Flexible Printed Circuit FPC Market Overview

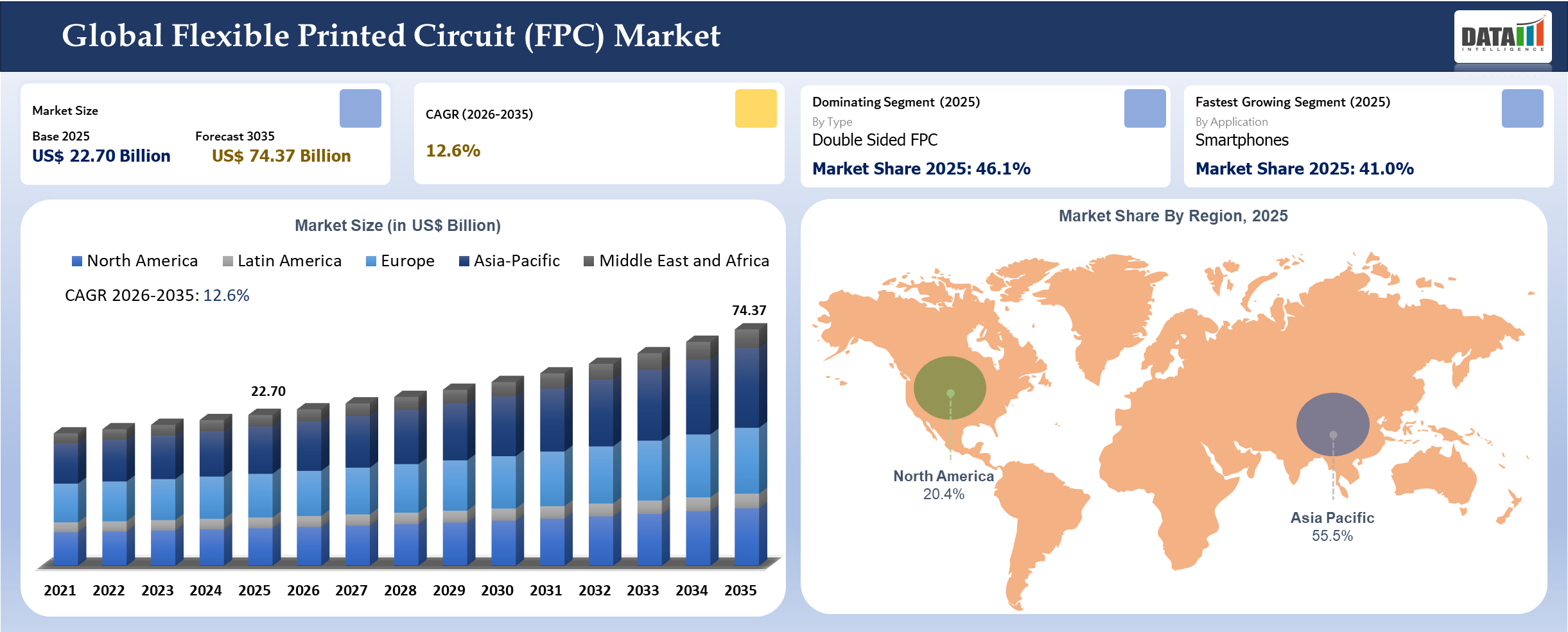

The global flexible printed circuit (FPC) market reached US$ 22.70 billion in 2025 and is expected to reach US$ 74.37 billion by 2035, growing with a CAGR of 12.6% during the forecast period 2026-2035. The market experiences a major technological leap caused by the rapid advancement of small and efficient electronics as well as connected devices in all industries. According to the statement of Japan Electronics and Information Technology Industries Association, the production of electronic goods continually rises owing to increasing demand for semiconductors and electronic parts used for assembling flexible circuit boards.

