Liquid Carbon Dioxide Market Overview

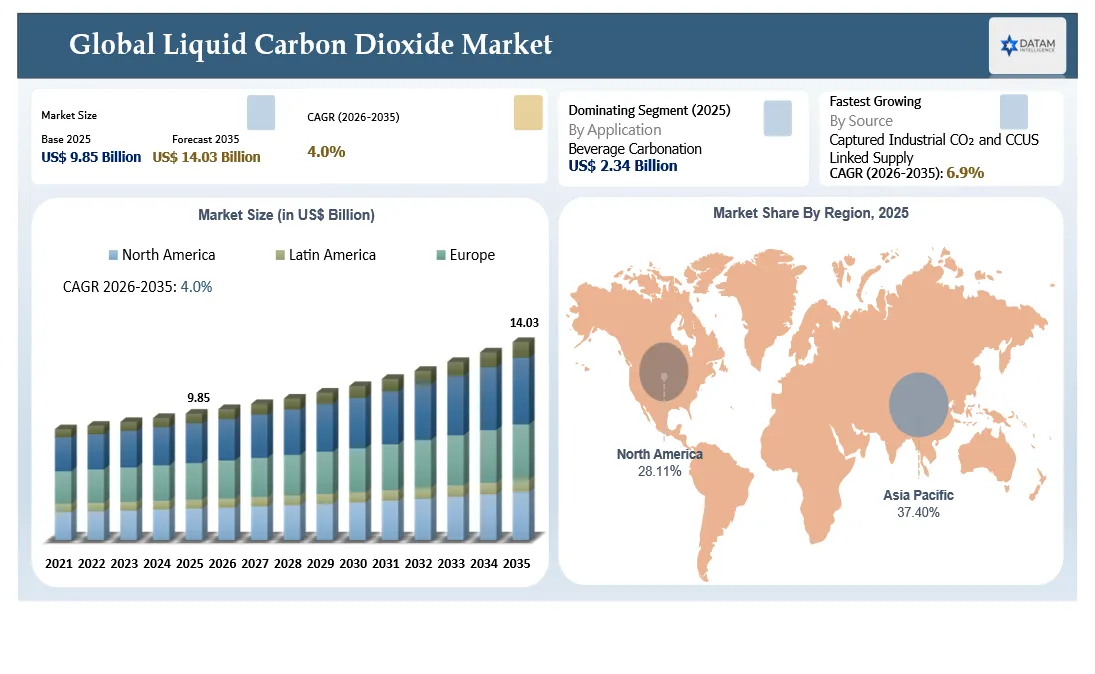

The global liquid carbon dioxide market is estimated at US$ 9.85 billion in 2026 and is projected to reach US$ 14.03 billion by 2035, growing at a CAGR of 4.0% during the forecast period. The market covers merchant, captive and distribution led liquid CO₂ supplied for carbonation, food preservation, dry ice, healthcare, oil and gas, chemical processing, welding, agriculture, water treatment and emerging carbon management applications.

Liquid CO₂ is no longer treated only as a low cost industrial gas. Buyers increasingly view it as a critical input tied to production continuity. Beverage bottling lines, breweries, meat processors, cold chain distributors, hospitals and oilfield operators can face immediate operational disruption when CO₂ availability tightens. In 2026, North American liquid CO₂ prices were affected by higher natural gas costs, ethanol plant turnarounds, ammonia turnarounds and diversion of CO₂ streams toward sequestration, showing how the market is exposed to upstream industrial activity and carbon management decisions.

The market is also shifting because CO₂ logistics is becoming a strategic infrastructure category. Northern Lights expanded its fleet with four additional liquid CO₂ ships in 2026 to support customer agreements and an expansion plan that raises transport and storage capacity to more than 5 million tonnes of CO₂ per year. This development shows that liquid CO₂ handling is expanding from beverage, food and industrial gas supply toward cross border carbon capture, transport and storage systems.

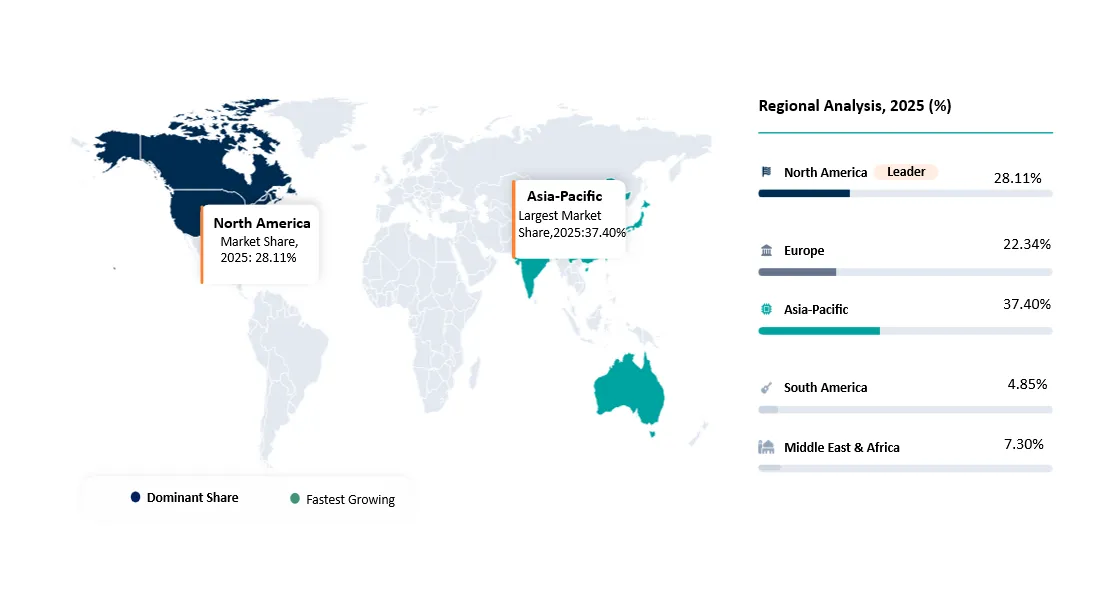

North America remains the largest regional market due to food and beverage demand, ethanol based CO₂ sources, oil and gas demand and established industrial gas distribution. Asia-Pacific is the fastest growing region due to food processing expansion, beverage consumption, industrial manufacturing, healthcare infrastructure and emerging carbon capture activity. Food and beverage remains the largest end use, while captured industrial CO₂ and CCUS linked supply is expected to be the fastest growing supply pathway.

