Insulin Patch Pump Market Overview

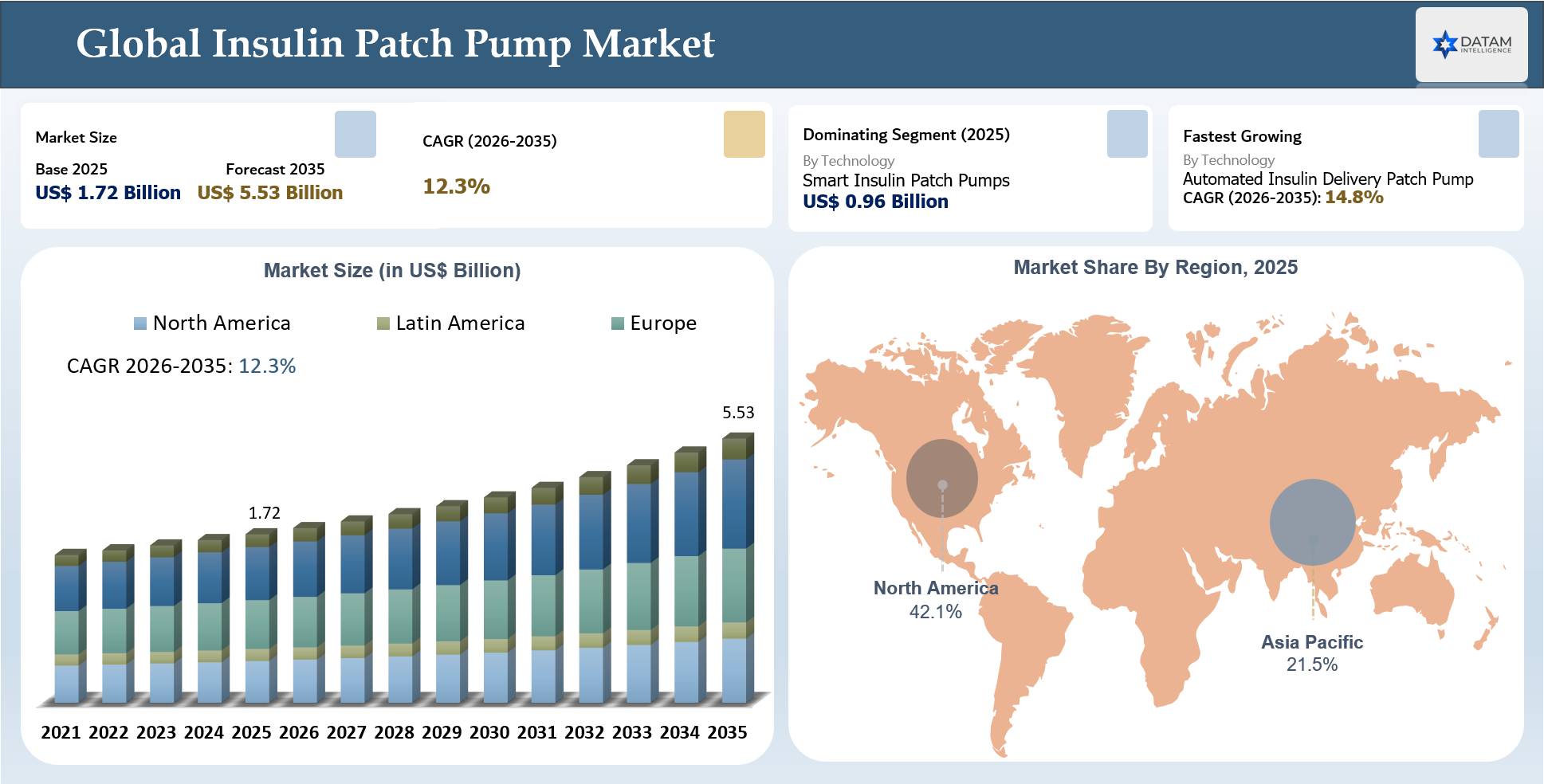

The global insulin patch pump market stood at US$ 1.72 billion in 2025 and is expected to reach US$ 5.53 billion by 2035, growing with a CAGR of 12.3% during the forecast period 2026-2035.

The global insulin patch pump market is witnessing an inflection point due to the penetration of large diabetes technology companies in the development of automated, tubeless insulin pumps. The notable development in this regard will include Medtronic’s MiniMed Fit insulin patch pump that will be submitted to the FDA by the fall of 2026. It is significant from a strategic perspective since it shows the shift from traditional pump wars towards smaller insulin pumps that are wearable and connected to continuous glucose monitoring sensors, as well as algorithms. The key reason behind this significance is the fact that it is not only a product launch event, but also a competitor reset.

Such progress might help boost innovation efforts related to technology miniaturization, rechargeable battery technology, dose accuracy, interoperability, patient experience, and digital diabetes treatment management. This advancement might add more pressure on incumbent companies to improve the evidence, payer coverage, post-market reliability, and software capabilities. Furthermore, procurement assessments will evolve from mere convenience of tubeless pumps to comprehensive platform advantages encompassing performance of the automatic insulin delivery system, compatibility with CGM technology, cybersecurity features, user-friendliness, payer suitability, and overall therapeutic effect. Companies that combine the convenience of the patch pump solution with reliable automation technology are likely to succeed.

