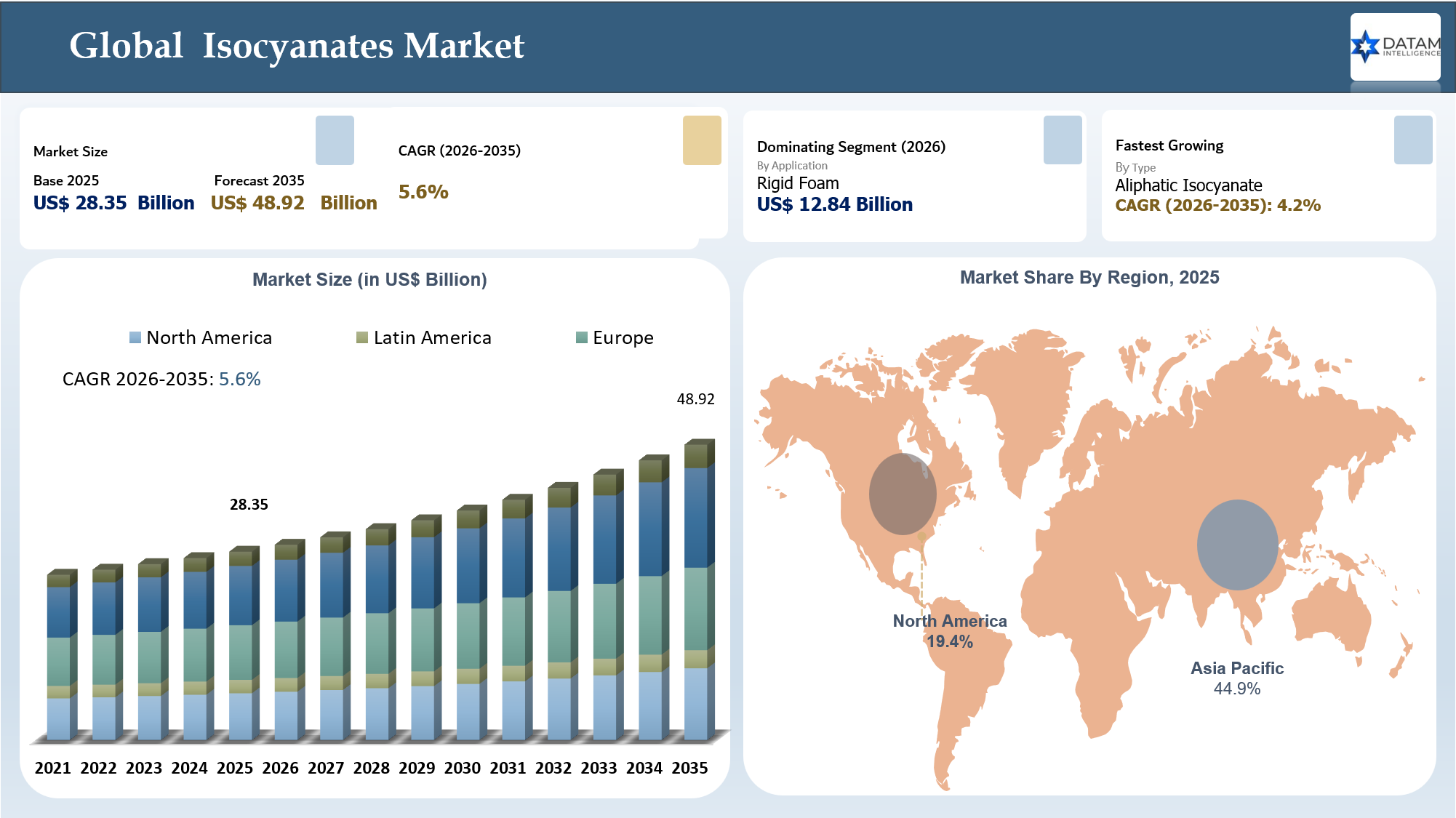

Isocyanates Market Size

The Global Isocyanates Market size stood at US$ 28.35 billion in 2025 and is expected to reach US$ 48.92 billion by 2035, growing with a CAGR of 5.6% during the forecast period 2026-2035.

The Isocyanates Market has become important due to the current wave of regulatory-led restructuring wherein procurement decisions have become highly dependent upon the criteria of safety, compliance, and reliability, along with the traditional elements of cost and volumes. The increased attention towards the risks related to diisocyanate exposure requires reconsidering relationships with suppliers and formulators and even product lines.

