In Vivo Gene Editing Market Overview

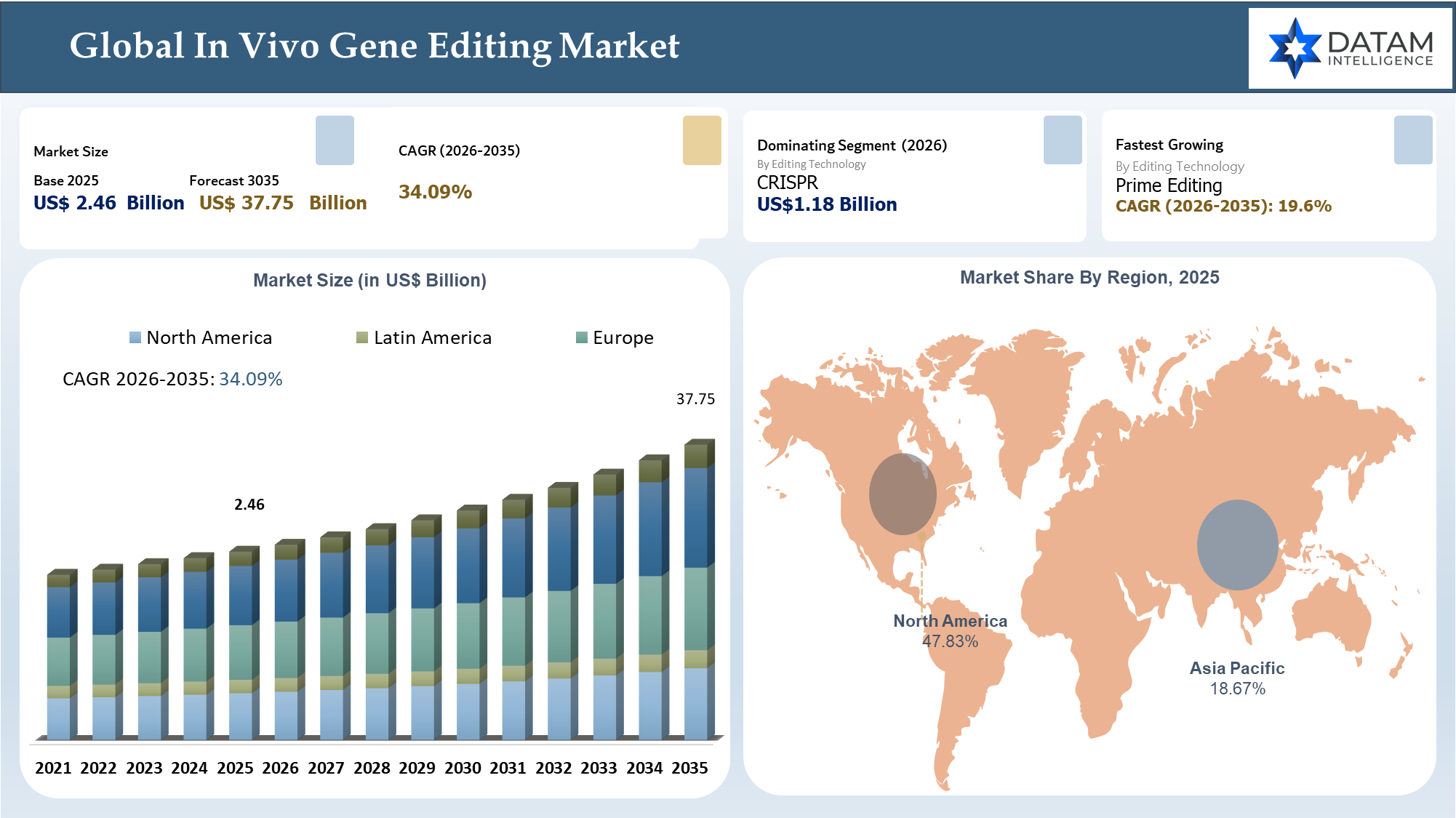

The Global In Vivo Gene Editing Market reached US$ 2.46 billion in 2025 and is expected to reach US$ 37.75 billion by 2035, growing with a CAGR of 34.09% during the forecast period 2026-2035.

