Endocardiography Market Size

The global endocardiography market stood at US$ 2.14 billion in 2025 and is expected to reach US$ 4.2 billion by 2035, growing with a CAGR of 7.2% during the forecast period 2026-2035.

The global endocardiography market is being impacted by the swift move from traditional 2D intracardiac visualization towards artificial intelligence-based 3D and 4D procedural guidance technologies. Such an adoption is critical in view of growing complexity in cardiology interventional procedures like atrial fibrillation ablation, left atrial appendage closure, transseptal access, and structural heart procedures, which call for better anatomical visualization, faster decision-making, and enhanced catheter manipulation. FDA approval for Siemens Healthineers' ACUSON Origin cardiovascular ultrasound system with the AcuNav Lumos 4D ICE Catheter was received in August 2024, demonstrating the adoption of artificial intelligence-based ultrasound with 4D ICE.

Buyers have to make a purchase since endocardiography is not an optional accessory but rather an instrument for enabling procedures and providing the physician with improved decision-making, reduced reliance on fluoroscopy, and assistance in performing minimally invasive interventions. The use of VeriSight Pro 3D ICE Catheter by Philips as a first case in Europe in 2025 further demonstrates that there is increasing adoption of real-time 3D intracardiac imaging in structural heart procedures. Healthcare facilities that utilize advanced ICE platforms may achieve greater workflow efficiency and improved capabilities, thus enhancing their market position in premium cardiology procedures.

Key Takeaways

- The global endocardiography market was valued at US$ 2.14 billion in 2025 and is projected to reach US$ 4.2 billion by 2035.

- The market is expected to grow at a CAGR of 7.2% during the forecast period 2026-2035.

