Metal Injection Molding Powders and Feedstock Market Overview

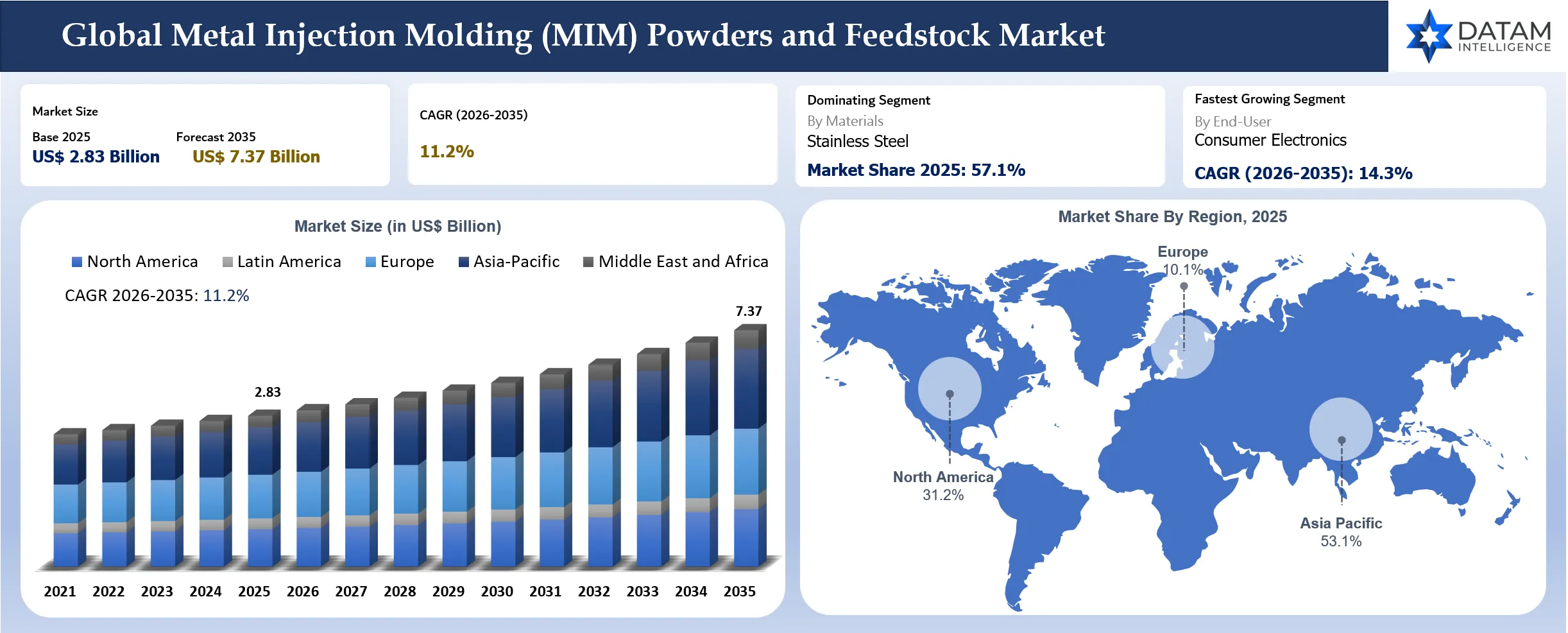

The global metal injection molding (MIM) powders and feedstock market reached US$ 2.83 billion in 2025 and is expected to reach US$ 7.37 billion by 2035, growing at a CAGR of 11.2% during 2026 to 2035. Demand is being driven by small complex metal parts that are difficult, costly or slow to machine at scale. Medical devices, consumer electronics, automotive systems, industrial tools, defense hardware and aerospace components are increasing demand for fine powders and stable feedstock because part geometry is becoming smaller and tolerance windows are becoming tighter. Feedstock quality has moved from a processing input to a commercial differentiator because flow, binder behavior, debinding stability and sintering shrinkage can directly affect yield.

