Ethane Market Overview

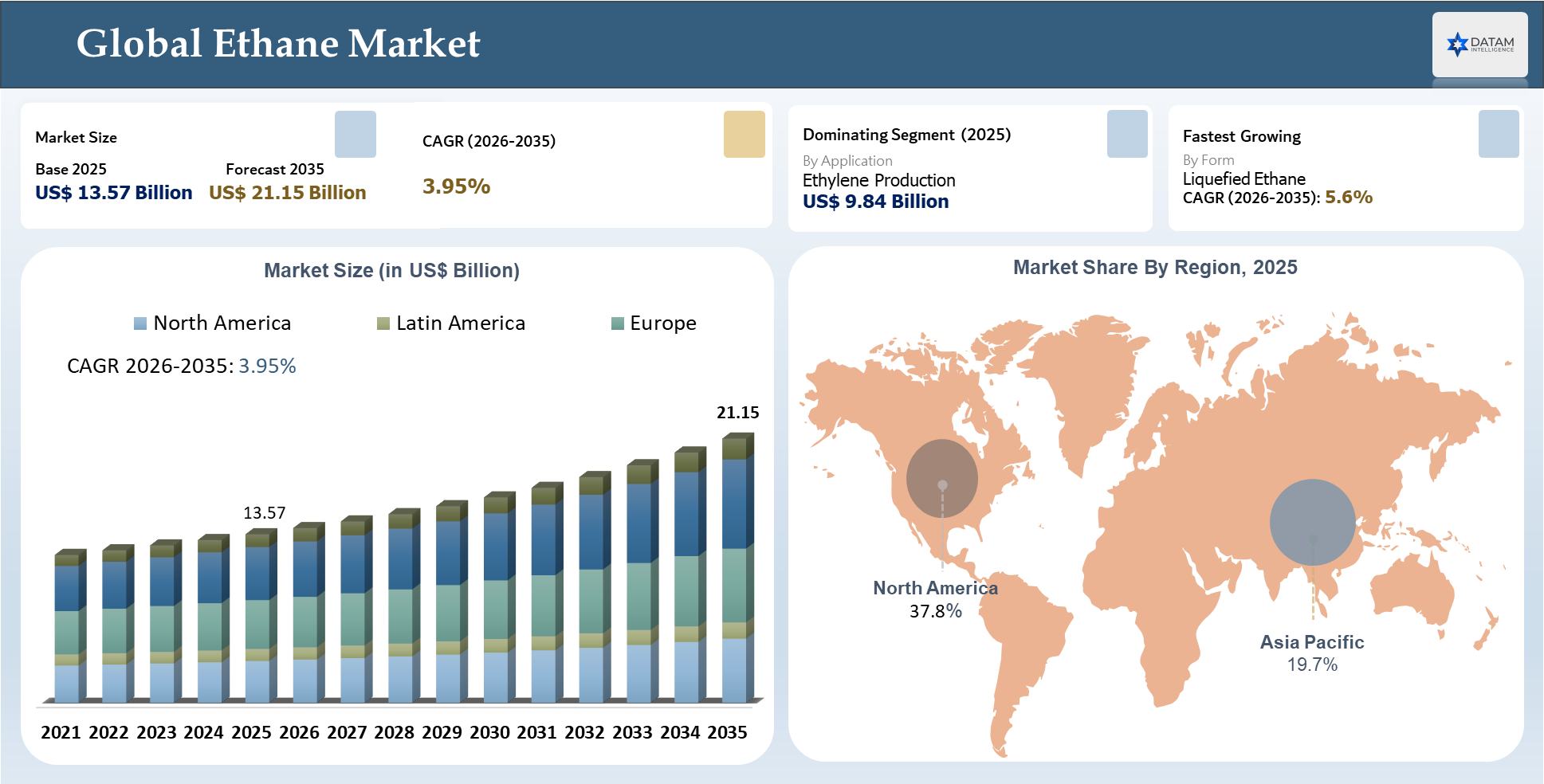

The Global Ethane Market stood at US$ 13.57 billion in 2025 and is expected to reach US$ 21.15 billion by 2035, growing with a CAGR of 3.95% during the forecast period 2026-2035. As ethane producers, NGL processors, and petrochemical feedstock consumers place greater emphasis on ethane, there has been an increase in the need for ethane recovery studies, fractionation plant capacity assessments, pipeline and terminal availability studies, and supply comparisons across countries. Feedstock consumers are not simply considering prices when looking at the market. They are also examining their ability to have reliable feedstocks, vessel availability, refrigerated storage, long-term agreements, and visibility in the cost of delivery.

The Iran war and closure of the Hormuz strait add additional weight to the importance of sourcing secure ethane. Even when there are no disruptions to ethane shipments, uncertainty in Gulf oil and energy transportation routes will increase shipping rates, insurance expenses, and continuity of feedstock supply for the importing countries. Ethane supply from non-Hormuz sources, especially those from the Gulf Coast of the United States, is preferred by Chinese, Indian, Japanese, and South Korean ethane consumers to minimize their exposure to transport risks. North America is still the leading supplier of ethane because of the abundance of shale gas production, extraction of natural gas liquids, fractionation capacity, storage, and export terminal facilities.

