Industrial Heat Pump Market Definition & Overview

What is the Industrial Heat Pump Market?

The industrial heat pump market covers equipment, engineering services, controls, installation, maintenance, and integration solutions used to recover low grade heat and upgrade it into useful process heat, hot water, steam, drying heat, or district energy supply for industrial facilities. It includes closed cycle, open cycle, mechanical vapor recompression, absorption, and high temperature heat pump systems deployed across food and beverage, chemicals, pulp and paper, textiles, pharmaceuticals, metals, refineries, manufacturing, and district energy networks. The market is shaped by industrial decarbonization, energy efficiency mandates, fossil fuel price exposure, waste heat recovery potential, and the transition from boiler based heat to electrified process heat.

Industrial Heat Pump Industry Background & Evolution

Parent market background: The market sits within industrial process heating, industrial HVAC, energy efficiency equipment, waste heat recovery, and industrial electrification. Process heat has historically depended on gas, coal, oil, and steam boilers because they offered high temperature output, simple operation, and mature service networks. Industrial heat pumps emerged as a lower carbon alternative where facilities can capture waste heat from chillers, condensers, compressors, wastewater, exhaust air, process streams, or ambient sources.

Roadmap evolution: 1980s to 1990s, early industrial heat pumps were concentrated in drying, district heating, and low temperature hot water. 2000 to 2010, screw compressors, better refrigerants, and control systems improved reliability. 2011 to 2019, waste heat recovery became a stronger energy cost reduction tool. 2020 to 2024, net zero targets and gas price volatility accelerated pilot deployments in food, paper, and chemicals. 2025 to 2026, high temperature heat pumps moved from pilots toward commercial industrial decarbonization programs. 2027 to 2035, adoption is expected to scale through steam generating units, heat as a service, digital optimization, and integration with renewable electricity.