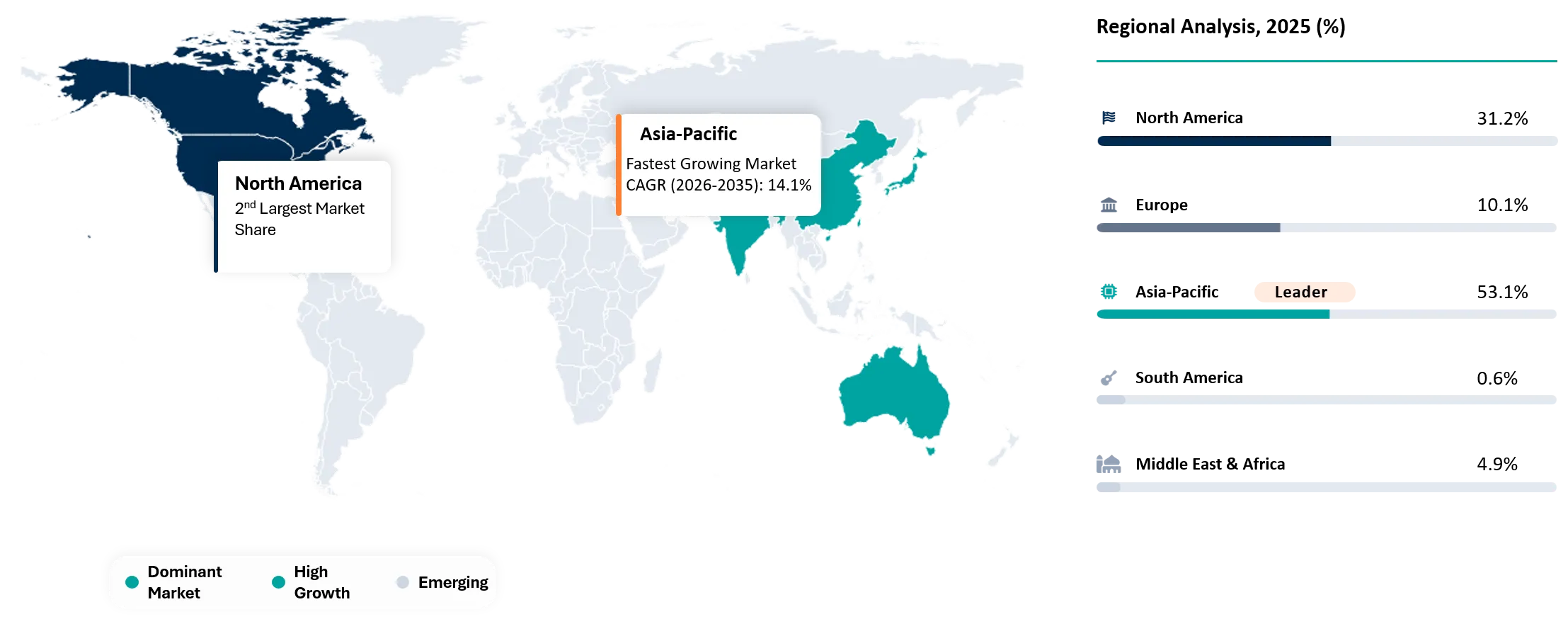

Asia-Pacific remains the largest demand center because China, Japan, South Korea, India, Malaysia and Singapore support electronics, medical device, precision component and automotive manufacturing. Europe and North America remain high-value regions where medical, aerospace, defense and industrial customers require stronger documentation and qualification support. Supplier differentiation will depend on powder consistency, feedstock rheology, debinding compatibility, sintering support, co-development capability and ability to reduce defect risk in high-volume precision programs.

Market Scope

| Metrics | Details | |

| Market Size in 2025 | US$ 2.83 Billion | |

| Market Size by 2035 | US$ 7.37 Billion | |

| CAGR During 2026 to 2035 | 11.2% | |

| Largest Region in 2025 | Asia-Pacific, market share 53.1% | |

| Fastest Growing Region | Asia-Pacific, CAGR 12.2% between 2026 and 2035 | |

| Leading Material | Stainless Steel | |

| Fastest Growing Material | Soft Magnetic Alloys | |

| Leading End-User | Medical | |

| Fastest Growing End-User | Consumer Electronics | |

| Market Maturity | Growth Stage | |

| Key Buying Question | Which powder and feedstock system can hold flow, shrinkage and sintered part consistency across tight tolerance production? | |

| By Material | Stainless Steel, Low Alloy Steel, Soft Magnetic Alloys, Titanium, Tungsten Heavy Alloys, Copper Alloys | |

| By Feedstock Performance | Standard Feedstock, High Flow Feedstock, Fine-Tolerance Feedstock, Micro MIM Feedstock, Application-Specific Feedstock | |

| By Part Complexity | Micro Components, Thin-Wall Parts, High-Precision Structural Parts, Magnetic Components, Wear-Resistant Parts | |

| By Manufacturing Support | Powder Supply, Compounded Feedstock, Co-Development Programs, Debinding Support, Sintering Optimization | |

| By End-User | Medical, Automotive, Consumer Electronics, Industrial Tools, Defense, Aerospace | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Key Takeaways

- Asia-Pacific remained the largest regional market with 53.1% market share in 2025 and is expected to reach 57.5% by 2035. Asia-Pacific is also the fastest-growing region with 12.2% CAGR between 2026 and 2035.

- North America is 2nd largest consumer, expected to decrease from 31.2% market share in 2025 to 30.2% market share by 2035, despite high CAGR of 10.8% between 2026 and 2035.

