Flexible Hybrid Electronics (FHE) Market Overview

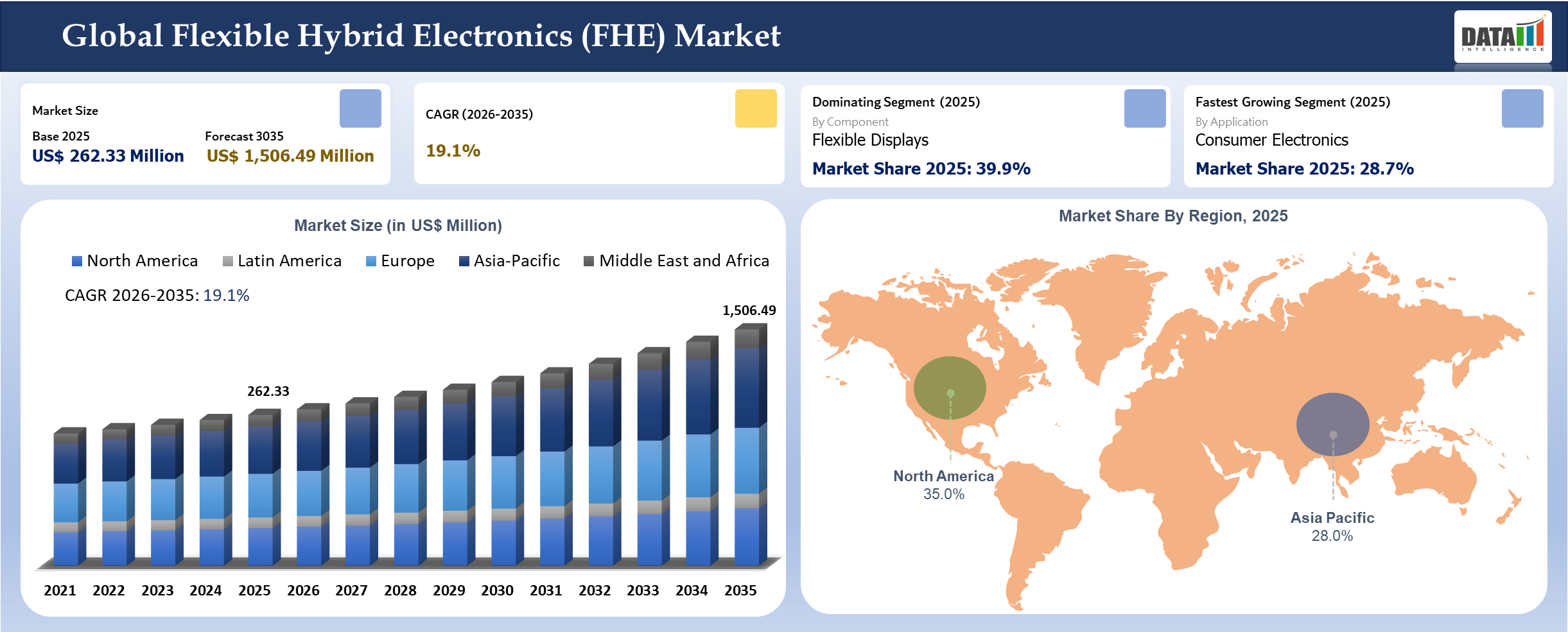

The global flexible hybrid electronics (FHE) market reached US$ 262.33 million in 2025 and is expected to reach US$ 1,506.49 million by 2035, growing with a CAGR of 19.1% during the forecast period 2026-2035. FHEs are very crucial in developing next-generation electronics due to the emergence of lightweight, conformable and highly integrated electronic systems. Integration of printed electronics, flexible substrates and silicon parts is facilitating manufacturing of lighter, more power efficient electronics and providing increased functionalities. According to OE-A, printed electronics and flexible electronics have gained momentum in such applications as smart wearable systems, patches in medicine and structural electronics due to the requirement of smaller and more integrated systems. NSF has sponsored numerous studies on flexible electronics and advanced materials which show their strategic importance in future electronics manufacturing.