Key Takeaways

- The Global Insulin Patch Pump Market was valued at US$ 1.72 billion in 2025 and is projected to reach US$ 5.53 billion by 2035.

- The market is expected to grow at a CAGR of 12.3% during 2026-2035, supported by rising diabetes burden, tubeless insulin delivery adoption, CGM integration, and automated insulin delivery growth.

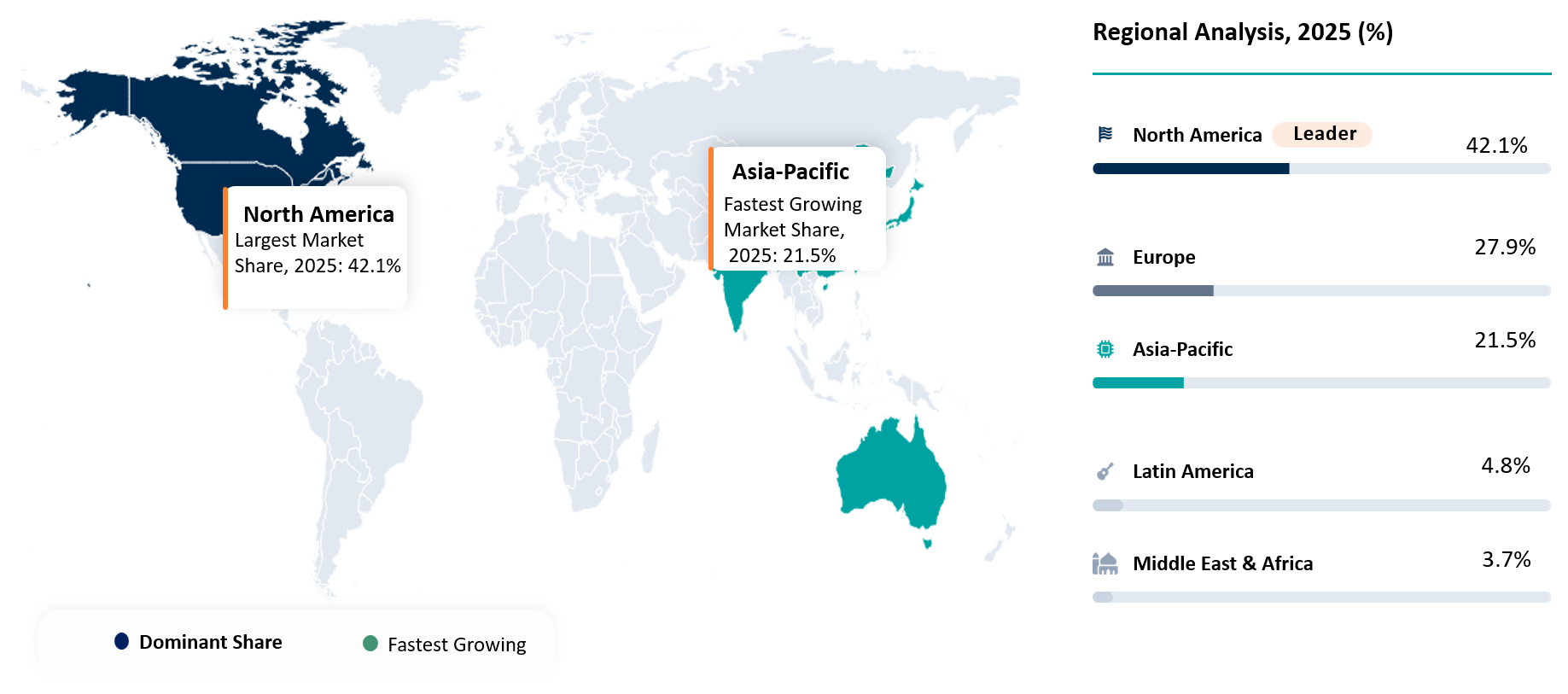

- North America held the highest market share at 42.1% in 2025, supported by advanced diabetes care infrastructure, reimbursement access, strong CGM usage, and early adoption of connected insulin delivery systems.

- Asia-Pacific is expected to be the fastest-growing region, driven by a large diabetes population, rising healthcare spending, expanding digital diabetes care adoption, and increasing demand for affordable wearable insulin delivery devices.

- Smart Insulin Patch Pumps dominated the technology segment in 2025, valued at approximately US$ 0.96 billion, supported by app-enabled control, dosing flexibility, patient convenience, and improved therapy adherence.

- Automated Insulin Delivery Patch Pumps are projected to be the fastest-growing technology segment, expanding at an estimated 14.8% CAGR during 2026-2035, driven by CGM integration and algorithm-based insulin adjustment.

- Procurement decisions are increasingly based on dosing accuracy, adhesive reliability, reservoir capacity, wear duration, CGM compatibility, app usability, reimbursement support, and post-market safety performance.

