Float Glass for Photovoltaics Market Overview

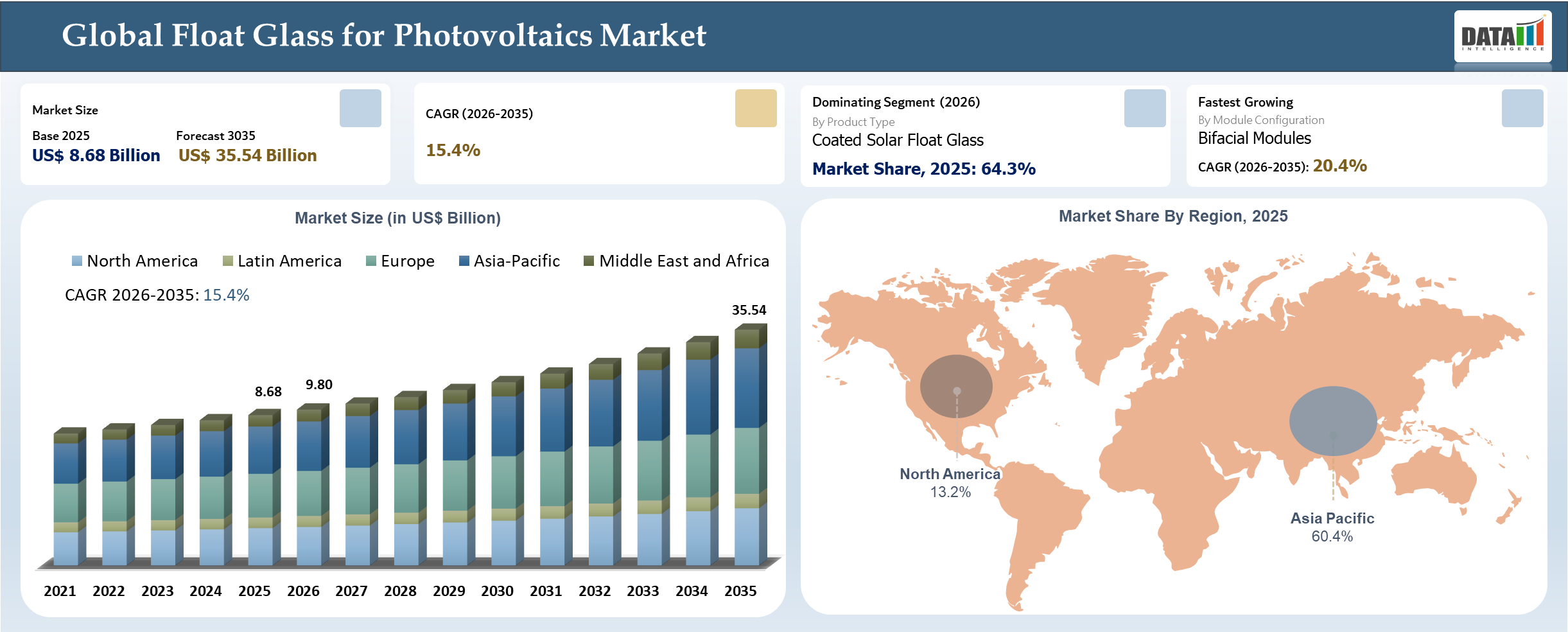

The global float glass for photovoltaics market reached US$ 8.68 billion in 2025 and is expected to reach US$ 35.54 billion by 2035, growing with a CAGR of 15.4% during the forecast period 2026-2035. Growing popularity of bifacial modules, as well as the use of dual-module configurations, is driving an increase in glass intensity per kilowatt of installed capacity, making the use of solar float glass more strategically significant in PV systems. Furthermore, there is an increasing trend towards diversified regional supply chains through the emergence of new manufacturing capabilities outside the existing centers. Another trend seen is the increased focus on sustainable practices like using recycled materials as well as more efficient production techniques. Information from both the International Energy Agency (IEA) and International Renewable Energy Agency (IRENA) suggests that solar expansion policies will drive demand growth.

Float Glass for Photovoltaics Industry Trends and Strategic Insights

- Bifacial and glass-glass module adoption has increased the utilization of glass on a per-installed power basis, generating a continuous lift in demand independent of additional solar installation growth.

