Germany Floating Solar Panels Market Size

Germany floating solar panels market is transitioning from pilot-scale experimentation into an early commercialization phase, supported by land scarcity pressures and the country’s aggressive renewable energy transition agenda.

Germany Floating Solar Panels Market is valued at US$ 3.28 million in 2025 and is projected to reach US$ 38.72 million by 2035, growing at a CAGR of 28% during 2025–2035.

Germany investment timing is becoming increasingly relevant as utilities, infrastructure operators, and industrial energy buyers evaluate non-land intensive solar solutions. With over 82.7 GWp of installed photovoltaic capacity and approximately 3.7 million solar systems already deployed, floating solar is positioned as a complementary expansion layer rather than a replacement technology.

A key driver shaping buyer interest is the utilization of artificial water bodies, including post-mining lakes, which represent untapped renewable generation zones. This aligns closely with Germany land optimization strategy, where agricultural and urban land competition limits traditional solar expansion.

The reader’s investment lens is particularly important here: the market is still small in value terms but structurally significant for long-term infrastructure planning, procurement frameworks, and utility-scale decarbonization strategies.

Key Takeaways

- Stationary floating solar systems already hold more than 50% share, indicating preference for low-complexity, fixed-installation models.

- Artificial lakes from lignite mining are emerging as high-potential deployment zones, reducing land-use conflicts for large-scale solar expansion.

- Germany dense PV ecosystem of 3.7 million installations provides integration readiness for hybrid solar expansion strategies.

- Competitive positioning is increasingly defined by engineering capability, lifecycle cost optimization, and regulatory compliance readiness.

- Investment attractiveness is closely tied to policy alignment and feasibility validation rather than immediate high-volume deployment.

Market Scope

| Metric | Details |

| Market Size (2025) | US$3.28 Million |

| Market Size (2035) | US$38.72 Million |

| CAGR (2025–2032) | 28% |

| Historic Years | 2023–2024 |

| Base Year | 2025 |

| Forecast Period | 2026–2035 |

| Segments Covered | Type (Stationary Floating Solar Panels, Others), Deployment Site (Reservoirs, Mining Lakes, Ponds), Application |

Market Dynamics: Structural Drivers Shaping Adoption

Land Scarcity and Infrastructure Repurposing Advantage

Germany limited availability of large land parcels is accelerating interest in floating solar systems. Agricultural zoning restrictions and urban density have made traditional ground-mounted solar expansion increasingly competitive. Floating systems provide an alternative that bypasses land acquisition challenges while leveraging existing artificial water bodies.

Mining Lakes as a Strategic Renewable Asset Base

A defining feature of Germany FPV expansion is the integration of solar installations on former lignite mining lakes. These sites offer large, underutilized water surfaces suitable for utility-scale generation. Government-supported feasibility studies are reinforcing investor confidence in these unconventional deployment zones.

Cost and Lifecycle Performance Constraints

Despite strong growth projections, high installation and maintenance costs remain a constraint. Floating systems require specialized anchoring, corrosion-resistant materials, and ongoing water-based maintenance, which increases total lifecycle cost compared to conventional solar farms. Procurement teams are prioritizing vendors capable of reducing operational expenditure through durable platform design.

Regulatory and Environmental Compliance Pressure

Floating solar projects in Germany must comply with strict environmental and water usage regulations. This includes aquatic ecosystem protection, water quality monitoring, and structural safety requirements. While this creates friction in deployment speed, it also ensures long-term project stability once approved.

Market Opportunities: Where Value Creation Is Emerging

From an investment perspective, Germany floating solar panels market is not driven by volume demand but by strategic infrastructure substitution. Investors are increasingly evaluating FPV systems as part of hybrid renewable portfolios rather than standalone assets.

Manufacturers have an opportunity to focus on modular floating platforms that reduce installation complexity and improve scalability across reservoirs and mining lakes. Suppliers offering corrosion-resistant materials and advanced anchoring systems are likely to gain procurement preference.

Technology companies are exploring digital monitoring systems for water-based solar farms, including predictive maintenance tools and performance optimization software. This is becoming a critical differentiation layer for vendors competing in early-stage tenders.

