Japan Plasma-Derived Therapeutics Market Overview

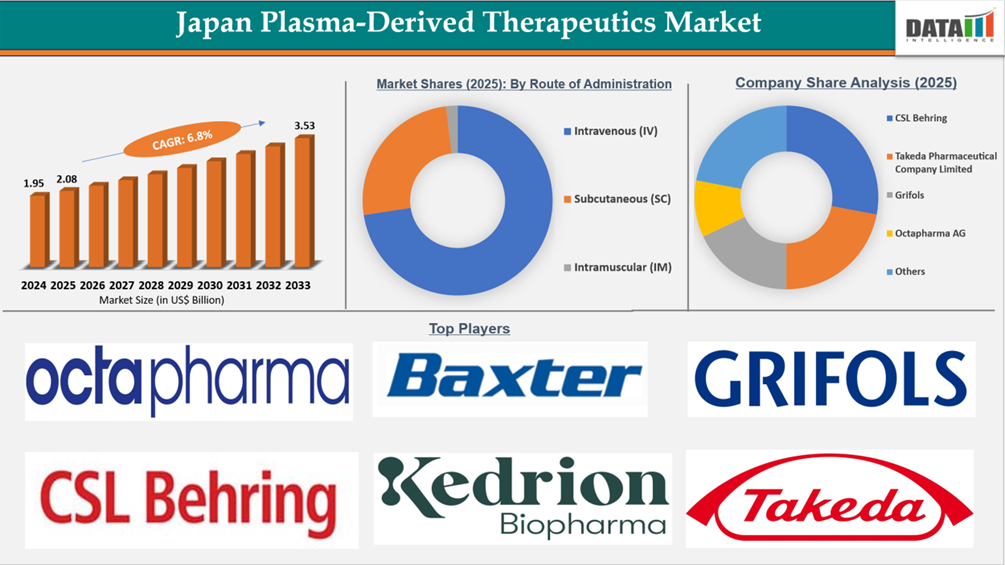

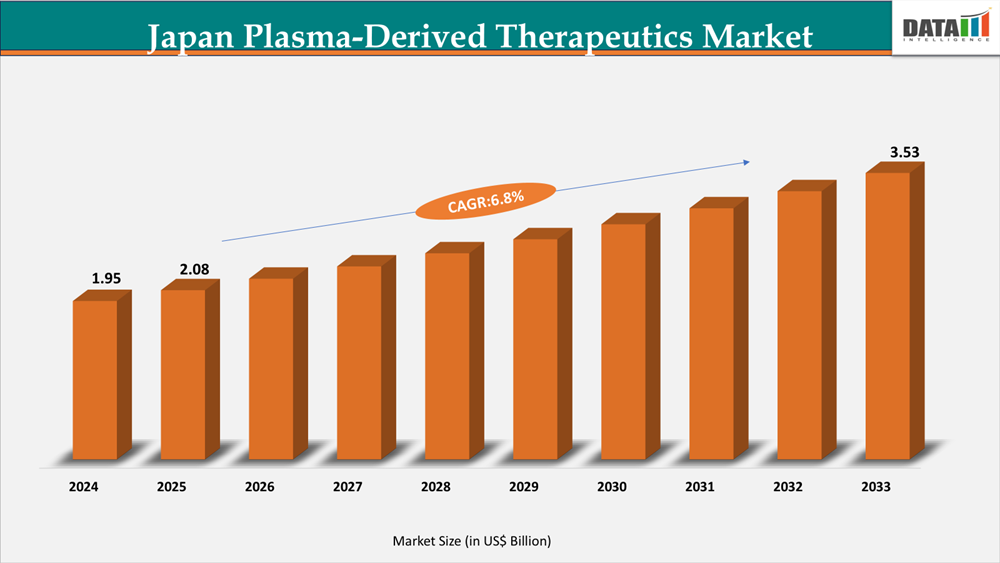

The Japan Plasma-Derived Therapeutics Market reached US$1.95 Billion in 2024, rising to US$2.08 Billion in 2025 and is expected to reach US$3.53 Billion by 2033, growing at a CAGR of 6.8% from 2026 to 2033.