Liquid Carbon Dioxide Market Scope

| Metric | Details |

| 2026 Market Size | US$ 9.85 Billion |

| 2035 Projected Market Size | US$ 14.03 Billion |

| CAGR 2026-2035 | 4.0% |

| Largest Region | North America |

| Fastest Growing Region | Asia-Pacific |

| Largest Segment | Food and Beverage Applications |

| Fastest Growing Segment | Captured Industrial CO₂ and CCUS Linked Supply |

| Key Sources | Ethanol fermentation, ammonia plants, hydrogen production, natural gas processing, industrial capture and natural sources |

| Key Applications | Carbonation, freezing and chilling, dry ice, EOR, medical use, welding, chemical processing, agriculture and water treatment |

| Report Insights Covered | Competitive landscape, supply risk, pricing intelligence, market size, buyer decision criteria and investment opportunities |

Liquid Carbon Dioxide Market Key Takeaways

- The liquid carbon dioxide market is estimated at US$ 9.85 billion in 2026 and is projected to reach US$ 14.03 billion by 2035, growing at a CAGR of 4.0% during 2026 to 2035.

- North America is the largest region due to mature beverage production, food processing, dry ice supply, oilfield demand and a broad industrial gas distribution network.

- Asia-Pacific is the fastest growing region, supported by expanding food processing, beverage consumption, electronics, healthcare, industrial manufacturing and emerging CO₂ infrastructure.

- Food and beverage is the largest application segment, supported by carbonation, chilling, freezing, modified atmosphere packaging and beverage dispense systems.

- Captured industrial CO₂ and CCUS linked supply is the fastest growing source segment as industrial emitters add purification, liquefaction and transport assets to convert captured CO₂ into merchant supply or sequestration flows.

- The market is increasingly influenced by upstream plant operations. Ethanol, ammonia, hydrogen and natural gas processing plants are key byproduct sources, so maintenance shutdowns and feedstock price movements can create regional shortages.

- In 2026, North American CO₂ pricing reflected higher natural gas costs, ethanol and ammonia plant turnarounds and sequestration diversion, showing that buyers need contract terms that cover force majeure, backup sourcing and delivered cost escalation.

- Northern Lights fleet expansion in 2026 indicates that liquid CO₂ handling is becoming important for carbon capture logistics, not only traditional industrial gas supply.

- Buyers are shifting from price based procurement toward supply assurance, purity documentation, tank telemetry, emergency backup, regional redundancy and multi source contracting.

- High reliability customers such as breweries, hospitals, cold chain operators and food processors increasingly require vendor audits, quality certifications and documented CO₂ source traceability.

Liquid Carbon Dioxide Industry Trends and Strategic Insights

- Industrial gas suppliers are expanding from bulk CO₂ delivery toward supply assurance services, including tank telemetry, reorder automation, backup sourcing and customer specific continuity planning.

- Food and beverage buyers are prioritizing beverage grade purity, delivery reliability and contracts that protect against summer demand peaks and upstream source shutdowns.

- Dry ice demand is linked to frozen food, pharmaceutical distribution, biologics logistics and emergency cold chain use, making CO₂ supply a strategic input for healthcare and e-commerce logistics.

- Carbon capture projects are creating a new liquid CO₂ logistics category, where captured CO₂ must be dried, compressed, liquefied, transported and either stored or used.

- Onsite recovery and purification systems are gaining attention among large users that want to reduce dependency on merchant supply during regional shortages.

- Buyers are increasingly evaluating Scope 3 and circular carbon positioning, especially when CO₂ is recovered from biogenic ethanol or industrial byproduct streams.

Why does this report matter in 2026?

In 2026, liquid carbon dioxide has become a critical supply chain input for industries that cannot operate smoothly during shortages. Food processors need CO₂ for freezing, chilling and modified atmosphere packaging. Beverage companies need beverage grade CO₂ for carbonation and dispense systems. Dry ice producers need reliable liquid CO₂ for pharmaceutical, frozen food and logistics customers. Oil and gas companies need CO₂ for EOR and pressure management in specific fields. Hospitals and laboratories require controlled supply for medical and research uses.

The report matters because liquid CO₂ supply is exposed to allied industries. A shutdown at an ethanol plant, ammonia plant or hydrogen facility can immediately reduce merchant CO₂ availability. Higher natural gas prices can raise liquefaction cost. Sequestration projects can divert CO₂ streams away from merchant buyers. Port and shipping infrastructure can reshape future CO₂ flows as liquid CO₂ carriers scale for CCS. The report gives buyers, suppliers and investors a practical view of where demand is growing, where supply is fragile and how contract structures need to change.

Liquid Carbon Dioxide Market White Space and Investment Opportunities

- Regional backup liquefaction hubs near beverage, meat processing and cold chain clusters where shortages can stop production quickly.

- Biogenic CO₂ recovery from ethanol and fermentation plants, especially where customers want lower fossil carbon exposure and traceable CO₂ sourcing.

- Small and mid scale onsite purification systems for breweries, food plants, greenhouse operators and industrial users that want reduced dependence on delivered CO₂.

- Liquid CO₂ tanker fleets, ISO containers and port receiving terminals that support CCUS logistics and cross border CO₂ transport.

- Digital tank monitoring and predictive delivery platforms that reduce runout risk and improve route efficiency for distributors.

- High purity CO₂ grades for medical, pharmaceutical, electronics and specialty applications where quality documentation commands premium pricing.

- Emergency supply networks and multi source contracts for customers exposed to seasonal peaks, plant turnarounds and geopolitical logistics disruption.

Liquid Carbon Dioxide Future Market Transformation

The liquid carbon dioxide market is expected to shift from traditional industrial gas supply toward a dual market structure. One side will remain focused on food, beverage, healthcare, welding, dry ice and industrial applications. The other side will be linked to carbon capture, utilization and storage infrastructure, where liquid CO₂ becomes a transportable carbon stream for storage hubs, ship based logistics and utilization facilities.

Future market leadership will depend on source reliability, not just distribution reach. Suppliers will need access to ethanol, ammonia, hydrogen, refinery, natural gas and captured industrial CO₂ streams. They will also need purification, dehydration, liquefaction and storage capacity close to demand centers. As customers demand more resilient supply, liquid CO₂ contracts will increasingly include backup source commitments, source disclosure, telemetry based inventory management and emergency delivery clauses.

