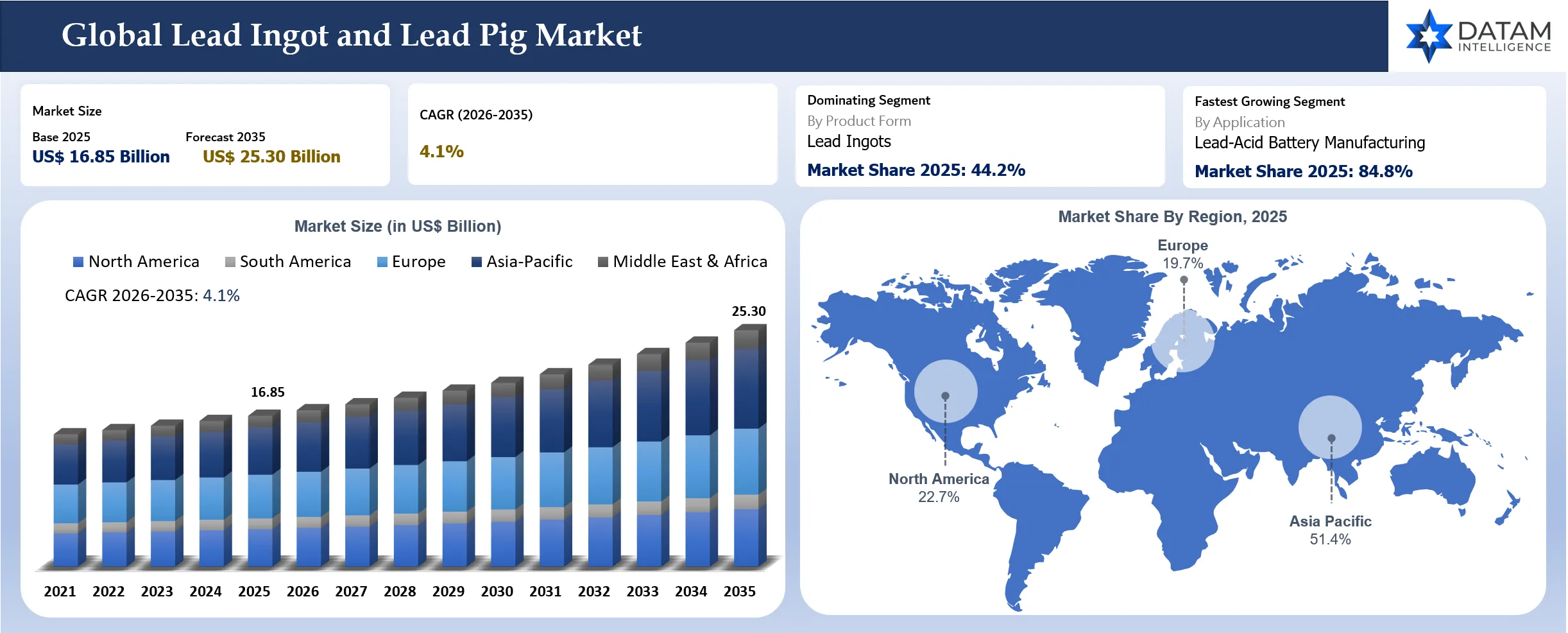

Lead Ingot and Lead Pig Market Size

The global lead ingot and lead pig market reached US$ 16.85 billion in 2025 and is expected to reach US$ 25.30 billion by 2035, growing with a CAGR of 4.1% during the forecast period 2026-2035. The use of lead ingots and pigs will continue to be very essential raw materials in the production of lead-acid batteries that are used in cars, industrial backup power generation, telecommunication infrastructures, renewable energy storage, forklifts, and data centers. Even with the fast development in lithium-ion batteries, the use of lead-acid batteries remains dominant in the starter, lighting, and ignition (SLI) applications and energy storage due to its economic feasibility, existing recycling systems, and high reliability. Another factor that is driving the lead-acid battery market is the development of formal lead recycling system and government-backed programs for the responsible collection of used batteries and production of secondary metals. Lead is one of the most recycled industrial metals with recycled metal accounting for a considerable proportion of global lead consumption. Lead secondary production will be more significant due to the sustainability concerns and fluctuating prices in mining operations.

The International Lead Association (ILA), quoting UNICEF and Pure Earth, estimates that as much as 50 percent of used lead-acid batteries from many low- and middle-income countries are recycled through informal means, thus presenting a large-scale opportunity for innovation in recycling processes that adhere to proper regulations. However, according to reports from the US Geological Survey (USGS), in 2023 alone, the United States imported around 365,000 metric tonnes of refined lead as well as 609,000 metric tonnes of used lead-acid batteries.