The Japan Plasma-Derived Therapeutics Market, which provides plasma-derived therapies (IVIg, albumin, and coagulation factors), is growing steadily due to increased demand from hospitals caused by an aging population, as well as an ongoing reliance on these products in treating patients with immunology, hematology, neurology, oncological, and critical care conditions. Plasma products are generally administered to patients in hospital settings in Japan (over 8,000 hospitals) and supported by Japan's universal health insurance coverage (more than 125 million people). The demand for supportive plasma therapies is strong in Japan because there are over 16 million yearly hospital admissions and over 1 million new cancer diagnoses each year. Further contributing to this strong ongoing demand for supportive plasma therapies, approximately 29% of Japan's population is 65 years of age or older. This demographic trend also contributes to high rates of chronic liver disease, autoimmune disorders, neurological diseases, as well as hematologic diseases (i.e., hemophilia) affecting an estimated 5,000–6,000 patients requiring indefinite factor replacement therapy. The immunoglobulin segment is the fastest growing and largest segment of the plasma-derived therapeutics market due to the rise in neurological and immune-related disease indications.

On the supply side, Japan keeps up a controlled voluntary plasma collection system that collects about 5 million liters a year. It is backed by a well-established domestic fractionation and manufacturing infrastructure that is closely monitored by the Ministry of Health, Labour and Welfare (MHLW) to guarantee quality compliance, traceability, and viral safety. Because of their biological complexity, high manufacturing barriers, and clinical necessity in treating immune deficiencies, bleeding disorders, and critical care conditions, plasma-derived therapies face limited substitution risk, even though periodic drug price revisions are implemented to control national healthcare expenditure under the reimbursement framework. This puts the market in a position for stable, necessity-driven growth at the long term.

Plasma-Derived Therapeutics Industry Trends and Strategic Insights

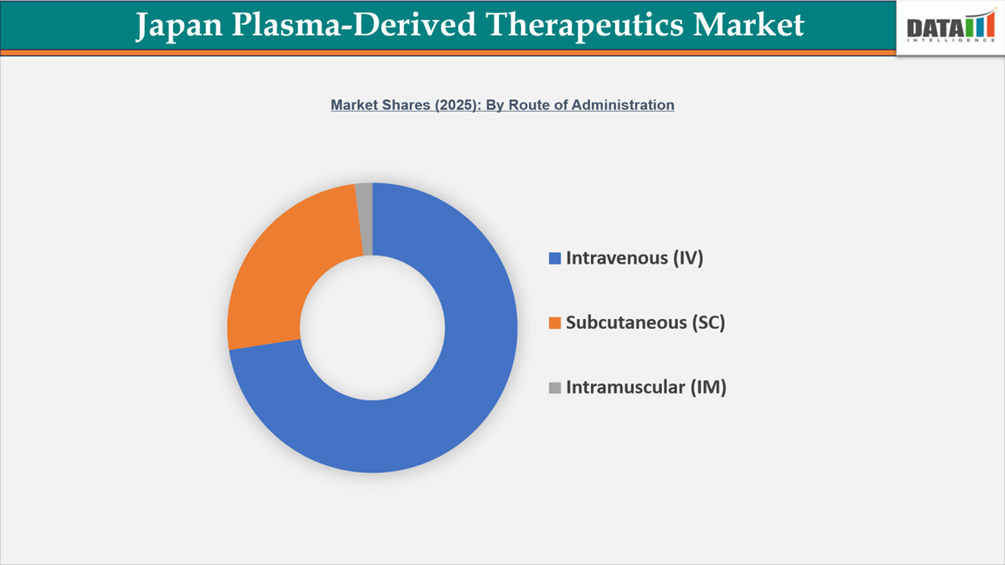

- By Route of Administration segment, Intravenous (IV) led the Japan Plasma-Derived Therapeutics Market, capturing the largest revenue share of 74% in 2025.