Industrial Heat Pump Market Snapshot

| Metric | Industrial Heat Pump Market Snapshot |

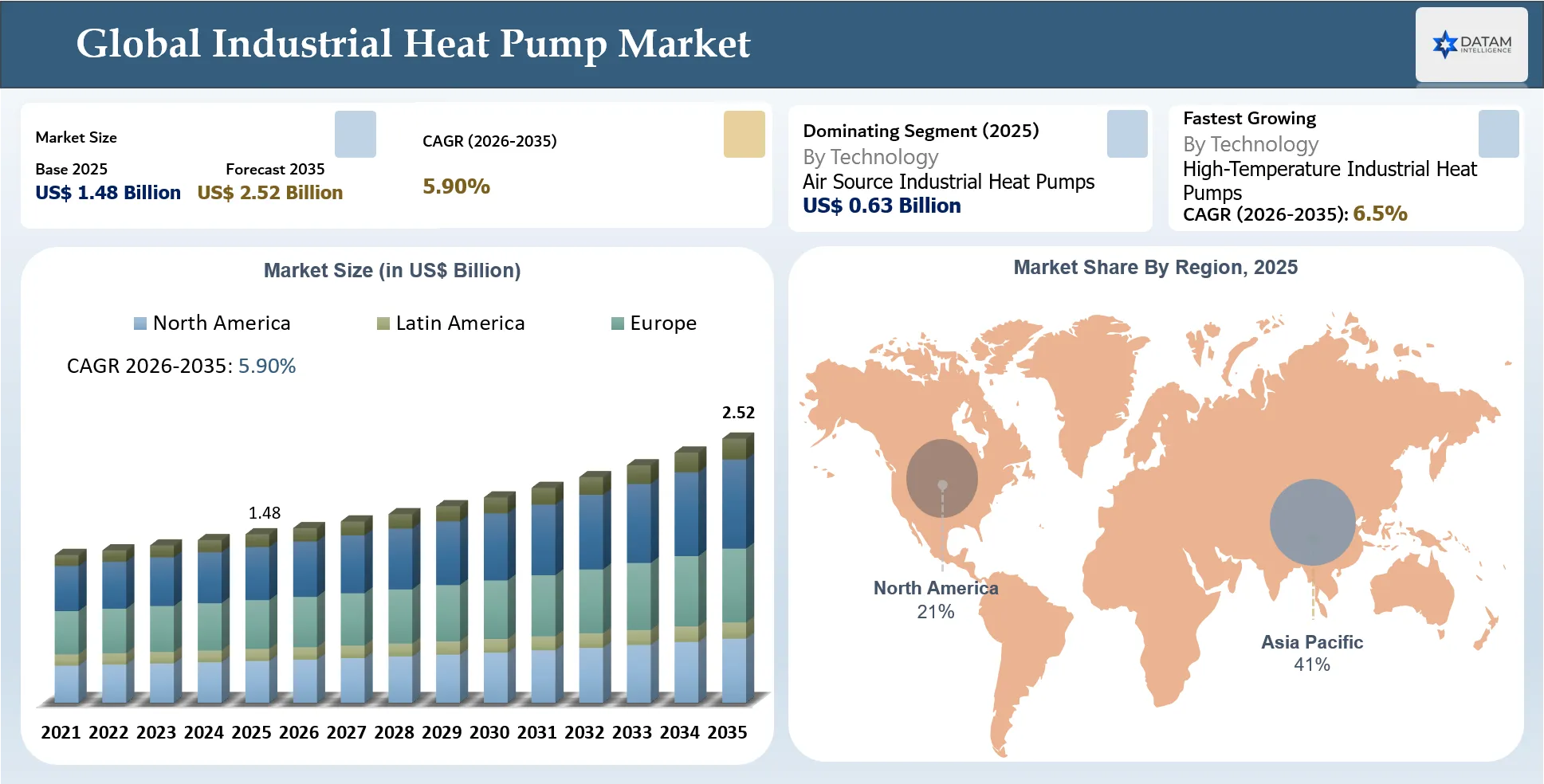

| Global Market Size (2025) | USD $1.48 Billion |

| Projected Market Size (2035) | USD $2.52 Billion |

| CAGR (2026-2035) | 5.90% |

| Largest Segment Name | Air Source |

| Largest Segment Share | 42.3% |

| Fastest Growing Segment Name | High-Temperature Industrial Heat Pumps |

| Fastest Growing Segment Growth/Share | 6.5% |

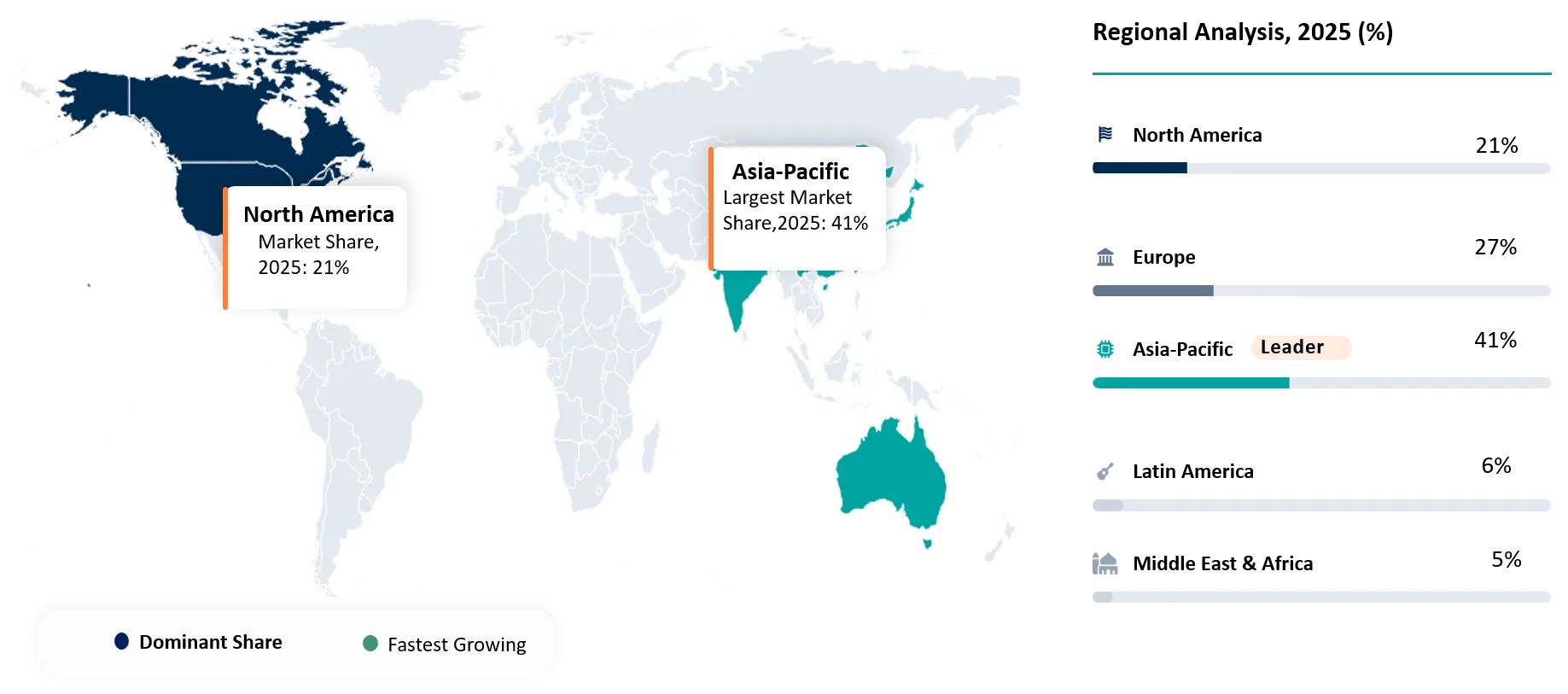

| Largest Region Name | Asia Pacific |

| Largest Region Share | 41% |

| Fastest Growing Region Name | Europe |

| Fastest Growing Region Growth/Share | 10.0% |

| Geographic Market Share for the 5 Regions | Asia Pacific: 41% Europe: 27% North America: 21% South America: 6% Middle East & Africa: 5% |

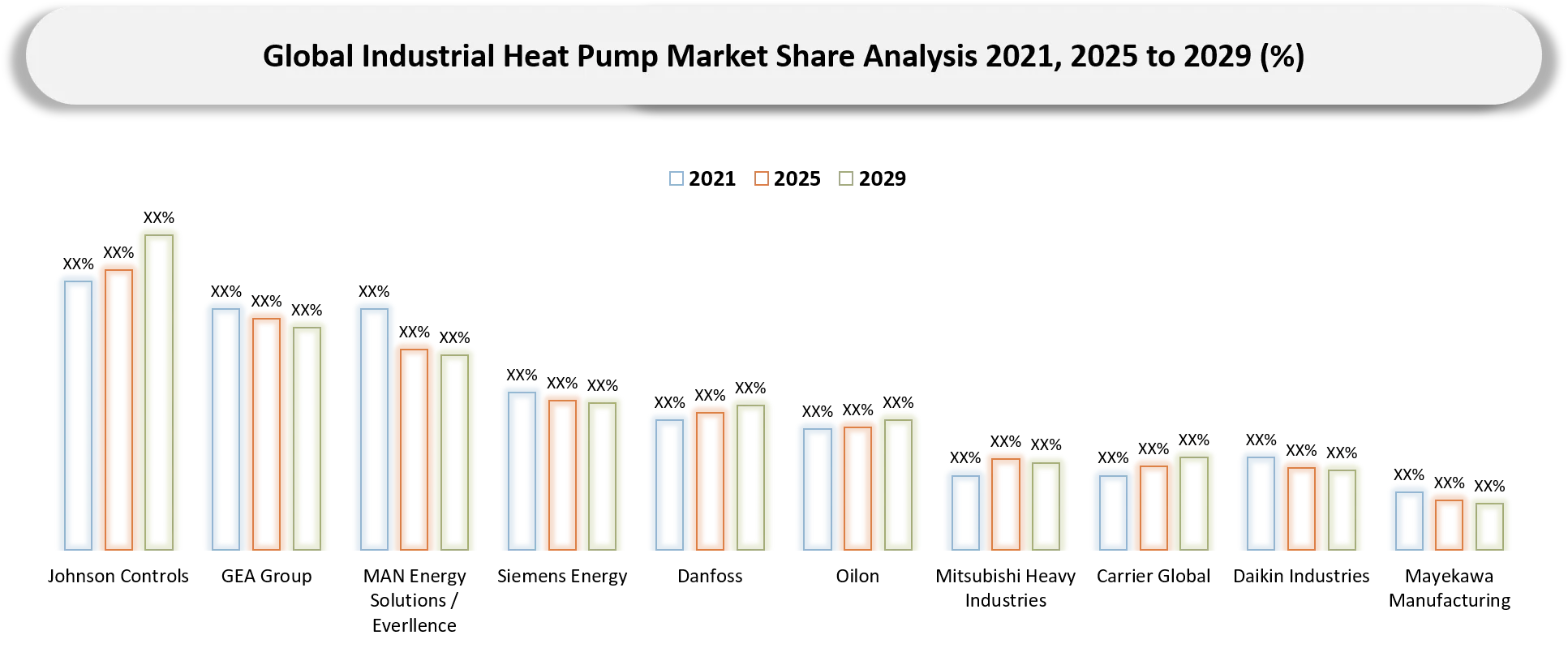

| Top Companies | Johnson Controls GEA Group MAN Energy Solutions / Everllence Siemens Energy Danfoss Oilon Mitsubishi Heavy Industries Carrier Global Daikin Industries Mayekawa Manufacturing |

Global Industrial Heat Pump Market Size & Forecast Analysis

Historical Industrial Heat Pump Market Trend Analysis

During 2021 to 2025, industrial heat pump demand shifted from energy efficiency retrofits toward strategic decarbonization projects. Early adoption was concentrated in facilities with stable low temperature heat demand, especially food and beverage, district energy, wastewater linked heating, and drying applications. The Russia Ukraine energy shock changed buyer behavior by exposing gas price risk and improving the payback logic for electrified heat in Europe. At the same time, corporate net zero targets moved heat pumps from sustainability pilots to capital planning discussions. Technology suppliers improved output temperatures, modular packages, compressor reliability, and refrigerant options, making systems more practical for steam adjacent applications. However, adoption remained uneven because electricity to gas price ratios, grid connection queues, site specific engineering, and limited installer capability slowed rollouts. The market therefore grew through larger custom projects rather than mass standardized deployment, with stronger momentum where policy incentives and carbon reduction targets supported industrial electrification.