Key Takeaways

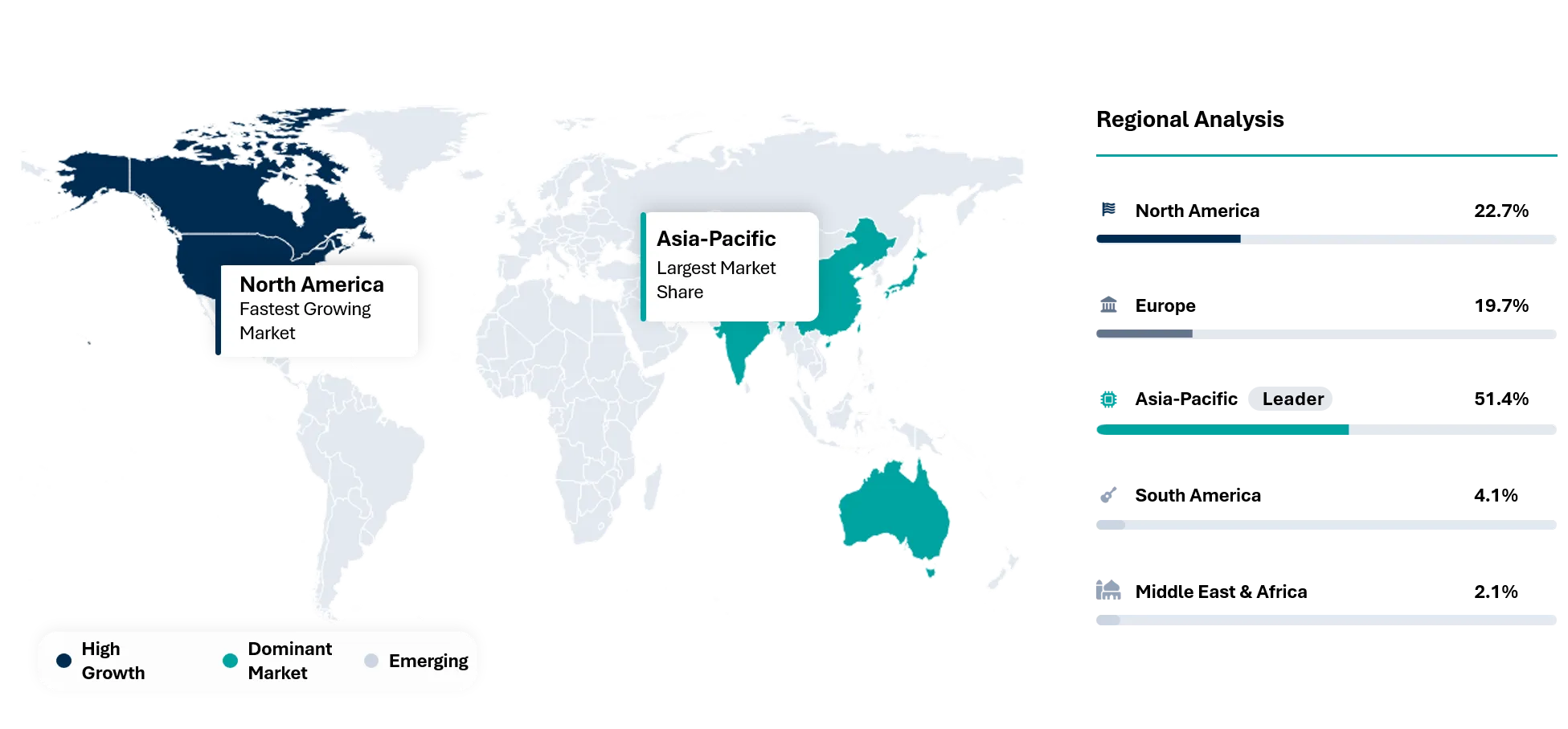

- Asia-Pacific is dominating with 51.4% market share throughout the forecast period, supported by its extensive secondary lead recycling ecosystem, expanding automotive battery manufacturing, and growing investments in energy storage systems, while Europe maintains a significant market position driven by stringent circular economy regulations and high lead-acid battery recycling rates.

- In 2025, Secondary (Recycled) lead accounted for the largest share of the global market, owing to its cost competitiveness, lower carbon footprint, and widespread use in lead-acid battery production across automotive, industrial, and backup power applications.

- The rapid expansion of closed-loop lead recycling systems and investments in advanced battery recycling infrastructure are major factors accelerating growth in the global Lead Ingot and Lead Pig Market, particularly as governments promote resource efficiency and stricter environmental compliance.

- Gravita India Ltd., Ecobat, and Korea Zinc have established themselves as leading players in the market through continuous capacity expansions, vertically integrated recycling operations, strategic acquisitions, and investments in high-purity secondary lead production to meet rising global demand from the automotive and energy storage sectors.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 16.85 Billion | |

| 2035 Projected Market Size | US$ 25.30 Billion | |

| CAGR (2026-2035) | 4.1% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | North America | |

| By Product Form | Lead Ingots, Lead Pigs, Lead Alloy Ingots, Jumbo Ingots, Small Ingots, Sows and Blocks, Others | |

| By Purity | 99.97% Lead, 99.985% Lead, 99.99% Lead, 99.995% Lead, Custom Alloy Grade Lead, Others | |

| By Source | Primary Refined Lead, Secondary Refined Lead, Lead From Battery Recycling, Lead From Mine Concentrate, Lead From Industrial Scrap, Others | |

| By Application | Lead-Acid Battery Manufacturing, Cable Sheathing, Radiation Shielding, Ammunition and Ballast, Solders and Alloys, Chemical and Pigment Production, Construction and Roofing, Others | |

| By End-User | Battery Manufacturers, Metal Traders and Distributors, Cable Manufacturers, Radiation Shielding Fabricators, Automotive Aftermarket Suppliers, Industrial Alloy Producers, Construction Material Suppliers, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia, Thailand, Vietnam, Philippines | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye, Nigeria | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why does this report matter in 2026?

