Milling Tools Market Overview

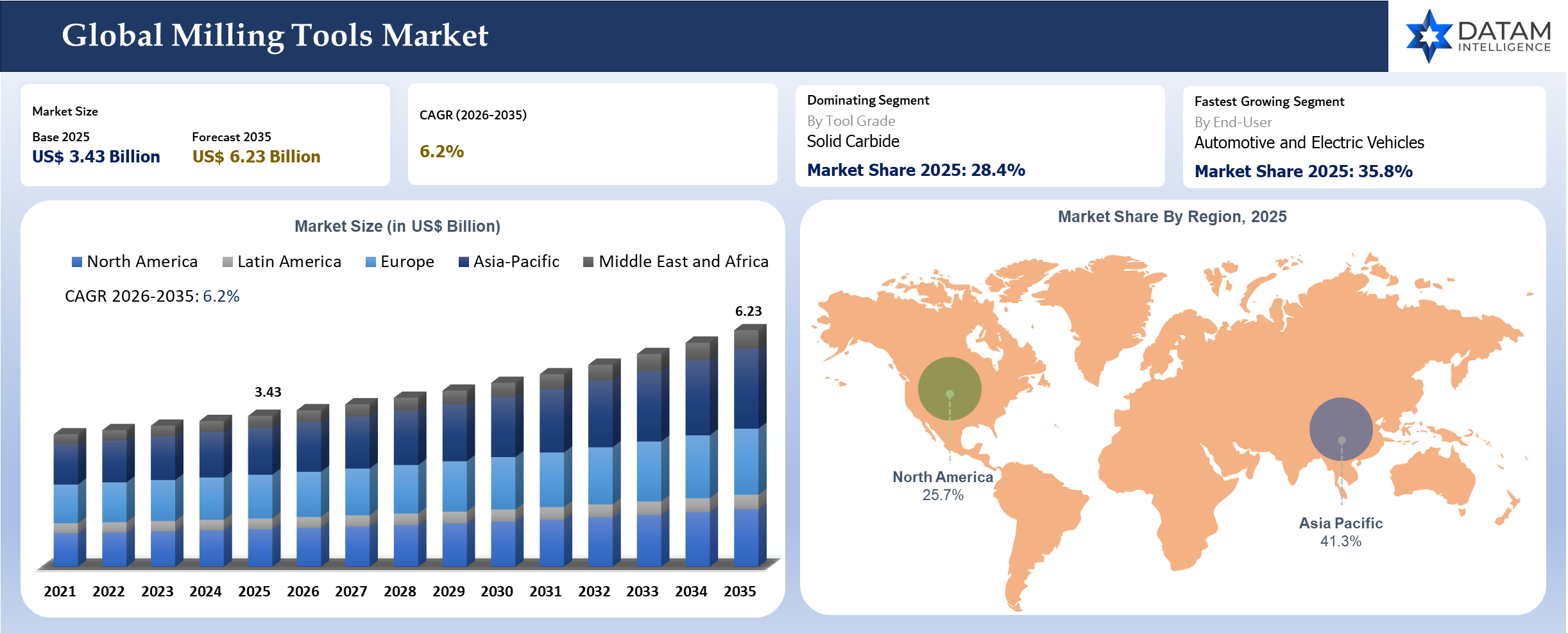

The global milling tools market reached US$ 3.43 billion in 2025 and is expected to reach US$ 6.23 billion by 2035, growing with a CAGR of 6.2% during the forecast period 2026-2035. Growing demand for precision machining due to their increasing use in sectors such as automotive, aerospace, defense, electronic, healthcare equipment, and industries has significantly influenced the adoption of milling machines in many parts of the world. A rising inclination among many manufacturers towards implementing CNC multi-axis machinery and manufacturing facilities where milling cutters, indexable insert cutting tools, and carbide mills contribute significantly in terms of accurate dimensioning and enhanced production efficiency. Use of light weight material including titanium, aluminum, and carbon-fiber in the construction of aerospace products and electric vehicles has further fueled the demand for milling cutters.

Governments are also facilitating advanced manufacturing innovation through significant digitization of the manufacturing industry. For example, the U.S. government has invested more than US$ 3 billion under the CHIPS and Science Act to enhance the capabilities of advanced manufacturing and domestic semiconductor manufacturing factories that rely heavily on ultra-precise milling technology for manufacturing of molds and tools. Likewise, Germany's Industry 4.0 campaign is rapidly boosting the deployment of smart factories in the machine tool industry, while China's "Made in China 2025" initiative is focusing on investing in advanced CNC machines and milling cutting technologies for industrial independence.

Milling Tools Industry Trends and Strategic Insights

- The growing use of 5-axis CNC machining equipment in aerospace and automotive industries has led to an increased requirement for solid carbide and indexable cutting tools that allow for highly accurate high-speed machining; as such, the Asia-Pacific region was the most dominant in the market in 2025, representing the highest output in industrial manufacturing globally.