Industrial Heat Pump Growth Outlook Summary

The industrial heat pump market is expected to grow steadily as industries move from boiler efficiency upgrades toward deeper process heat electrification. In the short term, 2026 to 2028, adoption will be strongest in food and beverage, pulp and paper, district heating, wastewater treatment, and chemicals where process temperatures below 150°C align with commercially proven systems. Projects will remain highly engineered because heat source mapping, process integration, and electricity infrastructure determine economics. In the mid term, 2029 to 2032, high temperature and steam generating heat pumps should expand the addressable market as compressor designs, natural refrigerants, and modular integration improve. Heat as a service models may reduce upfront capital barriers for mid sized manufacturers. In the long term, 2033 to 2035, the market should benefit from carbon pricing, low carbon product procurement, grid decarbonization, and industrial energy management platforms. Growth will not be uniform. Regions with favorable electricity pricing, strong industrial policy, and mature service ecosystems will capture faster deployment than markets where cheap gas and weak incentives persist.

Key Takeaways

- The market is moving from isolated efficiency retrofits to process heat electrification programs where engineering capability, heat-source mapping and operating guarantees matter more than equipment price alone.

- High-temperature systems are becoming the strategic battleground because they expand addressable demand from hot water into drying, evaporation, pasteurization, distillation support and low-pressure steam.

- Buyers increasingly compare industrial heat pumps against boiler replacement, waste heat recovery and thermal storage economics, so suppliers need lifecycle-cost selling rather than catalog-based product positioning.

- Natural refrigerants and low-GWP architectures are becoming procurement differentiators as customers try to avoid future retrofit risk under tightening refrigerant rules.

- Project execution capability is emerging as a competitive moat because downtime risk, control integration and utility upgrades determine whether pilots scale into repeatable rollouts.

- Largest Segment Takeaway: Air-source industrial heat pumps remain the largest heat-source segment because they offer the simplest retrofit pathway for factories with moderate-temperature heat loads and limited site-specific waste heat access.

- Largest Region takeaway: Asia Pacific holds the largest regional share because its manufacturing base, district heating needs, electronics supply chain and food processing capacity create a broad installed base for industrial heat demand.

- Fastest Growing Segment Takeaway: High-temperature industrial heat pumps are the fastest-growing segment as suppliers commercialize systems capable of serving process heat above conventional hot-water temperature ranges.

- Fastest Growing Region takeaway: Europe is the fastest-growing region because carbon pricing, industrial heat auctions, Fit for 55 implementation and energy-security priorities are converting decarbonization targets into fundable projects.

Industrial Heat Pump Market White Space & Investment Opportunities

White space opportunities show where suppliers, investors, and service providers can capture unmet demand through standardized systems, retrofit services, financing models, sector-specific integration, and recurring performance contracts across industrial facilities.

- Mid sized factories remain underserved because many suppliers focus on large custom projects, creating room for standardized, finance backed heat pump packages for breweries, dairies, textiles, and laundries.

- Industrial wastewater heat recovery offers underdeveloped potential where plants discharge warm effluent that can be upgraded for process water, cleaning, or nearby district energy.

- Retrofit services for boiler rooms represent a growing opportunity as manufacturers need audits, heat integration design, controls, and phased commissioning rather than standalone heat pump equipment.

Industrial Heat Pump Market Procurement & Buyer Behavior Analysis

Industrial Heat Pump Market Buyer Decision-Making Criteria

Industrial buyers procure heat pumps as strategic process assets, not as standard HVAC equipment. The highest-priority criteria are reliability under continuous operation, integration with existing steam or hot-water networks, verified COP, safety compliance, refrigerant future-proofing and credible lifecycle service. Procurement teams also prioritize references in similar industries because real process conditions can differ materially from design assumptions.

- Temperature output and lift suitable for the process

- Seasonal and process-specific COP under realistic load profiles

- Compatibility with existing boilers, heat exchangers, steam loops and controls

- Natural refrigerant or low-GWP refrigerant strategy

- Safety design, leak detection, ventilation and operator training

- Supplier reference projects in comparable applications

- Electrical interconnection requirements and peak-demand impact

- Commissioning support and performance validation

- Lifecycle service, spare parts and remote monitoring

- Payback period, emissions reduction and financing support

Industrial Heat Pump Market Economic & Investment Analysis

Industrial Heat Pump Market Macroeconomic Impact Factors

Industrial heat pump demand is being shaped by four macroeconomic themes: energy-price volatility, carbon-cost exposure, interest-rate sensitivity and industrial productivity pressure. High gas and power price spreads determine project payback, so countries with expensive fossil fuel heat and growing renewable electricity access are seeing stronger market growth. Carbon taxes, emissions trading and corporate scope 1 reduction targets are improving the strategic value of electrified process heat beyond simple fuel savings. However, elevated financing costs make buyers more selective, especially for large retrofits requiring heat-source mapping, electrical upgrades and production downtime. Inflation in compressors, heat exchangers, skilled labor and refrigerants also raises installed system size and cost. At the same time, manufacturers facing competitiveness pressure are using heat pumps to stabilize energy expenditure, reduce boiler exposure and improve ESG-linked financing access. Overall, macroeconomic conditions are pushing the market toward standardized systems, heat-as-a-service models and stronger lifecycle-cost justification.

Industrial Heat Pump Investment Trends in the Market

Investment is shifting from individual demonstration projects toward serial manufacturing, high-temperature product platforms and bankable retrofit delivery models. Capital is increasingly targeting technologies that shorten engineering cycles and expand the addressable market size for process heat below 200°C.

- Modular high-temperature heat pump production lines

- Natural refrigerant and low-GWP system redesign

- Turnkey industrial waste heat recovery and heat-as-a-service platforms

Industrial Heat Pump Market Funding & M&A Activity

Funding and M&A activity is expected to focus on high-temperature heat pumps, steam-generating platforms, natural refrigerant systems, industrial heat-as-a-service models and companies that can convert one-off engineered projects into repeatable productized deployments. Strategic buyers are seeking technology depth, service channels and access to industrial decarbonization customers.

- Enerin raised EUR 15 million Series A in November 2025 led by Climentum Capital, The Footprint Firm, Johnson Controls and Move Energy, with PSV Hafnium and Momentum participating, to industrialize modular high-temperature heat pumps.

