Graphite Recycling Market Definition and Overview

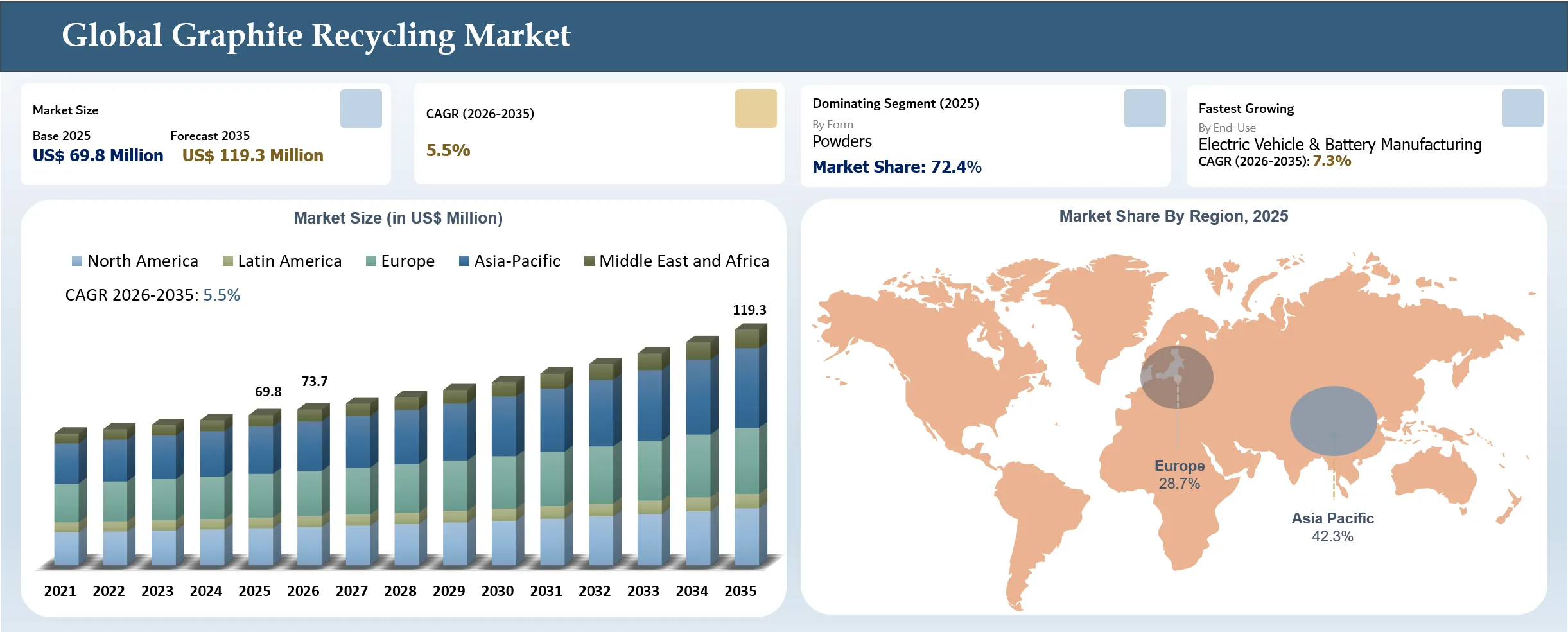

The global Graphite Recycling market reached USD 69.8 Million in 2025 and is expected to reach USD 119.3 Million by 2035, growing with a CAGR of 5.5% during the forecast period 2026-2035. The market continues to grow steadily through the rising amount of graphite recovered from end-of-life lithium-ion batteries, scrap batteries, old electrodes, and industrial carbon.

Rising need for securing critical minerals along with fast growth in the supply chain of electric vehicles and energy storage is fostering investments in graphite recycling facilities and technology. The new methods for graphite recycling have enabled the production of high purity recycled graphite for use in batteries and industry. Recycling of graphite is being done by industry players to meet the sustainability goals, domestic source needs, and regulations regarding the recycling of battery materials. Nevertheless, problems related to purity of graphite, inconsistency of feedstocks, logistical issues, and economics of recycled graphite vis-à-vis virgin graphite affect the market dynamics.

