Multilayer Flexible Packaging Market Size

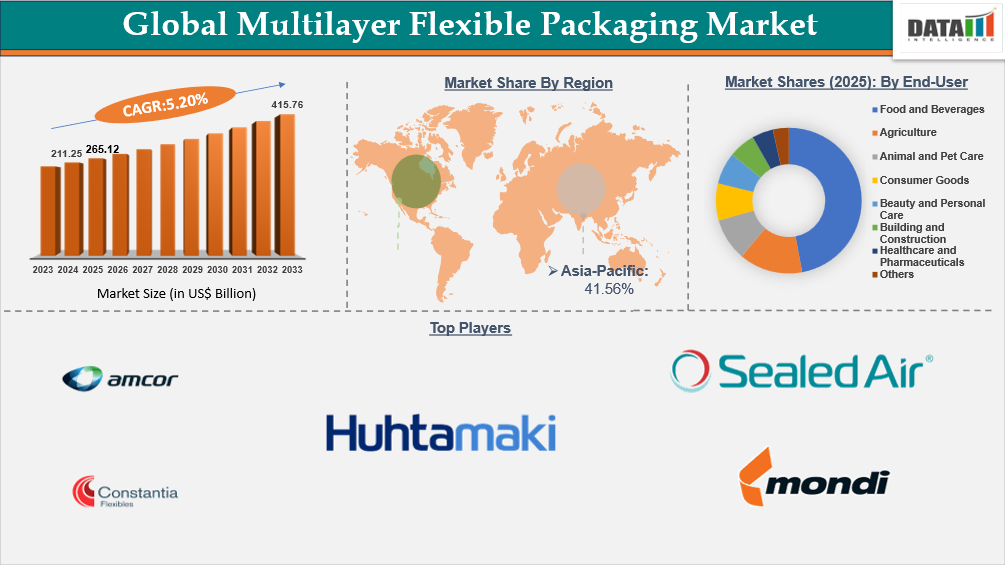

The global multilayer flexible packaging market size was reached US$ 256.12 billion in 2025 and is expected to reach US$ 415.76 billion by 2033, growing with a CAGR of 5.20% during the forecast period 2026-2033. The global multilayer flexible packaging market is expanding due to rising demand for lightweight, high-barrier, and convenience-oriented packaging solutions across food, beverage, and consumer goods applications. Manufacturers are increasingly shifting toward multilayer structures to extend shelf life, reduce material usage, and support efficient transportation while maintaining product protection and usability.

Packaging leaders are actively responding to this shift. For example, major flexible packaging producers have accelerated the launch of downgauged, high-performance multilayer films and recyclable mono-material structures in recent years, targeting ready-to-eat foods, snacks, beverages, and e-commerce applications. The product introductions and capacity expansions demonstrate that global packaging companies view advanced multilayer flexible packaging as a strategic solution to meet evolving convenience, performance, and logistics requirements across end-use industries.

Multilayer Flexible Packaging Industry Trends and Strategic Insights

- Asia-Pacific is the fastest-growing region in the multilayer flexible packaging market, capturing a share of 41.56% in 2025.

- By end-user, the food and beverages are projected to be the largest market, holding a significant share of about 40% in 2025.

Global Multilayer Flexible Packaging Market Size and Future Outlook

- 2025 Market Size: US$ 265.12 Billion

- 2033 Projected Market Size: US$ 415.76 Billion

- CAGR (2026-2033): 5.20%

- Largest Market: Asia-Pacific

- Fastest Market: Asia-Pacific

Key Takeaways

- The multilayer flexible packaging market is expanding steadily as brands shift toward high-barrier, lightweight packaging formats that extend shelf life, reduce material usage, and improve logistics efficiency across food, beverage, and healthcare supply chains.

- Sustainability is becoming the central design constraint. Traditional multi-material laminates are increasingly being challenged by recyclable mono-material structures, bio-based films, and downgauging strategies that aim to meet circular economy and regulatory packaging mandates.

- Food and beverage remains the dominant application segment. Rising demand for ready-to-eat meals, frozen foods, snacks, and convenience packaging is accelerating adoption of multilayer films that provide oxygen, moisture, and aroma barrier protection.