Strategically, the In Vivo Gene Editing Market has gained significance because of the capability to modify disease-causing genes directly inside the body of the patient and potentially provide a one-time solution for rare diseases affecting genetics, metabolism, heart, eyes, and nervous system. Several factors influencing the market include technological advances in CRISPR gene editing, base editing, prime editing, RNA editing, and other next generation platforms along with developments in terms of virus and non-virus based methods to achieve target tissues safely.

From a commercial perspective, the focus will be on transitioning from the proof of concept towards more scalable solutions which are also easier to operate with respect to systemic treatment compared to ex vivo treatment. A significant data point for market development is the declaration of NIH stating that its Somatic Cell Genome Editing Program would fund approximately $190 million over a period of six years for development of delivery technologies, improved safety assessment and overcoming translational barriers for genome editing. Simultaneously, FDA has completed finalizing its guidelines for Human Gene Therapy Products Incorporating Human Genome Editing in January 2024.

AI Impact Analysis

The impact of AI on the In Vivo Gene Editing Market is now becoming evident in terms of improvements in the way gene editing therapies are developed, evaluated, and taken to clinical trials. Target selection, guide RNA selection, prediction of off-target effects, delivery approaches, and biological data analysis are some areas where AI algorithms are being deployed. Such applications will help reduce inefficiency and hasten decision-making during preclinical development phases by facilitating better utilization of research data and resources.

From the developer point of view, AI technology can help achieve precise editing, minimize discovery times, and help select the right therapeutic targets out of large amounts of genomic information. The ability to predict targeting tissues, immune response, and safety concerns is a core consideration for an efficient in vivo application. From a commercialization viewpoint, AI can be helpful with respect to clinical trial planning, patient stratification, biomarkers, and even manufacturing processes. Given the growing maturity of the gene editing field, those companies who combine genome editing tools and delivery systems with AI have the potential for greater development efficiency and competitive advantage.

In Vivo Gene Editing Market Industry Trends and Strategic Insights

- The delivery technology sector will continue to be the most commercially important sector, since it is an indicator of the sectors where platform investments, clinical differentiation, and translational success are most assured within the in vivo gene editing market.

- Consumers and product developers will increasingly consider factors such as editing accuracy, organ specificity, and safety enhancement, especially when it comes to controlling off-target effects, immunogenicity reduction, and achieving sustained therapeutic expression.

- The North American region will continue to exert influence over market dynamics through its dominance in terms of clinical stage innovation, regulatory involvement, financial opportunities, and commercialization of genetic diseases.

- Leading firms will maintain their competitive advantage through a combination of superior editing technologies, effective delivery systems, proprietary intellectual property, and collaborations that facilitate faster development, higher clinical assurance, and platform scalability..