- The trend toward the manufacture of electric vehicles has increased demand for milling tools designed to be utilized in the fabrication of battery housings, light weight aluminum structures, and components in the electric drive train. According to the International Energy Agency, more than 17 million electric cars were sold globally in 2024.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 3.43 Billion | |

| 2035 Projected Market Size | US$ 6.23 Billion | |

| CAGR (2026-2035) | 6.2% | |

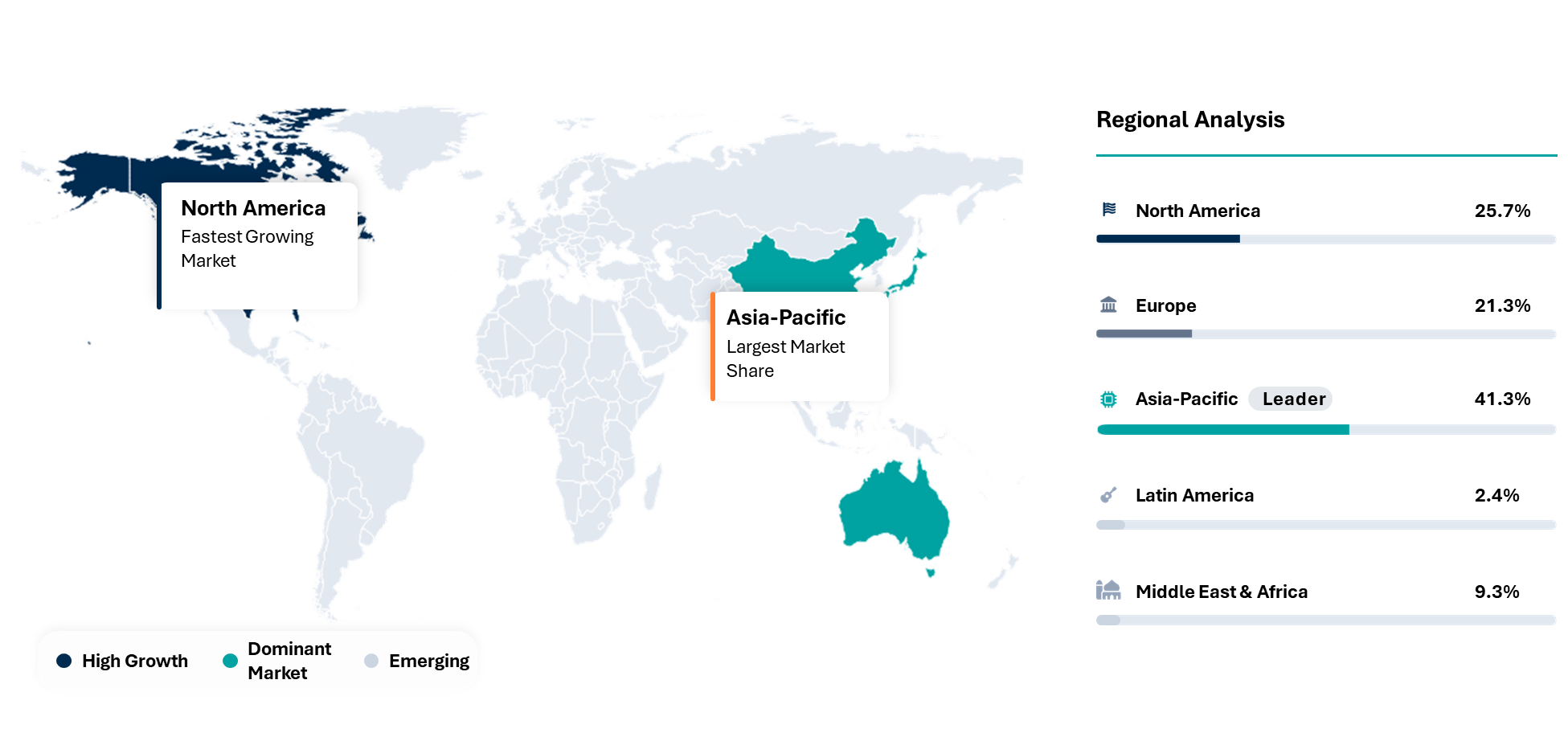

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Tool Grade | High Speed Steel (HSS), Solid Carbide, Cermet, Ceramics, Cubic Boron Nitride (CBN) and PCBN Tools, Diamond Tools | |

| ByMachine Type | 5-Axis Machining Center, Machining Center, Multi-Tasking Machines (Mill Turn Machines), Other | |

| By Workpiece Detail | P Steel, M Stainless Steel, K Cast Iron, N Non Ferrous Metals, S Super Alloys and Titanium, H Hardened Materials, Composites, Plastic, Wood | |

| By End-User | Automotive and Electric Vehicles, Aerospace and Defense, General Machining, Job Shops, Die and Mold, Industrial Machinery, Construction and Agriculture Equipment, Energy and Power Generation, Oil and Gas, Mining, Rail, Marine and Shipbuilding, Electronics and Consumer, Appliances, Semiconductor Equipment and Precision Parts, Medical Devices, Dental, Bearing Manufacturing, Others | |

