Overview

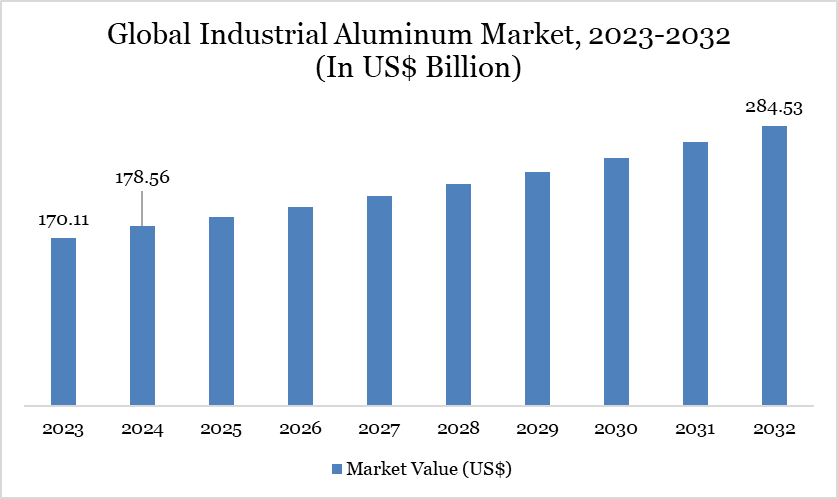

The global Industrial Aluminum market reached US$178.56 billion in 2024 and is expected to reach US$284.53 billion by 2032, growing at a CAGR of 6.11% during the forecast period 2025-2032.

The Industrial Aluminum market is being driven by rising demand across automotive, aerospace, and construction sectors due to its lightweight, corrosion-resistant, and recyclable properties. Increasing adoption in electric vehicles and renewable energy applications is further propelling market growth. Urbanization and infrastructural development, especially in emerging economies, are boosting aluminum consumption in building facades, transportation, and packaging industries.

According to the WBMS report, global Industrial Aluminum production in February 2025 reached 5.6846 million tons, slightly exceeding consumption of 5.6613 million tons, creating a surplus of 23,300 tons. In the first two months of 2025, production totaled 11.7991 million tons, while consumption was 11.6124 million tons, resulting in a cumulative surplus of 186,700 tons. This surplus, along with steady demand growth, indicates a stable market environment with potential for gradual expansion in the coming years.

Industrial Aluminum Market Trend

The Industrial aluminum market is witnessing steady growth driven by rising demand from automotive, construction, and aerospace sectors. Lightweighting initiatives and sustainability trends are boosting aluminum adoption over heavier metals. Technological advancements in production and recycling are improving efficiency and reducing environmental impact. Globally, market dynamics are influenced by supply-demand imbalances, as seen in recent WBMS data showing slight production surpluses.

Market Scope

Metrics | Details |

By Product Type | Primary Aluminum, Secondary Aluminum |

By Alloy Type | Wrought Alloys, Cast Alloys |

By Form | Plates, Sheets, Foils, Rods & Bars, Castings, Others |

By Process | Casting, Rolling, Extrusion, Forging, Others |

By Application | Automotive & Transportation, Building & Construction, Electrical & Electronics, Packaging, Consumer Goods, Others |

By Region | North America, South America, Europe, Asia-Pacific, Middle East and Africa |

Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Market Dynamics

Growing Demand in Automotive Sector

The growing demand in the automotive sector is a key driver for the industrial aluminum market as manufacturers increasingly prioritize lightweight materials to improve fuel efficiency and reduce vehicle emissions. Aluminum alloys, with their high strength-to-weight ratio, are ideal for body panels, engine components, and chassis structures. On 25 June 2025, National Aluminium Company Limited (NALCO), a Navratna CPSE under the Ministry of Mines, launched its IA90 Grade Aluminium Alloy Ingot specifically to meet the evolving needs of the automotive industry, highlighting how producers are innovating to support these requirements.

