Lithium Battery Pretreatment Market Definition and Overview

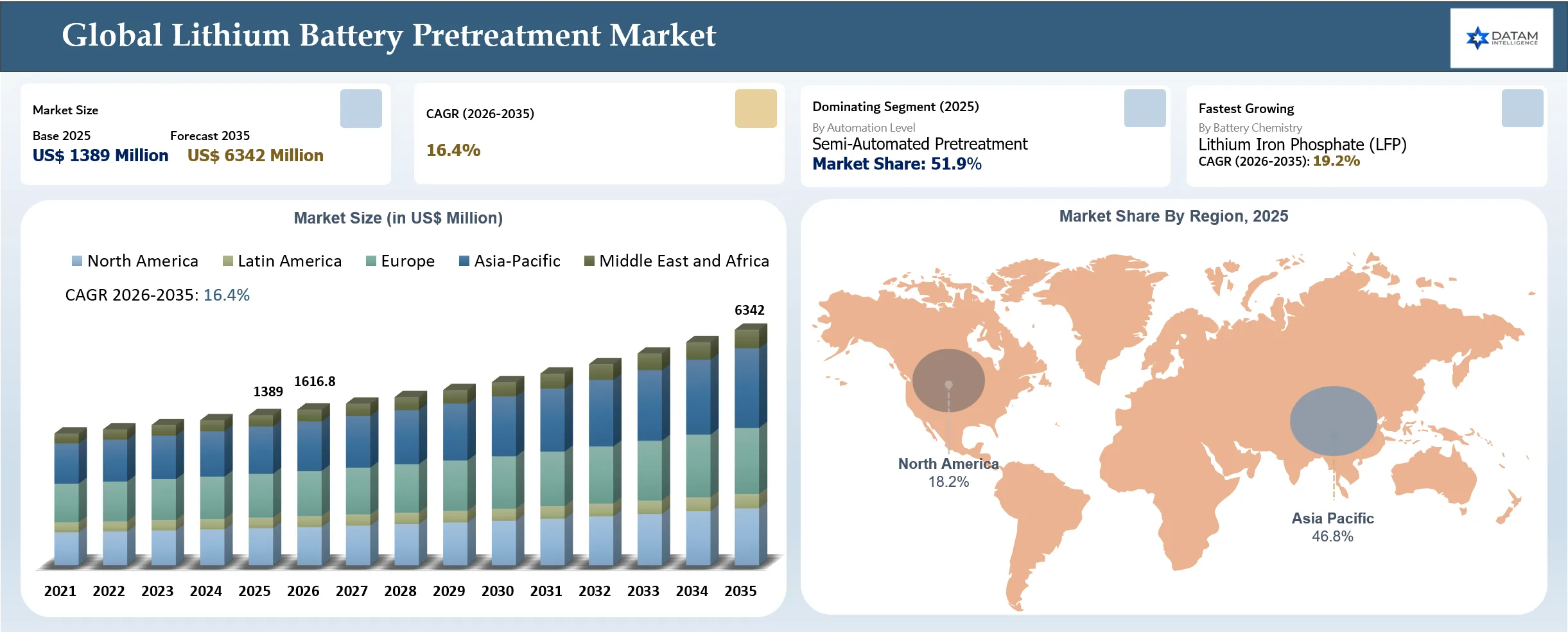

The global lithium battery pretreatment market reached USD 1389 million in 2025 and is expected to reach USD 6342 million by 2035, growing with a CAGR of 16.4% during the forecast period 2026-2035, due to the rapid increase of lithium-ion batteries at end-of-life, where global electric vehicle sales exceeded 20 million units in 2025, accounting for more than 25% of all vehicles sold. Global battery demand will exceed 1 TWh in 2025 according to the IEA, but battery production capacity is still growing.

This creates increased scrap from production processes that need to be pre-treated before recycling can take place. Investments in automated discharge systems, inert-atmosphere shredding, and black mass production systems are on the rise, driven by the EU Battery Regulation and its equivalents in North America and Asia-Pacific, due to the need to support domestic critical mineral value chains. Companies within the industry are building up their pretreatment capacities to increase efficiencies in lithium, nickel, cobalt, graphite, copper, and aluminum recovery as well as closed-loop battery manufacturing. But high capital costs, diversified battery chemistries, handling of hazardous substances, and lack of standardization of the pretreatment process are some of the main barriers. In May 2026, American Resources Corporation, through its subsidiary Electrified Materials Corporation (EMCO), procured its first lithium-ion battery shredding line. This would enable the company to enhance its capabilities for battery pretreatment and recycling. With the purchase of the shredding line, EMCO is now able to safely shred, process, and prepare its end-of-life/off-warranty/off-spec lithium-ion batteries.