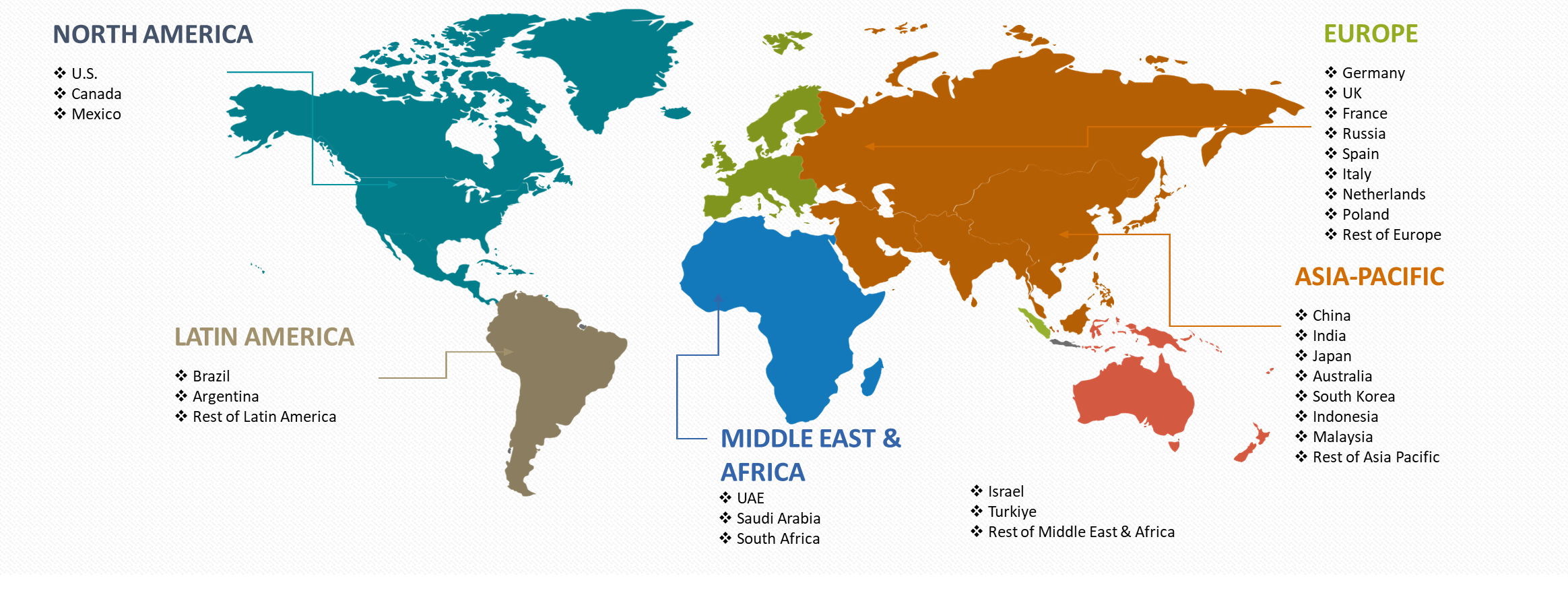

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Strategic Indicators For Milling Tools

High Regulation Impact

Export restrictions from China are driving regulatory pressures in the carbide, cobalt, and tungsten supply chains because China controls raw materials processing. The U.S. and European Union are imposing stricter regulations around critical minerals procurement with respect to their respective industrial policies, namely CHIPS and similar ones. In Europe, German and Japanese companies will be subjected to more stringent compliance requirements with regards to REACH standards for chemicals used in coating milling inserts. The Indian government is stepping up import regulations for precision tooling in its efforts to promote local production via “Make in India.”

High Investment Activity

The majority of investment initiatives revolve around manufacturing companies capable of automated tool manufacturing, particularly Germany, Japan, China, and the USA. Major companies are investing more in increasing CNC-compatible tool grinding and recycling of carbide tools. China is still making significant investments in the vertical integration of the supply chain process for tungsten carbide tools to decrease imports. Germany and Switzerland are focusing their investments on ultra-precise micro-milling tools aimed at EV parts. In India, there is mid-size investment happening for localized manufacturing of tooling components in and around Pune and Chennai.

Supply Chain Disruption

Structural continuity in supply chain disruptions is expected owing to the dependency on tungsten carbide from China. There are delays in the acquisition of tool coating based on cobalt from both Germany and Japan. Reshoring activities in the United States will be affected by a lack of powder metallurgy facilities domestically. Supply chain disruptions via Red Sea routes have an impact on imports into Europe. India faces sporadic shortages in the supply of high-quality carbide inserts owing to import dependence. Variations in energy prices in Europe affect the production cost of precision grinding tools.

Pricing Volatility

Volatility in the prices of milling tools is mainly affected by the input variations of tungsten, cobalt, and carbide. Export restrictions from China cause regular price increases in the acquisition of materials. In Germany and Switzerland, prices for the finished product are higher due to the energy consumption involved in precise production. The US has medium price inflation for its aerospace-quality milling tools, which is attributed to reshoring. Japan has stable prices due to supplier agreements; however, there are threats from imports of rare alloys. India has price volatility due to currency exchange and reliance on imports.

Procurement Pressure

The procurement pressure is increasing in the automobile, aerospace, and die mold sectors that require high precision milling tools. The US defense and aerospace companies are mandating more rigorous qualification processes, resulting in higher qualification expenses for suppliers. The German automakers are focusing on supplier consolidation, which leads to lower supplier margins. China's local producers are focusing on purchasing from within due to government policies. The Indian procurement process suffers from inefficiencies due to an unorganized distribution channel system. In Japan, there is long-term stability in the procurement process but pressure is put on suppliers to optimize cost.

New Technology Adoption

AI-assisted tool wear prediction, digital twin technology, and IoT-powered CNC tool monitoring are some of the latest trends in the usage of advanced milling tools. Germany is at the forefront in incorporating smart factory concepts like adaptive toolpath optimization. Japan is focusing on developing new nano coating techniques, which will help increase the lifespan of the tools used for micro-machining. Predictive maintenance through AI assistance is being adopted by the United States in aerospace machining facilities. Automated grinding of carbide tools is being used increasingly in China to boost self-reliance.

Regional Expansion Opportunity

Milling tool demands in Europe are growing through the restructuring of EV automobiles and recovery in the aerospace industry. High-precision tooling development is mainly carried out by Germany and Switzerland. Investment trends are mainly towards carbide recycling and sustainable milling tools systems in line with the EU carbon neutral directives.

China, Japan, and India are increasing their production capacities for milling tools. China is a leading producer of integrated materials, Japan produces micro-precision milling tools, and India produces low-cost manufacturing tool clusters.

Government Policy Support

The governments are gradually increasing their participation in strategic manufacturing systems. The US government has been supporting domestic tool manufacturing through industrial reshoring and defense manufacturing supply chain security initiatives. The European Union is implementing critical raw material independence policies concerning the procurement of carbides. The Chinese government has continued providing financial aid for the production and export of tungsten carbide tools and machining industries. The Japanese government has been subsidizing precision manufacturing processes using automation and robotic technologies. The Indian government has been encouraging local manufacturing of tools through production linked incentive programs.

