High-Performance Pigments Market Overview

Color is no longer just an aesthetic input. In modern manufacturing, pigments are expected to deliver durability, regulatory compliance, and lifecycle performance. This shift is reshaping procurement strategies across coatings, plastics, inks, and specialty applications, positioning high-performance pigments as a critical material category rather than a commodity.

What makes this market strategically important now is the convergence of three forces: stricter environmental regulations, rising demand for long-lasting coatings, and the shift toward premium materials in emerging economies. Buyers are increasingly prioritizing pigments that reduce maintenance costs, improve product lifespan, and meet sustainability standards.

Market Scope

| Metric | Details |

| Market Size (2025) | USD 5.49 Billion |

| Market Size (2035) | USD 9.40 Billion |

| CAGR (2026–2033) | 5.50% |

| Historic Years | 2023–2024 |

| Base Year | 2025 |

| Forecast Period | 2026–2035 |

| Segments Covered | Type, Application, Region |

| Leading Region | Asia-Pacific |

| Fastest Growing Region | North America |

Key Takeaways

- Coatings dominate demand, making this market highly dependent on construction, automotive, and industrial maintenance cycles.

- Inorganic pigments hold 60% share, reinforcing their importance in high-volume, durability-driven applications.

- Organic pigments are growing faster, driven by demand for brighter colors and regulatory-safe formulations.

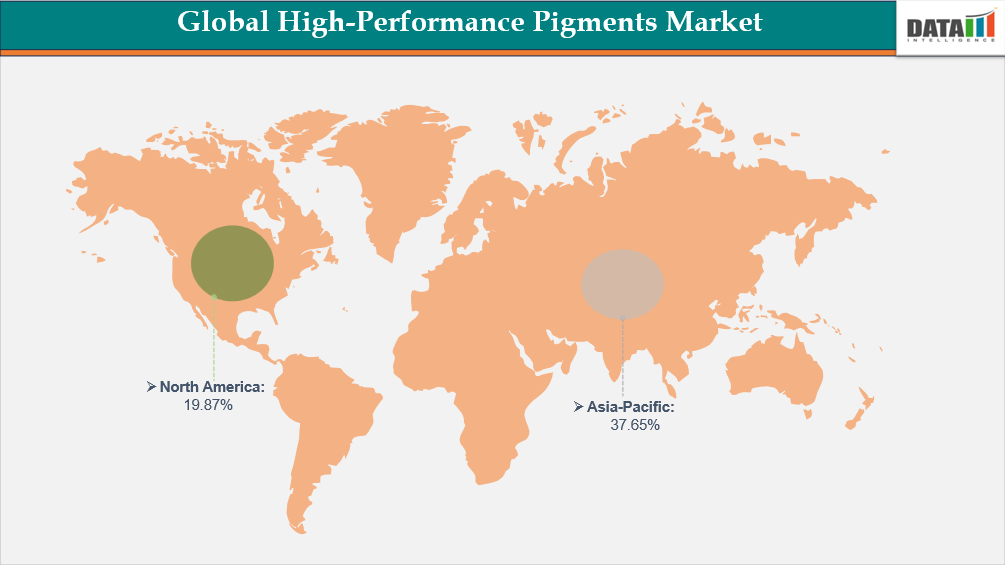

- Asia-Pacific accounts for 37% of global high-performance pigments market share, supported by large-scale industrial output.

- North America is emerging as the fastest-growing region, influenced by low-VOC regulations and premium coatings demand.

- Over 86% of architectural coatings in the U.S. are water-borne, directly increasing demand for stable, high-performance pigment systems.

- Sustainability trends indicate 35–40% of new pigment development is shifting toward eco-friendly formulations.

Market Dynamics: From Cost Efficiency to Performance Value

Demand for Long-Life Coatings is Driving Material Upgrades

Industries are increasingly prioritizing coatings that can withstand UV exposure, moisture, and chemical stress over extended periods. This is particularly evident in infrastructure, automotive, and industrial maintenance applications. High-performance pigments enable longer repaint cycles, which reduces lifecycle costs for end users.

Regulatory Pressure is Accelerating Product Innovation

Environmental regulations, particularly in North America and Europe, are pushing manufacturers toward low-VOC and non-toxic pigment systems. This is influencing R&D investment and accelerating the transition toward organic and hybrid pigments that meet compliance standards without compromising performance.

Construction and Automotive Cycles Remain Core Demand Drivers

Growth in residential and non-residential construction continues to sustain pigment demand. At the same time, automotive production, especially electric vehicles with higher plastic content, is increasing the need for heat-stable and weather-resistant pigments.

Segment Insights: Where Value is Being Created

Segmented by type (Organic High-Performance Pigments, Inorganic High-Performance Pigments, Hybrid High-Performance Pigments), by application (Coatings, Plastics, Inks, Cosmetics, Others), and by Region - Share, Trends, and Forecast to 2035.

Inorganic Pigments: The Structural Backbone

Inorganic pigments account for around 60% of the high-performance pigments market share, driven by their cost efficiency, UV resistance, and thermal stability. These pigments are widely used in coatings, construction materials, and automotive finishes where durability is critical.

Synthetic inorganic pigments, including iron oxides and titanium dioxide, dominate due to their consistent quality and scalability.

Organic Pigments: Growth Driven by Aesthetic and Compliance Needs

Organic pigments are gaining traction in applications requiring vibrant colors and precise shade control, such as printing inks, packaging, and consumer goods. Their adoption is further supported by regulatory shifts away from heavy-metal-based pigments.