Key Takeaways

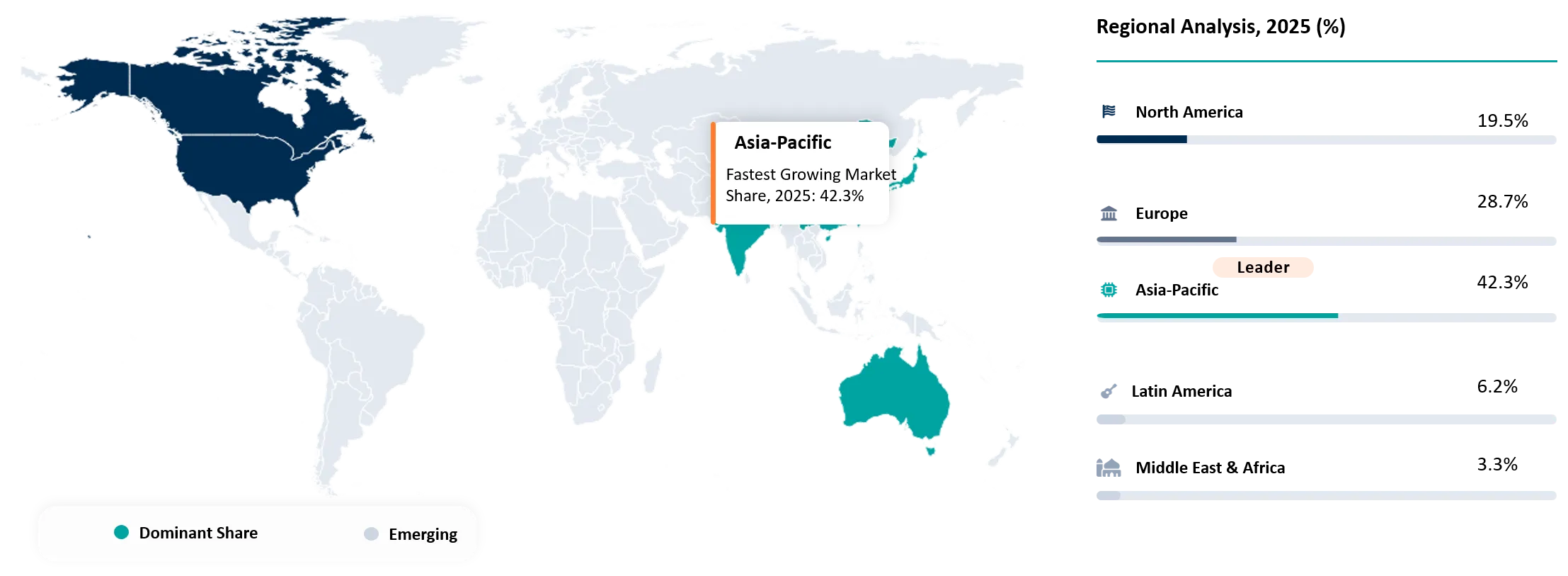

- Asia-Pacific is the largest regional market with a market revenue share of 42.3% in 2025, due to its strong presence in battery production and graphite processing.

- Powdered recycled graphite is the leading form segment, comprising a market revenue share of 72.4% in 2025, owing to its wide application in lithium-ion batteries and industrial uses.

- Graphite recovery rates of over 95% with purities greater than 99.5% have been realized by advanced recycling techniques to ensure the development of recycled graphite of battery grade.

- A process developed at the University of Pavia in 2025, for graphite recycling was able to recover more than 96% of graphite with 99.6% purity, proving the viability of using high-quality recycled graphite for battery anodes.

- The worldwide battery production system is projected to have a manufacturing capacity of more than 3 TWh by 2025–2026.

Graphite Recycling Market Industry Trends and Strategic Insight

- Supply chain localization and critical mineral security concerns are accelerating the investment in graphite recycling infrastructure

- Commercial preference is shifting towards hydrometallurgy, flotation, and thermal purification technologies because of their capacity to retain graphite's microstructure and electrochemical properties.

- Vertical recovery systems for closed-loop battery material ecosystems between battery manufacturers, electric vehicle original equipment manufacturers, and recyclers are being set up to recycle important materials such as graphite, lithium, nickel, and cobalt.

- The development of new technology will enable the purification and reconditioning of spent graphite for use as anode material in batteries instead of low-value uses in industry.

- Regulations are being introduced in Europe, North America, and Asia, including recycled content requirements and recovery targets, which provide future demand visibility for recycled graphite.