In 2026, the global ingot and lead pigs market will move into a more strategic stage as the demand for this product in the automobile batteries, energy storage, industrial production, and recycling sectors will be gaining momentum not only in developed but also in emerging nations. Investments in the production of batteries, development of renewable energy storage facilities, and an increasing focus on circular economy programs are driving the consumption of refined lead materials across the world.

On the other hand, lead producers and processors are under mounting pressures to assure sustainable sources of raw materials, adherence to tough environmental laws, and efficiency of production processes against volatile levels of mine production and supply of secondary lead. The introduction of more sophisticated smelting technologies, increased use of recycled lead, strictness of emission reduction policies, and demands in the manufacture of batteries are changing the business environment. More knowledge on lead procurement methods, efficiencies of secondary lead processing, refining capacity, prices, and regulation is demanded by buyers, investors, and industrial players in order to assess supply security and commercial competitiveness of lead ingot and lead pig producers.

White Space & Investment Opportunities

- Secondary lead recycling capacity remains undersupplied as battery scrap availability increases globally.

- Low-carbon lead smelting technologies attract investment amid tightening industrial emission regulations.

- Regional refining facilities in India, Southeast Asia, Africa, and South America support localized metal supply.

- High-purity lead ingot production for energy storage, radiation shielding, and specialty industrial applications offers premium growth opportunities.

Future Market Transformation

By 2035, the international lead ingot and lead pig markets will move towards a circular and low carbon metals ecosystem facilitated by modern recycling techniques, digitalized smelter processes, and increased environmental compliance. Manufacturers will start to include in their value chains collection, refining, emissions management, and verified low carbon lead production. The business models will become more focused on securing agreements on sustainable metal recycling and partnerships with battery makers and other industries. Automation, process optimization through artificial intelligence, and using renewable power for smelters will increase efficiency and reduce emissions. Most successful businesses will feature a combination of global recycling systems, environmentally friendly production, secured sources of feedstock, and lead production facilities.

Buyer Decision-Making Criteria

Batteries, cable manufacturers, companies that make products for protecting against radiation and industrial fabricators use criteria such as metal purity, quality, adherence to regulations, stable pricing and deliveries for assessing the quality of lead ingot and lead pig manufacturers. Chemistry of metal and purification of metal from impurities is one of the main selection criteria whereas supply reliability and possibility of using recycled materials play an important role in choosing suppliers. Buyers increasingly look for environmentally friendly suppliers and those who can provide recycled materials for meeting the sustainability goals.

Economic & Investment Analysis

Increasing prices of electricity and fuels will affect the economics of smelting directly, while increased regulations regarding emission will result in development of cleaner refining technologies. Variability in the supply of the concentrate of lead and batteries recycling will affect the availability of resources and their price levels. Fluctuation in currency rates influences global trade of the element, especially in Asia-Pacific, Europe, and the Americas regions. However, despite periodic demand for the product from the automotive industries, further investments in energy storage technologies, power supply in the industry, telecom systems, and circular economy will promote its usage in the future.

Investment Trends in the Market

- Advanced secondary lead recycling and battery recovery facilities.

- Automated smelting, refining, casting, and digital process control systems.

- Expansion of regional refining capacity near battery manufacturing hubs.

- Low-emission furnaces, renewable-powered operations, and carbon reduction technologies.

- High-purity lead ingot production for energy storage, radiation shielding, and specialized industrial applications.

Strategic Indicators For Lead Ingot and Lead Pig

High Regulation Impact

The global lead ingot and lead pig market is facing more stringent regulations since environmental compliance has become the key competitive edge in this market. In Europe, the EU has been making further tightening of industrial emissions and battery waste recovery under the new implementation of Battery Regulation, leading to higher cost of compliance for primary smelters and benefitting the secondary lead sector. In the U.S., air emission regulations and hazardous waste regulations in lead processing plants have been becoming more stringent, urging the improvement of facilities. In China, environmental checks on inefficient smelters have been increasing rapidly, while India has enforced stricter Extended Producer Responsibility (EPR) for batteries.

High Investment Activity

Investment trends in the international lead ingot and lead pig industry have become more focused on investments in secondary lead operations, battery recycling systems, and environmentally sustainable smelting technologies. China stays the leading country in investing in recycling systems related to electric vehicle and energy storage supply chains. India sees a significant rise in capacity among structured recyclers owing to better laws on batteries collection. The US is now investing in its critical mineral security and recycling facilities. Europe is updating their smelters with respect to their energy efficiency and regulation. Australia is increasing the mining efficiency of lead with automation for the future production of refined lead.

Supply Chain Disruption

Lead ingot and pig lead market is still experiencing supply chain issues due to scarcity of concentrate, logistic issues, and geopolitical adjustments. Environmental inspections in China tend to limit the throughput of lead smelting activities, thus leading to limited supplies of refined lead in the region. Australia and Peru still play an important role in supplying concentrates, which makes the global supply chain susceptible to mining issues and export limitations. European manufacturers are still struggling with high risks associated with producing due to high energy prices, while transportation disruptions through the Red Sea have delayed delivery times of refined lead shipments to Europe and Asia.

Pricing Volatility

Prices of lead ingot and pig have continued to be highly volatile due to the movement of refined metal prices on account of the dynamics of concentrate availability, recycling raw material availability, power cost, and demand from batteries industry. China still has the biggest influence by virtue of the rate of operations of its smelters and stock movements. The prices in Europe remain vulnerable to power cost which is critical for primary refining process, while those in North America remain resilient to replacement demand from battery manufacturers.