According to International Data Corporation, the number of smartphone shipments per year exceeds one billion items all around the world. It is a constant need for FPCs being used in displays, camera assemblies and battery packs of contemporary portable phones. The number of flexible devices is rising, and thus there is a greater need for robust materials, including polyimide films and thin copper laminates.

The growing adoption of automotive electrification and ADAS is also reshaping the demand environment for FPCs, considering that contemporary cars are made up of intricate wiring assemblies that need to be flexible and have improved space efficiency. According to the Organisation Internationale des Constructeurs d'Automobiles, there have been steady production levels across the globe of vehicles, thereby resulting in rising demand for light and compact electronic connections. On the other hand, the field of industrial automation and robotics has grown, as evidenced by the installation of a record number of robots globally, according to the International Federation of Robotics. It is possible with the help of FPCs that make it easy to achieve dynamic movement along with reliable connections despite the limited space.

Flexible Printed Circuit (FPC) Industry Trends and Strategic Insights

- Type remains the most commercially useful lens because it explains how buyers allocate budgets, compare suppliers and frame performance trade-offs inside the flexible printed circuit market.

- Demand is shifting toward solutions that can prove measurable value in Multi-Layer FPC and Rigid Flex PCB rather than relying on broad platform claims.

- Asia-Pacific is setting the competitive pace, with China and Japan shaping product design, supply decisions and go-to-market priorities.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 22.70 Billion | |

| 2035 Projected Market Size | US$ 74.37 Billion | |

| CAGR (2026-2035) | 12.6% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Type | Single Sided FPC, Double Sided FPC, Multi-Layer FPC, Rigid Flex PCB | |

| By Material | Polyimide, PET, LCP, Others | |

| By Application | Smartphones, Automotive Electronics, Medical Devices, Industrial Electronics, Consumer Devices | |

| By End-User | Consumer Electronics, Automotive, Healthcare, Industrial, Aerospace and Defense | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