For utilities and industrial energy buyers, floating solar offers a pathway to expand renewable capacity without competing for land resources, particularly in high-demand industrial zones. Regional players focusing on artificial lake development have a structural advantage in securing early project pipelines.

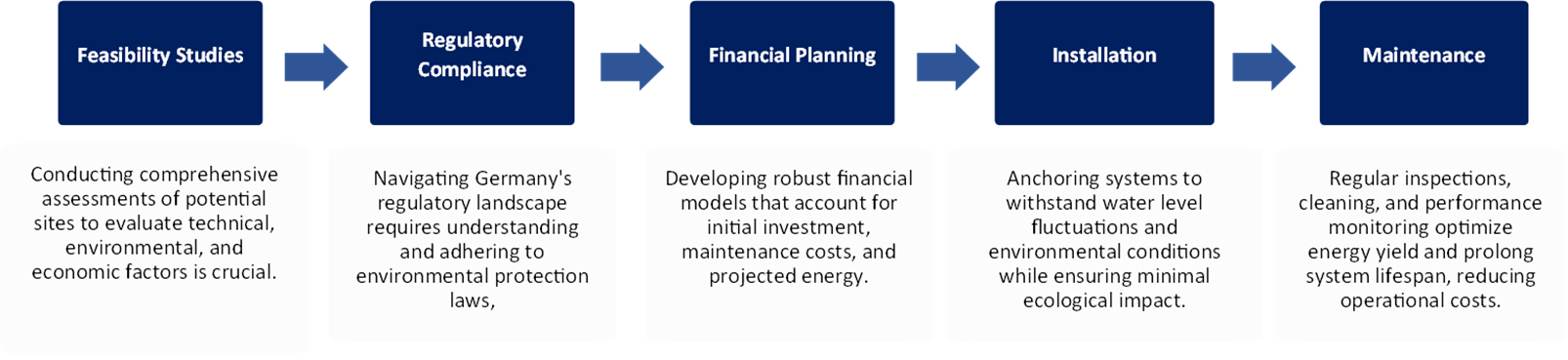

Procurement Analysis for Floating Solar

This report provides a comprehensive analysis of the feasibility studies, regulatory compliance, financial planning, installation, and maintenance. It includes insights into supplier landscapes, cost-benefit considerations, regulatory compliance, and quality assurance measures. Additionally, the report examines procurement challenges, risk mitigation strategies, and best practices for optimizing supply chain efficiency.

Segmentation Analysis: Stationary Systems Lead Early Deployment

Segmented by type (stationary floating solar panels, modular floating systems), by deployment site (reservoirs, artificial mining lakes, industrial ponds), by application (utility-scale power generation, industrial energy supply), and by region.

The stationary floating solar panels segment accounts for more than 50% market share, driven by its structural simplicity and lower operational complexity. These systems are fixed in position, making them suitable for controlled water bodies such as reservoirs and mining lakes where water level variations are predictable.

Industrial users and utility operators prefer stationary systems due to easier regulatory approval pathways and more stable performance characteristics. As Germany expands renewable capacity without increasing land usage, stationary FPV systems are expected to maintain dominance through 2035, although modular systems may gain traction in adaptive water environments.