Procurement Pressure

Procurement managers in the lead ingot and lead pig sectors have to confront ever-increasing challenges in acquiring compliant, traceable, and sustainable sources of refined lead while keeping costs competitive. OEMs from Europe have been demanding suppliers that have undergone ESG certification and recycled content validation, thus limiting the number of potential suppliers. Battery producers from the United States need to consider sourcing within the country to boost their supply security. Recyclers from India are competing intensely for the used batteries as input sources. Chinese companies are still using vertically integrated recycling facilities to ensure access to the inputs.

New Technology Adoption

The use of technology in the market of lead ingot and lead pigs has been centered around intelligent smelting, automatic disassembly of batteries, and advanced hydrometallurgical recycling. China is leading the way when it comes to the implementation of AI-based process optimization and digital control of integrated recycling plants for better metals recovery and decreased emissions. In Europe, the use of low-carbon smelting technologies has been on the rise thanks to high environmental goals. The U.S. is still making investments into automation and predictive maintenance in secondary lead plants. India is quickly updating its organized recycling plants with automation tools.

Regional Expansion Opportunity

The Asia-Pacific region provides the best scope for growth via robust battery recycling infrastructure, increased car production, and circular economy laws. China and India keep on improving their systems to recover lead in an organized manner, while the growth of manufacturing activity in Southeast Asia continues to fuel demand for refined lead, which can be used in automotive, industrial, and backup power generation activities. North America is a good source of growth potential due to critical mineral policies, enhanced battery recycling capacity, and reshoring measures within the region.

Government Policy Support

Government policy is becoming increasingly influential on the lead ingot and lead pigs markets via recycling requirements, critical minerals strategy, and environmental modernization efforts. The EU's battery regulations will boost secondary lead use in battery production chains. The U.S. government will keep supporting domestic critical minerals and battery recycling ventures via industrial policies. The Indian extended producer responsibility system will increase formal battery collection and organized recycling systems to bolster refined lead supplies. China's environmental regulations and resource efficiency drive will keep being enforced within its non-ferrous metal industry. Australia is developing sustainable mine investments to secure long-term concentrates for global refined lead production companies.

Import Export and Pricing Intelligence

The global trade trends for lead ingots and pigs are now driven by the rise in battery recycling, stringent environmental regulations, and localization strategy. China is the major player in the refined lead and recycled lead trade, whereas Australia is still supplying lead concentrates. The country of India is steadily decreasing its dependency on imports of refined lead through domestic recycling capability. European nations' import strategies have become more environment-friendly, thus changing the international trading dynamics.

The prices for lead ingots and pigs are now governed by the dynamics between availability of recycled lead, concentrate availability, energy prices, environmental compliance cost, and cycle of battery consumption. Regional price differentials are increasing owing to transport cost, compliance costs, and local supply-demand gaps. The buyers now engage in negotiating long-term contracts and benchmark-based pricing arrangements.

| HS Code | Reporter | Trade Flow | 2025 Trade Value (US$) | Interpretation |

| 780110 | U.S. | Import | 940.9 Million | Strong import dependence reflects robust domestic lead consumption across manufacturing industries. |

| 780110 | Singapore | Import | 607.8 Million | Regional trading hub drives substantial lead imports supporting industrial redistribution activities. |

| 780110 | South Korea | Export | 498.7 Million | Advanced smelting capacity strengthens export competitiveness in refined lead products globally. |

| 780110 | Australia | Export | 305.8 Million | Abundant mining resources support consistent refined lead exports to global markets. |

AI Impact Analysis

AI is changing the industry of lead ingots and lead pigs through efficient processes, predictive maintenance, raw material quality, and environmental compliance. The leading smelters in this industry have introduced AI-based process control that is used to manage and optimize the temperature inside furnaces and recover as much metal as possible in order to reduce energy consumption. AI-based predictive maintenance technology is helping to predict the quality of concentrate, the quantity of battery scrap, and the maintenance schedule, thereby avoiding any interruptions in the process. AI-based analytics help in procurement planning and computer vision technology helps to dismantle batteries.

Disruption Analysis

With the rise in the trend of secondary lead production, mining-based business models are being disrupted, with the amount of recycled lead constituting an ever-growing share of worldwide refined lead production. Investments in battery disassembly automation, smelting, and hydrometallurgical processes are contributing to an increase in metal recovery efficiency and to lower levels of both emissions and energy usage. Technological innovation allows producers to operate in a more efficient manner and meet all the necessary standards.

Manufacturers are increasingly obliged to make use of new environmentally friendly production techniques, emission filters, and closed recycling plants, thus establishing themselves as innovative companies and gaining a competitive advantage against traditional smelters. However, on the other hand, lead concentrate supply risks, political instabilities in terms of mining, and changes in world energy prices remain relevant.