Government and private-public partnerships are crucial in facilitating the development of the FHE ecosystem, especially in sectors like defense, health care and advanced manufacturing. In this regard, the NextFlex, which is funded by the United States Department of Defense, has been working on developing research projects related to FHE technologies, allocating millions of dollars toward the same.

Flexible Hybrid Electronics (FHE) Industry Trends and Strategic Insights

- Application remains the most commercially useful lens because it explains how buyers allocate budgets, compare suppliers and frame performance tradeoffs inside the flexible hybrid electronics market.

- Demand is shifting toward solutions that can prove measurable value in Wearables and Medical Patches rather than relying on broad platform claims.

- North America is setting the competitive pace, with USA and Canada shaping product design, supply decisions and go to market priorities.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 262.33 Million | |

| 2035 Projected Market Size | US$ 1,506.49 Million | |

| CAGR (2026-2035) | 19.1% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Component | Printed Sensors, Flexible Displays, Flexible Interconnects, Energy Storage Components, Embedded IC Modules | |

| By Material | Conductive Inks, Flexible Substrates, Encapsulation Materials, Adhesives | |

| By Application | Wearables, Medical Patches, Automotive Interiors, Industrial Monitoring, Consumer Electronics | |

| By Manufacturing Process | Screen Printing, Inkjet Printing, Roll to Roll, Hybrid Assembly | |

| By End-User | Healthcare, Consumer Electronics, Automotive, Industrial, Defense | |

