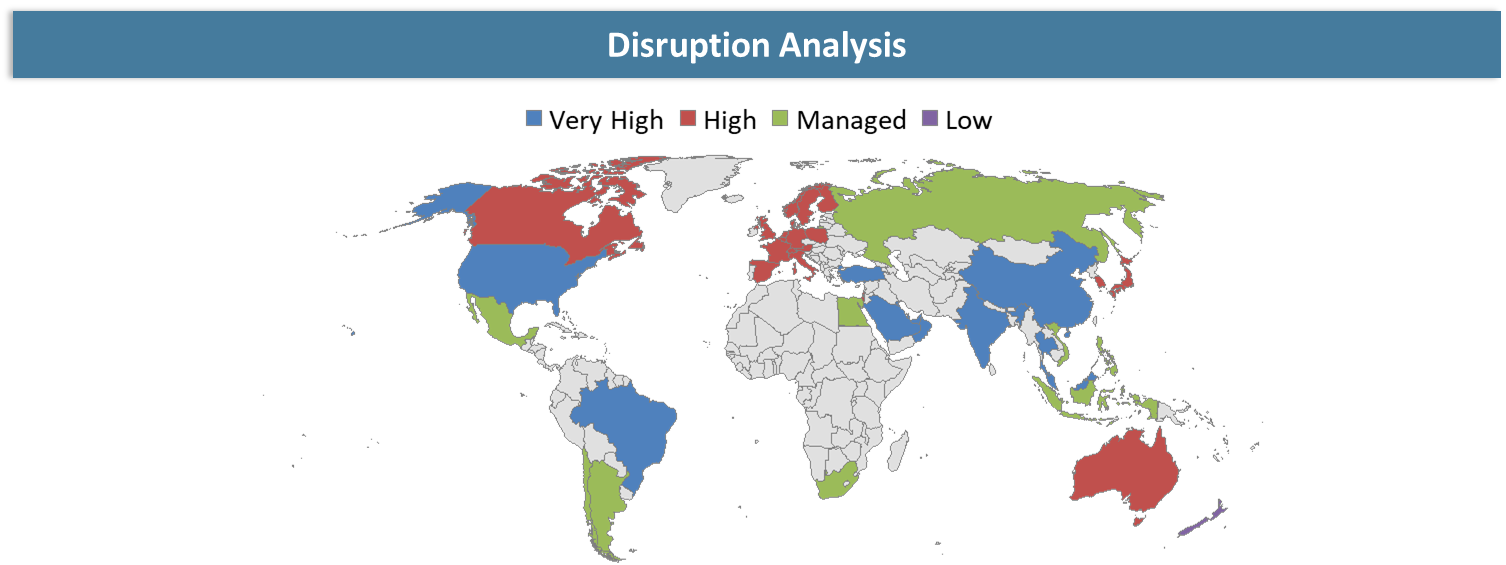

Disruption Analysis

The disruption that exists in the next-gen cloud 3.0 infrastructure market involves the evolution from features-first competitive positioning to results-oriented business value delivery. As more buyers look at the ability of the vendor solution to integrate quickly, operate reliably in production environments, and achieve measurable ROI within expected timelines, the ability to compete based on technical specifications becomes less relevant. Vendors have to show tangible results.

Additionally, a disruptive trend that occurs relates to changes in the commercial framework and how vendors gain and retain their customers. In today’s environment, it is critical for vendors to control adjacent processes, service layers, and the infrastructure environment. However, while technology remains equal, the vendors' ability to deliver reliable and resilient operations, ensure supply chain assurance, and provide continuous performance measurement after deployment becomes essential.

