Japan AI Data Centers Market Definition and Overview

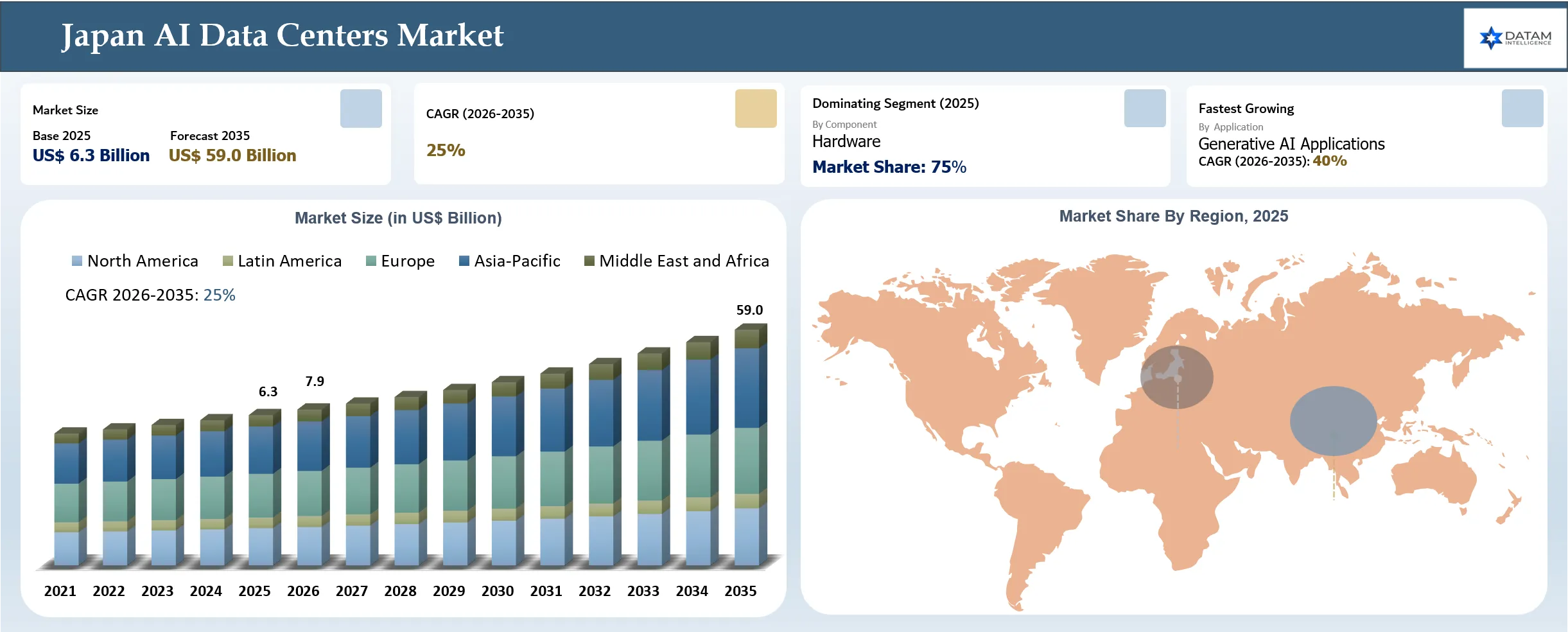

The Japan AI data centers market reached USD 6.3 billion in 2025 and is expected to reach USD 59.0 billion by 2035, growing with a CAGR of 25% during the forecast period 2026-2035, due to the rising demand for generative artificial intelligence (AI), large language models (LLMs), HPC, and enterprise AI systems. Data center spending on AI-driven resources is increasing because organizations require more GPU cluster support, high-density computing, low-latency networking, and scalable storage capacity. There is also an increase in AI-centric projects, such as cloud-based AI, sovereign AI, and digital transformation projects that are boosting infrastructure growth in metro areas. Major vendors of technology, cloud service providers, and colocation vendors are building facilities for AI with liquid cooling capability, efficient power systems, and next-generation network solutions to keep up with increased demand for compute power. But the lack of adequate power supplies, increased costs of construction, land scarcity in specific areas, and challenges of deploying dense AI infrastructure remain important factors affecting market growth.

Key Takeaways

- The commercialization of generative AI and large language models carries the most influence on drivers, with 40% market growth contribution, followed by enterprise AI adoption with 30% market growth contribution.

