Lithium Salts Market Overview

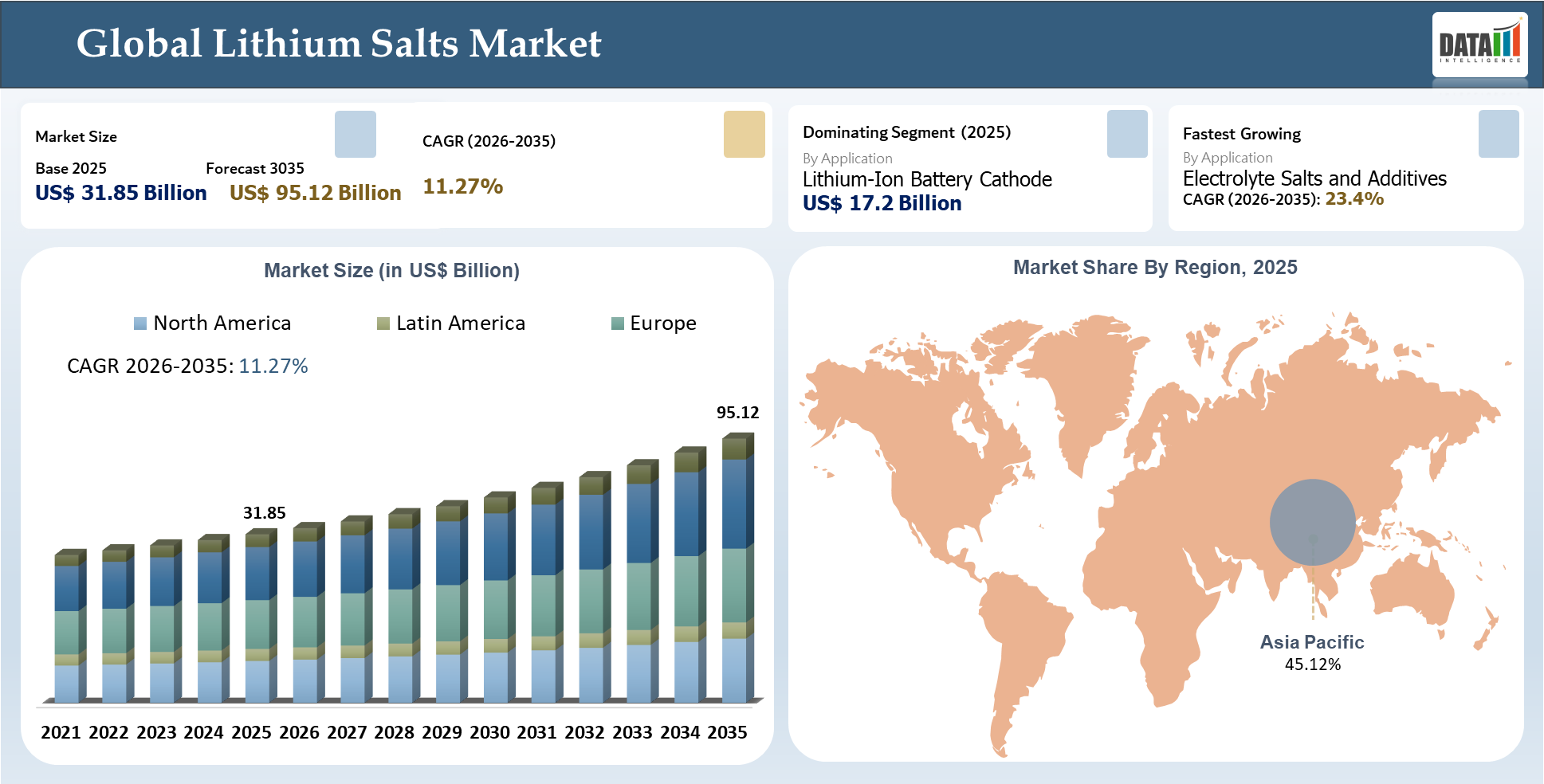

The global lithium salts market stood at US$ 31.85 billion in 2025 and is projected to hit US$ 95.12 billion by 2035, marking a CAGR of 11.27% through the forecast years 2026-2035. The global Lithium Salt Market is now emerging as one of the strategic markets in the overall battery material and specialty chemicals sector driven by the exponential growth of the electric vehicles and other uses of renewable energy, among others. The major lithium salts include lithium carbonate, lithium hydroxide, lithium chloride, and lithium bromide used in various applications ranging from lithium-ion batteries, pharmaceuticals, lubricants, ceramic industries, glass making, and even chemical manufacturing. Nonetheless, the largest demand for the lithium salts market is now being fueled by demand for lithium salts in batteries.

