Jet Fuel Market Overview

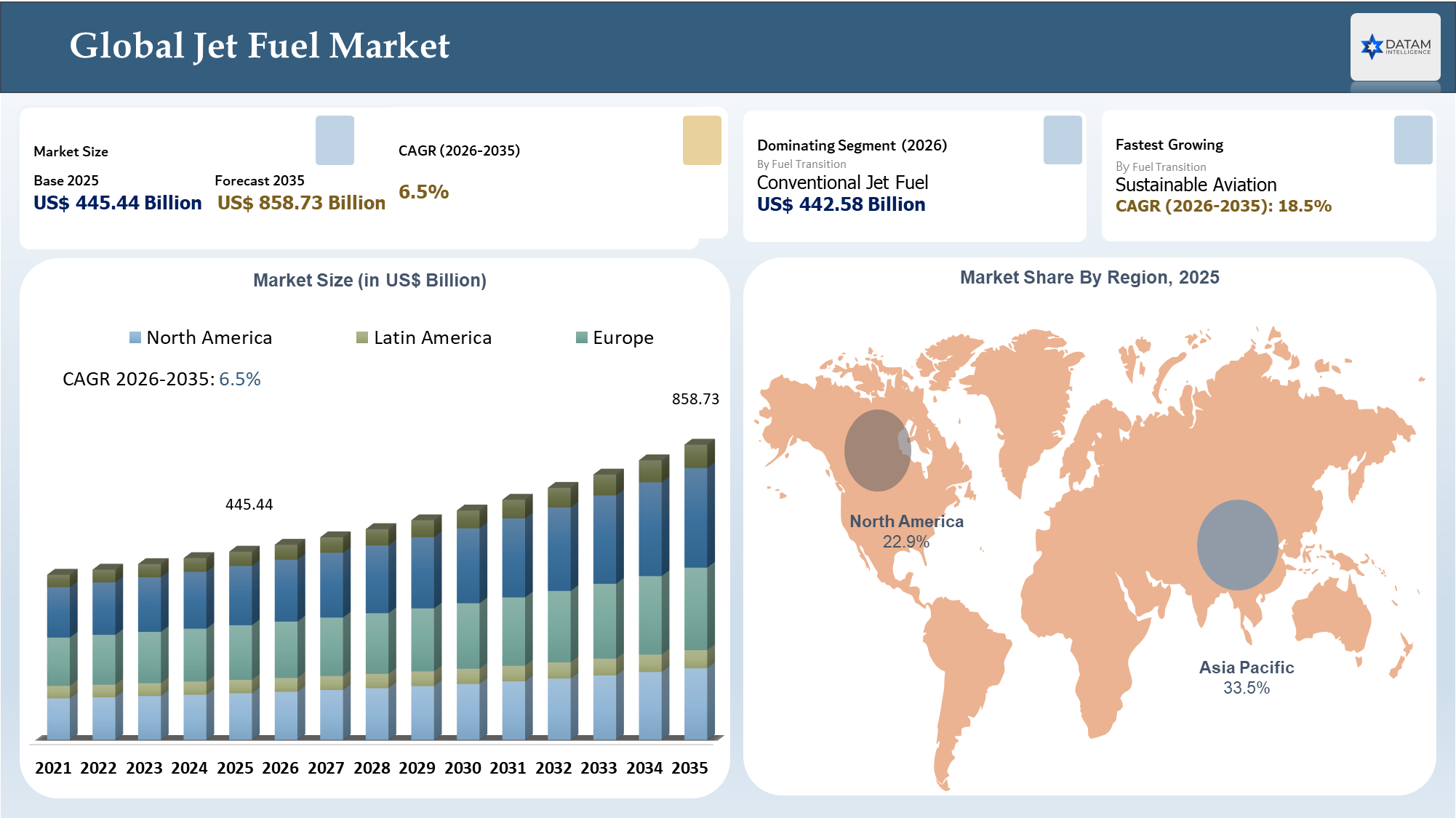

The Global Jet Fuel Market reached US$ 445.44 billion in 2025 and is expected to reach US$ 858.73 billion by 2035, growing with a CAGR 6.5% during the forecast period 2026-2035. The Jet Fuel market has entered a new period of growth and risk management that entails a strong revival in passenger air traffic volumes, efficient aircraft usage, enlarged airline fleets, higher cargo shipping services and traffic levels at busy airports. Conventional Jet Fuel is likely to remain dominant owing to the use of petroleum-based aviation turbine fuels by airliners, cargo airlines, military aviation and general aviation fleets. Meanwhile, Sustainable Aviation Fuels is expected to be the fastest growing category driven by decarbonization goals, government blends and SAFs purchase agreements.

The opportunities ahead look bright but securing supply becomes increasingly critical. The intensification of hostilities between Iran and other powers or even any disruptions in the Strait of Hormuz region would have adverse effects on crude oil transportation, refining capacity, marine insurance rates, shipping expenses and aviation fuel prices. As Jet Fuel prices are highly sensitive to crude oil and petroleum products trading patterns, any instability in the Middle Eastern region could very rapidly affect their purchasing costs.

The Iran conflict associated risks may also require buyers to evaluate their routes for procurement, concentration of suppliers and emergency fuel stocks. The import-reliant aircraft fuel market, in particular in the Asia-Pacific region, might be exposed to higher vulnerability as they depend heavily on Middle Eastern sources of crude and aircraft fuel. If this situation occurs, the airlines might hedge more extensively, make long term contracts, diversify suppliers and plan contingency fuel stock.

In terms of analysis, the aviation jet fuel should not only be treated as a commodity consumed by the aviation industry anymore. It is becoming a strategic aviation energy security market where success will depend on access to supplies, diversification of sources, hedging prices, geopolitics and storage of jet fuel.