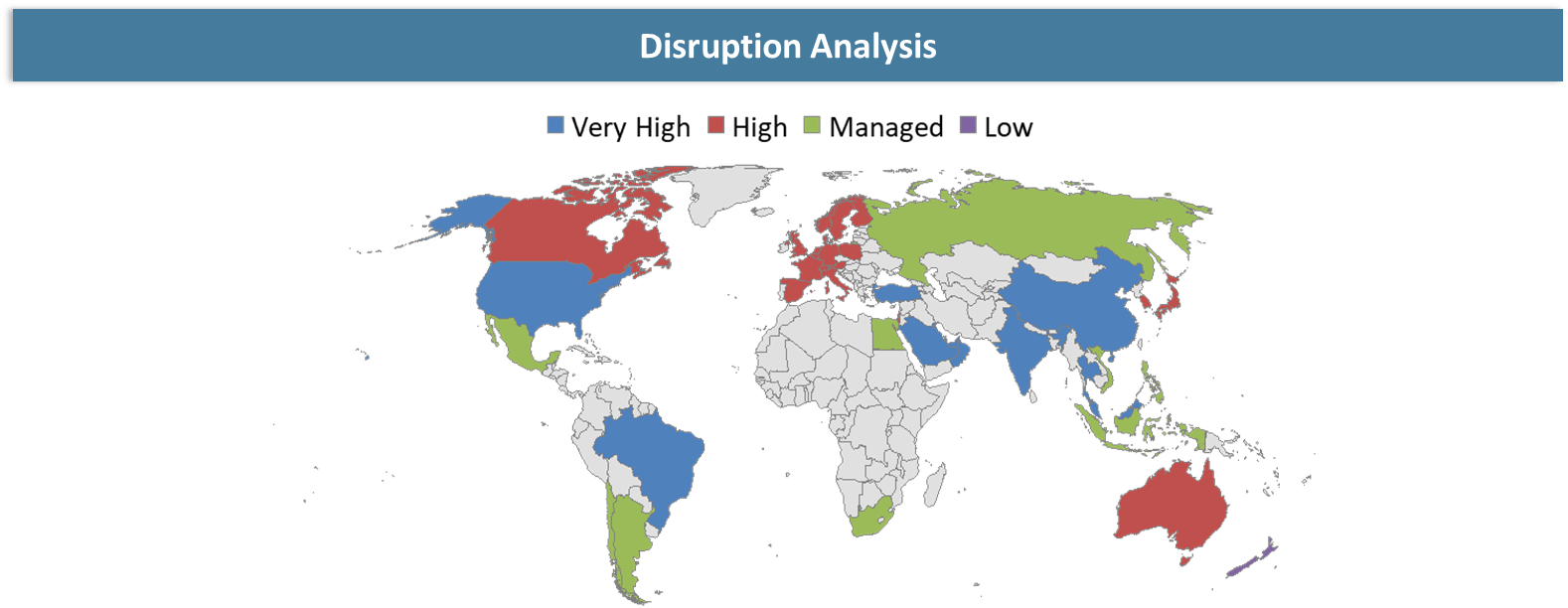

Disruption Analysis

New technologies, such as FHE, printed electronics, and substrates, are creating new standards for extremely thin, tough, and densely integrated circuitry. Automation and precise manufacturing through roll-to-roll technology are transforming cost models and economies of scale in favor of those with cutting-edge manufacturing environments. At the same time, the shift from rigid PCBs to flexible and rigid-flex PCBs for applications in automotive electronics, 5G connectivity, and wearables is changing the competitive landscape. Regionalization and geopolitics are also causing firms to think differently about supply chains, forcing them to adopt more local manufacturing operations. Sustainability considerations are driving companies to use sustainable materials and improve their recycling processes.