Liquid Carbon Dioxide Market Buyer Decision-Making Criteria

Buyers evaluate liquid CO₂ suppliers based on delivered reliability, purity grade, source diversification, local storage availability, tanker fleet depth, emergency response capability, delivery frequency and contract flexibility. Food and beverage customers prioritize beverage grade certification, taste neutrality, contaminant control, pressure stability and delivery consistency. Healthcare and pharmaceutical buyers require stronger documentation, traceability and compliance support. Oil and gas buyers focus on volume availability, injection compatibility, logistics cost and field proximity.

Procurement teams are moving away from lowest unit price. The new decision model weighs supplier redundancy, source risk, backup contracts, escalation clauses, storage telemetry, tank ownership, safety support and continuity of operations. Buyers increasingly ask whether the supplier depends on one ammonia or ethanol source, whether an alternate source is available within truckable distance and whether the supplier can maintain deliveries during plant turnarounds or regional demand spikes.

Liquid Carbon Dioxide Market Economic and Investment Analysis

Liquid CO₂ economics are shaped by source plant economics, capture cost, purification, refrigeration, liquefaction, storage, truck mileage, tank leasing and grade specific testing. Merchant CO₂ often depends on byproduct availability from ammonia, ethanol, hydrogen or natural gas processing plants. When these plants reduce output, conduct maintenance or redirect CO₂ for sequestration, merchant supply tightens and spot prices can rise. In 2026, North American pricing pressure was linked to natural gas cost, ethanol plant turnarounds, ammonia turnarounds and sequestration diversion.

Investment is flowing into three areas: source diversification, logistics infrastructure and carbon management. Source diversification includes biogenic CO₂ from fermentation, CO₂ recovery from industrial off gas and modular purification units. Logistics infrastructure includes road tankers, bulk storage, ISO containers, port terminals and dedicated liquid CO₂ vessels. Carbon management includes CCUS hubs, carbon utilization plants and cross border liquid CO₂ transport. These investment themes make the market more infrastructure intensive and more strategic for industrial buyers.

Liquid Carbon Dioxide Investment Trends in the Market

- Rising investment in CO₂ recovery from fermentation and industrial off gas to improve merchant supply security.

- Expansion of LCO₂ carrier fleets for cross border transport of captured CO₂ to permanent storage hubs.

- Greater focus on regional storage depots and bulk tanks near beverage, cold chain and food processing clusters.

- Investment in digital tank telemetry and predictive logistics to reduce customer stockout risk.

- Capacity additions in the U.S. Gulf Coast and Europe to support both industrial gas customers and carbon management applications.

- Emerging interest in onsite CO₂ recovery systems for breweries, fermentation plants, greenhouses and industrial users.

Strategic Indicators for Liquid Carbon Dioxide Market

| Strategic Indicator | Market Signal | Buyer Impact | Strategic Response |

| High Regulation Impact | Food grade, medical grade and transport safety requirements influence supplier qualification. | Customers need certified purity, safety documentation and compliant storage systems. | Build documentation led sales, quality audits and grade specific supply contracts. |

| High Investment Activity | CCUS and LCO₂ carrier projects are expanding the use of liquid CO₂ logistics. | New infrastructure can create alternative supply routes, but can also divert CO₂ from merchant markets. | Track carbon capture hubs and evaluate partnerships with storage or utilization projects. |

| Supply Chain Disruption | Ethanol, ammonia and hydrogen plant outages can reduce regional merchant CO₂ availability. | Buyers face runout risk, price spikes and production interruptions. | Adopt dual sourcing, backup contracts, telemetry and emergency supply agreements. |

| Pricing Volatility | Energy cost, refrigeration cost, seasonal demand and truck mileage affect delivered price. | Delivered CO₂ cost can vary sharply by region and distance from source plants. | Benchmark delivered cost by location and negotiate escalation clauses. |

| Procurement Pressure | Large users need guaranteed volumes and documentation across grades. | Procurement teams need to compare price, risk and operational continuity together. | Use total supply assurance models rather than simple price per tonne. |

| New Technology Adoption | Purification, liquefaction, telemetry and LCO₂ shipping are improving market reliability. | Customers can access better visibility and more resilient supply networks. | Prioritize suppliers investing in modern logistics and monitoring systems. |

| Regional Expansion Opportunity | Asia-Pacific and Middle East demand is rising with food processing, beverage and industrial growth. | New local supply chains are needed to avoid import or long distance dependence. | Invest near demand clusters and high growth industrial corridors. |

| Government Policy Support | CO₂ security and carbon capture policies are influencing supply decisions. | Policy can support new CO₂ recovery capacity but also redirect volumes. | Monitor subsidies, carbon storage incentives and food security interventions. |

Pricing Intelligence

Liquid CO₂ pricing varies by purity grade, source, contract length, storage model, delivery distance, region, tank ownership and emergency supply requirement. Bulk food grade contracts normally price differently from spot emergency deliveries, medical grade supply, dry ice feedstock and oilfield injection volumes. Delivered cost is heavily influenced by transportation because liquid CO₂ must be moved in pressure controlled cryogenic tankers or dedicated containers. Customers located far from CO₂ source plants face higher delivered cost and greater shortage exposure.

| Pricing Factor | Impact on Price | Buyer Question |

| Source plant type | Ethanol, ammonia, hydrogen and natural gas processing sources have different reliability and cost profiles. | How many qualified sources support the supplier in this region? |

| Purity grade | Food, medical and specialty grades require additional quality testing and documentation. | Is the grade certified for the exact application? |

| Delivery distance | Longer tanker mileage increases freight cost and shortage risk. | What is the distance from the liquefaction source to the customer site? |

| Seasonality | Summer beverage demand and seasonal food processing peaks can tighten availability. | Does the contract reserve volume for peak demand months? |

| Force majeure risk | Plant outages and upstream turnarounds can trigger supply interruption. | Does the supplier provide backup supply or only best effort delivery? |

| Tank model | Supplier owned tanks, customer owned tanks and telemetry service create different cost structures. | Who owns the bulk tank and who manages inventory? |

Trade Analysis - Export-Import Scenario

| HS Code / Flow | Reporter | 2026 Relevance | Interpretation |

| 2811 / Carbon dioxide | United States | High | Strong domestic demand and regional supply movements linked to food, beverage, dry ice, industrial and oilfield uses. |

| 2811 / Carbon dioxide | Germany | High | Important European industrial gas and chemical market with exposure to food, beverage, manufacturing and CO₂ security concerns. |

| 2811 / Carbon dioxide | Japan | Medium-High | Industrial and food grade CO₂ demand supported by manufacturing, healthcare, electronics and beverage applications. |

| 2811 / Carbon dioxide | UAE and Saudi Arabia | Medium-High | Industrial gas demand linked to oil and gas, food and beverage, chemicals and emerging carbon management activity. |

| 2811 / Carbon dioxide | India | High growth | Demand supported by beverage production, food processing, welding, healthcare and industrial expansion. |

AI Impact Analysis of Liquid Carbon Dioxide Market

AI is increasingly relevant in liquid CO₂ logistics because stockout risk depends on tank levels, route timing, customer consumption, plant reliability, weather, traffic and seasonal demand. AI enabled tank telemetry can forecast customer depletion, optimize tanker routes and prioritize deliveries during constrained supply periods. For distributors, this reduces empty miles, emergency dispatches and missed deliveries. For customers, it improves supply continuity and reduces the risk of line shutdowns.

