Japan Contract Sterile Fill-Finish Services Market Overview

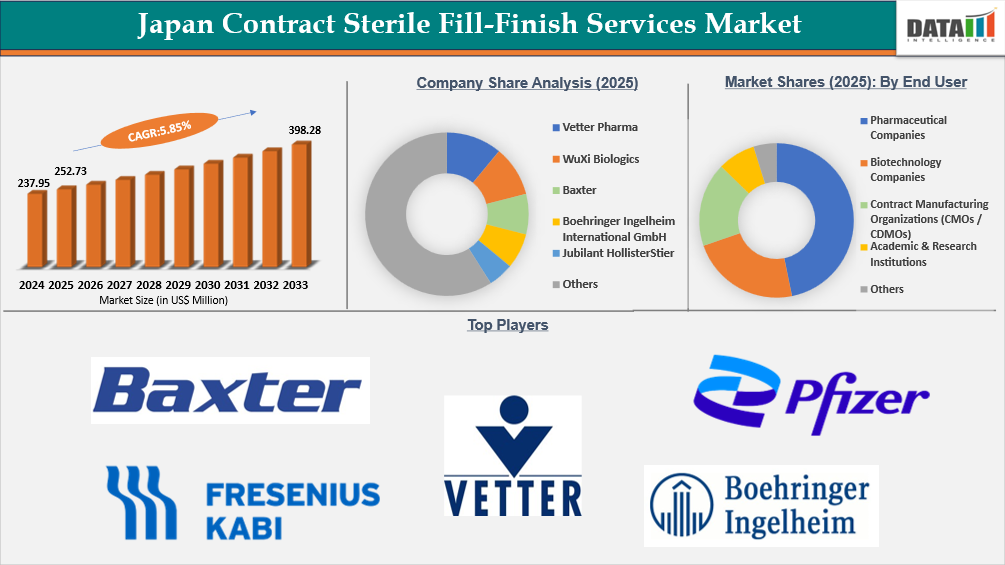

The Japan contract sterile fill-finish services market reached US$237.95 Million in 2024, rising to US$252.73 Million in 2025, and is expected to reach US$398.28 Million by 2033, growing at a CAGR of 5.85% from 2026 to 2033.

The market is primarily driven by the growing production of biologics, the strict regulations controlling the production of sterile drugs in Japan, and the outsourcing of aseptic manufacturing operations by pharmaceutical and biotechnology industries. Sterile fill-finish is a vital final-stage manufacturing procedure in which medicinal products are aseptically filled into vials, syringes, cartridges, or other primary containers in carefully controlled conditions. In Japan, sophisticated technologies like isolator-based filling lines, restricted access barrier systems, automated inspection systems, and integrated lyophilization capabilities are required to comply with GMP regulations enforced by the Pharmaceuticals and Medical Devices Agency (PMDA).

In 2023, biologics and high-value injectables accounted for a sizable portion of Japan's pharmaceutical output, which exceeded JPY 10 trillion, indicating a large need for sterile manufacturing. CDMOs providing high-value services like sterile compounding, lyophilization, and ready-to-use container filling are becoming more and more significant as product pipelines move toward complicated compositions that require precise aseptic processing and lower batch flexibility. Outsourcing demand is also supported by the need to speed up time-to-market for new injectable releases and capacity optimization tactics used by major pharmaceutical companies.