Key Takeaways

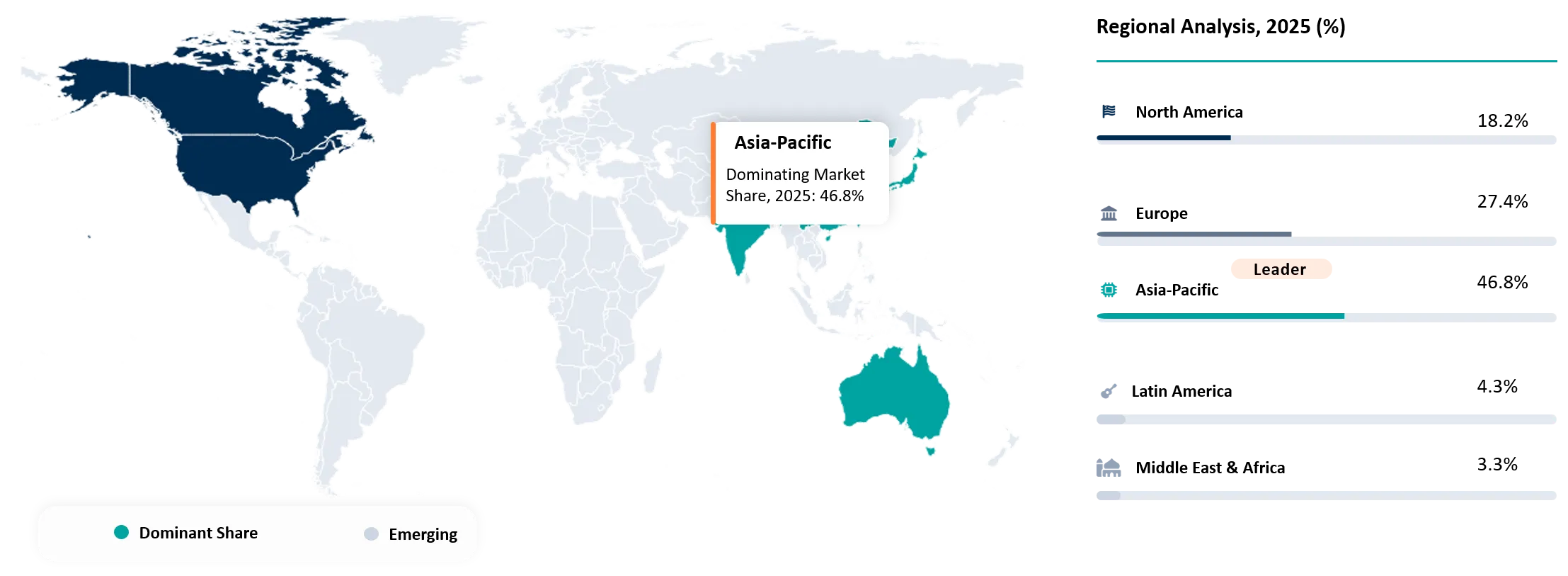

- Asia-Pacific was the dominant region in the lithium battery pretreatment market and had a 46.8% share in the global market in 2025. China is the country that heads this group with 70% of lithium-ion battery manufacturing capacity and over 75% of the cell manufacturing capacity of the world.

- The segment of semi-automated pretreatment processes has been dominating the market through its huge market share of 51.9% in 2025.

- In 2025, the project was piloted under the California Energy Commission for direct battery recycling, and it successfully managed to produce recycled cathode purity levels above 95%. The recycled batteries were able to maintain over 90% of their original capacity during this process.

- In 2025, Lithium Iron Phosphate (LFP) batteries accounted for nearly 50% of the total market demand for electric vehicles batteries. This is a huge change from the market preference that was experienced just five years back where the LFP battery had only a 10% share.

Lithium Battery Pretreatment Market Industry Trends and Strategic Insight

- Scrap from battery manufacturing is the emerging raw material for the pretreatment process, due to the increased production scrap resulting from the growth of the gigafactories, which have more uniform chemistry, less contamination, and fewer safety hazards.