- Pharmaceutical and healthcare packaging is gaining strategic importance. High-barrier multilayer structures are increasingly used for blister packs, sterile medical pouches, and sensitive drug formulations that require strict contamination control and extended stability.

- E-commerce and modern retail formats are reshaping packaging requirements. Demand is increasing for durable, puncture-resistant, and tamper-evident flexible packaging that can withstand long logistics chains while maintaining product integrity and branding.

- Material innovation is intensifying across polymer blends and coating technologies. Advanced extrusion, adhesive-less lamination, and nanocoatings are being deployed to balance performance, recyclability, and cost efficiency in high-volume production.

- Asia-Pacific remains a key manufacturing and consumption hub. Strong food processing industries, expanding pharmaceutical production, and large-scale packaging converters in China, India, Japan, and Southeast Asia are driving regional market leadership.

- Regulatory pressure is influencing packaging redesign globally. Governments and brand owners are pushing extended producer responsibility (EPR), plastic reduction targets, and recyclability labeling standards, forcing structural changes in multilayer packaging architectures.

Market Scope

| Metrics | Details |

| By Type | Spout Pouch, Standup Pouch, Retort Pouch, Flat Pouches, Flat Bottom Pouches, Quad Seal Pouches, Sachets and Stick Packs, Vacuum Pouches, Shrink Sleeves and Wraps, Rollstock or Rewind Films, Lidding Films (Roll-Fed), Large-Format or Bulk Pouches, Others |

| By Material | Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), Polyamide (PA or Nylon), Aluminum Foil, Paper-Based Materials, Multi-Material Laminates, Bio-Based and Compostable Materials, Polystyrene (PS), Others |

| By Layer | 2 Layers, 3 Layers, 4 Layers, 5+ Layer Structures |

| By End-User | Food and Beverages, Agriculture, Animal and Pet Care, Consumer Goods, Beauty and Personal Care, Building and Construction, Healthcare and Pharmaceuticals, Home Care, e-Commerce and Logistic Packaging, Industrial Packaging, Others |

| By Sustainability | Recycled Content, Mono-Material Paper, Mono-Material Plastic Packaging, Paper-Based Mono-Material Packaging, Light-Weighting or Downgauging, Bio-Based Materials, Carbon Footprint Reduction, Recyclable High-Barrier Structures |

| By Technology | Blown Film, Cast Film Extrusion, Flexo Printing, Extrusion Coating, Adhesive Lamination, Solvent-Free Lamination, Gravure Printing, Digital Printing, Barrier Coating Technologies, Others |

| By Region | North America, Latin America, Europe, Asia-Pacific, Middle East and Africa |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Market Dynamics

Growing Emphasis on Convenience-Driven and Lightweight Packaging Solutions

The multilayer flexible packaging market is being increasingly driven by the rising demand for convenience-driven and lightweight packaging solutions, as food manufacturers and consumer brands adapt to changing consumption patterns and sustainability priorities. By 2023, nearly 65% of food products globally featured tamper-evident and resealable packaging, reflecting strong demand for portability, safety, and ease of use. Advances in high-performance packaging technologies have also contributed to average shelf-life extensions that lifted perishable food sales by around 15%, supporting wider adoption of multilayer flexible formats.

The rapid growth of e-commerce and direct-to-consumer food platforms has further accelerated packaging innovation. In 2023, online food brands increased investments in packaging innovation by approximately 35%, with a strong focus on lightweight, durable, and transit-resistant packaging structures. At the same time, lightweighting initiatives across flexible packaging formats are delivering measurable sustainability gains, with raw material use and environmental impact reduced by up to 50% through downgauging and optimized multilayer film designs. Together, these trends underscore how convenience-focused functionality and lightweight engineering are emerging as key growth drivers for the multilayer flexible packaging market.

