Gene Editing Delivery Technologies Market Overview

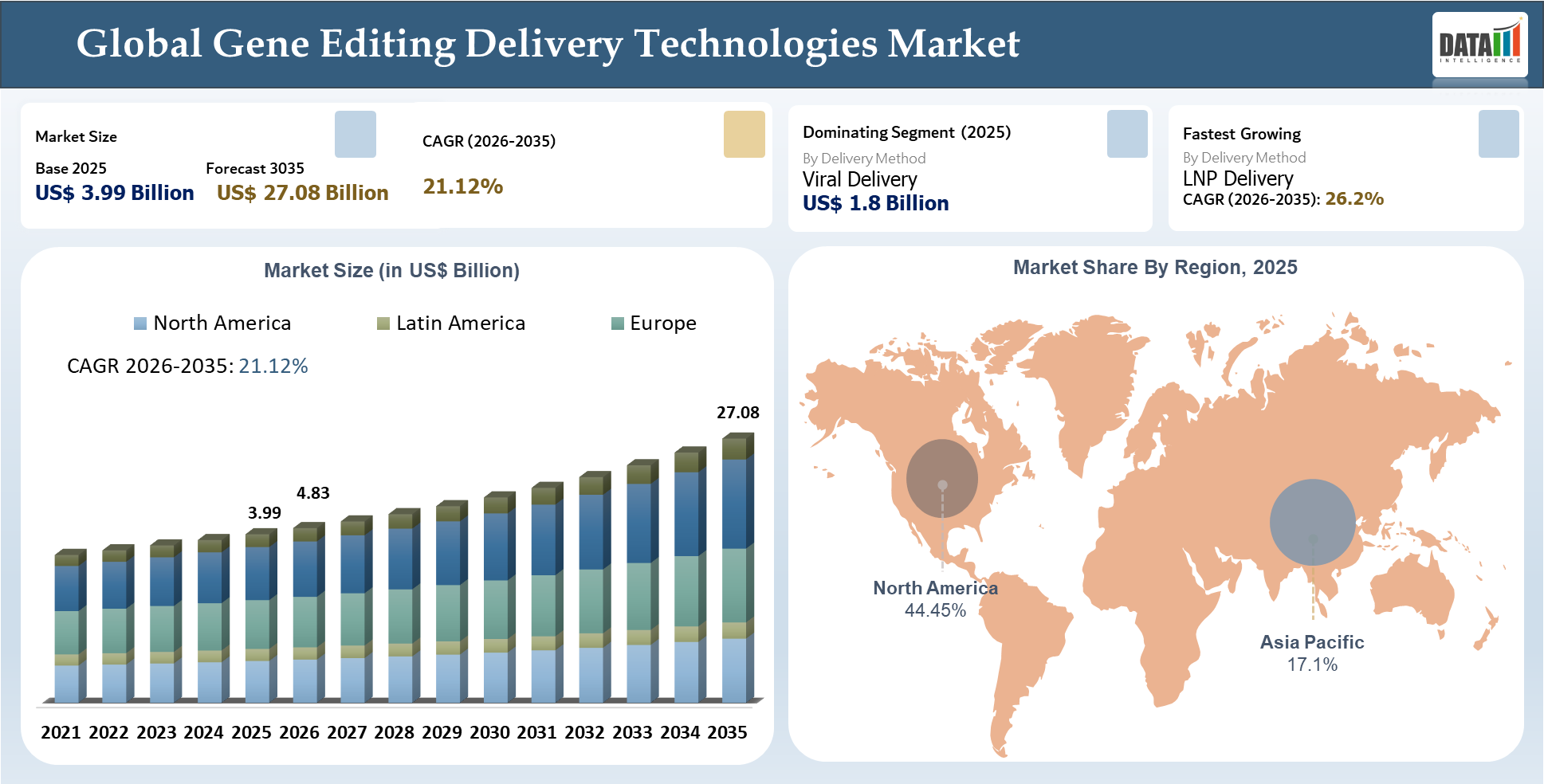

The Global Gene Editing Delivery Technologies Market stood at US$ 3.99 billion in 2025 and is projected to hit US$ 27.08 billion by 2035, marking a CAGR of 21.12% through the forecast years 2026–2035. Market growth is being driven by an exponential increase in the adoption of delivery systems, which have emerged to be among the most important elements in gene editing's success in research, translational, and therapeutic settings. Whereas gene editing technologies like CRISPR, base editing, and prime editing continue to evolve, commercial success will now be increasingly tied to the safe, effective, and precise delivery of payloads to targeted cells/tissues.