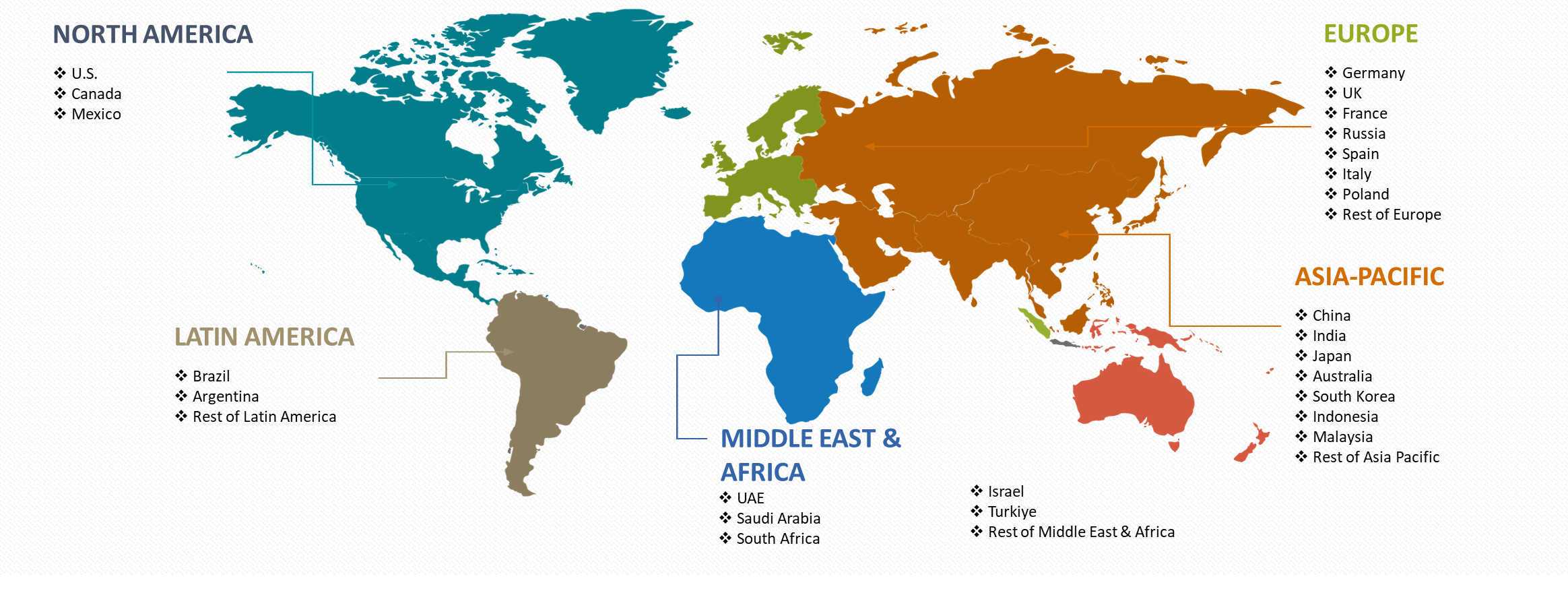

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

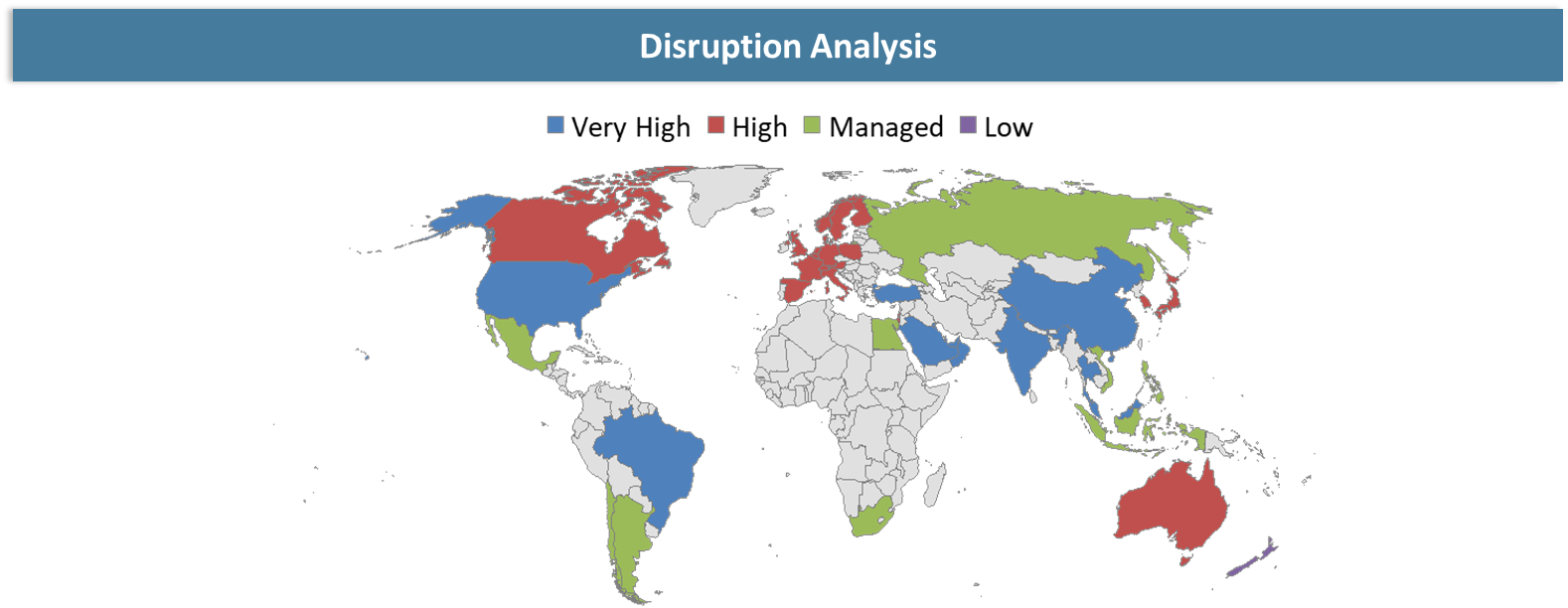

Disruption Analysis

The vendor cannot simply depend on spec sheets and innovative language anymore because the customer wants to know how quickly it will fit in with the current system, how reliable it is under load and how quickly it will justify its cost. The model of channels, partnering for integration and bundling solutions is influencing how vendors are being shortlisted by the customer. The market is being challenged through the increased demand for resilience and accountability. Consumers are starting to inquire into the origin of the product, local backing and how it copes with supply constraints, among others.