Why This Report Matters in 2026

Packaging buyers and brand owners enter 2026 under growing pressure to balance performance, sustainability, and cost efficiency in a rapidly tightening regulatory environment. The multilayer flexible packaging market is no longer viewed only as a materials upgrade decision, but as a strategic lever for reducing food waste, extending shelf life, improving logistics efficiency, and meeting circular economy commitments. As demand rises across food & beverage, pharmaceuticals, personal care, and industrial applications, stakeholders need clearer visibility into material innovation trends, recyclability challenges, and evolving compliance standards shaping purchasing decisions.

Supply chain and product development teams are also facing a structural transition in packaging design architecture. Organizations are actively evaluating trade-offs between traditional multilayer laminates, mono-material flexible packaging, recyclable barrier films, and bio-based alternatives. Each option carries implications for barrier performance, machinability, cost structure, recycling compatibility, and downstream recovery systems. A strong market perspective helps decision-makers compare material pathways and technology readiness levels rather than treating flexible packaging as a uniform category.

Sustainability mandates and regulatory scrutiny are becoming key drivers of procurement strategy in 2026. Governments, retailers, and global brands are increasingly enforcing extended producer responsibility (EPR), recycled content targets, and plastic reduction commitments, pushing converters and material suppliers to accelerate innovation. At the same time, companies across FMCG, healthcare, and industrial packaging require benchmark insights on regional demand shifts, key application segments, competitive positioning, and technology adoption curves. This report helps stakeholders identify where growth is concentrated, which material systems are gaining traction, and how the value chain is adapting to next-generation packaging requirements.

Complexity in Recycling and End-of-Life Management

One of the key restraints in the global multilayer flexible packaging market is the complexity of recycling and end-of-life management for multilayer structures. Multilayer flexible packaging relies on combinations of different materials such as polyethylene, polypropylene, aluminum foil, and barrier polymers to achieve strength, shelf life, and product protection. While these structures deliver superior performance, the bonding of dissimilar materials makes mechanical recycling technically challenging and economically less viable.

Recycling infrastructure in many regions remains optimized for mono-material streams, limiting the effective recovery of multilayer packaging waste. As a result, a significant share of multilayer flexible packaging continues to be diverted to landfills or energy recovery rather than circular reuse. Increasing regulatory pressure on plastic waste reduction, extended producer responsibility obligations, and recycling targets further amplify compliance costs and design constraints for manufacturers. The recycling complexity creates structural challenges for material selection, increases development costs, and slows the adoption of multilayer flexible packaging in sustainability-focused markets.

Segment Analysis

The global multilayer flexible packaging market is segmented based on type, material, layer, end-user, sustainability, technology, and region.

Rising Demand for High-Barrier, Shelf-Stable Packaging Drives Food and Beverage Applications

The food and beverages segment is driving consistent demand in the multilayer flexible packaging with a share of 40%, as brands require packaging solutions that ensure extended shelf life, product safety, and convenience while reducing material usage. Multilayer flexible structures provide critical barrier protection against oxygen, moisture, light, and contamination, making them essential for ready-to-eat meals, frozen foods, snacks, dairy products, sauces, and beverages. Lightweight formats such as stand-up pouches, retort pouches, lidding films, and rollstock films enable portion control, portability, and efficient transportation, which explains their widespread adoption across packaged food categories.

Packaging manufacturers are actively expanding high-barrier and convenience-focused solutions to meet evolving food industry requirements. For instance, in September 2024, Nestlé, a Switzerland-based global food and beverage company, introduced new paper-based high-barrier sustainable packaging innovations for multiple product categories, including paperboard canisters that reduce plastic usage by up to 90% and fully recyclable high-barrier paper refill packs for coffee that cut packaging weight by 97% while preserving product freshness and quality, marking a significant step toward science-based, recyclable, and circular packaging solutions across its global portfolio

Rising Demand for Durable and Lightweight Flexible Packaging in Pet Food and Animal Care Applications

The pet food and animal care segment is emerging as a key growth driver for the multilayer flexible packaging market, supported by rising pet ownership, increasing premiumization of pet nutrition, and growing demand for durable, lightweight, and high-barrier packaging formats. Pet food products, particularly dry kibble, treats, and nutritional supplements, require packaging solutions that deliver strong moisture, oxygen, and grease barriers while maintaining puncture resistance and transportation efficiency. In addition, lightweight flexible packaging helps reduce logistics costs and improves handling efficiency across both e-commerce and traditional retail channels.