- The hardware holds the largest market share of 75% in the component segment by 2026. Development in GPU, AI accelerator, HBM, and network technology accounts for 18% of the market growth.

- Japanese Government announces a USD 480 million (¥72.5 billion) investment towards AI and computing within Japan in 2024.

- Blackstone made an announcement that the company will invest around USD 30 billion in Japanese AI data centers over the course of next three to five years aiming at exceeding 1 GW of total power capacity.

- According to the International Trade Administration (ITA), Japan's AI infrastructure is rapidly expanding at a market value of USD 8.9 billion in 2024, and it is projected to reach USD 27.9 billion by 2029.

Japan AI Data Centers Market: Industry Trends and Strategic Insight

- Japan is becoming a strategic base for artificial intelligence, with international cloud companies, infrastructure operators, and financiers pouring billions of dollars into hyperscale data centers in order to satisfy increasing demand for AI models training and AI workloads from enterprises. Although growth is primarily occurring in Tokyo and Osaka, development is starting to take place in secondary regions to ensure power and land availability.

- Rising rack density is driving more to advanced liquid cooling technology direct-to-chip, immersion, and rear-door heat exchangers to be adopted due to the importance of cooling efficiency as a differentiating factor that determines AI compute performance.

- The desire of Japan for sovereignty of AI and data localization is forcing it to invest heavily in computing platforms and data centers within the country itself.

- Increasing development of latency-sensitive AI-driven applications in manufacturing, intelligent cities, robots, logistics, and autonomous transport, there is growing need for edge infrastructure, which will become a key complement to centralized hyperscale AI infrastructures.

- Rising demand for low-latency connections has led to an increasing interest in high bandwidth interconnects, AI networks, Ethernet infrastructure, and high-performance storage technologies in support of distributed artificial intelligence training and inference.

Japan AI Data Center Market Scope

| Metrics | Details |

| 2025 Market Size | USD 6.3 Billion |

| 2035 Projected Market Size | USD 59.0 Billion |

| CAGR (2026-2035) | 25% |

| By Component | Hardware, Software, Services |

| By Data Center Type | Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, Edge AI Data Centers |

| By Deployment Model | Cloud-based, On-premises, Hybrid |

| By AI Workload | AI Training, AI Inference, Generative AI, High-Performance Computing (HPC), Machine Learning & Analytics, Others |

| By Cooling Technology | Air Cooling, Liquid Cooling, Hybrid Cooling, Others |

| By Power Capacity | Up to 50 MW, 51-100 MW, Above 100 MW |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Japan AI Data Center Market Disruption Analysis

AI Semiconductor Supply Chain Volatility Creating Infrastructure Deployment Bottlenecks in Japan AI Data Centers

Disruption in the Japan AI Data Centers Market is increasingly becoming associated with the supply chain issues related to semiconductors used in advanced AI computation, including GPUs, AI accelerators, and high bandwidth memory (HBM). With increased investments being made by the hyperscale, cloud companies, and enterprise AI innovators into generative AI data center infrastructure, there has been an increase in demand that cannot be matched by the current supply of such computing technology globally. Shortages in the semiconductor sector go further than GPU and include key components such as HBM memory, substrate packaging, power semiconductors, and server components. By the AI semiconductor shortages that result in 6-12 month lead times for some components. Moreover, the centralization of the production and advanced packaging of AI chips among only a few vendors is leading to vulnerabilities within Japan's AI infrastructure ecosystem.

The revenues of NVIDIA in terms of data centers went beyond USD26.3 billion in just one quarter, while the demand for advanced AI equipment caused serious supply issues for both GPUs and HBM memory; even some of the upcoming AI processors were booked in advance for further periods of time. Meanwhile, the Japanese manufacturers of the components faced unprecedented levels of demand for parts for AI servers, cautioning about possible shortages of the electronic components, which can slow down the development of AI data centers.