- MIM powders and feedstock demand is strongest where small part complexity, high repeatability and high-volume production make machining less attractive.

- Stainless steel remains the leading material with 57.1% market share in 2025 because it is widely used in medical devices, consumer electronics, industrial tools and structural precision components.

- Soft magnetic alloys are expected to grow fastest as compact motors, sensors, actuation systems and electromagnetic components require net-shape magnetic parts.

- Medical remains a leading End-User because surgical tools, orthodontic parts, implant-related components and device hardware require precision, biocompatibility and repeatable quality.

- Consumer electronics is expected to grow fastest with a CAGR of 14.3% between 2026 and 2035, because hinges, camera modules, wearable components, connectors and small structural parts require compact and high-volume metal part production.

- Feedstock performance is becoming a strategic differentiator as part dimensions shrink and yield losses become more expensive.

- Supplier advantage is moving toward application-specific feedstock, co-development support, sintering optimization and local supply close to MIM houses.

Why Does This Report Matter In 2026?

The MIM powders and feedstock market matters in 2026 because precision part manufacturing is moving toward smaller, more complex and more functionally demanding components. Machining and casting become less economical when parts are small, intricate and required in high volumes. MIM creates value by enabling near-net-shape production while reducing multi-step machining and assembly.

Medical and electronics buyers are raising performance requirements. A tiny part failure can create a product recall, device malfunction or customer complaint. Powder particle size, chemistry, flow, binder loading, debinding behavior and sintering shrinkage now influence commercial approval. Customers are asking suppliers for process guidance, not only material supply.

Regionalized manufacturing is another shift. MIM houses increasingly want dependable local feedstock supply and technical support. Qualification cycles in medical, aerospace and defense remain long, so validated supply relationships are sticky. A strong report must evaluate both material demand and manufacturing support because powder alone does not create market value unless the final part meets performance and dimensional requirements.

Strategic Indicators For MIM Powders and Feedstock

High Regulation Impact

Regulation strongly affects MIM powders and feedstock where parts enter medical, defense, aerospace and automotive applications. Medical buyers require material traceability, biocompatibility documentation, process validation and tight control over contamination. Aerospace and defense customers require qualification evidence, IoT control and repeatable mechanical performance.

Feedstock changes can trigger requalification. A slight shift in powder chemistry, particle size distribution or binder system can affect shrinkage and final density. Buyers therefore prefer suppliers that provide consistent grades and technical documentation. Supplier switching is slow in regulated applications because process windows are narrow.

Environmental and workplace safety rules also matter. Powder handling, binder removal and sintering atmospheres require safety controls. Producers and MIM houses need documentation covering safe handling, emissions and waste management.

High Investment Activity

Investment is concentrated in fine powders, application-specific feedstock, micro MIM, soft magnetic alloys, titanium feedstock and regional MIM manufacturing capacity. Component makers are expanding where electronics, medical and automotive customers need small complex metal parts at scale.

Medical and electronics applications attract higher-value investment because customers pay for precision and repeatability. Feedstock suppliers that can support early design and process optimization can capture premium demand. Co-development programs are increasingly important because material selection, tooling and sintering must align from the beginning.

Asia-Pacific investment is strongest due to electronics, medical device and automotive component manufacturing. North America and Europe remain important for high-value regulated applications, especially where qualification and technical documentation are central to procurement.

Supply Chain Disruption

Supply risk is tied to metal powder availability, atomization capacity, binder systems, specialty alloy inputs, compounding capacity and regional logistics. Fine spherical powders and high-purity specialty grades are not always widely available. Supply disruptions can affect MIM houses that are locked into qualified materials.

Binder systems can also create bottlenecks. Catalytic, solvent and thermal debinding routes require feedstock compatibility and process stability. A change in binder supply can affect debinding cycle time, part integrity and sintering yield.

Regional supply is becoming more important because buyers want shorter lead times and lower logistics risk. MIM houses serving medical and electronics customers need responsive technical support. Suppliers with regional compounding and application teams are better positioned.

Pricing Volatility

MIM powder and feedstock pricing is affected by alloy type, powder size, purity, atomization method, binder system, lot size and documentation requirements. Titanium, tungsten heavy alloys and specialty magnetic alloys command premium pricing. Stainless steel and low alloy steel remain more competitive but still require consistency.

The commercial calculation is not only price per kilogram. A cheaper feedstock can become expensive if it increases scrap, causes shrinkage variation or requires longer debinding. Buyers evaluate material cost through yield, cycle time and final part acceptance.

High-value applications can absorb premium feedstock pricing when quality improvement reduces downstream losses. Medical and electronics customers are especially sensitive to defect cost because small components can create large product-level consequences.