- Pretreatment is becoming more of a value-addition step rather than a waste management process. Organizations have been focusing on improving their processes for black mass shredding, classifying, and separation since these have direct effects on hydrometallurgical processing efficiency downstream.

- Separate processing lines for various battery chemistries are emerging with the shift of recyclers from using mixed feed lines. Dedicated pretreatment processes for NMC, NCA, LFP, and future battery chemistries increase process efficiency, reduce contaminants, and add value to recovered materials.

- Deployment of digital battery identification and tracing techniques has made the pretreatment process more efficient for recyclers, making it easy to recognize the battery’s composition, condition, and design before disassembling it.

- Localized pretreatment facilities are being established close to locations where batteries are manufactured. By doing so, the distance that batteries travel is minimized, thus ensuring that the production of black mass becomes regionally feasible.

Lithium Battery Pretreatment Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 1389 Million | |

| 2035 Projected Market Size | USD 6342 Million | |

| CAGR (2026-2035) | 16.4% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | North America | |

| By Battery Chemistry | Lithium Iron Phosphate (LFP), Lithium Nickel Manganese Cobalt (NMC), Lithium Nickel Cobalt Aluminium (NCA),Lithium Cobalt Oxide (LCO), Lithium Manganese Oxide (LMO), Lithium Titanate Oxide (LTO), Others | |

| By Pretreatment Process | Battery Discharging, Dismantling & Disassembly, Crushing & Shredding, Sorting & Separation, Black Mass Production | |

| By Automation Level | Manual Pretreatment, Semi-Automated Pretreatment, Fully Automated Pretreatment | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Lithium Battery Pretreatment Market Disruption Analysis

Commercialization of Direct Recycling Technologies Reshaping Lithium Battery Pretreatment Processes

The disruption in the Lithium Battery Pretreatment Market is being driven by the industrialization of the technology behind direct recycling that is revolutionizing recycling practices by maintaining cathode active materials as opposed to metal recovery via pyrometallurgy and hydrometallurgy. The shift is changing the nature of pretreatments in terms of discharging, dismantling, shredding, and separation under controlled conditions to ensure that the cathode material is maintained. With increased industrialization of direct recycling, pretreatment is changing from a feedstock preparation process to a precise process whose success determines the efficiency of cathode regeneration and profitability of closed-loop battery production.

The disruption is validated further through advancements in direct recycling efficiency between 2025 and 2026. Specifically, a pilot project of the California Energy Commission (CEC) on direct recycling done in 2025 resulted in over 95% cathode purity, more than 90% active material yield, and 99% capacity in recycled cathodes compared to the virgin cathodes.