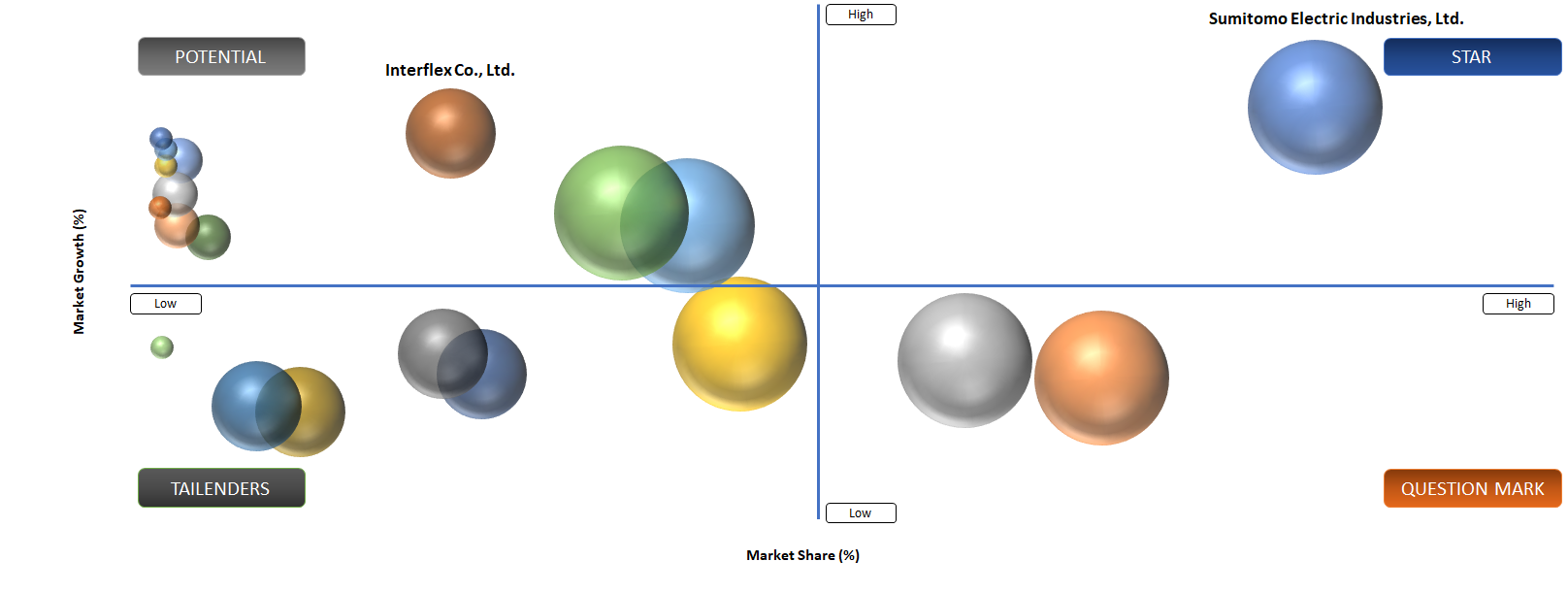

BCG Matrix: Company Evaluation

In BCG terms, the Stars in the global flexible printed circuit (FPC) market are usually the suppliers combining visible demand momentum with ecosystem control. Companies such as Sumitomo Electric Industries, Ltd., Nippon Mektron, Ltd. and Flexium Interconnect, Inc. tend to sit in this zone when they can link product depth with distribution reach, integration credibility and recurring account expansion.

Market Dynamics

Shift toward measurable operating value and application specific buying criteria

Buyers increasingly want a product or platform that can lift throughput, improve quality, shorten turnaround times, reduce labor intensity or unlock a new service model. The change matters because it favors suppliers that understand the customer workflow deeply enough to tie adoption to hard business metrics. The demand also come from how the procurement teams compare vendors. Customers look at deployment friction, support quality, compliance posture, integration effort and the credibility of promised savings or productivity gains.

Market expansion is also being reinforced by ecosystem maturity. Buyers can now access surrounding tools, implementation partners, connectivity layers or manufacturing support that make adoption less risky than it was a few years ago. Once those enabling pieces are available, the purchase decision becomes easier to defend internally, which broadens the addressable market.

End users are becoming less tolerant of generic products that create manual work after installation, demanding systems that fit existing infrastructure and scale without repeated redesign. The preference is steadily lifting demand for higher value suppliers and making commercially relevant segmentation more visible across this market.

Integration burden, compliance friction and longer enterprise decision cycles

The main restraint in the global flexible printed circuit (FPC) market is that customer interest does not always translate into fast deployment. Many buyers face integration complexity, validation demands, data or process constraints and procurement oversight that can stretch timelines even when the business case looks attractive. The friction is particularly visible when the product touches regulated workflows, capital budgets, legacy systems or multi stakeholder approvals. Suppliers underestimate the reality often overstate how quickly pilots will convert into scaled revenue.

Segmentation Analysis

The global flexible printed circuit (FPC) market is segmented based on the type, material, application, end user, sales channel and region.

Multi-Layer FPC Leads Early Adoption as Cost-Efficient Integration Drives Scalable Market Growth

Multi-Layer FPC and Rigid Flex PCB deserve the closest attention. Both are commercially relevant, but they win for different reasons. One usually benefits from scale, familiarity or easier integration, while the other gains share where control, compliance, performance or premium use case fit matter more. Multi-Layer FPC remains important because customers can often adopt it without redesigning the rest of their operating model. It tends to fit existing budgets, partner ecosystems and internal skill levels, which keeps the buying decision easier to justify. In many cases, the first wave of market growth lands here because the path to implementation is clearer and the organizational disruption is lower.

Geographical Penetration

Asia-Pacific Emerges as Strategic Nucleus for Scalable, Application-Driven Growth in Flexible Printed Circuit (FPC) Market

Asia-Pacific market is being shaped by real operating changes rather than by headline demand alone. Procurement behavior, channel structure, compliance expectations and product mix are all moving in ways that make the region more informative for future revenue concentration and competitive strategy. Asia-Pacific leads because flexible printed circuits sit at the center of device miniaturization, camera module complexity, battery routing and lightweight electronics design. The market is increasingly shaped by product architecture shifts in smartphones, automotive displays, wearables and compact industrial electronics.