AI can also improve source plant reliability through predictive maintenance on compressors, refrigeration units, purification skids and liquefaction assets. In markets where CO₂ availability depends on a limited number of ethanol or ammonia plants, maintenance prediction and early warning systems can be valuable. Industrial gas suppliers can use AI to model demand surges, identify customers at risk, reroute fleet capacity and adjust contracts before shortages become visible to end users.

Disruption Analysis of Liquid Carbon Dioxide Market

The main disruption is the change from byproduct dependent merchant CO₂ supply to more managed and diversified CO₂ sourcing. Historically, many markets relied on low cost byproduct CO₂ from ammonia, ethanol or hydrogen plants. This model can break down when source plants close, reduce output or divert CO₂ into sequestration. In 2026, the UK government backed the reopening of the Ensus plant to safeguard domestic CO₂ supply, showing how liquid CO₂ has become a strategic input for food, beverage and healthcare sectors.

The second disruption is the rise of liquid CO₂ logistics for carbon capture. Dedicated LCO₂ carriers, storage hubs and cross border CO₂ transport are creating infrastructure that may eventually reshape merchant supply. If captured CO₂ can be purified to usable grades, new supply pools may develop. If captured CO₂ is routed to permanent storage, merchant buyers may face greater competition for available volumes. The market will increasingly require visibility into both industrial gas demand and carbon management flows.

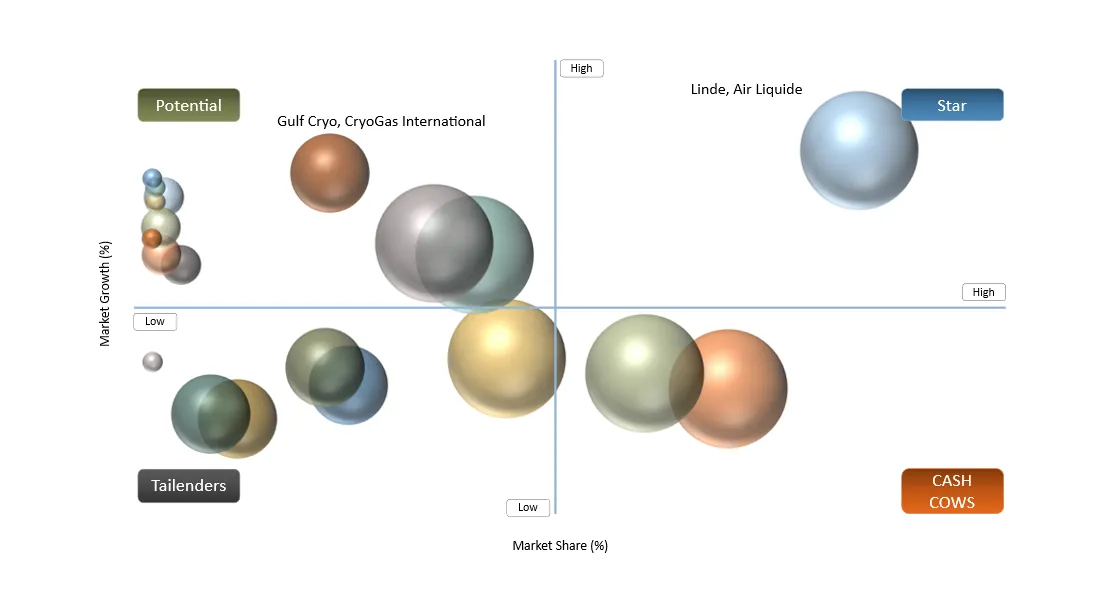

Liquid Carbon Dioxide Market BCG Matrix: Company Evaluation

STAR

Linde, Air Liquide, Air Products, Messer, Matheson, Nippon Gases and SOL Group are positioned as star players because they combine industrial gas scale, production assets, bulk logistics, customer contracts and purification expertise. Their networks allow them to serve food, beverage, healthcare, manufacturing and industrial customers while investing in carbon capture and liquefaction capabilities.

POTENTIAL

Regional suppliers, dry ice producers, CO₂ recovery specialists, biogenic CO₂ developers, storage terminal operators and LCO₂ carrier owners are potential growth players. These companies are positioned to benefit from supply shortages, local sourcing requirements, carbon capture logistics, brewery recovery systems, cold chain growth and demand for lower carbon or biogenic CO₂ sources.

Liquid Carbon Dioxide Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact | Demand Concentration | Impacted Use Case | Strategic Impact |

Food and Beverage Carbonation Demand | 24% | Global beverage and brewery clusters | Carbonation and dispense systems | Supports stable high volume food grade CO₂ contracts. |

Cold Chain and Dry Ice Growth | 20% | North America, Europe, Asia-Pacific | Frozen food, pharma, biologics, e-commerce logistics | Increases demand for liquid CO₂ feedstock and dry ice production capacity. |

CO₂ Supply Security Requirements | 18% | Regions with past shortages | Food, beverage, healthcare and meat processing | Drives multi source procurement and premium supply assurance contracts. |

CCUS and Captured CO₂ Logistics | 16% | Europe, North America, Middle East | LCO₂ shipping, terminals and storage hubs | Creates new infrastructure demand for purification, liquefaction and transport. |

Oil and Gas EOR Demand | 12% | U.S., Middle East, China | Enhanced oil recovery and field pressure support | Supports high volume industrial grade CO₂ supply where field economics are viable. |

Driver: Food, Cold Chain and Supply Assurance Demand

The strongest market driver is the combination of food and beverage consumption, cold chain growth and the need for supply continuity. CO₂ is required for beverage carbonation, modified atmosphere packaging, meat processing, freezing, chilling, dry ice and dispensing systems. These applications cannot easily switch to substitute gases without process redesign. When CO₂ supply tightens, customers may face production losses, product spoilage and logistics disruption. This makes liquid CO₂ a critical input for operational continuity.