Procurement Pressure

Procurement teams must balance material price with production yield and qualification risk. MIM parts often require tight process control. A supplier with lower price but variable feedstock can increase scrap or force revalidation. Purchasing decisions therefore involve engineering, quality and production teams.

Co-development support is becoming an important buying factor. Customers need help with material selection, mold design, debinding route, sintering profile and dimensional compensation. Feedstock suppliers that provide technical support can become preferred partners.

Local availability also influences procurement. Regional MIM houses need stable feedstock delivery and fast troubleshooting. Long-distance supply can create risk when production schedules are tight.

New Technology Adoption

Technology adoption is strongest in micro MIM feedstock, high-flow feedstock, fine-tolerance feedstock, soft magnetic alloys and titanium MIM materials. Micro components require fine powders and predictable binder behavior. Small geometry leaves little room for defects.

Soft magnetic MIM is gaining attention because compact sensors, actuators and electromagnetic devices require small magnetic components. Powder purity and sintering control are critical because magnetic performance depends on chemistry and microstructure.

Digital process control is also advancing. MIM houses can use data from molding, debinding and sintering to improve yield. Feedstock suppliers that help customers interpret process data can deepen commercial relationships.

Import-Export Scenario

MIM powders and feedstock trade is linked to metal powders, stainless steel powders, titanium powders, tungsten powders, copper powders and molded precision metal components. Trade codes do not isolate MIM feedstock perfectly, so analysis should combine powder codes and high-precision component trade indicators.

| HS Code | Trade Item | Import-Export Relevance |

| 720521 | Alloy Steel Powders | Supports review of steel powder flows used in powder metallurgy and selected MIM applications |

| 720529 | Iron and Steel Powders | Indicates broader ferrous powder supply used by MIM and powder metallurgy producers |

| 810820 | Titanium Powders and Unwrought Titanium | Tracks titanium feedstock exposure for medical and aerospace MIM applications |

| 810110 | Tungsten Powders | Indicates tungsten powder supply for high-density and wear-resistant MIM components |

| 740610 | Copper Powders | Supports review of copper alloy powder demand for conductive and thermal applications |

| 848690 | Parts For Semiconductor and Electronics Manufacturing Equipment | Provides a proxy for precision components used in advanced manufacturing equipment |

AI Impact Analysis

AI can improve MIM feedstock development by modeling powder-binder interactions, flow behavior, shrinkage and sintering outcomes. Feedstock design has many variables including powder size, particle shape, binder content, viscosity and debinding route. AI tools can reduce trial cycles and improve formulation decisions.

Production analytics can also improve yield. Molding pressure, melt temperature, debinding time, furnace atmosphere and sintering profile all influence final density and dimensions. AI-assisted monitoring can help identify drift before defects become visible in final parts.

AI will be most useful where high-volume parts generate enough production data. Medical and electronics programs can benefit because small yield improvements have meaningful financial value. Suppliers that combine feedstock knowledge with process data support will strengthen customer retention.

Disruption Analysis

Micro MIM is disrupting the market because smaller parts require more controlled feedstock and tighter process windows. Standard formulations may not work when wall thickness, feature size and tolerance requirements become more demanding. Fine powders and high-flow feedstock are becoming more important.

Soft magnetic components are creating new growth opportunities. Compact actuation, sensors and electromagnetic devices need high-precision magnetic parts. MIM can support complex geometries that are difficult to machine or assemble through conventional methods. Regional manufacturing is also disrupting supply strategy. Buyers want qualified feedstock close to production. Localized compounding and technical service can reduce risk for MIM houses serving fast-moving electronics and medical customers.

