Enterprise AI Agent Adoption Market Overview

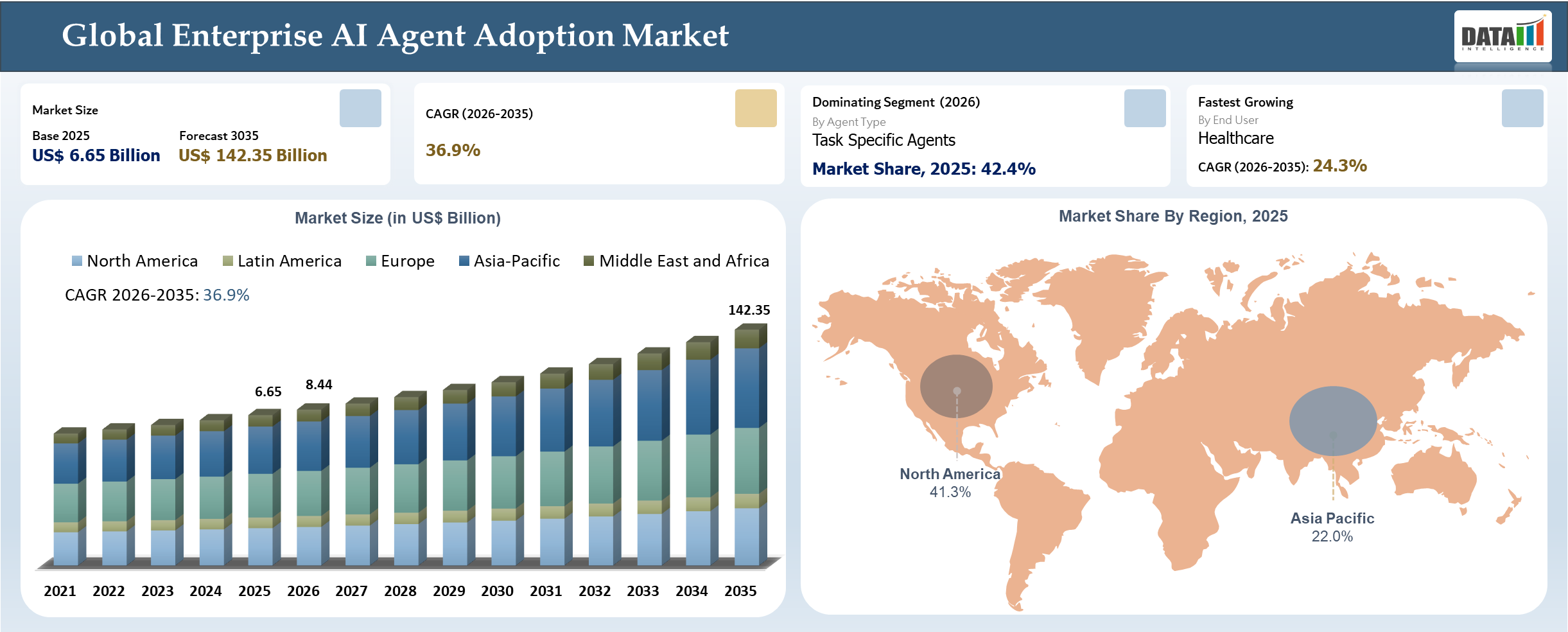

The global Enterprise AI Agent Adoption market reached US$ 6.65 billion in 2025 and is expected to reach US$ 142.35 billion by 2035, growing with a CAGR of 36.9% during the forecast period 2026-2035. The usage of enterprise AI agents is witnessing increasing popularity, as more than 90% of enterprises are adopting solutions based on agents, but less than 25% of enterprises have reached the production deployment stage because of data silos and governance issues. The focus areas for using AI agents include IT operations, customer service, and knowledge management; these areas see tangible benefits in terms of improved efficiency and faster decision-making. The demand for enterprise AI agents because of the rise of multi-agent orchestration platforms and enterprise data systems, allowing seamless interaction with other systems.