Import-Export And Pricing Intelligence

Trade in precision cutting tools is mainly from industrialized centers like Germany, Japan, and China to provide advanced carbide inserts and end mills, whereas the United States, India, and Southeast Asian countries receive such tools due to their needs for automotive and aerospace machining processes. Trade in re-export centers includes Singapore and the UAE.

| HS Code | Reporter | Trade Flow | 2025 Trade Value (US$) | Interpretation |

| HS 820770 | Japan | Export | 173,993,222 | Global leader; high-value precision tooling exports dominate |

| HS 820770 | USA | Import | 322,225,489 | Internal demand for reallocation of precision machining tools |

| HS 820770 | Italy | Export | 153,075,036 | Scale-driven exports with competitive pricing advantage |

| HS 820770 | Japan | Import | 61,881,461 | Strong industrial dependency on imported high-precision tools |

| HS 820770 | China | Export | 12,013,811 | Automotive and electronics-driven exports demand for premium milling tools |

The pricing of precision milling tools is dependent upon input costs associated with the use of carbides and tungsten, the volatile nature of alloys containing cobalt, and high-energy sintering operations. OEM tool manufacturing in Europe receives higher prices due to the tolerance requirements, while Asia is focused on cost efficiency via scale economies.

Company Coverage Preview

Sandvik AB (Sweden) continues to hold leadership positions globally in milling tools and is well-positioned in the carbide cutting tools, digital machine tools, and sustainable tooling technologies markets. Sandvik targets lucrative markets within aerospace and automotive EV machining applications. Key elements of its strategy include technology-based initiatives such as lifecycle management software and growth in coated carbide end mill tools. Vertical integration of material sciences capabilities and strong European and North American operations provide the competitive edge of Sandvik amidst raw material price fluctuations.

AI Impact Analysis

Artificial intelligence technology is turning the milling tool into an efficient tool that can predict manufacturing operations. Machine learning technology is used to track the wear and tear of the milling tool while machining, which improves efficiency in operations in the CNC machine. AI technology is applied in toolpath optimization in the machining process by United States aerospace industries. In Germany, AI is incorporated in the smart factory environment for adaptive milling precision controls. The Japanese are using artificial intelligence for micro-tool defect detection during semiconductor machining operations.

Disruption Analysis

The most important disruptions are the fast adoption of Industry 4.0 innovations, with the top-tier firms incorporating AI-based machining analytics, IoT-based tool condition monitoring, predictive maintenance systems, and digital twin technology into their milling processes. Sandvik Coromant and Seco Tools AB are both actively promoting digital machining ecosystems that maximize machining efficiency, minimize downtime, and increase tool life in automated manufacturing processes.

Difficult-to-machine materials, such as titanium alloys, composite materials, hardened steel, and aerospace materials are other important disruptors in the milling industry, since their use increases the requirement for advanced carbides, ceramics, PCD, and coated mill cutter blades. The trend forces conventional tool manufacturers to make substantial investments in material science and unique geometrical solutions. Moreover, the development of additive manufacturing and hybrid machining technologies threatens the dominance of subtractive milling by allowing near-net-shape machining while reducing material losses. The rise of electric vehicles creates a new pattern of tooling requirements for EV components that necessitate high-precision machining.

Cheap carbide tooling options presented by Asian manufacturers are challenging the pricing structures, causing greater competition among established Western and Japanese producers. Changes are taking place in customer purchasing strategies with respect to tool acquisition; specifically, they tend to lean towards tooling services including managed inventory and performance-based agreements rather than simply purchasing tools. In addition, sustainability measures, reuse of milling tools, and energy-efficient machining practices require manufacturers to reconsider their approaches and designs with respect to both production and coating processes.