BCG Matrix: Company Evaluation

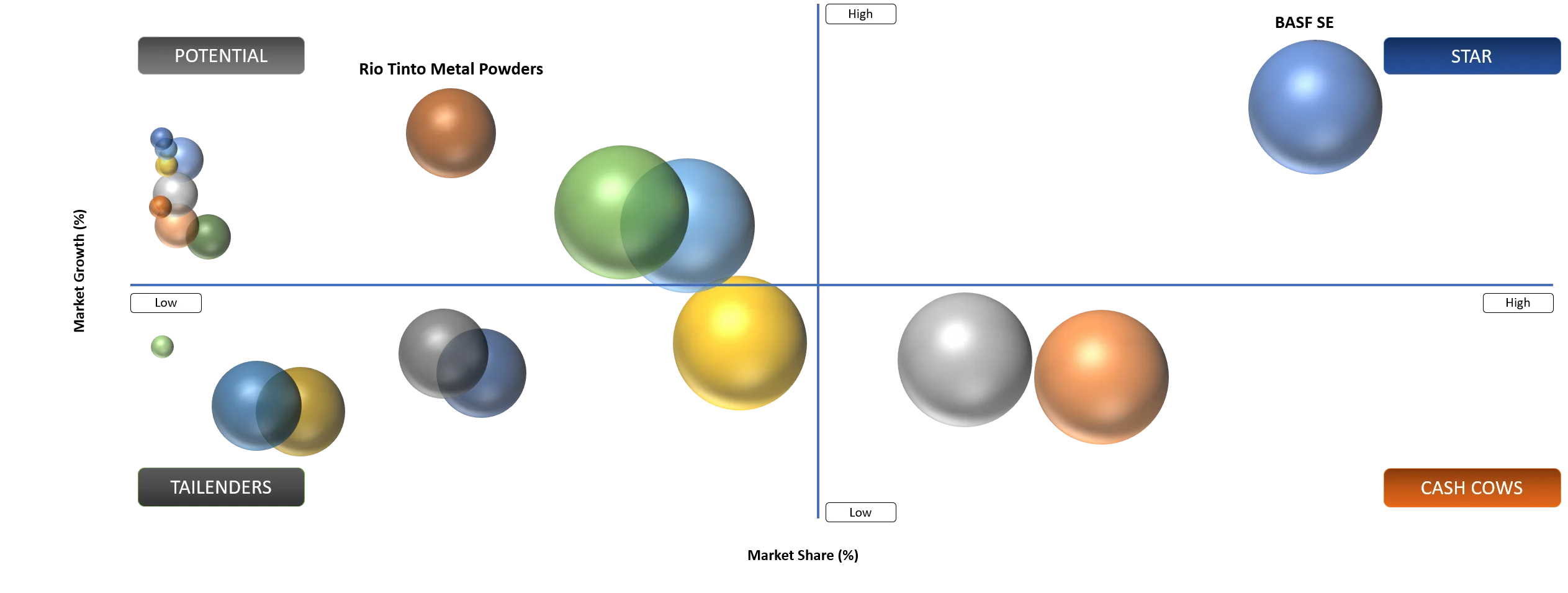

Star

Star players include BASF SE, Epson Atmix Corporation, Höganäs AB, Sandvik AB, Indo-MIM Private Limited, Elnik Systems, LLC and GKN Powder Metallurgy GmbH. These companies hold strong positions through feedstock expertise, powder quality, manufacturing capability, equipment support or customer qualification depth.

Potential

Potential companies include Plansee Group, Rio Tinto Metal Powders and MIMPlus Technologies GmbH and Co. KG. Plansee can grow in tungsten and refractory metal applications, Rio Tinto Metal Powders can benefit from ferrous powder scale and MIMPlus can expand through application-specific manufacturing support. Movement into stronger leadership positions will depend on customer qualification, specialty grade depth and regional support.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted End-User | Strategic Impact |

Miniaturized Complex Parts Push Manufacturers Toward MIM Where Machining Loses Efficiency | High | Electronics, Medical and Automotive | Micro Components and Precision Parts | Supports high-flow and fine-tolerance feedstock demand |

Medical and Electronics Buyers Need Tighter Dimensional Consistency In Small Metal Parts | High | North America, Europe and Asia-Pacific | Medical and Consumer Electronics | Raises demand for qualified feedstock |

Feedstock Quality Becomes Strategic As Geometry Gets Smaller and Tolerance Windows Tighten | Medium To High | Global MIM Houses | Fine-Tolerance Feedstock | Increases supplier switching barriers |

Miniaturized Complex Parts Push Manufacturers Toward MIM Where Machining Loses Efficiency

Miniaturization is the strongest demand driver because conventional machining becomes costly when parts are small, complex and produced at high volume. MIM allows complex shapes, internal features and small structural elements to be formed near net shape. This reduces machining steps and improves repeatability.

Consumer electronics and medical devices are the clearest use cases. Devices need smaller metal components that still provide strength, wear resistance and precision. MIM feedstock must flow into small cavities and retain dimensional stability through debinding and sintering.

Automotive and industrial tools also support demand. Sensors, locks, connectors, small gears and wear-resistant parts can benefit from MIM where part complexity is high. Suppliers that help customers redesign components for MIM can create new demand.

Restraint Impact Analysis

| Restraint | Drag On Market Growth | Primary Impact Area | Impacted End-User | Strategic Impact |

Qualification Cycles Remain Long In Medical Aerospace and Defense Programs | High | Regulated Applications | Medical, Aerospace and Defense | Slows supplier switching and new adoption |

Binder Debinding and Sintering Sensitivity Limit Easy Supplier Switching | High | Feedstock Performance | All Precision Parts | Raises validation burden |

Feedstock Variability Can Materially Change Part Economics | Medium To High | MIM Production | High-Precision Structural Parts | Increases scrap risk |

Binder Debinding and Sintering Sensitivity Limit Easy Supplier Switching

MIM feedstock is not a simple raw material. A change in binder or powder behavior can affect molding, debinding, shrinkage and final density. MIM houses hesitate to change feedstock because process revalidation can be costly and risky.