AI Impact Analysis

The advent of AI technology has made significant impacts in the Global Ethane Market for ethane producers, midstream operators, and petrochemical firms that are looking into ways of enhancing feedstock recovery, optimizing profit margins, and ensuring logistics resilience. In the gas processing segment, AI-powered analytics can help operators enhance their ethane recovery efficiencies through real-time analysis of gas composition, pressure, temperatures, and plant performances.

This ensures that operators make appropriate decisions on whether to extract or reject ethane based on fluctuations in natural gas, NGL, and ethylene price levels. On the other hand, ethane crackers can leverage AI algorithms to optimize their furnace severities, energy consumption, maintenance scheduling, and ethylene yields. Predictive maintenance models are key in averting unplanned cracker downtimes since the end-users rely on regular supplies of polyethylene, ethylene glycol, and ethylene oxide.

On the same note, AI helps trading and procurement teams forecast ethane prices, shipping costs, cracker margins, and regional demand shifts. Geopolitical disruptions such as the Iran War or Hormuz Strait Blockade can be analyzed through risk models that predict the effects of cargo delays, insurance premium escalations, and port congestions on ethane shipments.

Ethane Industry Trends and Strategic Insights

- Application remains the key commercialization parameter, as ethane demand is primarily driven by its use in ethylene production, which further supports polyethylene, ethylene glycol, ethylene oxide, vinyl chloride monomer, nitroethane and other downstream petrochemical value chains.

- Increasing demand is being witnessed for supply-secure ethane feedstock, especially among steam cracker operators seeking high ethylene yield, lower feedstock cost exposure, improved cracker utilization and better margin protection against naphtha and LPG volatility.

- North America remains the leading regional player, supported by shale gas availability, large-scale NGL recovery, mature fractionation assets, ethane-based crackers and U.S. Gulf Coast export infrastructure serving import-dependent markets.

- The winning players will be those that provide more than ethane supply, including integrated gas processing, fractionation, pipeline access, refrigerated storage, export terminal capacity, long-term contract flexibility and reliable delivery to petrochemical buyers.

- Hormuz Strait disruption is strengthening the strategic value of non-Gulf ethane supply, as import-dependent buyers in China, India, Japan and South Korea reassess route risk, vessel availability, freight escalation, marine insurance exposure and feedstock security.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 13.57 Billion | |

| 2035 Projected Market Size | US$ 21.15 Billion | |

| CAGR (2026-2035) | 3.95% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Source | Natural Gas Processing, Shale Gas, Associated Gas, Refinery Off-Gas, Biomass-Derived Ethane, and Others | |

| By Type | Conventional Ethane and Bio-Ethane | |

| By Purity Grade | Industrial Grade Ethane, Polymer Grade Ethane, Petrochemical Feedstock Grade Ethane, Lab Grade Ethane, Fuel Grade Ethane, and Others | |

| By Form | Gaseous Ethane, Liquefied Ethane, and Compressed Ethane | |

| By Application | Ethylene Production, Petrochemical Feedstock, Vinyl Chloride Monomer Feedstock, Nitroethane Feedstock, Refrigerant and Cryogenic Applications, Fuel and Energy Applications, Calibration Gas and Laboratory Use, and Others | |

| By End-Use Industry | Plastics and Polymers, Packaging, Automotive, Construction, Textiles, Consumer Goods, Chemicals, Oil and Gas, Healthcare and Laboratory, and Others | |

| By Supply Mode | Pipeline Supply, Tanker and Marine Transportation, Rail Transportation, Truck Transportation, and On-Site Captive Supply | |

| By Supply Position | Domestic Consumption, Export-Oriented, Import-Dependent, Captive Integrated Consumption, and Merchant Market | |

| By Pricing Model | Spot Pricing, Long-Term Contract Pricing, and Captive Transfer Pricing | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