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.46 Billion | |

| 2035 Projected Market Size | US$ 37.75 Billion | |

| CAGR (2026-2035) | 34.09% | |

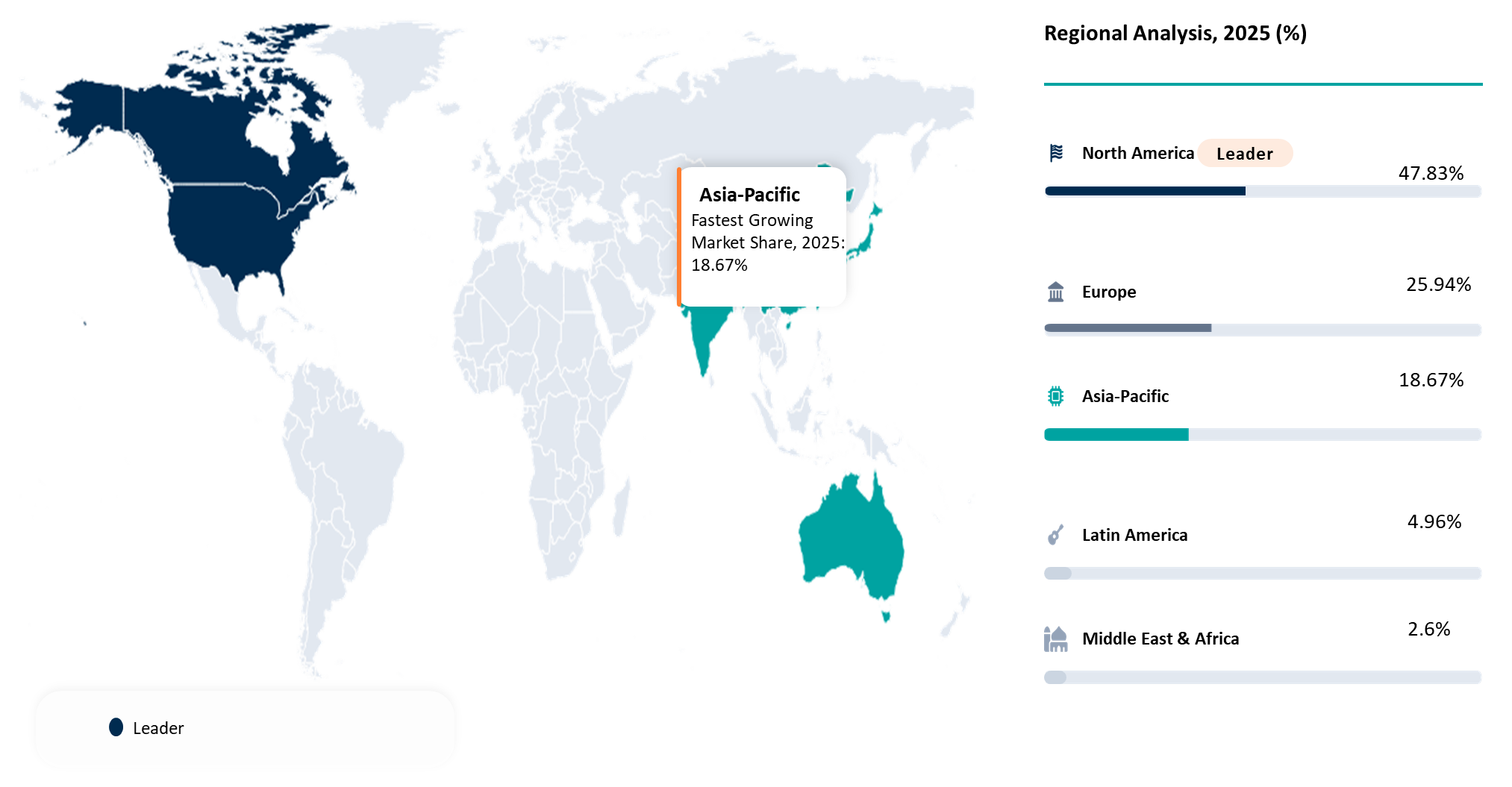

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Editing Technology | CRISPR, Base Editing, Prime Editing, TALEN, ZFN, RNA Editing, Epigenome Editing | |

| By Delivery Platform | Viral Vectors, Non Viral Delivery, Virus Like Particles | |

| By Payload Type | DNA, RNA, Protein, Ribonucleoprotein Complexes | |

| By Route of Administration | Intravenous, Intrathecal, Intravitreal, Intramuscular, Subcutaneous, Local Injection | |

| By Target Organ | Liver, Eye, Central Nervous System, Blood and Bone Marrow, Muscle, Lung, Heart, Kidney, Skin | |

| Application | Rare Genetic Disorders, Hematological Disorders, Cardiometabolic Disorders, Oncology, Neurological Disorders, Ophthalmic Disorders, Infectious Disease, Musculoskeletal Disorders | |

| Editing Outcome | Gene Knockout, Gene Correction, Gene Insertion, Gene Silencing, Gene Activation | |

| Development Stage | Discovery, Preclinical, Phase I, Phase II, Phase III, Commercial | |

| End User | Biotechnology Companies, Pharmaceutical Companies, Academic and Research Institutes, Contract Research Organizations, Hospitals and Specialty Centers | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Emerging Platform Disruption and Competitive Transformation in the In Vivo Gene Editing Market

In Vivo Gene Editing Market Size is experiencing growth through rising investments from biotech players and pharma innovators in advanced gene therapy tools designed to treat rare diseases, genetic disorders, and chronic conditions. The upcoming disruption is set to come from the combination of innovations in delivery technology, precise gene editing, and translational applications, thus driving the overall growth dynamics of the Gene Therapy Market Growth. Furthermore, the analysis of the CRISPR Therapeutics Market reveals that the competitive landscape in this segment now goes beyond editing efficiency, encompassing delivery accuracy, safety, production scale, and regulatory compliance. This trend is transforming the entire Genetic Medicine Market Trends, moving focus toward platform-based solutions versus asset-by-asset strategy. Also, according to Genome Editing Market Forecast, the introduction of in vivo technologies might be game-changing for the sector due to their potential to reduce complexity of treatment protocols linked to ex vivo gene editing..

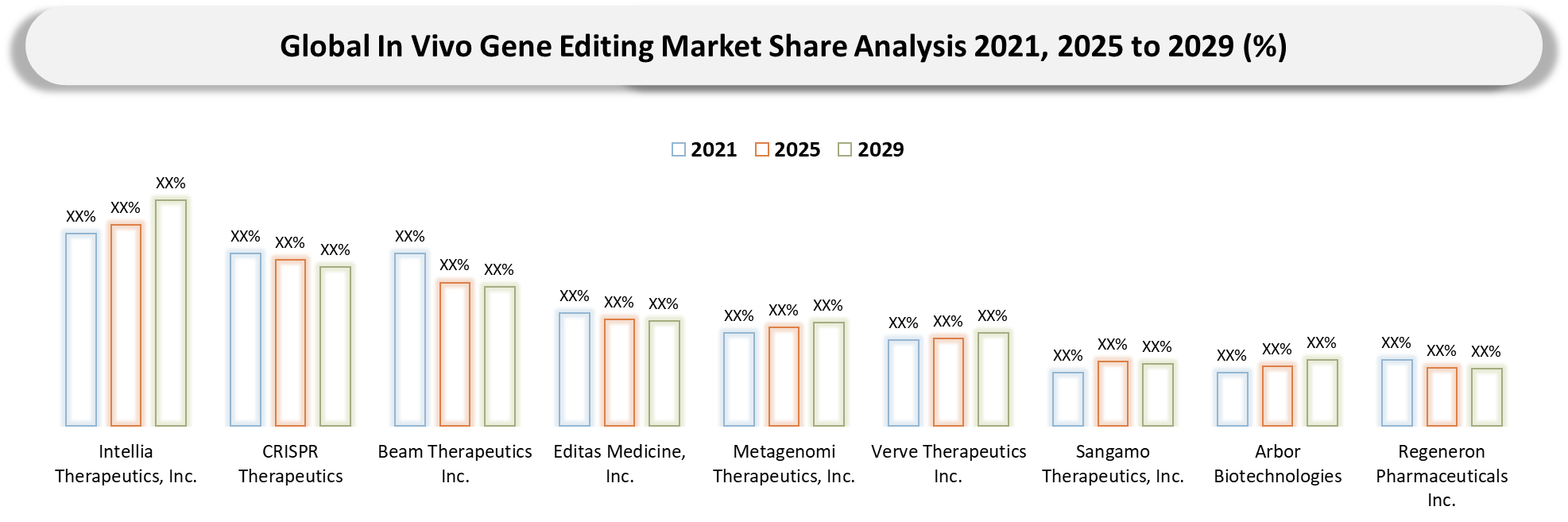

BCG Matrix: Company Evaluation

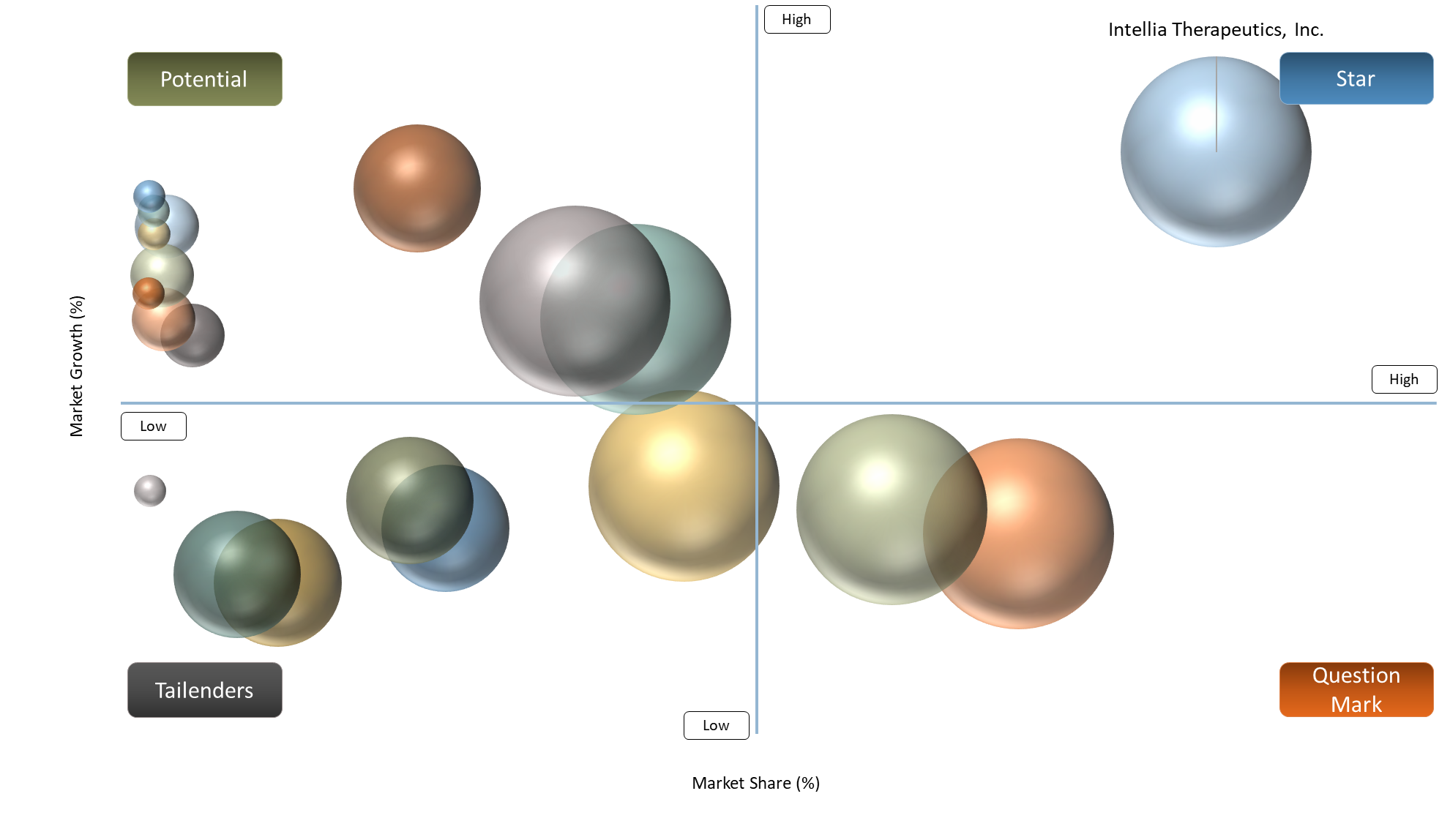

From the BCG Strategy Alignment standpoint, leaders in the In Vivo Gene Editing landscape usually comprise companies that possess superior gene editing technologies, strong clinical pipelines, and distinct delivery mechanisms. Leaders in the space include companies like Intellia Therapeutics, Inc., CRISPR Therapeutics, and Beam Therapeutics Inc. due to their first mover advantage in gene editing, unique editing mechanisms, and collaborations with major pharma giants. Their capacity for growing their clinical pipeline while building a portfolio of intellectual property gives them sustained leadership within the strategy framework.

Growth companies within the framework comprise growth-stage innovators like Editas Medicine, Inc., Prime Medicine, Inc., Verve Therapeutics Inc., and Sangamo Therapeutics, Inc.

Rising companies like Precision BioSciences, Arbor Biotechnologie, Metagenomi Therapeutics, Inc., Caribou Biosciences, Inc., Korro Bio, Inc., Mammoth Biosciences, and Scribe Therapeutics have been making waves because of their emphasis on advanced editing techniques, enzyme identification, and delivery systems. They are able to do so due to the use of platform technology licensing, partnerships, and disease-oriented innovation pipelines. On the other hand, established players like Regeneron Pharmaceuticals Inc. and Wave Life Sciences Ltd. bolster their presence using therapeutic portfolios, financial strength, and translational research expertise.