AI Impact Analysis

AI is increasingly emerging as a strategic enabler within the Jet Fuel Market through enhancing fuel procurement practices, fuel demand forecasting, fuel price risk management and fuel supply chains. The airlines, fuel suppliers, and airport operators are deploying AI-based models that predict the fuel usage per route, passenger traffic, cargo operations, weather disruption, refinery supply, and the price of jet fuel on the region. These insights enable the procurement departments to optimize contract negotiations, fuel sourcing, fuel price hedging, and airport-based fuel allocation. AI can also be deployed in predictive maintenance for fuel facilities, refinery output maximization, stock management, and logistic scheduling via pipelines, tanker ships, storage facilities, and hydrants. In sustainable aviation fuel, AI is useful for accelerating feedstock assessment, fuel blending, emissions tracking, and supplier selection. With the growing impact of geopolitics, crude oil price risks and sustainability regulations on aviation fuel procurement, AI-fueled insights will assist market stakeholders in identifying supply shortages, evaluating fuel suppliers, reducing fuel wastage, disruption risks and costs.

Jet Fuel Industry Trends and Strategic Insights

- The jet fuel market remains highly dependent on conventional aviation turbine fuel, as commercial airlines, cargo operators, defense aviation and airport fueling systems still rely on petroleum-refined supply for large-scale operations.

- Asia-Pacific is expected to remain the strongest demand center, supported by rising passenger traffic, domestic aviation growth, low-cost carrier expansion, airport capacity additions and higher aircraft utilization.

- Iran War escalation or potential Hormuz Strait blockage could increase crude-linked fuel price volatility, disrupt refinery feedstock movement, raise freight and insurance costs, and make fuel security planning more important for airlines and airport fuel buyers.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 445.44 Billion | |

| 2035 Projected Market Size | US$ 858.73 Billion | |

| CAGR (2026-2035) | 6.5% | |

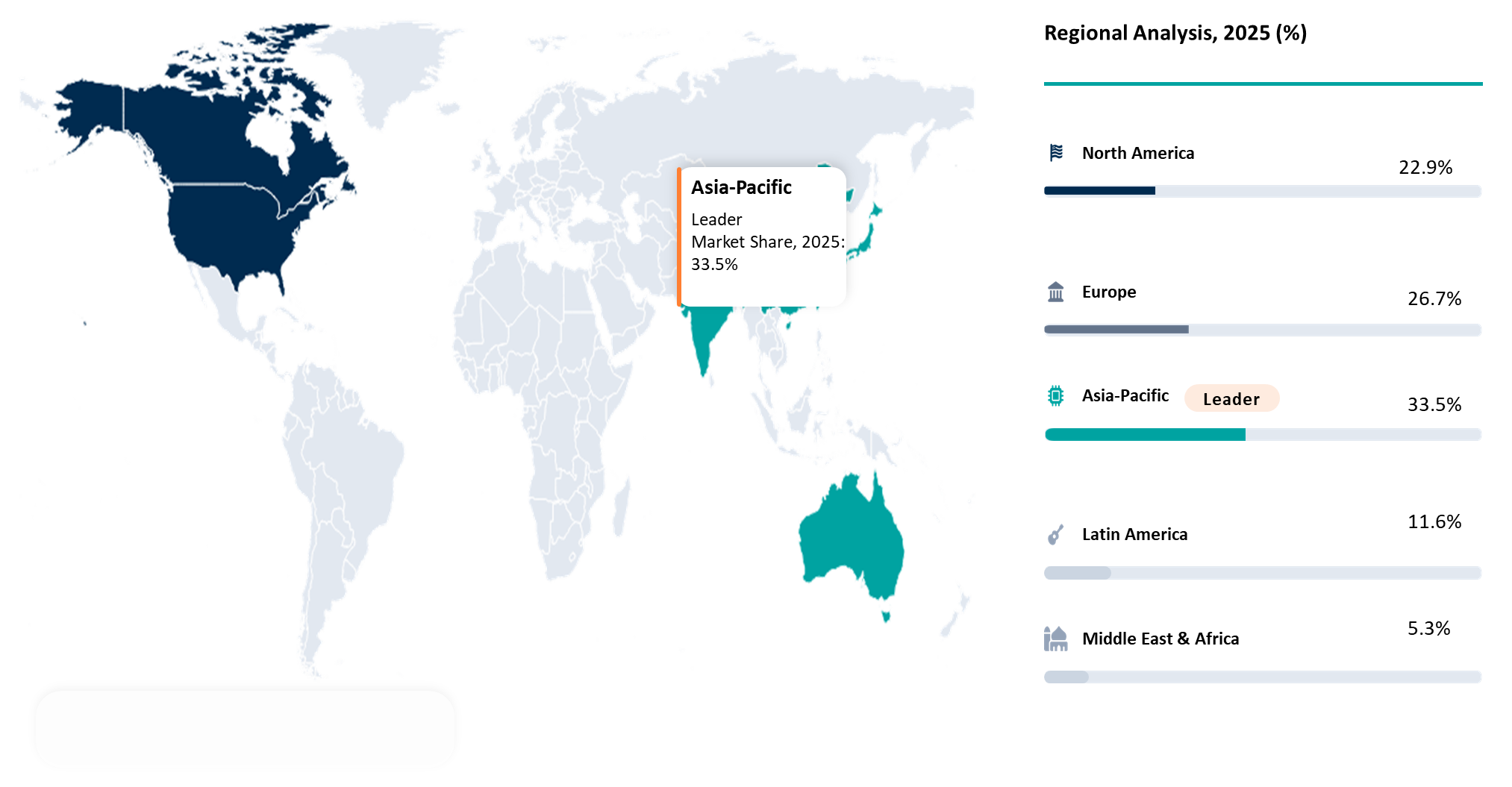

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Fuel Type | Jet A, Jet A1, Jet B and Military Grade Jet Fuel | |