Japan Plasma-Derived Therapeutics Market Size and Future Outlook

- 2025 Market Size: US$2.08 Billion

- 2033 Projected Market Size: US$3.53Billion

- CAGR (2026–2033): 6.8%

Japan Plasma-Derived Therapeutics Market Dynamics

Technological Advancements in Plasma Fractionation

Plasma fractionation technology developments are a major driver of growth in the Japan Plasma-Derived Therapeutics Market. Improvements in purification processes, chromatography systems, and viral inactivation technologies have improved product safety, yield efficiency, and consistency. These advancements allow producers to extract more immunoglobulins, albumin, and coagulation factors from each unit of plasma, increasing overall manufacturing capacity.

Advanced fractionation methods also lower the danger of pathogen transmission and ensure compliance with Japan's demanding regulatory norms, boosting physician confidence and promoting wider clinical adoption. Higher recovery efficiency promotes domestic plasma self-sufficiency and improves supply stability. As manufacturing methods become more complex and cost-effective, technical advancements improve product availability and drive long-term market growth.

Strict Regulatory Requirements in Japan

Strict regulatory regulations in Japan impose major constraints on the plasma-derived therapies sector. The Pharmaceuticals and Medical Devices Agency (PMDA), which is overseen by the Ministry of Health, Labour, and Welfare (MHLW), strictly regulates the market and imposes strict approval, quality, and safety criteria. Before being approved, plasma products must go through comprehensive clinical examination, tight donor screening, traceability verification, and advanced viral inactivation validation. Furthermore, producers must meet stringent Good Manufacturing Practice (GMP) standards as well as continuous pharmacovigilance obligations. Pricing is also vulnerable to government-controlled reimbursement adjustments, which reduce company margins. While these procedures protect patient safety and product quality, they raise compliance costs, slow clearance timeframes, and impede rapid market entrance and expansion.

Segmentation Analysis

The Japan Plasma-Derived Therapeutics Market is segmented based on product type, application, end user, source of plasma, and route of administration.

Intravenous (IV) Route Remains the Backbone of Japan Plasma-Derived Therapeutics Market

The Japan Plasma-Derived Therapeutics Market is primarily based on the intravenous (IV) route of administration. IV administration plays an important part in the treatment of immune disorders, neurological disorders, and bleeding disorders. Intravenous immunoglobulin (IVIg) is an important treatment option used to treat individuals with primary and secondary immunodeficiency, chronic inflammatory demyelinating polyneuropathy (CIDP), Guillain–Barré syndrome, and many autoimmune diseases. Japan has approximately 15,000–17,000 new cases of Kawasaki disease per year, which supports ongoing demand for hospital-based infusion services due to IVIg being the first line of treatment.

In addition to IVIg, there is another category of plasma-derived products that will utilize the IV route of administration. These products are plasma-derived coagulation factors; for example, Factor VIII, Factor IX, fibrinogen concentrates, and prothrombin complex concentrates. These medications are utilized by health care providers to provide fast systemic availability and correct dose adjustment following IV administration. Hemophilia patients are examples of those who will require the use of intravenous plasma-derived coagulation factors by a health care provider for both acute care and presurgical treatment. Because Japan has an older patient population—almost 29% of the population is 65 years or older—this will only contribute to the rising number of patients with immune disorders and hematologic disorders who require biologic treatment. Japan has a solid hospital infrastructure and implementation of specialist-directed infusion protocols, thus allowing the continued use of IV as the primary route for the administration of plasma-derived therapeutics throughout Japan.