Enterprise AI Agent Adoption Industry Trends and Strategic Insights

- Organizations are moving forward to implement AI agents within various areas like IT management, customer service, and accounting, where the results can be measured, but enterprise-wide implementation is being done step-by-step owing to certain challenges.

- Fragmented data systems and legacy architecture have been constraining end-to-end automation, thus making the adoption of unified data systems and orchestration solutions vital in facilitating scalability.

- The market has been witnessing competition from vendors that hold enterprise platforms, making it easy for them to integrate, distribute, and monetize AI agents.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 6.65 Billion | |

| 2035 Projected Market Size | US$ 142.35 Billion | |

| CAGR (2026-2035) | 36.9% | |

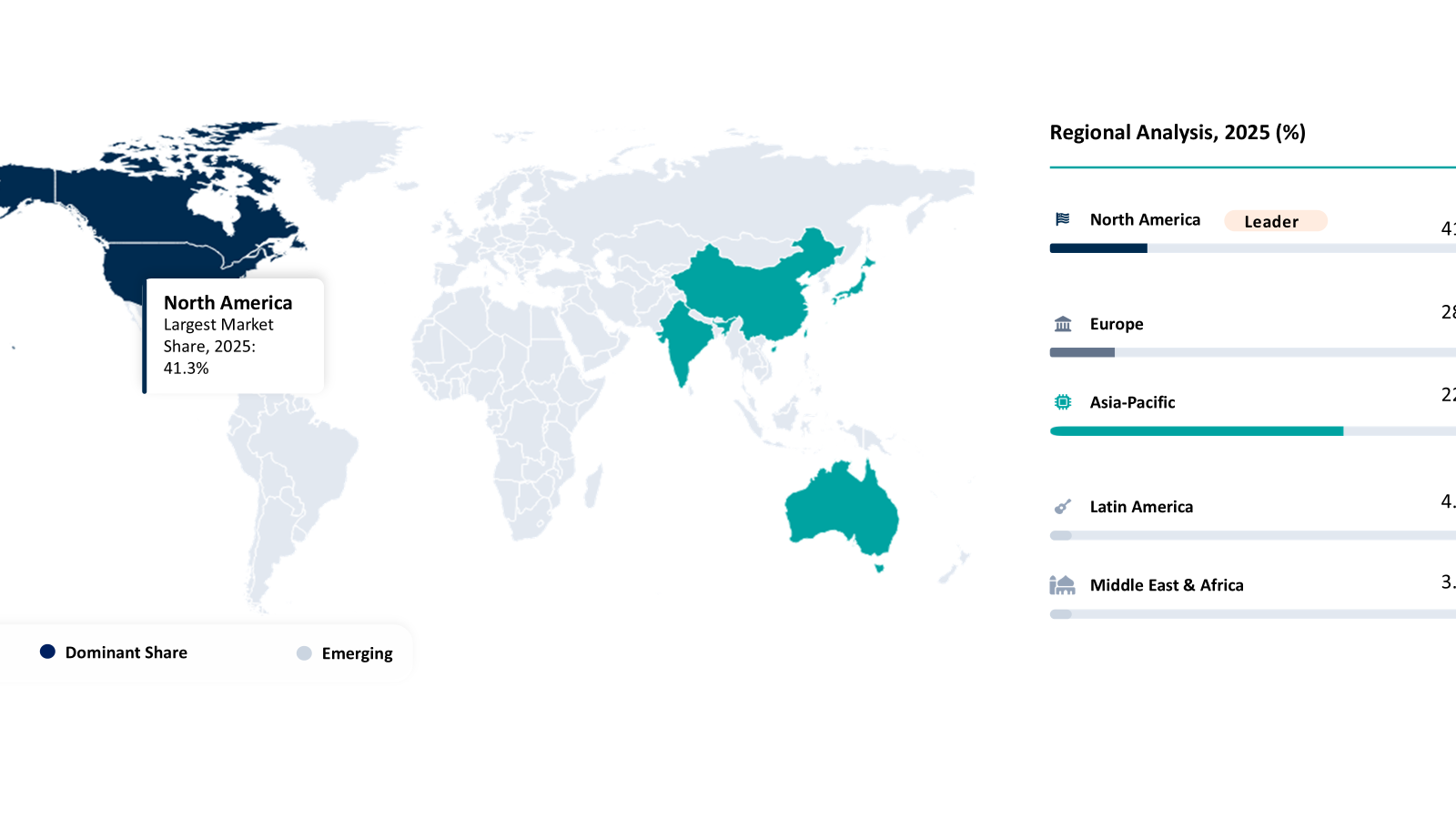

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Agent Type | Task Specific Agents, Workflow Agents, Customer Facing Agents, Developer Agents and Decision Support Agents | |