| By Fuel Transition Category | Conventional Jet Fuel, Sustainable Aviation Fuel and Blended Jet Fuel | |

| By Production Source | Petroleum Refined Jet Fuel, Bio Based Jet Fuel, Waste Derived Jet Fuel, Synthetic Jet Fuel and Co Processed Jet Fuel | |

| By End User | Commercial Passenger Airlines, Cargo and Logistics Operators, Defense and Military, Business and Private Aviation, General Aviation Operators, Emergency and Medical Aviation and Others | |

| By Aircraft Type | Narrow Body Aircraft, Wide Body Aircraft, Regional Aircraft, Business Jets, Cargo Aircraft, Military Aircraft, Helicopters and Others | |

| By Pricing Model | Spot Pricing and Long Term Fixed Contracts | |

| By Procurement Model | Long Term Supply Contracts, Spot Market Procurement, Index Linked Procurement, Fuel Hedging Based Procurement, Government Tender Based Procurement and SAF Offtake Agreements | |

| By Supply Channel | Direct Refinery Supply, Integrated Oil Company Supply, Independent Aviation Fuel Traders and Resellers and Airport Fuel Service Providers | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

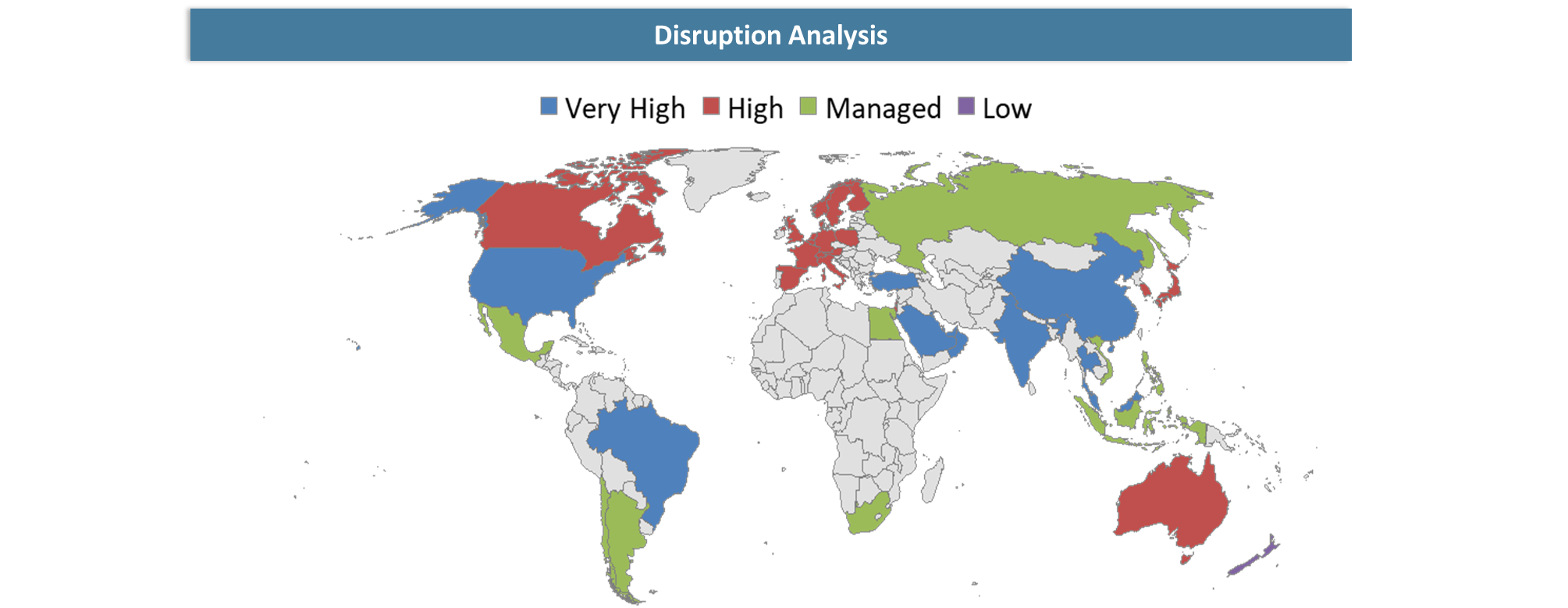

Disruption Analysis

Aviation Fuel Procurement Shifts Toward Supply Security, SAF Readiness and Price-Risk Intelligence

The Jet Fuel Market is experiencing a structural disruption, changing from an industry-driven crude oil commodity acquisition into a risk-managed supply category. Volatility in crude oil markets, SAF regulations, Middle Eastern conflict, refinery output limits, airport capacity issues, and aviation decarbonization plans are directly influencing jet fuel acquisition, pricing, contracts, and inventories.

Sustainable aviation fuel is the most potent disruption driver. There is significant pressure for airlines to source low-carbon fuel certified by regulators. However, SAF supply is constrained, high in cost, and contingent upon feedstock availability, technological process efficiency, and fuel blending infrastructure. This results in a struggle for SAF offtake contracts, leading suppliers to develop sustainable fuels via biological and waste materials, co-processing, and synthesis pathways.

Disruption through geopolitical developments is also relevant. Any further tension with Iran or obstruction at the Hormuz Straits will lead to higher crude oil costs, freight rates, insurance costs, and airport supply disruptions. This will lead to a greater emphasis on supplier diversification, fuel hedging, import risk assessments, fuel storage arrangements, and logistics systems by airlines, cargo services, and airport fuel suppliers. Winners in the market will be those with secure fuel supplies, SAF capability, price risk intelligence, and airport fueling capabilities.

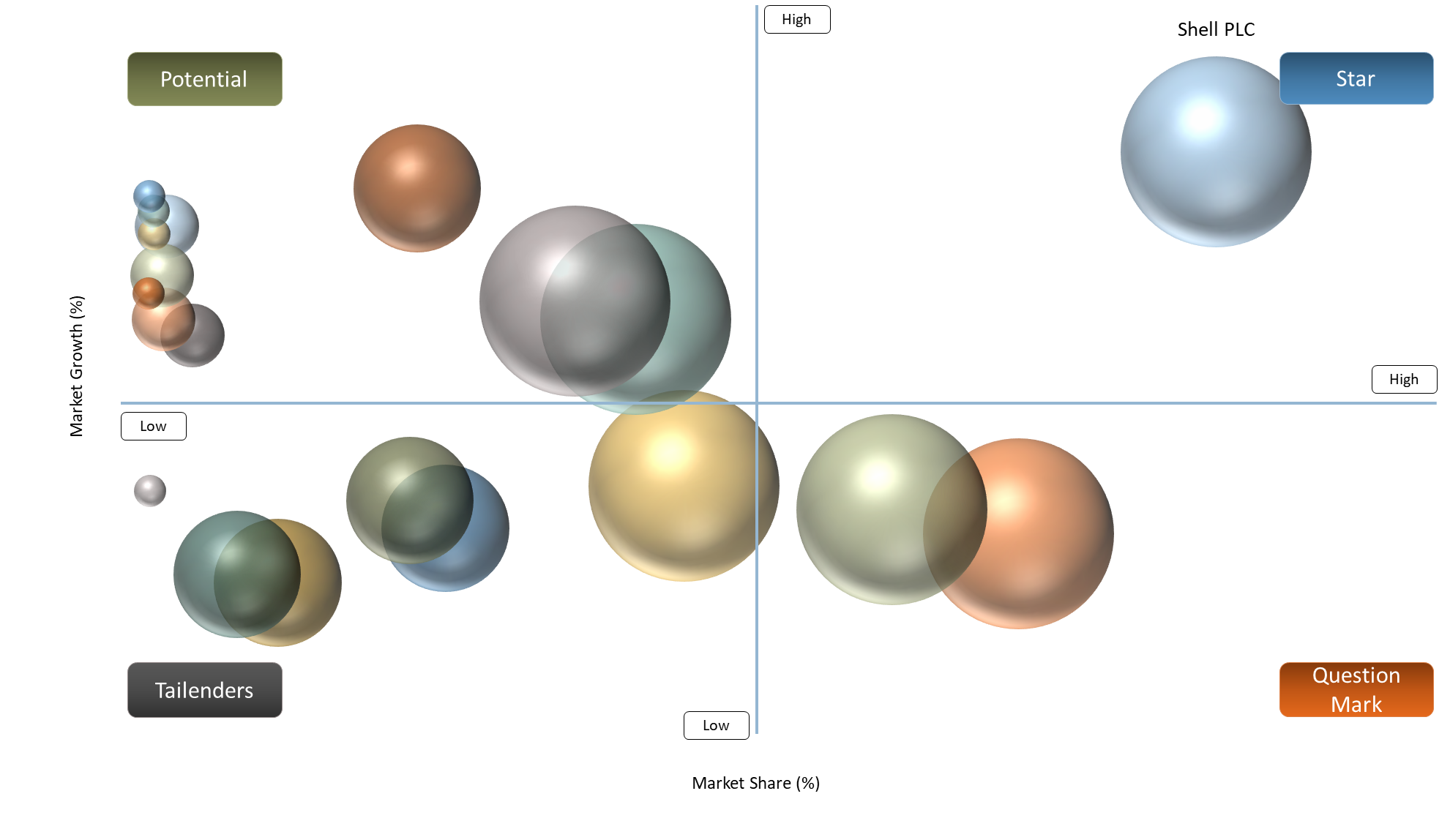

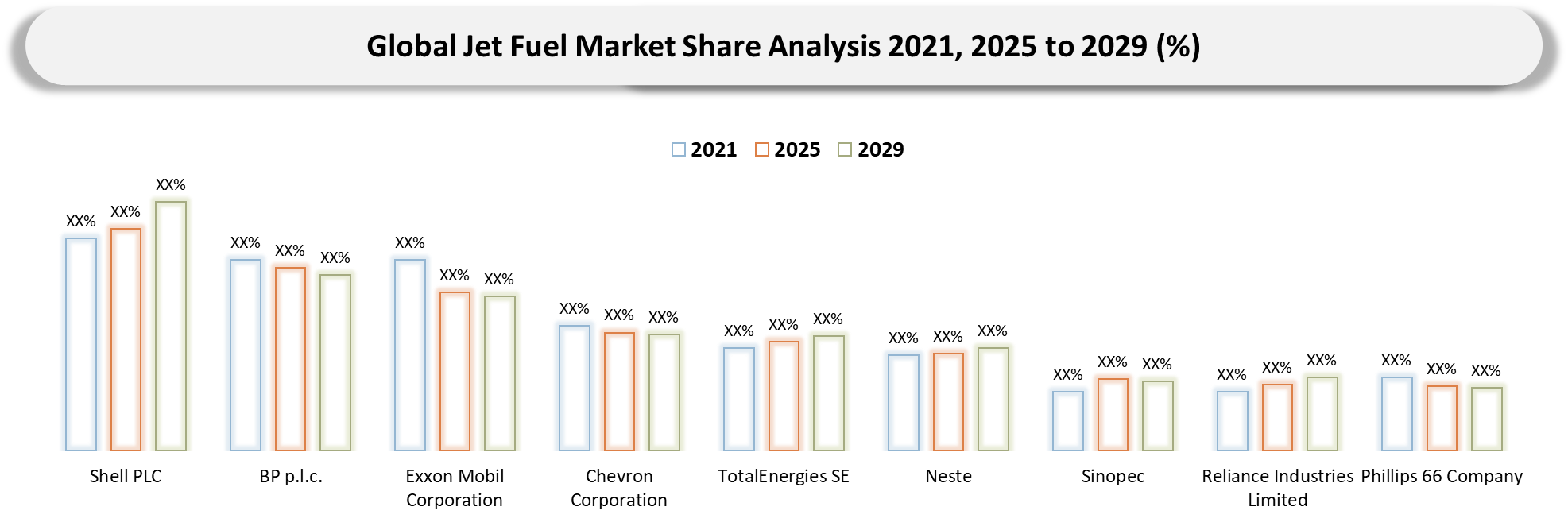

BCG Matrix: Company Evaluation

BCG Matrix Analysis of Jet Fuel Market is based on criteria like strength of the market, ability of fuel supply to airlines, refinery integration, safety fuel readiness, availability of airports, power to price and growth. Currently, the market is witnessing shift towards strategy of fuel supply beyond conventional jet fuel towards a fuel eco system due to fluctuations in crude prices, SAFs, regional fuel supplies, and purchase agreements from airlines.

Companies like Shell PLC, BP p.l.c., Exxon Mobil Corporation, Chevron Corporation, and TotalEnergies SE are positioned as Strategic Leaders due to their global aviation fuel distribution networks, refineries integration, financial power, customer relationship with airlines, and growing portfolio of SAFs. These firms benefit from providing both conventional jet fuel along with aviation fuel decarbonization.

Companies such as Neste, Eni S.p.A., Repsol, and OMV Aktiengesellschaft are seen as Growth Accelerators due to their renewable fuel expertise, SAFs, refining transformation and low carbon aviation fuels positions.Phillips 66 Company, Valero Marketing and Supply Company, and Marathon Petroleum Corporation are classified as Regional Value Anchors because of their strong refining capabilities, provision of jet fuel, infrastructure connectivity, and efficient production process.

Kuwait Petroleum International Limited, Sinopec, and Reliance Industries Limited have been classified under Market Access Specialists because of their strong refining capabilities that are linked with exports, potential to export, and strong access to fuel markets in the Middle East and Asia-Pacific regions..

Market Dynamics

Jet fuel cost exposure becoming a board-level procurement priority for airlines, cargo operators and airport fuel buyers

Fuel expense management is now emerging as a strategic issue on the boardroom agenda because jet fuel continues to be one of the most unpredictable cost areas for airlines and cargo operators. As per IATA estimates, in 2025, the average jet fuel cost is forecasted at US$86 per barrel which will amount to a total global airline fuel bill of US$236 billion, comprising 25.8% of total airline operational costs. For aviation industry stakeholders, the cost of fuel impacts route profitability, pricing strategies, Aircraft utilization, fuel hedging plans, and bottom line margins. It is for this reason that airlines, cargo operators, and airport-based fuel procurers have started to consider fuel procurement practices such as contractual arrangements, indexing systems, diversified supply chain networks, airport inventory monitoring, and benchmarking processes. The strategic relevance of fuel providers which offer guaranteed fuel availability, pricing options, airport connectivity, fuel hedging opportunities, and robustness against crude price fluctuations, refinery capacity shortages, and political instability will increase.