Japan Plasma-Derived Therapeutics Market Competitive Landscape

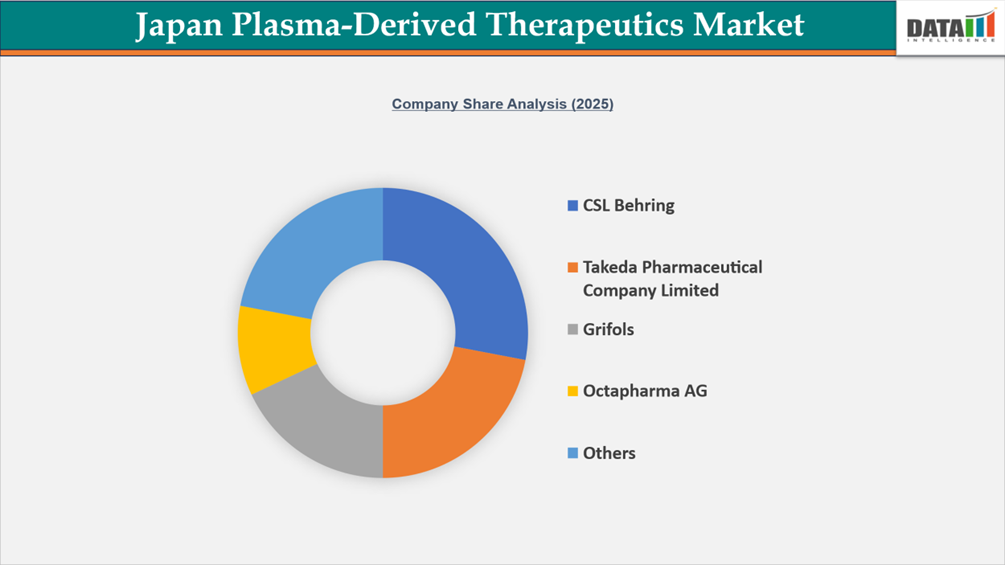

The Japan plasma-derived therapeutics market is fairly consolidated and primarily led by global plasma specialists, including CSL Behring, Takeda Pharmaceutical Company Limited, Grifols, and Octapharma AG. These four companies have an overwhelming market presence due to their predominance in the three major categories of plasma-derived products: immunoglobulins (IVIg / SCIg), coagulation factors, and albumin; the strength of their immunoglobulin and albumin portfolios is further enhanced through their sophisticated plasma fractionation processes and well-established hospital procurement networks. Takeda has the added advantage of being locally manufactured in Japan, has extensive experience with Japanese requirements for regulatory compliance, and therefore holds a strategic positional advantage in Japan.

Examples of domestically based organizations that promote and assist in achieving national plasma self-sufficiency and stability are the Japan Blood Products Organization and KM Biologics. Additionally, companies like Kedrion Biopharma, Biotest AG, LFB Group, and Baxter International are entering various specialized segments of the plasma product market. In general, competition for the entire Japanese plasma-derived therapeutics market will be driven by reliability of supply, regulatory compliance, product quality, and development of long-term relationships with hospitals, rather than by competition based upon price.

Japan Plasma-Derived Therapeutics Market Key Development

2026 – Regulatory Strengthening and Market Maturity Phase

- 2026 – Enhanced Regulatory Oversight by PMDA and MHLW

Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) strengthened regulatory requirements for plasma-derived products, focusing on GMP compliance, traceability systems, and viral inactivation validation standards, reinforcing Japan’s position as one of the most stringent biologics regulatory markets globally. - 2026 – Rising Clinical Demand Driven by Aging Population

Japan’s rapidly aging population (with nearly one-third aged 65+) continued to drive strong demand for immunoglobulin therapies, albumin, and coagulation factors, particularly in neurology, immunology, hematology, and critical care applications. - 2026 – Pipeline Advancement of Next-Generation Plasma Therapies

Industry players advanced development of long-acting immunoglobulins, high-purity plasma products, and improved coagulation factor formulations, aiming to enhance patient convenience and therapeutic efficacy. - 2026 – Expansion of Global Partnerships and Supply Chain Integration

The market saw increased cross-border collaborations, licensing agreements, and contract manufacturing partnerships, strengthening Japan’s integration into the global plasma supply ecosystem. 2026 – Policy Support for Biotechnology and Biopharma Growth