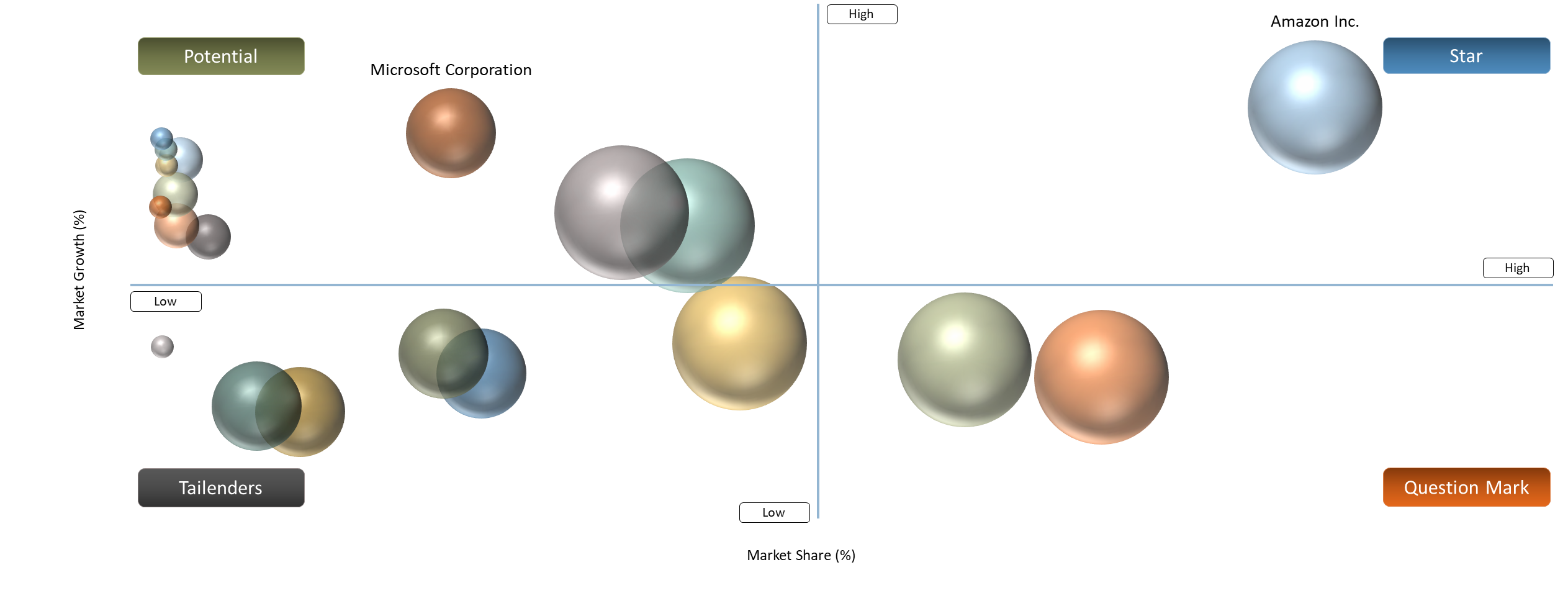

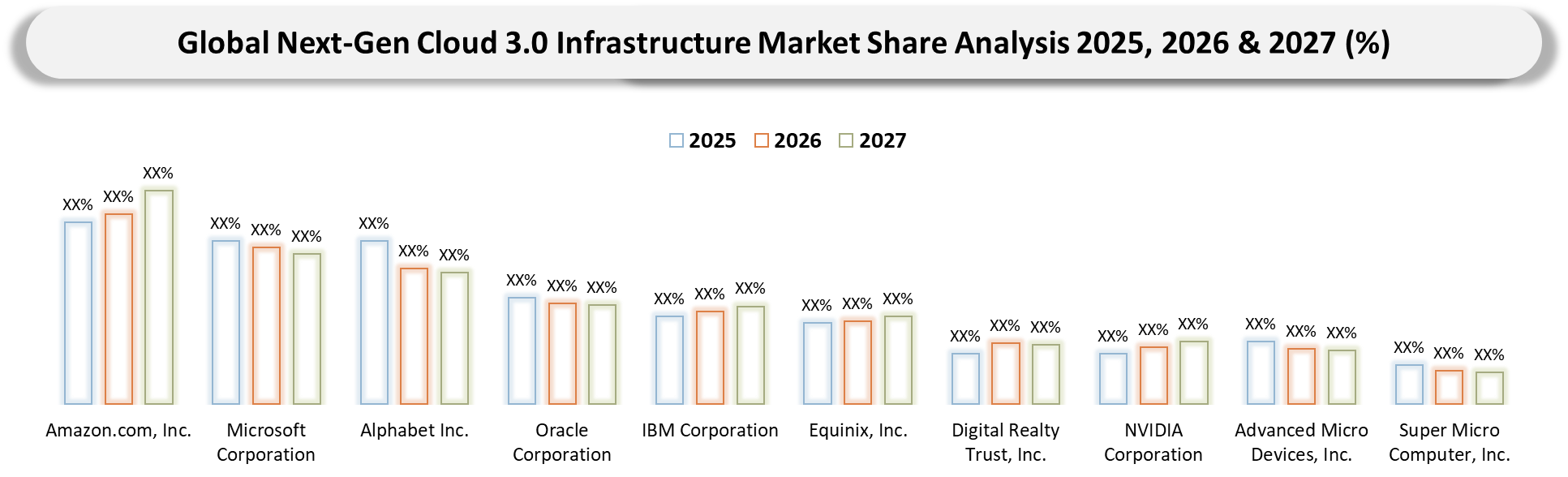

BCG Matrix: Company Evaluation

In the context of the BCG Matrix, Stars will be companies that have both high demand traction and an ecosystem position. The leaders in this group, such as Amazon.com, Inc., Microsoft Corporation, and Alphabet Inc., excel due to the alignment of their product offering with wide distribution, integration, and recurring revenues. These businesses have a competitive advantage in defining customers' expectations for integrated cloud services.