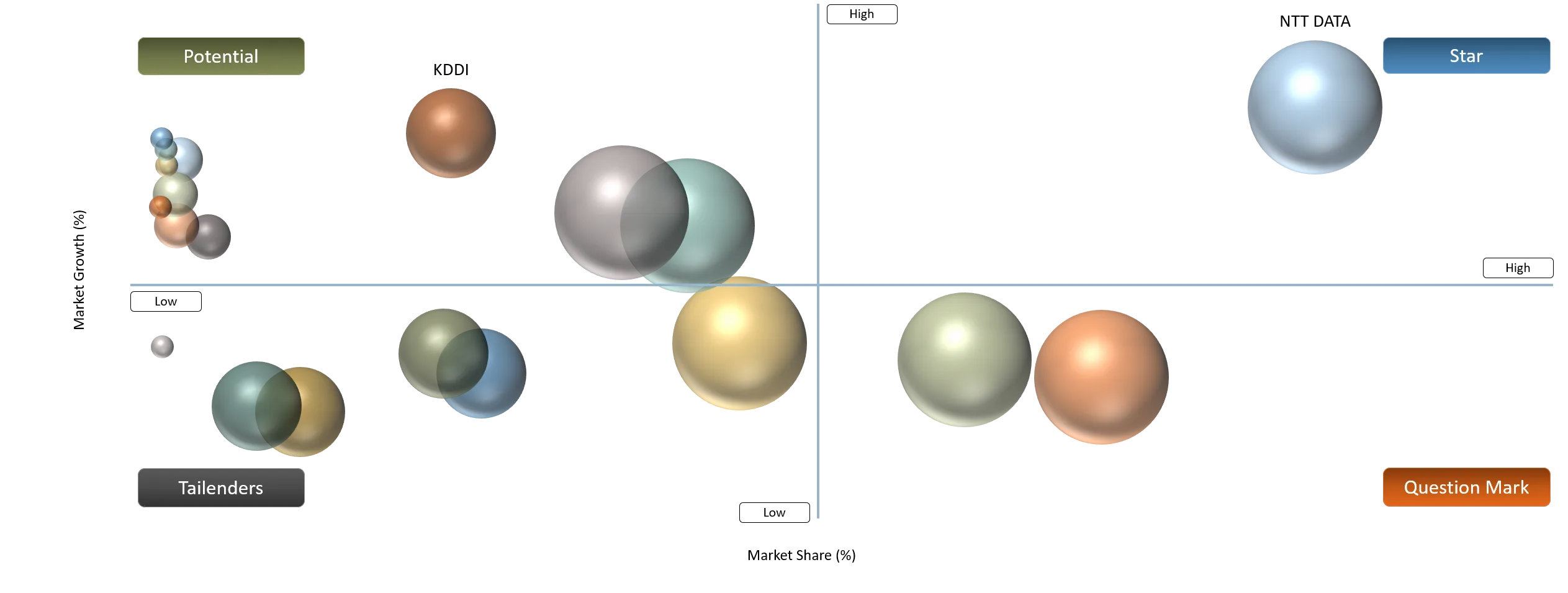

Japan AI Data Center Market BCG Matrix: Company Evaluation

Stars include NTT DATA, AWS, Microsoft, and Google Cloud, which are chosen for their significant capabilities in AI computation, having hyperscale data centers and clouds in Japan. The companies mentioned are rapidly growing in terms of GPU-driven computing and sovereign AI infrastructure to provide their solutions for generative AI, machine learning, and enterprise AI services. Question Marks include Digital Realty, Equinix, AirTrunk, and Colt Data Centre Services since they are rapidly scaling their hyperscale and colocation data center capacity in order to capitalize on the rise in demand for AI infrastructure. They have good growth opportunities given that there is a rising need for AI facilities.

Potential includes companies like KDDI, IDC Frontier, and NEC Corporation. These firms have an advantage due to the rise in the use of AI by enterprises, telecommunication infrastructures, and demand for domestic clouds. Although these firms are boosting their AI infrastructures, their AI-specific infrastructure presence is less compared to other hyperscale. Tailenders category includes Fujitsu due to the fact that its main advantage is in enterprise IT services, system integration, and AI solutions rather than in having big commercial AI data centers. It should be noted that the company operates in the digital infrastructure ecosystem of Japan.

Japan AI Data Center Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Commercialization of generative AI and large language models has created high demand for GPU-heavy infrastructure, leading to significant expansion of data centers in Japan. | 40% | Hyperscale cloud providers, AI model developers, enterprises, research institutions, financial services, and technology companies | Generative AI model training, large language model (LLM) deployment, AI inference, natural language processing, autonomous systems, and advanced analytics | Accelerates development of AI-optimized data centers with GPU clusters, high-density racks, advanced cooling systems, and high-speed networking infrastructure. Strengthens demand for dedicated AI computing campuses. |