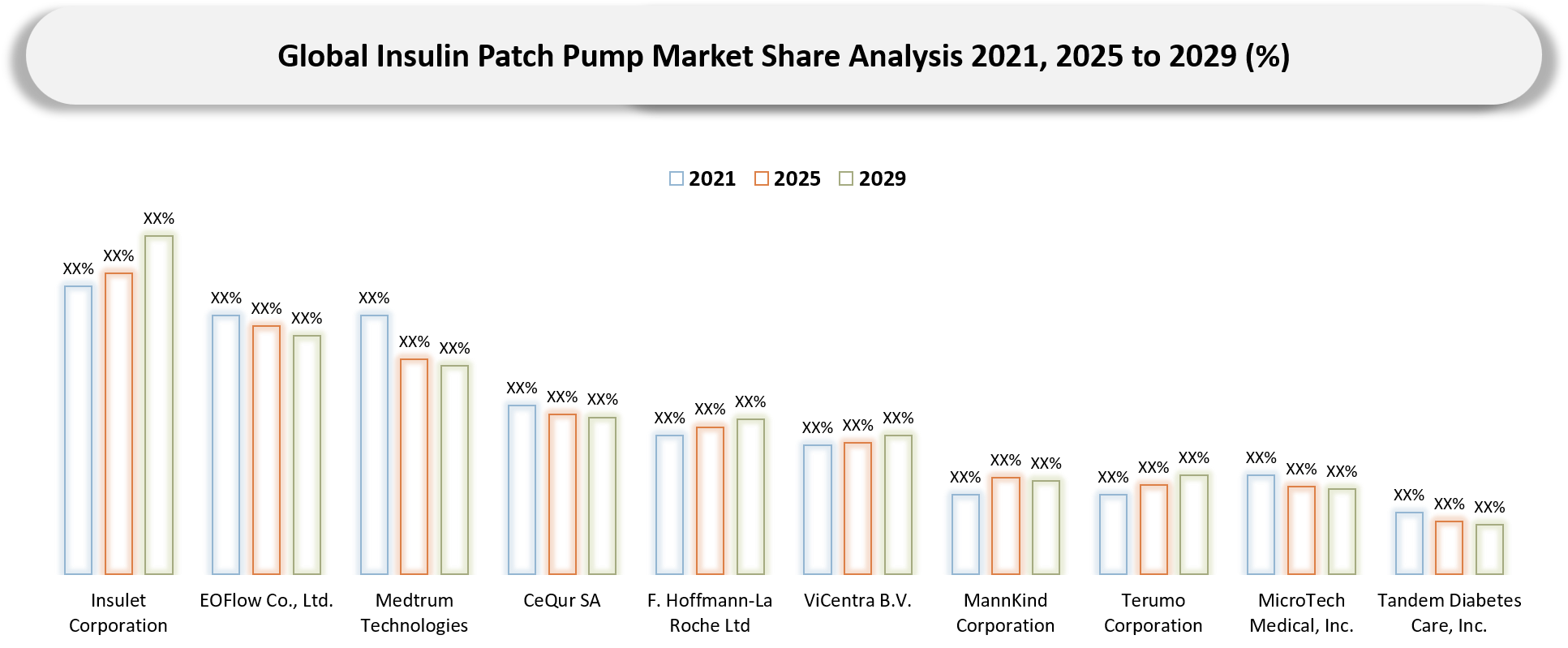

- The market has strong competitive intensity, with major players including Insulet Corporation, EOFlow Co., Ltd., Medtrum Technologies, CeQur SA, F. Hoffmann-La Roche Ltd, ViCentra B.V., MannKind Corporation, Terumo Corporation, MicroTech Medical, Inc., and Tandem Diabetes Care, Inc.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 1.72 Billion | |

| 2035 Projected Market Size | US$ 5.53 Billion | |

| CAGR (2026-2035) | 12.3% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Product Type | Disposable Patch Pumps, Reusable Patch Pumps, Hybrid Patch Pumps, and Others | |

| By Pump Design | Tubeless Patch Pumps and Semi-Tubeless Patch Pumps | |

| By Insulin Delivery Mode | Basal Insulin Delivery, Bolus Insulin Delivery, and Basal-Bolus Insulin Delivery | |

| By Technology | Manual Insulin Patch Pumps, Smart Insulin Patch Pumps, Automated Insulin Delivery Patch Pumps, and Others | |

| By Reservoir Capacity | Below 200 Units, 200 To 300 Units, and Above 300 Units | |

| By Wear Duration | Up To 3 Days, 4 To 7 Days, and Above 7 Days | |

| By Diabetes Type | Type 1 Diabetes, Type 2 Diabetes, Gestational Diabetes, and Others | |

| By Age Group | Pediatric, Adults, and Geriatric | |

| By Connectivity | Bluetooth-Enabled Patch Pumps, App-Controlled Patch Pumps, Cloud-Connected Patch Pumps, Non-Connected Patch Pumps, and Others | |

| By Use Case | Daily Insulin Management, Intensive Insulin Therapy, Home-Based Diabetes Management, Pediatric Diabetes Management, Hospital-Based Insulin Therapy, Remote Diabetes Monitoring, and Others | |

| By End User | Hospitals, Diabetes Clinics, Homecare Settings, Ambulatory Care Centers, and Others | |

| By Distribution Channel | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, and Direct Sales | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