Graphite Recycling Market Scope

| Metrics | Details | |

| 2025 Market Size | USD 69.8 Million | |

| 2035 Projected Market Size | USD 119.3 Million | |

| CAGR (2026-2035) | 5.5% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Source | Lithium-Ion Batteries, Electrodes, Motor Brushes & Crucibles, Foundry Facings, Nuclear Reactor Graphite, Industrial Graphite Scrap, Others | |

| By Form | Powders, Solid Chunks, Others | |

| By Graphite Type | Natural Graphite, Synthetic Graphite | |

| By Recycling Technology | Hydrometallurgical Processing, Thermal Purification, Chemical Treatment, Mechanical Processing, Flotation & Separation Technologies | |

| By Application | Batteries, Metal Casting, Lubricants, Refractories, Foundry Operations, Nuclear Reactors, Conductive Materials, Others | |

| By End-Use | Electric Vehicle & Battery Manufacturing, Metallurgy & Steel Production, Energy Storage Systems, Chemical & Lubricant Industry, Aerospace & Defense, Industrial Manufacturing, Nuclear Energy, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Graphite Recycling Market Disruption Analysis

Shift Toward Silicon-Enhanced and Next-Generation Battery Anodes Reshaping the Graphite Recycling Landscape

Disruption of the graphite recycling market can mainly be attributed to the fast commercialization of silicon-enabled anodes, high-performance LFP batteries, and upcoming solid-state batteries. This is slowly changing the graphite content per each battery cell and introducing different specifications of material usage along the entire battery supply chain. By 2025, the number of EVs sold globally will have reached over 20 million units, which is more than 25% of all vehicles sold globally that year, according to the International Energy Agency. This will drive up battery manufacturing rates, and there will be a need for next-gen anode materials. As battery manufacturers seek greater energy density and faster charging capability in their products, the conventional graphite anode designs are being gradually replaced by silicon-enabled materials.

Conversely, battery makers and recyclers are also being made to reconsider their recycling strategies in order to adapt to changes in anode chemistries. According to the International Energy Agency (IEA), 2025 reports that the battery production capacity will cross 3 TWh globally by 2025, thus creating a need for recycling facilities that have the flexibility to handle different types of batteries. This has created problems for traditional graphite recycling methods since the systems for purifying graphite can become less efficient in recovering battery-grade graphite from anodes containing silicon.