Limited certified SAF supply across major aviation hubs restricting large-scale blending and procurement commitments

Certified SAF availability is still a significant constraint within the Jet Fuel Market because the decarbonization efforts of the airlines continue to outpace production capacity and blending capabilities at the airport level. According to IATA, there will be an estimated production capacity of 2 million tonnes in 2025, which is less than 0.7% of the fuel that the airlines consume, and the volume is still projected to cost US$4.4 billion more globally. This is due to the inability to blend SAF on a large scale and the lack of long-term procurement capabilities within airports and airlines, such as cargo companies and business travel programs. Not only do airlines have to produce enough SAF, but they also need to get approved pathways, source feedstocks, have terminal blending capabilities, distribute it through the airport network, and have secure supply agreements.

Segment Analysis

The Global Jet Fuel Market is segmented based on the fuel type, fuel transition category, production source, end user, Aircraft type, pricing model, procurement model, supply channel, and region/countries.

Conventional Jet Fuel Remains the Revenue Backbone as SAF Scale-Up Lags Behind Aviation Demand

Conventional jet fuel has remained the commercial leader in the jet fuel industry due to the dependence of air travel on petroleum-based jet kerosene supplied by existing refining capacity, fuel storage facilities at airports, hydrants, into-plane fueling systems, and long-term supplier agreements. This is evidenced by the relatively slow adoption of alternative jet fuels. According to IATA, the production of Sustainable Aviation Fuels stood at 1 million tons or 1.3 billion liters in 2024, equivalent to just 0.3% of the total production of jet fuel, while production in 2025 is projected to hit 2.1 million tons or 2.7 billion liters, accounting for merely 0.7% of total jet fuel production.

Therefore, revenue generation, price risk and procurement risks associated with the jet fuel business continue to revolve around conventional jet fuel. IEA further points out that fuel demand in aviation is currently led by jet kerosene, while the usage of SAF forms less than 0.1% of the aviation fuels consumed. On the other hand, in the United States, scheduled airlines had consumed about 1.594 billion gallons of fuel by December 2024, 2.7% more than December 2019 consumption levels.

From a consulting perspective, conventional jet fuel is the most important segment to analyze because it captures the current demand pool, airline operating cost sensitivity, refinery dependency, regional supply security, crude-linked price volatility and contract structure. SAF will shape future transition strategy, but conventional jet fuel will continue to define the market’s near-term revenue base, pricing benchmarks and supply chain risk.