Enterprises adopting AI in various industries are creating constant demand for efficient computing resources to manage large amounts of data and conduct advanced analytics. | 30% | Manufacturing, automotive, BFSI, healthcare, retail, telecommunications, and industrial automation sectors | Predictive analytics, smart manufacturing, fraud detection, medical AI, customer intelligence, robotics, and enterprise automation | Drives sustained demand for scalable AI infrastructure, hybrid cloud environments, and localized data processing capabilities. Encourages enterprises to shift from AI experimentation toward production-scale deployments. |

The government-led digital transformation as well as sovereign AI programs in Japan are pushing government-backed investments in locally based AI infrastructure, creating long-term demand for domestic AI-specific data centers. | 20% | Government agencies, research institutions, defense, public sector organizations, and domestic AI developers | Sovereign AI platforms, secure government computing, national AI research, public data analytics, and digital services | Enhances Japan’s domestic AI computing capability and reduces dependency on overseas infrastructure. Supports investments in secure, resilient, and domestically controlled AI data center ecosystems. |

Advancements in GPUs, AI accelerators, HBM, and network technologies are making complex AI loads possible and pushing operators to deploy dedicated AI infrastructure. | 18% | Data center operators, semiconductor companies, cloud providers, HPC facilities, and AI infrastructure developers | High-performance computing (HPC), AI training clusters, deep learning workloads, simulation, and real-time AI processing | Promotes transition from conventional data centers toward AI-native facilities with liquid cooling, accelerated computing architectures, and ultra-high-speed interconnect technologies. |

Expansion of AI cloud providers such as GPU-as-a-Service and AI model development platforms are contributing to the increased usage of cloud-based AI resources. | 25% | Startups, enterprises, software developers, research organizations, and cloud service users | AI-as-a-Service, machine learning platforms, cloud inference, AI application development, and scalable computing services | Increases utilization of cloud AI infrastructure and strengthens demand for colocation, hyperscale facilities, and GPU availability models. Encourages partnerships between cloud providers and Japanese data center operators. |

Enterprises adopting AI in various industries are creating constant demand for efficient computing resources to manage large amounts of data and conduct advanced analytics

The rapid incorporation of AI within Japan’s leading industries is quickly developing into one of the key catalysts driving demand for AI data centers. Companies in the manufacturing, automotive, financial services, healthcare, telecoms, and retail industries are adopting machine learning algorithms, generative AI, predictive analytics, and automation applications that rely on computing power and need data to be stored securely. As per the Ministry of Economy, Trade and Industry (Japan), Japan’s manufacturing industry is pursuing digitalization efforts with the use of AI, IoT, and data-related technologies in order to boost efficiency, and thus the need for computing capabilities increases. Japan’s manufacturing industry accounts for about 20% of Japan’s GDP, which makes industrial adoption of AI a crucial source of data processing demand. The Japanese government recognizes that AI is an area of strategic technology and has made substantial investments in order to enhance its AI computing capability.

This year, in 2024, the Japanese government has announced ¥72.5 billion (approximately $480 million) worth of investments in domestic generative AI and computing. For instance, in August 2025, according to the International Trade Administration (ITA), Japan's AI infrastructure is rapidly expanding at a market value of $8.9 billion in 2024, and it is projected to reach $27.9 billion by 2029.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Scarcity of land that is suitable for constructing data centers, particularly in places like Tokyo and Osaka, along with cost implications and other factors, is hindering capacity growth in terms of expansion. | 22% | Site acquisition, facility expansion, and regional deployment planning | Hyperscale AI data centers, GPU-based AI training clusters, cloud AI infrastructure | Limited availability of data center-ready land in major hubs increases acquisition costs, extends project timelines, and forces operators to shift toward regional locations with additional investments in power and network infrastructure. |

Higher rack power densities have made conventional cooling inadequate, whereas the use of liquid cooling and other thermal management techniques introduces a lot of complications in infrastructure and maintenance costs. | 18% | Data center design, cooling infrastructure, and operational expenditure | AI training facilities, high-performance computing (HPC), GPU-intensive workloads | Increasing AI server densities require advanced cooling systems such as liquid cooling, raising deployment complexity, maintenance requirements, and capital expenditure. This creates challenges for operators scaling AI-ready facilities efficiently. |

Japan’s high vulnerability to earthquakes means that special engineering, fortification of buildings and redundancy of power systems is required for AI data centers, increasing costs of construction considerably. | 14% | Construction cost, facility resilience, and disaster preparedness | Mission-critical AI data centers, enterprise AI workloads, government and sovereign AI infrastructure | Seismic-resistant designs, reinforced structures, and redundant power systems increase upfront construction costs and lengthen development cycles. Operators must prioritize resilient infrastructure, reducing flexibility in site selection and increasing total project investment requirements. |