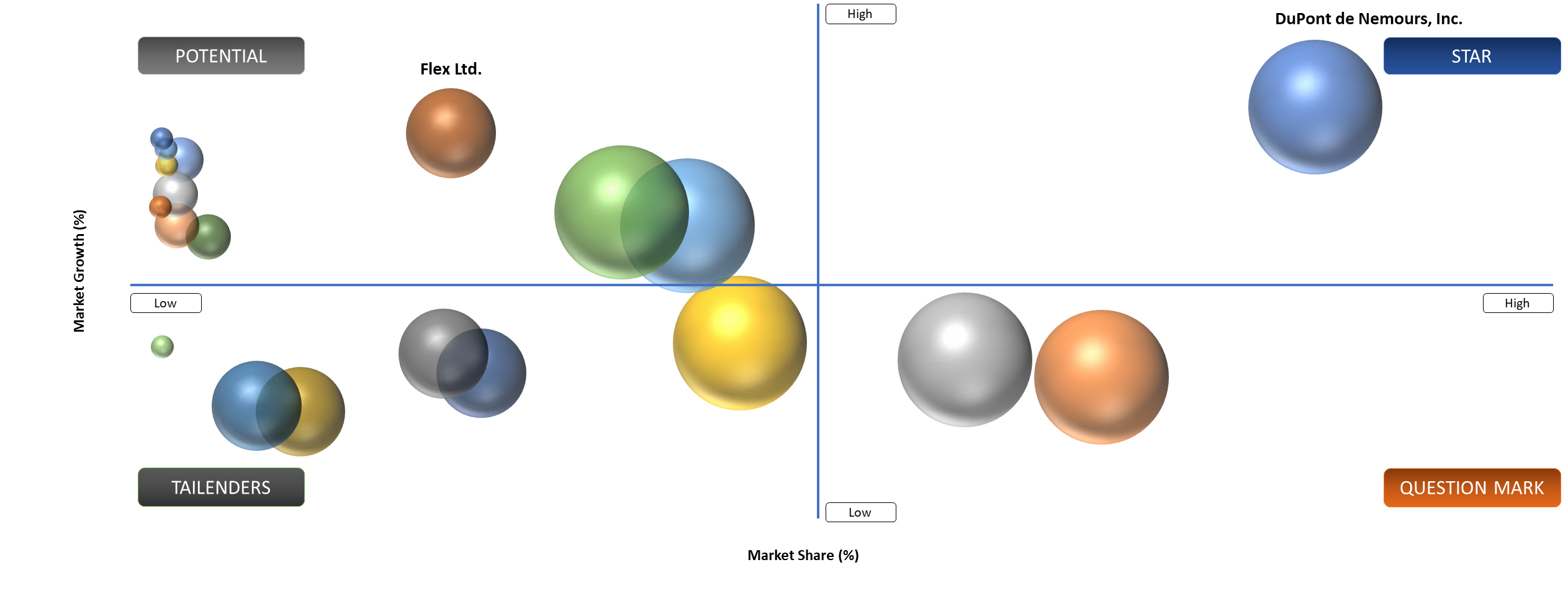

BCG Matrix: Company Evaluation

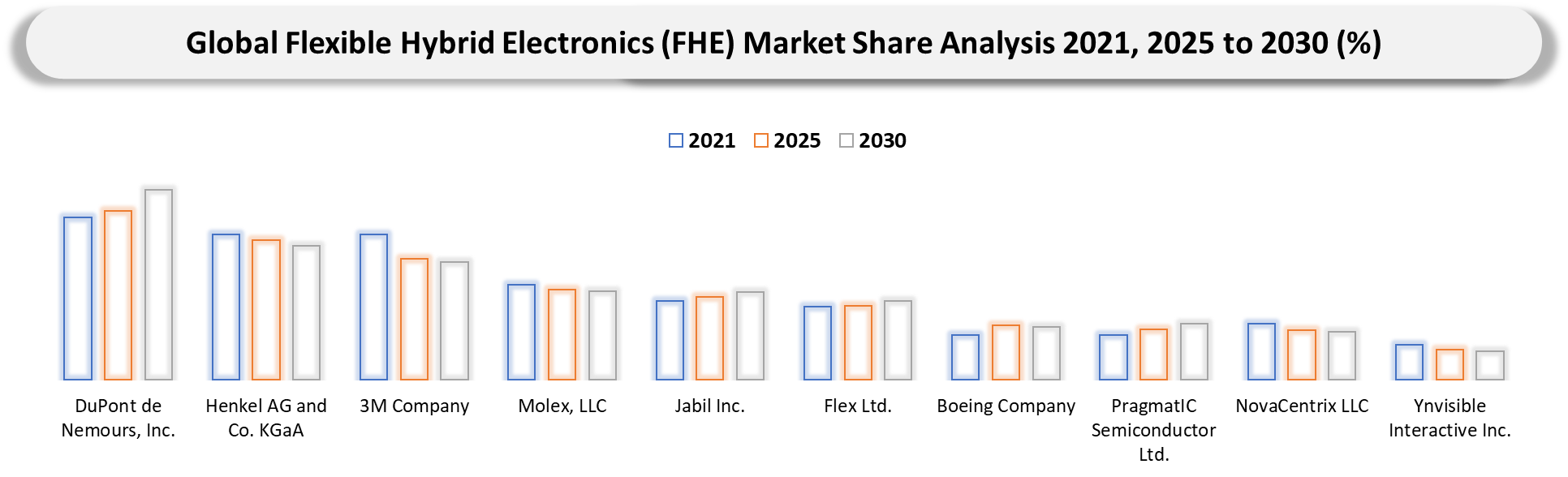

In BCG terms, the Stars in the global flexible hybrid electronics (FHE) market are usually the suppliers combining visible demand momentum with ecosystem control. Companies such as DuPont de Nemours, Inc., Henkel AG and Co. KGaA and 3M Company tend to sit in this zone when they can link product depth with distribution reach, integration credibility and recurring account expansion.

Question Marks in this market include younger specialists and adjacent vendors entering through a narrow wedge such as wearables or medical patches. The upside is strong if they can prove differentiated outcomes, but they still need scale, partner leverage or regulatory and commercial validation.

Market Dynamics

Shift toward measurable operating value and application specific buying criteria

Buyers increasingly want a product or platform that can lift throughput, improve quality, shorten turnaround times, reduce labor intensity or unlock a new service model. It change matters because it favors suppliers that understand the customer workflow deeply enough to tie adoption to hard business metrics.

Demand also comes from how procurement teams now compare vendors. The shortlist is rarely built on technical capability alone. Customers look at deployment friction, support quality, compliance posture, integration effort and the credibility of promised savings or productivity gains. Market expansion is also being reinforced by ecosystem maturity. Buyers can now access surrounding tools, implementation partners, connectivity layers or manufacturing support that make adoption less risky than it was a few years ago. Once those enabling pieces are available, the purchase decision becomes easier to defend internally, which broadens the addressable market.

End-users are becoming less tolerant of generic products that create manual work after installation. They want systems that fit existing infrastructure and scale without repeated redesign. The preference is steadily lifting demand for higher value suppliers and making commercially relevant segmentation more visible across this market.