Debinding sensitivity is especially important. Improper binder removal can cause cracks, distortion and internal defects. Sintering also introduces shrinkage that must be predictable. Small parts with tight tolerances leave little margin for variation. Medical, aerospace and defense programs face the highest switching barriers. Even if a new feedstock offers cost savings, qualification work can slow adoption. Suppliers with proven process stability and strong technical support have an advantage.

Segment Analysis

Stainless Steel Will Continue To Lead Material Demand

Stainless steel will remain the leading material because it offers a practical balance of corrosion resistance, strength, availability and processing familiarity. Medical instruments, consumer electronics components, locks, connectors and industrial parts often use stainless steel MIM materials.

MIM houses understand stainless steel processing well, which reduces adoption risk. Feedstock systems are widely available and sintering behavior is established. This makes stainless steel the default material for many small precision parts. High-value applications still require tight control. Medical and electronics customers need consistent surface finish, dimensional stability and lot-to-lot quality. Suppliers that provide documented stainless steel feedstock and processing guidance can defend share.

Soft Magnetic Alloys Are Becoming A High-Value Growth Pocket

Soft magnetic alloys are gaining demand because compact motors, sensors, actuators and electromagnetic devices need complex magnetic parts. MIM can create geometries that support compact design and assembly reduction.

Magnetic performance depends on powder chemistry, sintering profile and microstructure. Feedstock suppliers must support customers with material data and process guidance. A small variation can influence magnetic properties and final device performance. Electronics and automotive electrification support this opportunity. Sensors, actuator housings and magnetic cores are becoming smaller. MIM can serve selected applications where complexity and volume justify tooling.

Micro MIM Feedstock Will Gain Strategic Importance

Micro MIM feedstock is a high-growth performance category because small parts require tighter flow and shrinkage control. Standard feedstock may not fill tiny features consistently. Fine powders and optimized binders are needed.

Medical and electronics applications are the strongest adopters. Micro tools, device components, camera parts, connector elements and wearable hardware need high repeatability. Defect cost can be high because small components may be part of expensive assemblies. Micro MIM creates stronger supplier retention. Once a feedstock is validated for a tiny part, switching risk is high. Suppliers with proven micro MIM grades and application support can command premium value.

Market Segmentation

- By Material

- Stainless Steel

- Low Alloy Steel

- Soft Magnetic Alloys

- Titanium

- Tungsten Heavy Alloys

- Copper Alloys

- By Feedstock Performance

- Standard Feedstock

- High Flow Feedstock

- Fine-Tolerance Feedstock

- Micro MIM Feedstock

- Application-Specific Feedstock

- By Part Complexity

- Micro Components

- Thin-Wall Parts

- High-Precision Structural Parts

- Magnetic Components

- Wear-Resistant Parts

- By Manufacturing Support

- Powder Supply

- Compounded Feedstock

- Co-Development Programs

- Debinding Support

- Sintering Optimization

- By End-User

- Medical

- Automotive

- Consumer Electronics

- Industrial Tools

- Defense

- Aerospace

Geographical Penetration

Asia-Pacific Metal Injection Molding Powders and Feedstock Market Growth Outlook

Asia-Pacific remains the largest market because electronics, medical devices, automotive components and precision manufacturing are concentrated across China, Japan, South Korea, India, Malaysia and Singapore. Regional MIM houses need stable powder and feedstock supply to serve fast-moving programs.

China supports volume demand through electronics, automotive and industrial components. Local MIM production is large, but high-performance feedstock and specialty powders remain important for precision programs. Domestic suppliers are improving quality, creating stronger competition.

Japan and South Korea support premium demand because manufacturing quality standards are high. Epson Atmix, Mitsubishi Materials, Nippon Piston Ring and other regional companies contribute to technical depth. Buyers prioritize consistency and documentation. India is emerging through medical devices, automotive components and precision manufacturing. Indo-MIM gives India strong global relevance in MIM production. Local feedstock and powder support can strengthen the country’s position.

North America Metal Injection Molding Powders and Feedstock Market Demand Analysis

North America is a high-value market because medical, defense, aerospace, automotive and industrial customers require qualified components. The U.S. is the largest country market and supports demand for stainless steel, titanium, tungsten heavy alloys and specialty feedstock.

Medical device applications are important because small precision metal parts need documentation and repeatability. Feedstock suppliers serving medical customers need traceability and stable specifications. Qualification protects incumbent suppliers once approved. Defense and aerospace applications support demand for specialty alloys and high-performance parts. Adoption can be slower due to qualification cycles, but margins are attractive. Suppliers with documentation and technical support are better positioned.