Isocyanates Market Trends

These factors influence demand for isocyanates in rigid foams, flexible foams, coatings, adhesives, sealants, elastomers, and binders all areas where isocyanates are key materials, although their usage may need safer processing technologies and low free monomer content. Suppliers of isocyanates are becoming increasingly sought after due to their capability to provide necessary regulatory documents, technological assistance with formulations, risk management and reliable quality at volumes of use typical for large polyurethane facilities.

Furthermore, the volatility of prices for benzene, toluene, aniline, and energy-related raw materials is increasing the volatility of this market. This research provides information for isocyanates manufacturers, distributors, formulators, and investors on which application areas are stable, what geographical markets grow and where premium opportunities arise.

Key Takeaways

- The Global Isocyanates Market was valued at US$28.35 billion in 2025 and is projected to reach US$48.92 billion by 2035.

- The market is expected to grow at a CAGR of 5.6% during the forecast period 2026-2035.

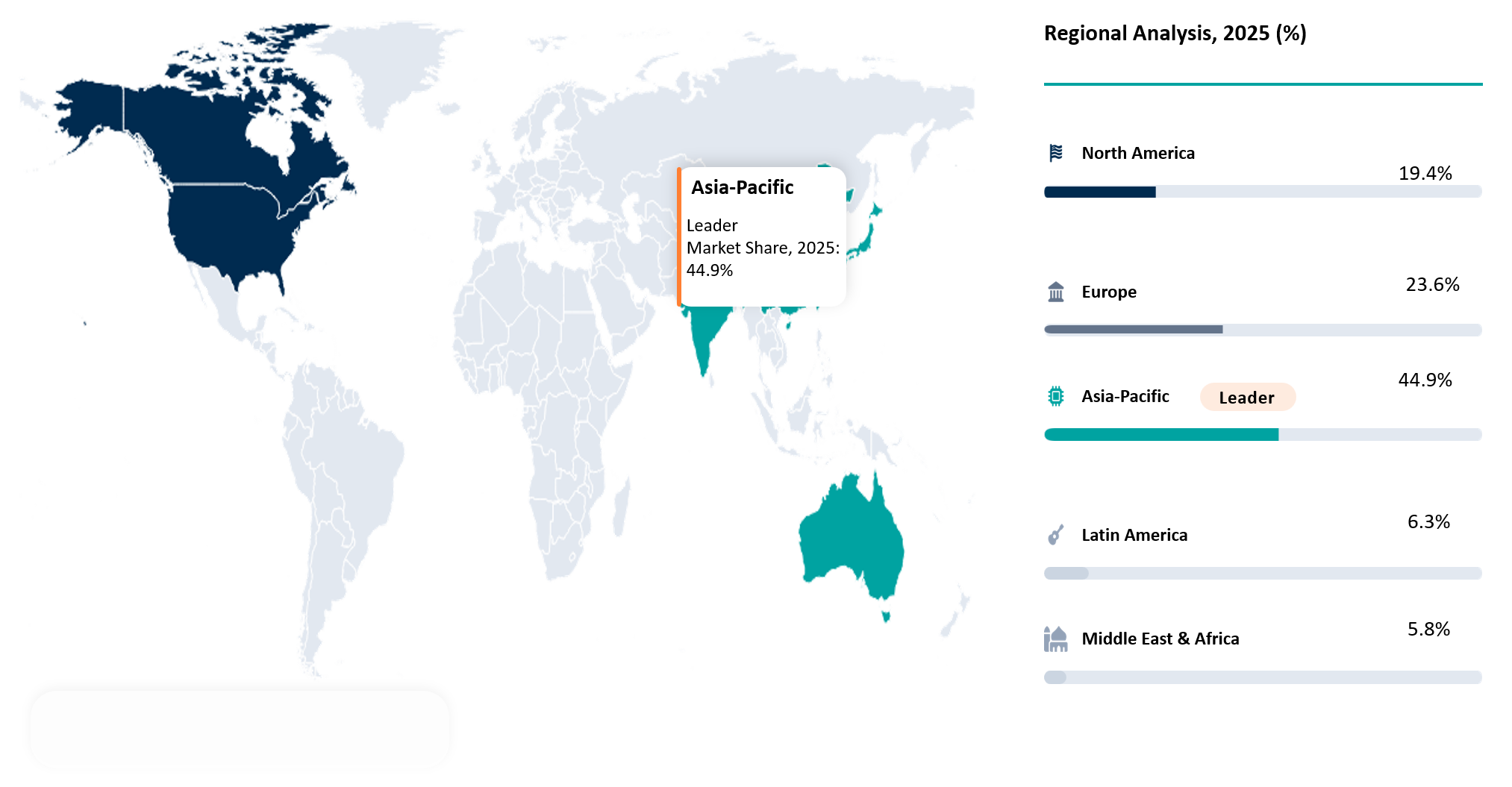

- Asia-Pacific held the highest market share at 44.9% in 2025, valued at approximately US$12.73 billion, supported by strong polyurethane demand from construction, automotive, furniture, footwear, appliances and coatings.

- Europe accounted for around 23.6% market share in 2025, valued at approximately US$6.69 billion, driven by energy-efficient building renovation, insulation standards and specialty polyurethane system demand. EU REACH regulation pullback will also positively impact the industry as the delays to any added complexity or substitution mandates will be reduced.