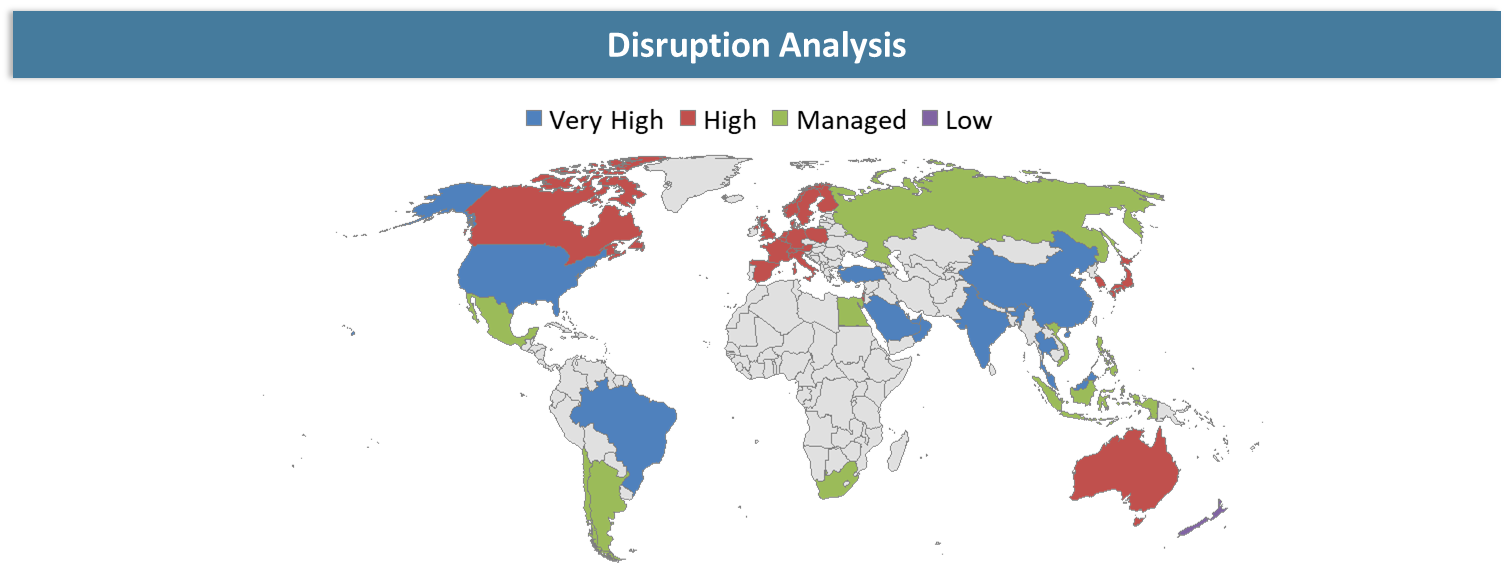

Disruption Analysis

Geopolitical Disruption and Feedstock Security Reshaping Ethane Market Dynamics

The Global Ethane Market is experiencing disruption due to geopolitical tensions, feedstock volatility, trade route threats, and changing economics of crackers. The Iran War and the potential closure of the Hormuz Strait are especially significant, as the region plays a key role in energy and petrochemical exports. Regardless of whether the ethane flow is not disrupted, the impact on the economics of cracker feedstock can alter its choice, favoring ethane-based cracking over naphtha cracking in Asia and Europe.

US ethane producers and exporters will be able to benefit from their strategically advantageous position as buyers search for alternatives to Hormuz feedstock supplies and logistics channels. At the same time, Middle East producers may have to deal with increased shipping rates, shipping delays, maritime insurance rates, and clients' concerns regarding delivery reliability. Import-dependent economies such as China, India, Japan, and South Korea are likely to revisit the issues of supplier concentration, contract flexibility, and contingency planning.

Moreover, the disruption is driving petrochemical firms to enhance feedstock flexibility, risk prediction, alternative transportation networks, and inventory management strategies. In general, ethane is moving from being a low-cost feedstock market to a market driven by petrochemical strategy.