Geographical Penetration

North America Jet Fuel market

North America is among the most commercially significant regions in the market for jet fuel, given the substantial presence of the U.S., its airline network, Aircraft usage intensity, and domestic air connectivity. According to IATA, the region accounted for 22.9% of global passenger traffic in 2024, thus becoming the third largest aviation region in the world after Asia-Pacific and Europe. Additionally, in 2024 North American airlines registered an annual 6.8% increase in their traffic volumes.

Jet fuel demand is driven by the needs of the U.S. airlines. According to the report issued by the U.S. Bureau of Transportation Statistics, in December 2024 scheduled U.S. airlines consumed 1.594 billion gallons of fuel, which exceeded December 2019 levels by 2.7%. In addition, in December 2024, the average price of jet fuel in the U.S. equaled $2.32 per gallon, increasing 16.0% compared to December 2019. The region's refinery capacity is another asset for the jet fuel business, as in 2024 the U.S. reached a record level of jet fuel production in its refineries.

Further, geopolitics and war bring another dimension of strategy to the jet fuel market in North America. For instance, conflicts between Russia and Ukraine, as well as Middle Eastern regions and the Hormuz situation could lead to increased prices for crude oil, interruption in the movement of refined products, and larger crack spreads for jet fuels. As IATA states, it is noteworthy that conflict in the Middle East revealed weaknesses of the jet fuel supply chain since normally about 20% of oil movements pass through the Strait of Hormuz. Thus, for North American airlines, fuel management and planning will involve hedging, supplier diversity, refinery access, storage strategies, and flexibility. Regarding consultations in such matters, North America is to be considered both an established market of jet fuel and a region affected by war-related price fluctuations.

U.S. Jet Fuel Market Trends

United States constitutes the main driver for jet fuel demand in North America, thanks to its well-developed aviation network domestically, high Aircraft utilization rates, significant cargo aviation activities, and the presence of some of the biggest hubs like Atlanta, Dallas-Fort Worth, Denver, Chicago O’Hare, Los Angeles, and New York. In December 2024, fuel consumption by scheduled U.S. air carriers reached 1.594 billion gallons, up 2.7% from December 2019, thus confirming the recovery of aviation fuel consumption above pre-COVID levels during critical time intervals. Fuel price changes directly affect airline performance margins, with BTS stating the average cost of airline fuel at US$2.32 per gallon, up 16% from December 2019.

There is also significant strength in the robustness of domestic refining capabilities in the US. According to EIA, jet fuel accounted for a record share of US refinery production in 2024, owing to better demand from the aviation sector than other modes of transportation. War and geopolitical tensions present another significant source of risk, especially concerning the potential for disruptions in the Middle East and the resulting price hikes in Russia-Ukraine energy-related conflicts. According to IATA, the Strait of Hormuz transports about 20% of the global oil supplies, so any disruptions due to conflicts would directly impact the fuel supply chain.

As a consulting overview, the US should be regarded as a mature yet highly exposed market for jet fuel, where robust demand, refinery economics, airline hedging policies, storage strategies, supplier diversification, and SAF conversion are key aspects.

Asia-Pacific Leads Jet Fuel Demand but Faces Rising Exposure to Iran War and Hormuz Strait Supply Risks

Asia-Pacific is the key region in the jet fuel market due to its biggest aviation passenger base and the demand from China, India, Japan, South Korea, Indonesia and Southeast Asian nations. Based on the figures released by the IATA in 2024, 33.5% of the world's passenger traffic share belongs to Asia-Pacific measured using RPKs, hence the region is the biggest aviation market in the world. IATA further revealed that the increase in the world RPKs by 10.4% in 2024 was due to Asia-Pacific airlines, indicating that there is growth in fuel demand in the region.

The biggest regional market in jet fuel will continue to be Asia-Pacific since it is directly connected to flights, Aircraft passenger loads, new routes and use of Aircraft fleet. In 2024, ACI World reported that the total global air passenger traffic was 9.5 billion passengers, with 57% coming from domestic air passenger traffic, which indicates strong growth prospects for the Asia-Pacific region where domestic aviation market is structurally bigger in China, India and Indonesia. Asia-Pacific therefore needs to be targeted as the key market due to passenger volume, low-cost carriers, airports, middle-class air travelers and fuel price risk.

The energy risks associated with conflict situations make it increasingly important to consider jet fuel planning strategies in the Asia-Pacific region. The Strait of Hormuz is one of the crucial oil shipping routes; the EIA has indicated that the average flow of oil via the Strait was 20 million barrels per day during 2024, equivalent to approximately 20% of global petroleum liquids consumption. Similarly, the IEA has indicated that roughly 20 million barrels per day, or 25% of worldwide sea oil shipments, pass through the Strait, with about 80% bound for the Asian region. Any escalation of an Iran conflict situation or the closure of the Strait would lead to increased jet fuel costs based on crude oil prices, disruptions in the flow of refinery feedstocks, higher shipping and insurance costs, and pressures on air carrier purchasing agreements in countries such as China, India, Japan, South Korea, and Southeast Asia.

Japan Jet Fuel Market Trends

Japan represents a vital market for jet fuel in Asia-Pacific, driven by the recovery of international air traffic, the country's dense network of air connectivity, and high consumption of jet fuel from various airports, including Tokyo Haneda, Narita, Kansai, Chubu, and Fukuoka airports. The aviation recovery in Japan depends on inbound tourism, where the country experienced a record number of 36.87 million international tourists in 2024, leading to increased flight frequencies, airport fueling activities, and higher airline capacity utilization.