The companies that have achieved large-scale penetration, global presence, and stability in their channel ecosystems, maintaining their margin levels through service agreements and switching costs. The Question Marks consist of specialist or adjacent competitors serving segments like hyperscale cloud and sovereign cloud. Growth opportunities in these segments exist and can be leveraged if the scale can be reached and demonstrated to stakeholders. Lack of uniqueness or ecosystem positioning might move vendors.

Market Dynamics

Enterprise Shift Toward Distributed and Hybrid Cloud Architectures

The trend toward distributed and hybrid cloud models will be a significant catalyst as companies seek to improve their flexibility, resilience, and efficiency in terms of workload deployment across various platforms. Companies will tend to migrate their workloads between different models of cloud - public cloud, on-premises infrastructure, and edge nodes as well as improve performance and reduce latency.

The shift will fuel increased interest in the development of interoperable platforms and efficient management of data between different systems. Those companies that manage to provide their customers with flexible deployment models and high performance through integrated platforms will win.

High Capital Intensity and Infrastructure Deployment Costs

High capital outlay is still an important limitation, especially when developing the next generation of cloud computing architecture, like data centers, edge sites, and high-performance computing setups. Such investments will put off growth plans, and only those organizations with deep pockets or long-term funding options will be able to participate.

Moreover, running costs such as power, maintenance, and upgrades further add to operating costs and return on investment cycles. Such constraints make it difficult for newcomers to enter and deploy cloud technologies.

Segmentation Analysis

The global Next-Gen Cloud 3.0 Infrastructure market is segmented based on infrastructure model, workload, hardware layer, deployment environment, end user and region.

Infrastructure Model Driving Market Clarity and Sizing Accuracy

Analysis of the next-generation cloud 3.0 infrastructure market can best be conducted using the Infrastructure Model because it allows buyers' decision-making process to be understood based on what they perceive to be true in terms of trade-offs as opposed to vendors' market positioning. It creates clarity on how budgeting, pricing, competition among suppliers, and deployment should be analyzed.

In terms of sizing, this market can be considered very well-defined in that purchases are clearly identifiable, products offered can be categorized, and applications served can also be identified. As compared to the broader strategic approach, this market lends itself better to bottom-up analysis.

Geographical Penetration

Asia-Pacific Accelerating Cloud 3.0 Adoption Through AI Expansion, Edge Deployment, and Digital Transformation Initiatives

The Asia-Pacific region is the fastest-growing region within the cloud 3.0 infrastructure industry due to its quick process of digitalization, internet economy growth, and government support towards developing AI and cloud ecosystem. It is evident that all nations within this region have progressed from just using cloud to incorporating AI and edge computing into their operations.

On the other hand, the growth of both hyperscale data centers and edge infrastructure is occurring in tandem to enable real time computing and applications with low latency. With the investments in 5G, Internet of Things (IoT), and digital infrastructure growing at an increasing pace, combined with the availability of a robust hardware manufacturing industry in the region, there are reduced costs and less dependency on supply.

China Next-Gen Cloud 3.0 Infrastructure Market Trends

China is dominant in the Asia-Pacific cloud 3.0 infrastructure market due to its widespread adoption of cloud computing, its well-defined government policy, and its integrated digital ecosystem. China has adopted many data centers and hyperscale centers to allow AI applications in manufacturing, smart cities, surveillance, and e-commerce, leading to consistent infrastructure needs.

The approach taken by China in building its economy is driven by massive deployment of AI workloads, with consistent investments being made in data centers and semiconductors made within China itself. The emphasis placed on the sovereignty of data has led to the growth of sovereign and private clouds. Also, the growth of smart cities has led to the use of cloud-edge architectures.

India Next-Gen Cloud 3.0 Infrastructure Market Outlook

The exponential growth in cloud 3.0 infrastructure in India, due to the migration from traditional IT architecture to hybrid clouds and intelligent cloud systems for sectors including BFSI, healthcare, retail, and telecom. Companies are moving towards scalable cloud solutions to implement machine learning algorithms and big data analytics and applications for enterprises, while digital initiatives by the government are driving more investments in regional data centers.