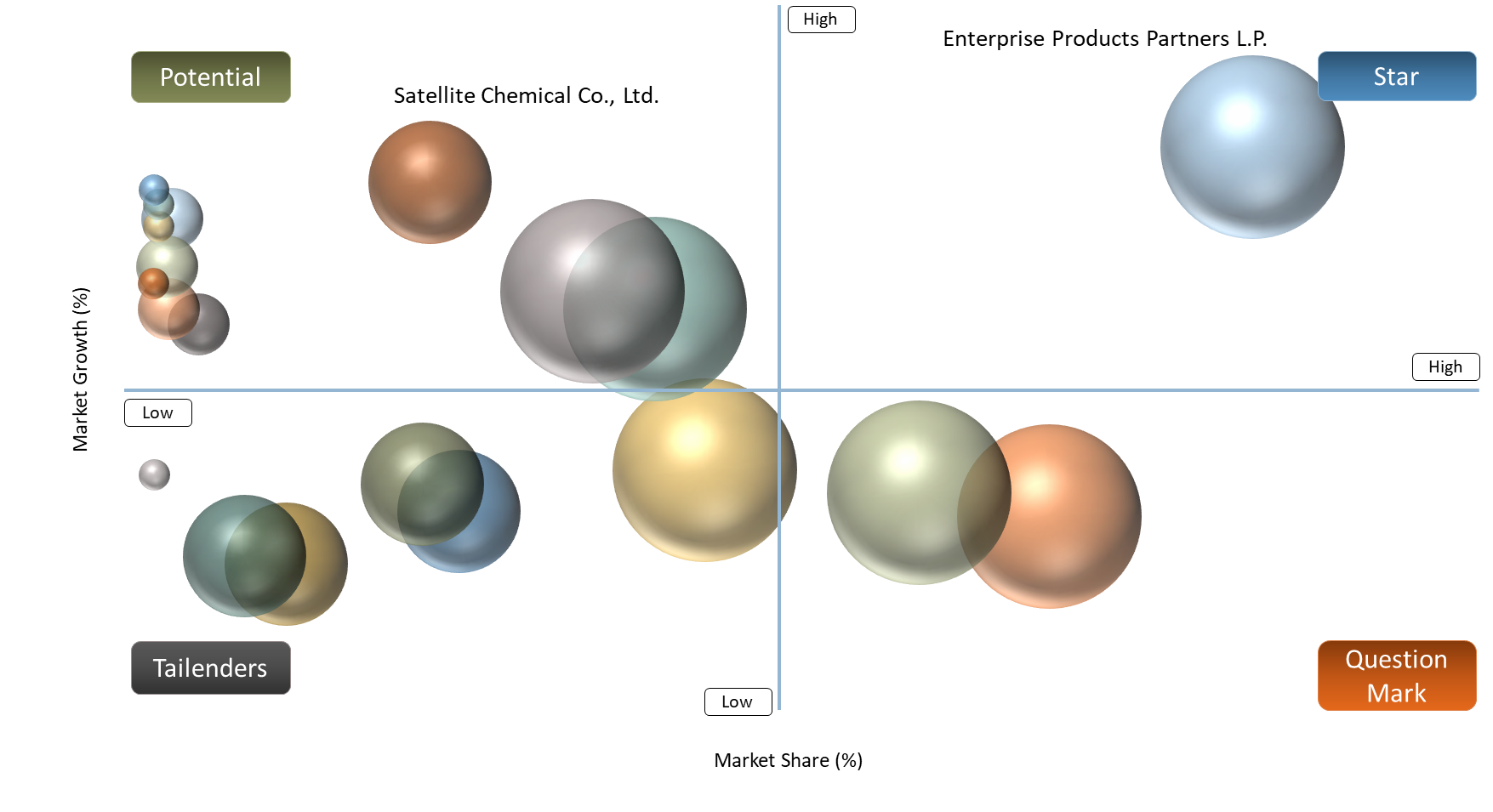

BCG Matrix: Company Evaluation

As for the BCG matrix, The Stars are the companies that have substantial control over the ethane feedstock market, NGL processing, exports, ethylene crackers, and downstream ethylene derivatives markets. Enterprise Products Partners L.P., Energy Transfer LP, ExxonMobil Corporation, Chevron Phillips Chemical Company LLC, QatarEnergy and Reliance Industries Limited are Stars since they are operating in the most value-adding points of the ethane chain. The competitive position of these players becomes more favorable amid growing buyer concerns about Hormuz-free, flexible ethane sourcing and ethylene production economics.

The Cash Cows are characterized by mature petrochemical facilities, diversified ethylene derivative product portfolios, and recurring revenue streams from petrochemicals manufacturers producing polyethylene, ethylene glycol, ethylene oxide, and industrial chemicals products. Companies such as Dow Inc., Shell plc, LyondellBasell Industries N.V., SABIC, and Saudi Aramco fit into the category due to their scale, asset integration, customer base, and downstream diversification.

The Question Marks are represented by Targa Resources Corp., ADNOC, INEOS Group and Satellite Chemical Co., Ltd. All these players' ethane significance is evident, yet their future positioning would depend on the development of export capacity, cracker economics, downstream demand, feedstock competitiveness and logistics dependability, as well as geopolitical risks of trade route disruptions.

Market Dynamics

Rising Ethane Recovery from Shale Gas and Natural Gas Processing is Increasing Commercial Ethane Availability for Petrochemical Producers

Growing ethane recovery from the production of shale gas and natural gas liquids is increasing the viability of ethane as a commercially sourced material for the petrochemical industry. Ethane extraction happens as part of natural gas processing and fractionation, with growing recovery rates resulting from greater amounts of recoverable natural gas liquids being produced from natural gas abundant basins. Growing supply visibility of ethane due to the production of shale gas in basins like the Permian, Eagle Ford, Marcellus and Utica is enabling petrochemical producers to allocate more ethane to dedicated petrochemical use, thus avoiding ethane rejection.

This helps ethylene producers by offering higher planning and margin visibility for their crackers versus crude-related naphtha feedstocks. Commercial availability of ethane makes it easier to develop business cases for ethane export infrastructure, cold storage facilities, pipelines and long-term agreements in regions that need to import the product. Petrochemical companies are finding benefit in ethane production as it allows high ethylene yield and large scale production of polyethylene and ethylene derivatives, all at reduced costs when crude oil, LPG and naphtha prices are volatile.

Import-Dependent Ethane Crackers Face High Exposure to Vessel Availability, Freight Escalation and Long-Term Supply Contract Rigidity

There is a significant limitation associated with an import-reliant ethane cracking facility since transporting ethane requires a specialized cold shipping vessel, an export terminal, and adequate receiving and storage facilities. In particular, during the Iran war and the closure of the Hormuz Strait, this aspect becomes even more important since vessel availability, marine insurance premiums, freights, and cargo scheduling risk becoming problematic could significantly rise.