Market Dynamics

Rising demand for one time curative therapies is accelerating interest in In vivo gene editing

The increased demand for one-time curative approaches serves as one of the significant drivers for the development of the in vivo gene editing market due to a change in focus on treatment values from long-term management of diseases to the possibility of their permanent correction. Such an approach is particularly important for rare, serious liver, and cardiometabolic conditions that involve patients' lifelong treatment and impose a great clinical and financial burden on their health. Market developments also indicate increased market interest in this field. According to FDA, as of December 9, 2025, there were 48 cellular and gene therapy products approved for medical use, which indicates increased regulatory acceptance of durable treatments. At the same time, ASGCT reports about 2,041 gene, cell, and RNA therapy products currently under development, including 100 transaction deals and raising of $557.1M by advanced molecular therapy companies in 14 transactions.

Off target editing and immune response risks continue to slow broader adoption

Off-target editing and immune responses pose another huge impediment to in vivo gene editing markets since they increase risks regarding safety, regulation, and developmental expenses. The FDA has raised the alarm that there is a risk associated with off-target genome alterations in genome editing products. These off-target genome alterations can bring about inappropriate gene expression, chromosomal translocation, carcinogenesis, and tumorogenesis. This problem is especially important in the in vivo case scenario because it involves making changes to the DNA structure while the substance is administered into the body. Off-target effects of CRISPR Cas9 genome editing have been reported in many cases at a rate of 50% or higher as noted by Lyu et al. At the same time, the immune responses towards genome editing molecules can decrease the efficiency of genome editing and pose greater dangers to patients.

Segment Analysis

The global In Vivo Gene Editing Market is segmented based on editing technology, delivery platform, payload type, route of administration, target organ, application, editing outcome, development stage, end user, and region/countries.

Editing Technology Segment Driving Innovation and Competitive Differentiation in the In Vivo Gene Editing Market

The Editing Technology category is by far the most strategic segmentation for studying the In Vivo Gene Editing Market since it directly represents scientific differentiation, scalability, translatability, and investor interest. The focus here is on what constitutes competitive advantages such as improved nuclease specificity, correction accuracy, minimized off-target effects, or ability to work in conjunction with delivery vectors. From this perspective, it is safe to say that CRISPR technologies possess the highest commercial and clinical relevance due to their programmable nature and increasing amount of proof-of-concept evidence involving human patients. An example of this is the study done by Intellia and reported in The New England Journal of Medicine, in which 6 patients were treated systemically using in vivo CRISPR-Cas9 therapy and experienced a mean reduction of 87% in serum transthyretin levels at day 28, with the range being from 80% to 96%. With regard to future developments, one may safely predict increased relevance of base editing and prime editing due to the market’s evolution towards improved precision and wider mutation spectrum coverage.

Geographical Penetration

North America Leadership Driven by Clinical Innovation and Regulatory Readiness in the In Vivo Gene Editing Market

North America is the major player within the In Vivo Gene Editing Market since it is the only market that possesses the most developed clinical infrastructure, the strongest translational research foundation, and the best regulatory environment for genome editing therapeutics. North America, headed by the United States, has served as the birthplace of multiple in vivo genome editing milestones, thereby creating an advantageous position for the commercialization of such products from the lab bench to the patient bedside. For instance, Intellia's NTLA-2001, published in The New England Journal of Medicine, was the first in vivo genome editing therapy utilizing CRISPR-Cas9 delivered systemically in humans. This pilot study, in which six subjects received treatment, demonstrated the reduction of serum transthyretin between 52% and 87% by day 28.

This is made even more certain by the public sector contributions and clear regulations. The NIH stated that it will spend about $190 million in six years on improving delivery methods, creating safe genome editors, and developing tools that will speed up clinical translation through the Somatic Cell Genome Editing program. Simultaneously, the FDA came out with the guidance document on Human Gene Therapy Products Incorporating Human Genome Editing in January 2024, stating how sponsors need to incorporate elements in their IND application for each step of product development including design, manufacturing, non-clinical safety, and clinical trials.

U.S. In Vivo Gene Editing Market Trends

The United States is considered the key country-level driving factor influencing the In Vivo Gene Editing Market. The U.S. has numerous innovations that contribute to the market, including highly advanced clinical trials and early regulations of genome editing. The United States is home to several top genome editing companies, such as Intellia Therapeutics, Inc., Editas Medicine, Inc., and Beam Therapeutics Inc., whose activities include developing innovative in vivo therapeutic approaches. One of the main milestones is associated with the successful in vivo human studies conducted by Intellia using the CRISPR-Cas9 system for treating hereditary transthyretin amyloidosis. As a result, participants of the study managed to experience up to 87 percent reduction in the levels of serum transthyretin protein within 28 days after treatment. Hence, the United States is recognized as one of the best validation centers for clinical genome editing. Moreover, the National Institutes of Health began a somatic cell genome editing program that aims at improving delivery, editing specificity, and safety evaluation techniques. It is planned to fund the program with approximately $190 million within six years. Additionally, the U.S. Food and Drug Administration released guidelines concerning genome editing in 2024.