- Coated low-iron float glass has become the go-to choice for photovoltaic module manufacturing, where differences arise based on efficiency, durability and overall performance.

- Manufacturing remains highly concentrated in the Asia Pacific region, especially China, which affects price structure. Expansion in other markets, including North America and India, is encouraging diversity within the value chain.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 8.68 Billion | |

| 2035 Projected Market Size | US$ 35.54 Billion | |

| CAGR (2026-2035) | 15.4% | |

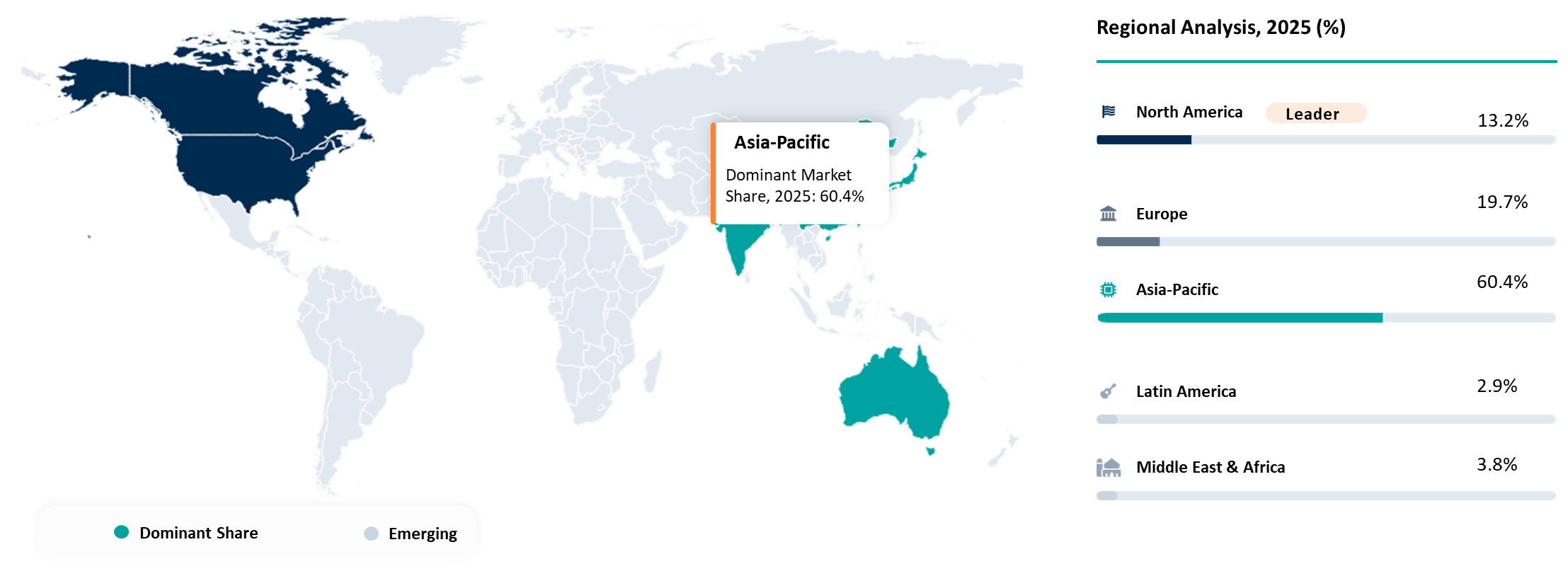

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | North America | |

| By Product Type | Uncoated Solar Float Glass and Coated Solar Float Glass | |

| By Module Configuration | Single Glass Modules, Dual Glass Modules and Bifacial Modules | |

| By Thickness | Up to 2 mm, 2-3.2 mm and Above 3.2 mm | |

| By Solar Technology | Crystalline Silicon Modules and Thin-Film Modules | |

| By End-Use Installation | Utility-Scale Solar, Commercial & Industrial (C&I), Residential and Building-Integrated Photovoltaics (BIPV) | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

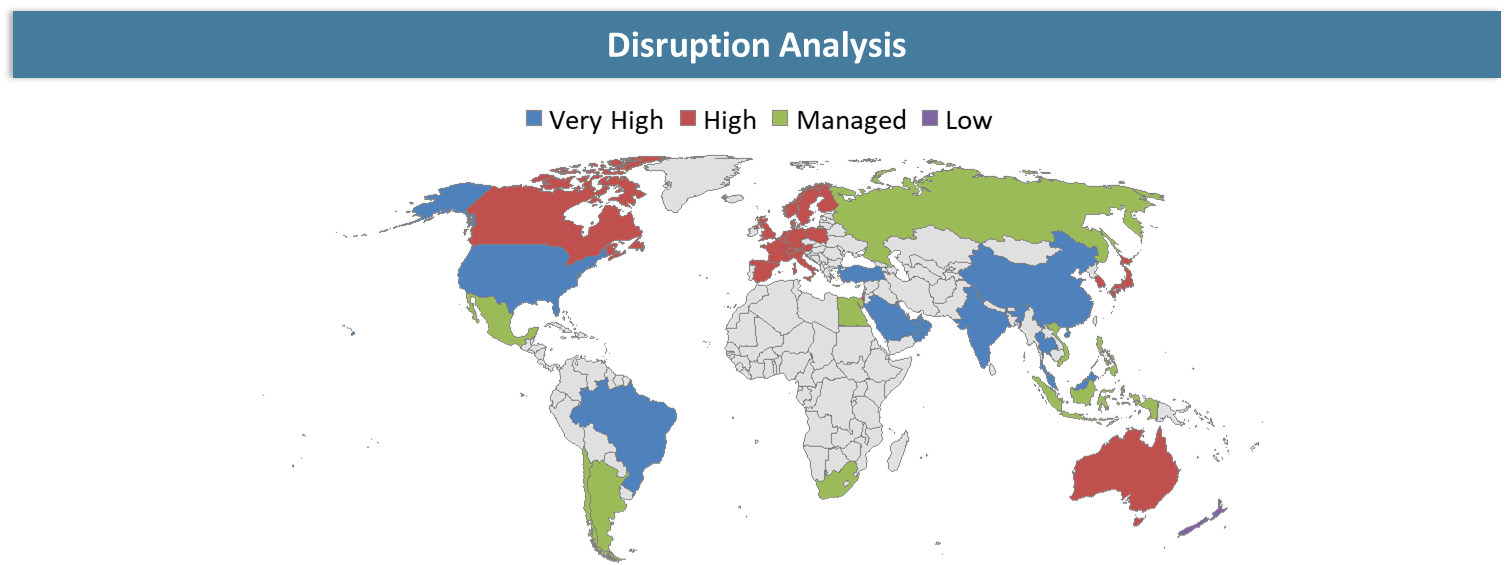

Disruption Analysis

Regional Supply Chain Diversification Transforming Photovoltaic Float Glass Market Dynamics

The production of photovoltaic float glass on a global level has been traditionally centered in Asia-Pacific, especially in China, where there are major players like Xinyi Solar Holdings and Flat Glass Group utilizing highly efficient and volumetric float furnaces. The concentration of production has helped achieve cost efficiency and pricing benefits but also made the region dependent on other geographical areas, especially North America and Europe, making the industry susceptible to various risks.

The emergence of regional supply chain diversification is due to various policy benefits and the requirement of supply chain security. Investment decisions from companies like Vitro Corporation in North America and Gold Plus Glass Industry in India are a reflection of an industry trend towards establishing manufacturing capacities within a particular region, which leads to a shifting pattern of production and the reduction of dependency on imported goods.