Packaging manufacturers are responding with reinforced, recyclable, and performance-optimized solutions tailored to pet food applications. For instance, in July 2024, Mondi Group, a UK-based global packaging and paper manufacturer, unveiled its FlexiBag Reinforced range of mono-PE-based recyclable flexible packaging solutions designed specifically for the pet food industry. The product line offers enhanced mechanical strength, improved puncture resistance, stiffness, and sealability, along with customizable barrier properties to maintain freshness and product integrity for both dry and wet pet food products. The launch marks a significant advancement in sustainable, high-barrier multilayer flexible packaging for premium pet nutrition applications.

Analyst View

DataM Intelligence Analyst Perspective

The multilayer flexible packaging market is transitioning from a cost-driven packaging segment into a high-performance materials ecosystem, shaped by sustainability mandates, food safety requirements, and rapid growth in e-commerce and consumer convenience products.

The long-term growth trajectory of the multilayer flexible packaging market will depend on:

- Rising demand for extended shelf-life and high-barrier packaging solutions across food, beverage, and pharmaceuticals

- Increasing regulatory pressure to reduce plastic waste and improve recyclability of multilayer structures

- Expansion of flexible packaging in ready-to-eat, frozen food, and personal care applications

- Technological advancements in co-extrusion, lamination, and bio-based polymer layers

- Cost efficiency and material optimization in multi-material film production

- Development of mono-material alternatives and recyclable barrier films

- Growth of e-commerce-driven lightweight and durable packaging formats

Asia-Pacific continues to dominate demand growth, led by China, India, Japan, and Southeast Asia, driven by expanding food processing industries, urbanization, and rising consumption of packaged goods. North America is focusing on sustainable packaging innovation and regulatory compliance, while Europe is leading in circular economy initiatives and recyclable multilayer film development.

Companies that can deliver recyclable high-barrier films, advanced mono-material multilayer structures, and scalable sustainable packaging technologies will be best positioned to capture long-term growth in the evolving global packaging transformation landscape.

Geographical Penetration

Rising Adoption of Convenience-Driven Food and Beverage Packaging in Asia-Pacific

The Asia-Pacific multilayer flexible packaging market represents both the largest consumption base and the fastest-growing region globally, driven by rising demand for ready-to-eat and processed foods across rapidly urbanizing economies. Changing lifestyles, increasing workforce participation, and growing disposable incomes are accelerating the shift toward packaged, convenience-oriented food products. The transition is strengthening demand for lightweight, space-efficient, and high-barrier multilayer flexible packaging formats that support extended shelf life, portability, and cost-effective distribution.

Expanding e-commerce penetration, improving cold-chain infrastructure, and the rapid growth of modern retail channels are further reinforcing the adoption of multilayer flexible packaging formats across food, personal care, and household product categories. For instance, in September 2024, Pakka Limited, an India-based sustainable packaging company, launched a new range of compostable flexible packaging solutions for the food and beverages sector, featuring multiple paper-based and non-metallized compostable structures with superior barrier properties, heat and cold sealability, lightweight performance, and food-grade certification marking a significant step toward eco-friendly, high-performance multilayer flexible packaging for chocolates, snacks, granola bars, nuts, tea, and other FMCG products.

China Multilayer Flexible Packaging Market Insights

China remains the largest contributor to Asia-Pacific growth, supported by its massive consumer base, integrated manufacturing ecosystem, and expanding packaged food and beverage sector. Rising consumption of snacks, frozen foods, dairy products, sauces, and ready meals is driving demand for high-performance multilayer films that offer moisture, oxygen, and light barriers. The rapid expansion of e-commerce and food delivery platforms is increasing the need for lightweight, durable, and protective packaging formats, while sustainability initiatives are encouraging material reduction, downgauging, and the development of recyclable multilayer structures.