Canada In Vivo Gene Editing Market Outlook

Canada is positioning itself as a strategically significant nation within the In Vivo Gene Editing Market due to its rich genomics research capabilities, financial backing from the government, and increasing translational framework for developing genetic medicines. The strength of Canada does not rely solely on its size, but rather on its ability to foster innovation capabilities through nationally orchestrated programs. According to the Government of Canada, it has pledged more than US$1.6 billion over a span of two decades through the Genome Canada fund for extensive applied and translational genomics. This investment reflects its ongoing commitment to the genomics community, which enables innovation in gene editing technology. Furthermore, Genome Canada noted that US$105.5 million was spent on genomics research during 2023-24, including US$46.5 million from Genome Canada and US$ 59 million from co-funders. Canada is further enhancing its capacity to go downstream. According to the National Research Council, Canada’s Genome Foundry is becoming one of the country’s premier research institutions where researchers can not only develop and design but also fine-tune their cell therapies under one roof, which is expected to enable more efficient translation of advanced therapies from idea to practice. In sum, Canada continues to evolve into an important innovation hub for in vivo gene editing.

Competitive Landscape

- The nature of competition within the In Vivo Gene Editing Market is evolving into one where differentiation arises from companies developing wide-ranging platforms versus those developing a more targeted, indication-driven approach. Some of the major players operating within the market include Intellia Therapeutics, Inc., CRISPR Therapeutics, Beam Therapeutics Inc., Editas Medicine, Inc., Prime Medicine, Inc., Verve Therapeutics Inc., Sangamo Therapeutics, Inc., Arbor Biotechnologies, Metagenomi Therapeutics, Inc., Regeneron Pharmaceuticals Inc., Wave Life Sciences Ltd., Korro Bio, Inc., Mammoth Biosciences, and Scribe Therapeutics. The former group includes Intellia and Verve that focus on in vivo studies as well as liver targeting. Other players include Beam, which is developing a platform technology for single-administration liver targeting. Additionally, Sangamo remains differentiated through its platform and delivery technology, whereas Regeneron offers a more supportive function through scale, capital, and translational benefits via its in vivo programs.

- On the contrary, companies like Precision BioSciences, Caribou Biosciences, Inc., and disease-oriented or modality-oriented startups such as Verve Therapeutics Inc., Korro Bio, Inc., and Wave Life Sciences Ltd. may gain advantage through focusing on therapeutic indications, better applicability, or unique forms of genome editing, rather than a broad platform. This means that it is not the company with the most expansive genome editing capabilities that dictates the competitive dynamics within the industry. Instead, companies that are able to control the entire value chain from target identification, to delivery technology development, to regulatory approvals, and even to demonstrating sustained efficacy will win the day. Those companies that can successfully position themselves for in vivo delivery, optimization of safety profiles, and consistent clinical results will secure their ability to retain pricing power, develop partnerships, and achieve dominance within the industry.

Key Developments

- March 2025 - Arbor Biotechnologies announced a US$73.9 million Series C financing to advance its gene editing pipeline in liver and central nervous system disorders, strengthening its ability to scale clinical development and reinforce its position in next-generation in vivo genetic medicines.

- March 2025 - Verve Therapeutics announced that the U.S. FDA cleared the IND application for VERVE-102, enabling clinical development of its investigational in vivo base editing medicine targeting PCSK9 for patients with heterozygous familial hypercholesterolemia and premature coronary artery disease.

- April 2025 - Verve Therapeutics reported positive initial data from the Heart-2 clinical trial of VERVE-102, highlighting dose-dependent LDL-C reductions and reinforcing the clinical promise of single-course in vivo base editing for cardiovascular disease.

- May 2025 - Prime Medicine announced a strategic restructuring to focus resources on high-priority programs, sharpening its execution around differentiated gene editing programs and improving capital allocation toward areas with stronger clinical and commercial potential.