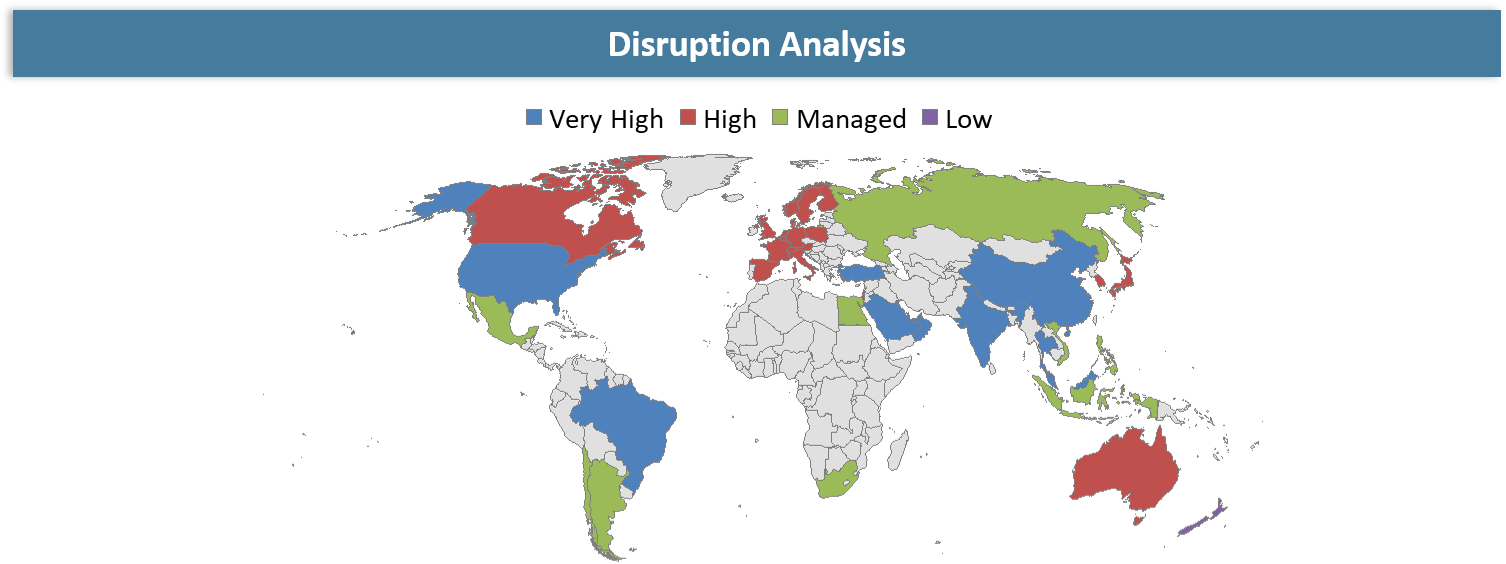

Disruption Analysis

Wearable Automation and Connected Care Are Redefining Competitive Advantage in Insulin Delivery

Disruption is occurring in the global insulin patch pump market due to the shift from traditional methods of insulin delivery towards more advanced and automated systems that integrate technology and connectivity to support insulin delivery. The tubeless insulin delivery patches are disrupting the market by providing an alternative method of insulin therapy without needing frequent injection or the use of tubed pumps. The integration of continuous glucose monitoring with patch pumps is shifting the focus from simply providing an insulin delivery device towards optimizing the therapy process with automation.

The buyers’ requirements have also been changing and, together with the increased regulatory scrutiny and challenges in obtaining reimbursement, creating an environment of disruption within the patch pump market. Payers and healthcare providers are beginning to measure the impact of using patch pumps on improving outcomes, patient adherence, preventing hypoglycemia and lowering the costs of treating diabetes. However, recalls, cybersecurity threats, reimbursement issues, and affordability may present hurdles to entering and gaining traction in the market. Vendors that combine regulatory credibility, scalable manufacturing, clinical evidence, CGM compatibility, remote monitoring and strong payer engagement will be better positioned to convert disruption into sustainable market leadership.