Edge computing is further being fueled by expanding telecom services, increased data consumption, and 5G readiness, making it possible for companies to run latency-sensitive and real-time applications. The vibrant developer community in India and strong IT service industry are driving innovation in implementation. Diverse use cases are continuously driving demand for flexible cloud models.

Competitive Landscape

Competition in the next-gen cloud 3.0 infrastructure market is defined by a split between scale players and focused specialists. Large vendors such as Amazon.com, Inc., Microsoft Corporation, and Alphabet Inc. use portfolio breadth, channel reach, and account access to shape category expectations, while specialist vendors try to win through product depth, faster implementation, or sharper use case alignment. As the market matures, the strongest positions are being built by companies that combine technical credibility with surrounding services, ecosystem partnerships, and support depth.

Market positioning is increasingly influenced by how well suppliers defend the full customer journey. Product quality still matters, but so do onboarding friction, integration capability, data or workflow control, application engineering, and lifecycle support. Vendors that can anchor around high value segments such as Hyperscale Cloud and Sovereign Cloud are generally in a better position to protect pricing and expand share.

Key Developments

- Apr 2026: European Commission awarded €180M cloud contract to regional providers to accelerate sovereign cloud infrastructure and reduce dependency on non-European hyperscalers.

- September 2025: Tata Consultancy Services partnered with Centre for Development of Advanced Computing to build India’s sovereign cloud infrastructure enabling data localization and AI-ready national cloud ecosystem.

- February 2026: CoreWeave increased capex to scale GPU-based AI cloud infrastructure and data center capacity for next-gen compute demand.

- October 2025: Oracle partnered with AMD to deploy large-scale GPU clusters for AI-driven cloud infrastructure expansion.

- October 2025: Gcore launched AI Cloud Stack enabling enterprises to build private and hybrid AI cloud infrastructure on GPU clusters.

- April 2026: Amazon Web Services partnered with Lumen Technologies to enhance cloud interconnect infrastructure for low-latency and private enterprise connectivity.

- April 2026: xAI expanded GPU cloud infrastructure by enabling external access to its compute clusters, positioning itself as an emerging AI cloud provider.

Why Choose DataM?

- Technological Innovations: Explores advancements shaping the next-gen cloud 3.0 infrastructure market, including AI-driven workload orchestration, edge-cloud integration, software-defined infrastructure, and energy-efficient data center design. These innovations are improving scalability, latency management, and cost efficiency across enterprise and hyperscale environments.

- Product Performance & Market Positioning: Evaluates how leading vendors perform across enterprise, hyperscale, and edge deployments, comparing factors such as workload handling, uptime reliability, scalability, security, and integration capabilities. Highlights how providers differentiate through platform depth, ecosystem strength, and service quality across industries.

- Real-World Evidence: Highlights use cases across sectors such as BFSI, healthcare, telecom, retail, and smart cities, demonstrating improvements in processing speed, operational efficiency, data utilization, and customer experience. Emphasizes measurable outcomes such as reduced latency, optimized workloads, and enhanced system resilience.

- Market Updates & Industry Changes: Tracks key trends including hyperscale data center expansion, edge infrastructure growth, sovereign cloud adoption, regulatory changes, and increasing investments across regions such as North America, Asia-Pacific, China, and India. Reflects how evolving demand patterns are reshaping infrastructure strategies.

- Competitive Strategies: Analyzes how leading vendors are strengthening market position through partnerships, multi-cloud integration, localized infrastructure, and platform-based offerings. Focuses on strategies such as ecosystem building, AI integration, and service-led differentiation to capture long-term enterprise value.

- Pricing & Market Access: Explains pricing structures including pay-as-you-go, subscription-based, and hybrid cost models across cloud and edge deployments. Reviews how pricing flexibility, financing options, and regional infrastructure availability influence enterprise adoption and vendor competitiveness.

- Market Entry & Expansion: Identifies growth potential in emerging markets driven by digital transformation, 5G rollout, and rising enterprise cloud adoption. Outlines expansion strategies through regional data centers, partnerships, and service optimization to scale operations and improve market penetration.

Target Audience

- Product strategy teams

- Corporate strategy and market intelligence teams

- Business development leaders

- Sales and channel leaders

- Investors and private equity firms

- Procurement and sourcing teams

- Technology and operations leaders

- Consulting and advisory teams