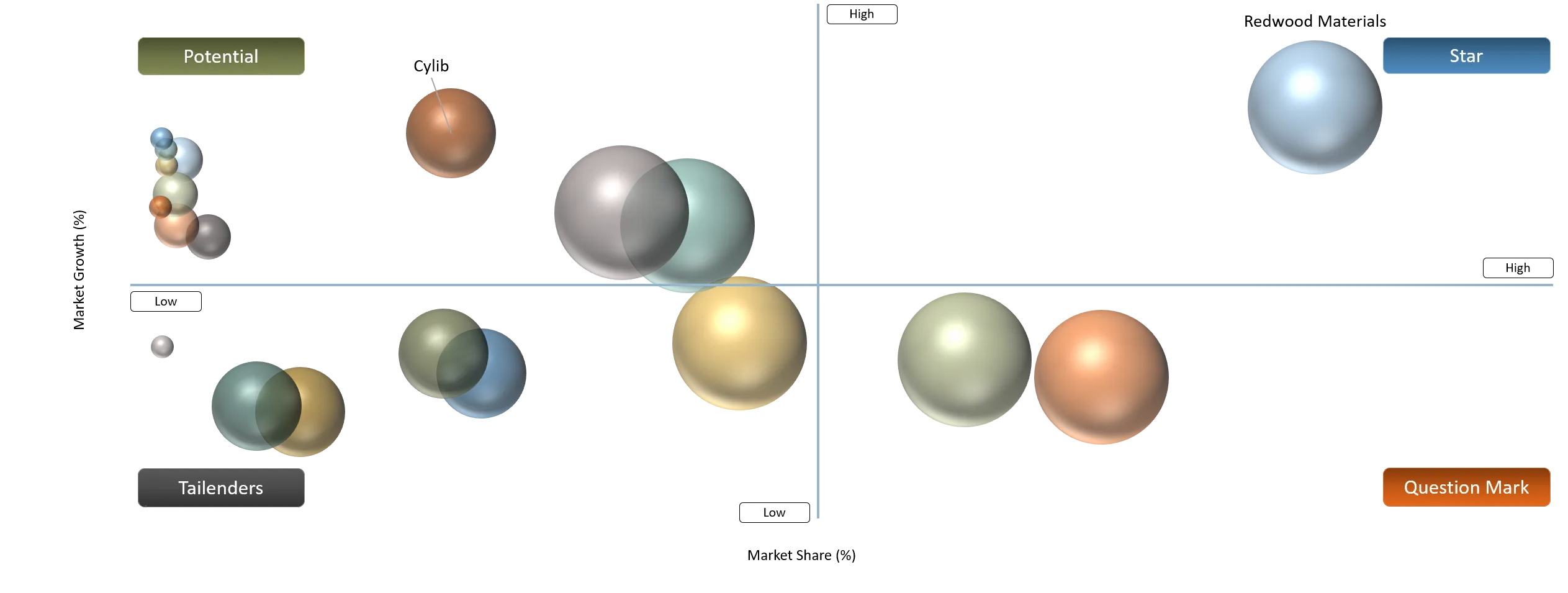

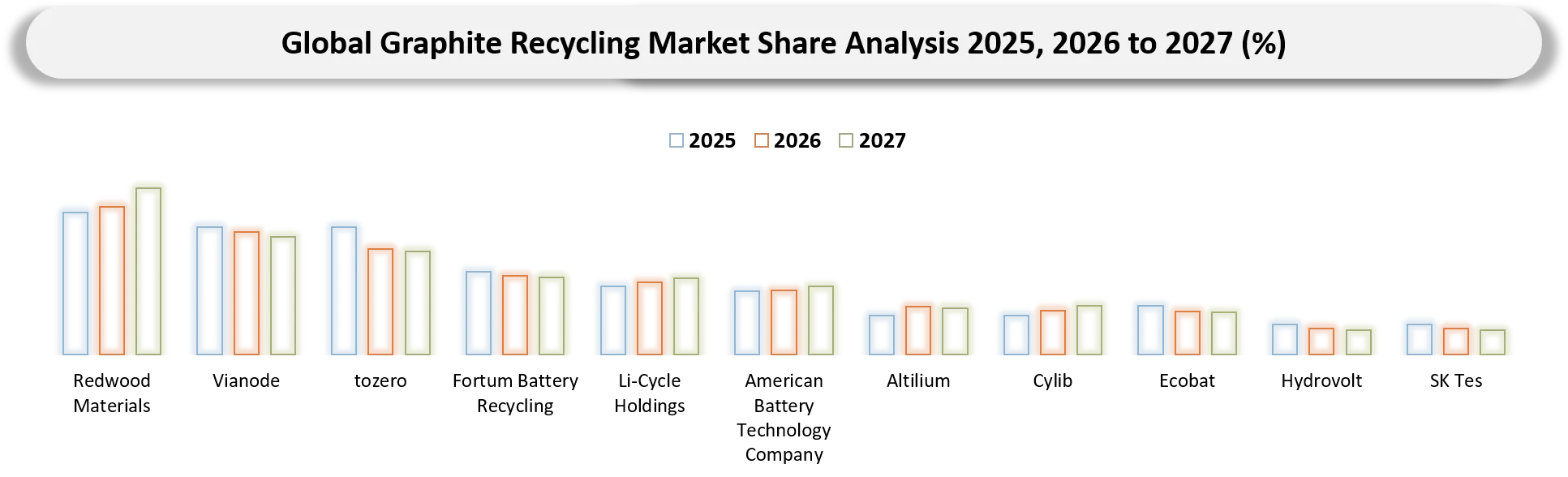

Graphite Recycling Market BCG Matrix: Company Evaluation

Star companies in this category include Redwood Materials, Li-Cycle Holdings, and Ascend Elements, owing to their solid presence within the lithium-ion battery recycling value chain, material recovery skills, and existing relationships with automobile manufacturers and battery makers. They are already in the process of ramping up their commercial operations as well as investing in technology that is capable of recovering high-purity graphite in addition to lithium, nickel, and cobalt. Question Marks companies are Fortum Battery Recycling, Vianode, tozero, American Battery Technology Company, and Altilium. These firms are aggressively pursuing technologies related to graphite extraction and purification and have shown much promise in developing battery-grade recycled graphite.