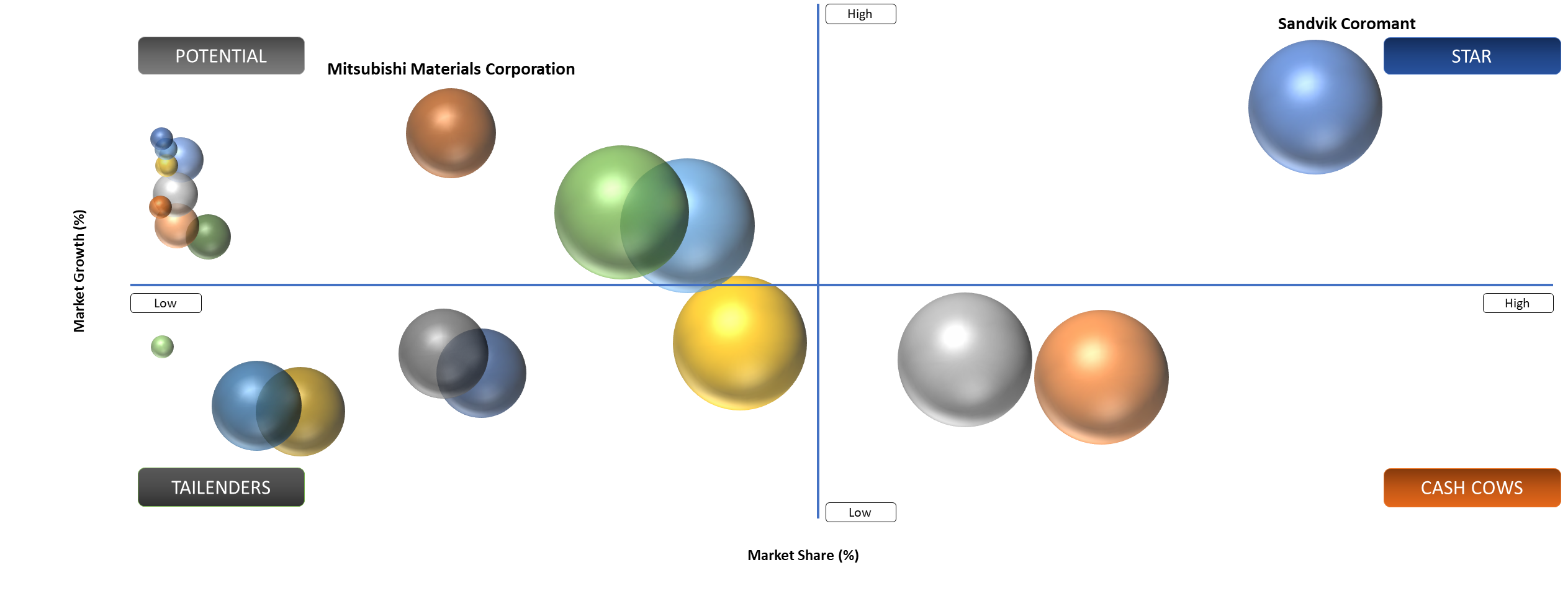

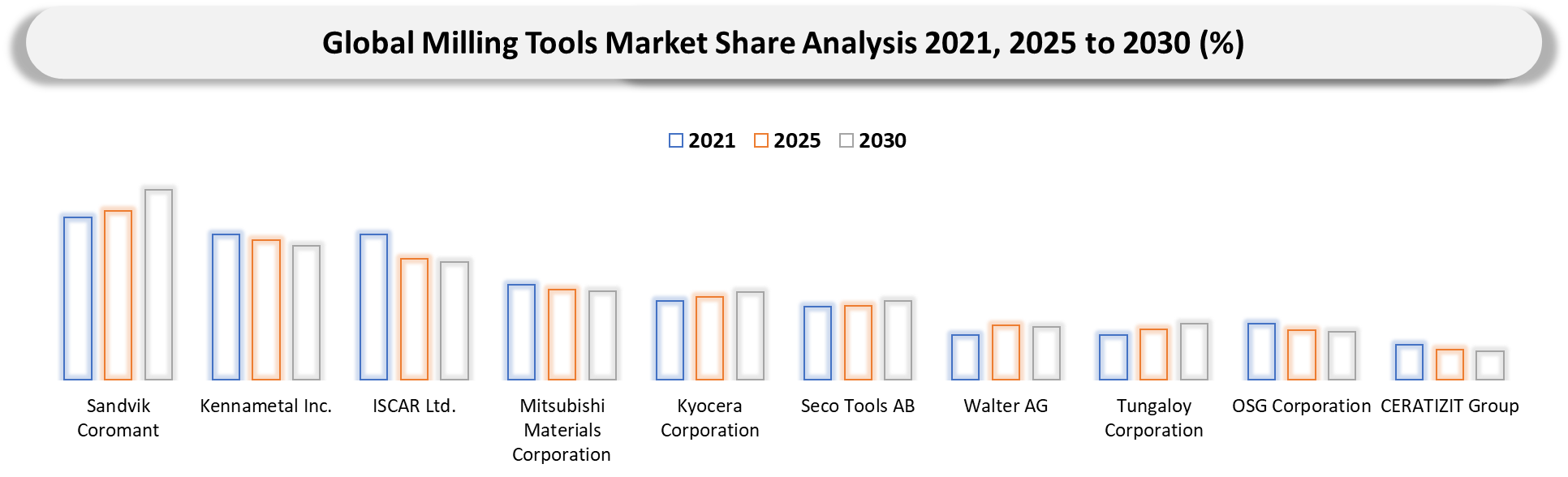

BCG Matrix: Company Evaluation

The market stars are Sandvik Coromant, Kennametal Inc., and ISCAR Ltd. because of their significant presence in the aerospace, automotive, EV machining, and precision manufacturing sectors. Star firms invest significantly in technology-driven machining systems, intelligent tooling systems, AI-powered tool tracking capabilities, and innovative carbide materials, which make it possible for them to lead the high-growth machining categories like CNC milling and indexable carbide tools. The cash cows have high brand value and steady revenues from the mature industrial machining market of Asia and Europe.

Examples of potential players in the market include Asian producers like YG-1, Korloy, and Chinese producers of carbide tools who are rapidly growing by offering cost-effective products and having manufacturing facilities within the region. Although these players have shown success among mid-level industrial companies, they lack the ability to offer premium tooling solutions and global presence. Higher levels of automation, the requirement for multiple material processing, and the implementation of Industry 4.0 are slowly but surely reducing the market shares of these players.

Market Dynamics

Rising Adoption of Advanced CNC Machining Technologies

With time, modern industries have come to adopt multi-axis machining centers that ensure increased efficiency, reduced wastage, and higher tolerances of microns. It is stated by the International Federation of Robotics that over 540,000 industrial robots have been installed globally in the year 2023, where automotive and electronics have emerged as the two biggest sectors that use automatic machining processes. For such industrial robots, hard mill inserts are needed that can work effectively at faster speeds.

In the aerospace industry, there is greater need for high-quality milling products owing to higher aircraft production and defense upgrades. In 2024, Airbus manufactured 766 aircrafts, whereas Boeing was increasing its production of aircrafts that use less fuel. Milling titanium parts for aerospace application requires faster consumption of the milling product due to heat and work hardening properties. Therefore, the company is encouraged to purchase carbide and ceramic milling technology products with improved durability and thermal stability.

High Tooling Costs and Supply Chain Volatility

One of the major obstacles that is faced by the global milling tool market is the increasing cost of raw materials such as tungsten, cobalt, carbide powder, and advanced ceramics which are used in the manufacture of premium quality milling tools. The price of tungsten has become highly unpredictable starting from 2023 and 2024 due to geopolitical threats and concentrated mining. More than 80% of tungsten mined in the world is produced in China.