Buying committees increasingly ask how quickly a solution can be deployed, how it performs in live environments and whether local partners, service teams or manufacturing footprints can support scale. It makes the region especially useful for understanding which business models are genuinely sustainable.

China Flexible Printed Circuit (FPC) Market Outlook

China requires separate consideration, owing to the way that it drives category evolution based on its unique combination of demand, policies, manufacturing capabilities, and purchasing practices. Chinese market developments provide clues as to which vendors can meet the needs of customers whose requirements are more challenging than simple global positioning strategies. In China, the emerging development seems to be that buyers no longer reward generic approaches to business.

China is also important because commercial success there increasingly depends on ecosystem coordination. Suppliers that can align implementation, service, compliance and adjacent technologies usually move faster than vendors relying on product-only narratives. It makes the country a strong indicator of who can scale profitably rather than simply generate interest.

Japan Flexible Printed Circuit (FPC) Market Trends

Japan serves as a perfect example of how specific demands, favorable policies, or deep expertise and concentration of talent may be factors driving higher-end segments within the overall industry. It pays off to be attentive to such trends from the very beginning when signs of differentiation start to emerge and positioning becomes clearer.

China is relevant in relation to the industry due to its capacity in terms of scale manufacturing, its domestic supply chain of electronic products, and its competitiveness, making the market very sensitive to OEM design trends and localization. Japan is still relevant due to its expertise in materials and processing and strong expertise in flexible solutions, which are highly reliable in complex electronic assemblies.

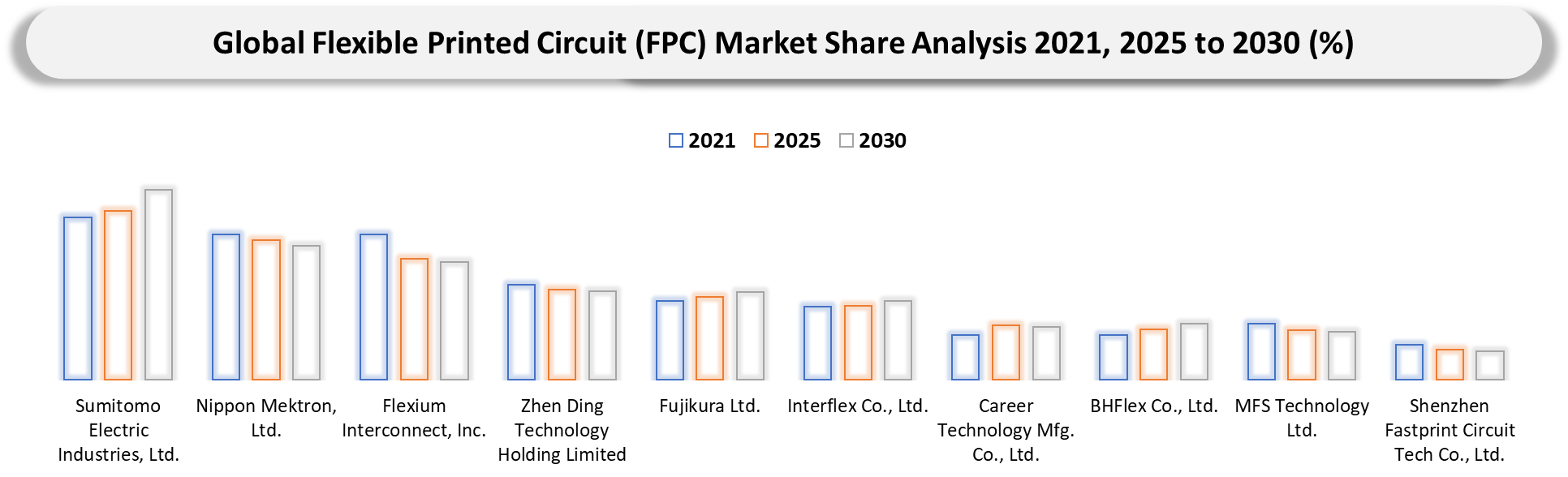

Competitive Landscape

- Competition in the global flexible printed circuit (FPC) market is defined by a split between scale players and focused specialists. Large vendors such as Sumitomo Electric Industries, Ltd., Nippon Mektron, Ltd., and Flexium Interconnect, Inc. use portfolio breadth, channel reach and account access to shape category expectations, while specialist vendors try to win through product depth, faster implementation or sharper case alignment.

- Market positioning is increasingly influenced by how well suppliers defend the full customer journey. Product quality still matters, but so do onboarding friction, integration capability, data or workflow control, application engineering and lifecycle support. Vendors that can anchor around high-value segments such as Multi-Layer FPC and Rigid Flex PCB are generally in a better position to protect pricing and expand share.

Key Developments

- April 2026: Zhen Ding Technology Holding Limited strengthened IC substrate and flexible circuit production for high-performance computing and Apple supply chain demand expansion.

- March 2026: AT&S Austria Technologie and Systemtechnik AG invested in IC substrates and flexible circuits for AI and high-performance computing, strengthening European semiconductor supply chain capabilities.

- March 2026: Luxshare Precision Industry Co., Ltd. increased investment in flexible interconnects and FPC assembly for consumer electronics, strengthening vertical integration with global OEM partners.

- February 2026: Flexium Interconnect, Inc. invested in advanced HDI and multilayer FPC technologies targeting AI servers and compact wearable electronics integration.

- February 2026: Unimicron Technology Corporation increased investment in HDI and IC substrate technologies supporting AI servers and next-generation semiconductor packaging.

- January 2026: Nippon Mektron, Ltd. accelerated commercialization of foldable-device FPC solutions, enhancing durability cycles and supporting next-generation OLED smartphone applications.

- January 2026: Ibiden Co., Ltd. expanded semiconductor package substrates and flexible circuit technologies supporting advanced processors and data center infrastructure growth.

- January 2026: Shenzhen Fastprint Circuit Tech Co., Ltd. expanded rapid PCB and FPC manufacturing lines to support telecom infrastructure and 5G base station electronics demand.

- October 2025: Molex, LLC launched advanced flexible interconnect solutions for automotive and medical applications, emphasizing miniaturization and high-speed data transmission.

- September 2025: Interflex Co., Ltd. expanded OLED display FPC supply agreements with smartphone OEMs, focusing on high-density interconnect designs for foldable devices.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Electronics & Consumer Device Manufacturers: OEMs producing smartphones, wearables, laptops, tablets, and other compact electronics leveraging FPCs for space-saving, lightweight, and high-performance circuit integration.

- Automotive OEMs & EV Manufacturers: Companies integrating FPCs in advanced driver-assistance systems (ADAS), infotainment systems, battery management systems, and electric vehicle architecture.

- Telecommunications & Networking Companies: Firms deploying FPCs in 5G infrastructure, antennas, routers, and high-speed data transmission equipment requiring flexible and high-density interconnections.

- Industrial & Medical Device Manufacturers: Manufacturers of medical imaging systems, diagnostic equipment, industrial automation systems, and robotics utilizing FPCs for precision, reliability, and compact designs.

- OEMs & PCB/FPC Manufacturers: Global and regional circuit manufacturers focusing on multilayer FPC innovation, miniaturization, and advanced material technologies for next-generation electronics.

- Investors & Private Equity Firms: Investment entities tracking growth in advanced electronics manufacturing, semiconductor packaging, and high-growth applications such as EVs, IoT, and wearable devices.

- Distributors & Supply Chain Players: Component suppliers, authorized distributors, and aftermarket service providers involved in sourcing, logistics, assembly support, and lifecycle management of FPC-based systems.