| By Deployment Model | Cloud and On Premises | |

| By Degree of Autonomy | Semi-Autonomous and Autonomous | |

| By Enterprise Function | Customer Service, IT Operations, Sales, Finance, Human Resources and Procurement | |

| By End User | BFSI, Healthcare, Retail and E-commerce, Manufacturing, Telecom and Public Sector | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

AI Impact Analysis

Innovations in large language models and reasoning engines are transforming the way organizations adopt AI agents by facilitating their ability to go from being mere helpers to executing multi-phase, context-sensitive workflows. The evolution is leading to the increased use of agents in strategic business processes, including IT operations, customer support, and financial management, which allows them to analyze enterprise information, initiate tasks, and finish operations within interconnected systems. Consequently, organizations are moving from pilot AI projects to operational applications motivated by gains in productivity, shortened cycle times, and efficient decision-making.

On the other hand, adoption becomes progressively reliant on data architecture and governance readiness, with agent efficacy relying on having access to integrated, consistent, and secured data ecosystems. The trend is spurring spending on enterprise data platforms, orchestration engines, and controlled deployments, especially private and hybrid cloud environments. Competitive landscape trends are becoming more towards platform-based ecosystems, with vendors integrating their agents within key enterprise applications, allowing scale-up adoption while supporting human-agent partnerships in terms of supervision and regulation.