The amount of power consumed by AI applications is increasing rapidly, thus creating problems for Japan as far as achieving its targets of cutting back on greenhouse gas emissions. | 28% | Energy availability, sustainability compliance, and operational costs | Large-scale AI model training, generative AI platforms, cloud AI services | Rising AI power consumption is becoming a major constraint as operators require high-capacity electricity supply while meeting Japan’s decarbonization objectives. Power availability and sustainability requirements are influencing site selection, operational costs, and the pace of AI data center expansion. |

Scarcity of land that is suitable for constructing data centers, particularly in places like Tokyo and Osaka, along with cost implications and other factors, is hindering capacity growth in terms of expansion

One of the major challenges that acts as an obstacle to the growth of data center infrastructure in Japan based on AI is a lack of adequate land, especially in areas like Tokyo and Osaka, where data centers exist in abundance. This has been caused by a rising demand for data centers that use artificial intelligence in their operations. Urban land costs, availability, and other factors have also made the project development process difficult. In fact, almost 90% of the data centers in Japan are situated in the Greater Tokyo and Greater Osaka areas. The shortage of suitable land is also a factor driving up capital investment in AI data centers. Higher expenses on land purchases, delays in preparing sites, and other construction-related costs are driving up the financial burden of the project. Tokyo has been noted to be one of the most expensive places in the world in terms of data center construction because of rising costs owing to the scarcity of space.

Since AI applications demand ultra-low latency and robust high-performance computing infrastructures, the strategic location of land is an important aspect that will determine the rate at which capacity expansion of AI data centers takes place in Japan. For instance, in June 2026, S&P Global Ratings pointed out that there is limited availability of suitable land, power, grid access, and construction resources within Japan's data center industry. This scarcity of sites suitable for development, especially in key data centers like the Greater Tokyo region, has resulted in higher costs and longer periods in developing the facilities.

Japan AI Data Center Market Segment Analysis

The Japan AI Data Center market is segmented based on infrastructure layer, data center architecture type, component, deployment model, application, end user, and region.

Hardware Components Driving Dominance in Japan AI Data Center Market

Hardware sub-segment dominates in the component segment market of Japan AI Data Center Market with a market share of 75% in 2026, owing to the quick installation of AI Servers, Graphics Processing Units (GPUs), AI Accelerators, High-Performance Storage systems, and Networking equipment that is required to handle heavy AI load. The rising use of generative AI, large language models, and enterprise AI solutions has led to an increase in demand for high-performance computing hardware systems. The AI computational workloads need unique architectural designs of hardware components, which may include GPU-enabled AI servers, AI accelerators, high-performance memory systems, and high-speed networking systems that can handle the complex workloads involved in training and inference. In Japan, the growth in AI computing power provided by cloud service providers, telecom operators, and other organizations has led to increased investments in data center hardware designed specifically for AI processing workloads.

According to the Japan Ministry of Economy, Trade and Industry (METI) Digital Infrastructure Strategy, Japan has been pushing towards building its own digital infrastructure and increasing its computing power to enable the adoption of AI technologies in industries. This is in addition to efforts by the Japanese government through investments in computing power and semiconductor infrastructure.

Japan AI Data Center Market Competitive Landscape

- The Japan AI Data Center Market features an intensely competitive environment that includes local data center players, international colocation providers, cloud hyperscalers, and Japanese IT companies. The top infrastructure providers, NTT DATA, Digital Realty, Equinix, AirTrunk, Colt Data Centre Services, KDDI, Fujitsu, NEC Corporation, and IDC Frontier, engage in competition via data center capacity build-up, geographical location, renewable energy incorporation, and AI-enabled infrastructure creation. International cloud providers Microsoft, AWS, and Google Cloud further boost the market with their hyperscale cloud regions, AI computing infrastructure, and GPU infrastructure deployment. Japan’s data center market is still very localized, with Tokyo and Osaka serving as key locations where top players account for a large portion of capacity. The market is still remains ecosystem-dependent in that the competitive edge revolves around data centers' footprint, power source, AI hardware capability, networks, cloud services, and the capacity to provide a high-performance AI computing environment.

- Key players include NTT DATA, Digital Realty, Equinix, AirTrunk, Colt Data Centre Services, KDDI, Fujitsu, NEC Corporation, IDC Frontier, Microsoft, AWS, and Google Cloud.