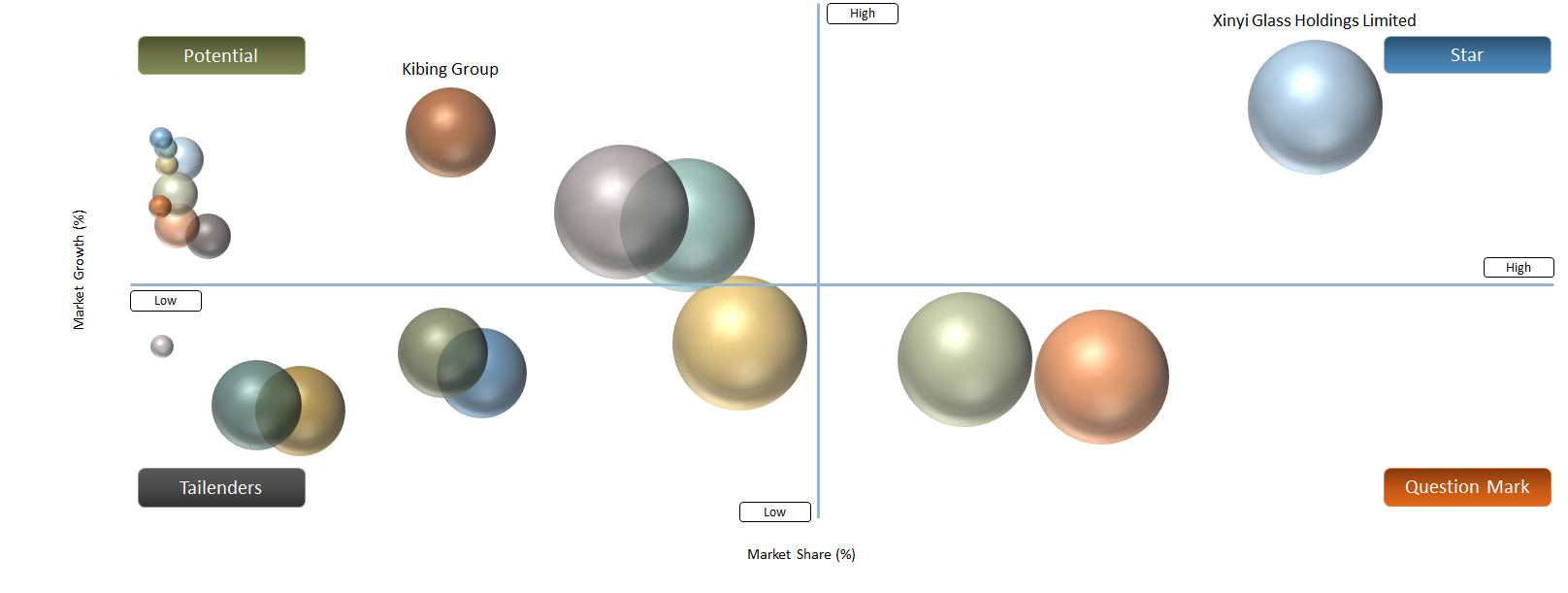

BCG Matrix: Company Evaluation

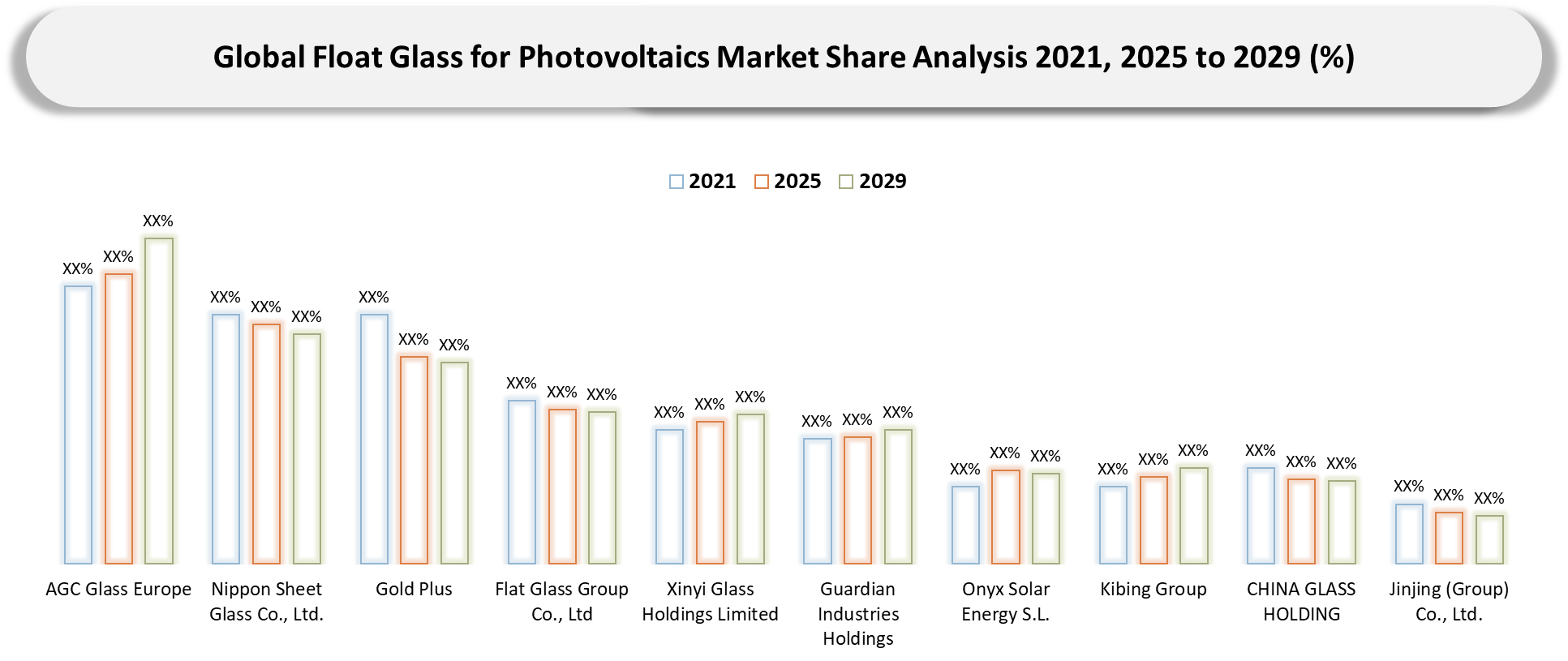

Flat Glass Group and Xinyi Glass Holdings (through Xinyi Solar) will be identified as Stars based on their leadership in photovoltaic glass capacity along with integration into module makers. Jinjing Group will be categorized as a Question Mark due to growing involvement in photovoltaic glass production with possibilities for future growth. Companies like Gold Plus Glass Industry, Kibing Group and China Glass Holding will fall under Potential companies due to ongoing expansions and regional exposure.

AGC Glass Europe, Nippon Sheet Glass and Guardian Industries Holdings are some diversified glass companies that are listed as Tailenders because they do not specialize in photovoltaic glass. This category also includes Onyx Solar because of its specialized business model focusing on BIPV. These classifications highlight the industry structure where dominance is seen among large players while emerging regional competitors seek growth through expansion of their capacities.

Market Dynamics

Glass Intensity Increase Driven by Module Architecture Shift

Glass intensity in photovoltaic modules is increasing due to a structural shift in material composition and module design, where glass is no longer a passive protective layer but a dominant material component. Industry data indicates that glass already accounts for 65-75% of total module weight and the transition toward dual-glass configurations is further increasing material usage per unit of capacity. At the system level, this translates into a significant scaling effect, with approximately 70,000 tonnes of solar glass required per GW of installed capacity, making glass demand highly sensitive to both installation volumes and module architecture choices. It is elevating glass from a secondary input to a cost-critical and volume-defining component, with recent industry analysis showing that glass now represents one of the largest contributors to overall module cost, comparable to polysilicon.

Furnace Economics and Inflexible Capacity Cycles

The manufacture of float glass is fundamentally limited by furnace economics since the furnaces have to run nonstop for 8 to 10 years before each shutdown and the process involves considerable capital outlay to construct, maintain and refurbish them. Once a furnace becomes operational, there will be heavy losses and technical difficulties if its rate of production is lowered. The supply situation is thus inherently inflexible and output remains fairly constant regardless of variations in demand.

As a consequence, there are clear capacity cycle imbalances, especially within the photovoltaic glass market segment, where growth in demand is uneven from one region and time period to another. In instances of rapid capacity build-up, especially where concentration is high, the market can have more supply than demand, thus causing pricing pressure and profit margin reduction. On the other hand, when there is sudden growth in demand, the supply cannot increase instantly because of the time required for constructing furnaces.

Segment Analysis

The global float glass for photovoltaics market is segmented based on product type, module configuration, thickness, solar technology, end-use installation and region.