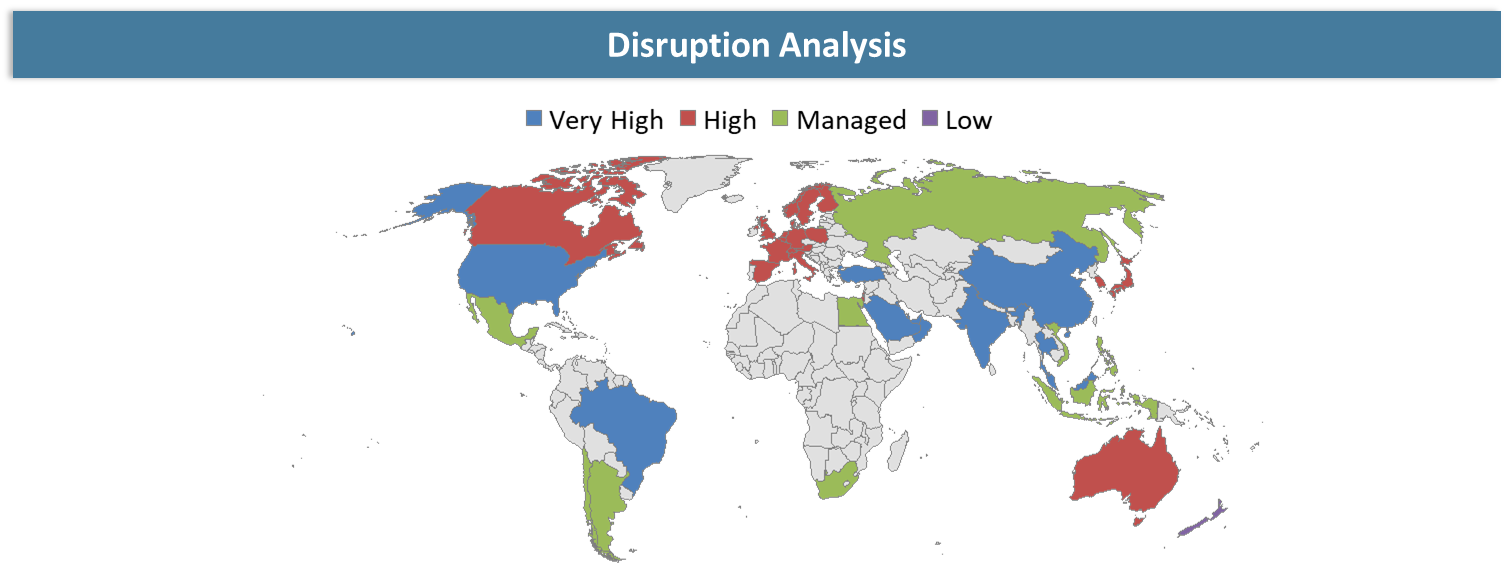

Disruption Analysis

Consolidation of Enterprise Workflows Through Embedded AI Agents

The AI agents embedded within enterprise systems such as CRM, ERP, and ITSM are enabling integration of separate workflows as these agents can perform tasks in multiple modules from one common system environment. Tasks like order processing, answering customer queries, and managing the employee life cycle have been taken over by AI agents, which has reduced the need for using separate SaaS applications.

The disruption is reshaping vendor dynamics, as enterprises prioritize platforms that offer deeply integrated, agent-enabled capabilities over fragmented point solutions. Software providers are being compelled to embed orchestration and execution intelligence directly into their ecosystems, while enterprises are optimizing software spend by eliminating redundant applications and focusing on platforms that deliver end-to-end workflow outcomes.

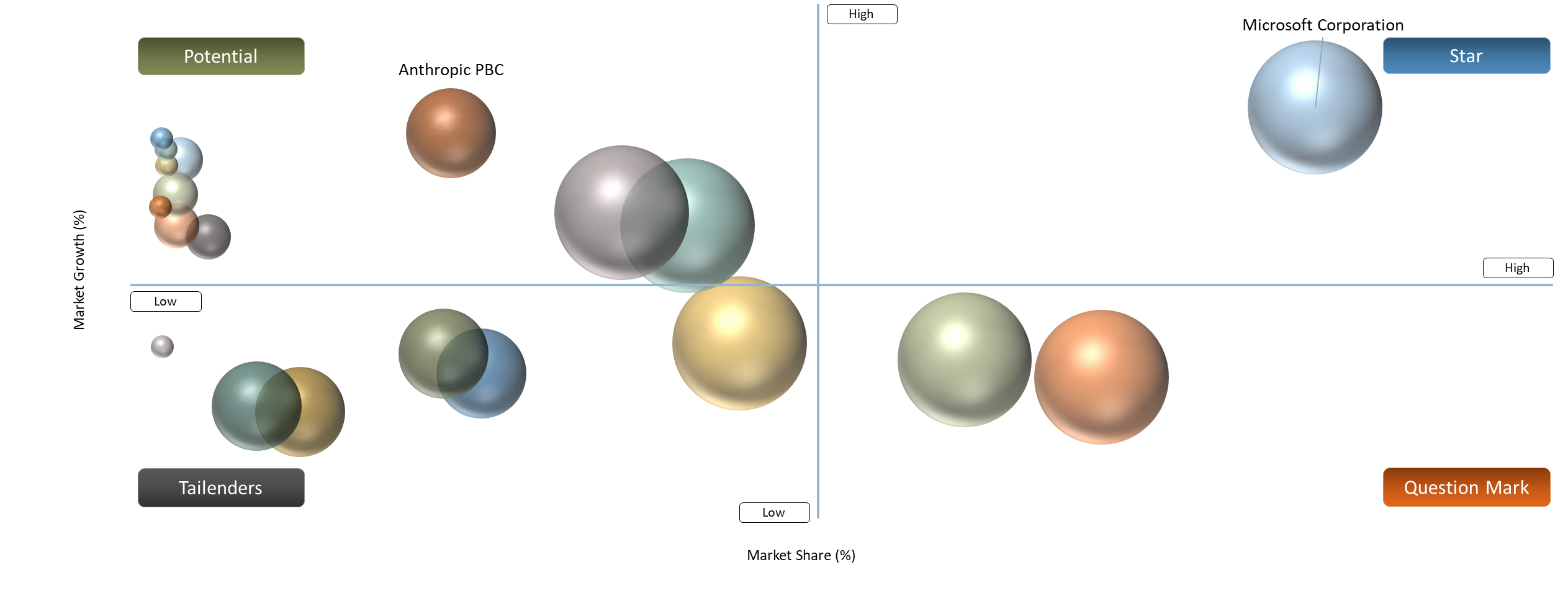

BCG Matrix: Company Evaluation

As per the BCG matrix, the organization employs a platform-centric leadership model where Microsoft Corporation is a definitive Star due to its substantial market share and rapid growth arising from the incorporation of intelligent agents into its cloud and enterprise software suites. Competing players within the same ecosystem like Amazon.com Inc., Alphabet Inc., Salesforce, Inc., and ServiceNow, Inc. are also operating in areas of high growth owing to increased competition in capturing enterprise processes via intelligent agents.

Companies like OpenAI Inc, Anthropic PBC, and Cohere Inc., which are native AI startups, are placed in the “Potential” quadrant. This represents high innovation potential, technological capabilities, and a limited presence among enterprises. The development pathway for such companies is determined by the ability to scale up by means of partnerships, integration into enterprise environments, and participation in ecosystems.

Established enterprise software providers like Oracle, SAP, and IBM are considered Question Marks due to the strength of their installed bases despite ongoing development of their agent approaches, whereas providers like UiPath, Automation Anywhere, Zoom, and HubSpot find themselves among Tailenders since they have yet to make progress towards the transition from existing automated or cloud-based processes. Overall, the matrix reveals that the market is undergoing an evolution towards consolidation based on ecosystem management and operationalizing AI agents.

Market Dynamics

Growing Demand for Intelligent Workflow Automation in Enterprises

The enterprise need for intelligent automation of its workflow is being fueled by the complexity of processes and cost-to-serve factors instead of small efficiency improvements. It is an increase in fragmentation of data and manual work in high-volume processes like IT help desk ticket management, claims processing in BFSI, and order-to-cash processes, resulting in extended lead times and elevated costs. AI agents are being implemented to collapse multistep workflows into a one-step execution process, wherein activities like data access, data verification, decision-making, and task execution are performed in a single process.

Adoption is further driven by the requirement for standardizing execution in the enterprise environment, especially in globally dispersed organizations that have to manage multiple systems and data sources. AI agents help deliver standardized decision-making and on-the-spot execution processes, leading to better service level agreement compliance and fewer mistakes in critical processes. Change in approach is not only driven by automation but rather the overall architecture design, where enterprises reconfigure their business processes based on the abilities of agents.

Data Integration and Quality Challenges Limiting AI Agent Performance

Performance of enterprise AI agents is limited by the fragmentation of data environments, where important data is scattered across various databases, including ERP, CRM, legacy systems, and other sources of data. Poor interoperability and inadequate data pipelines hinder the agents from gaining access to integrated and up-to-date data, thus limiting their effectiveness in performing workflows.

Data quality problems also affect the reliability of AI-based solutions, as problems such as incomplete, out-of-date, or disorganized data can cause inaccuracies in the results. In fact, this issue is especially important in the case of regulated industries, which have higher standards in terms of accuracy and auditability. For this reason, companies invest a lot in integrating various systems that can help maintain consistent data and thus implement AI agents across an entire organization.

Segmentation Analysis

The global Enterprise AI Agent Adoption market is segmented based on agent type, deployment model, degree of autonomy, enterprise function, end user and region.

Rapid Adoption of Workflow Agents for End-to-End Process Automation

Workflow agents are being rapidly adopted as they are capable of automating business process flows that involve multiple steps and multiple systems such as incident management, order handling, and financial processes. Businesses are adopting workflow agents within their IT operations and finance because they have high transaction volumes, resulting in cycle time improvements. Workflow agents do not operate like task-based agents since they perform processes in a single flow through ERP, CRM, and ITSM systems.