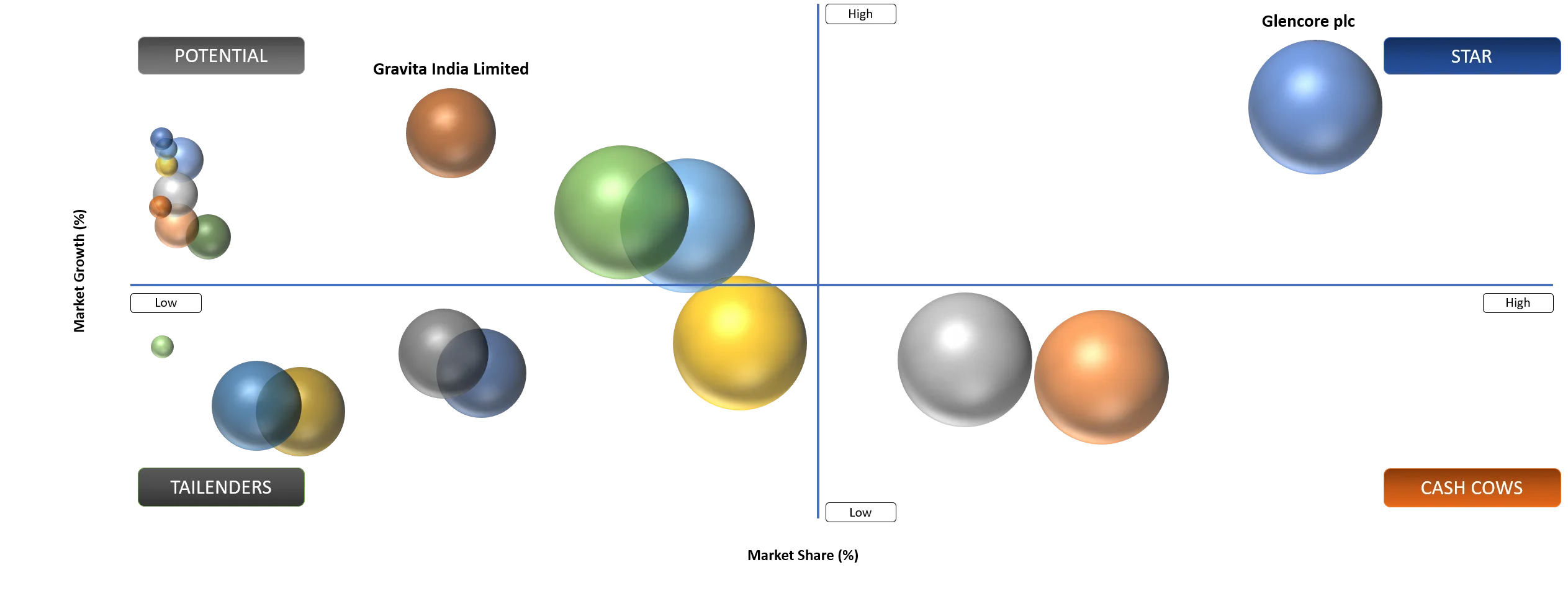

BCG Matrix: Company Evaluation

STAR

The stars segment comprises vertically integrated producers with strong refining capabilities, established recycling networks, and diversified supply contracts across automotive, industrial battery, radiation shielding, and infrastructure applications. Companies continue to strengthen their market leadership through capacity expansions, advanced secondary lead recycling technologies, sustainability initiatives, and long-term partnerships with battery manufacturers. The ability to maintain consistent product quality, comply with increasingly stringent environmental regulations, and optimize raw material procurement enables them to capture high-volume demand while preserving strong operating margins in both developed and emerging markets.

POTENTIAL

The potential players category includes regional smelters, emerging recyclers, and specialty lead manufacturers that possess significant expansion opportunities but currently maintain comparatively lower global market penetration. Companies are investing in modernization, emission-control systems, and circular economy initiatives to improve competitiveness. Rising demand for recycled lead, increasing localization of battery supply chains, and government support for sustainable metal recovery provide favorable growth conditions. Strategic acquisitions, technological upgrades, and expansion into high-purity lead products are expected to enable these companies to gradually improve their competitive positioning and evolve into stronger market participants.

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Rising Demand from Lead-Acid Battery Manufacturing Across Automotive and Industrial Sectors | 5.30% | China, India, U.S., Germany, and Southeast Asia battery manufacturing hubs | Automotive SLI batteries, industrial backup power, motive power batteries | Strengthens primary and secondary lead demand, supporting stable global production growth |

Expanding Renewable Energy Storage and Grid Backup Infrastructure | 4.90% | Asia-Pacific, Middle East, Europe, and emerging power infrastructure markets | Stationary energy storage, telecom towers, UPS systems, renewable integration | Increases lead ingot consumption for reliable and cost-effective energy storage solutions |

Growing Recycling Capacity Supporting Circular Lead Supply Chains | 4.60% | North America, Europe, China, and organized recycling ecosystems | Secondary lead production, battery recycling, refined lead manufacturing | Enhances raw material availability while reducing environmental footprint and production costs |

Increasing Demand from Construction, Radiation Shielding, and Industrial Applications | 4.20% | Healthcare infrastructure, nuclear facilities, and commercial construction markets | Radiation shielding, cable sheathing, industrial castings, protective barriers | Diversifies end-use demand beyond batteries, improving long-term market resilience |

Growing Demand from Lead-Acid Battery Manufacturing

Lead ingot and lead pig global market growth can be attributed mainly to the ongoing production of lead acid batteries, which have various uses ranging from automobiles to industries as well as renewable energy storage applications. In the view of the International Lead Association, batteries form 85% of the world’s total demand for refined lead. Besides, data centers, telecommunication facilities, hospitals, and industrial backup facilities keep driving the demand for high purity lead ingots. In addition, there is an increasing use of stationary lead acid battery technology as a result of the increased installation of renewable energy facilities in developing countries.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Stringent Environmental Regulations on Lead Production and Emissions | 4.50% | Primary smelting operations and compliance costs | Lead ingot manufacturing, secondary refining facilities | Increases operational expenses and limits capacity expansion across regulated markets |