The Potential Players group consists of Cylib, Ecobat, Hydrovolt, and SK Tes. They have well-developed battery recycling facilities as well as access to large amounts of battery waste. In addition to this, it can be used to develop their abilities in graphite recovery. At the same time, although their present business models do not deal with this type of work, the growing demand for graphite recycling can change this situation. Tailenders are EcoGraf Limited and Neometals Ltd. Although both companies are engaged in battery and recycling-related projects, their involvement in graphite recycling is modest compared to top battery recyclers and graphite recovery companies.

Graphite Recycling Market: Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Increasing interest by governments and industry in cutting their reliance on overseas, regionally centralized sources of graphite is helping to raise recycled graphite to the status of an important secondary resource. | 1.3% | High

| EV batteries, energy storage systems (ESS), battery anode manufacturing | Strengthens domestic critical mineral security, improves supply chain resilience, and accelerates investments in localized recycling infrastructure. |

The construction boom in battery gigafactories is creating significant amounts of production waste material that contains recoverable graphite. | 1.2% | Very High | Battery manufacturing scrap recycling, EV battery supply chain | Creates a stable feedstock pipeline, improves recycler utilization rates, and supports large-scale commercialization of graphite recovery operations. |

Advances in technology for hydrometallurgy, thermal treatment, flotation, and regeneration have improved the yield and purity of recycled graphite. | 1.1% | High | Battery-grade graphite production, anode material regeneration | Enables production of high-purity recycled graphite (>99% purity), expanding adoption in lithium-ion battery applications and improving project economics. |

There are fewer operations needed for recycling graphite and lower exposure to the risks of volatility associated with mining and refining, thus becoming cost-effective. | 0.9% | Medium-High | Industrial graphite applications, battery materials, conductive materials | Reduces exposure to mining-related price volatility and supports long-term procurement cost optimization for battery manufacturers. |

The emerging battery regulations in major markets that mandate high recovery rates and recycled content targets will create a policy-backed demand for recycled graphite. | 1.4% | Very High | EV batteries, battery recycling, energy storage systems | Establishes long-term market certainty, accelerates recycling capacity expansion, and promotes closed-loop battery material ecosystems. |

Advances in technology for hydrometallurgy, thermal treatment, flotation, and regeneration have improved the yield and purity of recycled graphite

Continuous technological advancements in hydrometallurgy, thermal processing, flotation, and graphite regeneration technology are becoming a key factor that is helping to propel the Graphite Recycling Market forward. New technological innovations are making it possible for recyclers to reclaim graphite with much higher purity while maintaining its structure in order to make it ready for use in battery manufacturing. According to PubMed Central (PMC) by 2025, various large-scale recycling operations have managed to achieve a recovery rate of over 95% for graphite while new purification methods enabled obtaining graphite of over 99.5% purity, which is necessary for use in lithium-ion batteries. As a result of all that, recycled graphite is turning into a valuable product rather than a waste byproduct.

Meanwhile, growing investments in battery recycling facilities is speeding up the adoption of the latest graphite regeneration technologies. The International Energy Agency (IEA) predicts that by 2025–2026, the world’s battery production capacity will be more than 3 TWh, thus requiring a sustainable supply of battery components, including recycled graphite. For example, in 2025, the Chemistry Europe Association, a Germany-based publishing association and federation, published a closed-loop process that is environmentally friendly for graphite recycling from waste lithium-ion batteries in 2025. This method was developed by the University of Pavia; the process comprised green froth flotation, mild organic acid leaching, and thermal rejuvenation. This process resulted in more than 96% graphite having 99.6% purity, hence ensuring that the recycled graphite can be further recycled and used as anodes in batteries having properties like commercial graphite.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

The commercialization of more sophisticated graphite recovery technologies is hindered by problems associated with scaling up in relation to efficiency, capacity, and profit margin. | 1.1% | Technology Commercialization & Processing Efficiency | Battery-grade graphite production, anode material regeneration | Delays large-scale deployment of recovery facilities and slows penetration of recycled graphite into premium battery applications. |

Insufficient collection facilities, waste segregation, and irregular supply of raw materials limit the amount of recycling and utilization of recovery plants. | 1.3% | Feedstock Supply Chain & Collection Network | End-of-life EV batteries, battery manufacturing scrap recycling | Creates raw material shortages, reduces operational efficiency, and restricts expansion of graphite recovery capacity. |