- HotGreen Solutions raised EUR 1.4 million pre-seed funding in October 2025 led by Empirical Ventures, with First Imagine! Ventures, The Conduit Impact Fund and Almanac Ventures, to advance industrial process heat decarbonization.

- Copeland announced an agreement in October 2025 to acquire Germany-based SPH Sustainable Process Heat, expanding its industrial high-temperature heat pump portfolio and sustainable process heat market reach.

Industrial Heat Pump Market Regulatory & Policy Analysis

Industrial Heat Pump Market Regulatory Framework Overview

The regulatory framework for industrial heat pumps is shaped by climate policy, energy-efficiency standards, refrigerant controls, industrial emissions rules, electrical safety and pressure-equipment requirements. Europe is the most regulation-driven market because F-gas rules accelerate the move away from high-GWP refrigerants, while industrial decarbonization policies push factories and district heating networks toward electrified heat. In North America and Asia, policy support is more fragmented but increasingly tied to clean energy incentives, industrial efficiency funding and emissions-reduction commitments.

- EU F-gas Regulation 2024/573 implementation from 2025 strengthens reporting, labelling and HFC phase-down requirements, pushing heat pump suppliers toward low-GWP and natural refrigerants.

- EU implementing acts on F-gas labelling and reporting became applicable in 2025, increasing compliance obligations for manufacturers, importers and service providers.

- Industrial decarbonization and clean heat funding programs in the U.S., Europe and Asia are improving project economics for heat pump retrofits in hard-to-abate industrial heat applications.

Industrial Heat Pump Policy Impact on Market Growth

Government policy is converting heat pumps from optional efficiency upgrades into strategic decarbonization infrastructure. The strongest impact comes where carbon targets, clean electricity, grants and refrigerant rules align, making industrial heat pump projects financially and technically easier to approve.

- Refrigerant policy accelerates redesign toward ammonia, CO2, propane and other low-GWP options, benefiting suppliers with proven natural-refrigerant platforms.

- Industrial decarbonization grants and tax incentives reduce upfront capex barriers and support first-of-a-kind steam and high-temperature projects.

- Public procurement and district heating decarbonization policies create anchor demand for large heat pumps, improving bankability and reference project visibility.

Industrial Heat Pump Market Trends & Innovation Landscape

Industrial Heat Pump Key Market Trends

The key trends show that the market is shifting from conventional energy-efficiency equipment toward a strategic industrial decarbonization solution. Buyers are prioritizing high-temperature capability, lower carbon heat, operating reliability and integration with waste heat sources, while suppliers are focusing on productized systems that reduce engineering complexity and shorten project development cycles.

- High-temperature heat pumps are moving from demonstration to commercial deployment as suppliers target process heat up to around 150°C to 200°C, increasing relevance for food, paper, and chemical plants.

- Procurement is shifting toward turnkey decarbonization solutions where OEMs, ESCOs, and engineering firms bundle equipment, controls, maintenance, and performance guarantees.

Industrial Heat Pump Market Technology Advancements

Technology development is concentrated around higher delivery temperatures, natural refrigerants, modular architectures and controls that can stabilize performance under variable industrial loads. These advancements are expanding the usable temperature range of heat pumps and improving buyer confidence in applications that were previously served almost entirely by fossil boilers.

- In 2025 and 2026, high-temperature compressor development and improved cycle configurations increased confidence in process heat applications above traditional hot water ranges, expanding use cases for steam-adjacent industrial loads.

- Natural refrigerant and transcritical CO2 system innovation is improving environmental performance while supporting higher output temperatures, making systems more attractive for buyers facing refrigerant regulation and long asset lives.

- April 2026: The International Institute of Refrigeration highlighted high-temperature heat pumps as a key technology for industrial decarbonization, reinforcing engineering confidence in process heat applications. Market impact: this supports specification activity among industrial buyers that need third-party technical validation before replacing boilers.

- 2025: Project 68 advanced a shared knowledge base on industrial high-temperature heat pump technologies. Market impact: stronger technology documentation helps reduce perceived risk, supports standardization and improves cross-country adoption learning.

Industrial Heat Pump Industry Transformation Trends

Industrial heat is shifting from fuel-based boiler ownership toward integrated energy systems combining waste heat recovery, electrification, thermal storage, renewable power procurement, and digital controls. This changes buyer evaluation from equipment price to lifecycle energy cost, carbon reduction, operating resilience, and process compatibility.

Industrial Heat Pump Market Disruption Analysis

Industrial heat pumps disrupt the incumbent boiler ecosystem by reducing dependence on combustion, creating new roles for electrical contractors, controls providers, refrigerant specialists, ESCOs, and process integration engineers. The disruption is strongest in low and medium temperature heat where heat pumps can deliver efficiency gains that boilers cannot match.

Industrial Heat Pump Market Disruption & Structural Shift Analysis

Industrial Heat Pump Market Technology Disruption Impact

Technology disruption is strongest where heat pumps move from peripheral utility systems into core production heat. This shift changes procurement, engineering, controls and service models because buyers need uptime assurance, process integration and verified emissions reduction rather than a conventional equipment replacement decision.

- Steam-capable high-temperature heat pumps are disrupting boiler replacement economics by extending electrification beyond hot water into process steam. This expands addressable demand in food, chemicals, paper, district energy and refineries, but forces suppliers to prove reliability, controls integration and long-term COP under real process conditions.

- Natural refrigerant systems using ammonia, CO2, propane and pentane are disrupting legacy HFC-based designs as F-gas restrictions tighten. The impact is a shift toward redesigned compressors, safety systems, ventilation, leak detection and installer training, creating advantage for vendors with mature natural-refrigerant engineering and certification capabilities.

Industrial Heat Pump Future Market Transformation

The industry business model is being transformed by electrified process heat, digital service contracts, natural-refrigerant redesign and industrial energy orchestration. Over the next decade, suppliers will increasingly sell guaranteed heat output, uptime, carbon reduction and energy optimization rather than only hardware. Industrial customers will seek bundled solutions combining heat pumps, thermal storage, renewable power procurement, grid flexibility, waste-heat recovery and boiler hybridization. As a result, project developers, utilities and OEMs will compete through performance guarantees, financing models and long-term service agreements, making reference projects and operational data as important as equipment specifications.

Industrial Heat Pump Market Growth Dynamics

Industrial Heat Pump Market Drivers

- Industrial decarbonization mandates are pushing manufacturers to replace fossil-fired boilers with electrified process heat where temperature levels and waste heat sources are suitable, creating demand beyond conventional energy-saving projects.

- Rising energy efficiency pressure is improving project economics because heat pumps can upgrade rejected heat that was previously vented, discharged, or cooled, reducing purchased fuel requirements.

- Expansion of high-temperature heat pump capability is widening addressable applications from hot water and drying into steam generation, evaporation, and chemical process heating.