Restraint Impact Analysis

| Restraint | Drag on Market Growth | Primary Impact Area | Impacted Use Case | Strategic Impact |

| High Storage and Transport Cost | 22% | Bulk logistics and delivered cost | Food, beverage, dry ice and industrial supply | Limits economic reach from source plants and favors local supply. |

| Dependence on Byproduct Sources | 20% | Merchant supply reliability | All bulk customers | Creates shortage risk during ammonia, ethanol or hydrogen plant outages. |

| Purity and Compliance Complexity | 14% | Food, medical and specialty grades | Beverage, healthcare, pharmaceutical and electronics | Raises qualification burden and limits supplier switching. |

| Carbon Capture Diversion Risk | 12% | Merchant availability | Food and industrial gas buyers | Captured streams may be routed to storage rather than merchant use. |

| Energy Cost Volatility | 10% | Liquefaction and refrigeration | All liquid CO₂ supply | Raises production cost and delivered price. |

Restraint: Dependence on Upstream Source Plants

The liquid CO₂ market is vulnerable because much of merchant supply comes from industrial byproducts. If an ethanol, ammonia, hydrogen or natural gas processing facility reduces production, regional CO₂ availability can tighten quickly. The customer may buy CO₂ from an industrial gas company, but the underlying source may still depend on a single upstream plant. This makes supply chain mapping a core buyer requirement. Customers with high production sensitivity should assess source concentration, backup distance and emergency supply terms before signing contracts.

Liquid Carbon Dioxide Market Segment Analysis

The global Liquid Carbon Dioxide market is segmented based on source, purity grade, application, storage and delivery mode, end user, contract model and region.

By Source: Ethanol Fermentation CO₂ Will Gain Strategic Importance

Ethanol fermentation is one of the most attractive liquid CO₂ sources because it produces relatively concentrated biogenic CO₂ that can be captured, purified and liquefied for food, beverage and industrial use. The segment is important for buyers seeking lower fossil carbon exposure and traceable CO₂ sourcing. However, it is also exposed to ethanol plant economics. If ethanol plants shut down or reduce production, merchant CO₂ availability can tighten. The UK Ensus case in 2026 illustrates this dependency, as government support was used to restart an ethanol plant to protect CO₂ supply for food, beverage and healthcare users. For suppliers, fermentation CO₂ creates a premium positioning opportunity when linked with sustainability claims, but it requires reliable plant operations, food grade purification, strong quality testing and contracts that manage seasonality.

By Source: Ammonia and Hydrogen Plants Remain Core Merchant Supply Anchors

Ammonia and hydrogen plants remain important liquid CO₂ sources because they generate concentrated CO₂ streams suitable for recovery and purification. These sources are often located near chemical, refining and industrial clusters, making them commercially attractive for large regional supply networks. The main buyer issue is operational dependency. Planned ammonia turnarounds and energy cost movements can directly affect merchant CO₂ availability and pricing. In March 2026, North American liquid CO₂ prices were influenced by ethanol and ammonia plant turnarounds as well as higher natural gas costs. Buyers need to understand whether their supplier depends on one ammonia or hydrogen plant, how long planned outages last and whether alternate sourcing is available within economic trucking distance.

By Purity Grade: Food Grade CO₂ Will Continue to Dominate Procurement Value

Food grade CO₂ is the most commercially important grade because it is used in carbonated drinks, beer, sparkling wine, meat processing, food freezing, modified atmosphere packaging and restaurant dispense systems. It requires strict control of moisture, hydrocarbons, sulfur compounds, odor, taste and other impurities that can affect product quality. Beverage customers treat CO₂ reliability as a production continuity issue because a shortage can stop bottling lines and dispensing networks. Food grade buyers increasingly require source traceability, certificates of analysis, supplier audits and emergency backup plans. The segment will remain attractive because customers value reliability and documentation, not only commodity price. Suppliers that can guarantee food grade quality across multiple regional sources will hold a procurement advantage.

By Purity Grade: Medical and Pharmaceutical Grade CO₂ Will Capture Premium Demand

Medical and pharmaceutical grade CO₂ has a smaller volume base but stronger quality requirements and premium pricing potential. It is used in medical procedures, respiratory mixtures, laboratory work, pharmaceutical processing, cryotherapy, biological sample handling and cold chain support through dry ice. Healthcare buyers require reliable documentation, validated supply chains and strict handling practices. The segment benefits from growth in pharmaceutical logistics, biologics distribution and cold chain monitoring. The commercial opportunity is strongest for suppliers that can combine medical grade gas quality with dry ice and cold chain services. The key challenge is compliance cost and the need for rigorous quality systems. Suppliers must maintain grade separation, traceability and customer support because switching risk is high in healthcare and pharmaceutical use.

By Application: Food, Beverage and Packaging Will Remain the Largest Demand Center

Food, beverage and packaging demand anchors the market because liquid CO₂ is used for carbonation, chilling, freezing, modified atmosphere packaging and product dispensing. Beverage carbonation is highly sensitive to purity and availability, while food processing values CO₂ for rapid cooling and microbial control support. Modified atmosphere packaging uses CO₂ to extend shelf life for meat, poultry, bakery, produce and ready meal products. This segment has strong buyer intent because customers need to reduce spoilage, protect production uptime and manage seasonal demand peaks. CO₂ shortages can lead to empty shelves, reduced beverage output and processing delays. Suppliers that offer tank telemetry, planned volume allocation and backup deliveries will be preferred by large food and beverage companies.

By Application: Dry Ice and Cold Chain Will Benefit from Pharma and E-Commerce Logistics

Dry ice production is a major downstream use of liquid CO₂ because dry ice is used for frozen food logistics, biologics, vaccines, laboratory samples, emergency cooling, airline catering and e-commerce grocery delivery. The segment is sensitive to liquid CO₂ feedstock availability because dry ice cannot be produced without reliable liquid CO₂ supply. Pharmaceutical logistics and specialty cold chain shipments increase demand for reliable dry ice quality and delivery. Buyers want predictable supply during seasonal peaks and emergency events. The commercial opportunity is strongest for suppliers that integrate liquid CO₂ supply, dry ice production, packaging and last mile cold chain services. As biologics and high value frozen logistics expand, dry ice users will place greater value on resilience and delivery assurance.