Contract Sterile Fill-Finish Services Industry Trends and Strategic Insights

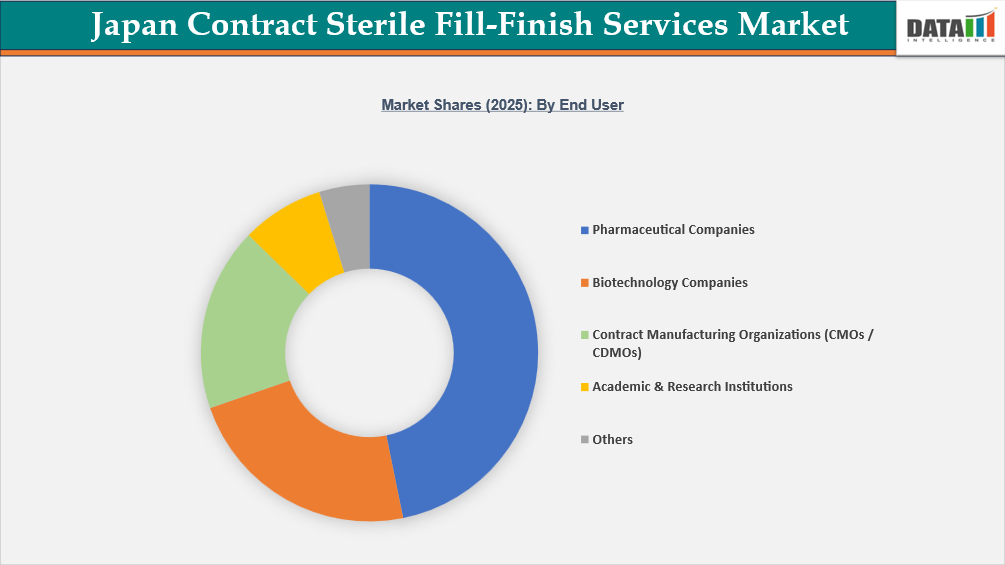

- By end user, pharmaceutical companies led the Japan contract sterile fill-finish services market, capturing the largest revenue share of 46.8% in 2025.

Japan Contract Sterile Fill-Finish Services Market Size and Future Outlook

- 2025 Market Size: US$252.73 Million

- 2033 Projected Market Size: US$398.28 Million

- CAGR (2026–2033): 5.85%

Market Dynamics

Growing demand for biologics, biosimilars, and complex injectable therapies

The Ministry of Health, Labour, and Welfare (MHLW) has established a specific policy target to encourage biosimilar adoption in Japan, to increase the proportion of active pharmaceutical ingredients (APIs) for which biosimilars have a market share of more than 80% to 60% by the end of 2029. This aim demonstrates the government's strong commitment to boosting the use of biologics and biosimilars as part of larger cost-cutting and supply-chain stability measures. Concurrently, Japan is experiencing continued growth in the development and commercialization of biologics, biosimilars, and other complex injectable therapies, such as monoclonal antibodies, antibody-drug conjugates, and long-acting formulations. This growth is particularly notable in oncology, immunology, and rare diseases, where injectable administration remains the standard of care.

From a Japan contract sterile fill-finish services market standpoint, the growing biosimilar penetration and the growing biologics pipeline directly fuel demand for high-containment manufacturing systems, lyophilization technologies, enhanced aseptic processing, and complex packaging formats like cartridges and prefilled syringes. Since many small-to-mid-sized pharmaceutical businesses and biotech companies lack internal sterile manufacturing infrastructure, it is becoming strategically necessary to outsource fill-finish operations to specialist CDMOs to ensure scalability, regulatory compliance, and effective commercialization.

Segmentation Analysis

The Japan contract sterile fill-finish services market is segmented based on product / primary container, service type, molecule type, application, scale of operation, end-user, packaging material, and technology platform.

Pharmaceutical Companies Dominate End-User Demand in Japan Contract Sterile Fill-Finish Services Market

Pharmaceutical Companies are the largest end-user category in Japan's contract sterile fill-finish services market, accounting for the majority of outsourced sterile manufacturing demand. This leadership is reinforced by Japan's strong pharmaceutical production base, which was around JPY 10 trillion in 2023, according to the Ministry of Health, Labour, and Welfare. Biological goods make up a large portion of overall manufacturing value, indicating the country's reliance on injectable and specialist medicines that need superior aseptic processing.

Furthermore, annual reports of the PMDA continuously show a large number of biologics, biosimilars, and other sterile injectable approvals, implying that commercial-scale fill-finish requirements will continue. Pharmaceutical companies are increasingly outsourcing sterile fill-finish operations to specialized CDMOs due to stringent GMP compliance standards and the high capital investment required for isolator-based filling and lyophilization infrastructure, allowing them to maintain the majority of the market share among end users in Japan.