Coated Solar Float Glass Driving Market Growth Through Advanced Surface Technologies

Anti-reflective coating on solar float glass plays a vital role in the determination of performance specifications for photovoltaic modules due to efficiency enhancement being an important criterion for acquisition. This type of coating is highly recommended as the most popular form of coating in utility-scale photovoltaics, given its high light-transmitting capacity and power production. Simultaneously, anti-soiling coating has been gaining momentum in dusty regions to minimize the need for cleaning and ensure energy production.

Advancements in coating technologies are enabling manufacturers such as Xinyi Solar Holdings and Flat Glass Group to deliver application-specific solutions tailored to environmental conditions and module design requirements. The shift toward performance-driven glass solutions is strengthening pricing power and reinforcing coated solar float glass as a key contributor to both efficiency gains and revenue growth within the photovoltaic value chain.

Geographical Penetration

Asia-Pacific Strengthening Global Leadership Through Integrated PV Glass Supply Chains

Asia-Pacific maintains its dominance in the float glass for PV applications due to its significant manufacturing capacity and integration within the entire solar industry value chain, which contributes to the ability of Asia-Pacific to provide cost-effective ecosystems for production and proximity to important centers for module manufacturing, ensuring an efficient supply of solar grade float glass at reasonable prices.

Continued investments in terms of growth in capacity and technology have made it easier for the region to cater to increasing demands from across the globe. An increased emphasis on manufacturing efficient products along with compatibility with the evolving requirements of modules is making Asia-Pacific the key base for PV Glass.

China Reinforces Market Dominance Through Scale Efficiency and Export-Oriented Supply

China’s leadership is underpinned by large-format float furnaces dedicated to photovoltaic glass and strong backward-forward integration across the solar value chain. Companies such as Xinyi Solar Holdings and Flat Glass Group operate at scale, enabling lower per-unit production costs and consistent supply to global module manufacturers. High domestic installation volumes further support furnace utilization, stabilizing production economics.

With enhancements in coatings technology and thinning of the glass substrate, Chinese companies are able to satisfy rising standards for module efficiency. The strengths of China as a low-cost producer, a technologically advanced entity and an exporter give it substantial power over pricing and supply conditions in the PV glass market.

India Advancing Toward Self-Reliance Through Targeted Capacity Expansion

India is moving towards becoming an exporter from a net importer in terms of PV float glass. It is due to the localization policies and addition of solar capacities in India. The visibility of module manufacturing capacity is driving a stable demand scenario, which is important for maintaining the utilisation of the float furnaces. Incentive structures like PLI (Production Linked Incentives) and Safeguard Duties are driving value chain localization and decreasing the import dependence on solar glass.

The capacity expansion by companies like Gold Plus Glass Industry represents a move towards an integrated production process for solar components, whereby resources are allocated towards the manufacture of low-iron glass and its further processing. While there is much to be done to match global players in terms of technological capability and scale of operations, India has been steadily developing expertise in the coated and high-quality glass markets. The country stands to become a cost-effective secondary market with export prospects in the future.

Competitive Landscape

- The market for float glass used in solar panels has a high concentration in terms of competition, with companies like Xinyi Solar Holdings and Flat Glass Group leading in the industry. The advantage of these companies lies in their exclusive PV glass production, integration with module producers and cost benefits due to their scale, which enables them to control prices and gain supply contracts for a long period of time. The rivalry among these companies revolves around the capacity of furnaces and coatings in accordance with modules.

- The market is shifting towards technology distinction and regional diversity, as players emphasize the production of high transmittance glass coating and specialized applications. Players with diversified products, like AGC Glass Europe and Nippon Sheet Glass, stay relevant with their specialty glasses, whereas new entrants, such as Gold Plus Glass Industry and Kibing Group, increase their production capacities to tap into growth opportunities tied to localized supply chains.

- Key players include AGC Glass Europe, Nippon Sheet Glass Co., Ltd., Gold Plus, Flat Glass Group Co., Ltd, Xinyi Glass Holdings Limited, Guardian Industries Holdings, Onyx Solar Energy S.L., Kibing Group, CHINA GLASS HOLDING and Jinjing (Group) Co., Ltd.

Key Developments

- April 2026 - Nippon Sheet Glass completed a pilot demonstrating the use of recycled solar panel cover glass in float glass production, confirming technical feasibility under controlled conditions and advancing circular manufacturing practices within the photovoltaic glass value chain.

- October 2025 - GlassKote Float Glass Industries announced an investment exceeding USD 780 million to develop two low-iron float glass plants in Australia and the UAE, with integrated capabilities for solar glass and BIPV applications, strengthening supply across architectural and renewable energy segments.

- January 2025 - Gold Plus Glass Industry announced its entry into the photovoltaic glass segment through the commissioning of a new manufacturing facility in Karnataka, incorporating a solar glass capacity of 109,500 metric tons per year, thereby expanding its float glass portfolio and strengthening domestic supply for solar applications.

- October 2025- AGC Glass Europe partnered with SOLAR MATERIALS to integrate high-purity recycled glass from end-of-life solar panels into float glass production, advancing circularity and reducing raw material consumption and carbon emissions in photovoltaic glass manufacturing.

- April 2023 - Vitro entered into a long-term agreement with First Solar to manufacture float glass for thin-film photovoltaic modules, supported by a USD 93.6 million investment to upgrade its Meadville facility, with production expected to commence in the second quarter of 2025.

Why Choose DataM?

- Technological Innovations: Explores the latest advancements in Float Glass for Photovoltaics design, including improved hydraulic systems, advanced operator controls, telematics integration, electric and hybrid powertrains and enhanced attachment versatility that are driving higher productivity and lower operating costs across construction and industrial applications.

- Product Performance & Market Positioning: Evaluates how different OEMs perform in real-world construction, landscaping, agriculture and municipal environments. The analysis compares lifting capacity, breakout force, fuel efficiency, durability, operator comfort and attachment compatibility, highlighting how leading manufacturers differentiate themselves globally.

- Real-World Evidence: Highlights practical use cases of Float Glass for Photovoltaics across infrastructure development, road maintenance, warehouse handling and smart city projects. It demonstrates measurable improvements in jobsite efficiency, reduced labor dependency, faster material handling and optimized equipment utilization.

- Market Updates & Industry Changes: Tracks important industry developments such as new product launches, electrification initiatives, localized manufacturing expansions, tightening emission standards (Stage V, Tier 4 Final) and shifts in construction spending across major regions, including North America, APAC, China and India.

- Competitive Strategies: Analyzes how leading manufacturers are expanding their footprint through dealer network strengthening, localized production, electric model introductions, strategic partnerships and technology-driven differentiation such as AI-enabled monitoring and autonomous-ready platforms.

- Pricing & Market Access: Explains pricing structures across standard, high-capacity and electric skid steer models, including outright purchase, leasing and rental models. It also reviews regional availability, distribution networks and financing strategies that enhance market penetration.

- Market Entry & Expansion: Identifies growth opportunities in emerging economies driven by infrastructure development, urbanization, smart city programs and expanding rental ecosystems. It also outlines strategies for OEMs to scale operations globally through regional manufacturing hubs and after-sales service optimization.

Target Audience 2026

- Photovoltaic Module Manufacturers: Tier-1 and Tier-2 solar module producers utilizing low-iron and coated float glass for crystalline silicon and thin-film modules, with a focus on efficiency optimization and durability enhancement.

- Solar Project Developers & EPC Companies: Utility-scale developers, engineering-procurement-construction (EPC) contractors and independent power producers sourcing photovoltaic glass for large-scale solar installations and bifacial module deployments.

- Glass Manufacturers & Processors: Float glass producers, coating technology providers and glass processors involved in manufacturing, tempering and coating of solar-grade glass to meet evolving module specifications.

- Renewable Energy Companies & Utilities: Solar energy companies and power utilities integrating photovoltaic systems into energy portfolios, driving demand for high-performance solar glass solutions.

- Building-Integrated Photovoltaics (BIPV) Developers & Construction Firms: Real estate developers, façade engineers and construction companies incorporating solar glass into building envelopes, façades and smart infrastructure projects.

- Investors & Private Equity Firms: Investment groups tracking opportunities in solar manufacturing, glass capacity expansion and supply chain localization within the renewable energy ecosystem.

- Dealers & Distribution Networks: Channel partners involved in distribution, logistics and supply chain management of solar glass and related components across regional markets