- North America held approximately 19.4% market share in 2025, valued at around US$5.50 billion, supported by construction insulation, automotive seating, furniture foam, coatings and domestic MDI capacity expansion.

- Rigid Foam was the largest application segment in 2025, accounting for around 39.3% share, valued at approximately US$12.84 billion, driven by building insulation, cold-chain, appliances and industrial thermal protection.

- Building and Construction led the end-user segment in 2025 with nearly 36.8% share, valued at approximately US$10.43 billion, driven by energy-efficiency regulations, insulation upgrades and demand for PU and PIR panels.

- Aliphatic Isocyanates are projected to be the fastest-growing type, with an estimated CAGR of 4.2% during 2026–2035, supported by premium coatings, automotive refinishing, adhesives, sealants and low-VOC polyurethane systems through 2035, supported by demand for advanced visualization, AI-assisted imaging and complex structural heart guidance.

Isocyanates Industry Scope

| Metrics | Details | |

| 2025 Market Size | US$ 28.35 Billion | |

| 2035 Projected Market Size | US$ 48.92 Billion | |

| CAGR (2026-2035) | 5.6% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Type | Methylene Diphenyl Diisocyanate, Toluene Diisocyanate, Aliphatic Isocyanate, and Others | |

| By Manufacturing Process | Phosgenation Process and Nonphosgenation Process | |

| By Application | Rigid Foam, Flexible Foam, Paints and Coatings, Adhesives and Sealants, Elastomers, and Binders | |

| By End-User | Building and Construction, Automotive, Healthcare, Furniture, and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