The sector is also under pressure owing to increased energy costs and logistics problems experienced during the manufacture of precision tools. The manufacture of advanced milling tools requires high levels of special grinding machines, special coatings and heat treatments that incur a lot of costs in operation. Medium and small-sized machine shops postpone the replacement of worn out milling tools due to increased tooling costs, hence reduced machining productivity.

Segmentation Analysis

The global milling tools market is segmented based on the tool grade, machine type, workpiece detail, end-user and region.

Automotive Industry Leads End-Use Demand

The automotive industry continues to be the largest market for milling tool components globally due to the extensive machining processes that are used in the production of engines, transmission assemblies, chassis, and batteries of electric automobiles. The current automotive assembly uses aluminum and high-strength steel components that are intricately shaped and require special wear-resistant finishes.

The production of electric vehicles is opening up more prospects for the milling tool industry. The machining of battery trays, e-axle and power electronics enclosures, which necessitate precise aluminum milling, is being scaled up by the companies. In 2024, Tesla kept on increasing the manufacturing capacity at its Gigafactory, while Chinese electric vehicle producers, including BYD, substantially invested in their manufacturing capacities.

Aerospace and Defense Applications Gain Momentum

Aerospace and Defense are fast becoming one of the most rapidly growing sectors for the use of state-of-the-art milling tools owing to rising global aircraft deliveries, military acquisitions, and space exploration programs. Milling of aircraft parts is highly demanding with respect to dimensional accuracy and finish because of the materials that have to be machined, such as titanium, nickel alloys, and composite materials. Rising global military spending is contributing to the rise in the acquisition of military aircraft, naval ships, and missiles.

Defense contractors and aircraft manufacturers are increasingly adopting high-feed milling strategies and digital tool monitoring systems to reduce machining cycle times while improving tool life. Space programs are also contributing to demand growth for ultra-precision milling solutions. SpaceX and government-backed space agencies continue investing heavily in reusable launch systems and satellite manufacturing, requiring complex milling operations on lightweight heat-resistant alloys and advanced engineered materials.

Geographical Penetration

U.S. Milling Tools Market Trends

The milling tool market in the US is witnessing tremendous technological advancements owing to breakthroughs in the fields of aerospace & defense, electric vehicles, semiconductors, and high-precision machining processes. In fact, currently, the US is one of the leading markets for CNC machining tools and high-speed milling machines due to investments by the government in the manufacturing sector and industry reshoring initiatives. Increased demand for semiconductors following the implementation of the CHIPS and Science Act has triggered growing demand for carbide milling tools, indexable milling tools, micro mills, and coated tools for machined aluminum, titanium, composites, and hardened steel machining.

The U.S. is fast emerging as another center of innovation for digital machining technology, predictive maintenance, and intelligent milling optimization. Factories have begun adopting industry 4.0 systems, digital twins, tool monitoring through sensors, and machine learning algorithms for spindle wear prediction to enhance efficiency and decrease downtime. Predictive maintenance studies employing machine learning and SHAP values have found spindle torque, temperature, and rotational speeds to be crucial parameters in optimizing milling machine performance.

Manufacturers of components for aerospace applications and electric vehicles in different states, such as Ohio, Texas, Michigan, and Arizona, are increasingly relying on sophisticated multi-axis machining centers needing high-feed milling cutters and solid carbide tooling options. Defense manufacturing, aircraft part manufacture, and precision metalwork industries have led to rising interest in coating options such as titanium aluminum nitride, diamond-like carbon, and nanocomposite coatings that offer high wear resistance.

Japan Milling Tools Market Trends

The milling tools market in Japan still ranks among the most technologically progressive due to its highly developed system of machine tools production, precise engineering, robotics, and auto industry. It is worth noting that Japanese manufacturers of machine tools are well-known for their production of extremely accurate milling cutters, micro milling tools, indexable inserts, and coated carbide milling tools utilized in aerospace, semiconductors, medical devices, and automotive manufacturing. The production process in the manufacturing environment of Japan implies an extreme level of preciseness, as well as high longevity of tools and automation efficiency.

Leading manufacturers in Japan are now implementing systems for automated monitoring of tools, adaptive feed rate controls, and machining simulation in real-time for better tool efficiency and lower variation in manufacturing processes. Research studies such as "DeepMill" have successfully proved the ability of manufacturability analysis through neural networks that can correctly predict inaccessible machining regions with a prediction accuracy of more than 94%, thus aiding the adoption of smart manufacturing systems by Japan.

The country's transition from gasoline-powered automobiles to electric vehicles, alongside light components that require precision manufacturing, are resulting in an increased demand for advanced milling cutters suitable for machining aluminum, titanium, carbon fibers, and high-strength steels at increased spindle speeds. Alongside, the semiconductor equipment manufacturing sector and robotic industries of Japan are creating new demands for ultra-fine micro-milling cutters for miniature components. Factory automation, energy efficient manufacturing, and supply chain resilience programs by the government are also promoting the use of longer-lasting coated tools.

China Milling Tools Market Trends

China is among the fastest-growing marketplaces for milling tools around the globe due to its immense capability for manufacturing industries, semiconductor manufacturing investment, electric vehicles manufacturing industry, and machinery manufacturing sector. The fast industrial modernization projects being conducted in China along with growing manufacturing sector demand high-performance carbide end mills, face mills, indexable cutters, and high-speed machining systems from automotive, aerospace, electronics, and heavy machinery industries. The Chinese government is making continuous investment in semiconductor manufacturing and self-reliance in the industry. It will create demand for highly precise milling tools required in the molding of semiconductors, electronic parts, and mechanical assemblies.

