Grid-Scale Battery Energy Storage System (BESS) Market Definition and Overview

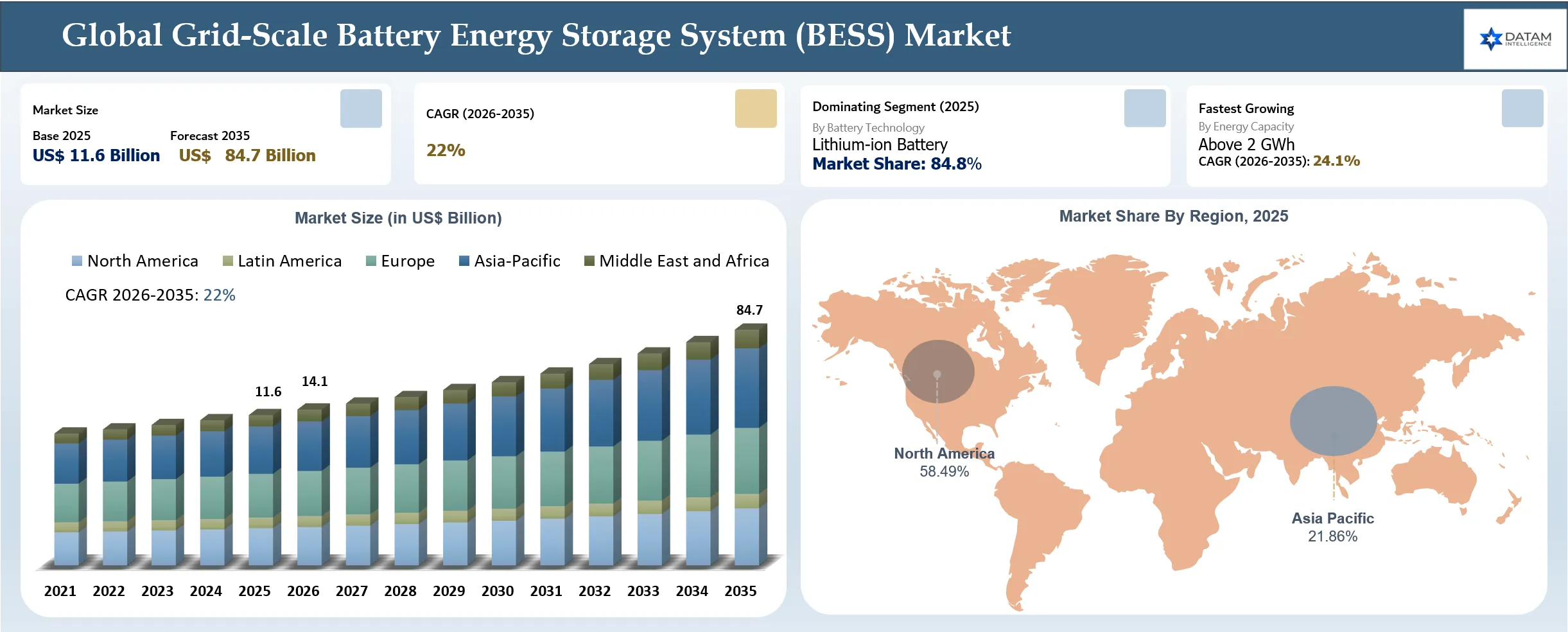

The global Grid-Scale Battery Energy Storage System (BESS) market reached USD 11.6 billion in 2025 and is expected to reach USD 84.7 billion by 2035, growing with a CAGR of 22% during the forecast period 2026-2035. The market is expanding rapidly due to increasing installation of utility-scale renewable energy projects and increased requirements for flexible grids that can balance the intermittency of solar and wind generation. As per the International Energy Agency (IEA) for 2026, utility-scale battery storage made up around 80% of all battery storage capacity additions, where some 87 GW of grid-scale battery additions were added globally. Batteries such as those based on lithium iron phosphate (LFP), coupled with enhanced energy management systems and power conversion systems, are contributing to better project economics and performance. Companies such as Tesla, BYD, Fluence Energy, Wärtsilä Energy, Sungrow Power Supply, and CATL are ramping up production capacity and releasing new storage solutions with higher capacities while forming utility partnerships. At the same time, long interconnection procedures, difficult permitting procedures, supply issues, and changes in the revenue mechanisms of the market are impacting the installation process.

It is anticipated that the additional financial support through the VGF scheme and ISTS charge waiver will boost investment in utility-scale battery storage solutions, which will enhance the economic feasibility of large-scale BESS projects in India. In August 2025, as per Energetica India, the Government of India has increased its financial assistance for grid-scale Battery Energy Storage System (BESS) projects with INR 9,160 crore allocation under the Viability Gap Funding (VGF) Scheme to install 43 GWh BESS capacity. This project was announced by Union Minister of State (Power), Manohar Lal, and will be amongst the largest energy storage programs worldwide.

