Overview

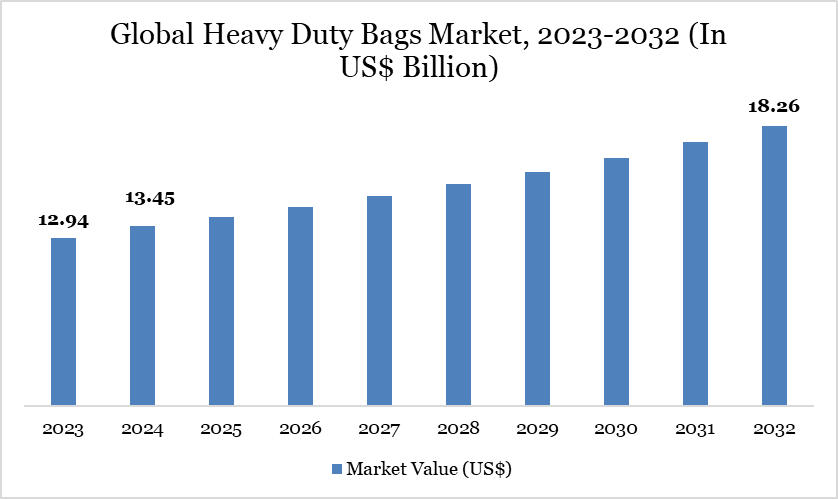

The global heavy duty bags market reached US$13.45 billion in 2024 and is expected to reach US$18.26 billion by 2032, growing at a CAGR of 3.90% during the forecast period 2025-2032.

The global heavy-duty bag market lies at a meeting point of industrial necessity and environmental development. On the one hand, demand remains robust in the construction, agriculture, food and chemical sectors, with bulk products necessitating durable and dependable packaging to support increased global trade and infrastructure development.

On the other hand, growing environmental scrutiny and raw material volatility pose challenges to existing corporate strategies. Governments and regulators are increasing restrictions on single-use plastics, driving manufacturers to explore with recyclable, biodegradable and reusable options. Meanwhile, digitalization is altering the competitive landscape, with smart packaging solutions increasing traceability and supply chain efficiency.

Heavy Duty Bags Market Trend

The integration of digital tracking and smart packaging technologies has become a game changer in the heavy-duty bag market. Manufacturers are progressively integrating RFID tags, barcodes and QR codes inside bags to improve traceability across the supply chain. This enables manufacturers, distributors and end users to track the location, handling circumstances and storage status of bulk products in real time.

Such improvements are quickly becoming commonplace in industries like chemicals and pharmaceuticals, which demand strict adherence to safety and traceability norms. In logistics-heavy sectors such as cement and agriculture, smart packaging helps optimize warehouse management, reduce theft and minimize losses due to spoilage or mismanagement.

Market Scope

Metrics | Details |

By Material | Plastic, Paper, Jute, Others |

By Product | Open Mouth Bags, Pasted Valve Bags, Gusset Bags, Woven Bags, Others |

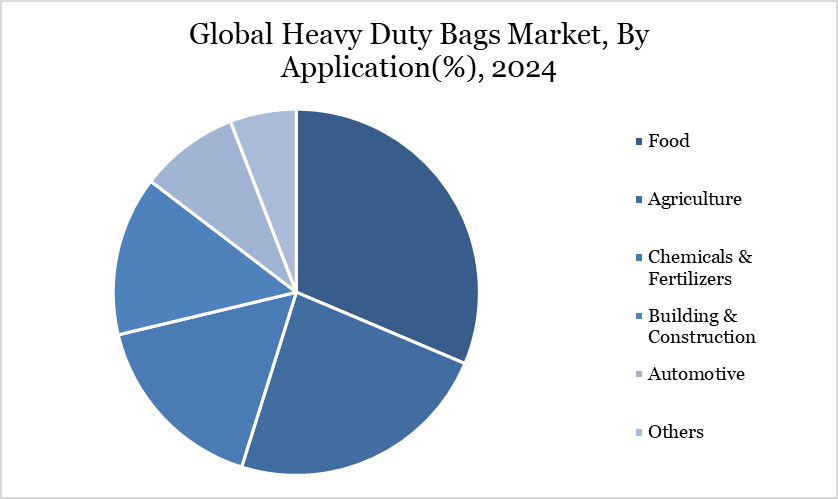

By Application | Food, Agriculture, Chemicals & Fertilizers, Building & Construction, Automotive, Others |

By Region | North America, South America, Europe, Asia-Pacific, Middle East and Africa |

Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Market Dynamics

Rising Global Agricultural Trade

One of the most important drivers of the global heavy-duty bag market is the expansion of international agricultural commerce. Brazil exports soybeans, India exports rice and the United States is a significant producer of corn and wheat, thus the demand for packaging solutions that can handle big volumes without sacrificing product quality has never been greater. Long-distance shipments require strong, tear-resistant bags that protect against pests and moisture.

Fertilizers and animal feed are being increasingly packaged in heavy-duty woven polypropylene or polyethylene sacks, which have become the preferred packaging solution across rural and industrial supply chains. The transition to value-added food exports in Asia-Pacific, Africa and Latin America has broadened the use of heavy-duty packaging for processed agricultural products. As worldwide demand for food security and commodity exports continues to climb, heavy-duty bags are rising in demand, establishing agriculture as the major driver for this market.

