Overview

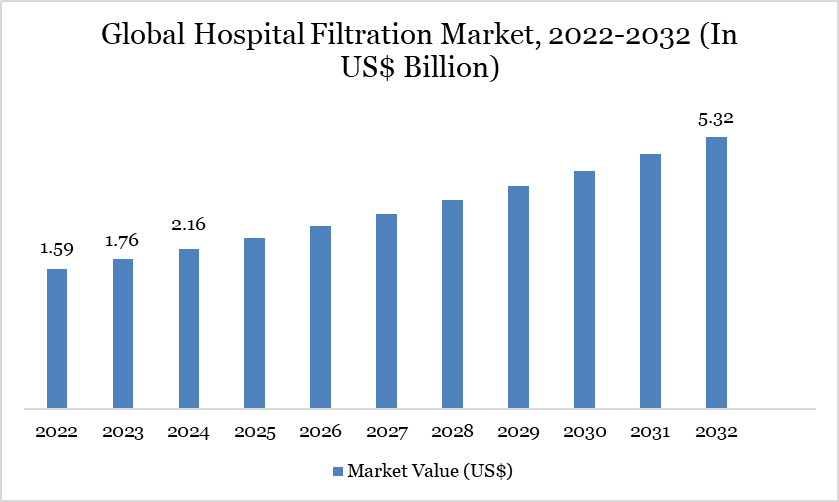

Global hospital filtration Market reached US$ 2.42 billion in 2025 and is expected to reach US$ 5.96 billion by 2033, growing with a CAGR of 12.06% during the forecast period 2026-2033.

Market Scope

Metrics | Details |

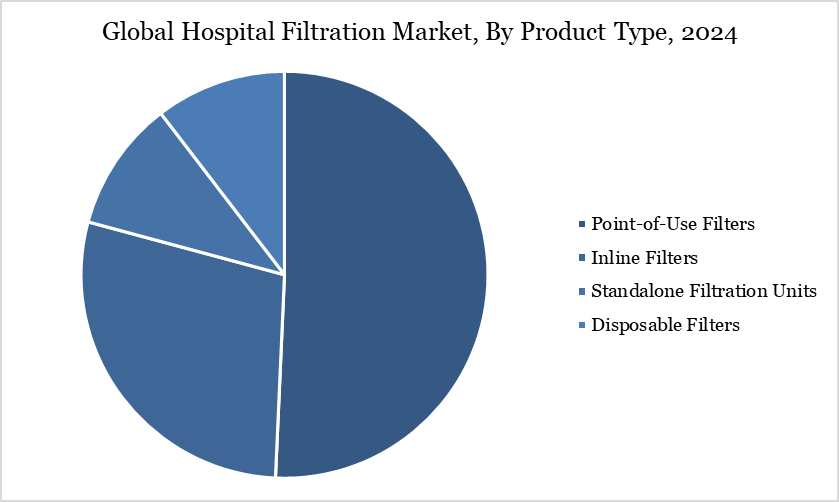

By Product Type | Point-of-Use Filters, Inline Filters, Standalone Filtration Units, Disposable Filters |

By Material Type | Polyethersulfone (PES), Polyvinylidene Fluoride (PVDF), Polypropylene (PP), Others |

By Application | Operating Rooms (ORs), Intensive Care Units (ICUs), Patient Wards, Laboratories, Diagnostic Centers, Medical Device Filtration, Others |

By Technology | HEPA Filtration, Reverse Osmosis (RO), Ultrafiltration, Gas Filtration, Activated Carbon Filtration, UV Germicidal Irradiation, Others |

By Region | North America, South America, Europe, Asia-Pacific and Middle East and Africa |

Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth |

Market Dynamics

Rising Focus on Airborne Infection Control in Healthcare Facilities

The global health authorities emphasized airborne infection as a critical threat, with hospital-acquired infections affecting up to 15% of patients in low- and middle-income countries. The US CDC updated its guidelines recommending HEPA-level air filtration in all patient care areas, prompting widespread adoption. Germany and Japan allocated new federal funding for hospital HVAC retrofits targeting improved airborne pathogen containment. These regulatory and institutional measures are significantly boosting global demand for advanced hospital filtration systems.