Growing demand for EV battery material components is one of the factors driving the growing market demand for lithium salt products. This is because lithium salts are key ingredients in battery chemistry especially with growing trend of battery cathodes containing more nickel which requires better lithium salt chemistry to optimize performance. On the other hand, the lithium carbonate production process is still commercially relevant because of its widespread applications in various battery types and lithium conversions.

The competitive landscape is becoming driven by advances in lithium refining technology such as spodumene processing, brine production, direct lithium extraction, and lithium recovery via recycling technology. In light of improved government policies on critical minerals and localization of the battery value chain, lithium salt companies are focused on refining scale, lithium purity, sustainability, and lithium supply agreements. Firms with end-to-end refining and processing capabilities are likely to be better positioned for success in the developing world of lithium salts.

AI Impact Analysis

The use of AI in decision-making processes is anticipated to have a positive impact on the global lithium salts market in areas such as exploration, refining, quality management, pricing intelligence, and logistics. As regards upstream sourcing of lithium salts, AI-powered geological models could assist firms in pinpointing sources of brines, clay minerals, and lithium deposits. The use of AI technologies in lithium salt refining and conversion could ensure better process control through the tracking of impurities, performance, energy consumption, and chemical uniformity during the production of lithium carbonate, lithium hydroxide, and specialty salts.

As for battery-grade lithium salts, the deployment of AI solutions in quality analytics could help producers achieve higher levels of quality management and minimize the risk of lithium salt batches rejection due to deviations from purity standards. Procurement of lithium salts can benefit from AI tools that could monitor the changes in the price dynamics, demand for lithium salts, inventory availability, logistics bottlenecks, and off-take agreements. Finally, recycling facilities could optimize their operations through the application of AI solutions for battery sorting, lithium materials recovery, and salt purification.

Lithium Salts Market Key Takeaways

- Product type still represents the most practical way to analyze this market because lithium carbonate, lithium hydroxide, lithium chloride and other lithium compounds have various applications in batteries, industries, medicines and special chemicals.

- The growing demand is becoming more focused on lithium carbonate and lithium hydroxide for batteries, storage facilities and cathodes.

- Asia-Pacific still dominates the competitive dynamics, with the influence of China, Japan and South Korea in processing facilities, batteries and purchasing policies.

- Success lies in companies having integrated mining, processing, purification and customer qualification processes, allowing them to cope with price fluctuations, sign up supply agreements and produce battery-grade lithium compounds.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 31.85 Billion | |