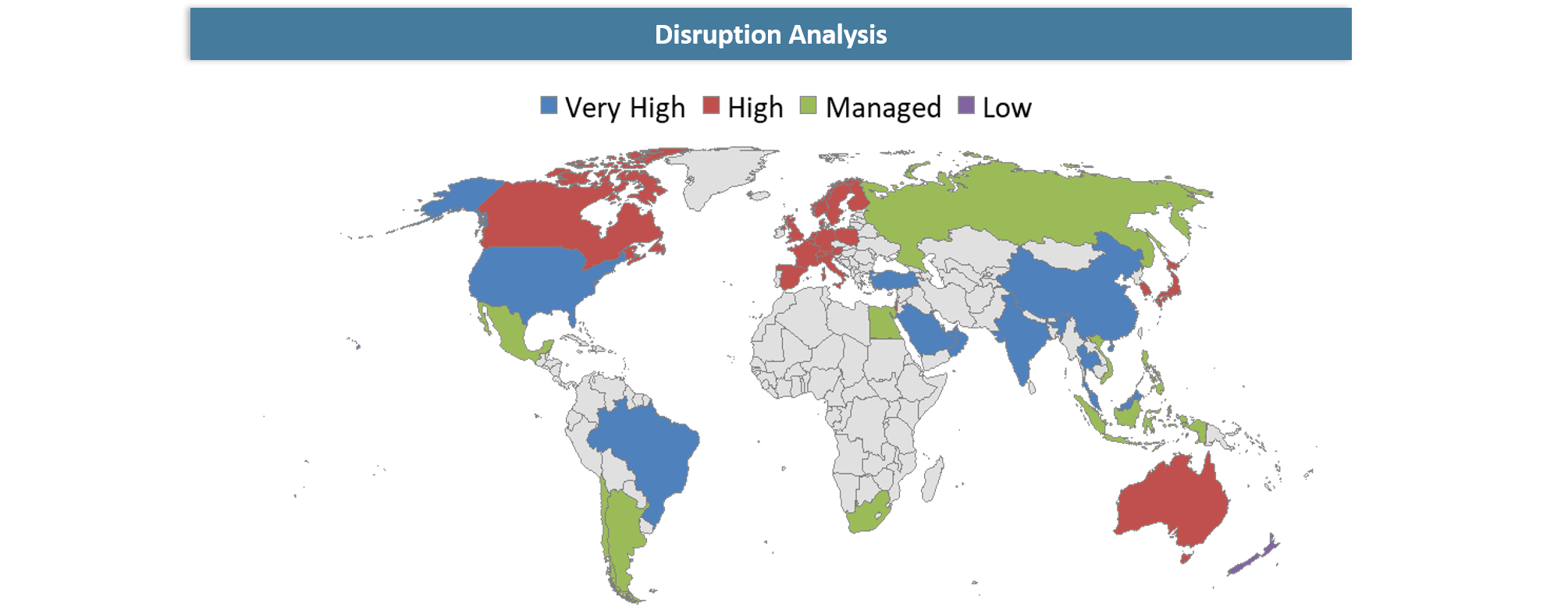

Disruption Analysis

Safety, Sustainability and Specialty Chemistry Are Redefining Isocyanate Demand

Disruption of the isocyanates market is taking place due to the transition from volume-based polyurethane production through conventional means to more sustainable alternatives that do not emit high levels of pollutants and pose risks to health. More stringent regulations concerning worker safety during the manufacture of diisocyanates are compelling suppliers to offer low-free-monomer products. Handling and storage systems that comply with these strict regulations will play an important role as demand for safe practices increases. Suppliers will have to be prepared for these new conditions as buyer priorities evolve to include compliance with environmental standards and other requirements beyond price and performance alone. Increasing concern about polyurethane waste is making chemical recycling, use of mass balance raw materials and alternatives to isocyanate polyurethanes more attractive. Increased price fluctuations in benzene, toluene, aniline and phosgene-related supply chains are impacting the price stability of MDI and TDI. Specialty products like aliphatic isocyanates for automotive paints and adhesives will attract increasing interest due to performance and margin improvements.