- June 2025 - Intellia Therapeutics announced positive three-year Phase 1 data for lonvo-z in hereditary angioedema, reinforcing confidence in the durability of one-time in vivo CRISPR-based therapies and supporting the broader market case for long-term therapeutic benefit from systemic editing approaches.

- July 2025 - Arbor Biotechnologies announced that the first patient was dosed in the redePHine Phase 1/2 study of ABO-101 at Mayo Clinic, marking an important clinical milestone for its investigational one-time IV-administered gene editing treatment for primary hyperoxaluria type 1.

- September 2025 - Editas Medicine announced the nomination of EDIT-401 as its lead in vivo development candidate, signaling a sharper strategic push into in vivo gene editing and strengthening its positioning in liver-directed cardiovascular applications.

White Space Opportunities

DataM recognizes a compelling white space opportunity in the In Vivo Gene Editing Market beyond the obvious race for platform scalability. Where much of the market is concentrated on blockbuster rare disease programs and the high-profile discussions around CRISPR technologies, there still exist underdeveloped niches within therapy areas where delivery precision, tissue selectivity, and practical clinical endpoints can provide more immediate value. Within these niches, the buyer or partner could be less concerned about platform scalability and more interested in the translatability, safety, and clear path forward. This may mean that the best strategy would be a narrow approach rather than trying to achieve as broad an indication portfolio as possible.

The second opportunity associated with the use of white spaces is not limited to technological editing capabilities alone, but also includes the packaging of the capabilities by suppliers in such a way that they can be evaluated and utilized effectively. Those suppliers that offer easy integration, evaluation, and validation of capabilities are more likely to win over others who just focus on technological editing. It must be understood that this market does not require sophisticated editing skills; rather, it requires a platform capability proposition in terms of delivery, manufacturing, and clinical execution.

DMI Opinion

According to DataM, the In Vivo Gene Editing Market is no longer determined by novelty but rather by the ability of gene editing developers to leverage their technology and convert it into something that works in a clinical setting. It is all about delivery predictability, safety, and effectiveness of the process rather than its capability to perform certain edits. In this situation, success does not lie in possessing the widest range of possible genetic manipulation but in delivering real results.

As per DataM, while many organizations continue to emphasize their editing abilities and platform advances, the real business issue is the ability to deliver with efficiency, tissue specificity, manufacturability, and safety validation in the long term. Organizations that are doing well in developing in vivo gene editing solutions are those with more narrow, yet clinically relevant applications in which the concept can be proven through clear endpoints and smaller patient populations. Therefore, the In Vivo Gene Editing Market must be seen as a precision development market, where organizations can succeed by lowering translational risks, improving clinical implementation, and developing treatment models.

Why Choose DataM?

- Technological Developments: Includes innovations in CRISPR technologies, base editing, prime editing, zinc finger systems, RNA editing, virus-based and non-virus-based delivery systems, lipid nanoparticles, tissue targeting methods, guide RNA design, and safety improvement tools.

- Market Positioning of Leading Competitors: Offers positioning of leading competitors on the basis of platform expertise, delivery capabilities, pipeline progress, indications, partnering capabilities, manufacturing proficiency, and ability to convert editing science into clinical benefits.

- Market Trends and Dynamics: Highlights market trends related to increasing popularity of one-time therapies, greater importance of tissue-specific delivery, need for more secure editing techniques, evolving regulation, platform multiplicity, and collaboration between biotechnology firms and pharmaceutical companies.

- Strategies Adopted by Key Players: Describes strategies employed by leading competitors, including pipeline extension, platform licensing, disease indication-specific development, partnering-driven validation, delivery technology refinement, and portfolio diversification using next-generation editing platforms.

- Pricing and Accessibility of the In Vivo Gene Editing Market: Considers issues such as drug development expenditures, manufacturing complexities, investment in clinical trials, regulatory considerations, reimbursement prospects, difficulties in patient accessibility, and affordability obstacles associated with cutting-edge treatments.

Target Audience 2026

- Biotechnology and gene therapy companies

- Pharmaceutical research and development teams

- Corporate strategy and market intelligence teams

- Clinical development and translational medicine leaders

- Business development and licensing teams

- Investors, venture capital, and private equity firms

- Academic and research institutions

- Contract research organizations and CDMOs

- Regulatory affairs and commercialization teams

- Consulting and healthcare advisory firms.