Europe Metal Injection Molding Powders and Feedstock Market Competitive Landscape

Europe remains a premium market for precision components, automotive systems, medical devices and industrial tools. Germany, UK, France, Italy and Czech Republic support demand through advanced manufacturing and regulated applications. Germany is central due to automotive engineering, industrial tools and precision manufacturing. Buyers value process reliability, documentation and co-development. Feedstock suppliers that can support qualification are preferred. UK and France support aerospace, medical and defense applications. Smaller volumes can still generate high value because material requirements are strict. Technical service and documentation are critical.

India Metal Injection Molding Powders and Feedstock Market Expansion Trends

India is growing as a MIM production and export base. Indo-MIM has built strong global visibility and regional manufacturing depth. Medical devices, automotive, aerospace and industrial components are creating demand for powders and feedstock.

Local supply development is an opportunity. Indian MIM houses need reliable feedstock with technical support. Imported feedstock can create lead-time and cost risk. Localized compounding could improve responsiveness. Qualification remains the main barrier. Export customers need consistent material documentation and process control. Suppliers that can support international standards will gain stronger traction.

Competitive Landscape

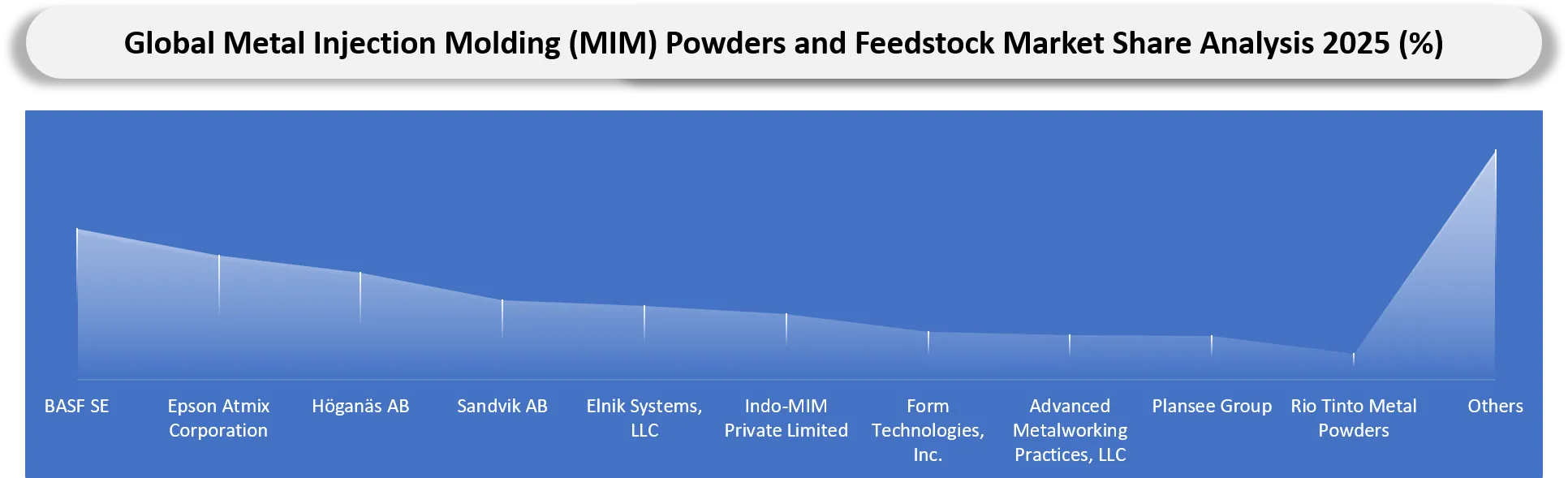

- Competition is split between powder producers, feedstock suppliers, MIM component manufacturers, furnace and debinding equipment providers and application engineering companies.

- BASF, Epson Atmix, Höganäs and Sandvik hold strong relevance in powder and feedstock supply, while Indo-MIM, Form Technologies, GKN Powder Metallurgy, CMG Technologies and MIMPlus hold strength through manufacturing and applicastion execution.

- Elnik Systems is relevant because debinding and sintering systems influence final part quality. Equipment suppliers can shape feedstock adoption by supporting stable processing windows.

- Competitive benchmarking should track powder consistency, feedstock rheology, binder system reliability, sintering support, medical documentation, local supply and co-development capability.

Company List

- BASF SE

- Epson Atmix Corporation

- Höganäs AB

- Sandvik AB

- Elnik Systems, LLC

- Indo-MIM Private Limited

- Form Technologies, Inc.

- Advanced Metalworking Practices, LLC

- Plansee Group

- Rio Tinto Metal Powders

- ARC Group Worldwide, Inc.