The adoption process is being driven by the efforts of companies like Microsoft, ServiceNow, and Salesforce to integrate workflow orchestration within their enterprise application offerings. This trend is driving IT spending towards solutions that provide full process results, and deployments are occurring mainly in areas where automation will improve SLAs and reduce costs.

Geographical Penetration

Platform-Led Scaling of Enterprise AI Agents in North America

North America represents the highest level of adoption of enterprise AI agents due to the high level of investment in enterprise IT infrastructure, mature cloud infrastructure environments, and the integration of data platforms and business application infrastructure. AI agents have been deployed in areas like enterprise IT management, customer support, and enterprise analytics, areas in which the use of AI agents can result in cost savings and more efficient services. The deployment of AI agents is closely associated with the availability of hyperscaler and enterprise software providers.

In addition, the growth in this region is also fueled by a balanced regulatory environment and robust investments from the private sector. Frameworks like NIST’s AI Risk Management are allowing the creation of an organized governance framework without hindering innovation, while investments in AI frameworks are propelling this region from pilot projects to a multi-agent production environment.

US: Enterprise-Driven Adoption with Platform Dominance

AI agent implementation is most prominent in the US because of significant enterprise-level requirements and the dominant role of platform vendors such as Microsoft, AWS, and Salesforce. AI agents are being incorporated within enterprise processes for workflow automation such as IT incident handling, customer engagement, and finance processes. The implementation of AI agents has been observed in key sectors such as BFSI, health care, and retail. Availability of enterprise data and advanced cloud infrastructure facilitates the use of multi-agent systems.

The investment intensity continues to serve as an important point of differentiation, with firms based in the United States setting aside considerable amounts of money for their companies' transformations through AI, as well as being guided by the U.S. government's position on AI governance and risk management.

Canada: Governance-Led Adoption with Gradual Enterprise Scaling

AI agent adoption by Canadian enterprises is defined by a research-based and policy-driven approach that is slowly being implemented in enterprises. The federal government’s actions in the Pan-Canadian Artificial Intelligence Strategy, together with the contributions of organizations like CIFAR, have improved Canada’s AI innovation skills, but its commercialization occurs steadily. The application of AI agents in businesses in industries like financial services, health care, and public sector services mainly takes place in areas that involve dealing with customers, handling documents, and ensuring adherence to policies.

The adoption trends are driven by the need for robust data management practices and reasonable corporate IT budgets that prefer reliability over scalability. Enterprises are making use of secure data management systems along with regulated deployment practices, most often using private and hybrid cloud infrastructures. It leads to gradual growth in the use of AI agents while preferring secure implementation over rapid adoption.

Competitive Landscape

- The leading players in the Enterprise AI Agent Adoption market include platform-focused technology vendors like Microsoft Corporation, Amazon.com, Inc., and Alphabet Inc. The key strengths of these companies include their robust cloud architecture, powerful data ecosystem, and enterprise application integration that support the implementation of AI agents. The organizations have expertise in orchestration systems, integration with large language models, and enterprise security that allows them to integrate AI agents into various processes in areas such as IT operations, customer interactions, and business process management.

- Salesforce, Inc., ServiceNow, Inc., Oracle Corporation, and SAP SE are other prominent companies that play a vital part in helping businesses adopt AI technology by ensuring application layer integration and incorporating AI agents into the CRM, ERP, and ITSM systems. Alongside this, AI-native and data platform companies like OpenAI, Inc., Anthropic PBC, and Databricks, Inc. are working on developing advanced models and AI agents, whereas AI-based automation companies like UiPath Inc. and Automation Anywhere, Inc. are shifting towards building automation based on agents. The strategic emphasis among all firms is centered around platform growth, ecosystem partnerships, and multi-agent integration.

Key Developments

- March 2026 - Accenture has partnered with Databricks to expand its existing collaboration, in order to speed up the adoption of artificial intelligence agents by creating specific infrastructure, AI agent development capabilities, and a specialized team for business. This will allow enterprises to transition from pilot testing to actual implementation in solving data, scale, and governance issues in AI agents.