The Chinese milling tools industry is also experiencing rapid advancements in the area of locally made smart manufacturing technologies, AI-based machining optimization, and digitalized production facilities. The country is actively adopting modern industrial robotics, automated machining centers, and intelligent production lines in order to increase efficiency and become less dependent on imports in terms of advanced manufacturing technologies. Domestic manufacturers of milling tools are investing heavily in the development of coated carbide cutting tools, ceramic inserts, and high-speed milling solutions that would be able to handle aerospace alloys and lightweight materials used in the manufacturing of EVs. The rise of the EV sector, batteries manufacturing, rail networks, and renewable energy equipment manufacturing creates a growing demand for highly efficient milling processes that would allow processing aluminum, hardened steels, and composite materials. On the other hand, Chinese tool makers are also working on developing local technologies for coatings and precise grinding to compete against top-notch Japanese and European suppliers.

Competitive Landscape

- The global milling tools market features intense competition among multinational cutting tool manufacturers, precision engineering firms and specialized carbide tooling companies competing on machining performance, tool life, coating technology and digital machining integration capabilities.

- Key players include Sandvik Coromant, Kennametal Inc., ISCAR Ltd., Mitsubishi Materials Corporation, Seco Tools AB, Walter AG, Mapal, OSG Corporation, Dormer Pramet and Tungaloy Corporation.

- Companies are increasingly differentiating themselves through advanced PVD and CVD coating technologies, AI-enabled machining optimization software, digital tooling ecosystems and customized milling geometries designed for difficult-to-machine materials such as titanium, Inconel and carbon-fiber composites.

Strategic investments in sustainable machining technologies, additive manufacturing for cutting tool production, recycled carbide recovery systems and Industry 4.0-enabled smart tooling platforms are becoming critical as manufacturers seek higher productivity, lower operational costs and improved environmental performance across precision machining operations.

MAJOR PAIN POINTS

- High Tool Wear and Frequent Replacement Costs: Rapid wear of milling cutters during high-speed and hard-material machining increases tooling expenses and production downtime.

- Volatility in Raw Material Prices: Fluctuating costs of tungsten carbide, cobalt, high-speed steel, and advanced coatings directly impact manufacturing margins and product pricing.

- Demand for Higher Precision and Surface Finish: End-users increasingly require ultra-precise machining tolerances and superior finishes, pressuring tool manufacturers to enhance performance continuously.

- Shortage of Skilled Machining Workforce: Lack of experienced CNC programmers and machining operators limits optimal tool utilization and production efficiency across manufacturing industries.

- Rising Competition from Low-Cost Manufacturers: Intense price competition from regional and low-cost suppliers reduces profitability and creates pricing pressure for premium milling tool brands.

- Challenges in Machining Advanced Materials: Aerospace alloys, titanium, composites, and hardened steels generate excessive heat and vibration, reducing milling tool life and operational stability.

- Integration Complexity with Smart Manufacturing Systems: Adoption of Industry 4.0, IoT-enabled tooling, and digital monitoring systems requires substantial investment and technical expertise.

- Supply Chain Disruptions and Delivery Delays: Global logistics bottlenecks and geopolitical uncertainties affect timely procurement of raw materials and distribution of finished milling tools.

- Increasing Sustainability and Environmental Compliance Requirements: Manufacturers face pressure to reduce waste, energy consumption, coolant usage, and carbon emissions while maintaining productivity.

- High R&D and Coating Technology Development Costs: Continuous innovation in nano-coatings, carbide grades, and advanced geometries demands significant research investment and long development cycles.

KEY DEVELOPMENTS

- March 2026 - Guhring KG introduced RF 100 Speed milling cutters featuring advanced nano-coatings, increasing machining productivity and reducing thermal wear during operations.

- March 2026 - Kennametal Inc. expanded GOmill PRO solid end mills portfolio featuring vibration-control flute geometry, improved coatings and enhanced chip evacuation capabilities.

- March 2026 - Kyocera Corporation introduced new MFAH high-feed milling cutters designed for automotive machining, reducing cycle times and increasing operational efficiency significantly.

- March 2026 - Sandvik Coromant introduced CoroMill MR20 indexable milling solution improving profiling stability, coolant delivery, productivity and titanium machining efficiency across aerospace applications.

- March 2026 - Tungaloy Corporation introduced DoFeedTri high-feed milling cutter supporting deeper cutting depths, stable machining and improved productivity for die-mold applications globally.

- February 2026 - Dormer Pramet expanded S-series milling cutters portfolio delivering enhanced edge security, smoother cutting action and improved machining consistency across metalworking industries.

- February 2026 - ISCAR Ltd. released upgraded LOGIQ milling solutions supporting higher metal-removal rates, improved insert durability and optimized aerospace component machining productivity.

- February 2026 - OSG Corporation expanded AE-VMS anti-vibration milling tools lineup improving deep-pocket machining performance, tool life and surface quality in aerospace manufacturing environments.

- February 2026 - Seco Tools AB enhanced Jabro solid milling range with optimized geometries delivering superior chip control, surface finish and tool longevity in titanium machining.

- January 2026 - CERATIZIT Group developed MaxiMill milling solutions with advanced carbide grades enabling higher machining speeds and superior wear resistance across industrial applications.

- January 2026 - MAPAL Group introduced customized milling solutions supporting electric vehicle component production with higher precision, efficiency and reduced manufacturing cycle times globally.

- January 2026 - Mitsubishi Materials Corporation expanded SMART MIRACLE milling series with advanced coating technologies improving wear resistance and machining stability for hardened steel applications.

- January 2026 - Sandvik Coromant partnered with MachiningCloud, integrating digital tooling data for streamlined CAM programming, tool assembly creation and milling process optimization globally.

January 2026 - Walter AG expanded Xtra·tec XT milling platform featuring improved insert stability, higher feed capabilities and enhanced sustainability for industrial manufacturing operations.