Coatings Application: The Largest Revenue Contributor

Coatings remain the dominant application segment, supported by demand from construction, automotive, and industrial sectors. The need for weather resistance, corrosion protection, and aesthetic retention makes high-performance pigments indispensable in this segment.

Regional Analysis: Demand Patterns and Industrial Strength

Asia-Pacific: Volume Leadership Backed by Industrial Expansion

Asia-Pacific holds approximately 37% of global high-performance pigments market share, making it the dominant region. High construction spending exceeding USD 2.3 trillion and coatings production above 48 million tonnes underline the region’s scale.

China leads with massive coatings and automotive output, while India is emerging as a high-growth market driven by packaging, automotive, and export demand.

North America: Growth Led by Regulation and Premiumization

North America is the fastest-growing region, supported by regulatory mandates for low-VOC coatings and increased demand for durable materials. The U.S. coatings industry alone generated USD 31.5 billion in shipments , creating strong downstream demand for high-performance pigments.

Europe: Sustainability-Driven Adoption

Europe’s market is shaped by strict environmental standards and a strong focus on sustainable materials. Adoption of eco-friendly pigments and circular manufacturing processes is accelerating across industries.

Competitive Landscape: Innovation and Compliance Define Leadership

The high-performance pigments market is highly competitive, with leading players focusing on advanced material science, regulatory compliance, and application-specific innovation.

Key companies include DuPont, BASF, Solvay, Evonik, Arkema, Celanese, Toray, SABIC, Victrex, and 3M.

Competitive strategies include:

- Development of low-toxicity and sustainable pigment formulations

- Expansion of production capacity in high-growth regions

- Strengthening partnerships with coatings and plastics manufacturers

- Investment in R&D for improved dispersion, stability, and color performance

Companies with strong technical support and global supply chain capabilities are better positioned to secure long-term contracts with OEMs and industrial buyers.

Recent Developments

In June 2026, BASF SE expanded its high-performance pigment portfolio with advanced color solutions designed for automotive and industrial coatings. The innovation focuses on enhanced durability and color stability. This supports long-lasting coating applications.

In May 2026, Clariant AG introduced new high-performance pigments with improved heat resistance and environmental compliance for plastics and coatings. The development enhances product performance and sustainability. This benefits multiple end-use industries.

In April 2026, DIC Corporation launched innovative organic pigments for high-end applications such as packaging inks and specialty coatings. The development improves color strength and dispersion properties. This supports premium product requirements.

In March 2026, Heubach Group strengthened its pigment portfolio with high-performance solutions offering superior lightfastness and chemical resistance. The innovation focuses on durability and regulatory compliance. This supports industrial applications.

In February 2026, Sun Chemical Corporation expanded its advanced pigment solutions with products designed for digital printing and high-performance coatings. The development improves color consistency and performance. This benefits printing and packaging sectors.

In January 2026, Venator Materials PLC introduced high-performance inorganic pigments with enhanced opacity and UV resistance for construction and coatings applications. The focus is on durability and efficiency. This supports infrastructure development.

Sustainability and Regulatory Outlook

Sustainability is becoming a central purchasing criterion. Manufacturers are shifting toward low-toxicity pigments, reducing emissions through energy-efficient processes, and adopting circular production models.

Regulatory frameworks are tightening globally, encouraging the use of environmentally safe materials and increasing transparency across supply chains. Companies that align with these requirements are gaining competitive advantage.

Strategic Insights and Investment Perspective

The high-performance pigments market is evolving toward value-added applications where performance, compliance, and sustainability determine pricing power.

Key opportunities include:

- Expansion into specialty and effect pigments

- Development of bio-based and recyclable pigment systems

- Targeting high-growth sectors such as packaging and EVs

- Leveraging regional manufacturing capabilities to reduce costs

Risks include raw material price volatility and regulatory uncertainties, particularly for legacy pigment chemistries.

What Sets This Global High-Performance Pigments Market Intelligence Report Apart

- Latest Data & Forecasts – Comprehensive, up-to-date insights and projections through 2032. Coverage includes global market value by type and application segments. Scenario forecasts include region-level splits (North America, Europe, Asia-Pacific, South America, Middle East & Africa) with sensitivity to factors such as raw-material price volatility, technological adoption, and regulatory changes.

- Regulatory Intelligence – Actionable analysis of regulatory frameworks impacting HPP commercialization, including polymer approvals, export/import controls, environmental compliance, permissible additives, and regional safety or labeling standards.

- Competitive Benchmarking – Standardized profiling and benchmarking of leading polymer manufacturers, specialty chemical companies, contract manufacturers, and high-performance material suppliers active in the market.

- Geographic & Emerging Market Coverage – Region-by-region market sizing, growth drivers, adoption dynamics, industrial demand, and market access considerations. Focus on high-growth regions and markets with evolving regulations.

- Actionable Strategies – Identify opportunities for launching innovative polymer grades, high-value applications, and new formulations, while leveraging strategic partnerships, licensing, and supply chain integration for maximum ROI.

- Pricing & Cost Analysis – In-depth assessment of price trends, raw material costs, production efficiencies, and sustainability-driven cost management across regional markets.

- Expert Analysis – Insights from industry experts, including polymer engineers, regulatory affairs specialists, and senior executives from leading HPP manufacturing companies.

Target Audience

- Pigment manufacturers and chemical companies

- Paints and coatings producers

- Plastics and packaging companies

- Automotive and construction firms

- Investors and market analysts

- Regulatory and compliance professionals