India Multilayer Flexible Packaging Market Outlook

India represents one of the fastest-growing markets within Asia-Pacific, supported by strong growth in the food processing industry and rising consumption of packaged and ready-to-eat foods. In 2024, the food processing sector accounted for approximately 8.80% of Gross Value Added (GVA) in manufacturing and 8.39% in Agriculture, while contributing 13% of India’s exports and 6% of overall industrial investment. GVA from food processing increased from Rs. 1.61 lakh crore in 2015–16 to Rs. 1.92 lakh crore in 2022–23, reflecting sustained and broad-based sectoral expansion. The growth is translating into rising demand for affordable, lightweight, and flexible packaging across snacks, dairy, staples, ready meals, personal care, and home care products. The widespread use of single-serve and small-format packs, combined with the expansion of organized retail and e-commerce logistics, is accelerating the shift from rigid to multilayer flexible packaging formats that offer superior cost efficiency and transportation advantages.

Sustainability Analysis

The global multilayer flexible packaging (MFP) market has a mixed but progressively improving sustainability profile, as flexible, lightweight packaging formats enable significant material efficiency, lower transportation emissions, and reduced resource use compared to rigid packaging alternatives. By replacing heavier materials such as glass, metal, and rigid plastics, multilayer flexible packaging reduces packaging weight per unit, improves pallet efficiency, and lowers fuel consumption across supply chains, particularly in food, beverage, and consumer goods applications.

The primary environmental impact of MFP stems from complex multilayer structures that combine multiple polymers, aluminum foil, or barrier layers, which complicate recycling and contribute to end-of-life waste challenges. However, sustainability initiatives are accelerating across the industry. For instance, in November 2024, Jindal Films Europe, a Belgium-based flexible packaging film manufacturer, committed to launching 5 to 10 new sustainable flexible film innovations annually, focusing on recyclable mono-material and high-barrier multilayer structures such as BOPE and mono-PP films designed to replace PET and aluminum foil in food and consumer packaging, marking a significant step toward improved sustainability, recyclability, and circular-economy alignment in multilayer flexible packaging solutions.

Competitive Landscape

- The global multilayer flexible packaging market is characterized by a competitive landscape that includes both established and regional players.

- Key players include Amcor plc, Sealed Air Corporation, Constantia Flexibles, Huhtamaki Oyj, Mondi Group, Sonoco Products Company, Winpak Ltd., Coveris Holdings S.A., ProAmpac, Smurfit Kappa Group

Recent Developments

- May 2026: Amcor plc expanded its multilayer flexible packaging production capacity in Asia-Pacific, focusing on recyclable barrier films and high-performance sustainable packaging solutions for food and healthcare applications.

- April 2026: Sealed Air Corporation introduced next-generation multilayer flexible packaging solutions with enhanced barrier protection and reduced plastic usage, supporting global circular economy targets.

- March 2026: Berry Global Group Inc. announced advancements in multilayer film technologies designed for improved recyclability and lightweight packaging across FMCG and personal care sectors.

- February 2026: Mondi Group strengthened its sustainable multilayer flexible packaging portfolio by integrating mono-material structures aimed at improving recyclability and reducing environmental impact.

- January 2026: Huhtamaki Oyj expanded its multilayer flexible packaging innovations for food packaging applications, focusing on extended shelf-life, barrier performance, and reduced material complexity.

- December 2025: Uflex Ltd. increased investments in high-barrier multilayer films and aseptic packaging solutions to support rising demand in processed food and pharmaceutical sectors.

- November 2025: Coveris Holdings S.A. advanced multilayer flexible packaging development with recyclable polymer blends and improved seal strength for industrial and retail packaging applications.

- October 2025: Toray Industries Inc. enhanced multilayer film technologies focusing on high-barrier resins and advanced polymer engineering for food preservation and industrial packaging uses.

- September 2025: Jindal Poly Films Ltd. expanded multilayer BOPP and BOPET film production capacity to meet increasing global demand for flexible and cost-efficient packaging solutions.

- August 2025: Taghleef Industries introduced new multilayer flexible packaging film solutions with improved oxygen and moisture barrier properties targeting food, beverage, and healthcare packaging markets.

Why Choose DataM?

- Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies