Healthcare Robotics Systems Market Size and Forecast

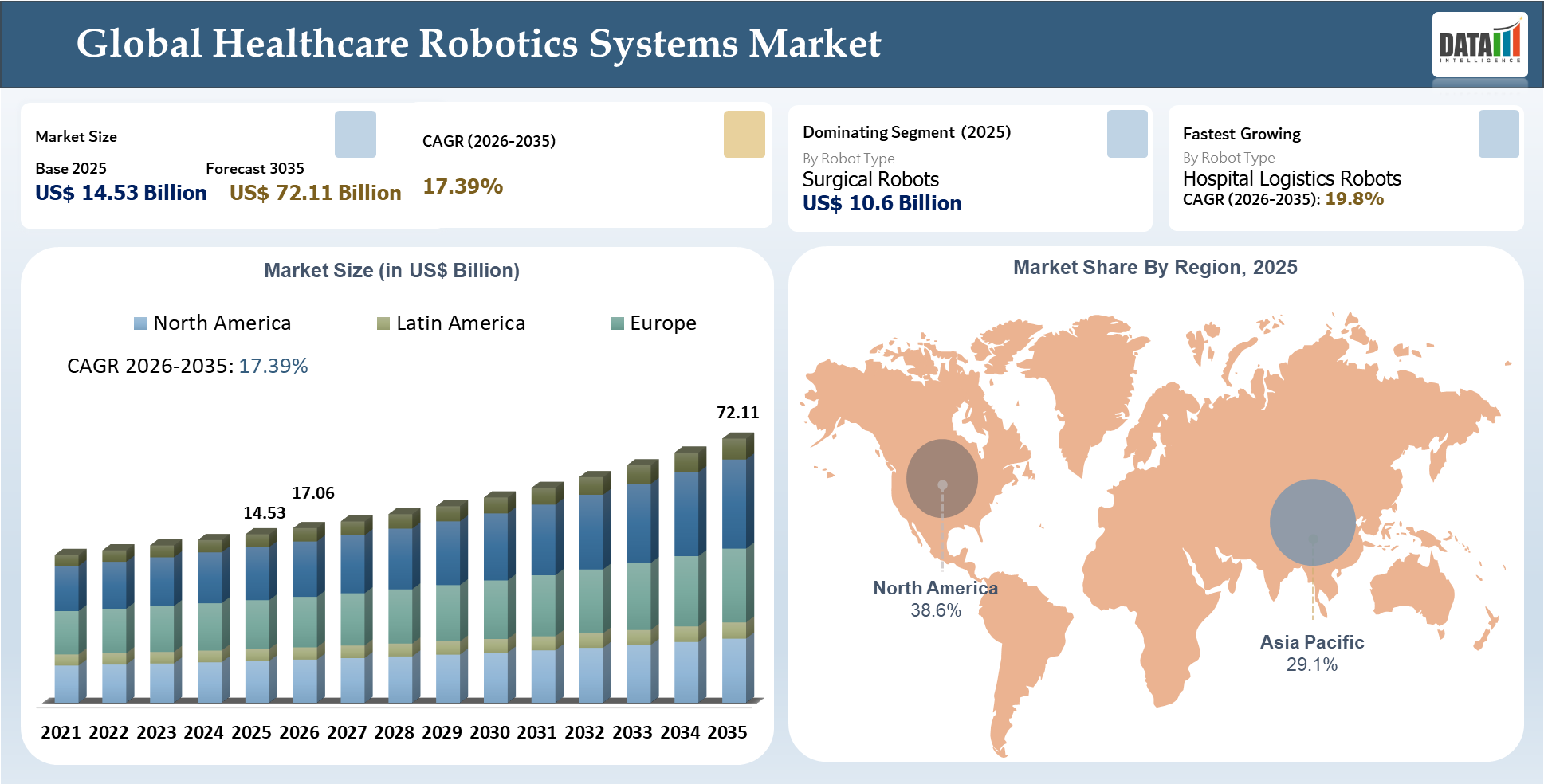

The global Healthcare Robotics Systems Market size was valued at US$ 14.53 billion in 2025 and is estimated to reach US$ 72.11 billion by 2035, exhibiting a CAGR of 17.39% during the forecast period from 2026 to 2035.

Market growth will be propelled by the growing uptake of robotic systems in the fields of surgery, rehabilitation, hospital logistics, pharmacy automation, and patient care support. Given the pressure on health institutions to achieve procedural precision, minimize the labor required, increase workflow efficiency, and improve patient outcome quality, there has been an increased demand for robotics technology in health services delivery. Other market drivers include the rising need for minimally invasive surgery and the increased hospital automation process, as well as the need to address personnel shortages.

Market dynamics will be influenced by constant innovations in surgical robots, rehabilitation robots, hospital logistics robots, and pharmacy robotics systems, all providing various benefits depending on their use case. Some of the benefits include greater precision in operation, effective workflow management, efficient processes, and greater scalability potential.

AI Impact Analysis

The influence of AI on the healthcare robotics systems market is being felt as an enhancing layer along the existing value chain, but not as an independent market segment. Evidence of this trend includes product optimization, workflow analysis, predictive services, quality improvement, and overall system monitoring, which are transforming the design and implementation of robotic platforms. The FDA's growing list of AI-enabled medical devices, as well as its recognition that artificial intelligence and machine learning will enable providers to make improvements in care based on data, is consistent with this approach.

The value of AI for healthcare providers is evident in the decrease in manual review, consistency of workflow, informed decision-making regarding procedures, and system usability. For instance, Medtronic's Touch Surgery ecosystem is described as an AI-driven system for turning surgical data into insights, while Performance Insights are designed to cut down manual review time by providing metrics such as anatomy recognition and instrument visibility.

The use of AI is enhancing after-sales value creation as well. In one example, Omnicell cites automation and AI-driven intelligence to enhance efficiency and patient safety as well as the outcomes of drug management.

Key Takeaways

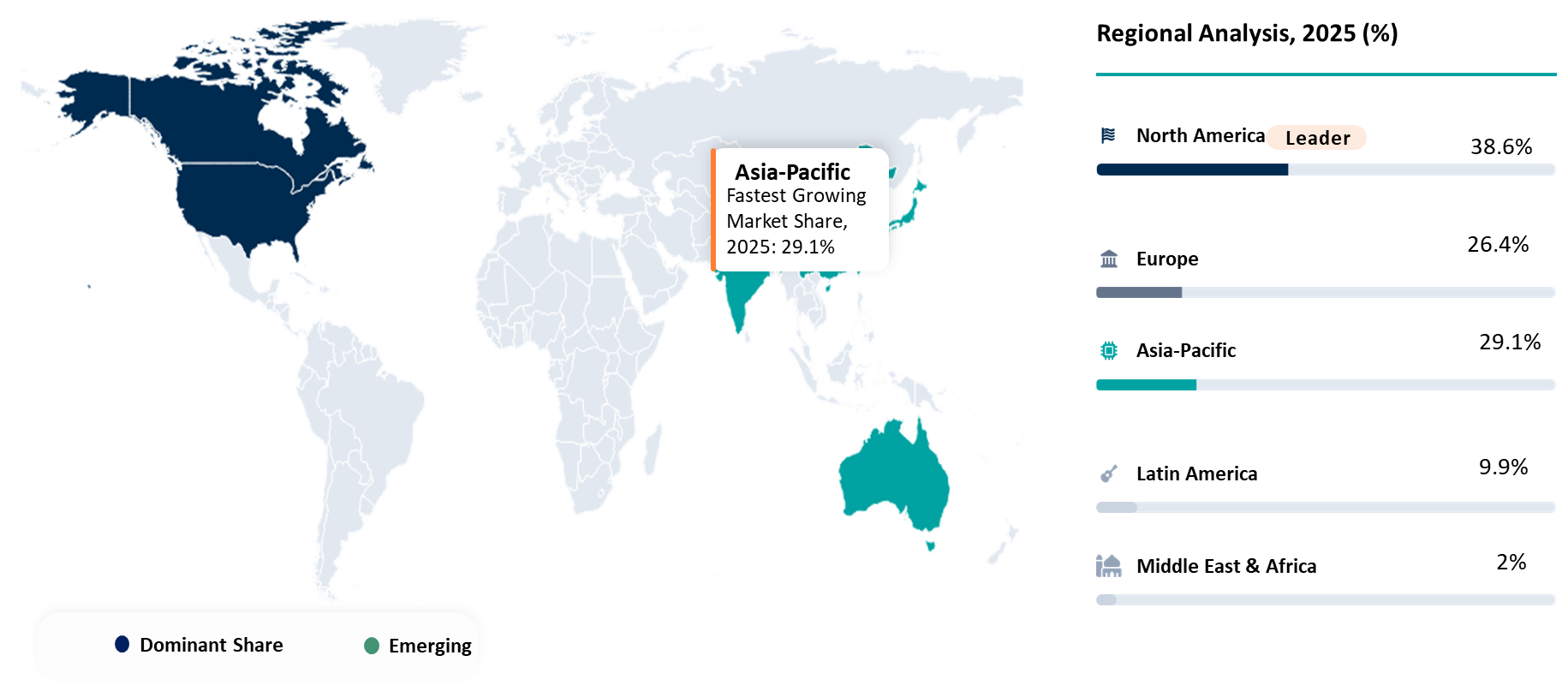

- North America accounts for approximately 40-42% of the global market, driven by advanced healthcare infrastructure, high surgical volumes, and widespread adoption of robotic-assisted procedures.

- Surgical robots contribute nearly 50-55% of total market revenue, owing to increasing demand for minimally invasive procedures and precision-guided surgeries.

- Hospitals account for more than 60% of total end-user demand, supported by growing investments in hospital automation, robotic surgery, and patient care technologies.

- Robotic-assisted surgeries can reduce hospital stays by up to 20-30% while improving surgical precision, patient outcomes, and recovery time.

- More than 70% of leading healthcare providers are investing in AI-powered robotic systems to improve workflow efficiency, clinical accuracy, and operational productivity.

- Hospital logistics and pharmacy automation robots are witnessing annual adoption growth exceeding 20%, driven by increasing demand for contactless healthcare operations and workforce optimization.

- AI-enabled healthcare robotics integrated with computer vision and machine learning are experiencing rapid adoption, enabling intelligent decision support and real-time clinical assistance.

- Asia-Pacific is expected to be the fastest-growing regional market, supported by expanding healthcare infrastructure, increasing healthcare expenditure, and government investments in medical technologies.

- Growing investments in digital healthcare, precision medicine, rehabilitation robotics, and elderly care automation are expected to accelerate long-term market expansion.

Healthcare Robotics Systems Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 14.53 Billion | |

| 2035 Projected Market Size | US$ 72.11 Billion | |

| CAGR (2026-2035) | 17.39% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Robot Type | Surgical Robots, Rehabilitation Robots, Hospital Logistics Robots, Pharmacy Automation Robots, and Disinfection Robots | |

| By Care Setting | Hospitals, Ambulatory Surgical Centers, Rehabilitation Centers, Pharmacies, and Elderly Care | |

| By Business Model | Capital Purchase, Lease and Service Model, and Robotics as a Service | |

| By Application | Minimally Invasive Surgery, Rehabilitation, Drug Dispensing, Material Handling, and Infection Control | |

| By End-User | Providers, Pharmacies, Long Term Care, and Home Care | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Healthcare Robotics Systems Market Disruption Analysis

Shift Toward Value-Based Competition and Operational Accountability in Healthcare Robotics Systems Market

The market for healthcare robotics systems is experiencing a period of disruption as there is a move away from feature competition towards operability. In today's healthcare industry, buyers are more interested in how fast a solution will fit within the hospital workflows, how well it will work in real-life situations, and how convincingly it will be able to justify the capital invested in acquiring a system in terms of efficiency, safety, and productivity improvements.

Another level of disruption occurring in the market comes from the business aspects. The ability of the product to integrate and the strength of its commercial ecosystem can influence the buying decision despite the presence of other competitors providing similar technology. Companies offering solutions that allow embedding their technology into a larger context of hospital workflows and providing end-to-end services, as well as supporting the right ecosystems, have an advantage in the market.

The healthcare industry is experiencing increased requirements for robustness and accountability. Providers put more weight on such features of solutions as supply chain resilience and service availability after the installation. This creates more pressure on the supplier's operational capability and delivery model.

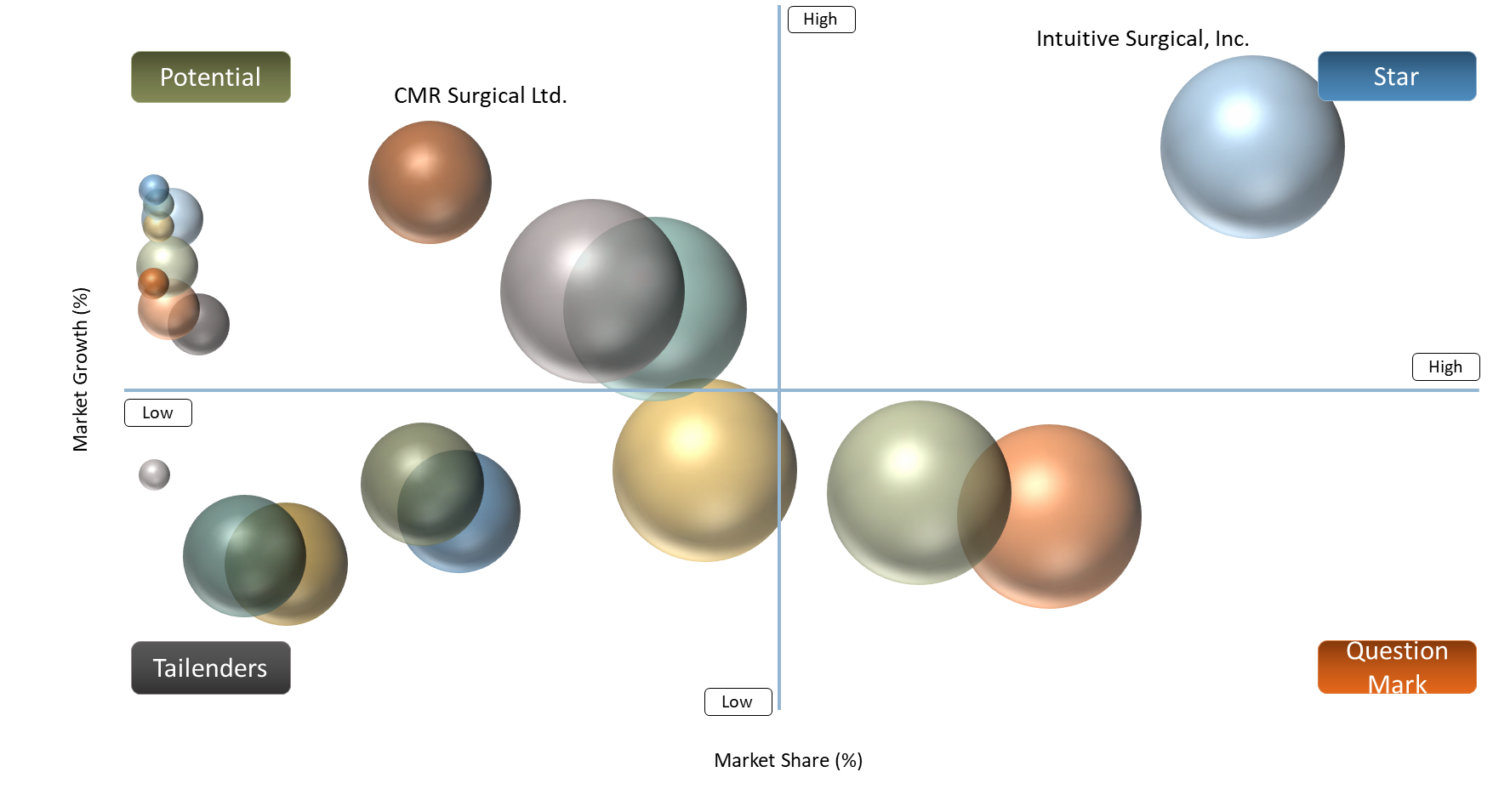

BCG Matrix: Company Evaluation

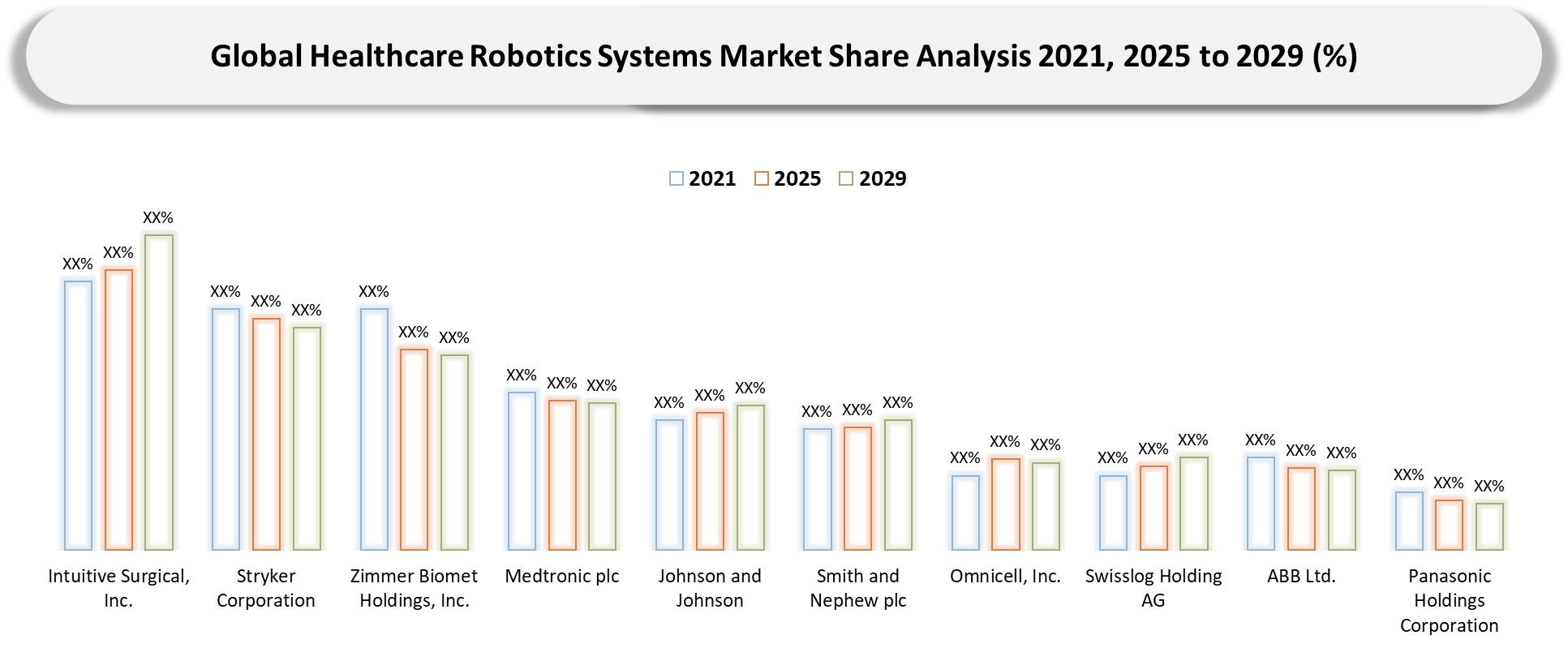

From a BCG perspective, the Stars in the market for healthcare robotics systems tend to be those firms that can achieve a good balance between growth exposure and competitive impact. Examples include Intuitive Surgical, Inc., Stryker Corporation, and Zimmer Biomet Holdings, Inc., which are usually classified under this category owing to their demand momentum, robust installed base, wide clinical acceptance, and ecosystem dominance. Such firms’ advantages not only pertain to their presence in the market but also their influence on customers’ expectations regarding workflow integration, service, training, and recurring revenue.

The Cash Cow position is usually occupied by the firms that are already well-established in the market, have wide geographical coverage, and possess strong customer relationships in the maturest sectors. Though they might not always be leading the growth areas, these firms are able to consistently produce revenue from service agreements, consumables, installed base, and switching costs.

Question Marks include firms that are new specialists or adjacent players that focus on surgical robots or hospital logistics robots. These firms have the potential for growth, although they still need scale, regulation, and commercial traction. The Dogs are vendors who lack differentiation, ecosystem synergy, or an outdated sales and delivery model.

Healthcare Robotics Systems Market Dynamics

Healthcare Robotics Systems Market Shift Toward Measurable Operating Value and Application-Specific Buying Criteria

One of the primary factors that is driving growth in the market for healthcare robotics systems is the move from general enthusiasm towards robotics to more considered decision-making with clear focus on specific benefits in terms of improved throughput, better-quality processes, faster turnaround, lower labor requirements, and ability to enable new business or services models. Such trends benefit players with profound understanding of their customers' operational realities, as well as those that are capable of delivering clear proof of positive impact in terms of business metrics.