This trend is further fueled by the global shift towards electric vehicles (EVs), which rely heavily on aluminum to offset battery weight while maintaining structural integrity. The introduction of advanced alloys like IA90 allows automakers to optimize performance without compromising safety or design. As automotive production grows in emerging and developed markets alike, demand for high-quality industrial aluminum continues to surge. Consequently, innovations in aluminum alloys and targeted product launches are directly driving market expansion and adoption across the automotive sector.

High Energy Consumption and Environmental Concerns

High energy consumption in aluminum production significantly increases operational costs, making it less attractive for manufacturers to expand capacity. The smelting process requires large amounts of electricity, often generated from fossil fuels, which contributes to a high carbon footprint. As environmental concerns grow, governments are imposing stricter regulations on emissions and energy usage, further increasing compliance costs.

These regulations limit production flexibility and may slow down market expansion, especially in regions with stringent environmental policies. Companies are compelled to invest in cleaner, more efficient technologies, which requires substantial capital expenditure. The high cost of sustainable practices, combined with energy-intensive production, can reduce profit margins. Consequently, these factors collectively restrain the overall growth of the industrial aluminum market.

Segment Analysis

The global Industrial Aluminum market is segmented based on product type, alloy type, form, process, application and region

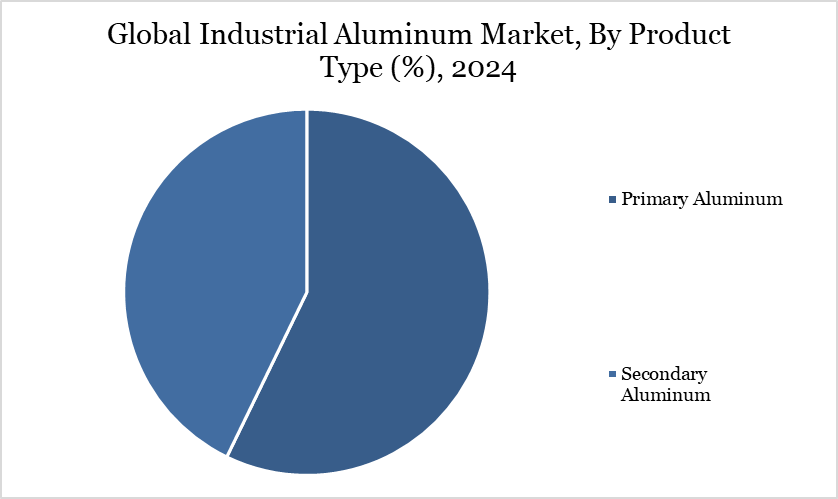

Primary Aluminum Holds a Significant Share in the Industrial Aluminum Market Due to its High Purity and Superior Mechanical Properties

Primary aluminum holds a significant share in the industrial aluminum market due to its high purity, consistent quality, and superior mechanical properties, making it ideal for applications in automotive, construction, aerospace, and electrical sectors. According to the International Aluminium Institute, total global primary aluminum production for 2024–2025 is estimated at 109,468 thousand metric tonnes, highlighting its dominant role in meeting industrial demand. China alone accounts for 65,222 thousand metric tonnes, reflecting its central position in global production and supply chains.

The large-scale production of primary aluminum ensures availability for high-performance alloys and critical industrial applications, reinforcing its market significance. Its recyclability further supports sustainable industrial practices while maintaining material integrity. With increasing industrialization and demand for lightweight, durable materials, primary aluminum continues to drive technological innovation and market growth across multiple sectors.

Geographical Penetration

Asia-Pacific is a Leading Shareholder in the Industrial Aluminum Market Due to Rapid Industrialization and Strong Demand from the Automotive and Construction

Asia-Pacific holds a significant share in the industrial aluminum market due to rapid industrialization, urbanization, and expanding infrastructure projects across the region. Countries like China, Japan, and India drive demand for aluminum in automotive, construction, and electronics sectors, where lightweight and durable materials are essential.