Integration burden, compliance friction and longer enterprise decision cycles

The main restraint in the global flexible hybrid electronics (FHE) market is that customer interest does not always translate into fast deployment. Many buyers face integration complexity, validation demands, data or process constraints and procurement oversight that can stretch timelines even when the business case looks attractive.

The friction is particularly visible when the product touches regulated workflows, capital budgets, legacy systems or multi stakeholder approvals. Suppliers that underestimate this reality often overstate how quickly pilots will convert into scaled revenue.

Segmentation Analysis

The global flexible hybrid electronics (FHE) market is segmented based on components, material, application, manufacturing process, end-user and region.

Wearables Drive Early Adoption While Medical Patches Capture High-Value, Compliance-Led Growth

Wearables and Medical Patches deserve the closest attention. Both are commercially relevant, but they win for different reasons. One usually benefits from scale, familiarity or easier integration, while the other gains share where control, compliance, performance or premium use case fit matter more. The contrast is exactly why these subsegments are useful in market research and consulting work: they reveal where revenue concentration and future pricing power may diverge.

Wearables remain important because customers can often adopt them without redesigning the rest of their operating model. It tends to fit existing budgets, partner ecosystems and internal skill levels, which keeps the buying decision easier to justify. In many cases, the first wave of market growth lands here because the path to implementation is clearer and the organizational disruption is lower.

Geographical Penetration

North America Emerges as Commercialization Benchmark Driven by Application-Focused Adoption and Evolving Procurement Dynamics

North America market is being shaped there by real operating changes rather than by headline demand alone. Procurement behavior, channel structure, compliance expectations and product mix are all moving in ways that make the region more informative for future revenue concentration and competitive strategy.

North America remains influential because commercialization in flexible hybrid electronics is increasingly tied to application fit rather than lab novelty. Programs that connect materials, assembly and real product economics in wearables, industrial sensing and medical monitoring are advancing faster than broad platform claims. Buying committees increasingly ask how quickly a solution can be deployed, how it performs in live environments and whether local partners, service teams or manufacturing footprints can support scale. It makes the region especially useful for understanding which business models are genuinely sustainable.

USA Flexible Hybrid Electronics (FHE) Market Outlook

USA shapes the category direction through its own mix of demand, policy, industrial structure and procurement behavior. Market movement in USA often reveals which suppliers can adapt to more demanding customer requirements rather than relying on broad global positioning.

In USA, buyers are no longer rewarding generic offers at the same rate. Buyers are asking for products and platforms that fit local cost structures, standards, integration realities and performance expectations. It changes according to vendors designing local go-to market plans, select channel partners and prioritizing product variants.

USA is also important because commercial success there increasingly depends on ecosystem coordination. Suppliers that can align implementation, service, compliance and adjacent technologies usually move faster than vendors relying on product only narratives. It makes the country a strong indicator of who can scale profitably rather than simply generate interest.

Canada Flexible Hybrid Electronics (FHE) Market Trends

Canada highlights the specialized demand, policy support, talent depth or industrial concentration which can lift higher value niches inside the broader market. It makes to watch for early premiumization signals and emerging competitive positions.

USA activity is shaped by defense and healthcare prototypes translating into product focused development, especially where low profile sensing and lightweight electronics create integration advantages. Canada is relevant through printed electronics research, smart textile innovation and early commercialization in sensing-oriented applications rather than mass scale consumer electronics.

Taken together, USA and Canada show that regional growth is not uniform. Revenue opportunity depends on where local operating realities favor the segment mix, commercial model and supplier capabilities that customers can adopt with confidence.

Competitive Landscape

- Competition in the global flexible hybrid electronics (FHE) market is defined by a split between scale players and focused specialists. Large vendors such as DuPont de Nemours, Inc., Henkel AG and Co. KGaA and 3M Company use portfolio breadth, channel reach and account access to shape category expectations, while specialist vendors try to win through product depth, faster implementation or sharper use case alignment. As the market matures, the strongest positions are being built by companies that combine technical credibility with surrounding services, ecosystem partnerships and support depth.