Another factor at play is changing procurement practices. In addition to looking at technological capabilities, potential customers will now assess the complexity of deployment, ease of integration, quality of customer service, compliance readiness, and authenticity of efficiency/productivity gains claimed by vendors. As a consequence of these changes, investment is increasingly concentrated in segments where there is proof of high value, most notably Surgical Robots and Hospital Logistics Robots.

Finally, increased maturity of the overall ecosystem is aiding market development. Buyers are gaining access to a wider range of implementation, connectivity, software and manufacturing resources that lower risk associated with the adoption process. On top of that, they become less inclined to purchase generic products.

Healthcare Robotics Systems Market Integration Burden, Compliance Friction, and Longer Enterprise Decision Cycles

One significant barrier for the market of health care robotics systems is the lack of correlation between client interest and swift uptake. While many health care organizations appreciate the benefits of using robots in the health care environment, the actual process of implementation is slowed down due to a number of different reasons including the complexity of installation, testing and acceptance, change in work processes, and purchasing regulations.

This issue tends to be even more acute when robots are integrated into regulated processes, require a considerable amount of spending to purchase and implement, or need to interface with existing infrastructure or involve more than one party in the decision process.

It results in a significant disconnect between client interest shown at the pilot level and the willingness to adopt robot technology on an organization-wide scale. Companies that fail to take into account all the regulatory issues related to robot use and installation might overestimate their revenues from clients..

Healthcare Robotics Systems Market Artificial Intelligence and Intelligent Healthcare Robotics Analysis

Artificial intelligence is fundamentally transforming healthcare robotics technologies by enabling intelligent clinical decision support capabilities, autonomous workflow management functionalities, and precision-guided patient care solutions across global healthcare environments. The convergence of robotics, artificial intelligence, machine learning algorithms, and computer vision technologies is substantially improving procedural precision while simultaneously enhancing operational efficiencies across hospitals, surgical centers, and rehabilitation facilities worldwide.

Recent industry developments continue highlighting the commercialization potential of intelligent healthcare robotics platforms. In July 2026, Johnson & Johnson received U.S. FDA marketing authorization for its OTTAVA robotic surgical system, marking the company's strategic entry into the highly competitive robotic-assisted soft tissue surgery market. The platform integrates robotic arms directly within the operating table and is designed to optimize operating room utilization capabilities while supporting minimally invasive surgical procedures. Similarly, Intuitive Surgical continues expanding its da Vinci 5 surgical platform deployments globally, strengthening intelligent robotic surgery capabilities across multiple clinical specialties. These developments demonstrate how artificial intelligence-enabled healthcare robotics technologies are rapidly transforming next-generation healthcare delivery models worldwide.

Healthcare Robotics Systems Market Surgical Robotics and Precision Medicine Analysis

Surgical robotics technologies continue representing one of the largest and fastest-growing segments across the Healthcare Robotics Systems Market globally. Healthcare providers are increasingly adopting robotic-assisted surgical platforms designed to improve procedural precision, minimize surgical complications, and accelerate patient recovery outcomes across minimally invasive surgical applications.

Precision medicine initiatives are substantially strengthening demand for intelligent surgical robotics technologies capable of supporting personalized therapeutic interventions worldwide. Advanced robotic platforms increasingly integrate real-time imaging technologies, artificial intelligence-assisted analytics capabilities, and intelligent instrument tracking functionalities designed to improve surgical outcomes considerably. Furthermore, growing investments supporting robotic-assisted orthopedic, cardiac, neurological, and urological procedures are anticipated to significantly influence future technological developments throughout the forecast period.

Healthcare Robotics Systems Market Hospital Automation and Smart Healthcare Infrastructure Analysis

Healthcare organizations worldwide are accelerating investments supporting intelligent hospital automation initiatives designed to address workforce shortages, improve operational efficiencies, and strengthen patient care delivery capabilities. Healthcare robotics systems are increasingly utilized across hospital logistics management, pharmacy automation activities, infection control operations, and intelligent patient monitoring applications globally.

For instance, healthcare institutions are increasingly adopting autonomous hospital robots developed by leading innovators such as Diligent Robotics for patient assistance and material handling applications, while intelligent pharmacy automation technologies developed by Omnicell continue improving medication management capabilities across healthcare environments. Furthermore, hospital automation initiatives involving robotic disinfection technologies and intelligent logistics systems are anticipated to substantially strengthen commercialization opportunities globally throughout the forecast period.

Healthcare Robotics Systems Market Robotics-as-a-Service (RaaS) and Digital Healthcare Transformation Analysis

Robotics-as-a-Service is emerging as an attractive commercialization model across the global healthcare robotics industry by enabling healthcare organizations to adopt advanced automation capabilities without substantial upfront capital investments. Subscription-based robotic deployment models are significantly improving accessibility capabilities across hospitals, ambulatory surgical centers, rehabilitation facilities, and elderly care environments worldwide.

Digital healthcare transformation initiatives involving cloud-connected robotic platforms, intelligent workflow orchestration capabilities, and predictive healthcare analytics solutions are substantially strengthening future commercialization opportunities globally. Furthermore, increasing adoption of telepresence robotics technologies and remote healthcare automation capabilities is anticipated to positively influence future market competitiveness considerably throughout the forecast period.