Utility-Scale Energy Storage Infrastructure Investments Creating Wide Space Opportunities

In August 2025, the Ministry of Power, Government of India, significantly expanded support for grid-scale Battery Energy Storage Systems (BESS) by earmarking INR 9,160 crore (approximately USD 1.09 billion) under the Viability Gap Funding (VGF) Scheme to facilitate the deployment of 43 GWh of battery energy storage capacity, making it one of the world's largest government-backed BESS support programs. The funding is intended to improve grid flexibility, accelerate renewable energy integration, reduce renewable power curtailment, and strengthen electricity system reliability. In addition to direct financial support for battery storage projects, the initiative includes 100% waiver of Inter-State Transmission System (ISTS) charges for eligible BESS projects commissioned by June 2028, improving project economics and encouraging large-scale private investment. The financial assistance will be utilized for utility-scale battery procurement, battery modules and cells, battery management systems (BMS), power conversion systems (PCS), energy management systems (EMS), transformers, grid interconnection infrastructure, engineering, procurement and construction (EPC), system integration, commissioning, and long-term operation and maintenance of storage assets.

The expanded VGF program is expected to generate substantial procurement opportunities across the grid-scale BESS value chain. Battery manufacturers and storage technology suppliers, including CATL, BYD, Tesla Energy, Sungrow, Fluence Energy, Wärtsilä Energy, LG Energy Solution, Samsung SDI, and Hitachi Energy, are well-positioned to supply utility-scale battery systems, inverters, and energy management technologies. Indian manufacturers and integrators such as Exide Industries, Amara Raja Energy & Mobility, Tata Power, Reliance New Energy, JSW Energy, L&T Energy, and Tata AutoComp Gotion Green Energy are expected to benefit through domestic battery manufacturing, system integration, EPC execution, and utility-scale storage deployments. The initiative is also likely to create opportunities for transmission utilities, renewable energy developers, EPC contractors, digital energy platform providers, and grid engineering firms involved in project design, installation, commissioning, monitoring, and lifecycle asset management as India accelerates the deployment of large-scale energy storage infrastructure to support its clean energy transition.

Grid-Scale Battery Energy Storage System (BESS) Market Key Takeaways

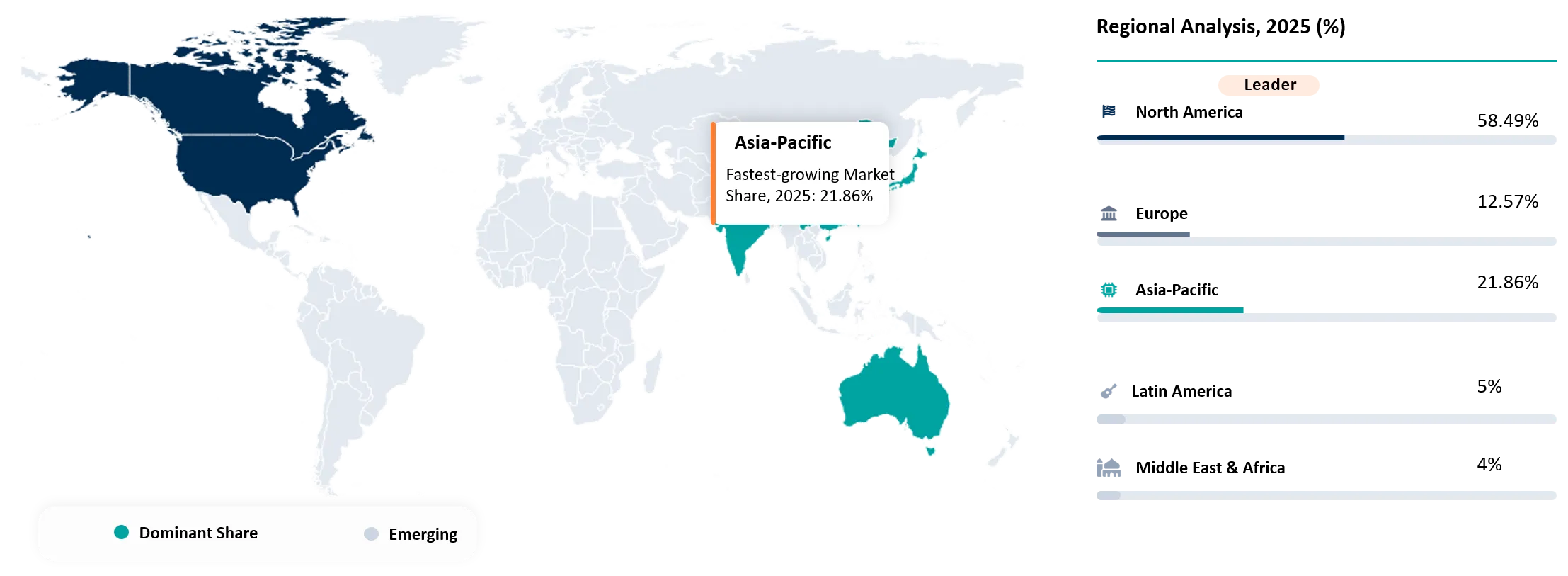

- North America established clear regional leadership by contributing approximately 58.49% of the global market share. Within this region, the United States energy storage market achieved 52% growth by adding 18.9 GW of capacity.