Industrial Heat Pump Market Driver Impact Assessment

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

| Industrial decarbonization mandates | 4.8% | Europe, Japan, South Korea, North American industrial clusters | Boiler replacement, steam decarbonization, low carbon manufacturing | Moves heat pumps into board level capex planning and long term emissions roadmaps |

| Waste heat recovery economics | 4.4% | Food and beverage, pulp and paper, chemicals, wastewater linked sites | Drying, washing, evaporation, hot water, district heat | Improves payback by monetizing internal heat streams and reducing fuel purchases |

| High temperature technology maturity | 3.9% | OEMs, engineering firms, process industries needing 120°C to 200°C heat | Steam generation, MVR, distillation, high temperature process heat | Expands addressable market beyond low temperature applications and improves replacement potential for boilers |

Industrial Heat Pump Market Restraints

- High upfront project cost limits adoption because industrial heat pumps often require heat exchangers, process redesign, controls, thermal storage, electrical upgrades, and downtime planning rather than only equipment procurement.

- Unfavorable electricity to gas price ratios weaken payback in regions where gas remains cheap and electricity tariffs include high demand charges or grid fees.

- Limited industrial integration expertise slows scale up because each site requires detailed heat mapping, source sink matching, refrigerant selection, and safety assessment.

Industrial Heat Pump Market Restraint Impact Assessment

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

| High upfront integration cost | 4.2% | Capital budgeting and project approval | Large capacity retrofits, steam generating heat pumps | Extends payback periods and favors large firms with decarbonization budgets |

| Electricity to gas price imbalance | 3.8% | Operating expenditure competitiveness | Boiler displacement, continuous process heating | Delays adoption unless carbon pricing, power procurement, or incentives improve economics |

| Shortage of system integration expertise | 3.5% | Engineering, commissioning, and maintenance ecosystem | Multi source waste heat recovery, high temperature projects | Limits repeatable deployment and increases project execution risk |

Emerging Industrial Heat Pump Growth Factors

Emerging growth factors highlight the next adoption layer where technology maturity, financing innovation, digital controls, refrigerant strategy, and modular systems expand industrial heat pump use beyond early retrofit projects globally.

- Natural refrigerant adoption is rising as buyers seek lower global warming potential systems, reduced compliance risk, and suitability for high temperature industrial heat recovery.

- Modular skid mounted heat pumps are shortening engineering cycles by packaging compressors, controls, heat exchangers, and safety systems into repeatable industrial units.

- AI enabled heat mapping and predictive control are improving source sink matching, maintenance planning, and operating efficiency across variable industrial loads.

Industrial Heat Pump Market Segmentation Analysis

Market segmentation analysis covers heat source, capacity, temperature range, and end-use application because these dimensions explain both buying behavior and technology complexity. Air-source and waste-heat-source systems dominate early adoption where integration is simpler, while high-temperature and steam-producing systems are becoming the strategic growth layer for deeper decarbonization. Food and beverage, chemicals, pulp and paper, district heating, and refining remain the most relevant demand pools because they need continuous process heat and have identifiable waste heat streams.

The major segment pattern shows adoption moving from low-temperature utility use toward integrated process-heating projects. Air-source systems remain commercially scalable, food and beverage remains a leading end-use because of repeatable hot-water and drying requirements, and high-temperature heat pumps are the most important future segment as they can replace boilers in processes approaching steam conditions. The market is headed toward application-specific packaged systems, hybrid boiler-heat-pump designs, and more supplier involvement in feasibility studies, digital monitoring, heat-source mapping, and lifecycle energy optimization.

Industrial Heat Pump Market by Heat Source Trends

Air-source systems remain the broadest commercial heat-source category because they are easier to retrofit, require less civil infrastructure and suit facilities needing moderate-temperature hot water or process support. The major trend is the shift from simple ambient extraction to hybrid and waste-heat-assisted designs that improve COP and reduce payback risk. Over the next decade, the market is expected to move toward deeper integration with process streams, wastewater loops, refrigeration condensers and thermal storage, allowing heat-source selection to become a strategic energy-system decision rather than a product choice.

Industrial Heat Pump Market by Capacity Trends

Mid-capacity systems are the most practical commercial layer because they match the heating loads of dairies, breweries, food plants, textile units and chemical facilities without requiring full-site thermal redesign. The main trend is modularization, with suppliers packaging compressors, controls, storage and heat exchangers to shorten installation time. The market is headed toward multi-unit cascades where several standardized systems manage variable loads, provide redundancy and reduce commissioning risk while still enabling large heat output across industrial campuses.

Industrial Heat Pump Market by Temperature Range Trends

Moderate-temperature applications currently account for the most bankable deployments because they align with washing, drying, pasteurization, hot-water and district energy requirements. The strongest trend is the acceleration of high-temperature platforms that can address process heat and low-pressure steam needs. Over time, the market is expected to move from low-risk utility heating toward core production processes, but adoption will depend on compressor durability, refrigerant safety, heat-source stability and proof that industrial uptime is not compromised.

Industrial Heat Pump Market Regional Analysis

Regional analysis shows Asia Pacific leading current demand because of its manufacturing base, while Europe is the fastest-growth region due to industrial decarbonization policy, carbon pricing, and fossil-boiler replacement programs. North America is moving from incentive-led pilots toward larger projects in food processing, chemicals, and district energy. South America and the Middle East & Africa remain smaller markets but present selective opportunities in food processing, mining, petrochemicals, and industrial energy-efficiency retrofits.

North America Industrial Heat Pump Market

North America industrial heat pump demand is shifting from early decarbonization studies toward bankable retrofit projects in food processing, chemicals, district energy, and institutional campuses. The U.S. is the core demand center because manufacturers are evaluating electrified process heat alongside waste-heat recovery, thermal storage, and low-carbon electricity procurement. Production capacity is improving through HVAC and compressor suppliers expanding industrial product lines, but the region still relies on specialized engineering for high-temperature applications. Demand changes are most visible in facilities with high natural gas exposure, corporate Scope 1 emission targets, and access to incentives or clean-power contracts. The 2026 to 2035 market outlook is therefore project-led rather than purely equipment-led, with growth tied to feasibility studies, process integration, and energy-service models that reduce upfront risk for plant owners.

Europe Industrial Heat Pump Market

Europe is the fastest-growing strategic region for industrial heat pumps because high energy prices, carbon costs, F-Gas rules, and EU industrial decarbonization policy are pushing factories to replace or hybridize fossil boilers. Production capacity expanded during the post-energy-crisis investment cycle, although recent demand volatility left some capacity underutilized. Germany, France, the Nordics, the Netherlands, and the UK remain important adoption centers due to district heating, food processing, chemicals, and industrial efficiency mandates. Demand is moving toward high-temperature systems, natural refrigerants, and steam-capable solutions. The region’s growth depends on stable subsidies, electricity-gas price spreads, grid readiness, and faster project engineering for brownfield plants.