Market dynamics are currently being influenced by the continuous development of viral delivery technologies, lipid nanoparticles delivery methods, and non-viral delivery systems, all of which bring their unique strengths when it comes to target specificity, scalability, ease of workflow compatibility, and regulatory acceptance. Market demand is currently being driven by increasing engagement in gene therapies, engineering of cell therapies, in vivo editing, and ex vivo modifications, whereas manufacturing capabilities, regulatory alignment, and tissue-specific delivery emerge as important competitive factors in the industry.

AI Impact Analysis

AI technology is gradually having an impact on this market with its commercial value due to the improvements it provides in terms of design, optimization, and scale of production of the delivery systems. Companies now increasingly apply AI to enhance the vector engineering process, optimization of LNP formulation screening, payload optimization, and prediction of delivery for particular targets.

AI is also contributing significantly in terms of process development and production of LNPs. Using AI, suppliers gain the ability to analyze formulation dynamics, process consistency, quality management, and shorten the development period. The commercial benefit of this approach for potential buyers comes from faster optimization of their products and a minimized need for testing.

Another benefit that suppliers may have with the help of AI technology would be the ability to find the best application and make decisions regarding the development of LNPs.

Gene Editing Delivery Technologies Market Key Takeaways

- Delivery Method continues to be the most commercially relevant framework for analysis, as it reveals how customers divide their budgets, assess vendor capabilities, and weigh performance considerations within the gene editing delivery technologies industry.

- The demand trend is now favoring products that can demonstrate quantifiable value through Viral Delivery and LNP Delivery approaches, rather than just leveraging platform technology arguments.

- The competitive lead is being established by North America, where the USA and Canada influence product development, sourcing strategies, and go-to-market initiatives.

- Winning suppliers leverage a combination of product breadth, domain expertise, and ecosystem partners to protect price and accelerate purchasing processes.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 3.99 Billion | |

| 2035 Projected Market Size | US$ 27.08 Billion | |

| CAGR (2026-2035) | 21.12% | |

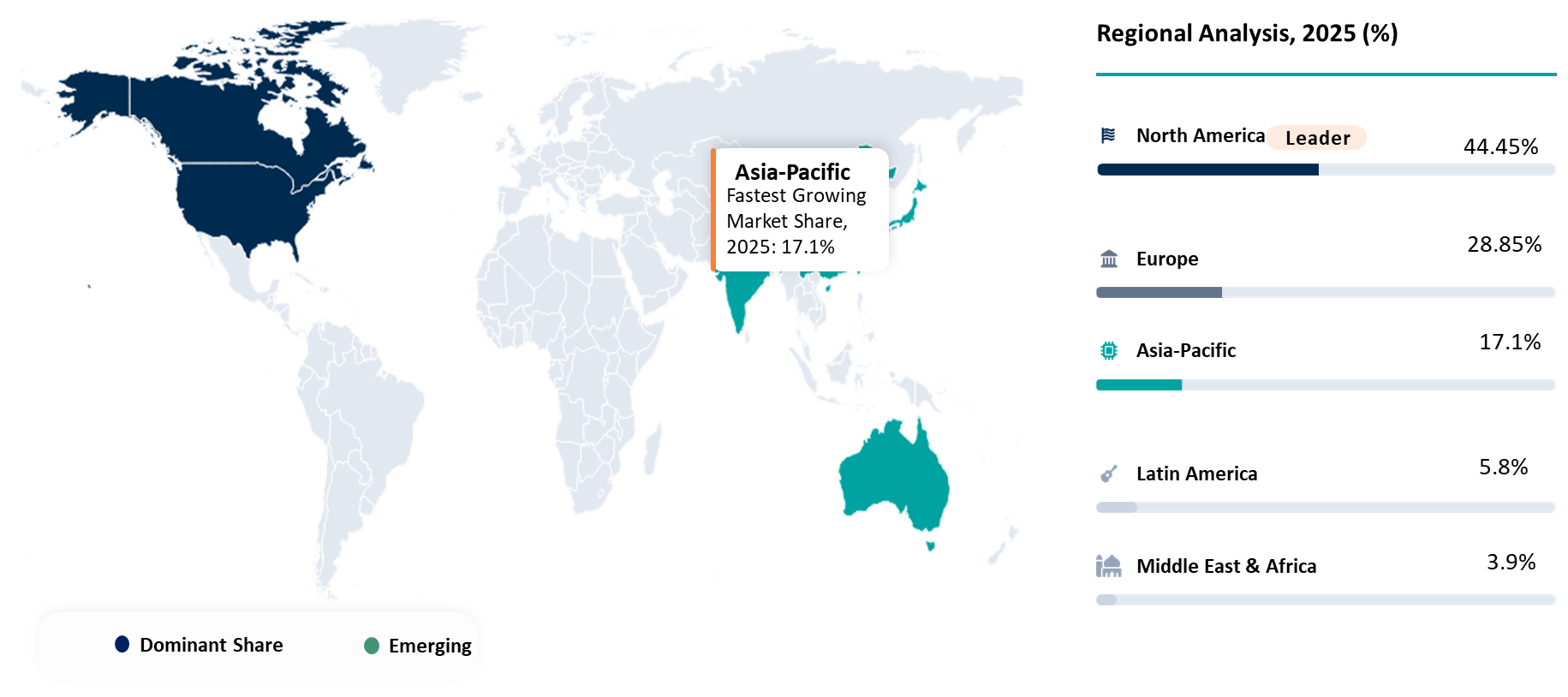

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Delivery Method | Viral Delivery, LNP Delivery, Electroporation, Polymeric Nanoparticles, and Physical Delivery Methods | |

| By Editing Modality | CRISPR Cas Systems, Base Editing, Prime Editing, TALEN, and ZFN | |

| By Target Area | Oncology, Rare Disease, Immunology, Liver Diseases, and Hematology | |

| By Application | Ex Vivo Cell Engineering, In Vivo Therapeutics, Research Use, and Agrigenomics | |

| By End-User | Biopharma, Academic Research, CDMO, and Government and Non-Profit Research | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

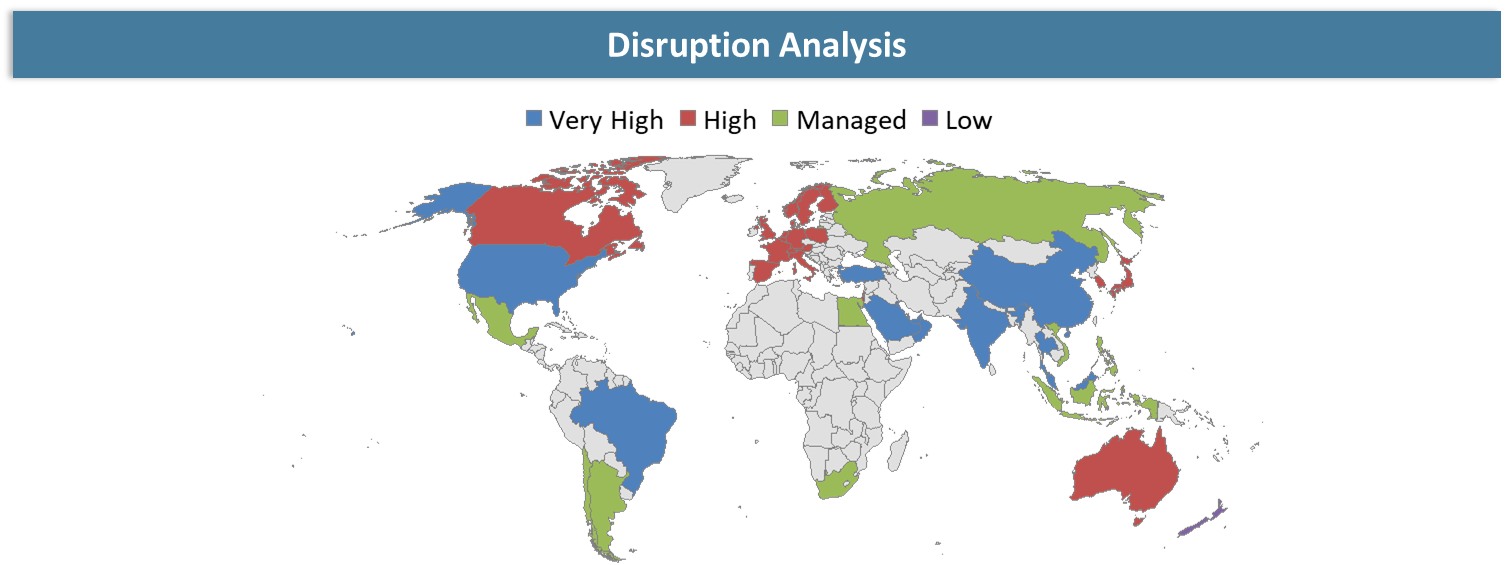

Disruption Analysis

Shift from Technical Differentiation to Commercial Execution, Integration Readiness, and Outcome Accountability