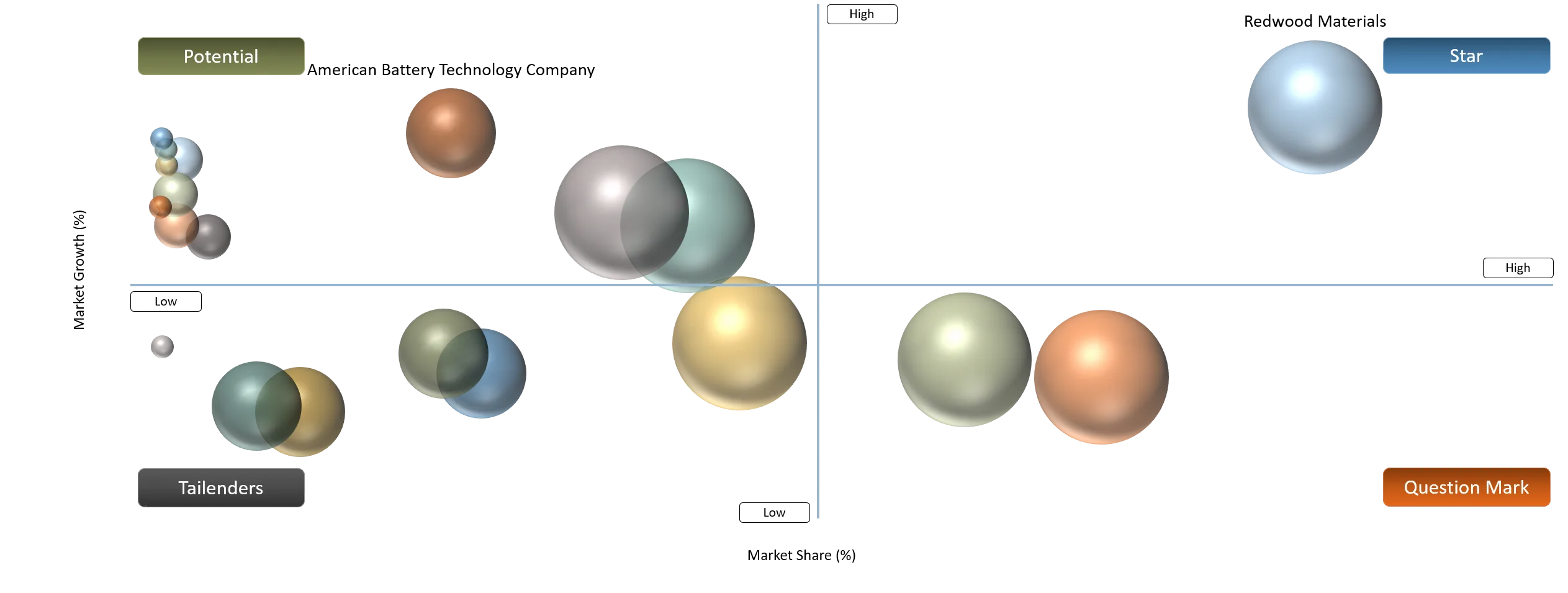

Lithium Battery Pretreatment Market BCG Matrix: Company Evaluation

Stars include Redwood Materials, Li-Cycle Holdings Corp., and Brunp Recycling because of their ability to have a lithium-ion battery recycling ecosystem that is equipped with effective pre-processing facilities, black mass generation facilities, and strategic relationships with OEMs and battery producers. Such companies are increasing their pre-processing capabilities while developing their lithium battery material supply chain, thus holding an advantageous position in the lithium battery pre-processing market. Question Marks companies included are Cirba Solutions, Ecobat, SungEel HiTech, and GEM Co., Ltd., since they are quickly increasing lithium battery pre-processing and recycling activities through new facilities and technologies.

The potential category consists of American Battery Technology Company, ACE Green Recycling, Fortum Battery Recycling, SK Tes, and Cylib GmbH. These businesses have made huge investments in high-tech pretreatment systems, automation of disassembly processes, and sustainable battery recycling technology platform development owing to government grants and partnerships. Tailenders comprise companies such as Primobius GmbH, STENA Recycling, and Duesenfeld GmbH due to their specialization in pretreatment of lithium batteries in their regions or on projects. The companies have pretreatment technology and engage in recycling projects.

Lithium Battery Pretreatment Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Rapid growth in End-of-Life lithium-ion batteries is significantly increasing the volume of batteries requiring a safe pretreatment process before recycling. | 40% | Very High in EV batteries, followed by Battery Energy Storage Systems (BESS) and consumer electronics | Battery discharge, dismantling, shredding, black mass production | Expands pretreatment capacity requirements, increases recycling throughput, and strengthens secondary critical mineral supply chains. |

Governments and private investors are establishing large-scale battery recycling facilities to ensure adequate supply of strategic minerals. | 30% | High in North America, Europe, and China | Commercial battery recycling plants, integrated pretreatment facilities | Accelerates investments in automated pretreatment systems and supports localization of lithium, nickel, cobalt, and graphite recovery. |

Rising adoption of automation of the battery discharge process and robot- assisted battery disassembly for higher efficiency and greater safety. | 22% | High in large-scale industrial recycling facilities | Automated battery discharge, robotic dismantling, AI-based sorting | Improves operational safety, processing efficiency, throughput, and consistency while reducing labor dependency and hazardous handling risks. |

The rapid construction of battery gigafactories has resulted in large amounts of production scrap, faulty cells, and non-conforming modules. | 20% | Very High in battery manufacturing hubs across China, South Korea, Europe, and North America | Manufacturing scrap recycling, defective cell processing, black mass preparation | Creates a stable feedstock for pretreatment facilities, improves resource recovery from production waste, and supports closed-loop battery manufacturing. |

Rapid growth in End-of-Life lithium-ion batteries is significantly increasing the volume of batteries requiring a safe pretreatment process before recycling

The rapid increase in end-of-life (EoL) lithium-ion batteries serves as a key factor that propels demand for lithium battery pretreatment technologies. A massive number of batteries, which need to be discharged, dismantled, shredded and separated, arise from the increasing use of electric vehicles, battery energy storage systems and portable devices. According to the International Energy Agency (IEA), the total number of electric vehicles reached 20 million vehicles globally in 2025, substantially increasing the future pipeline of batteries entering the recycling stream. At the same time, according to Benchmark Mineral Intelligence, the total capacity of lithium-ion battery recycling in 2025 was more than 1.5 million tonnes per year. For instance, in April 2026, Mobec Innovation highlighted that there will be a huge increase in end-of-life lithium-ion batteries in India due to the fast adoption of electric vehicles.