According to the Indian government, India, the world’s fifth-largest economy, has witnessed rapid infrastructure growth over the past decade, with budget allocations reaching US$110 billion (₹10 lakh crore) in 2023-24, highlighting the scale of construction investments. Combined with the region’s competitive production costs and availability of raw materials, this makes Asia-Pacific a dominant player in global industrial aluminum production and consumption.

Sustainability Analysis

The industrial aluminum market is increasingly prioritizing sustainability as industries face growing environmental concerns and stricter regulations, driving the adoption of circular economy practices. Aluminum’s recyclability allows companies to significantly reduce energy consumption and carbon emissions, making recycled aluminum an attractive alternative to primary production. In May 2025, Pure Aluminum, a secondary aluminum producer in Saranac, Michigan, partnered with Traxys and Consortium Metals to recycle aluminum and manufacture value-added products like secondary aluminum specification alloys, recycled secondary ingot (RSI), wrought alloys, and aluminum deoxidizers, directly supporting sustainable material flows.

This collaboration strengthens supply chains for steel, die casting, and primary aluminum industries while embedding circular economy principles into industrial processes. By promoting the reuse of materials, it enables automakers, aerospace manufacturers, and construction companies to adopt more eco-friendly solutions without compromising performance. The growing integration of recycled aluminum in high-demand sectors reduces overall environmental impact while encouraging innovation in green production technologies. As companies continue investing in sustainable practices, the industrial aluminum market is increasingly balancing profitability with environmental responsibility, demonstrating that growth and sustainability can advance hand in hand

Competitive Landscape

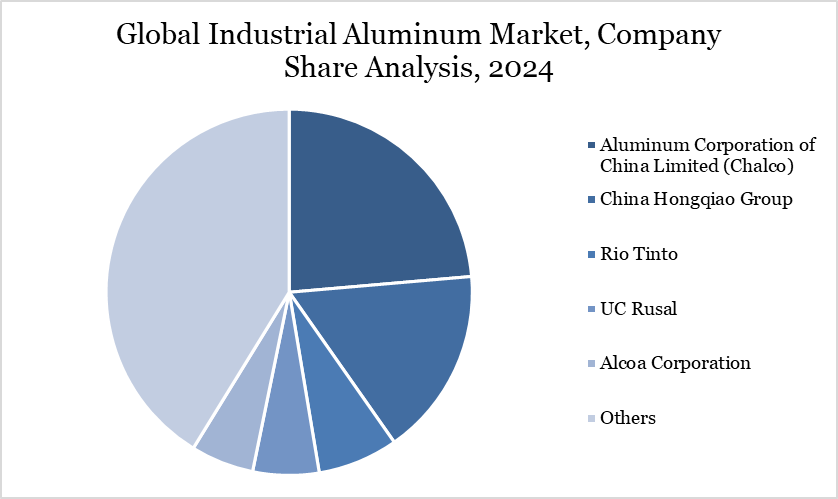

The major global players in the market include Aluminum Corporation of China Limited (Chalco), China Hongqiao Group, Rio Tinto, UC Rusal, Alcoa Corporation, Hydro Aluminium, Hindalco Industries Limited, Emirates Global Aluminium (EGA), China Minmetals Corporation, Kaiser Aluminum Corporation

Key Developments

In June 2025, the Shanghai Futures Exchange (SHFE) launched China’s first cast aluminum alloy futures and options, enabling risk management and providing transparent price signals. Produced from recycled aluminum scrap, these contracts support low-carbon development and promote the industry’s shift toward sustainable secondary aluminum.

In March 2024, Emirates Global Aluminium (EGA) signed an agreement to acquire German secondary aluminum producer Leichtmetall Aluminium Giesserei Hannover GmbH. The specialty foundry, producing up to 30,000 metric tons annually with 80% recycled aluminum and using renewable energy, strengthens EGA’s global growth in low-carbon primary and recycled aluminum.

Why Choose DataM?

Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience 2024

Manufacturers/ Buyers

Industry Investors/Investment Bankers

Research Professionals

Emerging Companies