Competitive Landscape

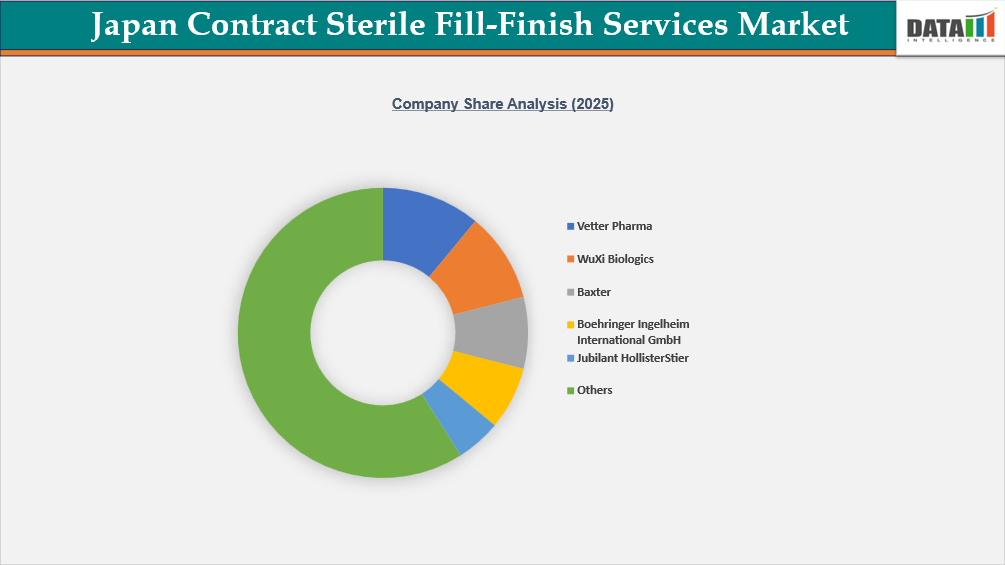

A fairly competitive and technologically advanced environment is created by the presence of both international CDMOs and a few indigenous manufacturing experts in the Japan Contract Sterile Fill-Finish Services Market. In order to compete, multinational companies like Baxter, Boehringer Ingelheim International GmbH, Vetter Pharma, Fresenius Kabi, Pfizer Inc., Aenova Group, WuXi Biologics, and Jubilant HollisterStier use high-containment systems, prefilled syringe and cartridge filling capabilities, integrated global supply networks, and advanced aseptic technologies.

Domestic and regionally engaged firms, like TAIYO PHARMA TECH CO., LTD. and AJINOMOTO CO., INC., contribute to local sterile production capacity by utilizing established regulatory knowledge and domestic distribution networks. In Japan, competitive strategies include expanding isolator-based filling lines, lyophilization capacity, high-potency injectable handling, biologics-ready single-use systems, and long-term collaborations with innovators and biosimilar developers looking for compliant, scalable sterile fill-finish solutions.

Key Developments

- In December 2025, the Japanese government allocated approximately USD 100 million under its FY2025 supplementary budget to strengthen domestic manufacturing facilities for regenerative medicine and cell and gene therapies. According to the Japan Contract Sterile Fill-Finish Services Market, this endeavor is anticipated to fuel future demand for high-containment fill-finish services and specialized aseptic processing.

- In October 2025, Alfresa Holdings Corporation, Kidswell Bio Co., Ltd., Kaiom Biosciences Inc., and Mycenax Biotech Inc. signed a basic agreement to form a joint venture for domestic biosimilar API and formulation manufacturing as part of Japan's Ministry of Health, Labour, and Welfare's biosimilar facility development support project. This program is projected to increase local biologics and injectable manufacturing capacity, enhance CDMO integration, and encourage long-term growth in sterile fill-finish outsourcing.

What Sets This Japan Contract Sterile Fill-Finish Services Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive and up-to-date market intelligence with forecasts through 2033, covering Japan demand by key segmentation, including product / primary container, service type, molecule type, application, scale of operation, end-user, packaging material, and technology platform.

- Regulatory Intelligence – In-depth assessment of Japan’s pharmaceutical manufacturing and GMP regulatory frameworks impacting sterile production and outsourcing, including requirements from the PMDA and alignment considerations with FDA and EMA standards, covering facility approvals, aseptic processing compliance, quality validation, serialization, and post-marketing obligations.

- Competitive Benchmarking – Structured benchmarking of leading domestic and international CDMOs operating in Japan based on sterile capacity, technology platforms, service integration, client portfolio, expansion strategies, and strategic partnerships in the market.

- Actionable Strategies & Cost Dynamics – Strategic insights into capacity expansion planning, outsourcing trends, pricing structures, capital expenditure requirements, high-containment manufacturing, and operational cost drivers, supported by expert perspectives from CDMO executives, regulatory specialists, and industry consultants.