- The lithium-ion battery segment dominated the technology landscape by securing a commanding 84.8% market share. This position was solidified as global stationary energy storage demand expanded by 51% year-on-year.

- Power producers in the United States planned a record deployment of 86 GW of additional capacity. This pipeline strategically allocates 43.4 GW (51%) to solar installations and 24 GW (28%) to battery storage solutions.

- The Government of India allocated INR 9,160 crore (approximately USD 1.09 billion) under its Viability Gap Funding scheme. This massive state support program is explicitly designed to facilitate the deployment of 43 GWh of battery storage.

Grid-Scale Battery Energy Storage System (BESS) Market Industry Trends and Strategic Insight

- Utilities and independent power producers (IPPs) are increasingly procuring 4-hour to 8-hour battery systems instead of traditional 1–2-hour configurations to support renewable energy shifting, evening peak demand, and capacity adequacy.

- Hybrid renewable energy projects integrating battery storage with solar photovoltaic (PV) and onshore wind farms are becoming the preferred project architecture.

- Grid-scale BESS is evolving from a peak-shaving resource into a multi-service grid asset capable of providing frequency regulation, voltage control, spinning reserve, synthetic inertia, black start capability, congestion management, and transmission deferral.

- Battery systems equipped with grid-forming inverters are gaining strategic importance as electricity networks integrate higher shares of inverter-based renewable generation.

- Governments are strengthening domestic battery ecosystems through production incentives, local content requirements, and manufacturing subsidies.

- Digital energy platforms integrating artificial intelligence (AI), machine learning, and predictive analytics are optimizing battery dispatch, state-of-health monitoring, degradation forecasting, thermal management, and revenue optimization.

Grid-Scale Battery Energy Storage System (BESS) Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 11.6 Billion | |

| 2035 Projected Market Size | USD 84.7 Billion | |

| CAGR (2026-2035) | 22% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Battery Technology | Lithium-ion Battery, Sodium-ion Battery, Flow Battery, Sodium-Sulfur (NaS) Battery, Lead-Acid Battery, Other Advanced Battery Technologies | |

| By Energy Capacity | Up to 100 MWh, 101–500 MWh, 501 MWh–1 GWh, 1–2 GWh, above 2 GWh | |

| By Storage Duration | Up to 2 Hours, 2–4 Hours, 4–8 Hours, above 8 Hours | |

| By Grid Connection | Transmission Grid, Distribution Grid, Hybrid Renewable Energy Projects | |

| By Application | Renewable Energy Integration, Frequency Regulation, Peak Shaving & Peak Demand Management, Energy Arbitrage, Transmission & Distribution (T&D) Deferral, Capacity Firming, Ancillary Services, Grid Resilience & Backup Power, Others | |

| By End User | Electric Utilities, Independent Power Producers (IPPs), Transmission System Operators (TSOs), Distribution Network Operators (DNOs), Government & Public Utilities, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Türkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Grid-Scale Battery Energy Storage System (BESS) Market Disruption Analysis

Shift Toward Lithium Iron Phosphate (LFP) Battery Chemistry Reshaping the Grid-Scale Battery Energy Storage System (BESS) Market

The disruption in the Grid-Scale Battery Energy Storage System (BESS) market is primarily driven by the rapid transition from Nickel Manganese Cobalt (NMC) batteries to Lithium Iron Phosphate (LFP) chemistry for utility-scale energy storage deployments. LFP batteries are becoming the preferred technology due to their lower capital cost, longer cycle life exceeding 6,000–10,000 charge-discharge cycles, superior thermal stability, and reduced dependence on critical minerals such as nickel and cobalt. According to the International Energy Agency (IEA), lithium iron phosphate (LFP) batteries accounted for around 90% of global battery storage deployments in 2025, reflecting the rapid transition toward lower-cost, longer-life, and safer battery chemistries for grid-scale energy storage applications. The declining cost of LFP battery cells is also improving the levelized cost of storage (LCOS), enabling utilities and independent power producers to accelerate deployment of large-scale BESS projects.