Healthcare Robotics Systems Market Aging Population and Rehabilitation Robotics Analysis

The rapidly growing global aging population continues creating attractive commercialization opportunities across rehabilitation robotics and intelligent elderly care technologies worldwide. Healthcare providers are increasingly investing in robotic rehabilitation platforms capable of improving mobility outcomes, accelerating therapeutic interventions, and enhancing patient engagement capabilities significantly.

Advanced rehabilitation robotics systems supporting neurological disorders, musculoskeletal conditions, and post-operative recovery programs are substantially strengthening future market expansion globally. Furthermore, intelligent exoskeleton technologies and patient assistance robotics platforms are anticipated to significantly improve quality-of-life outcomes across elderly care environments throughout the forecast period.

Healthcare Robotics Systems Market Regulatory and Compliance Landscape Analysis

The Healthcare Robotics Systems Market operates within a highly regulated healthcare environment characterized by stringent medical device approval frameworks, cybersecurity requirements, and intelligent healthcare validation standards globally. Regulatory authorities worldwide continue emphasizing patient safety capabilities, artificial intelligence governance frameworks, and intelligent robotic system reliability requirements designed to strengthen healthcare delivery outcomes considerably.

The increasing number of regulatory approvals involving robotic-assisted surgical technologies and intelligent healthcare automation solutions is substantially strengthening commercialization opportunities globally. Furthermore, evolving international regulatory standards governing artificial intelligence-enabled healthcare technologies are anticipated to significantly influence future market competitiveness across major healthcare economies throughout the forecast period.

Healthcare Robotics Systems Market Segmentation Analysis

The global healthcare robotics systems market is segmented based on robot type, care setting, business model, application, end-user, and region.

Robot Type Is Where Healthcare Robotics Systems Economics Start to Separate

Robot Type is one of the most effective filters to use in the analysis of the market for healthcare robots since it reveals trade-offs that buyers take into consideration in reality. The issues of budget distribution, price power, differentiation, and risks become much more obvious under such analysis. In addition, it is one of the most quantifiable segments since its dynamics are better monitored from an overall strategy standpoint.

In this segment, Surgical Robots and Hospital Logistics Robots must be given special consideration as they present distinct approaches to realizing business opportunities. Surgical Robots typically enjoy advantages such as greater clinical knowledge, more extensive deployment, and smoother incorporation within current surgical facilities, making them more likely to achieve higher adoption rates and increased volume usage. On the other hand, Hospital Logistics Robots find favor among those who require improved workflow management, efficiency, and reliability in difficult environments.

This difference highlights the importance of this segment in terms of marketing research and consultancy. Surgical Robots tend to offer more substantial volume revenues, whereas Hospital Logistics Robots may hold higher strategic significance and premium status.

Healthcare Robotics Systems Market Geographical Penetration

Asia-Pacific Is Emerging as a Key Competitive Force in the Healthcare Robotics Systems Market

The Asia-Pacific region will become increasingly significant as a key driver in the market for robotic systems due to its pragmatic shift towards the use of robotics rather than hype surrounding demand. Value-based purchasing practices, wherein purchasers analyze deployment times, real-world performance, and efficiencies in workflow management, are gaining ground. Factors such as workforce deficiencies, the aging demographics of the population, and limitations within hospitals themselves drive the need for robotics that provide tangible results. Unlike previous stages of adoption that were influenced by considerations of prestige, buyers in the market now consider metrics such as utilization rates and staff reductions. The Asia-Pacific region is benefiting from ecosystem maturity, including greater capabilities in implementation, partnerships, and manufacturing, which lowers the risk associated with procurement. In other words, not only is Asia-Pacific a growing region, but it is also setting trends for how suppliers develop products and market their value proposition.

Japan Healthcare Robotics Systems Market Trends

Japan is a key player in the healthcare robotics system market because of its distinctive mix of demographics, technology, and purchasing habits. The rapidly aging Japanese population and reduced workforce are driving up the need for robotics in surgeries, rehabilitation treatments, hospital management logistics, and assistance for the elderly. Purchasers in Japan are very picky about their buying practices and prefer reliable and effective technology solutions over any promises of innovations. Adaptability to local cost structures and regulatory framework is a must for any supplier in Japan; the lack of flexibility will lead vendors to fail. Collaboration with other players within the ecosystem becomes crucial, as successful entry into the Japanese market means not only offering competitive technologies but also being able to implement them successfully. The reliance on global strategies or universal marketing approaches makes scaling difficult; therefore, a focus on local solutions and proven outcomes brings much more success.

South Korea Healthcare Robotics Systems Market Outlook

The South Korean market is considered one of the most promising and rapidly evolving in the field of healthcare robotics systems due to the high level of development of the country's healthcare facilities and advanced technologies. The technological advancement of South Korea's healthcare institutions creates good prerequisites for implementing robots that increase the effectiveness of treatment through the efficiency, accuracy, and automation of operations. The main drivers of demand for healthcare robotics systems are fields in which there will be tangible performance gains: surgeries, hospital logistics, and care delivery systems. In addition, the presence of highly developed electronics, automation, and IT infrastructure contributes to the introduction of new robotics systems. There are active government programs aimed at the introduction of smart hospitals. This allows buyers to appreciate highly valuable offers but requires evidence of high performance and scalability. Consequently, South Korea acts as an indicator of the future trends in the regional market.