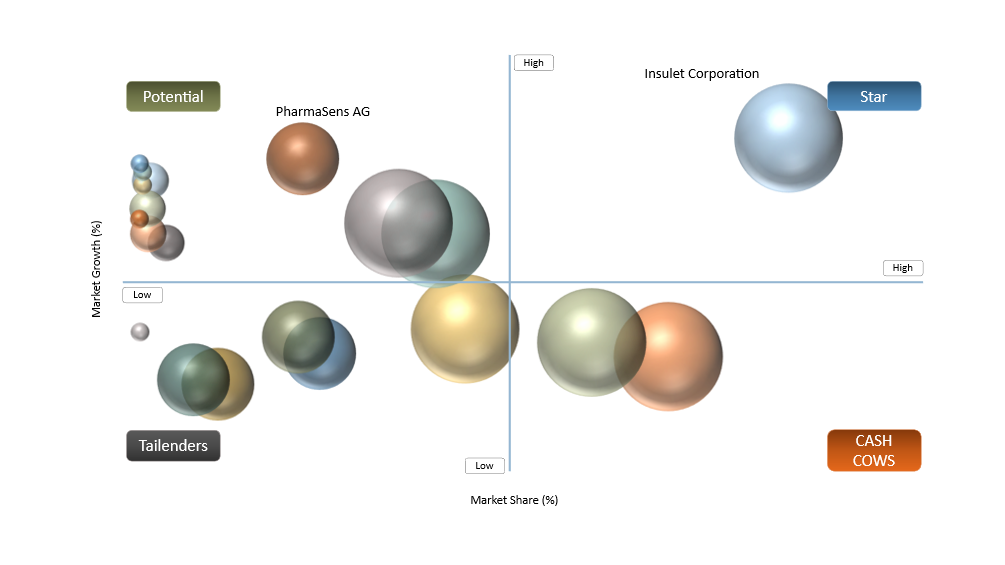

BCG Matrix: Company Evaluation

As for the BCG matrix, In the global insulin patch pump market, Stars refer to firms that have strong visibility from a business perspective, possess product platforms that are scalable, established patch pumps, wide positioning in the field of diabetes technology as well as brand influence amongst their target markets. Insulet Corporation is clearly a Star in the market owing to its Omnipod tubeless insulin delivery system, global operations, automated insulin delivery capacity as well as positioning in type 1 diabetes and insulin-dependent Type 2 diabetes. EOFlow Co., Ltd. and Medtrum Technologies are clearly high growth stars or emerging stars in the industry on account of their wearables patch pump technology, tubeless insulin delivery systems and significance in connected diabetes care.

Cash Cow is an organization that has earned a reputation for credibility in terms of its medical devices and has mature portfolios when it comes to diabetes, experience in terms of regulations, and a defendable position when it comes to insulin administration devices regardless of whether it uses the patch pump technology alone. The organizations F. Hoffmann-La Roche Ltd, Terumo Corporation, MannKind Corporation, MicroTech Medical, Inc., and Tandem Diabetes Care qualify for classification as cash cows because of their reputation in diabetes devices, product dependability, brands, and their capability to deliver devices to hospitals, clinics, and home users.

Question Marks comprise firms with good technology of patch pumps or platforms but relatively lesser commercial potential. CeQur SA, ViCentra B.V., Debiotech S.A., SFC Fluidics, Inc., PharmaSens AG, SOOIL Development Co., Ltd. and Medtronic MiniMed, Inc. qualify for being Question Marks based on their stages of commercialization, availability of products, development of technology and competitiveness. They will be able to make the move into the Stars segment based on various parameters such as CGM capabilities, reimbursement possibilities, automated insulin administration and scalability.

Market Dynamics

Shift From Multiple Daily Injections to Tubeless Wearable Insulin Delivery

The Global Insulin Patch Pump Market is seeing significant impetus from the move towards moving from daily injections to discreet, tube-less and wearable insulin delivery options. For many diabetics, daily injections are cumbersome, cause fatigue, provide a burden on dosing and adherence, and also lead to social issues due to the nature of their application. The use of insulin patch pumps addresses these issues by providing a means of delivering insulin continuously through wearable devices, thus minimizing the number of injections required daily.

Commercially, the move has seen the adoption of insulin patch pumps evolve from being a high-end diabetic device to being one that facilitates the improvement of adherence. In evaluating patch pumps commercially, hospitals, endocrinologists, payers and homecare services are now assessing devices on their comfort factor, precision in dosing, ease of learning how to operate the devices, and ability to support therapy over time. With diabetes management moving increasingly towards home care environments, tube-less wearable insulin delivery becomes an important differentiator.

Device Reliability Concerns, Adhesive Performance Issues and Recall Risks Are Increasing Buyer Caution

The reliability of a device represents a physical limitation in the Global Insulin Patch Pump Market, given that the device is responsible for controlling insulin administration and cannot afford any tolerance towards failure. Consumers are growing wary of such factors as occlusion, insulin leakage, faulty pod operation, battery functioning, alarm system malfunction, software-related problems, consistency at infusion sites, adhesive detachment, and irritation of the skin. All the aforementioned problems might be hazardous to health, impact adherence to therapy, and make physicians less confident. Therefore, the criteria for selecting vendors are moving beyond convenience for hospitals, clinics, and payers.

A recent example is Insulet Corporation’s 2026 voluntary medical device correction for certain Omnipods after a manufacturing issue created potential insulin under-delivery or leakage risk. The FDA notice stated that around 7 million pods were included in the action, representing about 8.5% of 2025 global Omnipod pod production, with 24 serious adverse events reported globally and no deaths. This highlights why procurement teams increasingly prioritize robust manufacturing controls, transparent safety communication, reliable replacement programs and proven field performance before scaling patch pump adoption.

Segmentation Analysis

The global insulin patch pump market is segmented based on the product type, pump design, insulin delivery mode, technology, reservoir capacity, wear duration, diabetes type, age group, connectivity, use case, end-user, distribution channel, and region.