- MIMPlus Technologies GmbH and Co. KG

- Mitsubishi Materials Corporation

- GKN Powder Metallurgy GmbH

- CMG Technologies Ltd.

- Smith Metal Products

- CN Innovations Holdings Ltd.

- Nippon Piston Ring Co., Ltd.

- Mimtech Sdn. Bhd.

- PIM International Ltd.

Company Coverage Preview

BASF SE remains a major reference point through its Catamold feedstock platform and long-standing position in MIM feedstock. BASF’s strength lies in feedstock formulation, processing familiarity and customer qualification history. The company is well positioned where MIM houses need dependable compounding and debinding behavior.

Epson Atmix Corporation and Höganäs AB are important because metal powder quality is central to MIM success. Powder particle size distribution, chemistry, flow and purity influence feedstock consistency and final part performance. These suppliers support the material base that enables MIM growth across precision applications.

Indo-MIM Private Limited, Elnik Systems, LLC, Form Technologies, Inc., MIMPlus Technologies GmbH and Co. KG, GKN Powder Metallurgy GmbH and CMG Technologies Ltd. add value through manufacturing, processing and application support. The market increasingly rewards companies that connect material knowledge with final component performance.

Major Pain Points

- Feedstock variation can change shrinkage and final part acceptance.

- Medical and aerospace qualification cycles slow supplier switching.

- Debinding defects can create cracks, distortion and scrap.

- Micro MIM requires tighter particle size and flow behavior.

- Specialty alloy powders can face supply and cost volatility.

- MIM houses need earlier design support to avoid manufacturability problems.

- Regional supply gaps can delay high-volume production.

- Small defects can cause large product-level failures.

Recent Developments

- February 2026: Tube Investments of India announced a majority acquisition plan for Orange Koi, signaling stronger Indian investment in MIM and advanced precision manufacturing.

- 2025: BASF continued supporting MIM customers through its established Catamold feedstock platform for high-volume precision metal parts.

- 2025: Indo-MIM continued expanding its relevance in global precision component manufacturing through MIM, ceramic injection molding, additive manufacturing and metal powder capabilities.

- 2025: Elnik Systems continued supplying debinding and sintering solutions used by MIM manufacturers seeking tighter process control and stable part quality.

- 2025: Höganäs continued positioning metal powders for powder metallurgy and precision applications where chemistry and particle consistency influence final component performance.

Analyst View and Opinion

- MIM powders and feedstock will remain a precision manufacturing market rather than a commodity powder market.

- Stainless steel will continue to dominate because it has broad application fit and established processing familiarity.

- Soft magnetic alloys and micro MIM feedstock will create higher-value growth pockets.

- Asia-Pacific will remain the largest region due to electronics and precision manufacturing concentration.

- Medical and aerospace programs will protect qualified suppliers because switching requires validation.

- Feedstock suppliers that offer process support will outperform suppliers selling material alone.

- Localized feedstock supply will become more important as regional MIM houses expand.

- AI and process analytics will improve yield but physical validation will remain essential.

- Component complexity will remain the strongest demand trigger.

- Supplier advantage will depend on shrinkage control, debinding behavior, documentation and co-development support.

Target Audience

| Industry | Who Should Buy This Report? | Reason To Buy This Report |

| MIM Component Manufacturers | Production Leaders, Technical Teams, Sourcing Teams | Evaluate powder and feedstock demand, supplier risk and process support |

| Medical Device Companies | Materials Teams, Procurement Teams | Understand precision component supply and qualification requirements |

| Electronics Manufacturers | Product Engineering Teams | Track micro component and high-volume part opportunities |

| Automotive Suppliers | Component Engineers, Purchasing Teams | Assess MIM use in small structural and functional parts |

| Powder Producers | Strategy Teams, Product Managers | Identify demand for stainless steel, magnetic and specialty powders |

| Feedstock Suppliers | Commercial Teams, Application Engineers | Evaluate application-specific feedstock opportunities |

| Investors | Advanced Manufacturing Investors | Assess growth pockets in precision powder and feedstock supply |

| Consulting Firms | Manufacturing and Materials Teams | Support market entry, supplier benchmarking and production strategy |

What DataM Uniquely Provides

- DataM maps demand by material, feedstock performance, End-User, part complexity, manufacturing support and region.

- DataM separates powder supply from compounded feedstock and application development support.

- DataM evaluates how micro MIM, soft magnetic components and medical applications influence premium demand.

- DataM benchmarks suppliers across powder consistency, feedstock behavior, debinding support and sintering optimization.

- DataM tracks regional manufacturing shifts across Asia-Pacific, North America and Europe.

- DataM provides import-export indicators for metal powders, titanium, tungsten, copper powders and precision parts.