With that country handling nearly 50,000 tonnes of waste lithium-ion batteries in 2025, it is forecasted that in 2026 there will be about 60,000 tonnes of lithium-ion battery waste with total recycling capacity of over 100,000 tonnes per annum. The company also noted that only 25 to 30% of used batteries are currently collected through formal recycling systems.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

The rising variety of chemistry types of Lithium-Ion batteries and advanced battery designs are increasing complexity for pretreatment systems. | 26% | Battery pretreatment technology, equipment design, and process optimization | Multi-chemistry battery processing, battery dismantling, shredding, and material separation | Increases equipment customization, raises operating costs, and slows standardization and large-scale automation of pretreatment facilities. |

There is an imbalance due to inefficiencies in collection, fragmentation of the reverse logistics process, and the long life span of batteries. | 22% | Feedstock availability and battery collection network | End-of-life battery collection, transportation, and pretreatment plant utilization | Reduces feedstock consistency, lowers plant utilization rates, and delays return on investment for pretreatment infrastructure. |

Commercial direct cathode recycling is forcing changes in pretreatment, as it requires more refined input materials and less contaminated input material. | 19% | Pretreatment process quality and contamination control | Precision dismantling, inert-atmosphere shredding, and high-purity black mass production | Requires advanced pretreatment technologies and higher process precision, increasing capital expenditure while accelerating technology upgrades. |

Pre-treatment facilities need to adhere to tight environmental regulations concerning emissions, sewage disposal, waste handling, and occupational safety. | 16% | Regulatory compliance, environmental management, and workplace safety | Hazardous waste handling, air emission control, wastewater treatment, and worker protection | Increases compliance and operating costs, extends facility permitting timelines, and necessitates continuous investment in environmental and safety systems. |

The rising variety of chemistry types of Lithium-Ion batteries and advanced battery designs are increasing complexity for pretreatment systems

One of the major factors that have hampered the expansion of the Lithium Battery Pretreatment Market is the growing variety of the types of lithium-ion batteries and changing design structure of battery packs. The modern battery recycling plants need to handle a variety of battery chemistries such as Lithium Iron Phosphate (LFP), Nickel Manganese Cobalt (NMC), Nickel Cobalt Aluminum (NCA), Lithium Cobalt Oxide (LCO), and Lithium Manganese Oxide (LMO). The challenge is getting compounded as the battery technology continues to evolve. As per estimates by the International Energy Agency (IEA), Lithium Iron Phosphate (LFP) batteries made up almost 50% of global demand for electric vehicle batteries in 2025, which was only around 10% five years earlier.

For instance, in November 2025, as per Prism – Sustainability Directory, the rapid development of lithium-ion battery technology is making it increasingly difficult to recycle, due to different types of battery chemistries (like LFP, NMC, NCA) and battery designs, calling for a more sophisticated process of recycling.

Lithium Battery Pretreatment Market Segment Analysis

The global lithium battery pretreatment market is segmented based on battery chemistry, pretreatment process, automation level, and region.

Semi-Automated Pretreatment Dominates the Lithium Battery Pretreatment Market Due to Its Balance of Processing Efficiency and Capital Cost

The semi-automated pretreatment process segment dominates the Lithium Battery Pretreatment Market, with a market share of 51.9% in 2025, due to the perfect balance of efficiency, safety, flexibility, and cost. The vast majority of commercial battery recycling plants use automated processes for battery discharging, crushing, shredding, and separating while still relying on manual labor for the purposes of battery inspection and module disassembly as well as the processing of batteries that vary in chemistry and packaging. This operational approach allows battery recyclers to work with different types of lithium-ion batteries without spending huge sums on the implementation of fully automated production lines. Further, the dominance of this market segment is augmented by the fast development of battery recycling facilities from 2025 to 2026.