Smart and Automated Patch Pumps Are Redefining Technology Leadership in Insulin Delivery

By technology, Smart Insulin Patch Pumps dominate the Global Insulin Patch Pump Market in 2025, supported by their strong balance of usability, connectivity, dosing flexibility, and patient convenience. The segment is estimated at US$ 0.96 billion in 2025, representing a major share of the total market value of US$ 1.72 billion. Smart patch pumps are gaining preference because they address key patient and clinician needs, including simplified insulin administration, app-based control, improved therapy tracking, discreet wearability, and better adherence compared to multiple daily injections.

The fastest-growing technology segment is Automated Insulin Delivery Patch Pumps, expected to grow at a CAGR of 14.8% during 2026–2035, ahead of the overall market CAGR. Growth is being driven by increasing integration with continuous glucose monitoring, algorithm-based insulin adjustment, remote monitoring, and rising demand for low-intervention diabetes care. As buyers shift toward outcome-driven diabetes management, automated patch pumps are expected to capture stronger adoption among Type 1 diabetes users, insulin-requiring Type 2 diabetes patients, pediatric users, and homecare settings.

Geographical Penetration

North America Leads the Insulin Patch Pump Market as Reimbursement Strength, CGM Adoption and Automated Delivery Scale Commercial Access

The North American region is the leading contributor to the global insulin patch pump market, with a share of 42.1%, due to its advanced infrastructure for diabetes care, better awareness about wearable insulin pumps, and adoption of connected diabetes management solutions. There is significant maturity in the field of endocrinology, well-structured diabetes management programs, prevalence of CGM technology, and inclination towards tube-less insulin delivery systems among insulin-dependent people in this region. With increasing preferences for convenient insulin delivery solutions that can alleviate the pain and discomfort associated with daily insulin injections, patch pumps are becoming more relevant.

Moreover, this regional market is fueled by better receptiveness to innovative technologies, prominent presence of top diabetes technology companies, and the convergence of CGMs, smartphone apps, insulin patch pumps, and automated dosing algorithms among other factors. Hospitals, diabetes centers, insurers, and home health care providers are focusing on evaluating various insulin patch pumps based on the aspects of reliable dosing, treatment adherence, comfort of wear, ease of training and learning, reimbursement possibilities, and overall therapeutic value of devices. However, recurring cost of pods, safety of devices, poor adhesion properties, and insurer concerns still present major hurdles. Vendors with robust technologies.

U.S Insulin Patch Pump Market Trends

The U.S. insulin patch pump market is shifting from niche Type 1 diabetes adoption toward broader insulin delivery use, supported by automated insulin delivery, CGM integration, and patient preference for tubeless therapy. A major trend is expansion into insulin-requiring Type 2 diabetes, after Insulet’s Omnipod 5 became FDA-cleared in 2024 for adults with Type 2 diabetes, broadening the eligible user base beyond traditional pump users. This is important because the CDC notes that about 1 in 8 Americans has diabetes, with most cases being Type 2 diabetes.

Commercial momentum is also strengthening around pharmacy access, app-enabled care, and connected dosing platforms. Insulet reported U.S. Omnipods revenue of US$515.6 million in Q1 2026, up 28.3% year-over-year, indicating strong domestic demand for tubeless insulin delivery. At the same time, buyer scrutiny is rising around pod reliability, recalls, adhesive performance, replacement support, and total therapy cost, making post-market safety and payer alignment critical competitive differentiators.

Japan Insulin Patch Pump Market Outlook

Japan’s insulin patch pump market is developing as a premium, patient-centric diabetes technology segment, supported by aging demographics, mature specialist care, and demand for discreet insulin delivery. The country has a meaningful diabetes treatment base, with IDF reporting 8.97 million adults with diabetes in Japan in 2024 and an adult diabetes prevalence of 8.1%. This creates a long-term opportunity for wearable insulin delivery devices that reduce injection burden, improve therapy flexibility, and support home-based diabetes management among patients requiring intensive insulin therapy.

Japan is also strategically relevant because local medical device innovation is supporting patch pump adoption. Terumo’s MEDISAFE WITH is positioned as an insulin patch pump designed for discreet use and remote-controlled insulin administration, aligning with Japan’s preference for compact, high-quality, patient-friendly medical devices. Future adoption will depend on stronger reimbursement support, clinician confidence, CGM integration, training simplicity, adhesive reliability, and evidence showing improved adherence and convenience. Japan is expected to remain a selective but high-value market where trusted domestic players and clinically validated connected insulin delivery platforms can gain stronger commercial relevance.

Competitive Landscape

The Global Insulin Patch Pump Market exhibits moderate concentration, with competitors being characterized by their ability to incorporate wearables manufacturing, insulin dispensing efficiency, software connectivity, and regulatory approval. Insulet Corporation maintains an unassailable competitive advantage within the market due to its Omnipod technology, bolstered by innovations in tubeless devices, automatic insulin dispensation, and widespread adoption by patients suffering from diabetes. Competitors including EOFlow Co., Ltd., Medtrum Technologies, CeQur SA, ViCentra B.V., and MicroTech Medical, Inc. are intensifying competition with innovations in disposable insulin pumps, small devices, application software, and unique dispensing techniques.