By Application: Oil and Gas EOR Will Remain a High-Volume Industrial Use

Oil and gas enhanced oil recovery can consume large volumes of CO₂ where geological conditions and field economics support injection. CO₂ is used to improve oil mobility, maintain reservoir pressure and increase recovery from mature fields. The use case is concentrated in regions with pipeline infrastructure, nearby CO₂ sources and favorable project economics. Liquid CO₂ can be relevant where transport distances or storage conditions require liquefied logistics, although large EOR systems often use pipeline supply. The segment’s demand is influenced by oil prices, field redevelopment plans, carbon capture incentives and availability of industrial CO₂. Suppliers serving this segment need scale, pressure management expertise and long term volume agreements. EOR also links liquid CO₂ markets with carbon capture development because captured industrial CO₂ can become an injection feedstock.

By Storage and Delivery Mode - Bulk Tanks and Road Tankers Will Define Customer Reliability

Bulk tanks and road tankers remain the backbone of merchant liquid CO₂ supply. Large customers use onsite bulk tanks connected to beverage, freezing, packaging or industrial processes. Suppliers manage replenishment through scheduled delivery or tank telemetry. The main buyer issue is runout risk. If a tank is not refilled during peak consumption or regional shortage, production can stop immediately. Road tanker availability, driver availability, truck mileage and loading terminal access all affect delivered reliability. Bulk supply contracts increasingly include minimum tank levels, telemetry, emergency refill windows and backup delivery terms. Suppliers with dense regional tanker fleets and multiple loading points can provide stronger service levels than suppliers dependent on long-distance trucking from one source plant.

By Storage and Delivery Mode: Dedicated Liquid CO₂ Carriers Will Open CCUS Logistics

Dedicated liquid CO₂ carriers are emerging as a strategic transport mode for carbon capture and storage. In 2026, Northern Lights expanded its fleet with four additional CO₂ ships, with each of the first three vessels having 12,000 cubic meters cargo capacity and the expansion supporting more than 5 million tonnes per year of transport and storage capacity. This matters for the liquid CO₂ market because it expands CO₂ from local truck based distribution into cross border maritime logistics. The opportunity is not only in industrial gas use, but also in carbon management infrastructure. Ports, storage terminals, compression facilities and liquefaction systems will become part of the value chain. Suppliers that understand both merchant CO₂ and CCS transport can capture new infrastructure opportunities.

By End User: Breweries and Beverage Producers Will Prioritize Supply Assurance

Breweries, carbonated drink companies and beverage dispense operators are highly exposed to CO₂ shortages. CO₂ affects carbonation, packaging, tank blanketing and draft dispense systems. During shortages, small breweries and beverage companies often face greater risk because larger customers may have priority allocation under contract. Buyers in this segment increasingly ask for source redundancy, emergency supply guarantees, food grade certification and transparent pricing formulas. The strongest opportunity for suppliers is to create tailored brewery and beverage programs that include bulk CO₂, cylinders, tank monitoring, backup supply and preventive service. Some breweries are also evaluating CO₂ recovery from fermentation to reduce purchased CO₂ dependence. This creates a niche opportunity for onsite recovery and circular beverage CO₂ systems.

By Contract Model: Long Term Bulk Contracts Will Replace Pure Spot Buying

Long-term bulk supply contracts are becoming more attractive because liquid CO₂ shortages can create sharp price and availability shocks. Spot buying may work for low criticality users, but food, beverage, healthcare and dry ice customers need guaranteed availability. Contracts are evolving to include volume reservation, escalation formulas, delivery service levels, tank telemetry, source disclosure, force majeure clauses and backup source options. Buyers are also using dual supplier strategies in regions with known supply risk. For suppliers, long term contracts improve asset utilization and justify investment in tanks, tankers and storage. The key commercial challenge is balancing committed volumes with upstream source uncertainty. Contracts that clearly define outage response, allocation rules and emergency pricing will become more important.

By Supply Chain Role: Captive and Onsite CO₂ Recovery Will Gain Attention

Captive and onsite CO₂ recovery is gaining attention among breweries, fermentation facilities, greenhouses and industrial users that want to reduce dependence on merchant supply. Onsite recovery can capture CO₂ generated within the customer’s process, purify it and reuse it for carbonation, inerting or process needs. The model is attractive where CO₂ is produced regularly and where purchased CO₂ exposure is high. It can reduce delivered gas cost, truck deliveries and shortage risk, but it requires capital investment, maintenance capability and quality assurance. The opportunity is strongest for medium and large breweries, ethanol plants, food fermentation facilities and greenhouse operators. Suppliers can position recovery systems as a resilience solution rather than only a sustainability tool.

Liquid Carbon Dioxide Market Geographical Penetration

U.S. Liquid Carbon Dioxide Market Landscape

The U.S. is the largest country level market due to its large beverage industry, meat processing base, dry ice demand, oilfield use and extensive industrial gas infrastructure. The country benefits from ethanol fermentation CO₂ sources, ammonia and hydrogen facilities, natural gas processing and regional gas distribution networks. However, the U.S. market is also exposed to source outages and regional logistics constraints. In 2026, North American liquid CO₂ pricing was affected by higher natural gas costs, ethanol plant turnarounds, ammonia plant turnarounds and sequestration diversion. This makes buyer strategy highly operational. Food and beverage companies need backup contracts, dry ice producers need source redundancy and oilfield buyers need long term volume planning. The U.S. market will reward suppliers that combine Gulf Coast production, Midwest ethanol sources, trucking depth and tank telemetry.

Canada Liquid Carbon Dioxide Market Outlook

Canada’s liquid CO₂ demand is supported by beverage production, breweries, frozen food, meat processing, healthcare, industrial manufacturing and oil and gas activity. Western Canada also has strategic relevance because of carbon capture and storage development, industrial clusters and energy sector demand. The market is geographically challenging because large distances increase delivered cost and make regional storage important. Canadian buyers evaluate supplier reliability, winter logistics, food grade documentation and emergency supply availability. For investors, the opportunity sits in regional storage depots, food grade CO₂ distribution, dry ice and carbon capture linked CO₂ logistics. The strongest demand centers are around major population and industrial corridors, while oil and gas demand is more concentrated in energy producing regions.