Key Developments

- June 2026: Blackstone had announced its plans to invest an estimated USD 30 billion into Japan’s AI data centers within the next three to five years, with talks underway for building centers having a combined power capacity of over 1 GW.

- June 2026: NTT DATA launched an AI agent offering that would help in early-stage product planning for consumer products through the application of generative AI technologies.

- June 2025: KDDI has partnered with Hewlett Packard Enterprise (HPE) to launch AI data centers in Japan by early 2026, utilizing KDDI’s capabilities in operating data centers along with HPE’s technologies in AI infrastructure.

- June 2026: To expand its footprint in Japan, GDS formed a partnership with Gaw Capital Partners for the development of a 40 MW data center in Tokyo.

- March 2026: DigitalBridge and Japan Exchange and Industry (JEXI) concluded the acquisition of selected data center facilities from NEC Corporation, improving their standing in Japan’s digital infrastructure industry.

- October 2025: SoftBank and Oracle formed a strategic alliance for providing their AI and sovereign cloud offerings to companies in Japan via the Oracle Alloy technology. This partnership allows SoftBank to deploy OCI-based AI and cloud offerings in their local data centers that ensure security in AI computing, data sovereignty, and building up of an AI-ready data center infrastructure in Japan.

- May 2026: Fujitsu entered into a partnership with Anthropic in order to facilitate the faster adoption of generative AI solutions in Japan and around the world. This partnership entails the integration of Anthropic’s Claude AI with the AI platforms of Fujitsu.

Key Procurement Priorities and Buyer Evaluation Criteria

- Companies entering the Japan AI Data Center Market have started choosing infrastructure providers based on their capability of providing high-performance computing facilities for AI processing such as GPU-optimized data centers, high density server facilities, cooling, and high-power facilities.

- Innovation in the area of procurement decision making is being steered towards the fast pace of developments in generative AI, LLMs, machine learning tools, cloud AI services, and automation, thus making the need for data centers that support AI more urgent.

- When buying AI data centers in Japan, buyers consider many things, including the reliability of the data center, availability of electricity, energy efficiency, cooling performance, network connection, security compliance, and disaster recovery capabilities.

- The criteria for selection of AI data center providers include security standards, data sovereignty, compliance with Japan’s regulations, cybersecurity protocols, and protection from any form of unauthorized access.

- Buyers will be increasingly evaluating the partners' abilities in terms of workload optimization using AI, GPU clusters, cloud integration, and their capacity to deliver hyperscale AI.

Why Choose DataM?

- Technological Innovations: Explores advancements in Fan-Out Wafer-Level Packaging including high-density RDL, panel-level packaging, and heterogeneous integration, enabling improved performance, reduced power consumption, and smaller form factors for AI, 5G, and high-performance computing applications.

- Product Performance & Market Positioning: Evaluates how different players deliver packaging solutions based on I/O density, thermal performance, miniaturization, and cost efficiency, highlighting how leading companies differentiate through advanced integration and scalability across consumer electronics and automotive applications.

- Real-World Evidence: Highlights adoption of FOWLP in smartphones, wearables, automotive electronics, and AI chips, demonstrating benefits such as enhanced processing speed, reduced footprint, improved energy efficiency, and optimized system-level performance.

- Market Updates & Industry Changes: Tracks key developments such as capacity expansions, new packaging platforms, panel-level innovations, and regional semiconductor investments across Asia-Pacific, North America, and Europe, supporting the shift toward advanced packaging ecosystems.

- Competitive Strategies: Analyzes how leading companies expand through capacity scaling, technology innovation, strategic partnerships, and integration of advanced packaging with chip design to address rising demand from AI and high-performance computing markets.

- Pricing & Market Access: Explains pricing variations based on complexity, wafer size, and integration level, along with access through OSAT providers, foundries, and integrated device manufacturers supporting global supply chains.

- Market Entry & Expansion: Identifies growth opportunities driven by AI, 5G, automotive electronics, and data centers, while outlining strategies such as regional capacity expansion, technology differentiation, and ecosystem partnerships to scale globally.

Target Audience

- Cloud Service Providers and Hyperscale Companies

- AI and Machine Learning Companies

- Data Center Operators and Colocation Providers

- Telecommunication Companies

- Enterprise IT and Digital Transformation Leaders

- Government Agencies and Public Sector Organizations

- Financial Services and Banking Institutions