The competition is moving away from being about the availability of devices towards being based on their capabilities within an overall diabetes ecosystem. The key attributes of companies are now based on the capabilities of their CGM systems, dosing accuracy, adhesion, reservoir volume, wear time, ease of use, reimbursement capability, scale of manufacture, and safety performance once launched. Companies such as F. Hoffmann-La Roche Ltd, Terumo Corporation, MannKind Corporation, Tandem Diabetes Care, Debiotech S.A., SFC Fluidics, Inc., PharmaSens AG, SOOIL Development Co., Ltd., and Medtronic MiniMed bring more competition due to their experience in diabetes technologies and their clinical networks. Future leadership will depend on automated insulin delivery, Type 2 diabetes expansion, affordability, real-world evidence, and connected care integration.

Recent Developments

- May 2026: Insulet Corporation initiated a voluntary medical device correction for certain Omnipod pods due to potential insulin under-delivery, reinforcing the importance of manufacturing quality, safety monitoring, and post-market surveillance in patch pump adoption.

- May 2026: A U.S. appeals court overturned Insulet’s US$59.4 million trade-secret verdict against EOFlow, reducing legal uncertainty around EOPatch and supporting competitive intensity in wearable insulin pump innovation.

- March 2026: Medtronic MiniMed received FDA clearance for MiniMed Flex, while MiniMed Fit, its AID insulin patch pump with a rechargeable battery, is planned for FDA submission by fall 2026, signaling stronger competitive pressure in next-generation patch pump development.

- April 2026: PharmaSens advanced clinical feasibility work for its all-in-one insulin patch pump integrated with CGM technology, supporting the market shift toward combined insulin delivery and glucose monitoring platforms.

- January 2026: ViCentra expanded its Series D financing to US$98 million to accelerate European commercialization and prepare next-generation Kaleido insulin patch pump access for the U.S. market.

- March 2025: Insulet expanded Omnipod 5 into Australia, Belgium, Canada, and Switzerland, strengthening its global footprint in tubeless automated insulin delivery systems.

- June 2025: PharmaSens and SiBionics collaborated to develop the niia signature all-in-one insulin patch pump with integrated real-time glucose sensing, advancing next-generation connected diabetes care.

- August 2024: Insulet received FDA clearance for Omnipod 5 use in adults with Type 2 diabetes, expanding patch pump relevance beyond Type 1 diabetes into a broader insulin-using population.

AI Impact Analysis

AI is now an integral component in the Global Insulin Patch Pump Market as companies shift from devices-only approaches in insulin delivery to the creation of intelligent diabetes management systems. Algorithms that utilize AI have the potential of improving the personalization of insulin delivery via analysis of glucose trends, insulin administration, eating habits, physical activity, sleeping behaviors, and other factors. Thus, the use of AI enhances the business case of patch pump devices in particular when it comes to automated insulin delivery, which is characterized by accuracy, responsiveness, and fewer human interventions.

In terms of competition, the focus of companies has shifted from being solely on hardware design to device-software functionality due to the role played by AI technology. Businesses with expertise in continuous glucose monitoring integration, cloud-based analytics, software algorithm development, cyber security, and generation of real-world data will likely have greater success winning over payers and clinicians. However, AI adoption also increases regulatory scrutiny around algorithm validation, data privacy, interoperability, liability, and post-market monitoring. As a result, future market leadership will depend on clinically reliable, explainable, secure, and patient-friendly AI-enabled insulin delivery platforms.

White Space Opportunities

Opportunities for White Space within the Global Insulin Patch Pump Market include addressing underserved patient populations, extending the wear time of the patch pump, reducing costs of disposables, and simplifying insulin delivery for Type 2 diabetes. The current user base for patch pumps tends to be concentrated on Type 1 diabetes with greater access to diabetes technology. Thus, an opportunity exists in expanding use in other populations, such as insulin dependent Type 2 diabetics, geriatric patients, pediatric populations, and emerging countries. Manufacturers could pursue differentiation through creating patch pumps which are less expensive and easier to train, and which provide improved adhesion properties and fewer handling steps with alternative reservoirs.

Another key opportunity in the market is found in integration as opposed to discrete product solutions. By integrating their patch pumps with a broader array of capabilities, vendors have opportunities to grow beyond the wearable itself into providing additional support to their healthcare system partners and end-users. Integrating capabilities such as CGM connectivity, automated insulin delivery, remote monitoring capabilities, physician dashboards, and refills would allow for reimbursement support and patient education, thereby providing greater value from the patch pumps themselves. Vendors that position patch pumps as part of a measurable outcomes platform, rather than only a wearable device, can unlock stronger adoption across clinics, homecare programs, and value-based diabetes care models.

DMI Opinion

As per the findings of DataM, the Global Insulin Patch Pump Market is set to enter a phase of high-value transformation, where usage would depend more on convenience, automation, connectivity, and confidence in clinical results rather than simply insulin administration. The patch pumps have much potential for benefiting from the growing trend towards home-based diabetes management, therapy enabled by CGM use, and fewer injections required. Nevertheless, this market will not grow homogenously; instead, its development will be driven by the capabilities of patch pumps in achieving better compliance, reducing therapy complexity and dosing inaccuracies, as well as integrating seamlessly into diabetes technology ecosystems.