High Initial Implementation and Integration Costs

High initial implementation and integration costs continue to restrain adoption of hospital filtration systems globally. In 2024, US federal data estimated that full HVAC and filtration retrofits in medium-sized hospitals ranged more than US$ 1 million, often excluding operational disruptions. Smaller healthcare facilities in Southeast Asia reported delays in upgrades due to lack of access to capital subsidies or government-backed financing programs.

Segment Analysis

The global hospital filtration market is segmented based on product type, material type, technology, application and region.

Point-of-Use Filters Segment Driving Hospital Filtration Market

The point-of-use (POU) filters segment is significantly driving growth in the global hospital filtration market by offering localized, high-efficiency filtration at patient touchpoints. In 2024, it emerged as the fastest-growing segment due to its cost-effectiveness and utility in areas like dialysis units, surgical suites, and faucet outlets. Clinical evaluations at cancer care centers showed these filters effectively prevented Legionella exposure for over 12 weeks while reducing bacterial load. Similar results were seen in Canadian hospitals, where 0.2 µm POU filters consistently eliminated harmful pathogens from faucets and showers, supporting infection control mandates in healthcare settings.

Geographical Penetration

North America Drives the Global Hospital Filtration Market

North America, comprising the US, Canada, and Mexico, dominates the hospital filtration market, accounting for approximately 28% of the global US$ 2.16 billion market in 2024—about USD 605 million in regional demand. The US market alone reached more than US$ 1 billion underscoring high investments in advanced air and water sterilization technologies, including HEPA and ULPA systems.

Government regulations and rigorous infection-control standards in hospitals continue to drive procurement of point-of-use filters and inline systems. In 2024, stringent guidelines for healthcare facility HVAC upgrades led to a 20% rise in retrofitting projects across the region, supported by federal tax incentives targeting sustainability and safety compliance.

Sustainability Analysis

In 2024, hospitals were found to account for 9.8% of total US greenhouse gas emissions, highlighting the critical need for energy-efficient hospital infrastructure, including advanced filtration systems. Pilot HVAC retrofitting projects funded in California demonstrated over 20% reduction in natural gas usage in hospital environments. Tax incentives for energy upgrades helped hospitals achieve year-over-year energy and emissions reductions of around 27%, with further improvements expected through the Inflation Reduction Act.

In Europe, hospitals have adopted green procurement strategies aimed at cutting CO₂ emissions by 75% by 2030, prompting increased demand for sustainable air filtration technologies. Additional studies showed that simple HVAC control adjustments could reduce energy consumption in hospitals by up to 36%, reinforcing the role of intelligent filtration systems in meeting global healthcare sustainability goals.

Competitive Landscape

The major global players in the market include Merck Life Science Private Limited, Danaher Corporation, Sartorius AG, Parker-Hannifin Corporation, 3M Company, Donaldson Company, Inc., Camfil Group, Atlas Copco AB, GE Healthcare, and Thermo Fisher Scientific, all of which offer specialized filtration solutions for medical and hospital environments.

Key Developments

February 2026: Increasing focus on infection prevention and indoor air quality across healthcare facilities significantly accelerated the adoption of advanced filtration systems, particularly in critical areas such as ICUs and operating rooms.

January 2026: Technological advancements in HEPA and ULPA filters, along with smart monitoring systems, improved filtration efficiency and enabled real-time performance tracking in hospital environments.

December 2025: Leading companies such as 3M, Camfil, Parker Hannifin, Freudenberg Filtration Technologies, and Donaldson Company expanded investments in product innovation and high-efficiency filtration solutions to enhance patient safety.

November 2025: Increasing regulatory standards and compliance requirements for healthcare hygiene and safety significantly boosted demand for regulatory compliance solutions in hospital filtration systems.

October 2025: Rising healthcare infrastructure development, including expansion of hospitals and ambulatory surgical centers, drove demand for infrastructure growth and advanced air and liquid filtration technologies.

September 2025: Growing awareness of hospital-acquired infections and the need for contamination control accelerated the adoption of infection control filtration solutions across global healthcare facilities.

The market is rapidly evolving toward high-efficiency, technology-driven filtration systems, where innovations in air, liquid, and medical device filtration are enhancing patient safety, ensuring regulatory compliance, and supporting modern healthcare infrastructure development.

Why Choose DataM?

Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience 2024

Manufacturers/ Buyers

Industry Investors/Investment Bankers

Research Professionals

Emerging Companies