Asia Pacific Industrial Heat Pump Market

Asia Pacific is the largest regional market because China, Japan, South Korea, and India combine large industrial heat demand with strong manufacturing supply chains. China provides scale through industrial parks, electronics, chemicals, textiles, and district heating projects, while Japan and South Korea contribute advanced compressor, refrigerant, and high-temperature heat pump technologies. Production capacity is comparatively strong because many global HVAC and compressor suppliers are based in the region. Demand is shifting from conventional efficiency upgrades to process electrification, especially where governments promote energy security and carbon reduction. Growth is strongest in applications with repetitive heat loads, including food processing, electronics, chemicals, and drying.

Industrial Heat Pump Market Country-Level Analysis

United States Industrial Heat Pump Market Size/Forecast

The United States industrial heat pump market is advancing through food and beverage, chemicals, pulp and paper, universities, district energy networks, and industrial decarbonization projects. Demand is strongest where facilities have predictable low- to medium-temperature heat loads and recoverable waste heat from refrigeration or compressed-air systems. Production capacity is improving as domestic HVAC players, compressor suppliers, and engineering firms expand industrial electrification offerings, but high-temperature steam applications still require customized integration. The market is expected to grow as Inflation Reduction Act-linked incentives, corporate emission targets, and lower-carbon electricity procurement make heat pumps more attractive than new gas-fired boiler capacity in selected industrial sites.

Japan Industrial Heat Pump Market Size/Forecast

Japan is a mature technology market for industrial heat pumps, supported by long-standing expertise in compressors, refrigeration, and high-efficiency thermal systems. Demand is concentrated in food processing, chemicals, machinery, electronics, district energy, and facilities seeking energy savings under Japan’s carbon-neutrality pathway. Production capacity is strong because Japanese suppliers such as Daikin, Mitsubishi Electric, Mayekawa, and Panasonic have deep heat-pump engineering capabilities. Market growth is not only volume-driven; it is also focused on higher-temperature performance, reliability, and compact systems for constrained industrial sites. Adoption should expand where factories can combine waste-heat recovery, electrification, and energy management to reduce fuel imports and emissions.

China Industrial Heat Pump Market Size/Forecast

China is one of the most important industrial heat pump demand and supply markets due to its large manufacturing base, district heating needs, and policy focus on energy efficiency and carbon peaking before 2030. Demand is expanding in chemicals, textiles, food processing, electronics, industrial parks, and wastewater heat recovery. Production capacity is broad, with domestic HVAC, compressor, and heat-pump manufacturers scaling air-source and water-source platforms while also moving into larger industrial systems. The market is headed toward integrated electrified heat solutions for industrial clusters, supported by China’s renewable power expansion and need to cut coal and gas use in low- and medium-temperature heat.

India Industrial Heat Pump Market Size/Forecast

India is an emerging industrial heat pump market with strong long-term potential across dairy, food processing, textiles, chemicals, pharmaceuticals, hotels, and industrial hot-water applications. Demand is currently limited by upfront cost sensitivity, electricity pricing, and lower awareness of process-heat electrification, but rising fuel costs and export-oriented decarbonization pressure are changing buyer interest. Production capacity is developing through local HVAC manufacturers and partnerships with global suppliers, while advanced high-temperature systems are still largely imported or engineered case-by-case. Growth should accelerate where factories have continuous heat loads, rooftop solar, refrigeration waste heat, and energy-efficiency mandates.

Industrial Heat Pump Market: Other Key Countries

- Germany Industrial Heat Pump Market: Germany is a core European market because chemicals, food processing, machinery, district heating, and industrial clusters face strong decarbonization pressure. Demand is focused on high-temperature systems, boiler hybridization, and waste-heat recovery, while production benefits from strong engineering and component supply chains.

- France Industrial Heat Pump Market: France is gaining momentum as electrification policy, low-carbon power availability, and industrial efficiency programs support heat pump adoption. Food processing, district heating, and chemicals are key demand pools, with interest rising in steam-capable systems and retrofit packages.

- South Korea Industrial Heat Pump Market: South Korea combines electronics, chemicals, batteries, and advanced manufacturing demand with strong domestic HVAC and compressor capabilities. Adoption is supported by energy-efficiency goals and carbon reduction pressure in export-led industries requiring cleaner process heat.

- United Kingdom Industrial Heat Pump Market: The UK market is developing around food and beverage, district heating, public estates, and industrial decarbonization clusters. Growth depends on grid access, stable incentive design, and converting feasibility studies into bankable retrofit projects.

- Brazil Industrial Heat Pump Market: Brazil has opportunities in food processing, dairy, pulp and paper, sugar, and industrial hot-water applications. Demand is supported by energy-efficiency needs and multinational decarbonization targets, although project economics depend on electricity pricing and imported equipment availability.

Industrial Heat Pump Market Competitive Landscape

Industrial Heat Pump Market Competitive Benchmarking

Competitive benchmarking shows that leading suppliers are not competing only on equipment specifications. The strongest players combine compressor depth, high-temperature know-how, controls, refrigerant strategy, industrial references and service capability. Their target strategy increasingly focuses on sectors where process integration creates repeatable value and long-term customer lock-in.

- Johnson Controls: Strongest in large commercial and industrial heat pump packages through Sabroe-branded systems, natural refrigerants, factory testing and district-heating/customer-engineering centers. Its strategy targets European district heating, food and beverage, public infrastructure and mission-critical process heat where reliability and validation reduce buyer risk.

- GEA Group: Differentiates through ammonia and natural-refrigerant heat pump engineering, food and beverage process knowledge and high-temperature industrial waste-heat recovery. The company is positioned around process-specific integration rather than equipment-only sales, with strong traction in food, sugar, dairy, refrigeration-linked applications and medium-output industrial heat.

- MAN Energy Solutions / Everllence: Competes in the large-scale, steam-capable heat pump niche using turbo-compressor and CO2/VCC technology. Its target strategy focuses on district energy, industrial steam networks and hard-to-electrify heat loads where single projects can reach tens of megawatts.

- Danfoss: Benchmarked as an enabling technology supplier rather than a pure systems integrator, with compressors, drives, controls, heat exchangers and application know-how. Its strategy targets OEMs, local manufacturing partners and energy-transition infrastructure, giving it leverage across multiple heat pump brands and regions.

- Oilon: Competes with modular ChillHeat systems and containerized/end-to-end packages. Its use-case focus is industrial waste heat, district heating, data centers, hospitals and campuses where scalable 30 kW to multi-MW configurations are valued.