Volatility in Lead Ore and Recycled Scrap Supply | 4.10% | Raw material availability and procurement stability | Battery-grade lead production, industrial lead casting | Creates supply disruptions and impacts long-term production planning |

Rising Competition from Alternative Lightweight Materials | 3.70% | Material substitution in automotive and construction sectors | Cable sheathing, radiation shielding, industrial components | Reduces demand in non-essential lead applications and accelerates material replacement |

High Energy Costs and Carbon Reduction Pressures | 4.00% | Smelting efficiency and manufacturing economics | Primary and secondary lead ingot production | Compresses producer margins and delays investments in production capacity |

Stringent Environmental Regulations and Smelting Compliance Challenges

Production of lead is an energy-intensive activity, which calls for considerable expenditures on air pollution, water purification, and occupational health programs. As reported by UNEP and WHO, lead pollution continues to be a major problem in terms of environmental health in the world, thus forcing governments to introduce tougher emission requirements for primary and secondary smelters. Tougher compliance with environmental standards has increased operating costs and constrained capacity growth in some regions. Moreover, licensing problems for new smelters and increases in energy prices are imposing pressures on companies to produce more recycled lead and less primary mining lead.

Segmentation Analysis

The global lead ingot and lead pig market is segmented based on product form, purity, source, application, end-user and region.

By End-User

Automotive Battery Manufacturing Leads Market Demand

The automotive battery industry constitutes the biggest sectoral consumer of lead ingots and pigs due to continued requirement of SLI batteries in automobiles, trucks, farm equipment, and construction vehicles. Even as the adoption rate of electric vehicles increases, conventional vehicles still need lead-acid batteries for auxiliary services. At the same time, a huge number of internal combustion vehicles around the globe are contributing to continued replacement battery demand. The factors ensure continued demand for refined lead-based products as well as encourage battery manufacturers to have a steady supply of recycled and virgin lead ingots.

By Source

Secondary Lead Recycling Gains Strategic Importance

Lead recycling from batteries is becoming the fastest growing method of production because of the development of circular economy initiatives and government support for battery collection schemes. The International Lead Association claims that recycling rates of 99% for lead-acid batteries can be observed in many developed countries, which makes these batteries the most recycled products among consumers in the world. According to USGS, secondary lead production remains the major source of refined lead in the USA, helping to avoid reliance on newly extracted lead ores. The investments in such areas as automation in battery disassembling, hydrometallurgy, and emissions reduction are leading to improved efficiency and decreased negative effects on the environment.

Geographical Penetration

U.S. Lead Ingot and Lead Pig Market Landscape

The United States remains one of the world's most strategically important markets for lead ingots and lead pigs, supported by its highly developed secondary lead recycling industry and resilient demand from automotive, industrial, defense, and energy storage applications. According to the U.S. Geological Survey, the U.S. produced approximately 1.05 million metric tons of refined lead in 2025, with more than 90% originating from recycled lead-acid batteries, making it one of the most circular metal value chains globally.

Growing investments in grid resilience, data center backup systems, telecommunications infrastructure, and industrial uninterruptible power supply (UPS) installations are sustaining demand for refined lead products despite increasing electric vehicle adoption. Simultaneously, stricter domestic environmental regulations are encouraging smelters to modernize refining technologies and improve emission controls, supporting higher-quality lead ingot production with reduced environmental impact.

According to the International Lead Association, lead-acid batteries continue to account for over 70% of rechargeable battery demand by unit volume worldwide, reinforcing steady consumption of lead ingots across replacement automotive batteries manufactured in North America. Additionally, continued infrastructure upgrades supported through federal investment programs are increasing demand for reliable backup power systems across hospitals, transportation hubs, utilities, and communication networks, where lead-based batteries remain the preferred technology due to proven reliability, safety, recyclability, and lower lifecycle costs.

Japan Lead Ingot and Lead Pig Market Outlook

Japan represents a technologically sophisticated lead ingot and lead pig market characterized by advanced recycling capabilities, high-purity refining technologies, and stringent environmental standards. Unlike resource-rich countries, Japan relies heavily on secondary lead recovery and imported concentrates while maximizing material efficiency through its well-established circular economy. According to the Japan Oil, Gas and Metals National Corporation and the Ministry of Economy, Trade and Industry, recycling remains central to Japan's non-ferrous metals strategy, with lead recovered primarily from end-of-life automotive and industrial batteries.

Japan is also strengthening supply-chain resilience through investments in advanced recycling technologies and sustainable metallurgy. The Japanese government has expanded support for resource circulation under its national circular economy initiatives, encouraging greater recovery of strategic metals from end-of-life products while reducing reliance on imported raw materials. According to the International Energy Agency, Japan continues investing heavily in grid resilience and energy storage infrastructure to improve electricity security, supporting ongoing deployment of stationary battery systems where lead-acid technology remains widely used for emergency backup applications.

China Lead Ingot and Lead Pig Market Trends

China continues to dominate the global lead ingot and lead pig industry through its integrated mining, smelting, refining, and battery manufacturing ecosystem. Strong domestic demand from automotive batteries, electric bicycles, industrial motive power batteries, telecom infrastructure, and renewable energy backup systems continues to sustain production volumes. China also remains the world's largest producer of lead-acid batteries, supported by its extensive manufacturing base and export competitiveness. The country's rapidly expanding renewable power infrastructure, including large-scale solar and wind installations, has increased demand for stationary energy storage solutions where advanced lead batteries remain cost-effective for backup and grid-support applications. Government initiatives promoting resource efficiency have also accelerated investments in environmentally compliant secondary lead recycling facilities, improving raw material availability while reducing dependence on primary mining.