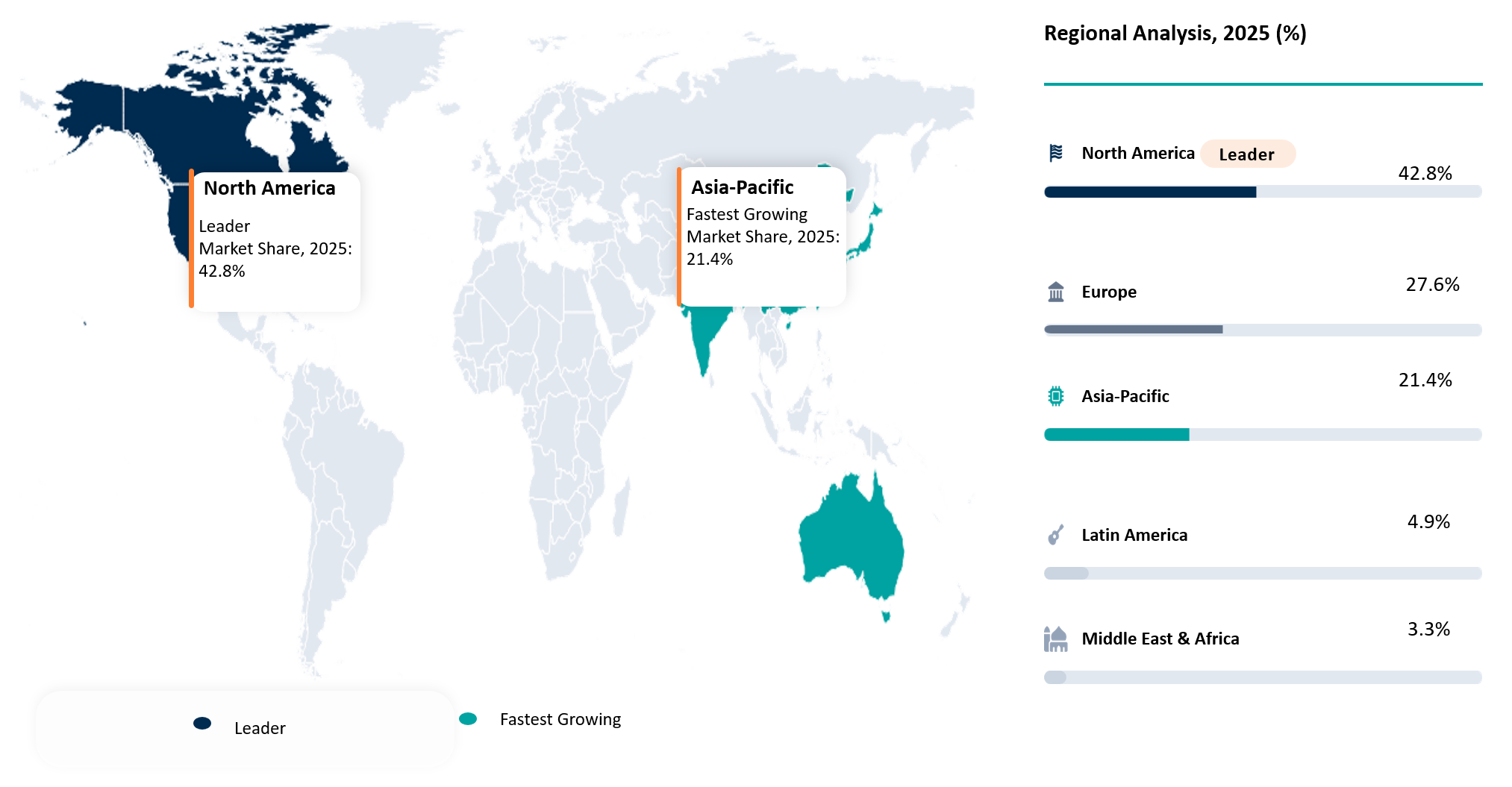

- North America held the highest market share at 42.8% in 2025, valued at approximately US$0.92 billion, supported by advanced EP labs, structural heart programs, and early adoption of ICE catheters.

- Europe accounted for around 27.6% market share in 2025, valued at approximately US$0.59 billion, driven by strong cardiac imaging infrastructure and structural heart intervention adoption.

- Asia-Pacific held approximately 21.4% market share in 2025, valued at around US$0.46 billion, and is expected to be the fastest-growing region due to expanding cardiac centers and rising minimally invasive procedures.

- Intracardiac Echocardiography Catheters were the largest product type segment in 2025, accounting for around 54.7% share, valued at approximately US$1.25 billion.

- 2D Intracardiac Echocardiography dominated the imaging technology segment in 2025 with an estimated 43.6% share, supported by broad physician familiarity and established EP procedure use.

- Single-Use Catheters led the catheter configuration segment in 2025 with approximately 61.3% share, supported by sterility requirements and recurring hospital procurement demand.

- Electrophysiology Procedure Guidance was the largest application segment in 2025 with nearly 38.9% share, driven by AF ablation, catheter navigation and transseptal access workflows.

- 3D and 4D Real-Time Intracardiac Echocardiography is projected to be the fastest-growing technology segment through 2035, supported by demand for advanced visualization, AI-assisted imaging and complex structural heart guidance.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 2.14 Billion | |

| 2035 Projected Market Size | US$ 4.2 Billion | |

| CAGR (2026-2035) | 7.2% | |

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Product Type | Intracardiac Echocardiography Catheters, Imaging Consoles and Workstations, Imaging and Procedure Guidance Software, Accessories and Consumables, and Others | |

| By Imaging Technology | 2D Intracardiac Echocardiography, 3D Intracardiac Echocardiography, 4D Real-Time Intracardiac Echocardiography, Doppler-Based Intracardiac Imaging, Phased-Array Intracardiac Imaging, Rotational Intracardiac Imaging, and Others | |

| By Catheter Configuration | Single-Use Catheters, Reusable Catheters, Steerable Catheters, Non-Steerable Catheters, Forward-Looking Catheters, Side-Looking Catheters, and Others | |

| By Application and Use Cases | Electrophysiology Procedure Guidance, Structural Heart Procedure Guidance, Transseptal Access Guidance, Ablation Guidance, Device Deployment Guidance, Intracardiac Anatomy Visualization, Thrombus and Pericardial Effusion Detection, Procedure Complication Monitoring, and Others | |

| By Disease Area | Atrial Fibrillation, Ventricular Arrhythmia, Structural Heart Disease, Valvular Heart Disease, Congenital Heart Disease, Thromboembolic Risk Conditions, and Others | |

| By End User | Hospitals, Specialty Cardiology Centers, Ambulatory Cardiac Procedure Centers, Academic and Research Institutes, and Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Real-Time Intracardiac Guidance Is Disrupting Conventional Cardiac Intervention Workflows

Disruption in the Global Endocardiography Market stems from the replacement of traditional fluoroscopy and external imaging with real-time catheter-based intracardiac visualization systems. More hospitals and cardiac centers are adopting endocardiography in order to increase the accuracy of catheter interventions in electrophysiology and structural heart diseases, such as atrial fibrillation ablation, transseptal crossing, LA appendage closure, and valve interventions. In doing so, endocardiography ceases to be an auxiliary visualization technology but becomes the backbone of catheter-based procedures.

Another disruptive trend within the market concerns the development of 3D and 4D ICE, AI-enhanced visualization, and catheter navigation-mapping systems. Instead of competing based solely on the image quality offered by their equipment, vendors now compete in terms of workflow integration, catheter handling, efficiency of procedures, user-friendly interface, and cost-per-procedure. The adoption of safer, faster, and more precise minimally invasive cardiac interventions is expected to give a competitive edge to ICE vendors offering high-quality catheters and innovative AI technologies.

BCG Matrix: Company Evaluation

The BCG Matrix analysis of the Endocardiography Market indicates that the market structure for intracardiac imaging involves some level of consolidation where some direct intracardiac imaging competitors have better strategic positioning while many adjacent companies drive procedural requirements. The Stars in this context are Siemens Healthineers, Johnson & Johnson MedTech, Abbott, Koninklijke Philips N.V. and Boston Scientific Corporation for being relevant directly in ICE catheters, cardiac imaging, EP procedures and support of structural heart procedures. GE HealthCare, Medtronic and Edwards Lifesciences Corporation are Cash Cows because of strong cardiovascular portfolios, good hospital relationships and established procedural infrastructure. The other adjacent players are Stryker, EnChannel Medical Ltd., Stereotaxis and Baylis Medical Technologies Inc. as being able to grow either through reprocessing, EP mapping, robotics navigation or transseptal access without having much direct involvement in ICE technology yet. Merit Medical Systems, Cook and Atricure, Inc. are Niche Players in the market.