The problem with Asian ethane crackers is that they are highly dependent on imported ethane and are, therefore, sensitive to disruptions to maritime routes due to the impact on costs, schedule risks, and utilization of the crackers. Even if ethane is available in sufficient quantities, delays in the shipping process can lead to problems with feedstock supply, planning issues, and increased demand on working capital management. Although the existence of long-term off-take agreements helps secure supplies, it may also limit flexibility in the process. Thus, an import-dependent producer is required to consider not only ethane prices but also issues related to the shipping of ethane when choosing to adopt ethane-based cracking.

Segment Analysis

The Global Ethane Market is segmented based source, type, purity grade, form, application, end-use industry, supply mode, supply, position, pricing model and region.

Ethylene Production Emerges as the Strategic Value Hub for Ethane Amid Feedstock Volatility and Hormuz-Linked Supply Risk

Ethylene Production is the critical value transformation process in the ethane business chain. Low cost availability of the raw material becomes value in terms of production of ethylene, its derivative demand and favorable cracking margins. Ethane is a highly productive input for use in steam crackers for the production of ethylene, which in turn feeds several derivative chains, such as polyethylene, ethylene glycol, ethylene oxide, vinyl chloride monomer among others. The choice of ethane is not just a feedstock cost decision for petrochemical firms anymore but increasingly a margin protection strategy.

Ethylene producers who have access to cheap ethane from shale gas, natural gas liquids and natural gas processing facilities will be better able to protect their profit margins against volatile crude oil-based naphtha and LPG prices. As countries with a high dependency on imports renegotiate their feedstock agreements, consider new transportation routes, and deal with price risks, this is increasingly becoming a vital factor. Given the threat of conflict with Iran and disruption in the Hormuz Strait, ethylene production that uses ethane as a feedstock is now taking on a greater strategic significance as consumers look for ways to avoid relying on Hormuz and achieve more predictable crack economics. With roughly 20 million barrels per day of crude oil flowing out of the Hormuz Strait by 2025 but only 3.5 million to 5.5 million barrels of alternative crude oil export capacity from the Gulf region, imbalance in the supply route is driving up the premium placed on ethane supply sources, especially from the US Gulf Coast.