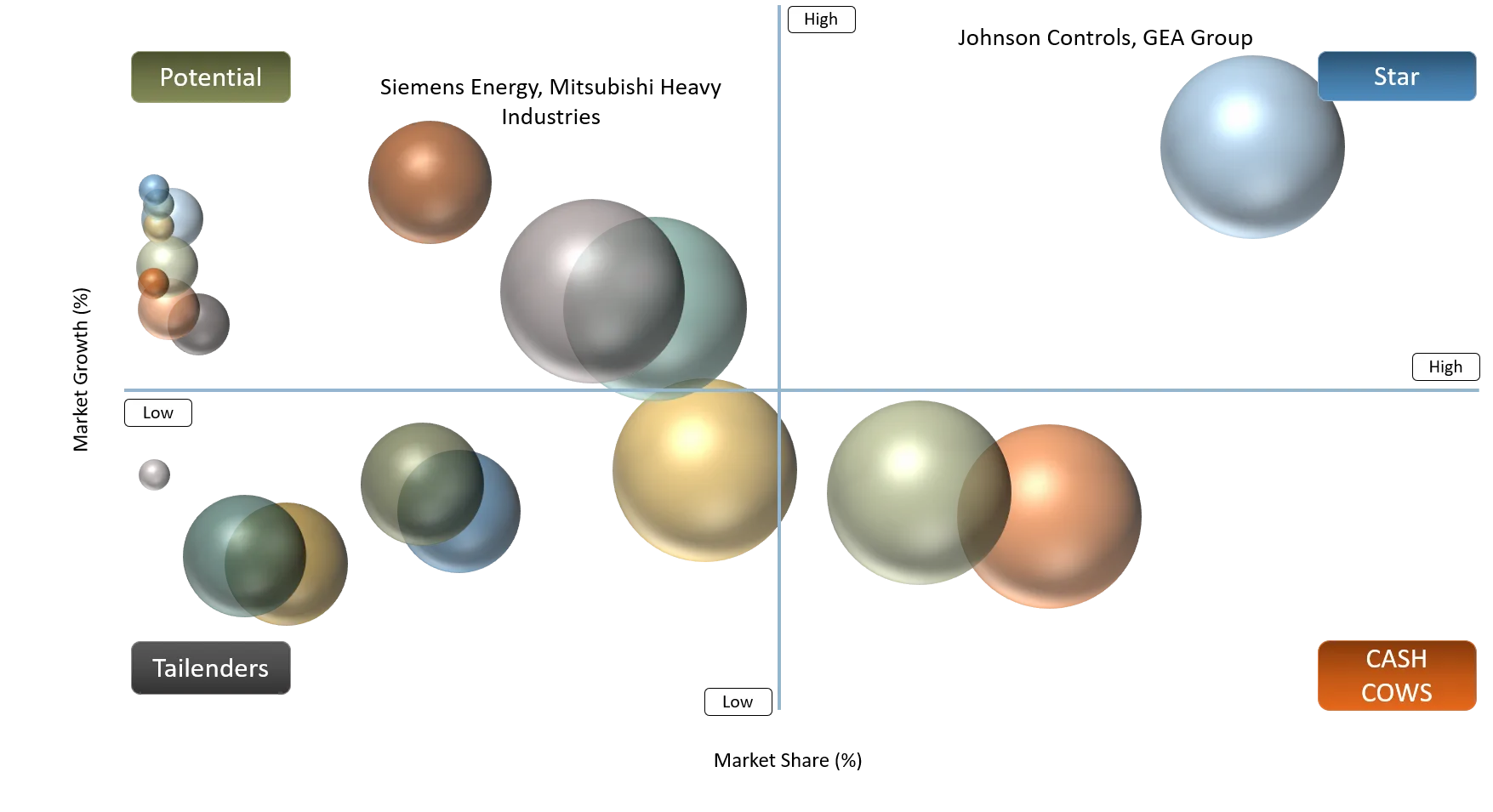

Industrial Heat Pump Market BCG Matrix List

- Stars: Johnson Controls; GEA Group

- Question Marks: Siemens Energy; Mitsubishi Heavy Industries

- Cash Cows: Danfoss; Carrier Global

- Niche / Potential Players: MAN Energy Solutions / Everllence; Oilon

Industrial Heat Pump Market BCG Matrix Analysis

Johnson Controls and GEA Group sit in the Stars category because both combine recognized industrial heating portfolios with strong execution capability in natural refrigerants, testing infrastructure and process-specific heat pump integration. Their position benefits from immediate demand in Europe, district heating and food processing, where buyers prefer bankable vendors with reference projects. Siemens Energy and Mitsubishi Heavy Industries are Question Marks because they have strong energy and thermal engineering capabilities, but industrial heat pumps represent a more selective growth platform compared with their broader power, turbomachinery and HVAC portfolios. Danfoss and Carrier Global act as Cash Cows because their compressor, controls, refrigeration and HVAC installed bases generate recurring demand and component pull-through, even when they are not always the lead project integrator. MAN Energy Solutions / Everllence and Oilon fall into Niche / Potential Players because they are highly relevant in high-capacity steam, district energy and modular industrial applications, but depend on large project pipelines and specialized engineering demand.

Industrial Heat Pump Market Expansion & Partnership Strategy

- Johnson Controls opened an expanded Holme, Denmark engineering, production and customer center in May 2026, doubling production capacity and strengthening testing for high-capacity industrial heat pumps. The expansion improves European supply availability, supports natural-refrigerant systems and reduces buyer risk by enabling precision testing before deployment.

- Vicinity Energy, DCO Energy and Everllence began construction of a 35 MW river-source industrial heat pump complex at Kendall Square in 2025, targeting steam generation for Boston and Cambridge. The project validates large heat pumps as district steam infrastructure, creating reference value for utilities and industrial campuses.

- Danfoss India announced plans to invest Rs 1,500 crore through 2030 to expand localization, compressor capacity and India-led R&D. The investment strengthens component availability for heat pumps and cooling systems, while improving regional manufacturing depth for energy-transition applications in Asia and global export markets.

Industrial Heat Pump Market Key Developments (2025–2026)

Industrial Heat Pump Major Industry Developments

Recent industry developments show that industrial heat pumps are gaining support from policy funding, strategic acquisitions and investor-backed commercialization. The most important changes are not isolated product announcements; they indicate a broader transition toward scalable high-temperature heat, project financing and integrated decarbonization offerings.

- October 2025: Copeland announced an agreement to acquire SPH Sustainable Process Heat, strengthening its industrial high-temperature heat pump technology portfolio and expanding sustainable process heat capabilities.

- November 2025: Enerin raised EUR 15 million Series A funding led by Climentum Capital, The Footprint Firm, Johnson Controls and Move Energy to industrialize modular high-temperature heat pumps.

- October 2025: The European Commission published terms and conditions for the first Innovation Fund industrial heat decarbonization auction, creating subsidy visibility for electrified process heat projects.

- May 2026: The European Commission awarded EUR 400 million to 65 industrial heat decarbonization projects across 10 countries, improving demand visibility for heat pumps and adjacent electrification technologies.

- April 2026: The International Institute of Refrigeration published a technical brief positioning high-temperature heat pumps as a key industrial decarbonization technology, improving confidence among engineers, policymakers and buyers.