This technological transition is reshaping procurement processes, manufacturing investments, and competition within the battery storage value chain. Battery manufacturers have been increasing their production capacity for LFP cells, whereas system integrators and utilities have become interested in using LFP battery-based storage systems for integration with renewables, frequency regulation, and grid resiliency applications. Companies such as CATL, BYD, Tesla Energy, Sungrow, Fluence Energy, and Hithium, among others launched LFP batteries of increased capacity dedicated to grid storage applications during 2025-2026 in response to changing trends in the battery storage market moving beyond NMC battery systems. Given the importance of safety, longevity, and cost of ownership in the utilities' decision-making process regarding battery choice, LFP technology continues to challenge established practices and change the technology landscape of energy storage projects.

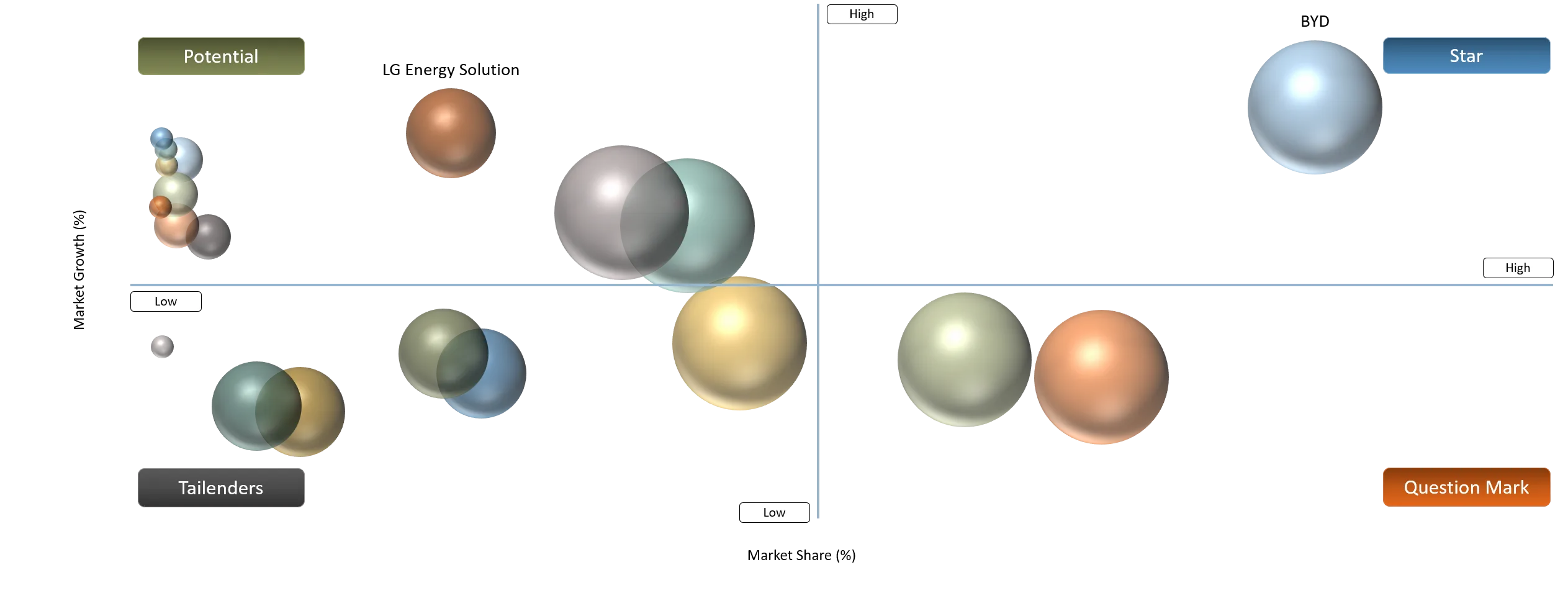

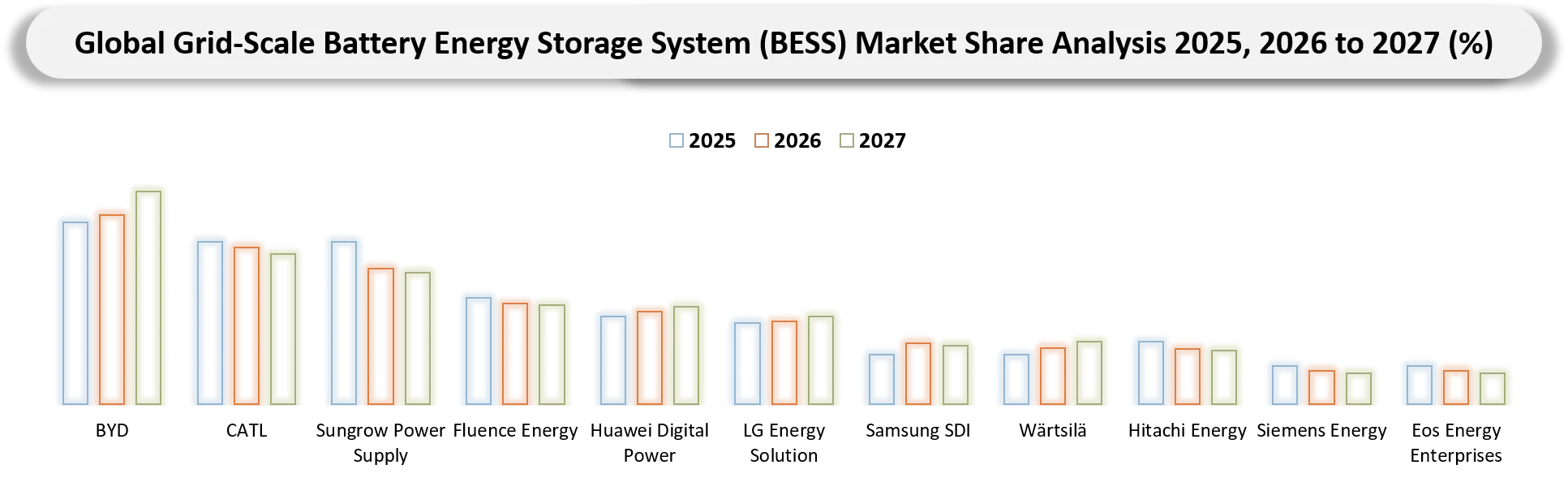

Grid-Scale Battery Energy Storage System (BESS) Market BCG Matrix: Company Evaluation

Stars include CATL, BYD, Sungrow Power Supply, and Fluence Energy because they hold leading positions in the global grid-scale BESS market through extensive utility-scale project deployments, strong battery manufacturing capabilities, advanced energy storage platforms, and integrated energy management software. These companies benefit from large-scale production capacity, diversified global project portfolios, and strategic partnerships with utilities, independent power producers (IPPs), and renewable energy developers. Question Marks category companies, such as Huawei Digital Power, Hitachi Energy, Siemens Energy, and Wärtsilä are positioned because they possess strong power electronics, grid integration, and digital energy capabilities, but continue to expand their market share amid intense competition from established battery manufacturers and dedicated BESS integrators.

The Potential category includes LG Energy Solution, Samsung SDI, and GE Vernova, which benefit from increasing global demand for utility-scale battery storage and strong technological expertise in battery cells, grid infrastructure, and power systems. Tailenders include Eos Energy Enterprises and Form Energy because their commercial activities are primarily focused on emerging long-duration energy storage (LDES) technologies rather than the mainstream lithium-ion BESS market.

Grid-Scale Battery Energy Storage System (BESS) Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Accelerating Utility-Scale Renewable Energy Deployment, driving demand for battery storage to balance intermittent solar and wind power generation. | 32% | Very High | Renewable energy integration, energy shifting, renewable curtailment reduction | Accelerates deployment of utility-scale BESS as a core grid flexibility asset supporting high renewable penetration. |

Increasing Grid Modernization Investments, strengthening the adoption of utility-scale BESS for transmission and distribution network flexibility. | 26% | High | Transmission & distribution (T&D) support, congestion management, grid deferral | Encourages utilities to deploy BESS as a cost-effective alternative to conventional grid expansion while improving network resilience. |

Rising Demand for Grid Stability and ancillary services is encouraging utilities to deploy battery storage for frequency regulation and voltage support. | 22% | High | Frequency regulation, voltage support, spinning reserve, black start | Expands multi-service revenue opportunities and increases the commercial value of grid-scale battery assets. |

Government Incentives and Energy Storage Policies are accelerating large-scale BESS deployment through funding programs, tax incentives, and storage mandates. | 25% | Very High | Utility-scale BESS deployment, capacity markets, renewable integration | Improves project economics, attracts private investment, and accelerates large-scale procurement of battery storage systems. |

Expansion of Hybrid Solar-Plus-Storage and Wind-Plus-Storage Projects is increasing the integration of grid-scale battery systems with renewable energy assets. | 20% | High | Hybrid renewable power plants, energy arbitrage, peak shifting | Increases dispatchability of renewable generation and enhances long-term utilization of transmission infrastructure.

|

Accelerating Utility-Scale Renewable Energy Deployment, driving demand for battery storage to balance intermittent solar and wind power generation

The increasing development of utility-scale solar and wind power production capacity is among the main factors that stimulate the growth of demand for Grid-Scale Battery Energy Storage Systems (BESS). The rising share of renewable energy sources within the electricity systems leads to the increasing use of batteries by electric utility companies and grid operators for managing the variability of generation and ensuring stability and efficiency of renewable energy generation. According to the International Energy Agency (IEA), wind and solar PV are predicted to represent over 90% of the growth in global electricity consumption in 2025, whereas combined production of wind and solar energy is forecasted to surpass 5,000 TWh, confirming the need for grid-scale battery energy storage systems to manage the variability of renewable generation and to ensure the stability of the electricity grid.