Graphite recycling frequently becomes a secondary priority than the extraction of more valuable metals such as lithium, nickel, and cobalt. | 1.0% | Capital Allocation & Technology Development | Integrated battery recycling operations | Limits investment in graphite-specific recovery technologies and delays development of dedicated graphite circularity ecosystems. |

The feasibility of graphite recycling is yet questionable because of its dependence on fluctuating graphite prices, available feedstock, yield rate, and level of technology advancement. | 1.2% | Project Economics & Profitability | Commercial recycling projects, battery material supply chains | Increases investment uncertainty and slows adoption of large-scale graphite recovery infrastructure. |

Graphite recycling frequently becomes a secondary priority than the extraction of more valuable metals such as lithium, nickel, and cobalt

One of the important constraints in the Graphite Recycled market is the ongoing concentration of efforts in mining other high-value battery minerals such as lithium, nickel, and cobalt, making graphite a secondary option. Most battery recycling facilities derive the bulk of their recycling income from these battery minerals and thus allocate efforts to optimize processes and develop technology around them. The International Energy Agency (IEA) estimates that global battery demand will be above 1.5 TWh by 2025 and production capacity above 3 TWh by 2026. This would require substantial investments in the infrastructure for critical mineral recovery; however, most of the investment goes toward lithium, nickel, and cobalt recovery.

The challenges are made more difficult because of the relatively low market price of graphite compared to other battery materials. While it is often true that graphite forms the bulk of a lithium-ion battery by weight, recycling plants still regard graphite-containing black mass as a secondary processing stream rather than a primary revenue source. For example, in 2025, Wiley Online Library published a study that revealed that battery recycling processes have always focused more on recovering precious metals like lithium, nickel, and cobalt than graphite. The study stressed that the increasing need for graphite recovery and regeneration techniques was essential to create a more efficient battery recycling process and hence boost the Graphite Recycling Market.

Graphite Recycling Market Segment Analysis

The global graphite recycling market is segmented based on source, form, graphite type, recycling technology, application, end-use, and region.

Powdered Recycled Graphite Dominates the Market Owing to Strong Demand from Battery and Industrial Applications

Graphite powders are the dominating segment of the Graphite Recycled market in terms of revenue share, holding an estimated 72.4% share of the market in 2025. This is attributed to their widespread application in lithium-ion batteries, conducting compounds, lubricants, refractory materials, and metallurgy. Graphite in powder form is the commercial choice because graphite recovery processes involve processes such as milling, purifying, and sizing of particles. Increased demand for high-purity graphite powders from battery-grade applications has been spurred by the fast-growing supply chains of EVs and battery storage devices. Graphite Recovery companies are increasingly inclined towards the production of graphite powder of grades above 99.5% purity, which allows for their direct use in the lithium-ion battery value chain.

This form of material is also easier to handle, blend, and process when compared to bigger graphite pieces, making it the preferred form in terms of battery production and the industry overall. Due to the demand from battery manufacturers for circular material sourcing and increasing regulations that encourage recycled material use, powdered recycled graphite keeps its place as the largest market revenue segment.

Graphite Recycling Market Geographical Penetration

Asia-Pacific Leads the Graphite Recycling Market Through Battery Manufacturing Dominance and Expanding Circular Material Infrastructure

The Asia-Pacific Region dominates the Graphite Recycling Market, accounting through an anticipated market share of 42.3% of total market revenues in 2025, due to its dominance in lithium-ion battery production, electric vehicles manufacture, as well as graphite production processes. The three countries of China, Japan, and South Korea form the largest battery manufacturing ecosystem in the world that produces considerable amounts of battery manufacturing waste and old batteries, serving as a good source of raw materials for graphite recycling. Moreover, rising government backing towards critical minerals security and battery recycling further enhances the market position of the Asia Pacific region.

Another factor contributing to the dominance of Asia Pacific is the well-integrated battery materials value chain that allows effective collection, processing, purification, and recycling of graphite back into the battery-making process. It is forecasted that Asia Pacific region will remain the leading revenue contributor for the Graphite Recycling Market. For instance, in May 2026, EcoGraf Limited, an Australian-based supplier of battery anode materials, was awarded an Indian patent (Patent No. 587710) for its HFfree technology, its first-generation purification process.