| 2035 Projected Market Size | US$ 95.12 Billion | |

| CAGR (2026-2035) | 11.27% | |

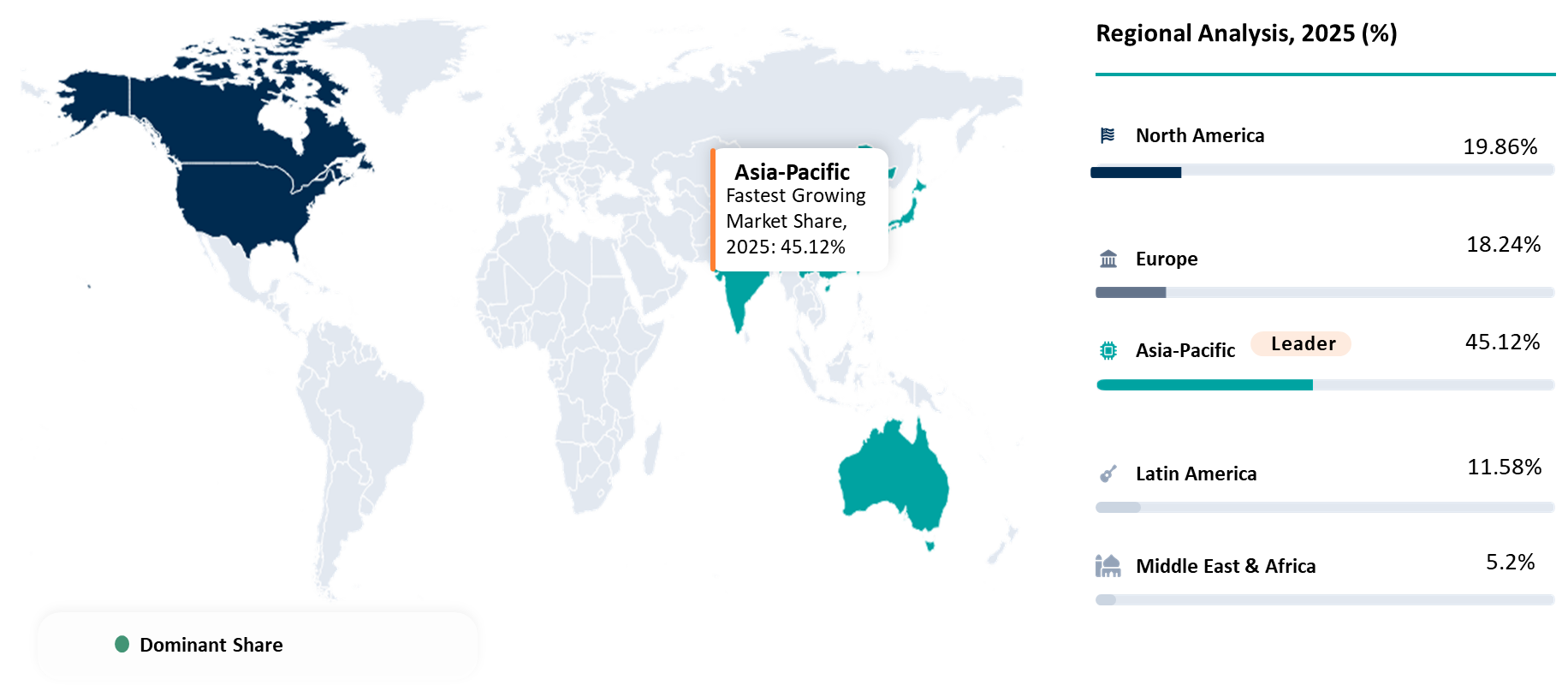

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Salt Type | Lithium Carbonate, Lithium Hydroxide, Lithium Chloride, Lithium Fluoride, Lithium Bromide, Lithium Sulfate, Lithium Nitrate, Lithium Acetate, Lithium Hexafluorophosphate, and Others | |

| By Grade | Battery Grade, Technical Grade, Pharmaceutical Grade, and High Purity Grade | |

| By Source | Brine Based Lithium Salts, Mineral Based Lithium Salts, Clay Based Lithium Salts, Lepidolite Based Lithium Salts, and Recycled Lithium Salts | |

| By Application | Lithium-Ion Battery Cathode, Electrolyte Salts and Additives, Glass and Ceramics, Lubricating Greases, Pharmaceuticals, Air Treatment and Dehumidification, Metallurgy and Aluminum Processing, Polymer and Chemical Synthesis, and Others | |

| By End Use Industry | Automotive, Consumer Electronics, Energy and Utilities, HVAC-R, Glass and Ceramics, Pharmaceuticals, Chemicals, Metallurgy, and Others | |

| By Distribution Channel | Direct Supply, Distributor Sales, and Specialty Chemical Suppliers | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

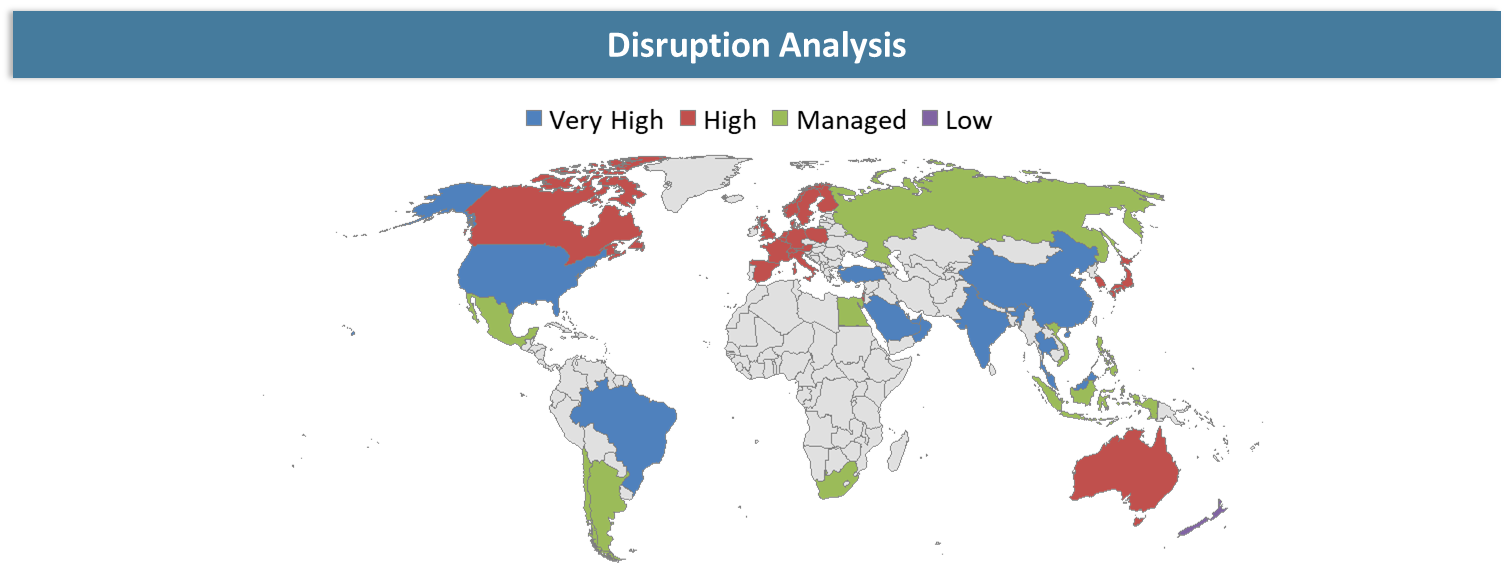

Disruption Analysis

Shift Toward Integrated Refining, Supply Localization and Battery-Grade Qualification Reshaping Competitive Dynamics in the Lithium Salts Market