The key disruption in the gene editing delivery technologies market is not a product launch but rather a shift in the dynamics of the market from generic features-based competition to operating value metrics. In a world where customers expect to know how quickly and efficiently the product can be integrated within their existing architecture and whether it can justify its costs, vendors cannot afford to depend on specifications sheets or lofty technical terminology.

A second disruption in this market is occurring in the commercial space, whereby channel models, integration partnerships, and offer bundles are shifting customer purchasing dynamics. In many cases, the vendor that is able to control the process around the core product is able to win an opportunity despite competitors having equivalent technology.

The third disruption occurring within the gene editing delivery technologies market is the increase in customer demands for resilience and accountability. Today, customers want to know not only where the product comes from, where local support is available, and how resilient the product is during times of crisis, but they also seek post-deployment outcome metrics.

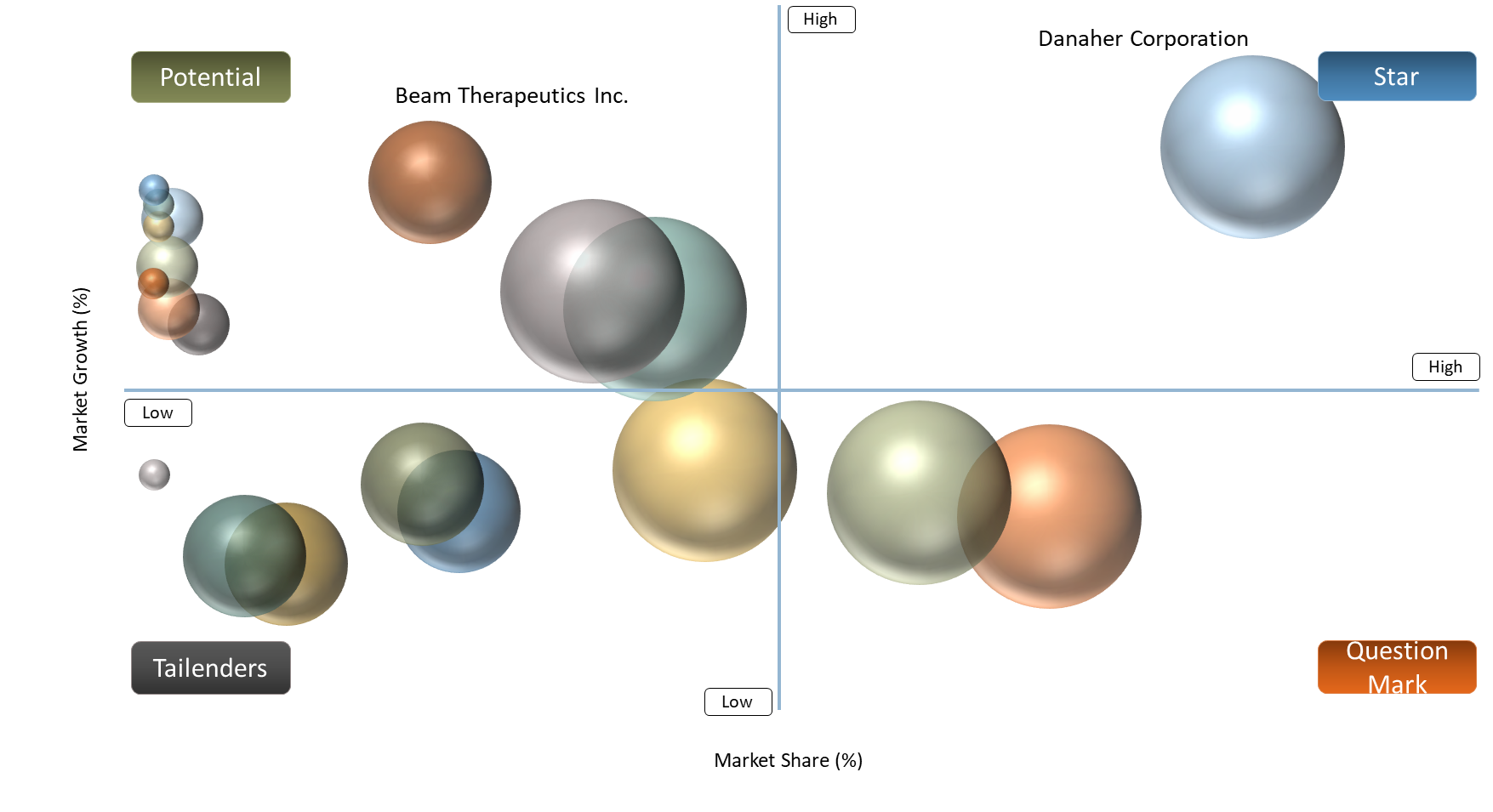

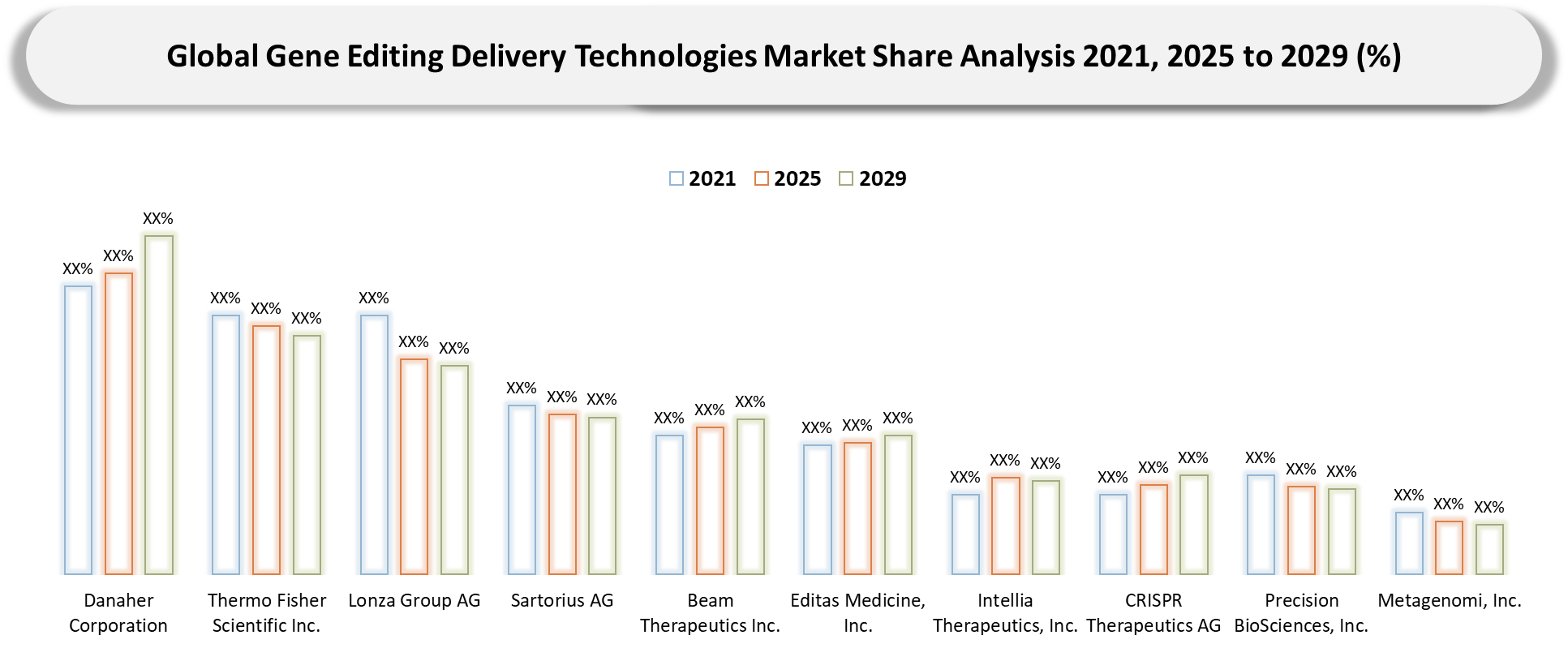

BCG Matrix: Company Evaluation

In terms of the BCG matrix, Stars would be represented by the organizations with robust market momentum and ecosystem control. The typical examples would be Danaher Corporation, Thermo Fisher Scientific Inc., and Lonza Group AG if they possess platform depth, credible manufacturing processes, extensive distribution channels, and integration of solutions for customers’ workflows. Such companies benefit not only from their size but also from setting procurement expectations and increasing their share through multi-point accounts.

Cash Cows may refer to the organizations with a large installed base and well-established relations with their customers and commercial coverage. Despite having a smaller growth rate compared to rapidly growing competitors, Cash Cows defend their margins with deep service offerings, application know-how, process familiarity, and switching costs rather than relying on disruptive approaches.

The Question Mark category would consist of new specialists and adjacent competitors that target narrow markets with certain delivery niches, for instance, viral vectors or LNP delivery. If these organizations outperform others in delivery efficiency, safety, and application fit, they can have high growth potential. However, they require improved scale, commercial alliances, and regulatory/user acceptance.

Market Dynamics

Shift Toward Measurable Operating Value and Application-Specific Buying Criteria

One of the most stable drivers of market growth is the shift in buyer behavior from the general interest in technology to focused purchases with concrete improvements in metrics as the basis for evaluation. Buyers are less concerned about evaluating the delivery platform in isolation and are more interested in solutions that would increase throughput, improve editing efficiency, decrease TAT, and minimize operational complexity. The trend favors companies that have a deep understanding of buyers' processes and can deliver results.

Another growth driver is the change in procurement decision-making logic. The choice of vendor is less dependent on technical expertise and is determined by other criteria such as delivery complexity, integration complexity, compliance, and post-implementation support. This is driving investments in more scalable and validated delivery segments such as viral and LNP deliveries.

In addition to this, expansion into markets can also be attributed to the increasing maturity of ecosystems. Complementary offerings, in terms of manufacturing support, implementation partners, and enabler tools, have minimized the risks associated with adoption. As a result of the evolution of the ecosystem, investments can now be more easily justified, allowing the market to grow even larger.

Lastly, user requirements are increasingly trending towards integration-friendly solutions. In this context, users are no longer satisfied with generic platforms that would need customization. Rather, the preference leans towards delivery technologies that fit seamlessly within their infrastructures and scale easily.

Integration Burden, Compliance Friction, and Longer Enterprise Decision Cycles

The principal constraint in this market is the fact that demand is not always converted into rapid adoption. There are many reasons why many consumers may find themselves unable to use the product quickly despite having a favorable business case for doing so. This usually involves factors such as the level of difficulty involved in integrating a delivery platform into the existing workflow of research, production, or clinical operations without generating additional operational work.

This is especially true when a particular innovation is dependent on factors such as regulatory controls, capital expenditures, legacy systems, and multi-party approvals. When this is the case, the decision-making process will involve not just technical considerations but also those relating to quality, compliance, procurement, operations, and management. As a consequence, any early interest in piloting the product might take more time before generating significant revenues.

Segmentation Analysis

The global Gene Editing Delivery Technologies market is segmented based on delivery method, editing modality, target area, application, end-user, and region.

Delivery Method Is Where Market Economics Begin to Diverge

Delivery Method becomes the most suitable lens to analyze the dynamics of this market since it is an indication of what buyers perceive when considering practical tradeoffs during procurement instead of relying on overall product stories. Budget planning, pricing influence, supplier differentiation, and deployment risks become much clearer through this lens, which increases its feasibility in analyzing and estimating this market.

In particular, within Delivery Method, Viral Delivery and LNP Delivery can be considered the two most commercially viable segments. First, Viral Delivery remains relevant due to the compatibility of this technology with current work processes, infrastructure, and competencies. Second, by leveraging adjacent products and services, Viral Delivery can significantly increase its commercial viability due to reduced risks and uncertainty. Third, LNP Delivery becomes increasingly important in high-end and mission-critical use cases, where buyers need control, flexibility, and integration into existing workflows. Although this approach requires more time for adoption, it promises more opportunities to deliver account-level value and establish relationships as strategic partners.

Geographical Penetration

North America Leading Gene Editing Delivery Technologies Advancement Through Innovation Density and Commercial Execution Leadership

North America is emerging as the most crucial geography in this market, not only for its significant demand but also for how intensely it is testing the viability of delivery platforms in practice. Market readiness is being established in North America not only based on criteria such as delivery efficiency, manufacturability, regulation, workflow integration, and repeatability, but also on the extent to which suppliers can prove their technology in development and commercial settings; provide tangible return on investment; and integrate within broader processes. It is clear why North America is an especially challenging and revealing geography for suppliers, as technologies validated in North American markets can often have a greater reputation elsewhere. North America boasts an unusually rich collection of biotech firms, translational centers, advanced therapies, and specialist manufacturers. For all of these reasons, North America provides one of the best glimpses into future revenues, scalable delivery platforms, and competitive supplier advantage.