Healthcare Robotics Systems Market Competitive Landscape

- Market competition for healthcare robotics systems is characterized by a dichotomy between scale players and specialized vendors. The former leverage portfolio diversity, distribution channels, and client relationships to set category standards, while the latter try to compete on product specialization, rapid deployment, and/or use case fit. In mature markets, competitive advantage is being gained by those organizations with technical authority, along with complementary offerings and support.

- The positioning strategies of market participants are increasingly driven by their ability to provide defense against the entire customer journey. Product performance remains important, but onboarding costs, scalability, data or workflow management capabilities, and application engineering also play a role. Those companies that are able to anchor their business model to high-value niches, including Surgical Robots and Hospital Logistics Robots, tend to have a stronger competitive position.

Healthcare Robotics Systems Market Key Players:

Intuitive Surgical, Inc., Stryker Corporation, Zimmer Biomet Holdings, Inc., Medtronic plc, Johnson & Johnson, Smith & Nephew plc, Omnicell, Inc., Swisslog Holding AG, ABB Ltd., Panasonic Holdings Corporation, Toyota Motor Corporation, Mitsubishi Electric Corporation, KUKA Aktiengesellschaft, Cyberdyne Inc., Ekso Bionics Holdings, Inc., ReWalk Robotics Ltd., Asensus Surgical, Inc., CMR Surgical Ltd., Diligent Robotics, Inc., Aethon, Inc.

Recent Developments in Healthcare Robotics Systems Market

- June 2026 - Intuitive Surgical, Inc.: Expanded its robotic-assisted surgery portfolio with new AI-enabled capabilities to enhance surgical precision and workflow efficiency.

- June 2026 - Medtronic plc: Advanced its robotic-assisted surgery platform with new technologies supporting minimally invasive procedures across multiple specialties.

- May 2026 - Stryker Corporation: Launched enhanced robotic orthopedic solutions with improved planning software and intraoperative guidance features.

- May 2026 - CMR Surgical Ltd.: Expanded the global adoption of its Versius surgical robotic system through new hospital installations and market expansion.

- April 2026 - Zimmer Biomet Holdings, Inc.: Introduced next-generation robotic-assisted orthopedic technologies to improve joint replacement accuracy and patient outcomes.

- April 2026 - Swisslog Holding AG: Expanded its healthcare automation portfolio with robotic pharmacy and hospital logistics solutions to improve operational efficiency.

- March 2026 - Asensus Surgical, Inc.: Enhanced its digital laparoscopic platform with AI-powered performance analytics and intelligent surgical assistance.

- March 2026 - Diligent Robotics, Inc.: Expanded deployments of its Moxi hospital service robot to automate routine clinical support tasks and improve healthcare workflows.

Healthcare Robotics Systems Market Investment and Strategic Collaboration Analysis

Public and private sector investments supporting intelligent healthcare robotics innovations continue creating substantial commercialization opportunities across global markets. Healthcare organizations are increasingly allocating resources toward robotic-assisted surgery platforms, rehabilitation technologies, intelligent patient care systems, and digital healthcare transformation initiatives designed to improve clinical performance outcomes significantly.

Strategic collaborations involving healthcare providers, robotics manufacturers, cloud technology organizations, and academic institutions are substantially accelerating technological innovation activities worldwide. Intuitive Surgical continues expanding its technological ecosystem through innovations supporting force feedback technologies, telecollaboration capabilities, and intelligent surgical instruments across its da Vinci portfolio. Additionally, major healthcare technology organizations are increasingly pursuing acquisitions and partnerships supporting intelligent healthcare automation capabilities globally. Growing investments supporting precision medicine initiatives are anticipated to substantially strengthen future market competitiveness throughout the forecast period.

Healthcare Robotics Systems Market Emerging Technologies Analysis

Emerging technologies involving autonomous surgical robotics platforms, artificial intelligence-assisted clinical decision support systems, collaborative healthcare robots, intelligent rehabilitation technologies, and cloud-connected robotic ecosystems are substantially transforming future market opportunities worldwide. Innovations supporting machine vision capabilities, digital surgery technologies, predictive healthcare analytics, and remote robotic assistance functionalities are anticipated to significantly improve healthcare delivery capabilities globally.

Furthermore, increasing integration between intelligent healthcare technologies and advanced robotic automation ecosystems is expected to strengthen commercialization opportunities considerably throughout the forecast period. The convergence of precision medicine initiatives and next-generation healthcare robotics technologies is anticipated to significantly influence future technological developments across the Healthcare Robotics Systems Market.

Healthcare Robotics Systems Market Future Market Trends (2026-2035)

The Healthcare Robotics Systems Market is expected to witness substantial growth throughout the forecast period driven by increasing adoption across robotic-assisted surgical procedures, intelligent hospital automation initiatives, and precision healthcare programs worldwide. Future market expansion will be supported by artificial intelligence innovations, connected healthcare infrastructures, minimally invasive surgical technologies, and digital healthcare transformation initiatives across global markets.

Increasing investments supporting intelligent healthcare ecosystems, technological advancements, and regulatory modernization programs are anticipated to substantially strengthen commercialization opportunities globally. Furthermore, growing demand for highly automated healthcare environments capable of improving patient outcomes while simultaneously optimizing clinical efficiencies is expected to significantly influence future market dynamics across major healthcare economies through 2035.

Healthcare Robotics Systems Market White Space Opportunities

As per DataM, one of the best examples of white space in the healthcare robotics systems market exists outside the highly visible purchasing programs. The vast majority of players focus their efforts on large flagship hospital accounts and big installations for surgery, while unexploited demand still persists in small, high-friction use-cases that favor workflow fit, reliability, and operational impact over sheer scale.