Fuel planning in Japan still remains relevant since jet fuel demand is resilient amidst anticipated contraction in oil products demand. According to METI, Japan's domestic jet fuel consumption will grow to 27 million barrels in FY2029-30 compared to FY2024-25 but lower than its FY2022-23 levels, amid an expected drop of 11% in total oil product consumption. The shift towards SAFs in Japan makes the country more attractive for the jet fuel industry, with the Japanese government aiming at replacing conventional jet fuel with SAF by 10%. According to USDA FAS, Japanese airports will need 2.5-5.6 billion liters of SAF within total jet fuel consumption of 10.9-12.3 billion liters by 2030.

Risk due to energy security associated with wars brings another dimension to the jet fuel market in Japan. According to EIA, oil shipments via the Strait of Hormuz averaged 20 million barrels per day in 2024, representing approximately 20% of worldwide petroleum liquids consumption. Japan is at particular risk as per IEA as both Japan and Korea are heavily dependent on oil shipments through Hormuz, and much of the Hormuz crude exports go to Asia. This way, any further escalation of war in Iran or blocking of oil transit in Hormuz will result in increased costs of crude oil, leading to higher costs of ATF, shortage in availability of refinery feedstocks, rising shipping charges, higher cost of insurance and procurement issues for Japanese airlines and airport jet fuel suppliers. For consultant analysis purposes, it would be wise for Japan to project itself as a high-value and import-dependent market for jet fuel.

Import Analysis

Iran War and Hormuz Strait Risk Exposure in the Jet Fuel Market

Iran War escalation or a potential Hormuz Strait blockage would turn jet fuel importing into a critical aviation energy security issue. Import-dependent countries would face higher exposure to crude oil disruption, refinery feedstock pressure, tanker rerouting, freight escalation, insurance premium increases and aviation fuel price volatility. For jet fuel buyers, the risk is not only higher prices, but also uncertainty in fuel availability across major airport hubs.

From an import-risk perspective, China, India, Japan, Korea, Republic of and Singapore are the most strategically exposed Asian markets because they combine large aviation demand with strong dependence on imported crude oil or refined petroleum product flows. Based on the import analysis for 2024, these five economies together recorded imports of around US$ 5,123.05 billion. Within this group, China accounted for 50.5%, followed by Japan at 14.5%, India at 13.7%, Korea, Republic of at 12.3%, and Singapore at 8.9%.

For the jet fuel market, this concentration shows that any Middle East disruption can create stronger procurement pressure across Asia’s largest aviation and refining-linked economies. Airlines, airports and fuel distributors in these markets need stronger fuel security planning, including alternative sourcing, long-term supply contracts, emergency reserves, supplier diversification, hedging strategies and real-time geopolitical monitoring.

Competitive Landscape

- The jet fuel market structure will be determined by international integrated energy companies, state-owned oil companies, renewable fuel specialists and large refinery-based jet fuel suppliers competing for supply reliability, refinery strength, presence at airports, trading capacity, flexible pricing and low carbon fuel availability. The competitive position of Shell PLC, BP p.l.c., Exxon Mobil Corporation, Chevron Corporation and TotalEnergies SE is based on their significant refining operations, extensive global aviation fuel supply chain, fueling services at airports and longstanding airline partnerships. The company's unique competitive position in the transitional category lies in its competitive advantage in sustainable aviation fuel and renewable fuel manufacturing.

- Competitive advantages of Sinopec, Reliance Industries Limited and Kuwait Petroleum International Limited are due to their regional refinery strength and access to supply sources. Highly relevant companies operating in the refinery-based jet fuel category include Phillips 66 Company, Valero Marketing and Supply Company and Marathon Petroleum Corporation, which have particular relevance to mature aviation sectors. Eni S.p.A., Repsol and OMV Aktiengesellschaft are increasing their competitive strength via investments in cleaner fuel and aviation fuel supply in Europe..

Key Developments

- May 2023: Eni S.p.A. supplied sustainable aviation fuel for Kenya Airways’ Nairobi–Amsterdam flight, marking one of the first long-haul SAF uses from Africa and strengthening SAF visibility in the jet fuel supply chain.

- June 2024: Neste supplied SAF blended with conventional jet fuel to Singapore Airlines Group through Changi Airport’s fuel hydrant system, supporting SAF integration into existing airport jet fuel infrastructure.

- July 2024: Repsol signed an agreement with IAG for the purchase and supply of more than 28,000 tonnes of SAF, described as Spain’s largest SAF purchase agreement to date.

- September 2024: TotalEnergies SE expanded its SAF offtake agreement with Air France-KLM to supply up to 1.5 million tons of SAF over a 10-year period, strengthening long-term low-carbon jet fuel procurement.

- November 2024: OMV Aktiengesellschaft subsidiary OMV Petrom signed a SAF supply contract with TAROM, marking the first sustainable aviation fuel supply agreement for Romanian aviation.

- March 2025: The U.S. Energy Information Administration reported that U.S. refineries produced a record-high share of jet fuel in 2024, reflecting stronger aviation fuel demand compared with other transport fuels.

- October 2025: Shell PLC’s Avelia platform expanded with Moeve as the first external SAF supplier; by June 2025, Avelia had enabled more than 41 million gallons of SAF injection across 17 airport locations.

- April 2026: The UK Department for Transport published its SAF Task and Finish Group report, reiterating the mandate pathway from 2% of jet fuel demand in 2025 to 10% in 2030 and 22% in 2040, reinforcing policy-led demand for low-carbon jet fuel.

Major Pain Points

- High Exposure to Crude Oil Price Volatility: Jet fuel prices remain closely linked to crude oil movements, making airline operating costs highly unstable. Sudden price increases directly affect airline margins, ticket pricing, route profitability and fuel procurement budgets.