China Graphite Recycling Market Trends

China has dominating position in the Asia-Pacific Graphite Recycling Market, due to a large lithium-ion battery production capacity, expertise in the processing of graphite and increasing recycling infrastructure for batteries. This is because of the highly integrated battery value chain, which consists of anode material producers, battery cell makers, electric vehicles OEMs, and battery recyclers that help in the recovery of graphite from battery manufacturing waste and spent batteries. According to International Energy Agency (IEA), China is projected to represent over 70% share of the total lithium-ion battery manufacturing capacity in the year 2025, which will further solidify its position as the top producer of recycled battery materials.

For instance, in 2024, GEM Co., Ltd., a prominent company in battery recycling and materials production in China, has signed a cooperation agreement with China Minmetals Graphite Industry Co., Ltd. and Shenzhen Eigen Equation Graphene Technology Co., Ltd. This will help improve the process of recycling graphite from lithium-ion batteries, as well as the development of anode materials.

South Korea Graphite Recycling Market Outlook

South Korea is fastest growing country in the Asia-Pacific Graphite Recycling Market due to its top-class battery production ecosystem, investments in battery recycling facilities, and efforts in sourcing critical battery materials domestically. As a home to large battery producers including LG Energy Solution, Samsung SDI, and SK On, the nation produces large quantities of battery production waste and future waste batteries that can be recycled for graphite recovery. As per the IEA, South Korea continues to be one of the largest producers of lithium-ion batteries in the world in 2025, while the government continues to fund circular economy projects that will help reduce reliance on imported critical materials.

For instance, in August 2025, SK On, an of South Korea-based electric vehicle battery manufacturing company, collaborated with Ecopro to create a battery recycling ecosystem and acquire a steady supply of black powder extracted from scrapped batteries in manufacturing processes and at the end of the useful life of the batteries.

Graphite Recycling Market Competitive Landscape

- The graphite recycling market is comprised of three main stakeholder groups, including integrated battery recyclers, graphite recovery/anode materials firms, and circularity technology companies. Among market leaders are Redwood Materials, Li-Cycle Holdings, Ascend Elements, Ecobat, SK Tes, and Fortum Battery Recycling, which dominate the market via large-scale battery recycling and recovery networks that can recycle lithium-ion battery waste and end-of-life batteries. Vianode, tozero, Altilium, Cylib, and American Battery Technology Company are building up their presence in the market with their investments in battery-grade graphite recovery and purification, along with their closed-loop battery material supply chain development. On the other hand, EcoGraf Limited, Neometals Ltd., and Hydrovolt concentrate on advanced graphite purification technology and sustainable battery material recovery, along with their strategic alliances towards commercialization of recycled graphite for battery production. Therefore, the highly circular market competitiveness is determined by feedstock availability, graphite purification expertise, qualification of battery grade material, and integration into battery manufacturing ecosystem.

- Key players involved are companies such as Fortum Battery Recycling, Vianode, tozero, Redwood Materials, Li-Cycle Holdings, American Battery Technology Company, Altilium, Cylib, Ecobat, Hydrovolt, SK Tes, Ascend Elements, EcoGraf Limited, and Neometals Ltd.

Key Developments

- May 2025: Vedanta Aluminium, which is a largest aluminium manufacturer in India, unveiled its revolutionary patented technology that will extract more than 99% pure graphite from the wastes generated in aluminium manufacturing processes.

- May 2025: Battery X Metals, a Canada-based company specializing in battery recycling technology, made a significant breakthrough in achieving 98.6% recovery rate of graphite and 96.3% purity of metal oxides using their unique two-stage flotation technique.

- September 2025: Talga Group, an Australia-based battery materials manufacturer, launched Talnode-R, a recycled graphite anode product manufactured from lithium-ion battery waste.

- May 2025: Vianode, a Norwegian battery materials firm, collaborated with Finnish battery recycling firm Fortum Battery Recycling to obtain recycled graphite concentrate from decommissioned EV batteries and produce recycled graphite materials used in anode manufacturing on a commercial scale.

- February 2025: Altilium, a UK-based clean technology and battery recycling company, entered into an MoU agreement with Talga Group for the supply of up to 16,000 tonnes of recycled graphite derived from used EV batteries that can be utilized in making battery anodes.