Disruption in the global lithium salts market is being caused by the shift from resource ownership to competency in the provision of qualified chemicals. Access to mineral resources is not enough anymore since consumers demand the same level of consistency when it comes to lithium carbonate, lithium hydroxide, and lithium hexafluorophosphate. The process shifts the focus of the value chain away from the mining stage towards the refining and conversion stages. Refining companies and chemical suppliers who can qualify for high standards of purity and quality can become more valuable and influential in the market.

Another major disruptive factor is the tendency to localize production within each region. For example, North America, Europe, and India are now building their own refining and recycling capabilities to diversify their dependence on a limited number of regions where the lithium industry concentrates.

The development of downstream capabilities is another important aspect of disruption within the industry. Companies that have a comprehensive set of processes, including sourcing, purification, logistics, and even customer qualification, are able to enter into long-term agreements and maintain their supply chains stable.

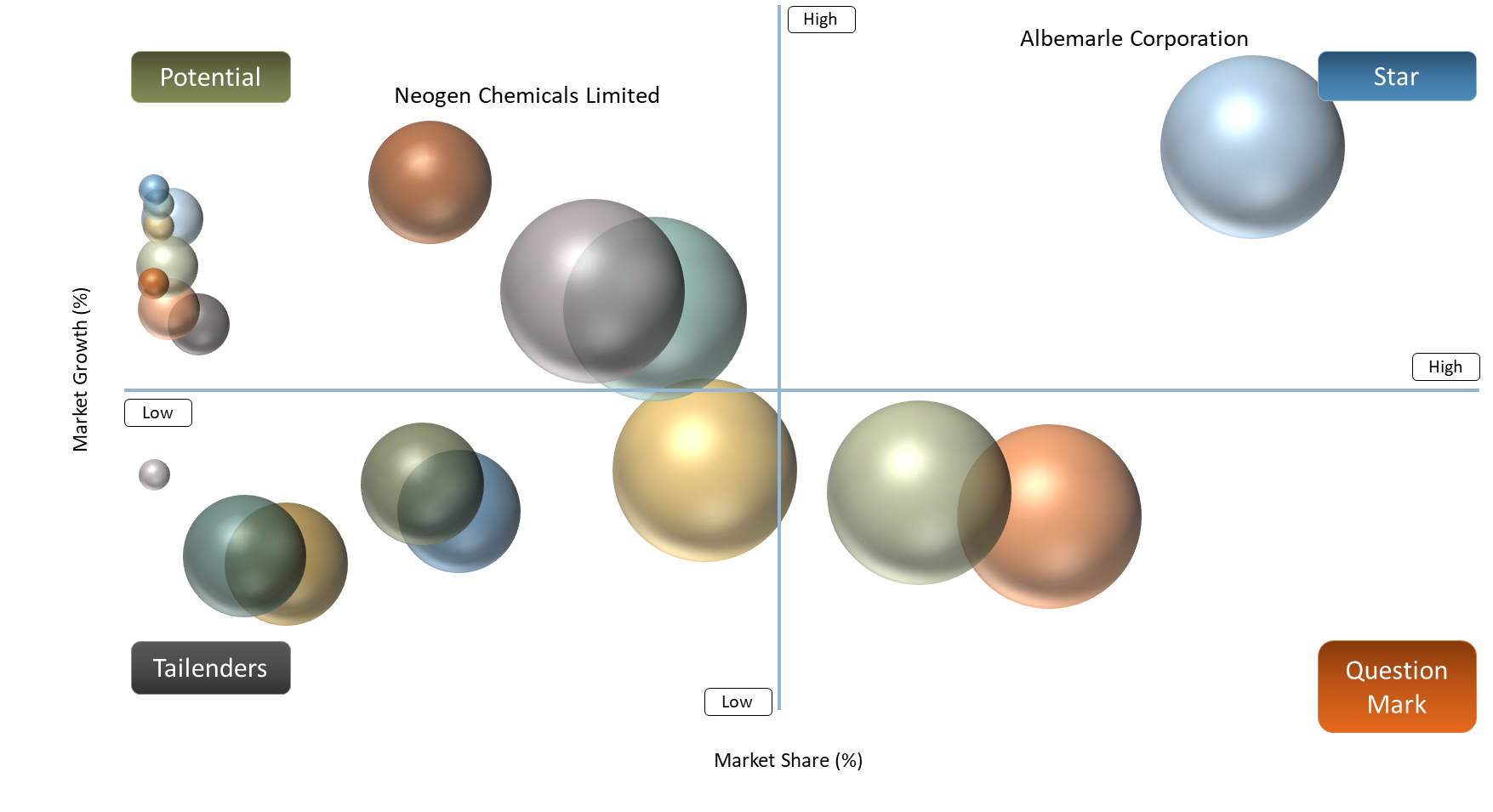

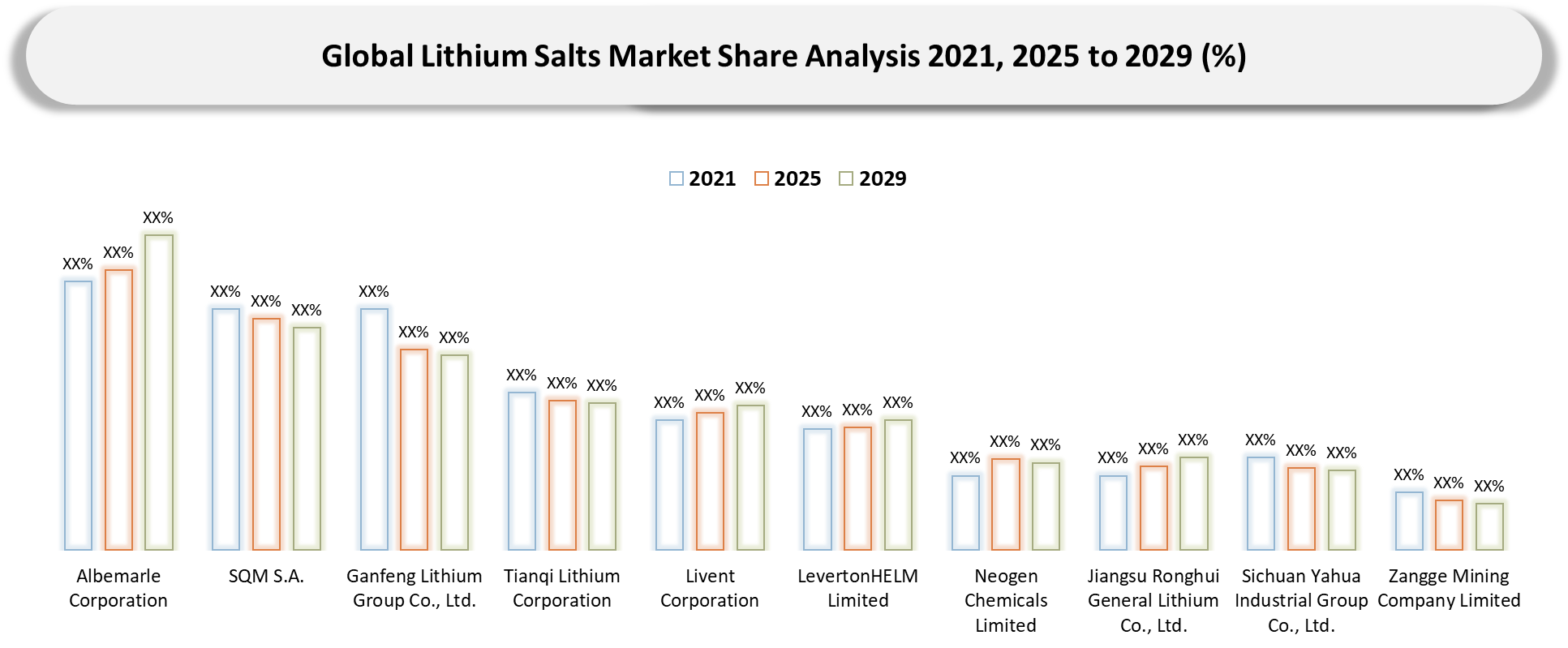

BCG Matrix: Company Evaluation

In the global lithium salts market, Stars refer to companies with robust lithium chemical portfolio, advanced refinement capacity and exposure to battery demand growth. Examples of companies that can be considered Stars include Albemarle Corporation, SQM S.A., Ganfeng Lithium Group Co., Ltd. and Tianqi Lithium Corporation because of their integrated chain structure, global lithium conversion assets and positioning on lithium carbonate and lithium hydroxide market segment. Such companies benefit from long-term partnerships with battery producers and expanding role in the EV supply chains.

Cash Cows include existing specialized producers of lithium salts and experienced chemicals providers such as LevertonHELM Limited, Livent Corporation and Neogen Chemicals Limited, with diversified revenues earned thanks to wide application range in industrial, pharmaceutical and other segments. The companies occupy advantageous market position thanks to the use of technical capabilities, quality standards and experience in working with industrial customers.