The future winners of the Global Insulin Patch Pump Market will be those who offer a combination of features such as no-tube design, effective adhesives, automated insulin administration, favorable reimbursement programs, real-world results, and stable supply chains. Extending treatment of type 2 diabetes with the use of patch pumps presents a significant business opportunity, although pricing and insurance coverage continue to represent key challenges.

Why This Report Matter in 2026?

In 2026, the Global Insulin Patch Pump Market is expected to emerge as a strategically vital industry owing to the shift in diabetes management from injection-based therapy and tubed insulin pumps towards wearable, discreet, and smart insulin delivery devices. The focus of buyers is no longer limited to the basic functionality of delivering the insulin dose, but rather encompasses considerations of comfort, safety, ability to work with continuous glucose monitoring systems (CGMs), mobile application interface, suitability for automated insulin delivery, and the degree of patient engagement that can be fostered through the use of a particular device.

This report provides crucial insights into the evolving demands within Type 1 diabetes, insulin-dependent Type 2 diabetes, pediatric segment, home care setting, and digital diabetes management systems segments. The importance of this report lies in the fact that competition among players is heating up owing to new developments in tubeless design, disposable pod solutions, software-driven therapies, and integrated glucose-insulin ecosystem. It assists manufacturers, investors, payers, distributors, and healthcare facilities in better understanding their market positioning.

Why Choose DataM?

- Insulin Patch Pumps Value Chain Analysis: In-depth analysis of the full value chain for insulin patch pumps, covering medical grade polymers, microfluidics, reservoirs, cannulas, adhesives, batteries, sensors, controllers, software platforms, disposable cartridges, assembly, sterilization, device packaging, distribution, healthcare practitioners, insurers, and end-users.

- Product and Technology Assessment: Examination of key insulin patch pump technology innovations, such as disposable insulin patch pumps, reusable insulin patch pumps, hybrid insulin patch pumps, tubeless systems, semi-tubeless systems, basal-bolus insulin delivery systems, smart insulin patch pumps, automated insulin delivery systems, integrated CGM devices, and app-based insulin delivery devices.

- Application/Uses Cases and End User Assessment: Monitors the demand for insulin patch pumps based on applications such as type 1 diabetes, insulin-dependent type 2 diabetes, diabetes care for children, diabetes treatment for adults, at-home insulin treatment, diabetes clinic treatment, hospital insulin treatment, ambulatory treatment settings, and remote diabetes monitoring.

- Regulatory, Safety and Compliance Assessment: Evaluates the influence of regulatory approval for medical devices, insulin delivery safety considerations, dosing accuracy concerns, biocompatibility, cybersecurity, data privacy, post-marketing surveillance, reimbursement, recall activity, clinical evidence, and regional regulatory approaches on product adoption and market access.

- Competitive Strategy Benchmarking: Monitors leading players such as Insulet Corporation, EOFlow Co., Ltd., Medtrum Technologies Inc., CeQur SA, and F. Hoffmann-La Roche Ltd based on product portfolio strength, patch pump innovation, CGM compatibility, automated insulin delivery capability, regulatory presence, geographic reach, clinical adoption, pricing strategy, reimbursement access, and partnership strategy.

- Insulin Patch Pump Pricing, Procurement and Market Access: Emphasizes patient requirements, payer reimbursement, reimbursement methods, procurement preferences, device pricing, pod pricing, total cost of therapy, hospital and clinic purchasing trends, technical support needs, product availability, training, and vendor considerations in the usage of insulin patch pump.

- Market Expansion and Innovation: Points out growth areas for tubeless insulin administration, higher durability of disposables, CGM compatible patch pump, automation in insulin delivery algorithms, Type 2 diabetes application, pediatric devices, mobile therapy management, monitoring systems, novel market access routes, and next generation of wearable insulin delivery systems.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Global Insulin Patch Pump Market are increasingly prioritizing devices that deliver accurate insulin dosing, consistent basal and bolus delivery, strong adhesive wear performance, low occlusion risk, comfortable body placement, discreet design, and reliable operation during daily activities such as exercise, sleep, bathing, and work.

- Procurement decisions are shifting toward integrated diabetes management solutions that support continuous glucose monitoring compatibility, automated insulin delivery, smartphone or controller-based operation, remote monitoring, data-sharing with healthcare professionals, and improved patient adherence, while also meeting clinical safety, usability, cybersecurity, and regulatory requirements.

- Hospitals, diabetes clinics, homecare providers, endocrinologists, payers, and diabetes care programs are evaluating vendors based on dosing accuracy, device safety, reservoir capacity, wear duration, alarm reliability, ease of training, patient comfort, CGM interoperability, app usability, reimbursement support, technical service, supply continuity, and total cost of therapy.

- Vendors with strong capabilities in tubeless patch pump design, disposable pod technology, automated insulin delivery algorithms, CGM integration, patient-friendly software, low-profile wearable design, and scalable manufacturing are better positioned to win long-term procurement contracts as buyers move toward safer, connected, convenient, and outcome-driven insulin delivery solutions.