- June 2026: Bridge Green, a India-based battery recycling firm, established Tamil Nadu's first critical minerals recovery plant for recycling lithium-ion batteries and scraps from battery production processes.

- March 2026: Hydrovolt, a company specializing in battery recycling, signed an MoU with POSCO HY Clean Metal and Mitsui & Co. to set up a circular supply chain for used lithium-ion batteries, allowing black mass containing battery material such as graphite to be recycled and used for manufacturing new batteries.

Key Procurement Priorities and Buyer Evaluation Criteria

- Companies developing graphite recycling and battery material supply chain sustainability strategies have started preferring suppliers who can provide highly pure recycled graphite capable of meeting all battery-grade specifications, including particle size distribution, purity percentage, electrochemical behavior, and batch-to-batch consistency. With the rise in usage of recycled graphite in the manufacture of lithium-ion batteries, procurement strategy is more concerned with qualification of the material itself and its supply continuity.

- The procurement process is being heavily impacted by the rapid-growing trend towards EVs, batteries gigafactories, and regulations stipulating recycled content in battery materials. The buyers are looking for recyclers able to help develop closed-loop battery material ecosystem, minimize dependency on graphite imports, and provide the traceable and low-carbon sources of critical raw materials needed for batteries.

- Buyers evaluate potential suppliers by using variables graphite recovery efficiency, such as purification process capability, capability to certify graphite as battery grade, feedstock availability, production scalability and traceability. Efficiently recovering graphite while still maintaining its purity is increasingly becoming a criterion in supplier evaluation and procurement decisions.

- The decision-making in procurement strategy is becoming more influenced by the capability of the supplier to provide for new technologies such as silicon-based anodes, lithium-ion technology, and future energy storage technology. Hence, recycling companies with strong research and development skills and expertise in battery material qualification and partnership within the battery supply chain will become the preferred suppliers.

Why Choose DataM?

- Technological Innovations: Presents developments in the field of graphite recycling techniques such as mechanical separation, hydrometallurgical purification, thermal regeneration, direct anode material recycling, AI process optimization, and closed-loop recycling, thereby facilitating high-quality graphite recovery, low energy use, and better utilization of battery grade anode materials.

- Product Performance & Market Positioning: Discusses the strategies adopted by prominent firms to distinguish themselves based on graphite recovery efficiency, purification techniques, quality of materials, adaptability of raw materials, scalability of the process, and cost effectiveness, emphasizing the strategies aimed at increasing the availability of recycled graphite for lithium-ion batteries.

- Real-World Evidence: Presents the implementation of graphite recycling by commercial entities within electric vehicle battery recycling facilities, consumer electronics recycling plants, battery manufacturing plants, and critical mineral recycling projects, thereby providing advantages including decreased dependency on natural graphite mining, reduced carbon footprints, improved resource efficiency, and secure sourcing of battery grade anode material.

- Market Updates & Industry Changes: Identifies key trends such as commercialization of state-of-the-art graphite extraction processes, growth in recycling facilities, partnerships between recyclers and battery producers, investment in battery ecosystems, and new policies to support the recovery of critical minerals from North America, Europe, and Asia Pacific.

- Competitive Strategies: Examines how top corporations reinforce their competitive position by utilizing their own graphite purification technology, building strategic alliances with battery makers and car manufacturers, expanding recycling capacity, licensing technologies, and incorporating themselves into closed-loop battery materials production chains.

- Pricing & Market Access: Pricing mechanism is discussed according to graphite grade, feedstock mix, recovery rate, process technology, and battery grade specifications while evaluating market entry options via battery recyclers, anode materials manufacturers, battery manufacturers, and collaborations in the global battery industry value chain.

- Market Entry & Expansion: Highlights the potential growth areas that include end-of-life lithium-ion batteries, demand for eco-friendly anodes, secure sourcing of critical minerals, and circular economy policies, and discusses approaches like building regional recycling facilities, use of high-tech purification methods, partnering with other entities, and recycling materials for sustained market growth.

Target Audience

- Battery Manufacturers and Cell Producers

- Electric Vehicle (EV) Manufacturers

- Battery Recycling Companies

- Graphite Processors and Anode Material Manufacturers

- Critical Minerals and Advanced Materials Companies

- Energy Storage System (ESS) Developers and Manufacturers

- Conductive Material and Carbon Product Manufacturers