The International Energy Agency (IEA) reports that the total annual battery manufacturing capacity worldwide amounted to more than 3 TWh in 2024, which resulted in the growth of production scrap and necessitated the pretreatment stage to be implemented before recovery of materials. Moreover, the number of lithium-ion battery gigafactories constructed, planned, and operated in 2025 reached 400 gigafactories according to Benchmark Mineral Intelligence.

Lithium Battery Pretreatment Market Geographical Penetration

Rapid Expansion of Battery Manufacturing and Recycling Infrastructure Strengthening Asia-Pacific's Market Leadership

The Asia Pacific region is dominating the Lithium Battery Pretreatment Market, accounting for 46.8% of the global market share in 2025, due to the presence of lithium-ion battery manufacturers, electric vehicle manufacturers, and battery recycling of batteries. This region has the highest presence of battery cell manufacturers, battery recyclers, and processors of critical minerals, especially China, Japan, and South Korea. Due to the constant growth of battery gigafactories, manufacturing waste, and retired electric vehicle batteries, there has been an investment in the development of advanced battery discharge, automated disassembly, inert atmosphere shredding, and black mass production plants. The government’s support for the circular economy and critical minerals has further enhanced the market share of the region in the global lithium battery pretreatment market.

For instance, in June 2026, N.A.N. GreenMet and Silox formed a joint venture with equal partnership to build India's largest platform for lithium-ion batteries' recycling and extraction of critical minerals in the state of Andhra Pradesh. This development will happen in stages, with a capacity target of 40,000 tons per year (TPA) for shredding of waste batteries and 20,000 TPA for hydrometallurgical processing to enhance battery pre-treatment and critical metals recovery amid rising demand for electric vehicles and energy storage systems in the Asia-Pacific market.

China Lithium Battery Pretreatment Market Trends

China’s dominance in the Asia-Pacific Lithium Battery Pretreatment market is the presence of a complete lithium-ion battery manufacturing industry, along with battery recycling facilities and government initiatives for critical mineral recovery. China has developed an integrated battery supply chain involving the presence of battery cell makers, battery recyclers, black mass manufacturers, and metal refineries, which facilitate the effective collection, pretreatment, and subsequent processing of materials. The presence of prominent recycling firms like Brunp Recycling, GEM Co., Ltd., and others, together with the constant upgrading of automated battery discharging, shredding, and black mass making processes, has solidified the supremacy of China in lithium battery pretreatment. China continues to expand its market share through capacity expansion and investments in 2025–2026.

The International Energy Agency estimates that China accounted for 70% of the global capacity for lithium-ion battery production in 2025, and Benchmark Mineral Intelligence reports that it was more than 75% of the capacity of battery cell production in the world. For instance, in February 2026, China intensified efforts to develop an infrastructure for its lithium-ion battery recycling industry by formulating policies aimed at developing a “standardized, safe, and efficient” battery recycling process in preparation for an anticipated spike in the quantity of EV batteries that have reached the end of their lifespan. The annual volume of end-of-life EV batteries is expected to hit about 1 million tonnes by 2030.

India Lithium Battery Pretreatment Market Outlook

India is emerging as one of the fast-growth countries in the Asia-Pacific Lithium Battery Pretreatment Market, which can be attributed to the growth in the electric vehicle market in India, growing capacity for battery manufacturing in India, and government support for battery recycling. The implementation of the Battery Waste Management Rules 2022 and the Production Linked Incentive (PLI) Scheme for ACC manufacturing have led to increased investment in battery collection, pretreatment, and recycling systems. In addition, India will experience high capacity growth in the battery value chain from 2025 to 2026. As per data from India Brand Equity Foundation (IBEF), India's total Advanced Chemistry Cells (ACC) manufacturing capacity through the PLI Scheme is 50 GWh, which is helping to build a local battery supply chain and increase recycling feedstock in the future. Moreover, as per the estimates of NITI Aayog, India's lithium-ion battery demand will cross 260 GWh per year by 2030, which will drive investments in battery recycling and pretreatment facilities from 2025 to 2026.

For instance, in April 2026, Rocklink India commissioned a new lithium-ion battery and rare earth recycling plant established in Uttar Pradesh. This would help increase India’s battery pre-processing and recycling facilities. It has a capacity of 10,000 tonnes per annum (TPA) for lithium-ion battery recycling; this process involves battery disassembling and physical segregation of black mass.