- Market positioning is increasingly influenced by how well suppliers defend the full customer journey. Product quality still matters, but so do onboarding friction, integration capability, data or workflow control, application engineering and lifecycle support. Vendors that anchor around high-value segments such as wearables and medical patches are generally in a better position to protect pricing and expand share.

Key Developments

- March 2026: Henkel AG & Co. KGaA expanded its advanced conductive inks portfolio, supporting printed electronics and FHE applications, targeting automotive and wearable integration markets through material innovation initiatives.

- March 2026: Jabil Inc. expanded design-to-manufacturing services for flexible hybrid electronics, supporting healthcare and industrial IoT applications with scalable printed electronics production capabilities.

- March 2026: NovaCentrix LLC advanced photonic curing technology for printed electronics, improving conductivity and enabling high-speed manufacturing of flexible hybrid electronic components across industries.

- February 2026: Molex, LLC advanced flexible interconnect solutions for medical and automotive electronics, enabling compact, high-reliability FHE assemblies with improved signal integrity and miniaturization.

- February 2026: Boeing Company increased adoption of lightweight flexible hybrid electronics in aerospace systems to enable conformal sensing, structural health monitoring and reduced system weight.

- January 2026: 3M Company showcased flexible electronics materials and adhesives for hybrid integration at global electronics events, enhancing durability and conformability for next-generation wearable devices.

- January 2026: Flex Ltd. highlighted integration of AI and digital twin technologies with flexible hybrid electronics at FLEX Technology Summit, accelerating smart manufacturing and product lifecycle optimization.

- November 2025: DuPont de Nemours, Inc. completed spin-off of its electronics materials business into Qnity Electronics, strengthening its focus on advanced flexible circuit materials and semiconductor solutions.

November 2025: PragmatIC Semiconductor Ltd. promoted FlexIC technology, enabling ultra-thin, flexible chips with low-energy manufacturing, unlocking scalable applications in smart packaging, wearables and IoT devices.

Why Choose DataM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

Target Audience 2026

- Consumer Electronics & Wearable Device Manufacturers: OEMs and product developers integrating Flexible Hybrid Electronics into smartwatches, fitness trackers, foldable displays and next-generation portable devices for enhanced functionality and lightweight design.

- Healthcare & Medical Device Companies: Medical technology firms, diagnostic equipment manufacturers and digital health startups leveraging FHE for biosensors, smart patches, remote patient monitoring systems and implantable electronics.

- Automotive & Mobility OEMs: Automotive manufacturers and Tier-1 suppliers utilizing FHE in advanced human-machine interfaces (HMI), in-cabin sensors, flexible displays and lightweight electronic components for electric and autonomous vehicles.

- Aerospace & Defense Organizations: Defense contractors and aerospace companies adopting FHE for lightweight avionics, structural health monitoring systems, wearable soldier systems and next-gen communication devices.

- Industrial & IoT Solution Providers: Industrial automation firms and IoT developers incorporating FHE in smart labels, asset tracking systems, predictive maintenance sensors and connected industrial ecosystems.

- Research Institutions & Universities: Academic institutions and R&D centers focusing on material science innovations, printed electronics, nanotechnology and scalable manufacturing processes for FHE advancements.

- Government & Regulatory Bodies: Public sector agencies, innovation councils and funding organizations supporting flexible electronics development through policies, grants and national digitalization initiatives.

- Investors & Venture Capital Firms: Private equity players and venture capitalists tracking high-growth opportunities in advanced electronics, wearable technologies and next-generation semiconductor alternatives.

- Material Suppliers & Component Manufacturers: Providers of conductive inks, substrates, semiconductors and flexible materials enabling scalable production and performance optimization in FHE systems.

- Distributors & Technology Integrators: Channel partners, system integrators and solution providers involved in commercialization, deployment and lifecycle support of FHE-based products across industries.