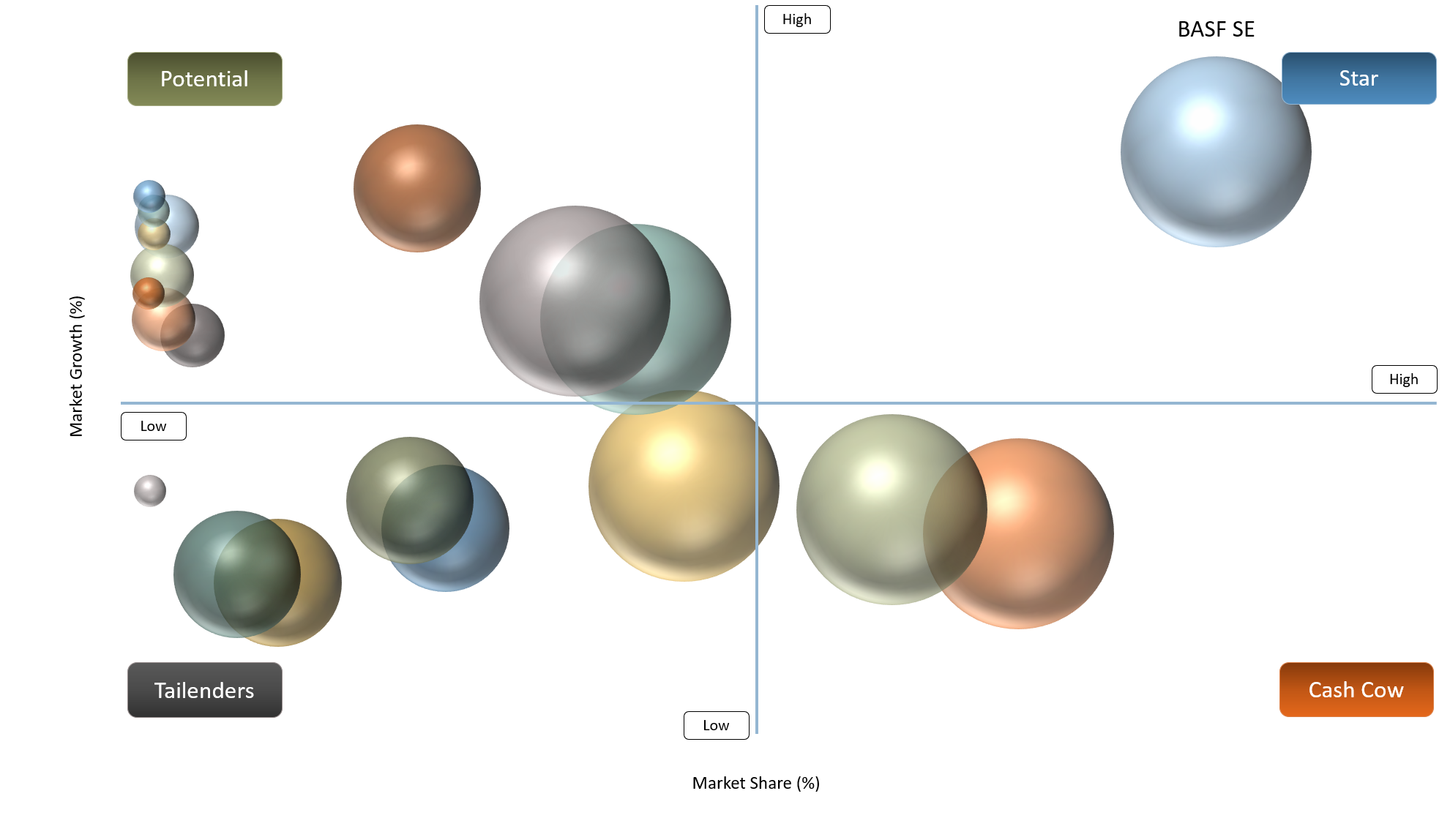

BCG Matrix: Company Evaluation

In Isocyanates Market, companies such as BASF SE, Covestro AG, Wanhua Chemical Group Co., Ltd., Huntsman Corporation and Dow Inc. may qualify as Stars due to their extensive MDI, TDI and Specialty Isocyanates products, global customer coverage and integrated offerings in polyurethanes, coatings, adhesives and industrial applications. Such players have potential to benefit from increased growth in construction insulation, automotive lightweighting, furniture foam and advanced polyurethane formulations.

Players including SABIC, Tosoh Corporation, Mitsui Chemicals, Inc. and Kumho Mitsui Chemicals, Inc. could fall into the Cash Cows category owing to their presence in select geographies, consistent feedstock demand for polyurethanes and well-established customer relationships with industries. Competitive advantages will depend on their reliability of supply, economies of scale and established relationships within the regional chemical value chains in Asia and Middle East regions.

The company categories of Question Marks include Evonik Industries AG, Asahi Kasei Corporation, Perstorp Group and Vencorex due to their focus on growth in specialty Aliphatic isocyanates, cross-linkers and coating applications. Premium profit margins will be driven by ongoing technological differences.

Companies like BorsodChem Zrt. and OCI Company Ltd. may be regarded as Niche Players.

Market Dynamics

Rising demand for isocyanate among end-user industries is driving the market share for the product

Building and construction, automotive, health care, and aerospace are just a few of the major end-user industries for isocyanates that boost the product's market share.

One of the primary drivers driving the market's growth is significant growth in the automobile sector, accompanied by growing industrialization worldwide, particularly in emerging economies. Furthermore, the construction industry's growing adoption of isocyanate-based products is helping to drive market expansion.

Because of their outstanding insulation characteristics, isocyanates are utilized in rigid PU foams to insulate panels and gap fillers in the surrounding doors and windows. It is also utilized on the exterior components of vehicles to reduce total vehicle weight and increase fuel efficiency.

The worldwide isocyanates market is predicted to grow faster than the paints and coatings sector. Isocyanates are frequently employed in producing paints, varnishes, and elastomers. Hexamethylene diisocyanate (HDI) and isophorone diisocyanate are commonly used in automotive paints. As a result, increased vehicle production is likely to contribute to market growth.

Isocyanates are also primers or adhesives and produce flexible and rigid foams and fibers. Methylene diphenyl diisocyanate (MDI) and toluene diisocyanate (TDI) are used as adhesives and sealants because of their weather resistance. The use of methyl isocyanate (MIC) in insecticides has increased its use in the agricultural sector. Thus improving demand for isocyanate among various end-users is boosting the market share for the product.