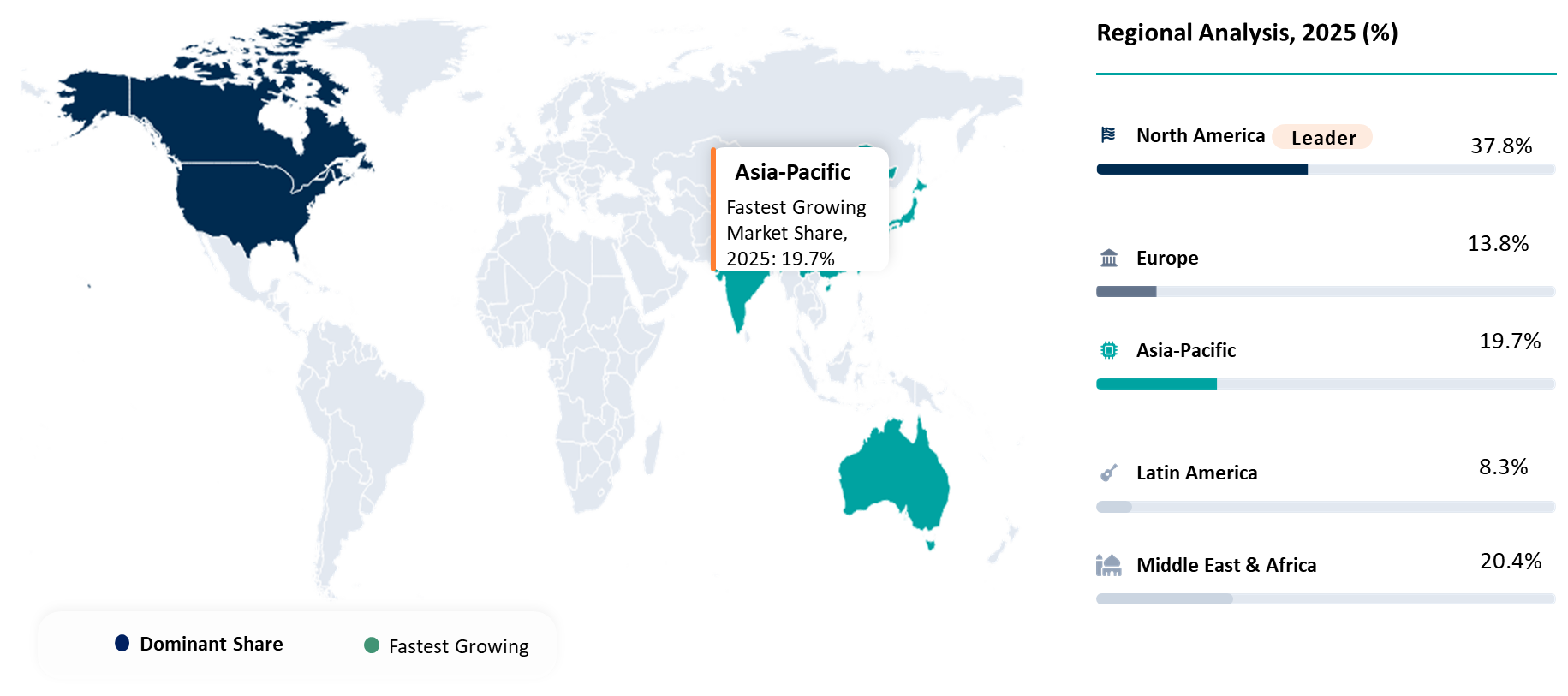

Geographical Penetration

North America Strengthens as the Leading Non-Hormuz Ethane Supply Hub

North America dominates the Global Ethane Market due to the abundance of shale gas production, robust natural gas processing facilities, and advanced NGL infrastructure. The US continues to be the driving force behind the region's growth, owing to its ability to produce sufficient quantities of ethane, aided by basins that contain natural gas resources, namely the Permian Basin, the Eagle Ford Basin, the Marcellus Basin, and the Utica Basin. With substantial fractionation facilities, pipeline infrastructure, storage infrastructure, and export terminals, producers can turn their excess ethane production into domestic cracking operations or exports.

North America is best positioned in terms of ethylene production as the presence of low-cost ethane offers better economics compared to heavy feedstock linked to oil prices like naphtha and LPG. Petrochemical complexes situated around the US Gulf Coast capitalize on the availability of ethane, polyethylene output and exports. Risks such as disruptions associated with the Iran War and Hormuz Strait pose increasing importance to North America as a secure ethane supplier which is non-Hormuz based. With the growing uncertainty of the Middle Eastern region in terms of vessel delays, higher shipping rates and marine insurance costs, US Gulf Coast ethane supply has grown increasingly significant.

U.S Ethane Market Trends

The U.S. ethane market is transforming from one based on the domestic production of ethane feedstocks to an export-driven supply platform, driven by shale gas production, natural gas processing facilities, NGL production, fractionation infrastructure, storage, transportation, and Gulf Coast ethane-integrated petrochemicals. The U.S. consumes close to 80% of its ethane domestically, exports just below 20%, and remains the world's sole exporter of waterborne ethane. This makes the U.S. ethane market unique since the ethane supply is integrated into a gas processing chain, backed by logistics, exports, and long-term demand from the ethane-fired steam crackers.

Ethane exports have become a primary market trend in the U.S., as its exports are forecasted to increase from 530,000 barrels per day in 2025 to 630,000 barrels per day in 2026, owing to increased petrochemical activity in Asia, improved capacity in ethane carriers and export infrastructure development. Import-reliant nations such as China and India are actively considering imports of U.S. ethane to minimize risks of reliance on volatile crude oil-based naphtha and LPG. As a result, under potential threats of Hormuz Strait blockage, ethane becomes strategically vital for buyers looking for supply security outside the Gulf, with stable routes, contracts, and cost expectations.

Japan Ethane Market Outlook

As an option for feedstock diversification, the Japan ethane market represents a unique case study for the reasons of its strategic importance, including the limited domestic ethane production in Japan, high dependency on foreign petrochemical resources, and necessity to increase the competitiveness of ethylene production. In contrast to the United States and Middle Eastern countries, Japan does not have any shale gas-related ethane sources; therefore, its ethane market depends heavily on imports, supply agreements, ethane tankers, import terminals, and cracker suitability.

The strategic importance of ethane arises from its ability to assist in reducing the risk of price fluctuations related to crude oil prices in Japan. In this regard, the importance of ethane for Japanese petrochemical companies implies the assessment of U.S. ethane sourcing, alternative routes to avoid the Hormuz Strait, refrigeration facilities, import terminals, and the economics of ethane cracking. In the event of an Iran War and Hormuz Strait blockade, the importance of ethane in Japan will rise significantly, forcing buyers to revise their approach to Middle Eastern energy supplies, delays, maritime insurance premiums, and feedstock security.

Import Analysis Based on Hormuz Strait Disruption

As per import analysis data, China, India, Japan and South Korea emerge as key import-exposed markets under a Hormuz Strait disruption scenario. In 2024, China accounted for 35.2% of global imports, followed by India at 7.9%, Japan at 4.5% and South Korea at 2.2%. This indicates that ethane-linked import vulnerability is most concentrated in China and India, where petrochemical producers depend heavily on external feedstock flows to support ethylene, polyethylene and other downstream derivative value chains.

China is the most exposed market, with imports of around US$3.10 billion in 2025, making supply continuity, origin diversification and non-Hormuz sourcing critical for its cracker network. India also shows a strong import dependency profile, with imports of around US$722.6 million in 2025, which could accelerate its focus on U.S. ethane sourcing, dedicated VLEC contracts, receiving infrastructure and feedstock diversification. Japan and South Korea have smaller but still import-heavy positions, with Japan importing US$214.6 million in 2025 and South Korea importing US$260.6 million in 2025.