- Iran War and Hormuz Strait Disruption Risk: Any escalation around Iran or potential blockage of the Strait of Hormuz can disrupt crude movement, refinery feedstock availability, tanker insurance, freight rates and jet fuel supply security, especially for Asia-Pacific and import-dependent markets.

- Limited SAF Availability and High Cost Premium: Airlines are under pressure to reduce emissions, but SAF supply remains limited and significantly more expensive than conventional jet fuel. This creates a gap between sustainability commitments, regulatory mandates and actual fuel procurement feasibility.

- Refinery and Airport Fuel Infrastructure Dependency: Jet fuel availability depends heavily on refinery output, storage terminals, pipelines, hydrant systems and airport fueling infrastructure. Any bottleneck in refining, logistics or airport storage can create supply shortages and operational delays.

- Procurement Complexity and Contract Risk: Airlines, cargo operators and airport fuel buyers must balance spot purchases, long-term contracts, index-linked pricing, hedging, supplier diversification and emergency reserves. Poor contract structuring can expose buyers to higher costs, supply gaps and weak negotiation power.

White Space Opportunities

One white space that exists in the jet fuel industry pertains to the war-related issues related to fuel supply security and threat of disruption of the Hormuz Strait. Any event related to the Iran issue or any disruption in the Strait of Hormuz can have an impact on crude oil supplies, refinery feedstock logistics, freight insurance, freight rates, jet fuel procurement, and pricing.

For the airline industry, airports, and aviation fuel service providers, there are several white spaces that arise out of the need for effective fuel risk management. These may include multiple supplier agreements, diversification in the procurement of jet fuel, stockpiling of jet fuel during emergencies, alternate shipment routes, flexible pricing agreements, hedging services, risk rating of suppliers, and geopolitical fuel assessment.

In essence, the white space exists in positioning the jet fuel as a strategic product within the aviation energy security context.

DMI Opinion

According to DataM, Jet Fuel growth will not only depend on growing aviation traffic, but also on the ability of providers to ensure safety, reliability, price security, and disruption readiness in fuel supply. More and more airlines, airports, cargo carriers, and defense aviation organizations are changing their approach to aviation fuel purchase by moving from simple fuel procurement to fuel planning, which is focused on such factors as availability, access to refineries, storage, contract flexibility, SAF preparedness, and geopolitical risks.

Iran War threat and possibility of Hormuz Strait closure is an essential element of risk for the market. Any kind of disruption related to this critical location might have an impact on the following: crude oil flows, availability of refinery feedstocks, increased cost of tanker insurance, higher freight costs, price increase, and profitability. For fuel consumers, it becomes crucially important to diversify fuel sources, conclude long-term agreements, create emergency fuel reserves, find hedging partners, and develop alternative sourcing routes.

Therefore, it is obvious that the Jet Fuel market is no longer purely a volume-oriented aviation fuel market. It becomes an aviation energy security market.

Why Choose DataM?

- Jet Fuel Supply and Aviation Fuel Intelligence: Deals with Jet A, Jet A1, military jet fuel, standard jet fuel, SAF, blended jet fuel, jet fuel supply related to refinery, aviation fuel infrastructure at airports, hydrant system, storage facilities, aviation fuel procurement strategies and pricing.

- Positioning of Jet Fuel Supplier and Refinery: Positions key players on the basis of their refinery position, aviation fuel supply ability, access to airports, trading network, airline contracts, storage facilities, logistics facility, SAF readiness and blending ability.

- Risk Analysis for Iran War and Hormuz Strait Blocking Effect on Crude Oil Price and Airline Procurement Security: Analyzes the effect of Iran War escalation and Hormuz Strait blocking on crude oil transport, refinery feedstock, tanker insurance, shipping costs, jet fuel prices and procurement safety for airlines.

- SAF Transition & Compliance Monitoring: Monitors SAF mandates, airline carbon reduction goals, SAF purchase agreements, blending needs, life cycle emissions criteria, certification processes, government subsidies and SAF infrastructure at airports.

- Trends in Jet Fuel Markets: Assesses traffic recovery in aviation, Aircraft usage, airport capacity additions, cargo aviation demand, low-cost airlines, fuel hedging policies, fuel supply agreements and strategic fuel sourcing in aviation, focusing particularly on Asia since the IEA says that most Hormuz crude is shipped to.

Who should buy this report?

- Airlines and Cargo Operators: To assess jet fuel pricing, long-term fuel procurement, supplier diversification, SAF adoption, fuel hedging and Iran War or Hormuz Strait disruption risks.

- Airport Operators and Fueling Service Providers: To understand jet fuel storage needs, hydrant infrastructure, refueling demand, SAF blending readiness, emergency fuel reserves and airport-level supply continuity planning.

- Oil Majors, Refiners and Fuel Suppliers: To evaluate demand outlook, airline procurement behavior, airport supply opportunities, regional fuel demand, SAF transition and competitive positioning.

- Aviation Fuel Traders and Distributors: To identify trading opportunities, supply gaps, pricing volatility, refinery-linked fuel flows, alternate sourcing routes and geopolitical risk exposure.

- SAF Producers and Renewable Fuel Companies: To understand SAF demand potential, blending mandates, airline offtake opportunities, airport readiness, certification requirements and market entry opportunities.

- Government, Defense and Aviation Regulators: To assess fuel security, strategic reserves, military aviation fuel demand, SAF policy design, import dependency and energy security risks.

- Investors, Private Equity and Infrastructure Funds: To evaluate opportunities in airport fuel infrastructure, storage terminals, SAF production, aviation fuel logistics, refinery assets and energy transition investments.

- Consulting, Strategy and Procurement Teams: To support market entry, sourcing strategy, supplier benchmarking, contract planning, price-risk analysis, decarbonization strategy and aviation energy security decisions.