This fast growth of utility-scale solar and batteries shows how important grid-scale BESS are becoming to handle the intermittency of renewable energy sources, increase grid flexibility, and guarantee reliable electric power production. In February 2026, according to the U.S. Energy Information Administration (EIA), US power producers plan to develop a record number of 86 GW of additional capacity in 2026, where 43.4 GW (51%) will be solar, and 24 GW (28%) will be battery energy storage. It should be noted that there has been a fast growth in battery storage capacity in the USA over the last five years (more than 40 GW).

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

Lengthy Grid Interconnection and Permitting Processes delay the commissioning of utility-scale BESS installations. | 22% | Project Development & Grid Connection | Utility-scale standalone BESS, renewable energy integration, transmission-connected storage | Extends project development timelines, delays revenue generation, and increases project execution costs. |

Battery Degradation and Limited Operational Lifetime increase lifecycle replacement and maintenance costs for grid-scale systems. | 19% | Asset Lifecycle Management | Frequency regulation, energy arbitrage, renewable energy firming | Increases total cost of ownership (TCO), requiring battery augmentation, long-term service agreements, and higher lifecycle expenditure. |

Uncertain Revenue Models in Emerging Electricity Markets reduce investment confidence for standalone grid-scale BESS projects. | 20% | Project Financing & Investment | Merchant BESS projects, ancillary services, capacity markets | Slows private investment, reduces project bankability, and delays large-scale commercial deployment. |

Transmission Infrastructure Constraints limit the integration of large-scale battery storage with renewable energy projects. | 24% | Grid Infrastructure | Solar-plus-storage, wind-plus-storage, transmission support | Restricts renewable energy integration, postpones BESS commissioning, and increases dependence on costly transmission network upgrades. |

Battery Degradation and Limited Operational Lifetime increase lifecycle replacement and maintenance costs for grid-scale systems

One of the main constraints that restricts the economics of Grid-scale BESS business in the long run is battery degradation, where battery capacity, power, and round-trip efficiency all deteriorate over time as part of the battery lifetime. Grid-scale batteries used for renewable energy balancing, frequency control, and daily charge-discharge cycles continue to age electrochemically; therefore, capacity upgrades and even battery cell replacements are required periodically to maintain the contracted performance. According to the National Renewable Energy Laboratory (NREL), utility-scale lithium-ion battery projects are expected to last about 15–20 years, but battery capacity continuously decreases based on the cycle rate, depth of discharge, temperature, and charging practices.

This study shows the need to consider battery degradation during the planning of grid-scale BESS to maximize efficiency and minimize costs. As per Oak Ridge National Laboratory (ORNL), scientists have developed a model that considers the effect of battery aging in planning of grid-scale battery energy storage systems (BESS) by considering the impact of electrochemical degradation on power system planning. The researchers discovered that consideration of battery degradation increases the precision of the investment and operations decision-making process by 14%.

Grid-Scale Battery Energy Storage System (BESS) Market Segment Analysis

The global Grid-Scale Battery Energy Storage System (BESS) market is segmented based on battery technology, energy capacity, storage duration, grid connection, application, end user, and region.

Lithium-ion Battery Dominance in Grid-Scale BESS Driven by High Energy Density, Cost Decline, and Renewable Integration Demand

The lithium-ion batteries segment holds a dominant position in the battery technology type in the Grid-Scale Battery Energy Storage System (BESS) market, with a market share estimated at 84.8% in 2025. This segment dominance is mainly due to the use of advanced battery technology characterized by higher energy density, high round-trip efficiency, fast charge and discharge rates, and existing global production infrastructure. The decreasing cost structure associated with lithium-ion batteries has contributed significantly to their wide adoption in large-scale utility storage projects. In 2025, lithium-ion battery pack prices kept falling, with stationary storage lithium-ion systems being positively affected by the expansion in large-scale production volumes. Global demand for lithium-ion batteries rose by 29% in 2025 to 1.59 TWh, while the stationary energy storage demand grew by 51% in 2025 year-on-year, according to ESS news.

The increasing preference for lithium-ion batteries that use LFP chemistry has further reinforced the position of the segment through the period from 2025 to 2026 due to safety considerations and long service life, as well as reduced total costs of ownership for both utilities and renewable energy companies. With ongoing capacity expansion in battery production, cost reductions, and the growing need for flexible power grids, lithium-ion batteries will continue to lead market growth through the forecast period.