Question Marks include new regional refiners and lithium salt suppliers such as Jiangsu Ronghui General Lithium, Sichuan Yahua Industrial Group Co., Ltd., Zangge Mining Company Limited and Jiangxi Special Electric Motor Co., Ltd. They work in fast-growing markets, but need to develop their activities internationally, build customer base and downstream operations.

Market Dynamics

Battery-Grade Lithium Salts Remain Critical Feedstock for EV and Energy Storage Battery Manufacturing

Lithium salts are now seen as a strategic raw material in the manufacture of batteries for EVs and battery energy storage devices, since lithium carbonate and lithium hydroxide form an integral part of the battery cathode chemistry. Lithium compounds affect the performance, efficiency, stability, and life cycle of battery cells, and thus are critical in terms of their purity and uniformity. The link between lithium salt consumption and demand for batteries is quite clear since over 17 million electric vehicles were sold globally in 2024, up from last year's 25%. This accounts for more than 20% of all new cars sold globally.

As EV and stationary storage capacity expands, battery manufacturers are increasingly dependent on qualified suppliers that can provide high-purity lithium salts with low impurity levels, consistent particle characteristics and reliable batch-to-batch performance. Unlike standard industrial lithium chemicals, battery-grade materials require stricter purification, technical validation and long customer qualification cycles. This is pushing cathode producers, cell manufacturers and automakers to secure long-term supply agreements with lithium refiners and converters. The market growth is therefore not only about lithium availability, but also about the ability to deliver battery-grade salts at commercial scale. As battery supply chains localize across Asia-Pacific, North America and Europe, lithium salts will remain a foundational material supporting electrification, renewable energy storage and long-term energy transition strategies.

Lithium Price Volatility and Supply Concentration Create Procurement Uncertainty for Battery and Specialty Chemical Manufacturers

The fluctuating price of lithium continues to be a huge constraint in the global lithium salts market because of the uncertainties involved in procurement. The prices of lithium carbonate and lithium hydroxide are determined by trends in EVs as well as new capacities added for refining lithium chemicals and lithium inventory situations. Sudden jumps in prices increase costs while falls pose risks of inventory write-offs and contract renegotiations.

Supply is another source of risk because there is concentration in both lithium mining and refining processes in a few countries, including Australia, Chile, Argentina, and China. According to the International Energy Agency, China accounted for nearly 65% of global lithium chemical refining capacity in 2023, creating strong dependence on a concentrated processing ecosystem. This exposes buyers to geopolitical risk, export policy changes, logistics disruptions and regional production constraints.

Furthermore, the battery-grade lithium salts need considerable time for certification processes. Hence, suppliers cannot change quickly when faced with supply chain disruptions. Consequently, companies in the lithium salts market are trying to diversify their suppliers, build regional relationships, and secure long-term contracts for procurement purposes.

Segmentation Analysis

The global lithium salts market is segmented based salt type, grade, source, application, end use industry, distribution channel, and region.

Lithium-Ion Battery Cathode Materials in Application Segment Leads Demand Through Expanding EV and Energy Storage Production

Lithium-Ion Battery Cathode is the leading in Application segment of the global lithium salts market owing to the extensive usage of lithium carbonate and lithium hydroxide salts in the manufacturing of cathode materials. These lithium salts serve as crucial raw materials for the manufacture of battery chemistry that is used in electric vehicles, electronic products, and energy storage applications.

Production of cathode materials demands purity and consistent chemical composition in lithium salts. Lithium salt companies that meet this criterion have an edge over others in the competition, as switching between suppliers is a tough task for lithium battery manufacturers that entails technical verification, quality assurance and product qualification. Of take agreements signed between lithium salt manufacturers, cathode manufacturers and battery producers further contribute to the growth of the segment. The supremacy of this segment is likely to persist as efforts towards global electrification, renewable energy storage, and battery localization quicken their pace. Lithium salts employed in cathode production will be the key drivers for demand, rendering this segment the most lucrative application segment within the market.

Geographical Penetration

Asia Pacific Leads the Lithium Salts Market Through lithium refining technologies and Battery Manufacturing Dominance

Asia Pacific holds an overwhelming dominance in the global lithium salts market owing to its robust lithium refining capacity, battery manufacturing environment, and high requirement of lithium salts from sectors like electric vehicles, consumer electronics, and energy storage systems. The region derives a distinct advantage in the presence of a robust supply chain including processes such as lithium conversion, cathode manufacturing, and battery cell manufacturing. Some of the leading countries driving lithium salts demand in the region include China, Japan, South Korea, and India backed by the presence of increasing investment in battery materials and clean energy technologies. Among all countries, China stands as the leader owing to high lithium refining capacity which makes China the global leader in manufacturing of lithium carbonate, lithium hydroxide, and specialty lithium salts. Industry analysts suggest that Asia Pacific held more than 45.12% share in the global lithium salts market in 2025. Favorable government policies, manufacturing economics, and increased adoption of electric vehicles continue to drive the regional market growth. Besides, growing investment in battery giga factories and energy storage systems related to renewable energy systems add to regional dominance.