Hazardous Exposure Risks and Stringent Regulations Are Limiting Market Flexibility

The dangers of using isocyanates represent one of the major obstacles in the market development owing to the possibility of causing respiratory irritation, skin sensitization, occupational asthma, among other issues at workplaces where they are not used appropriately. Consequently, manufacturers and formulators, as well as subsequent users, face additional demands on their compliance with the necessary exposure limits, labeling, storage, transport, employee training, and personal protection equipment requirements. These factors lead to an increase in costs in production processes, in particular, for smaller polyurethane processors which cannot afford sophisticated safety technologies. Moreover, customers in such applications as coatings, adhesives, sealants, and foams are looking for alternative or low free monomer isocyanate systems to minimize hazards while using the materials. Though there is no easy replacement of isocyanates in many polyurethanes, tighter regulations and enhanced safety requirements are hindering their implementation into certain sectors.

Segmentation Analysis

The Global Isocyanates Market is segmented based on type, manufacturing process, application, end-users, and region.

Rigid Foam Anchors Isocyanate Demand as Energy Efficiency Becomes a Regulatory Priority

The rigid foam segment has proven to be the most significant one in terms of application in the isocyanates market since it relates directly to MDI demand and energy-saving construction, cold chain infrastructure, household, and industrial insulation. Rigid polyurethane/polyisocyanurate (PU/PIR) is an essential raw material used for producing rigid PU and PIR foam insulation, which, as BASF suggests, contributes to energy saving in buildings and appliances due to insulation by pMDI. Therefore, the segment proves to be strategically important due to its relation to the focus on energy savings. Indeed, it has been revealed that about 40% of total energy consumption in buildings happens in Europe. Moreover, 80% of energy consumption in European households goes to heating and cooling purposes, thus making it important to increase the efficiency of insulation materials. As for isocyanate producers, rigid foam provides a stable demand for their products with a high link to regulations concerning insulation and high demand resilience compared to discretionary segments.

Geographical Penetration

Asia-Pacific’s Polyurethane Manufacturing Scale Positions It as the Fastest-Growing Isocyanates Market

The Asia-Pacific region is predicted to grow at the highest CAGR in the isocyanates market due to its substantial polyurethane manufacturing capabilities, increasing construction demand, automobile manufacturing activities, and high demand for both rigid and flexible foams. Asia is currently the largest consumer of polyurethane. As per BASF's analysis, Asia represents almost 60% of the total global polyurethane market and hence becomes the largest consumption base for MDI & TDI.

China continues to remain the key strategic region because of its large MDI and TDI capacity additions, whereas India and Southeast Asia are adding marginal demand through the use of rigid and flexible foams in insulation applications, furniture, footwear, household appliances, coatings, and adhesives. In addition, capacity expansions in MDI by China's Wanhua Chemical company, whose MDI capacity may reach 4.5 million tons/year from its current capacity of 3.8 million tons/year following the company's expansion in Fujian.

Automotive demand is another factor driving the region's growth, wherein India's automobile production is estimated to be 25.9 million units in FY2024.

Japan Isocyanates Market Trends

The Japanese market represents an advanced yet strategically important market for isocyanates owing to the demand driven by high-end polyurethane-based products such as those utilized in automotive interiors, appliances, paints, adhesives, elastomers, and energy-saving building materials. While the demand is lower compared to that seen in markets such as China and India, the key strength in the Japanese market is the precision engineering and quality-driven formulation needs in end-use applications. The automotive industry represents a major application driver where Japan manufactured 8.23 million motor vehicles in 2024 for polyurethane use in seating, insulation, acoustic materials, adhesives, and other lightweight automotive interior parts.

Another demand driver is represented by building energy efficiency regulations. The revised Building Energy Efficiency Act requires energy-saving compliance on new residential and non-residential buildings since April 2025, making way for improved insulation material needs, including rigid polyurethane foam systems. From the supply side perspective, Tosoh represents a significant company for isocyanates through MDI and blends for polyurethanes while the Japanese specialty chemicals segment supports coating, elastomer, and adhesives segments. In essence, Japan offers stable growth through regulation-compliant and specialty polyurethane application demands.

U.S Isocyanates Market Overview

The U.S. Isocyanates Market is set to retain its status as one of the strategically important markets in North America, thanks to construction insulation, automobile interior, furniture foam, home appliances, coatings, adhesives, and elastomers. Growth is largely associated with the consumption of polyurethanes since polyurethanes are synthesized from the reaction of polyols with either diisocyanate or polymeric isocyanate; the share of flexible polyurethane foams constitutes approximately 30% of the North American market, which is used primarily for bedding, furniture, and automobiles.