China is simultaneously strengthening environmental governance across the lead industry through stricter emission standards and circular economy policies. The Ministry of Ecology and Environment of the People's Republic of China continues to enforce tighter pollution control requirements for non-ferrous metal smelters, encouraging modernization of refining operations and closure of inefficient facilities. According to the China Nonferrous Metals Industry Association, investment in intelligent smelting technologies, waste heat recovery, and cleaner metallurgy has accelerated as producers seek greater efficiency and lower carbon intensity. China also maintains one of the world's largest battery recycling networks, supporting continuous production of secondary lead ingots for domestic consumption.

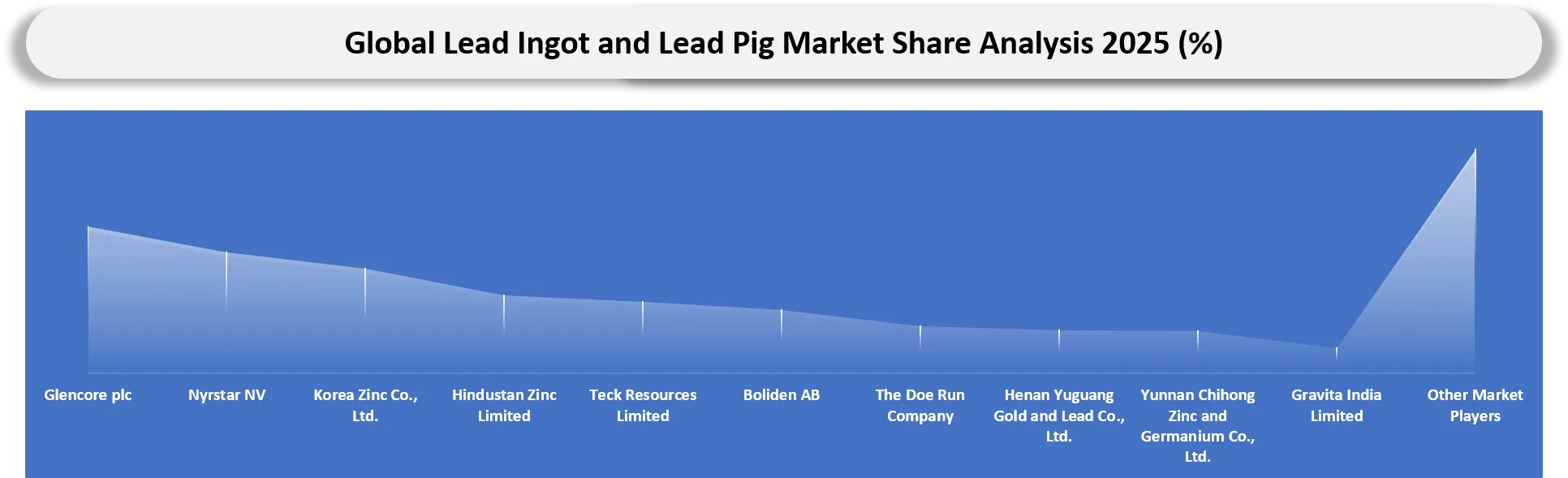

Competitive Landscape

- The global lead ingot and lead pig market is moderately consolidated, with competition centered on integrated mining operations, secondary recycling capabilities, refining efficiency, product purity, environmental compliance, and secure raw material sourcing.

- Major participants continue investing in battery recycling, low-emission smelting technologies, energy-efficient refining processes, and closed-loop supply chains to strengthen sustainability credentials and comply with tightening environmental regulations.

- Strategic partnerships between battery manufacturers, recycling companies, and metal refiners are becoming increasingly important as governments promote circular economy initiatives and domestic critical mineral independence.

Company Coverage Preview

Glencore plc has established itself as one of the most influential participants in the global lead ingot and lead pig market through its extensive vertically integrated mining, smelting, refining, and metals marketing operations. The company possesses significant expertise in primary lead production, secondary lead recycling, concentrate processing, and global commodity logistics, enabling a reliable supply to battery, automotive, construction, and industrial manufacturing sectors. Its diversified portfolio of mining assets and metallurgical facilities across multiple regions strengthens supply security and operational resilience amid evolving market conditions. Continuous investments in smelter optimization, responsible sourcing, emissions reduction, and circular economy initiatives reinforce its competitive position. Backed by a broad international trading network and integrated value chain, Glencore remains strategically positioned as a leading supplier of high-quality refined lead ingots and lead pigs for global industrial applications.

Key Companies

- Glencore plc

- Nyrstar NV

- Korea Zinc Co., Ltd.

- Hindustan Zinc Limited

- Teck Resources Limited

- Boliden AB

- The Doe Run Company

- Henan Yuguang Gold and Lead Co., Ltd.

- Yunnan Chihong Zinc and Germanium Co., Ltd.

- Gravita India Limited

- Ecobat Resources

- Campine NV

- Recylex S.A.

- Toho Zinc Co., Ltd.

- Mitsubishi Materials Corporation

- Dowa Holdings Co., Ltd.