China Lithium Salts Market Trends

The Chinese lithium salts market is underpinned by its dominant presence in lithium refinery, cathodes manufacturing, cell-making and vehicle production industries. Currently, the country still constitutes a notable demand center for lithium carbonate, lithium hydroxide and lithium hexafluorophosphate, underpinned by significant consumption of these lithium salts by the LFP, NMC and other battery technologies. One of the most prominent industry trends is the development of battery grade lithium salt manufacturing, due to the need for high-quality lithium raw material by domestic batteries producers. Other trends in this market relate to supply diversification strategies pursued by Chinese companies via investments abroad and offtake agreements for lithium salts. According to the International Energy Agency data, in 2023, China had more than 65% share of lithium chemicals refining capacity across the world. Recycling of lithium salts is becoming increasingly important since more lithium is being reused by converting it to useable form for batteries. Price volatility is one of the defining features of the market, where lithium carbonate is subject to rapid changes influenced by EV demand and changes in supplies and inventories.

India Lithium Salts Market Outlook

The Indian Market for lithium salt is forecasted to grow steadily due to increasing demand for electric vehicles, energy storage systems, consumer electronics, and localization of battery manufacturing in India. Currently, the Indian market is dependent on imports from overseas markets for key lithium salts such as lithium carbonate, lithium hydroxide, and electrolyte derivatives. Hence, there are opportunities for refining operations, recycling of lithium salt materials, and establishment of long-term procurement agreements. Demand for the Indian Lithium Salt market is closely tied with growth in lithium-ion battery manufacturing as any increase in battery production in India will be required to have access to battery grade lithium salt materials with assured purity. An important demand factor driven by government policy in India includes the ACC battery PLI scheme which has budget allocation of ₹18,100 crore for achieving 50 GWh of battery manufacturing capacity in India. This would increase demand for Lithium salt materials used in cathodes and electrolyte applications. Though the domestic lithium production is at nascent stages, the Indian market is likely to shift towards localization of their supply chains.

Competitive Landscape

- The market for lithium salts around the world can be considered to be moderately concentrated. The factors influencing competition within this sector include the extent of refining capabilities, product qualification for batteries, purity of products and long-term agreements between companies. Integrated firms like Albemarle Corporation, SQM S.A., Ganfeng Lithium Group Co., Ltd., Tianqi Lithium Corporation and Livent Corporation occupy a prominent position on account of their ability to produce lithium carbonate and lithium hydroxide, global distribution network and business ties with battery materials producers.

- There are other firms engaged in the production of lithium salts that are classified as specialty/ regional suppliers like LevertonHELM Limited, Neogen Chemicals Limited, Jiangsu Ronghui General Lithium Co., Ltd., Sichuan Yahua Industrial Group Co., Ltd., Zangge Mining Company Limited, Jiangxi Special Electric Motor Co., Ltd., Shanghai Zhongli Industrial Co., Ltd. and Mody Chemi Pharma Limited. Their competitiveness stems from the production of specialty lithium salts, regional strength, production of customized grades and applicability to industrial sectors. Competition within this market will be moving away from the availability of lithium into the use of highly pure salts used in batteries, pharmaceuticals, chemicals and HVAC-R.

Key Developments

- April 2026: Huayou Cobalt exported Africa’s first lithium sulphate from Zimbabwe, processed at its US$400 million plant with 50,000 tons annual capacity, strengthening Africa’s role in downstream lithium salt supply.

- February 2026: Albemarle Corporation announced plans to idle its Kemerton lithium hydroxide plant in Australia, while continuing to serve customers through other production channels, reflecting cost discipline amid lithium price volatility.

- March 2026: Albemarle Corporation projected 2026 lithium demand growth of 15-40% year-on-year, supported by EV, energy storage and battery supply-chain recovery, reinforcing long-term demand visibility for lithium carbonate and hydroxide.

- March 2026: SQM indicated strong lithium volume momentum and expected global lithium demand to grow around 25% in 2026, supported by recovering battery demand and supply disruptions.

- April 2026: Ganfeng Lithium Group Co., Ltd. forecast a return to profitability in Q1 2026, estimating net profit of RMB 1.6-2.1 billion, signaling margin recovery for integrated lithium salt producers.

- February 2025: Ganfeng Lithium Group Co., Ltd. started production at the Mariana project in Argentina, targeting 20,000 tons per year of lithium chloride, improving upstream security for battery-grade lithium salt production.