U.S. Gene Editing Delivery Technologies Market Trends

The United States needs specific attention due to the role it plays in driving market evolution through a combination of high levels of demand intensity, industry depth, regulation, and sophisticated buyer behaviors. The United States is particularly unique in terms of the way that it demonstrates whether or not certain suppliers have gone past the stage of merely presenting technology positioning and are now competing on execution. Buyers are now assessing delivery solutions not just based on the science behind it, but rather by their ability to fit into development pipelines, meet regulatory criteria, align with manufacturing paths, and minimize scale-up hurdles. The implications of this are significant since it alters the nature of competition from broad-based technological messaging to tangible commercial results. Additionally, the United States has one of the most robust ecosystems when it comes to bio-innovators, cell and gene therapy companies, CDMOs, academic medical centers, and investments in the biopharma space. Suppliers who have the ability to collaborate on implementation, customer service, manufacturing capabilities, and ecosystem collaboration outpace those who simply promote their products.

Canada Gene Editing Delivery Technologies Market Outlook

Canada is gaining importance due to its strategic significance in the regional setting. It is important not for the size of its market but because of its quality research, translational platform, expert niche workforce, and innovative collaboration setting. Canada presents a good example of the regions that might be used to identify future niches, which would benefit from scientific credibility, institutional involvement, and technological advancement. In particular, Canada's expertise in cellular therapies, bioprocessing solutions, and academic-commercial collaborations makes the region ideal for the development and validation of next-generation delivery technologies. This example helps show how policy, funding, and expertise could be used by suppliers in their attempts to establish a premium position before expanding to other locations. Hence, Canada represents a strategic rather than a mass market in terms of gene editing delivery solutions.

Competitive Landscape

- Competition within this market will increasingly be driven by a dichotomy between larger, platform-focused vendors and more specialized solutions vendors. Larger organizations such as Danaher Corporation, Thermo Fisher Scientific Inc., and Lonza Group AG have the ability to set the expectations of the category based on breadth, footprint, manufacturing strength, and multi-point access to customers. On the other hand, smaller specialist vendors would likely compete on aspects such as superior application fit, greater technical expertise, implementation speed, or applicability within delivery niches. Over time, competitive advantage in this market will not only come from the technical superiority of products themselves but also from their ability to offer credible technology alongside comprehensive supporting services.

- Positioning in this market will increasingly depend upon how effective vendors are at managing the complete customer experience rather than just the quality of their products alone. Apart from the technical quality of offerings, vendors' products will also need to score high on criteria such as onboarding ease, integration capabilities, process fit, application support, and service depth throughout the entire lifecycle. Vendors able to develop strong footprints within high-growth segments such as Viral Delivery and LNP Delivery would be well-positioned.

Key Developments

- April 2026: CRISPR Therapeutics AG reaffirmed progress in its proprietary LNP delivery platform for in vivo liver editing, highlighting programs including CTX310, CTX340, and CTX321 in its business update.

- April 2026: Beam Therapeutics, Inc. announced publication of BEACON Phase 1/2 data in The New England Journal of Medicine, reinforcing the company’s position as an integrated gene editing, delivery, and manufacturing platform player.

- March 2026: Cytiva and the San Raffaele Telethon Institute for Gene Therapy launched a new Danaher Beacon collaboration to advance next-generation medicine platforms, reflecting deeper ecosystem integration around advanced therapies.

- November 2025: CRISPR Therapeutics AG reported positive Phase 1 clinical data for CTX310, a program supported by its proprietary LNP delivery platform for liver-directed gene editing.

- July 2025: Aldevron LLC opened a new Discovery Center in Waltham, Massachusetts, expanding capabilities in DNA, RNA, molecular biology, gene editing, and mRNA analytics for advanced therapy customers.

- May 2025: Aldevron LLC and Integrated DNA Technologies manufactured the world’s first personalized mRNA-based CRISPR therapy, demonstrating how delivery-enabling manufacturing infrastructure is becoming a strategic differentiator.

- May 2025: Metagenomi, Inc. presented ASGCT data showing extrahepatic in vivo gene editing with all-in-one delivery to the central nervous system, a notable step beyond liver-focused delivery approaches.

- March 2025: Prime Medicine, Inc. unveiled its alpha-1 antitrypsin deficiency program built on a universal liver LNP platform, underscoring continued commercial momentum behind non-viral delivery strategies.

- March 2025: Metagenomi, Inc. announced a Nature Communications publication describing large targeted genomic integration supported by a streamlined all-in-one mRNA delivery approach for in vivo editing.

- March 2025: AstraZeneca PLC agreed to acquire EsoBiotec, adding the ENaBL in vivo lentiviral delivery platform to strengthen its cell therapy and genomic medicine capabilities.

- October 2024: Prime Medicine, Inc. presented in vivo proof-of-concept data highlighting the breadth of its universal liver LNP platform across multiple prime editing programs.

- June 2024: Intellia Therapeutics, Inc. reported the first clinical proof-of-concept data for redosing an investigational LNP-based in vivo CRISPR therapy, an important milestone for repeat dosing potential.

- February 2024: Intellia Therapeutics, Inc. and ReCode Therapeutics entered a strategic collaboration combining Intellia’s editing platform with ReCode’s SORT LNP technology to target cystic fibrosis in the lung.

White Space Opportunities

As per DataM, one of the most visible white space opportunities in gene editing delivery technologies is one that goes beyond the apparent delivery programs. The emphasis of many providers is on tried-and-tested applications, while there is unmet demand in more niche, higher-friction applications where the customers value reliable delivery, accurate tissue targeting, and validation help. Secondly, an unmet demand is available in the commercial packaging of these solutions, where providers who make things easier for their clients through onboarding, regulatory alignment, and application enablement will be able to grow faster compared to others, depending solely on their technology's robustness. There are other white space opportunities available among mid-sized biotech and research institutions that continue to go unexplored despite having consistent demand.

DMI Opinion

As per DataM, the most significant challenge in gene editing delivery technologies is not whether there is demand for the product, but what suppliers have the capability to translate interest in the technology into repeatable adoption success without raising delivery complexity faster than value creation. The market rewards suppliers who make the adoption process operationally realistic.

In reality, delivery performance, delivery to desired tissues, production scaling capability, and regulatory compliance readiness become equally relevant criteria along with the efficiency of editing itself. Customers do care more about workflow integration, validation support, and protocol alignment than technology itself. Competitive advantages arise from suppliers' ability to reduce friction for customers throughout their entire journey to adopting gene editing. It means the market is shifting towards more focused opportunities where delivery performance becomes key.

In fact, many players in the gene editing market continue to rely too much on general technology hype and fail to understand customer adoption mechanics. Therefore, suppliers capable of delivering meaningful value to customers and translating technological advances into tangible results and adoption success are likely to win in the future market environment.

Why Choose DataM?

- Technology Innovation for Delivery Technologies: Discusses innovations within the delivery of gene editing technologies, focusing on viral vectors, LNP systems, non-viral systems, electroporation technology, and more.

- Performance in Platform Technology & Market Positioning: Assesses the performance of competing companies in actual scenarios for the use of gene therapies, cell therapies, in vivo gene editing, and ex vivo gene editing. The report assesses efficiency in delivery, targeting ability, manufacturing capabilities, workflow suitability, regulatory compliance, and scalability to understand how market leaders distinguish themselves from others in this space.

- Real-World Evidence: Identifies actual use cases where delivery technologies for gene editing are applied in clinical applications, translational research, and advanced therapies.

- Industry Developments & Market News: Monitors key industry trends that include launches, initiatives for deliveries, manufacturing capacity upgrades, regulatory advancements, and investment movements within important markets, such as North America, Asia-Pacific, China, and Europe.

- Business Strategies: Examines competitive business moves that are being undertaken by key players to increase their presence in terms of platform variety, delivery, partnerships, manufacturing capacities, and ecosystem advantages.

- Product Pricing & Distribution: Provides an understanding of value generation in research-based, clinical-level, and advanced delivery platforms, along with the review of commercial and regional access strategies, as well as service partnerships.

- Market Penetration & Business Strategy: Outlines market penetration strategies through the examination of opportunities within untapped applications, emerging areas, and regional markets, as well as business strategies for scaling up through manufacturing readiness and application support.

Target Audience 2026

- Product strategy teams

- Corporate strategy and market intelligence teams

- Business development leaders

- Sales and channel leaders

- Investors and private equity firms

- Procurement and sourcing teams

- Technology and operations leaders

- Consulting and advisory teams.