Under Hormuz Strait disruption, these countries may face higher landed-cost volatility, freight escalation, vessel delays and marine insurance pressure due to wider instability in Middle East-linked crude, LPG, naphtha and petrochemical feedstock flows. Moreover, the disruption will push importers toward risk-adjusted sourcing, supplier diversification, route-risk assessment, terminal readiness and secure long-term ethane-linked supply contracts.

Competitive Landscape

Global Ethane Market Competitive Environment is characterized by those firms involved in the extraction of ethane supply, NGL recovery and fractionation, pipeline infrastructure, export terminals, steam cracking and ethylene derivatives downstream processes. Enterprise Products Partners L.P., Energy Transfer LP and Targa Resources Corp. are prominent American midstream firms with strong capabilities in ethane recovery and logistics with Gulf Coast export relevance. ExxonMobil Corporation, Chevron Phillips Chemical Company LLC, Dow Inc., Shell plc and LyondellBasell Industries N.V. engage themselves in competition through integrated cracker facilities, ethylene manufacturing, polyethylene manufacturing and extensive global petrochemical customer’s base.

SABIC, Saudi Aramco, QatarEnergy and ADNOC have a competitive edge because of their advantageous gas-based feedstocks and integration into the petrochemicals industry in the Middle East, however, due to the potential problems in the Hormuz waterways, there is added pressure on export security. Reliance Industries Limited, INEOS Group and Satellite Chemical Co., Ltd. can be considered competitive firms due to their dependence on imports and therefore demand side, where competitiveness is driven by securing consistent ethane sources, shipping, cracker economics and cost certainty.

Key Developments

- April 2026: Enterprise Products Partners L.P. reported higher ethane export-led terminal margin as gross operating margin from its Morgan’s Point and Neches River terminals increased by US$6 million, primarily due to higher ethane export volumes, reinforcing the role of U.S. Gulf Coast terminals in global ethane trade.

- March 2026: EIA projected stronger U.S. ethane exports supported by INEOS Project One, with the Antwerp cracker expected to come online in Q3 2026 with about 80,000 b/d of ethane capacity, creating a new structural demand outlet for U.S. ethane in Europe.

- January 2026: U.S. ethane output outlook remained expansionary, with EIA forecasts cited by Argus indicating ethane recovery of around 3.15 million b/d in 2026, supporting continued feedstock availability for domestic crackers and export markets.

- July 2025: ONGC and Mitsui O.S.K. Lines signed an agreement to develop two Very Large Ethane Carriers for supplying imported ethane to OPaL’s dual-feed cracker, with ONGC planning to import 800,000 tons per year from May 2028, strengthening India’s ethane import strategy.

- July 2025: Enterprise Products’ Neches River terminal moved into commissioning, adding 120,000 b/d of Phase 1 capacity and supporting future ethane export flexibility from the U.S. Gulf Coast to Asia and Europe.

- June 2025: U.S. ethane export restrictions to China exposed trade-policy risk as EIA forecasts indicated export controls could materially reduce U.S. ethane shipments and disrupt China-linked petrochemical feedstock security.

- May 2025: Asian petrochemical producers accelerated ethane feedstock evaluation as companies including SP Chemicals, PTT Global Chemical and Mitsui Chemicals assessed higher ethane use to protect cracker margins, with SP Chemicals targeting ethane use of up to 90% at its Jiangsu complex.

- April 2025: Asian ethane demand gained momentum from lower-cost U.S. supply, with regional producers evaluating ethane as a margin-improvement lever amid weak naphtha-based cracker economics and petrochemical oversupply.

- February 2024: QatarEnergy and Chevron Phillips Chemical started building the Ras Laffan polymers complex, including a 2.08 million tons per year ethane cracker and 1.68 million tons per year of HDPE derivative capacity, reinforcing the Middle East’s ethane-based petrochemical scale.

Major Pain Points of Global Ethane Market

- Feedstock economics are becoming harder to defend: Ethane buyers must continuously compare ethane against naphtha, LPG and propane because cracker margins now depend on volatile gas, crude, NGL and freight-linked price movements.

- Import-dependent crackers face high supply-continuity risk: Ethane imports require specialized vessels, receiving terminals, storage assets and long-term contracts, making buyers vulnerable to vessel shortages, delivery delays and limited supplier-switching flexibility.

- Hormuz Strait disruption is increasing route-risk exposure: Iran War and Gulf shipping uncertainty can raise freight costs, marine insurance premiums and cargo delay risks, pushing buyers to reassess supplier origin, route security and non-Hormuz sourcing options.

- Ethane commercialization is infrastructure-heavy: Producers cannot monetize ethane at scale without gas processing, NGL recovery, fractionation, pipelines, refrigerated storage and export terminals, creating high capital barriers for new entrants.

- Downstream demand cyclicality affects ethane offtake: Ethane demand is tied to ethylene and derivatives such as polyethylene, ethylene glycol and ethylene oxide, making offtake vulnerable to petrochemical oversupply, weak polymer demand and regional cracker utilization cuts.