The construction sector remains an important source of demand for MDI-based rigid foam insulation. As per the latest data released by the U.S. Census Bureau, the construction industry recorded an expenditure of US$2,185.5 billion during March 2026 at a seasonally adjusted annual rate.

In terms of production, the planned capacity increase to around 600,000 metric tons annually by BASF in its Geismar, Louisiana MDI plant facility is likely to boost supply stability for MDI in North America.

Competitive Landscape

Isocyanates Market Analysis highlights high consolidation levels where competition is driven by integrated chemical manufacturers having access to upstream raw materials, capacity for both MDI and TDI, as well as the ability to formulate polyurethane systems. BASF SE, Covestro AG, Wanhua Chemical Group Co., Ltd., Huntsman Corporation and Dow Inc. continue to be key industry competitors on account of their diversified product offerings, formulation expertise and broad reach into construction, automotive, furniture, coatings and industrial sectors.

Regional competition in Asia-Pacific is gaining momentum from local participants like Wanhua Chemical Group, Tosoh Corporation, Mitsui Chemicals, Kumho Mitsui Chemicals and OCI Company Ltd., owing to rising regional supply concerns amidst Asia-Pacific being the largest consumer base of polyurethanes. Competition from specialty players such as Evonik Industries, Asahi Kasei, Perstorp Group and Vencorex takes place through the use of aliphatic isocyanates, HDI, IPDI and specialty crosslinking technologies.

Industry competition is gradually moving away from bulk volumes towards safety concerns, free monomer levels, supply concerns, sustainable market positioning and application-specific polyurethane systems.

Recent Developments

- March 2026: BASF announced a US$500 per metric ton price increase for Lupranate MDI and Lupranate TDI in East Asia, excluding Mainland China, reflecting sustained raw material, transportation and energy cost pressure across the isocyanates value chain.

- February 2026: BASF increased prices for Lupranate MDI basic products by US$200 per metric ton in ASEAN countries, indicating tighter supply conditions and continued pricing pressure in regional polyurethane feedstocks.

- December 2025: Huntsman reported an unplanned outage at its Rotterdam Polyurethanes facility, with the larger of two MDI lines affected and expected to resume production by mid-December, highlighting supply reliability risks in European MDI production.

- October 2025: Wanhua Chemical’s Fujian MDI technology-upgrading and capacity-expansion project received EIA approval, with the project designed to upgrade the existing 800 kt per year MDI plant to 1.5 million tons per year capacity.

- August 2025: Covestro expanded its specialty isocyanate footprint by acquiring former Vencorex sites in the U.S. and Thailand, strengthening its aliphatic isocyanates position for coatings and adhesives applications.

- January 2025: Wanhua Chemical completed and accepted major MDI-related capacity projects, including a 1.8 million tons per year MDI technical transformation project, supporting stronger production scale and modified MDI availability.

AI Impact Analysis

The impact of AI on the Isocyanates Market will include increased production efficiency, safety surveillance, formulation innovation, and demand forecasting. Regarding production process, the implementation of AI technology will allow producers to adjust reactions and increase efficiency while minimizing energy consumption during MDI, TDI, and specialty isocyanates manufacturing processes. At the same time, for downstream applications involving polyurethanes, AI will allow predicting properties such as density, curing, coating durability, adhesive power, and elastomer performance.

Furthermore, artificial intelligence allows for safer operation by detecting worker exposure risks and abnormal reactions, as well as by supporting predictive maintenance in chemical plants with high risk factors. Concerning commercial activities, forecasting tools based on artificial intelligence allow suppliers to monitor demand changes in various sectors that include building construction, automotive, furniture, coating, adhesive, and appliance markets. Companies utilizing artificial intelligence for formulation intelligence, demand forecasting, and compliance management will be capable of achieving enhanced cost controls and more efficient innovation processes.

White Space Opportunities

White space opportunities in the isocyanates market exist for suppliers with safer handling formulations and low free monomer options due to increasing stringent worker safety and labeling regulations. Differentiation from pure pricing wars would be possible by offering compliance-ready MDI, TDI and aliphatic isocyanates. Aliphatic isocyanates for high performance coatings such as automotive refinishes, industrial protective coatings, marine coatings, as well as weatherable finishes represent another valuable opportunity. Rigid Polyurethane Foam for energy-saving buildings, cold chain facilities, and appliance insulation represents another significant market segment driven by energy efficiency considerations. EV production brings new opportunities for polyurethane adhesives, sealants, elastomers, acoustic insulation, as well as adjacent parts for batteries. At the same time, customers are increasingly interested in circular polyurethane products, including chemical recycling, mass balance raw materials and lower carbon systems. New manufacturing centers in India, Southeast Asia, and the Middle East also offer unexploited potential for isocyanate producers.