Industrial Heat Pump: Recent Market Announcements

Copeland’s October 2025 agreement to acquire SPH Sustainable Process Heat is a major market announcement because it signals that established climate technology suppliers are moving aggressively into industrial high-temperature heat pumps. The deal expands Copeland’s portfolio beyond conventional HVAC and refrigeration into fossil-free process heating and steam-related applications. Its impact is strategic: it validates industrial heat pumps as a consolidation market, increases competitive pressure on specialist manufacturers and improves customer confidence in service availability, product support and global channel reach. The acquisition also suggests that future market share may depend on combining compressor expertise, controls, application engineering and industrial sales networks.

Industrial Heat Pump Market Technology Launches & Partnerships

Technology launches and partnerships are accelerating the move from pilot projects to commercial industrial heat platforms. The most relevant announcements combine product innovation with manufacturing scale, policy support or customer deployment, which helps reduce perceived technology risk and expands the investable opportunity in industrial process heat.

- October 2025: Copeland announced its agreement to acquire SPH Sustainable Process Heat, adding high-temperature process heat technology and strengthening its ability to serve industrial decarbonization customers.

- November 2025: Enerin raised EUR 15 million Series A funding to industrialize modular high-temperature heat pumps, accelerating the shift from engineered pilots to scalable product platforms.

- May 2026: The EU confirmed a second Industrial Heat Auction following strong industry interest, improving policy continuity for industrial heat electrification projects and giving suppliers better demand visibility.

Industrial Heat Pump Market Strategic Insights & Analyst Perspective

Analyst Insights of Industrial Heat Pump Market

From a DataM Intelligence perspective, the industrial heat pump market is moving from a policy-supported sustainability niche into a measurable industrial productivity and decarbonization market. The 2025 market is still led by applications with moderate temperatures, available waste heat and short payback logic, such as food processing, district heating interfaces, washing, drying and low-pressure hot water. By 2035, the competitive boundary will shift toward high-temperature process heat, steam generation, digital controls and repeatable retrofit packages. The most important market impact is not simply equipment replacement; it is the redesign of factory heat flows. Companies that can map waste heat, optimize electricity demand, integrate thermal storage and guarantee uptime will capture a higher share than suppliers offering stand-alone units. Country-specific market size and share will depend heavily on electricity-to-gas price ratios, carbon pricing, grid capacity, refrigerant policy and industrial subsidy design. Asia Pacific is expected to retain strong volume and manufacturing relevance, while Europe will be the innovation and policy-led deployment region. The market forecast points to disciplined growth, but the winners will be those that lower project complexity, offer financing models and demonstrate verified carbon savings. The report should therefore be used not only for market size tracking but also for strategy, sourcing, partnership and investment prioritization.

Strategic Recommendations of Industrial Heat Pump Market

Recommendation 1: Companies should prioritize standardized high-temperature platforms for repeatable applications rather than relying only on customized engineering. A focused portfolio for 90°C to 200°C process heat in food, chemicals, pulp and paper and district energy can reduce sales-cycle friction, improve installation learning curves and strengthen forecast visibility. Suppliers should combine modular hardware, application playbooks, validated COP data and financing options to convert pilot interest into scaled market growth.

Recommendation 2: Companies should build partnerships with utilities, EPC firms, automation vendors and industrial energy service providers. Many buyers do not procure heat pumps as isolated equipment; they evaluate grid upgrades, controls, downtime, steam backup, carbon accounting and lifecycle risk. A partner-led go-to-market strategy can improve country specific market access, expand service reach, reduce integration risk and increase share in retrofit-heavy industrial clusters.

Industrial Heat Pump Future Market Outlook (2035 Vision)

In 2025, the Industrial Heat Pump Market remains concentrated in early commercial deployments, energy-intensive factories, public funding projects and applications where heat demand is below the highest boiler-temperature range. Buyers still evaluate projects mainly through payback, operating reliability, integration complexity and energy price assumptions. By 2035, the market is expected to look more standardized, larger and more strategic. High-temperature heat pumps will be used not only for hot water but also for steam, drying, evaporation and process integration. Digital monitoring, thermal storage and demand response will become normal features, enabling factories to optimize electricity use while reducing fuel exposure. Natural refrigerants and low-GWP systems will gain market share due to policy and procurement pressure. The competitive model will also change: suppliers will sell performance, emissions reduction and uptime rather than equipment alone. The biggest difference between 2025 and 2035 will be that industrial heat pumps will move from sustainability pilots to core industrial infrastructure within the global decarbonized process heat forecast.

Industrial Heat Pump Market Target Audience

- Industrial heat pump manufacturers: Need market size, forecast, segment share and competitive intelligence to prioritize applications, capacity ranges and country specific market entry.

- Compressor, heat exchanger and refrigerant suppliers: Use the report to identify component demand shifts and low-GWP technology opportunities.

- EPC firms and system integrators: Need adoption trends and buyer criteria to build retrofit and turnkey project pipelines.

- Food, beverage, chemical, pharmaceutical, paper and textile manufacturers: Use the report to benchmark decarbonization options and investment timing.

- Utilities and energy service companies: Need insights into electrified heat load creation, flexibility and heat-as-a-service models.

- Investors and private equity firms: Use the report to evaluate growth platforms, M&A targets and technology risk.

- Government agencies and policy bodies: Need market evidence for subsidy design, industrial emissions policy and clean heat programs.

Who Should Buy this Report?

This report should be purchased by organizations that need a practical view of market size, forecast, share, growth, country specific market opportunities, procurement criteria and competitive positioning. It is most useful for teams converting industrial decarbonization interest into commercial strategy, investment planning, product development or regional expansion decisions.

- Industrial heat pump OEMs seeking application prioritization and regional growth mapping.

- Compressor, heat exchanger, controls and refrigerant suppliers assessing component demand.

- EPC firms and system integrators building industrial electrification pipelines.

- Food, beverage, chemicals, pulp and paper and pharmaceutical manufacturers benchmarking decarbonization options.

- Utilities and renewable power developers evaluating flexible industrial electricity demand.

- Investors, private equity firms and corporate strategy teams screening acquisition and funding opportunities.

- Government bodies and economic development agencies assessing policy impact and clean industrial heat adoption.

Why Choose DataM Intelligence?

- Business outcome focus: DataM Intelligence links market size, share and forecast analysis to commercial decisions such as product launches, geographic expansion, pricing strategy and partnership targeting.

- Competitive strategy support: The report helps clients benchmark major players, identify white space and understand how portfolio focus affects future growth.

- Country specific intelligence: DataM highlights market, size and share trends across priority countries to guide sales allocation and local entry planning.

- Procurement insight: The analysis clarifies buyer decision criteria, risk considerations and procurement priorities for industrial heat pump solutions.

- Investment prioritization: DataM supports investors by mapping funding, M&A, technology readiness and high-growth application clusters.

- Actionable segmentation: The report breaks down heat source, capacity, temperature, refrigerant, application and end-use segments to support targeted go-to-market execution.