Volatility in Raw Material Price

Despite their increasing utility, the market for heavy-duty bags is constrained by raw material price instability. Most heavy-duty bags are made of polypropylene and polyethylene, therefore their production costs are linked to crude oil prices. Any movement in the oil market, whether due to geopolitical tensions, OPEC production cuts or supply disruptions, has an immediate impact on polymer resin pricing, resulting in cost instability for bag producers.

For example, during oil price spikes, the cost of polypropylene granules can climb dramatically, making it difficult for packaging companies to maintain consistent profitability. Smaller regional manufacturers are susceptible because they lack purchasing power and hedging tools to mitigate price changes. In a price-sensitive industry where modest changes in material costs may have consequences across the supply chain, such instability acts as a barrier to expansion for the market.

Segment Analysis

The global heavy duty bags market is segmented based on material, product, application and region.

Rising Reliance of the Food Sector on Bulk Packaging

In 2024, food accounted for the vast bulk of the worldwide market. The food industry's increasing need for hermetic and durable bulk packaging, ranging from grains and flour to sugar and seeds, is a major driver of demand for heavy-duty bags. Purdue Improved Crop Storage bags, which have dual polyethylene liners and a woven polypropylene outer layer, protect against pests and moisture, allowing smallholder farmers in Africa and parts of Asia to reduce post-harvest losses by keeping grains viable for months without the use of insecticides.

Adoption of hermetic bagging technologies has increased across global food supply chains where quality, spoilage reduction and safety are critical. The benefits highlight why the food sector continues to lead demand for durable, high-capacity packaging in countries with demanding storage and transportation circumstances.

Geographical Penetration

Rapid Expansion in Agriculture and Construction Setors Drives Asia-Pacific Market

Asia-Pacific had the largest geographical contribution, accounting for over 40% of worldwide revenue in 2024, because to thriving industries such as construction, agriculture and food packaging. The region's strong rise in agricultural and construction, both fundamental applications of heavy-duty packing, is a primary driver of the Asia-Pacific heavy-duty bag market. As per the Department of Fertilizers, fertilizer usage in India would exceed 62 million tons by 2023, resulting in a steady demand for woven polypropylene and polyethylene bags to store and transport bulk fertilizers and grains.

Similarly, China's cement output exceeds 2 billion tons per year (National Bureau of Statistics of China), necessitating a huge supply of heavy-duty bags for cement and construction supplies. Beyond agricultural and construction, the region's rapidly expanding e-commerce sector—particularly in Southeast Asia, is promoting greater use of reusable and high-strength bags for logistics and last-mile delivery. These dynamics demonstrate that structural industrial and agricultural growth, combined with packaging needs in transportation, are the major drivers propelling heavy duty bag demand across Asia-Pacific.

Sustainability Analysis

The heavy-duty bag sector is rapidly embracing circular economy principles by incorporating recycled components into its main products. Gravis's novel flexible intermediate bulk container (FIBC), composed entirely of recycled PET (rPET), has a 70% lower carbon footprint than typical virgin polypropylene bags.

Each shipment of 48 pallets using these rPET bags saves roughly 26 metric tons of CO₂, highlighting practical improvements in emission reduction through material innovation. Simultaneously, prominent producers are experimenting with biodegradable and compostable options, such as bio-based heavy-duty bags utilizing polymers like BASF's Ecovio®, in line with increased regulatory expectations for ecologically friendly packaging materials.

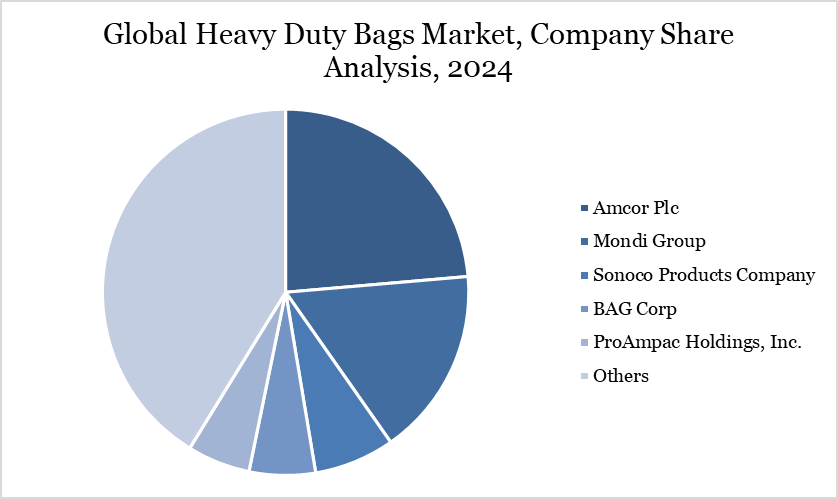

Competitive Landscape

The major global players in the market include Amcor Plc, Mondi Group, Sonoco Products Company, BAG Corp, ProAmpac Holdings, Inc., Novolex Holdings, Inc., LC Packaging International BV, Nihon Matai Co.,Ltd., Siko Co., Ltd. and Dow Inc..

Key Developments

In May 2024, Sonoco Products Company opened a new multi-billion-dollar complex at 2850 Charter Street in Columbus, Ohio.

In Septmeber 2023, Berry Global announced to introduce heavy-duty bags made from recovered ocean plastic. The new range is designed to significantly strengthen the company's sustainability standards.

Why Choose DataM?

Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience 2024

Manufacturers/ Buyers

Industry Investors/Investment Bankers

Research Professionals

Emerging Companies