ANALYST VIEW / OPINION

- Adoption of multi-axis CNC machining accelerating demand for high-precision milling tools globally.

- Aerospace lightweight material machining increasing preference for advanced carbide milling solutions.

- EV manufacturing expansion driving high-volume demand for aluminum-compatible milling cutters worldwide.

- Tool life optimization technologies becoming critical differentiators among premium milling tool manufacturers.

- Digital manufacturing integration strengthening usage of smart and sensor-enabled milling tools.

- Asia-Pacific manufacturing expansion continuing to dominate global milling tools consumption growth trends.

- Demand for customized milling geometries increasing across automotive, medical, and electronics industries.

- Coated carbide tools witnessing stronger adoption due to superior wear resistance performance.

- Sustainability initiatives encouraging dry machining and energy-efficient milling tool development strategies.

- Consolidation among tooling manufacturers intensifying competition through innovation and distribution expansion.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Automotive & Electric Vehicle Manufacturers | Manufacturing Engineering Teams, CNC Milling Managers, Production Heads | Analyze demand for high-speed milling tools used in EV housings, engine blocks and lightweight component machining |

| Aerospace & Defense Companies | Aerospace Machining Engineers, Precision Manufacturing Teams, Procurement Departments | Evaluate advanced milling technologies for titanium, superalloys and composite material machining applications |

| Industrial Machinery Manufacturers | Plant Operations Teams, Industrial Engineering Managers, Production Planning Departments | Optimize milling productivity, tool life and machining efficiency in industrial equipment manufacturing |

| Metal Fabrication & General Engineering Companies | Fabrication Managers, CNC Programmers, Workshop Supervisors | Identify cost-efficient milling tools for precision metal cutting and complex machining operations |

| Die & Mold Manufacturing Companies | Tool Room Managers, Mold Design Engineers, Precision Machining Teams | Assess advanced end mills and contour milling solutions for high-accuracy mold production |

| Construction & Heavy Equipment Manufacturers | Production Engineering Teams, Manufacturing Operations Managers, Supply Chain Departments | Understand durable milling tool requirements for machining heavy-duty equipment components |

| Oil & Gas Equipment Manufacturers | Reliability Engineers, Heavy Machining Teams, Procurement Managers | Evaluate wear-resistant milling tools for critical industrial equipment and pipeline component machining |

| Energy & Power Generation Companies | Turbine Manufacturing Teams, Plant Engineering Departments, Strategic Sourcing Teams | Analyze milling tool demand for turbines, generators and precision-machined power equipment |

| Mining Equipment Manufacturers | Machining Operations Teams, Maintenance Departments, Manufacturing Engineers | Identify high-performance milling solutions for abrasive material processing and heavy machining |

| Railway & Marine Equipment Manufacturers | Production Engineering Teams, Fabrication Managers, Operations Heads | Track milling technologies for rail infrastructure and marine equipment manufacturing |

| Medical Device Manufacturers | Precision Manufacturing Teams, R&D Departments, Quality Assurance Managers | Study micro-milling and ultra-precision tooling solutions for medical instruments and implants |

| Electronics & Semiconductor Equipment Manufacturers | Advanced Manufacturing Teams, Automation Engineers, Product Development Teams | Evaluate miniature milling technologies for precision electronic and semiconductor components |

| CNC Machine Tool Manufacturers | Product Strategy Teams, Automation Specialists, Business Development Managers | Identify integration opportunities between CNC systems and advanced milling tool technologies |

| Milling Tool & Cutter Manufacturers | Product Innovation Teams, Competitive Intelligence Departments, Sales Strategy Teams | Benchmark competitor products, coatings, tool geometries and market expansion opportunities |

| Carbide, Ceramic & Coating Material Suppliers | Technical Sales Teams, Market Intelligence Departments, R&D Teams | Analyze future demand for carbide grades, coatings and advanced milling tool materials |

| Industrial Automation & Smart Manufacturing Companies | Industry 4.0 Teams, Smart Factory Engineers, Automation Consultants | Evaluate adoption of automated milling operations and intelligent machining technologies |

| Industrial Distributors & Tooling Suppliers | Category Managers, Regional Sales Teams, Inventory Planning Departments | Understand regional milling tool demand and optimize industrial tooling portfolios |

| Contract Manufacturing & Job Shops | CNC Workshop Managers, Production Supervisors, Business Owners | Identify profitable machining applications and tooling investment opportunities across industries |

| Research Institutions & Universities | Manufacturing Research Teams, Industrial Engineering Faculties, Material Science Researchers | Analyze innovations in milling technologies, coatings and high-speed machining systems |

| Investors & Consulting Firms | Investment Analysts, Industrial Consultants, Market Intelligence Teams | Evaluate market growth opportunities, competitive landscape and emerging milling technology trends |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT “DATAM” UNIQUELY PROVIDES

- Real-time raw material dependency mapping across tungsten and cobalt chains

- OEM-level benchmarking of global cutting tool manufacturers

- AI-driven tool life predictive analytics for manufacturing efficiency

- Geopolitical risk scoring across machining supply networks

- Price elasticity modeling under commodity volatility scenarios

- Plant-level production footprint intelligence for reshoring decisions

QUESTIONS THIS REPORT ANSWERS

- What is the current and forecast market size of the global milling tools market through 2035?

- Which end-users are driving demand growth, and why?

- Which regions and milling tool categories present the highest growth and investment opportunities?

- How are investments in CNC machining, smart manufacturing and Industry 4.0 technologies reshaping competitive dynamics and production efficiency?

- How do regulatory standards, raw material price fluctuations and global supply chain risks affect milling tools manufacturing and deployment?

- Which tool materials and technologies are shaping next-generation milling tools manufacturing?