The Japanese government continued to promote biotechnology and advanced biologics through structured investment policies, supporting innovation in plasma-derived therapies, regenerative medicine, and rare disease treatment pipelines.2025 – Capacity Expansion and Strategic Investment Phase

- September 2025 – Takeda Expands Plasma-Derived Therapies Manufacturing Capacity in Osaka (Juso Facility)

Takeda reaffirmed its major investment in the Juso, Osaka manufacturing facility, with total investment revised to approximately JPY 153 billion due to inflationary pressures and construction cost increases. The facility is expected to significantly strengthen Japan’s long-term plasma-derived product supply security. - 2025 – Rising Demand for Immunoglobulin and Specialty Plasma Products

Demand for IVIg, SCIg, albumin, and coagulation factors continued to grow across Japan, driven by increasing diagnosis rates of immunodeficiency disorders and neurological conditions, alongside an aging population. - 2025 – Strengthening of Domestic Plasma Supply Chain Ecosystem

Japan intensified efforts to improve plasma collection, fractionation efficiency, and national supply security through collaboration between the Ministry of Health, Labour and Welfare (MHLW), Japan Blood Products Organization (JBPO), and domestic manufacturers such as KM Biologics. - 2025 – Strategic Collaborations and R&D Expansion

Global and Japanese players, including Takeda, CSL Behring, Grifols, and KM Biologics, expanded partnerships and R&D initiatives focused on improving product purity, yield efficiency, and viral safety in plasma fractionation technologies. - In December 2024, Takeda Pharmaceutical Company Limited received regulatory approval from Ministry of Health, Labour and Welfare, Japan for HYQVIA® 10%, an fSCIg therapy indicated for treatment of agammaglobulinemia and hypogammaglobulinemia. HYQVIA® is the first ever approved fSCIg product in Japan, allowing larger infusion volumes to be given with less frequent doses than conventional subcutaneous immunoglobulin therapies. The approval of this unique, first-in-class fSCIg will improve treatment options available for patients requiring long term immunoglobulin replacement therapy.

What Sets This Japan Plasma-Derived Therapeutics Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive and up-to-date market intelligence with forecasts through 2033, covering demand by product type, application, end user, source of plasma and route of administration, supported by detailed analysis of consumption patterns, plasma supply dynamics, and reimbursement impact.

- Regulatory Intelligence – In-depth analysis of the regulatory and policy framework that governs plasma-derived therapies, including MHLW and PMDA oversight, plasma safety and traceability standards, fractionation guidelines, NHI pricing revisions, pharmacovigilance requirements, and biologics lifecycle management policies.

- Competitive Benchmarking – Benchmarking domestic and global plasma fractionators and biologics manufacturers based on product portfolios, fractionation capacity, plasma sourcing strategies, pipeline strength, technology adoption, pricing positioning, hospital procurement relationships, and strategic collaborations.

- Actionable Strategies & Cost Dynamics – Actionable insights into plasma supply security, self-sufficiency initiatives, fractionation yield optimization, pricing pressures from biennial NHI drug price revisions, immunoglobulin demand expansion, and manufacturing cost structures, with input from clinicians, regulatory specialists, and plasma industry executives.

Japan Plasma-Derived Therapeutics Market: Economic & Investment Analysis

The Japan plasma-derived therapeutics market exhibits robust macroeconomic resilience, underpinned by an advanced healthcare infrastructure, universal health coverage, and a rapidly aging demographic profile. Driven by an escalating prevalence of chronic, immunological, and hematological conditions, the market is structurally necessity-driven rather than discretionary. Japan's National Health Insurance (NHI) reimbursement mechanisms provide a stable framework that ensures consistent patient access and highly predictable revenue streams for industry participants.

Macroeconomic Drivers & Pricing Dynamics

- Sustained Demand Indicators: The market benefits from exceptionally high per-capita healthcare expenditure and committed government funding for biologics and orphan drug management.

- Fiscal Controls: Periodic NHI drug price revisions and stringent cost-containment policies introduce moderate pricing compression.

- Strategic Mitigation: To counter regulatory pricing pressures, manufacturers must prioritize operational efficiency, domestic supply chain optimization, and value-based innovation.