UK and Europe Liquid Carbon Dioxide Market Outlook

Europe has become a highly strategic liquid CO₂ market because food security, beverage production and carbon capture infrastructure are all shaping supply. In 2026, the UK government committed £100 million to reopen the Ensus CO₂ plant in Teesside after concerns over shortages affecting food, beverage, healthcare and nuclear sectors. This shows that CO₂ supply is now viewed as a national resilience issue. Europe is also leading liquid CO₂ transport for CCS. Northern Lights is expanding its fleet and transport capacity to more than 5 million tonnes per year. European buyers need to assess whether available CO₂ will be routed into merchant markets or permanent storage. The market opportunity is strongest in supply assurance, LCO₂ carriers, receiving terminals, food grade distribution and carbon capture linked logistics.

Germany Liquid Carbon Dioxide Market Outlook

Germany is a major demand market because of its beverage production, food processing, chemicals, industrial manufacturing, healthcare and environmental technology base. The country’s manufacturing depth creates demand for industrial grade CO₂, while breweries and beverage producers require food grade supply. Germany also sits within Europe’s changing carbon management ecosystem, where captured CO₂ transport and storage is becoming more important. Buyers need to manage energy cost exposure, regional source dependency and cross border logistics. The strongest opportunity is in high purity CO₂, long term supply contracts, dry ice distribution and CO₂ recovery from industrial sources. Suppliers with strong documentation and multi country European networks will be more competitive than single source regional suppliers.

China Liquid Carbon Dioxide Market Trends

China is one of the most important growth markets because of food processing, beverage manufacturing, chemicals, welding, electronics, healthcare and industrial applications. Large industrial clusters create multiple CO₂ source opportunities from ammonia, hydrogen, petrochemical and fermentation plants. China also has expanding carbon capture and utilization activity, which may improve captured CO₂ availability over time. Buyer needs differ by segment. Beverage and food users prioritize food grade consistency, chemical and welding customers prioritize delivered cost and reliable bulk supply, while specialty applications need higher purity documentation. The market is expected to grow with industrial production, cold chain expansion and domestic consumption. Local suppliers with regional logistics networks and high purity capability will gain advantage.

India Liquid Carbon Dioxide Market Trends

India is a high growth market supported by expanding beverage consumption, food processing, frozen food, breweries, pharmaceuticals, healthcare, welding, water treatment and industrial manufacturing. Demand is moving beyond cylinders toward bulk tanks and distribution systems as large customers scale. India’s challenge is supply reliability across regions because liquid CO₂ production, storage and tanker networks are uneven. The strongest opportunities are in beverage grade bulk supply, dry ice for pharma and food logistics, small bulk tanks for mid sized processors and high reliability supply contracts. Suppliers also have an opportunity to develop CO₂ recovery from fermentation and industrial sources. Buyers will increasingly evaluate quality documentation, delivery reliability and emergency backup rather than basic price alone.

Japan and South Korea Liquid Carbon Dioxide Market Outlook

Japan and South Korea are advanced industrial markets with demand from food and beverage, healthcare, electronics, chemical manufacturing, welding, dry ice and specialty uses. These markets place strong emphasis on quality, documentation and supply reliability. Japan is also important in liquid CO₂ carrier technology and maritime carbon capture logistics. Japanese shipping companies such as K Line and MOL are involved in Northern Lights related LCO₂ carrier agreements, giving the country a strategic role in the future CO₂ transport ecosystem. Demand growth is steady rather than explosive, but premium grades and carbon management infrastructure create high value opportunities. Suppliers that can support electronics, medical, food grade and CCS linked applications will have stronger positioning.

GCC Liquid Carbon Dioxide Market Outlook

The GCC market is strategically important because it combines oil and gas operations, petrochemicals, food and beverage growth, healthcare, cold chain and carbon management activity. Saudi Arabia, UAE and Qatar have strong industrial gas demand linked to refineries, chemicals and manufacturing, while food and beverage imports and local production require reliable food grade CO₂. The region also has potential for CO₂ use in EOR, methanol, chemicals and carbon capture hubs. Buyers require dependable bulk supply, high temperature logistics capability and quality documentation. The market opportunity is strongest in integrated CO₂ recovery from industrial facilities, storage depots near food and beverage clusters and partnerships with oil and gas companies for CO₂ utilization and storage.

South America Liquid Carbon Dioxide Market Outlook

South America demand is supported by beverage production, breweries, meat processing, frozen food, agriculture, healthcare and oil and gas. Brazil and Argentina are the most important countries due to food and beverage scale and industrial activity. Regional opportunity is linked to fermentation CO₂ recovery, beverage grade supply and cold chain expansion. However, logistics and currency volatility can affect delivered cost. Buyers in this region value supplier continuity and local distribution reach. The strongest investment opportunities are in bulk storage, tanker fleet upgrades, dry ice production and CO₂ recovery near ethanol or fermentation sites. Supplier competitiveness depends on local presence and ability to support food grade customers across large geographies.

| Region | Key Countries | Demand Drivers | Buyer Intent Signal |

| North America | U.S., Canada, Mexico | Beverage, dry ice, food processing, oilfield, healthcare, industrial gas | Supply assurance, backup contracts, source diversification and telemetry. |

| Europe | Germany, UK, France, Spain, Italy, Poland | Food security, beverage, healthcare, manufacturing and CCS logistics | Resilience planning, LCO₂ carriers, plant restart policy and carbon storage linkages. |

| Asia-Pacific | China, India, Japan, South Korea, Australia, Southeast Asia | Food processing, beverage, industrial manufacturing, healthcare and cold chain | Bulk conversion, regional supply buildout and high purity demand. |

| South America | Brazil, Argentina | Beverage, meat processing, breweries, agriculture and food logistics | Local recovery, bulk storage and food grade supply. |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye, Nigeria | Oil and gas, petrochemicals, beverage, healthcare and food processing | Integrated CO₂ recovery, EOR supply, storage hubs and industrial gas distribution. |

Liquid Carbon Dioxide Market Competitive Landscape

- Competition is moving from basic CO₂ supply toward reliability led solutions with tank telemetry, backup sourcing, multi grade supply and emergency delivery service.

- Large industrial gas companies hold advantages through production assets, purification capability, tanker fleets, bulk tank ownership and customer contracts.

- Regional suppliers compete through local proximity, responsive delivery, flexible contracts and strong relationships with food processors, breweries and dry ice producers.

- CO₂ recovery specialists are gaining attention as customers seek onsite recovery, biogenic CO₂ sources and lower carbon supply options.

- Shipping companies and CCS infrastructure developers are entering the liquid CO₂ ecosystem through LCO₂ carrier agreements and terminal development.