Lithium Battery Pretreatment Market Competitive Landscape

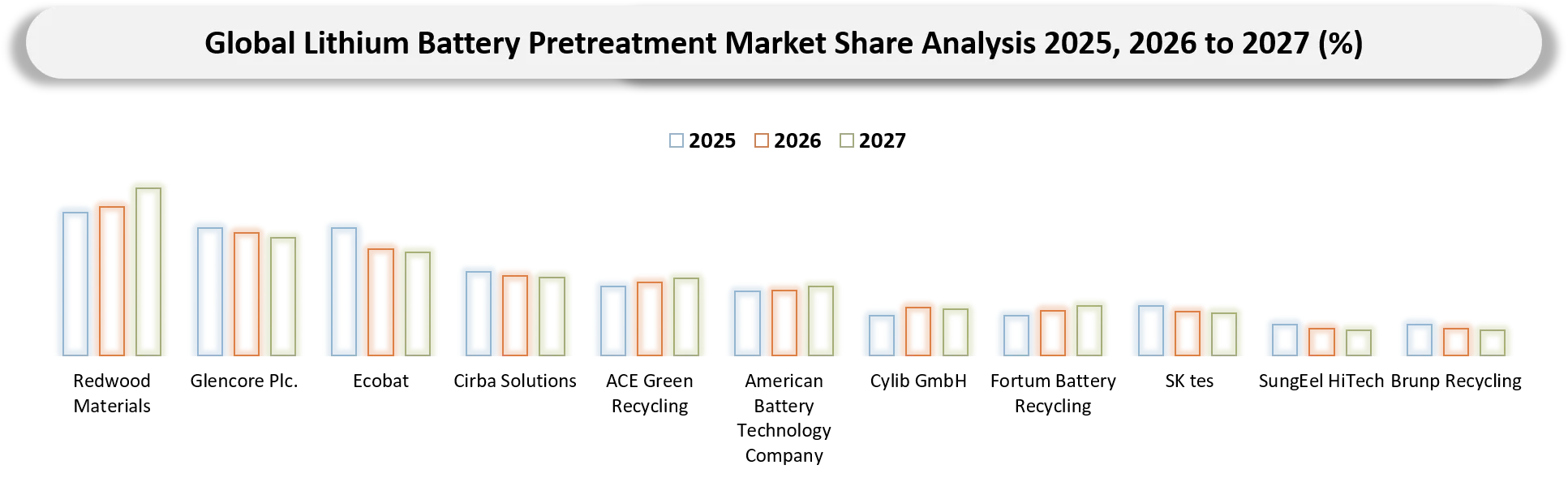

- The market features three main types of participants, which include vertically integrated battery recyclers, providers of advanced lithium battery pretreatment technology, and producers of industrial recycling equipment. The leading companies in the market include Redwood Materials, Brunp Recycling, GEM Co., Ltd., SungEel HiTech, Cirba Solutions, Ecobat and Fortum Battery Recycling. These companies operate in the field by means of vertical integration of battery recycling involving collection of batteries, pretreatment, black mass manufacturing and critical mineral recovery. Such players as ACE Green Recycling, American Battery Technology Company, Cylib GmbH, Duesenfeld GmbH and Primobius GmbH enhance their position by developing advanced low-emission recycling technology and pretreatment systems. In addition, companies such as SK tes, STENA Recycling and Glencore Plc. capitalize on their global recycling network, industrial waste management and metal refining skills in order to increase the lithium battery pretreatment capacity.

- Key players include Redwood Materials, Glencore Plc., Ecobat, Cirba Solutions, ACE Green Recycling, American Battery Technology Company, Cylib GmbH, Fortum Battery Recycling, SK tes, SungEel HiTech, Brunp Recycling, GEM Co., Ltd., Primobius GmbH, STENA Recycling, and Duesenfeld.

Key Developments

- June 2025: The BASF corporation, a Germany-based chemical company, started commercial operations at its Black Mass plant located in Schwarzheide, Germany. This plant will further enhance the ability of the company to process and recycle its lithium-ion battery pretreatment. It is the largest commercial black mass plant in Europe with a processing capacity of 15,000 tonnes of lithium-ion batteries annually.

- January 2025: Marubeni Corporation, a Japan-based trading and investment firm, has made a monetary investment amounting to USD 5 million in Altilium, a UK-based company that deals with lithium-ion battery recycling.