Grid-Scale Battery Energy Storage System (BESS) Market Geographical Penetration

Accelerating Grid Modernization and Renewable Energy Integration Driving North America’s Leadership in Grid-Scale BESS Market

North America is the dominating region in the Grid-Scale Battery Energy Storage System (BESS) Market, contributing approximately 58.49% of the market share in 2025, owing to various factors such as modernization of grid systems, large-scale deployment of renewables, positive policies regarding energy storage, and increased need for power infrastructure. As per the statistics provided by American Clean Power Association (ACP), the United States Energy Storage market witnessed approximately 18.9 GW of battery energy storage system additions, which indicate 52% growth from last year, while total additions stood at 57.6 GWh.

The acquisition strengthens North America’s domestic manufacturing capability for batteries and provides solutions in the form of utility-scale BESS systems that can be used for the modernization of the electricity grids. In June 2026, T1 Energy, a US-based renewable energy and energy infrastructure company, acquired KORE Power, a US-based battery cell manufacturing and energy storage solutions company, and thus is entering the battery and data center infrastructure businesses. The deal brings the utility-scale BESS solutions of KORE Power under T1 Energy's ownership.

U.S. Grid-Scale Battery Energy Storage System (BESS) Market Trends

The United States holds a dominating market share of the North American Grid-Scale Battery Energy Storage System (BESS) market owing to its rising renewable energy capacity, robust storage solution installation pipeline, sophisticated power network, and favorable energy policies. Large renewable energy companies, battery storage technology suppliers, and utility players have helped to hasten the development of large BESS solutions. Solar and wind power integration, growing demand for electricity from data centers and industries, and the requirement for grid flexibility have boosted the use of battery storage systems for energy shifting, frequency regulation, peak load management, etc.

This acquisition comes amid an increasing trend of investments being made in utility-scale battery storage as the need for energy storage becomes ever more prevalent in the United States. In June 2026, LIXTE Biotechnology Holdings, Inc., a U.S.-based clinical-stage biotechnology company, announced the acquisition of NOMAD Transportable Power Systems, a U.S.-based provider of mobile, utility-grade Battery Energy Storage Systems (BESS). The acquisition marks the entry of LIXTE into the energy storage industry. NOMAD has successfully delivered over 3 GWh of mobile utility-grade BESS and is known for developing transportable energy storage systems.

Canada Grid-Scale Battery Energy Storage System (BESS) Market Outlook

Canada represents a significant market in the North American grid-scale battery energy storage system (BESS) market owing to its growing renewable energy generation capacities, increased grid modernization efforts, and greater need for flexibility in power management. The country’s rich hydroelectric power, growth in renewable energy generation through wind and solar, and greater industrial electrification are generating a need for energy storage technologies in the region. In Canada, grid-scale BESS is being utilized mainly to improve grid stability and manage renewable energy generation, lower peak demand, and reliability in areas where there is high energy consumption.

The installation of the PowerBank Ontario BESS project highlights the fast-paced adoption of utility-scale energy storage facilities in Canada to deal with grid balancing and renewable intermittency issues. In January 2026, PowerBank Corporation, which is a Canada-based renewable energy developer and Independent Power Producer (IPP), announced its 4.99 MW Battery Energy Storage System (BESS) project in Ontario, Canada. This utility-scale facility has been installed to provide large-scale electricity storage capability.

Grid-Scale Battery Energy Storage System (BESS) Market Competitive Landscape

- The market is characterized by three key participant groups: battery cell manufacturers and BESS suppliers, integrated energy storage solution providers, and grid infrastructure technology companies. Leading battery manufacturers such as CATL, BYD, LG Energy Solution, and Samsung SDI dominate lithium-ion battery supply and large-scale storage deployments due to their manufacturing scale, cost competitiveness, and global project presence. System integrators and energy storage specialists, including Sungrow Power Supply, Fluence Energy, Huawei Digital Power, and Wärtsilä, focus on complete BESS solutions covering battery systems, power conversion systems, energy management platforms, and grid integration. Meanwhile, companies such as Hitachi Energy, Siemens Energy, and GE Vernova strengthen the market through grid automation, transmission solutions, and utility-scale energy infrastructure integration. This creates a highly ecosystem-driven landscape where battery technology leadership, project execution capability, supply-chain strength, and grid integration expertise define competitiveness.

- Key players include BYD, CATL, Sungrow Power Supply, Fluence Energy, Huawei Digital Power, LG Energy Solution, Samsung SDI, Wärtsilä, Hitachi Energy, Siemens Energy, Eos Energy Enterprises, Form Energy, and GE Vernova.

Key Developments

- January 2026: NeoVolta Inc., a U.S.-based energy technology company specializing in energy storage solutions, has launched NeoVolta Power, LLC, a joint venture with PotisEdge, a Canada-based Battery Energy Storage System (BESS) manufacturer, and LONGi Green Energy, a China-based renewable energy technology company, to establish a domestic U.S. BESS manufacturing platform.