- July 2025: Codelco secured regulatory approval for lithium extraction quotas linked to the SQM partnership, enabling potential long-term production of up to 330,000 tons LCE annually after 2031.

- November 2025: China conditionally approved the Codelco–SQM lithium joint venture, with conditions focused on maintaining stable lithium carbonate supply to Chinese customers.

- January 2024: Livent and Allkem completed their merger to form Arcadium Lithium, creating a larger integrated lithium chemicals platform with lithium carbonate, hydroxide and spodumene assets across Argentina, Australia, Canada and Japan.

- March 2024: Tianqi Lithium participated in drafting the first global product carbon footprint guidelines for battery-grade lithium carbonate and lithium hydroxide, highlighting the shift toward traceability and low-carbon lithium salts.

- October 2024: Rio Tinto agreed to acquire Arcadium Lithium for about US$6.7 billion, marking a major consolidation move in lithium chemicals and positioning Rio Tinto as a stronger player in lithium carbonate and hydroxide supply.

White Space Opportunities

As per DataM, opportunities in the global lithium salts market extend far beyond traditional lithium carbonate and lithium hydroxide products. The key white space in the global market is related to battery-grade lithium salts, in which demand is growing due to purity, traceability, and long-term supply stability needs of EV battery, cathode material, and electrolyte manufacturers. One more potential white space is lithium salts refinement and production localization in North America, Europe, and India where producers seek ways to minimize imports of lithium salts and other chemicals. Opportunities associated with recycled lithium salts have also become relevant in connection with EV battery recycling and growing requirements to use circular and ESG-oriented raw materials.

One more white space opportunity is specialty lithium salts including lithium hexafluorophosphate, lithium bromide, lithium fluoride, and lithium chloride used in electrolytes, HVAC-R applications, pharmaceuticals, lubricants, and chemical synthesis. Producers able to deliver custom-made products, offer technical expertise, and have advantages regarding logistics will be able to compete with pure commodities providers. There is also increased potential for joint efforts by lithium miners, lithium salts suppliers, battery material producers, carmakers, and recyclers to develop sustainable supply chains.

DMI Opinion

DataM Intelligence sees the Global Lithium Salts Market transitioning towards an era where competitive differentiation would not solely rely on lithium mining capabilities but also require downstream chemical expertise. While lithium extraction continues to be significant, the industry is moving towards firms which can provide high-quality salt products with consistent purity levels and have established refineries and qualification procedures.

There is growing differentiation within the global lithium salts market between lithium mineral commodity firms and lithium chemical specialists. The focus of battery producers and other industries is increasingly on establishing long-term relationships based on reliability of supply and consistency of performance. This provides an opportunity for conversion plants, purification methods and regional refineries.

According to DataM Intelligence, lithium salts are now seen as an integral component in various industrial sectors and subject to policies relating to energy, localization and downstream production. Although lithium salts demand is subject to cyclicality and fluctuations in raw material costs associated with battery consumption, their overall demand is likely to grow significantly driven by trends towards electrification.

Why Choose DataM?

- Lithium Salt Portfolios' Insights: Includes the major lithium salts including lithium carbonate, lithium hydroxide, lithium chloride, lithium bromide, lithium fluoride, lithium hexafluorophosphate and more.

- Evaluation of Grades of Li Salts: Evaluates the demand for various grades of lithium salts including battery grade, technical grade, pharmaceutical grade and high purity grade.

- Sources of Li Salts' Evaluation: Evaluates the sources of Li salts including brines, mineral ores, clays, lepidolite and recycles.

- Li Salts' Consumption Insights: Assesses the demand for Li salts from various segments including battery cathode material, electrolyte salts and their additives, glass and ceramics, greases, pharmaceutical industry, HVAC-R and others.

- Pricing & Procurement Insights: Offers insights about the pricing, contract negotiations for long term supplies and offtake agreements, and other procurement related topics of concern.

- Competitive Landscape & Strategies: Analyzes the leading producers of Li salts through their production capacity, lithium conversion capability, product portfolios, collaborations and geographical locations among others.

- Market Entry and Business Strategies: Identifies the white spaces for business strategies including local refining, battery-grade lithium salts, recycled lithium salts, specialty applications and more.

Target Audience 2026

- Lithium chemical manufacturers

- Battery material and cathode producers

- EV battery manufacturers

- Energy storage system companies

- Specialty chemical companies

- Glass and ceramics manufacturers

- Lubricant and grease manufacturers

- Pharmaceutical and API manufacturers

- Procurement and raw material sourcing teams

- Corporate strategy and market intelligence teams

- Business development and sales leaders

- Investors, private equity firms and mining funds

- Lithium miners and refining companies

- Recycling and circular battery material companies

- Consulting and advisory teams