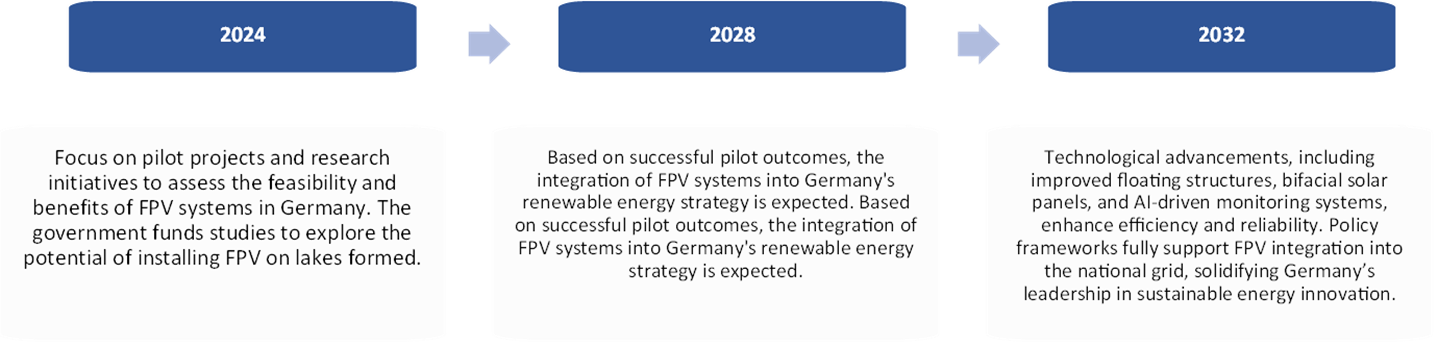

Technological Road Map (2024, 2028, 2032)

The technological road map outlines the phased development and adoption of emerging technologies within a specific market, covering milestones for innovation, commercialization, and large-scale deployment. It typically includes key targets for production capacity, infrastructure expansion, cost reduction, policy support, and sustainability goals over Current, mid-term (4 years), and long-term (8 years) horizons.

Regional Analysis: Germany as a High-Control Renewable Innovation Market

Germany (Core Market)

Germany remains the central hub for floating solar development in Europe, driven by its renewable leadership and structured energy transition policies. The country’s dense solar infrastructure provides integration readiness, while its mining regions offer scalable deployment zones. Government-backed feasibility studies are reinforcing investor confidence in FPV deployment.

Europe (Adjacent Influence Zone)

Neighboring European markets are closely observing Germany FPV adoption model. Countries with similar land constraints and industrial water bodies are evaluating replication potential, particularly for post-mining landscapes and reservoir-based energy systems.

Asia-Pacific (Technology Benchmark Comparison)

Although not a direct competitor in scale within this context, Asia-Pacific provides technological benchmarking for floating solar innovation. Germany adoption trajectory is influenced by global efficiency improvements and cost reduction trends originating from Asian manufacturing ecosystems.

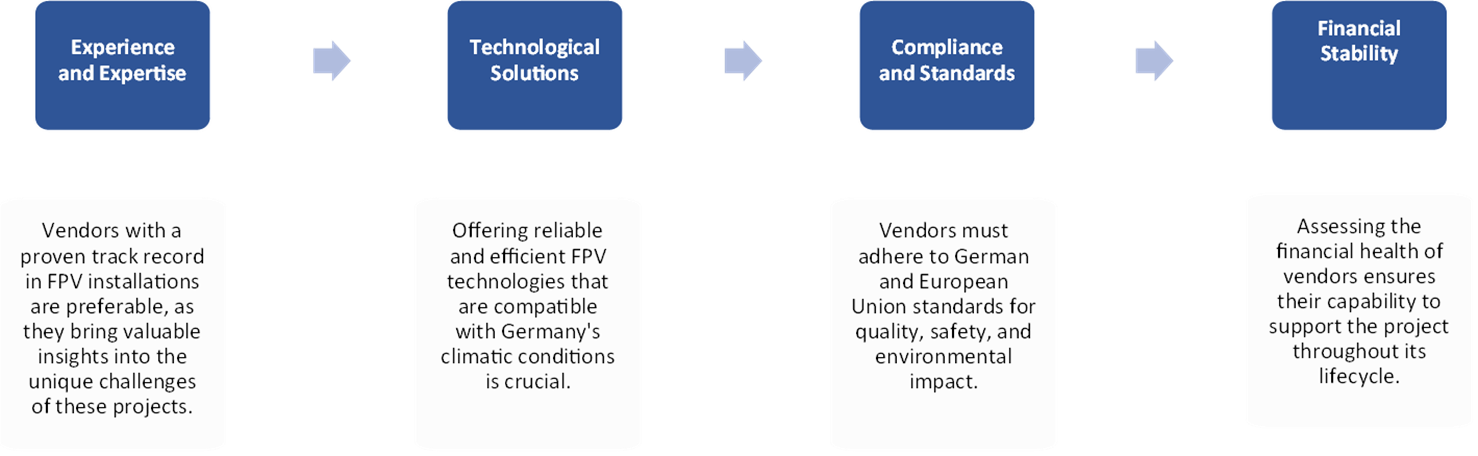

Vendor Selection Criteria for Floating Solar

This report will provide a comprehensive analysis of vendor selection criteria, covering key aspects such as technical expertise, regulatory compliance, financial stability, product reliability, scalability, and after-sales support. It will include insights into best practices for evaluating vendors, ensuring quality assurance, mitigating procurement risks, and optimizing long-term value through strategic partnerships.