- May 2026: Ford Energy, a U.S.-based energy storage subsidiary of Ford Motor Company, and EDF Power Solutions North America, a U.S.-based renewable energy developer and power solutions provider, have signed a five-year framework agreement for the supply of up to 20 GWh of Battery Energy Storage Systems (BESS).

- August 2025: FlexGen Power Systems, LLC, a U.S.-based energy storage technology company and battery energy storage solutions provider, completed the acquisition of key assets and intellectual property from Powin LLC, a U.S.-based battery energy storage system (BESS) integrator and energy storage technology company.

- November 2025: Bimergen Energy Corporation, a U.S.-based independent power producer (IPP) and utility-scale Battery Energy Storage System (BESS) project developer, has entered into a Joint Development Agreement (JDA) with Eos Energy Enterprises, Inc., a U.S.-based energy storage technology company specializing in zinc-based long-duration BESS solutions, to accelerate U.S. battery storage deployment.

- December 2025: Vertiv Holdings Co., a U.S.-based critical digital infrastructure and power management solutions company headquartered in Westerville, Ohio, launched the Vertiv™ EnergyCore Grid, a utility-grade battery energy storage system (BESS) designed for large-scale grid-interactive applications across North America.

Key Procurement Priorities and Buyer Evaluation Criteria

- Organizations investing in the Grid-Scale Battery Energy Storage System (BESS) Market are increasingly selecting suppliers based on their ability to provide reliable, high-capacity energy storage solutions with long operational life, high round-trip efficiency, advanced safety features, and scalability for utility-scale deployment.

- The procurement decision-making process is being influenced by the growing demand for renewable energy integration, grid stabilization, peak-load management, and long-duration energy storage solutions. Buyers are prioritizing BESS providers that can support large-scale solar and wind projects, enhance grid flexibility, and provide intelligent energy management capabilities.

- Buyers evaluate key factors such as battery chemistry performance, energy density, cycle life, degradation rate, thermal management, safety certifications, system efficiency, and warranty terms while selecting their BESS technology partners. The increasing adoption of lithium-ion batteries, particularly LFP-based systems, has made reliability, cost competitiveness, and lifecycle performance critical procurement considerations.

Why Choose DataM?

- Technological Innovations: Explores advancements in grid-scale Battery Energy Storage System (BESS) technologies, including lithium-ion battery systems, lithium iron phosphate (LFP) chemistries, long-duration energy storage solutions, advanced battery management systems (BMS), and intelligent energy management platforms, enabling improved storage efficiency, enhanced safety, longer lifecycle performance, and reliable integration with renewable energy sources.

- Product Performance & Market Positioning: Evaluates how different BESS providers differentiate their solutions based on energy capacity, round-trip efficiency, cycle life, degradation performance, thermal management, safety features, response time, and cost competitiveness, highlighting the positioning of leading companies across utility-scale renewable integration, grid balancing, peak shaving, and backup power applications.

- Real-World Evidence: Highlights real-world adoption of grid-scale BESS solutions in renewable energy projects, utility networks, microgrids, and large-scale power infrastructure, demonstrating benefits such as improved grid stability, reduced renewable energy curtailment, enhanced peak demand management, and increased reliability of electricity supply.

- Market Updates & Industry Changes: Tracks key developments including large-scale battery storage project deployments, domestic battery manufacturing expansions, renewable-plus-storage investments, regulatory updates, and technology advancements across North America, Asia-Pacific, and Europe, supporting the transition toward flexible and resilient energy systems.

- Competitive Strategies: Analyzes how leading companies expand through battery manufacturing capacity expansion, strategic partnerships, utility-scale project development, technology innovation, and integration of hardware and digital energy management platforms to address increasing demand for renewable energy storage and grid modernization.

- Pricing & Market Access: Explains pricing variations based on battery chemistry, storage duration, system capacity, project scale, installation requirements, and integration complexity, along with access through battery manufacturers, energy storage system integrators, utilities, renewable energy developers, and independent power producers supporting global deployment.

- Market Entry & Expansion: Identifies growth opportunities driven by renewable energy penetration, increasing electricity demand, grid reliability requirements, data center power needs, and electrification trends, while outlining strategies such as regional manufacturing expansion, next-generation battery technology development, utility partnerships, and customized BESS solutions to strengthen global market presence.

Target Audience

- Battery Manufacturers & Energy Storage System Providers

- Energy Utilities & Grid Operators

- Renewable Energy Developers & Independent Power Producers (IPPs)

- Battery Technology & Component Suppliers

- Energy Storage System Integrators & Solution Providers

- Government Bodies & Regulatory Authorities

- Investment Firms, Venture Capitalists & Financial Institutions