- April 2026 - Adobe and AWS have entered into a partnership to enable enterprises to adopt agentic AI technology faster through a seamless process that allows enterprises to create, deploy, and manage their AI agents in their marketing and customer experiences workflows. The project leverages integration among the services offered by both companies’ solutions such as Adobe Experience Platform Agent Orchestrator and Amazon Bedrock AgentCore.

- April 2026 - Adobe launched the CX Enterprise solution, which is an agentic AI platform aimed at automating marketing processes through AI agents, agent skills, and orchestration abilities. The incorporation of an AI coworker brings about agentic AI capabilities and makes it possible for businesses to move from trying out AI applications to using AI for specific business outcomes in customer engagement and marketing activities.

- October 2025 - The AI Agent Marketplace was introduced by Oracle in its Oracle Fusion Cloud Applications to enhance the use of AI agents by facilitating the effortless integration of AI agents developed by partners into enterprise applications that are critical to functions such as accounting, human resource management, and supply chain management. The platform incorporates the capabilities of AI agents into enterprise processes without coding, security standardization, and ecosystem collaboration.

- April 2025 - Google developed Agentspace to boost the integration of AI agents into enterprises by providing capabilities for unified enterprise search, no-code agent construction, and the implementation of pre-constructed agents. The system integrates multimodal AI features along with data from the enterprise itself in order to facilitate the ability for employees to search for, analyze, and leverage data effectively.

Why Choose DataM?

- Technological Innovations: Explores advancements in agentic AI architectures, including multi-agent systems, orchestration frameworks, LLM integration, and no-code/low-code agent development platforms, enabling scalable automation and intelligent decision-making across enterprise environments.

- Product Performance & Market Positioning: Evaluates how leading players differentiate through agent accuracy, reasoning capabilities, integration depth, latency, and scalability, highlighting competitive positioning across enterprise applications such as CRM, ERP, ITSM, and data platforms.

- Real-World Evidence: Highlights enterprise deployments of AI agents across customer service, IT operations, marketing, and finance, demonstrating measurable improvements in productivity, workflow efficiency, and decision speed.

- Market Updates & Industry Changes: Tracks developments such as strategic partnerships, agent marketplaces, platform integrations, and increasing enterprise investments in agentic AI, along with regulatory and governance advancements shaping adoption.

- Competitive Strategies: Analyzes how key companies expand through ecosystem partnerships, platform integration, multi-agent capabilities, and vertical-specific solutions, driving enterprise-scale adoption and differentiation.

- Pricing & Market Access: Explains pricing models based on subscription, API consumption, and usage-based billing, along with enterprise access strategies through cloud platforms, SaaS integration, and partner ecosystems.

- Market Entry & Expansion: Identifies growth opportunities driven by enterprise automation demand, digital transformation initiatives, and AI-led productivity gains, with expansion strategies focused on scalable deployment, cross-functional integration, and industry-specific use case development.

Target Audience

- Enterprise Software Providers (CRM, ERP, ITSM): Companies integrating AI agents into core enterprise applications to enhance automation, decision-making, and workflow efficiency across business functions.

- Cloud Service Providers and Hyperscalers: Organizations offering AI infrastructure, agent frameworks, and platform services to enable scalable deployment of enterprise AI agents.

- AI Platform and Model Providers: Companies developing LLMs, agent frameworks, and orchestration tools that power enterprise-grade AI agents and multi-agent systems.

- System Integrators and Consulting Firms: Service providers supporting enterprises in deploying, customizing, and scaling AI agents across workflows, ensuring integration with legacy systems and governance frameworks.

- Data and Analytics Platform Providers: Organizations enabling unified data environments and real-time data access, critical for training, deploying, and optimizing AI agents.

- Automation and Workflow Solution Providers: Vendors offering RPA, intelligent automation, and orchestration platforms that are evolving toward agent-driven workflow execution.

- Investors & Private Equity Firms: Entities investing in AI agent platforms, enterprise AI startups, and ecosystem players driven by rapid adoption and scalability potential.

- Developer Ecosystem and Technology Partners: Independent developers, ISVs, and technology partners building, customizing, and distributing AI agents through marketplaces and enterprise platforms.