Secondly, opportunities arise from white space in commercialization rather than technology. Increasingly, buyers will reward vendors who make it easy for them to adopt the technology, from training to onboarding to validation assistance, integration, and post-sale services. It is particularly important when compliance requirements, workflow efficiency gains, and improvements in utilization are worth more than purely technical considerations.

Thirdly, another set of white spaces resides in the coverage of regions or tiers of customers. Despite recurring demand, mid-tier hospitals, specialized institutions, and even secondary care facilities may go underserviced. Comparability is becoming simpler with time in robotic platforms, leading to more competition on service quality and lifecycle support.

DMI Opinion

As per DataM, the healthcare robotics systems industry is becoming more favorable towards suppliers who can leverage customer interest into recurrent revenues while ensuring the complexity of implementation does not exceed the pace of value realization. The leading companies are no longer depending solely on their ability to sell innovative messages or superior technical characteristics. Instead, they have found ways to ensure adoption is a credible operationally by fitting in the workflows and achieving tangible results.

The larger message by DataM is that the competitive edge is more likely to come from flawless execution rather than just market presence alone. Companies that minimize adoption costs, provide training, match their systems with the clinical and operational workflows, and link robotic technology to financial gains or productivity increases are more likely to succeed. This holds true for industries where customers prioritize smooth implementation, efficiency improvements, regulatory compliance, and robust after-sales services. On the other hand, those that rely on general marketing campaigns, insufficient technical support, and single-pronged sales approaches could find themselves at a disadvantage amid increased buyer demands for accountability, ROI, and outcomes.

Why Choose DataM?

- Technological Innovations: DataM explores advancements across robotic-assisted surgical systems, artificial intelligence-enabled healthcare automation technologies, intelligent rehabilitation robotics platforms, cloud-connected healthcare infrastructures, and precision medicine capabilities that are enabling healthcare organizations worldwide to improve clinical outcomes and operational efficiencies. Recent examples include Intuitive Surgical's da Vinci 5 platform incorporating force feedback technologies and intelligent surgical capabilities alongside Medtronic's Hugo robotic-assisted surgery system expansion supporting minimally invasive procedures across multiple clinical specialties.

- Product Performance & Market Positioning: The report evaluates how leading market participants deliver healthcare robotics solutions based on critical performance parameters such as procedural accuracy, clinical workflow integration capabilities, intelligent analytics functionalities, operational flexibility, scalability characteristics, and patient outcome improvements, highlighting how organizations differentiate through technological innovation and intelligent healthcare excellence across global clinical environments.

- Real-World Evidence: DataM highlights the adoption of healthcare robotics technologies across hospitals, ambulatory surgical centers, rehabilitation facilities, and precision healthcare ecosystems worldwide. More than 20 million patients globally have benefited from da Vinci-assisted surgical procedures, demonstrating the substantial clinical adoption of intelligent robotic technologies across modern healthcare infrastructures. Healthcare robotic systems continue delivering measurable benefits including reduced hospital stays, enhanced procedural precision, accelerated patient recovery timelines, and improved operational efficiencies across healthcare organizations globally.

- Market Updates & Industry Changes: The report tracks key developments including Johnson & Johnson's entry into the U.S. robotic surgery market through the commercialization of its Ottava platform during 2026, Medtronic's first commercial U.S. procedures utilizing the Hugo robotic-assisted surgical system, and ongoing investments supporting next-generation intelligent healthcare technologies across major global markets.

- Competitive Strategies: DataM analyzes how leading organizations expand through artificial intelligence innovations, strategic acquisitions, intelligent healthcare technologies, cloud-enabled robotic capabilities, product portfolio diversification initiatives, and regional commercialization programs designed to address increasing demand for minimally invasive procedures, precision medicine applications, and intelligent healthcare automation solutions worldwide.

- Pricing & Market Access: The report explains pricing variations based on robotic system configurations, procedural capabilities, intelligent software functionalities, deployment complexities, healthcare infrastructure requirements, and clinical integration considerations, along with market access opportunities through hospitals, healthcare providers, medical device distributors, and strategic technology partnerships supporting global commercialization initiatives.

- Market Entry & Expansion: DataM identifies attractive growth opportunities driven by increasing investments supporting healthcare modernization initiatives, accelerating adoption of minimally invasive surgical technologies, expanding rehabilitation robotics applications, and growing demand for intelligent healthcare solutions globally. The report further outlines strategic approaches involving regional expansion initiatives, technology differentiation strategies, customized healthcare automation platforms, and collaborative commercialization models designed to support successful market entry and long-term business expansion across emerging and established healthcare robotics markets.

Target Audience

The report is strategically developed for stakeholders operating across the global healthcare robotics, medical technology, precision medicine, and intelligent healthcare ecosystem. It provides actionable market intelligence for robotic-assisted surgery manufacturers, healthcare institutions, rehabilitation technology developers, intelligent healthcare solution providers, and medical device organizations seeking to strengthen their competitive positioning within rapidly evolving healthcare markets. Furthermore, regulatory organizations, academic institutions, investment firms, government agencies, and strategic business leaders can utilize the report to evaluate emerging technological innovations, commercialization trends, healthcare modernization initiatives, and future growth opportunities shaping the Healthcare Robotics Systems Market through 2035.