- Future competition will depend on source control, regional redundancy, purity documentation, logistics reliability and ability to serve both merchant and carbon management customers.

Key Companies of Liquid Carbon Dioxide Market

- Linde plc

- Air Liquide

- Air Products and Chemicals, Inc.

- Messer Group

- Matheson Tri-Gas

- Nippon Gases

- SOL Group

- Gulf Cryo

- INOX Air Products

- Iwatani Corporation

- Continental Carbonic Products

- Coregas

- MISC Berhad

- Kawasaki Kisen Kaisha

- Mitsui O.S.K. Lines

- Northern Lights JV

- Chart Industries

- CryoGas International

- BOSCO India

- SICGIL Industrial Gases

Liquid Carbon Dioxide Market Major Pain Points

- Dependence on upstream source plants creates exposure to ethanol, ammonia, hydrogen and natural gas processing outages.

- High transportation cost limits economic delivery range from liquefaction plants.

- Food grade and medical grade documentation increases supplier qualification burden.

- Seasonal beverage and food demand creates peak period tightening.

- Customers often lack visibility into supplier source concentration and backup supply availability.

- Dry ice and cold chain users face immediate disruption if liquid CO₂ feedstock is unavailable.

- CCUS projects may compete for captured CO₂ streams, changing merchant market availability.

- Small buyers face higher risk during regional allocation events because large contracted customers may receive priority.

Liquid Carbon Dioxide Market Recent Developments

- January, 2026: MISC Berhad, in partnership with K Line, secured a long term Time Charter Party from Northern Lights JV DA to provide a dedicated liquefied carbon dioxide carrier for the next phase of the Northern Lights CCS transport and storage project.

- February, 2026: Northern Lights announced expansion of its fleet with four additional CO₂ ships, supporting signed customer agreements and the expansion of transport and storage capacity to more than 5 million tonnes of CO₂ per year.

- March, 2026: The UK government committed £100 million to reopen the Ensus CO₂ plant in Teesside to protect national CO₂ supply for food, beverage, healthcare and nuclear sector requirements.

- April, 2026: A second newbuild LCO₂ carrier award was expected under the Northern Lights expansion sequence following the first time charter announcement, strengthening the maritime liquid CO₂ logistics ecosystem for European CCS.

- March, 2026: North American liquid CO₂ pricing was affected by higher natural gas costs, ethanol plant turnarounds, ammonia plant turnarounds and sequestration diversion, reinforcing the need for buyer contracts that manage source and logistics risk.

- July, 2026: Air Liquide announced more than US$200 million of investment to support chemical manufacturing expansion in Texas, underlining continued industrial gas infrastructure investment in U.S. Gulf Coast industrial corridors.

Analyst View / Opinion on Liquid Carbon Dioxide Market

- The Liquid Carbon Dioxide market is expected to shift from transactional gas supply toward supply resilience and source assurance based procurement.

- Food and beverage will remain the largest use case, but carbon capture logistics will become the most disruptive long term infrastructure theme.

- Buyers will increasingly demand source transparency, tank telemetry, emergency backup plans and force majeure protection.

- CO₂ recovery from fermentation and industrial byproduct streams will gain stronger strategic importance because it supports both supply security and sustainability positioning.

- Regional shortages will continue to occur when upstream source plants undergo maintenance, close or redirect CO₂ to storage projects.

- Suppliers with diversified source portfolios, local storage, tanker fleet depth and high purity documentation will gain long-term market leadership.

Liquid Carbon Dioxide Market Target Audience

| Industry | Who Should Buy This Report? | Reason to Buy This Report |

| Industrial Gases | Business Development Heads, Supply Chain Leaders, Regional Managers | To identify demand clusters, source risk, pricing dynamics and investment opportunities in CO₂ recovery and distribution. |

| Food and Beverage | Procurement Heads, Plant Managers, Quality Teams | To evaluate CO₂ supply reliability, food grade requirements, backup contracts and regional supplier risk. |

| Breweries and Beverage Dispense | Brewery Owners, Operations Managers, Distributors | To plan carbonation supply, onsite recovery, emergency sourcing and cost management. |

| Cold Chain and Dry Ice | Dry Ice Producers, Pharma Logistics, Frozen Food Logistics | To assess liquid CO₂ feedstock reliability, storage, dry ice demand and backup supply models. |

| Oil and Gas | EOR Teams, Carbon Management Leaders, Procurement Heads | To understand CO₂ sourcing, logistics, injection use and links between EOR and CCUS. |

| Healthcare and Pharmaceuticals | Medical Gas Buyers, Pharma Supply Chain Leaders | To evaluate high purity CO₂, dry ice logistics, documentation and critical supply continuity. |

| Shipping and Ports | LCO₂ Carrier Owners, Terminal Operators, Port Authorities | To identify liquid CO₂ transport and CCS logistics opportunities. |

| Investment and Consulting | Investors, PE Firms, Strategy Consultants | To identify high growth assets in CO₂ recovery, storage, logistics, digital telemetry and CCUS transport. |

Why Choose DATAM?

- Data-driven insights with granular market analysis, pricing intelligence, value chain mapping and buyer decision criteria.

- Post-purchase support and expert analyst consultations tailored to specific supply, procurement, investment and market entry questions.

- Quarterly white papers and case studies related to purchased titles, supporting operational, commercial and market strategy decisions.

- Annual updates on purchased reports, allowing clients to stay aligned with technology shifts, supply events, regulations and competitive changes.

- Specialized focus on emerging markets with country level insights instead of generic geographic overviews.

- Strategic value through customized intelligence that goes beyond broad databases and supports actionable business decisions.

What DATAM Uniquely Provides

- Detailed 10 year market predictions by source, purity grade, application, storage and delivery mode, end user, contract model and region.

- Thorough competitive analysis covering industrial gas suppliers, recovery technology providers, dry ice companies, distributors and LCO₂ transport players.

- Comprehensive supply chain analysis covering ethanol, ammonia, hydrogen, natural gas processing, captured industrial CO₂, purification, liquefaction, storage and distribution.

- Strategic market insights through pricing intelligence, import-export analysis, AI impact evaluation, BCG matrix and disruption analysis.

- Actionable white space and investment opportunity mapping across regional backup supply, onsite recovery, biogenic CO₂, high purity grades and LCO₂ transport infrastructure.

- Country level recommendations that support procurement, market entry, supplier evaluation, investment screening and risk mitigation.