- June 2025: Ace Green Recycling, a Singapore-based battery recycling technology firm, signed a strategic partnership agreement with Enecell, which is an Australian-based battery collection and recycling firm, to create a sustainable lithium-ion battery recycling ecosystem in Australia.

- January 2025: Ace Green Recycling, a Singapore battery recycling technology company, launched an initiative to expand their battery recycling facilities for lithium iron phosphate (LFP). They are planning to build the largest LFP battery recycling facility in Mundra, Gujarat.

- August 2025: Glencore, a Swiss-based minerals trading firm, successfully acquired Li-Cycle's battery recycling business, which includes Spoke processing plants and the Rochester Hub project.

- March 2026: Lyten, a US-based battery technology manufacturer, acquired the Revolt battery recycling factory in Skellefteå, Sweden from Northvolt to increase its capacity for lithium-ion battery recycling and pretreatment.

- March 2025: Navprakriti International, an India-based battery recycling company, partnered with Nash Energy, an India-based energy storage solutions provider, to develop a circular lithium-ion battery ecosystem by strengthening the collection, pretreatment, and recycling of end-of-life batteries across eastern India.

Key Procurement Priorities and Buyer Evaluation Criteria

- Procurement choices are becoming more dependent on the fast-paced developments of EV battery recycling, development of direct recycling processes, implementation of battery passports, and development of local critical mineral supply chains. Procurement managers are looking for pretreatment processes that can be easily scaled up, can support different battery chemistries, have automation capabilities, and can integrate with downstream hydrometallurgy and direct recycling processes.

- Buyer assessments include battery discharge efficiency, disassembly accuracy, shredding and sorting efficiency, black mass purity, processing capacity, safety of operations, energy efficiency, and the capacity to handle batteries from electric vehicles (EVs), scrap material from battery production processes, and stationary energy storage batteries. The capacity to reduce lithium losses, limit contamination levels, and maintain feedstock quality consistency is increasingly important for purchases.

- Companies that invest in the Lithium Battery Pretreatment Market are increasingly opting for suppliers who can offer safe, high-capacity and automated systems for the pretreatment of different kinds of lithium-ion batteries. The procurement emphasis lies in obtaining systems that will ensure maximum quality of black mass, increased efficiency in material recovery, minimal contamination, and compliance with regulatory standards.

Why Choose DataM?

- Technological Innovations: Discusses the advances in lithium battery pre-treatment processes through the use of automated battery discharge systems, mechanical disassembly by robots, inert atmosphere shredding process, AI-powered battery recognition, and manufacture of high-purity black mass.

- Product Performance & Market Positioning: Examines the way in which some of the major firms differentiate themselves through their pretreatment processes according to the processing throughput rate, purity of black mass, contamination levels, compatibility with the battery chemistry, automation, and energy efficiency.

- Real-World Evidence: Points out the commercial application of lithium battery pre-treatment techniques in electric vehicle battery recycling facilities, battery manufacturing scrap treatment facilities, and stationary energy storage recycling projects to show the effectiveness of such technologies.

- Market Updates & Industry Changes: Highlights key developments such as expansion of recycling capacities, commissioning of automated pretreatment facilities, launching of direct recycling technology, battery passports, and government spending on battery recycling infrastructure in Asia-Pacific, North America, and Europe.

- Competitive Strategies: Explores how top firms can secure competitive advantage by developing cutting-edge pretreatment technology, increasing capacity, forming collaborations with battery makers and auto OEMs, investing in automation, and integrating black mass processing.

- Pricing & Market Access: Describes pricing differences due to plant processing capacity, degree of automation, sophistication of battery chemistry, requirement for inert atmosphere processing, and quality of black mass. Describes market entry via integrated battery recycling firms, pretreatment technology companies, engineering firms, and equipment suppliers.

- Market Entry & Expansion: Growth opportunities resulting from end-of-life EV batteries, scrap batteries, localized sourcing of critical minerals, and battery recycling regulations will be highlighted, alongside expansion strategies that will include regional pretreatment operations, chemical-specific recycling technologies, automation improvements, and collaborations in the battery recycling chain.

Target Audience

- Lithium-Ion Battery Manufacturers

- Electric Vehicle (EV) Manufacturers (OEMs)

- Battery Recycling Companies

- Lithium Battery Pretreatment Technology Providers

- Black Mass Producers

- Critical Mineral Recovery & Refining Companies

- Battery Collection & Reverse Logistics Service Providers