DMI Opinion

Isocyanates Market transition from a market for commodity chemicals to one that will drive demand based on performance, regulatory compliance, and end-user application development. Demand will continue to be driven by MDI and TDI due to rigid and flexible polyurethane foam applications, however, the greatest growth will be in specialty isocyanates, low free monomer content, and pre-formulated polyurethane products.

DMI feels that suppliers that can balance the ability to provide consistent access to raw materials, regulatory benefits, product expertise, and safer handling grades of products will win greater buyer preference. The key demand segments are construction insulation, lightweighting in autos, furniture cushioning, appliances, coatings, adhesives, and elastomers; however, growth in margins will increasingly become reliant on premium applications.

In future years, companies will be well positioned for growth in the Isocyanates Market if they align themselves with innovations associated with energy efficiency, safety, low emission chemistry, and circular polyurethanes.

Why This Report Matters in 2026?

The Isocyanates Market will experience an evolution in its purchase process in 2026, with growth being generated not only through bulk demand for MDI and TDI but also from preparation for regulatory requirements, product performance and material security. Applications such as construction insulation, vehicle lightweighting, furniture foams, appliance insulation, coatings, adhesives and elastomers will sustain demand, but buyers are also taking into account their partner's safety, compliance, formulation expertise and availability.

This market study becomes significant in that it can assist companies in determining areas of value in the polyurethane economy. Rigid foams will remain key to energy savings and refrigeration, with aliphatic isocyanates increasingly becoming important in high-value coatings and polyurethane specialties. Simultaneously, the fluctuating price environment, tightening regulations on diisocyanates and pressures around PU recycling will influence procurement strategies.

For manufacturers, distributors, formulation businesses and investors, this study will provide actionable insight into areas of growth, risk, competition, application-based demand and commercialization in the dynamic Isocyanates Market.

Why Choose DataM?

- Application-Level Market Intelligence: DataM provides detailed insights across rigid foam, flexible foam, paints and coatings, adhesives and sealants, elastomers and binders, helping clients understand where isocyanate demand is actually scaling.

- Commercially Feasible Segmentation: Our segmentation is built around measurable revenue pools such as type, manufacturing process, application, use cases and end-user industries, reducing overlap and improving market-sizing accuracy.

- Competitive and Value Chain Mapping: DataM tracks direct isocyanate producers and adjacent polyurethane ecosystem players across MDI, TDI, aliphatic isocyanates, polyols, PU systems, coatings, adhesives and insulation materials.

- Decision-Ready Strategic Add-Ons: Clients receive actionable insights such as BCG matrix, white space opportunities, raw material impact analysis, recent developments, market dynamics and procurement priorities to support business planning.

- Client-Specific Growth Support: DataM helps companies identify high-growth applications, priority geographies, potential partners, specialty product opportunities and commercialization routes across the evolving Isocyanates Market.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Isocyanates Market prioritize consistent MDI, TDI and aliphatic isocyanate quality, as even small variation in purity, reactivity and moisture sensitivity can affect polyurethane foam density, coating durability, curing performance and final product consistency.

- Regulatory compliance is a major evaluation factor, with customers assessing supplier documentation, safety data sheets, diisocyanate handling guidance, worker exposure controls and alignment with regional chemical regulations.

- Supply reliability is critical because isocyanates are core feedstocks for polyurethane production, and disruptions can directly affect construction insulation, automotive seating, furniture foam, coatings, adhesives and elastomer manufacturing.

- Buyers increasingly prefer suppliers that offer low-free-monomer, low-VOC and safer-handling formulations, especially for coatings, adhesives, sealants and other applications exposed to stricter workplace safety standards.

- Technical formulation support is becoming a strong differentiator, as customers require help with processing stability, curing speed, foam performance, coating adhesion, weather resistance and end-use customization.

- Price competitiveness remains important, but buyers are evaluating total cost of ownership, including yield efficiency, processing losses, compliance cost, storage requirements, safety training and downstream performance benefits.