Competitive Landscape: Engineering and Compliance Define Market Positioning

The competitive structure of Germany floating solar panels market is moderately consolidated, with key players including BayWa r.e., RWE, and Suntech Deutschland GmbH shaping early market direction.

BayWa r.e. is focusing on renewable project development and integrated energy solutions, positioning itself across both engineering and deployment phases. RWE is leveraging its utility-scale infrastructure expertise to explore large water-based renewable assets, particularly in industrial and post-mining zones. Suntech Deutschland GmbH is contributing through solar module innovation and supply chain integration.

Competitive differentiation is increasingly based on system durability, regulatory compliance capability, and long-term operational efficiency rather than price alone. Companies are investing in R&D to enhance floating platform stability, reduce corrosion risk, and extend system lifespan. Strategic partnerships with water infrastructure operators are becoming a key entry strategy for scaling deployment pipelines.

Recent Developments: Market Formation Phase Activities

- May 2026 – BayWa r.e. expands floating photovoltaic project development across German inland water bodies

BayWa r.e. continued strengthening its floating solar portfolio by advancing utility-scale floating PV installations on quarry lakes and artificial reservoirs in Germany. The company focused on improving system stability, anchoring technologies, and environmental compatibility to support land-efficient renewable expansion. - May 2026 – RWE Renewables accelerates hybrid renewable energy integration including floating solar systems

RWE expanded its renewable energy strategy by integrating floating solar concepts with existing hydro and wind assets, aiming to enhance generation stability and optimize land use efficiency in Germany’s renewable energy transition framework. - April 2026 – Suntech Deutschland GmbH advances high-efficiency photovoltaic modules for floating solar applications

Suntech Deutschland strengthened its supply of corrosion-resistant and high-efficiency PV modules tailored for floating solar installations, focusing on improved moisture resistance, durability, and long-term performance in aquatic environments. - April 2026 – Germany increases regulatory support for floating solar deployment on artificial water bodies

German energy policy developments continued to encourage floating PV adoption on man-made lakes and industrial reservoirs, supporting sustainable energy generation without competing for agricultural or urban land. - March 2026 – BayWa r.e. enhances engineering capabilities for large-scale floating solar infrastructure

BayWa r.e. expanded its technical expertise in mooring systems, floating platform durability, and environmental monitoring to improve efficiency and ecological safety of floating solar projects in Germany. - March 2026 – RWE explores multi-technology renewable hubs integrating floating solar with energy storage

RWE advanced feasibility studies for combining floating PV systems with battery storage and other renewable sources, supporting Germany’s broader grid flexibility and decarbonization goals.

Impact Analysis: Regulation and Infrastructure Readiness

Regulatory frameworks in Germany significantly influence project approval timelines. Environmental assessments and water-use permissions remain critical bottlenecks in early-stage deployment. However, once approved, projects benefit from strong policy alignment with national renewable energy targets.

Supply chain dependency on specialized floating infrastructure components creates procurement complexity, particularly for anchoring systems and corrosion-resistant materials. This is pushing companies to localize supply chains and form long-term vendor partnerships to mitigate cost volatility.

Report Benefits

This report provides actionable insights for manufacturers evaluating product adaptation strategies, investors assessing early-stage renewable infrastructure opportunities, and utilities planning land-constrained energy expansion. It also supports procurement teams in vendor evaluation, cost benchmarking, and lifecycle risk assessment, while helping technology providers identify integration opportunities in monitoring and maintenance systems.

Why Choose DataM?

- Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares, and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Report Updates: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience

- Energy infrastructure investors

- solar technology manufacturers

- utility companies

- EPC contractors

- government energy planners

- procurement heads

- renewable energy consultants

- industrial energy buyers