- Vedanta Limited

- Penox Group GmbH

- Hunan Shuikoushan Nonferrous Metals Group Co., Ltd.

- Exide Industries Limited

MAJOR PAIN POINTS

- Volatile lead concentrate and recycled scrap availability disrupts stable raw material procurement.

- Stringent environmental regulations increase compliance costs across lead smelting and refining operations.

- Fluctuating lead prices reduce profitability and complicate long-term supply contract negotiations.

- High energy consumption significantly elevates production costs and operational efficiency challenges.

- Growing occupational health concerns require continuous investments in worker safety and emissions control.

- Dependence on automotive battery demand exposes manufacturers to end-market demand fluctuations.

- Limited high-grade lead ore reserves increase reliance on secondary lead recycling sources.

RECENT DEVELOPMENTS

- April 2026: Nyrstar NV completed sale of its U.S. mining and smelting assets to Korea Zinc after regulatory approvals, ensuring uninterrupted operations.

- April 2026: Korea Zinc Co., Ltd. acquired Nyrstar's Tennessee smelter and mining assets, strengthening North American lead and critical-metals production capabilities.

- February 2026: Boliden AB reported stable smelter production, with Bergsöe lead recycling and Rönnskär operations supporting refined lead supply continuity.

- January 2026: Glencore plc confirmed 2025 operational performance and continued optimization across global metals assets supporting refined lead production activities.

- December 2025: Nyrstar NV announced agreement to sell Nyrstar USA to Korea Zinc for developing an integrated large-scale U.S. smelting complex.

- December 2025: Korea Zinc Co., Ltd. signed agreement to acquire Nyrstar USA, expanding integrated smelting capacity for zinc, lead and strategic metals.

- May 2025: Hindustan Zinc Limited commissioned additional roaster capacity at Debari Zinc Smelter, enhancing integrated metal production and operational efficiency.

ANALYST VIEW / OPINION

- Expansion of electric vehicle production will steadily increase demand for refined lead in battery manufacturing despite accelerating lithium-ion adoption.

- Secondary lead recycling capacity will become a decisive competitive advantage as sustainability regulations tighten across major industrial economies.

- Asia-Pacific will continue dominating production and consumption due to expanding automotive, industrial, and battery manufacturing ecosystems.

- Lead alloy innovation will strengthen demand from specialized industrial applications requiring improved corrosion resistance and mechanical performance.

- Stable infrastructure investments in power backup systems will sustain long-term consumption of lead ingots and lead pigs globally.

- Environmental compliance costs will encourage industry consolidation, favoring technologically advanced and vertically integrated lead producers.

- Growing investments in renewable energy storage will create additional opportunities for lead-based stationary battery applications in developing economies.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Lead Smelters & Refiners | Plant Managers, Refining Engineers, Production Heads | Analyze demand trends, secondary lead production, and refining technology developments globally |

| Battery Manufacturers | Procurement Managers, Raw Material Sourcing Teams, Supply Chain Directors | Evaluate lead ingot and lead pig supply, pricing trends, and sourcing strategies |

| Automotive OEMs | Purchasing Teams, Materials Engineers, Manufacturing Heads | Assess lead requirements for automotive batteries and component manufacturing applications |

| Battery Recycling Companies | Recycling Operations Managers, Sustainability Teams, Plant Engineers | Identify secondary lead availability, recycling capacity expansion, and circular economy opportunities |

| Cable & Wire Manufacturers | Product Development Teams, Procurement Specialists, Manufacturing Engineers | Understand lead demand for cable sheathing, specialty wires, and industrial insulation applications |

| Radiation Shielding Manufacturers | Medical Equipment Engineers, Defense Procurement Teams, Product Managers | Evaluate lead material demand for radiation protection, nuclear facilities, and healthcare infrastructure |

| Chemical & Industrial Product Manufacturers | Operations Managers, Industrial Procurement Teams, Production Engineers | Analyze lead consumption across pigments, chemicals, alloys, and industrial process applications |

| Metal Traders & Raw Material Distributors | Commodity Traders, Strategic Sourcing Teams, Market Intelligence Managers | Track regional supply-demand dynamics, pricing trends, and international lead trade flows |

| Government & Environmental Organizations | Regulatory Authorities, Mining Departments, Environmental Policy Teams | Support policy development, recycling initiatives, emissions compliance, and critical material security |

| Investors, Private Equity & Consulting Firms | Investment Analysts, Strategy Consultants, Corporate Development Teams | Evaluate market growth potential, competitive landscape, investment opportunities, and regulatory risks |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- Granular assessment of primary versus secondary lead production competitiveness across major producing countries and emerging recycling hubs.

- Comprehensive benchmarking of smelter modernization, recycling technologies, operational efficiency, and ESG performance among leading global manufacturers.

- Country-level regulatory impact analysis covering environmental legislation, battery recycling mandates, emissions compliance, and producer responsibility frameworks.

- End-to-end supply chain intelligence tracking concentrate sourcing, recycling feedstock availability, refining capacity, logistics risks, and trade dynamics.

- Detailed pricing intelligence integrating concentrate availability, recycled lead supply, energy costs, procurement trends, and regional market movements.

- Strategic investment mapping highlighting capacity expansions, technology upgrades, recycling infrastructure development, and cross-border partnership activities.

- Executive-level competitive intelligence identifying market positioning, expansion strategies, innovation pipelines, and future growth opportunities across global participants.