White Space Opportunities

Areas of white space within the Global Ethane Market include security of supply, import substitution, infrastructure buildup, and ethane/derivative integration. The most compelling area is non-Hormuz ethane supply sourcing from the US Gulf Coast, where Asia-based petrochemical companies that rely on imports seek to diversify their sourcing and protect against route disruption, shipping delays, and cost escalation. This is possible through access to shale-based ethane sources, ethane fractionators, ethane storage, and ethane exports.

Another white space opportunity includes ethane infrastructure buildup in Asia Pacific, where India, China, and South Korea have the potential to consider ethane receiving facilities, ethane source procurement, and modifications to existing ethane crackers for increased feedstock flexibility. There are additional areas of opportunity related to ethane/ethylene derivatives downstream such as the conversion to polyethylene, ethylene glycol, ethylene oxide, and vinyl chloride monomer chains.

Other white spaces in the ethane market relate to bio-ethane and low-carbon ethane positioning for petrochemical companies considering biomass-derived ethane, carbon capture-enabled cracking process modification, and low carbon petrochemical feedstocks.

DMI Opinion

As per DataM, the critical issue facing the Global Ethane Market is not demand generation, but rather the capacity of the suppliers and petrochemical producers to leverage the presence of ethane into feedstock availability through efficient logistics systems. The current market scenario favors players who have a strong presence in all aspects ranging from gas processing to transport ships and storage facilities in order to provide secure delivery channels to customers. This means buyers are now looking beyond low prices, but also taking into account supply security, origin risks, ship availability, flexible terms of contracts and potential disruptions, like the Iran War and Hormuz Blockade.

Cracking economics, feedstock reliability, non-Hormuz sources, increasing freight costs, marine insurance risks and feedstock security are increasingly important parameters for companies dependent upon imported feedstock to build new crackers. Petrochemical companies in Asia, including those from China, India, Japan and South Korea, have started looking at other sources of ethane, which help them reduce their dependence on crude oil-derived feedstock.

Why Choose DataM?

- Ethane Feedstock Economics: Analyzes the competitiveness of ethane versus naphtha, LPG, and propane as cracking feedstocks in terms of margin spreads, feedstock spread economics, ethane recovery economics, and ethane to ethylene economics.

- Hormuz and Geopolitical Risk Assessment: Examines the potential impact of the Iran War and Hormuz Strait disruption on ethane-derived petrochemical supply chain economics, shipping costs, availability, marine insurance, ethane import dependence, and alternative sourcing strategies outside of Hormuz.

- Ethane Trade Intelligence: Monitors ethane shipments, U.S. Gulf Coast export readiness, Asian-Pacific ethane import dependency, Middle East ethane supply risk, and country-level changes in ethane sources for China, India, Japan, South Korea, and Europe.

- Ethane Supply Chain and Logistics: Addresses ethane production, NGL extraction, fractionation, pipeline transportation, cryogenic storage, export facilities, dedicated ethane carrier ships, terminal handling, and integration into steam crackers.

- Application & Derivative Analysis: Correlates ethane demand with ethylene output and related derivative chains involving polyethylene, ethylene glycol, ethylene oxide, vinyl chloride monomer, ethylene dichloride, styrene and alpha olefins.

- Competitive Strategy Benchmarking: Analyses leading players based on their access to ethane, NGL logistics, crackers, export potential, downstream operations, routes, customer base and resilience to supply interruptions.

- Pricing & Contract Analysis: Analyses spot prices, long-term contract prices, captive pricing, ethane rejection economics, escalation of freight costs, exposure to landed cost and import sourcing risks.

- Market Entrant & Growth Support: Assists in market identification, supplier gaps, infrastructure requirements, partnership potential and growth opportunities for petrochemical manufacturers, exporters, importers, midstream operators and investors.

Who Should Buy This Report?

- Ethylene and steam cracker operators: To evaluate ethane-based feedstock economics, cracker margin protection and switching opportunities against naphtha and LPG volatility.

- Integrated petrochemical companies: To assess ethane-to-ethylene value creation, downstream derivative integration and long-term competitiveness.

- Natural gas processors and NGL fractionators: To identify ethane recovery, fractionation, domestic supply and export monetization opportunities.

- Ethane exporters and terminal operators: To track Asia-Pacific and Europe demand, export capacity needs and long-term offtake opportunities.

- Polyethylene, ethylene glycol and ethylene oxide producers: To understand feedstock security, ethylene availability and derivative chain cost competitiveness.

- Procurement and sourcing teams: To manage ethane contracts, vessel availability, freight escalation, supplier reliability and landed-cost exposure.

- Asia-Pacific petrochemical importers: To evaluate non-Hormuz supply options and reduce exposure to crude-linked feedstock volatility.

- Investors and strategy teams: To assess ethane-linked infrastructure, crackers, terminals, shipping assets and petrochemical growth opportunities.

FAQ’s