- Market Resilience: The critical, non-substitutable nature of plasma-derived therapies effectively mitigates substitution risks and guarantees long-term demand stability.

Investment Landscape & Strategic Imperatives

The Japanese market presents a highly compelling thesis for global plasma fractionation enterprises and biologics manufacturers, characterized by high barriers to entry, a rigorous regulatory framework, and a structural deficit in domestic plasma self-sufficiency.

Current capital allocation and strategic initiatives are concentrated across three core pillars:

| Strategic Focus Area | Operational Execution |

|---|---|

| Capacity Expansion | Scaling domestic fractionation throughput and enhancing technological capabilities in immunoglobulin and coagulation factor production. |

| Supply Chain Security | Strengthening localized plasma collection networks to mitigate global supply volatility. |

| Regulatory Alignment | Formulating joint ventures, partnerships, and localization strategies to navigate PMDA expectations and secure market access. |

Target Audience

This report is designed for a wide range of stakeholders across the healthcare, pharmaceutical, and investment ecosystem, including:

- Pharmaceutical and biotechnology companies involved in plasma fractionation, biologics, and rare disease therapeutics

- Plasma product manufacturers and suppliers of immunoglobulins, albumin, and coagulation factors

- Hospital procurement teams and healthcare providers specializing in immunology, hematology, neurology, and critical care

- Research institutes and academic organizations focusing on plasma-derived therapies and biologics innovation

- Investment firms, private equity groups, and venture capitalists evaluating opportunities in the biologics and plasma therapy sector

- Regulatory authorities and policy makers involved in healthcare planning, biologics approval, and reimbursement frameworks

- Contract manufacturing organizations (CMOs) and life sciences service providers supporting biologics production and supply chain operations

- Market research analysts and consulting firms tracking pharmaceutical and specialty therapeutics markets

Who Should Buy This Report?

This report is highly valuable for organizations and professionals seeking deep insights into Japan’s plasma-derived therapeutics ecosystem, including:

- Companies planning to enter or expand within the Japanese biologics and plasma-derived therapeutics market

- Existing manufacturers aiming to strengthen competitive positioning through market intelligence and strategic benchmarking

- Investors and financial institutions evaluating high-growth opportunities in rare disease and plasma-based therapeutics

- Healthcare strategists and policymakers analyzing demand-supply dynamics in biologics and critical care therapies

- Supply chain and procurement managers seeking insights into plasma sourcing, fractionation capacity, and product availability

- R&D teams focusing on next-generation immunoglobulins, coagulation factors, and advanced plasma-derived formulations

- Consulting firms advising pharmaceutical clients on market entry, expansion, and regulatory compliance strategies

- Distributors and healthcare service providers aiming to optimize product access and hospital partnerships in Japan

Why Choose DataM Intelligence?

DataM Intelligence provides a robust, data-driven approach to healthcare and life sciences market research, delivering actionable insights backed by primary and secondary research methodologies. This report offers a comprehensive understanding of the Japan Plasma-Derived Therapeutics Market, enabling stakeholders to make informed strategic decisions with confidence.

Key advantages include:

- Comprehensive Market Coverage: In-depth analysis across product types, applications, end users, and distribution channels with precise revenue forecasts and growth projections

- Strategic Insights: Clear identification of market drivers, restraints, opportunities, and emerging trends shaping the plasma-derived therapeutics landscape

- Competitive Intelligence: Detailed profiling of leading global and regional players, including their strategies, pipelines, and market positioning

- Regulatory & Policy Analysis: Insight into Japan’s stringent regulatory framework, including PMDA oversight and NHI reimbursement policies

- Data Accuracy & Forecasting: Reliable projections supported by validated research models and continuous market tracking

- Actionable Business Intelligence: Insights designed to support investment planning, market entry strategies, and portfolio expansion decisions

- Expert-Led Research: Developed by experienced analysts with domain expertise in biologics, rare diseases, and pharmaceutical markets