Market Dynamics

Rising Adoption of Image-Guided Cardiac Interventions Across EP and Structural Heart Procedures

The growing acceptance of image-guided cardiac interventions is one of the key factors fueling the growth of the Endocardiography Market. Hospitals are increasingly moving towards performing procedures that require real-time visualization inside the heart chamber, better catheter handling and improved accuracy. During electrophysiological procedures like atrial fibrillation ablation, ventricular arrhythmia therapy, and other catheter-based complex procedures, endocardiography can help cardiologists visualize the heart anatomy and guide catheter placement within the chamber along with monitoring any complication during the procedure. In structural heart intervention procedures like trans-septal crossing, left atrial appendage occlusion, septal defects repair and valvular intervention procedures, it provides support for device placement without being completely reliant on fluoroscopy alone. This becomes increasingly essential since cardiac procedures have now become complex, minimally invasive and goal-oriented. For hospitals and cardiac facilities, endocardiography is definitely a value add during the procedure. This is evident with the increasing scope of Electrophysiology laboratories.

Limited Adoption in Cost-Sensitive Hospitals and Emerging Healthcare Systems

Adoption constraints in cost-conscious hospitals and emerging healthcare delivery systems continue to act as the critical factor affecting the Endocardiography Market, considering that endocardial imaging devices tend to involve costly investments, recurrent catheter expenses, and require skilled personnel. Indeed, many institutions in developing countries find it convenient to use traditional imaging assistance technologies like fluoroscopy and transesophageal echocardiography owing to their availability, familiarity among doctors and low operating costs. The use of specialized catheters and single-use products increases the procedure’s overall costs, thereby complicating efforts by smaller hospitals and cardiac centers to adopt the technology. Furthermore, lack of adequate reimbursement and funding may lead to delayed purchases even in cases where the clinical value of the innovation has been identified. This leads to delayed adoption in hospitals and health care delivery settings other than the premium cardiac centers.

Segmentation Analysis

The Global Endocardiography Market is segmented based on product type, imaging technology, catheter configuration, application and use cases, disease area, end user, and region.

Intracardiac Echocardiography Catheters Anchor Market Revenues as Procedure Volumes Shift Toward Real-Time Cardiac Guidance

The intracardiac echocardiography catheters have become a major product in the Endocardiography market as they are the most significant revenue generators which involve the use of catheters inside the heart. The usage of these catheters is significantly driven by the need for atrial fibrillation ablation, transseptal access, left atrial appendage (LAA) closure, and other valve procedures that involve catheter navigation workflows wherein the visualizing process of the procedure is essential. The segment is commercially lucrative as most ICE catheters are considered single-use catheters, providing recurring revenue for manufacturers and a definite need for hospitals. There have been recent advances in this product that will help boost its commercial appeal; in August 2024, Siemens Healthineers obtained FDA clearance of the AcuNav Lumos 4D ICE Catheter to provide 4D intracardiac imaging capabilities. In May 2025, Johnson & Johnson MedTech rolled out its SOUNDSTAR CRYSTAL Ultrasound Catheter in the US for cardiac ablation procedures.

Geographical Penetration

North America Leads Endocardiography Adoption as Advanced EP and Structural Heart Infrastructure Accelerates Intracardiac Imaging Demand

The North American region is projected to continue its dominance in the global Endocardiography Market due to wide acceptance of sophisticated electrophysiology and cardiac structural procedures performed in the United States and Canada. The North American region is favored by its high volume of procedures performed, well-established cath labs and electrophysiology laboratories, fast adoption of intracardiac echocardiography catheters, and more purchasing power among major hospitals. The prevalence of atrial fibrillation is expected to be a critical demand stimulant since according to CDC, about 12.1 million people in the United States will be affected by AFib by 2050, requiring regular ablation, image, and mapping-guided cardiac procedures.

Furthermore, North America is characterized by solid expenditure in cardiac care spending. According to the CMS, in 2024, hospital spending in the USA reached US$1,634.7 billion, and physicians & clinical spending amounted to US$1,109.7 billion. This spending will fuel investments in premium cardiac procedures. Moreover, North America's domination is fueled by the presence of top ICE and cardiac imaging vendors, fast regulatory clearance, higher adoption rates of intracardiac imaging among physicians, and increasing preferences for real-time guidance in atrial fibrillation ablation procedures, LAA closure, and transseptal and structural heart procedures.

U.S Endocardiography Market Trends

The U.S. Endocardiography Market is experiencing increased momentum in 2024-2026 due to changes in workflows for cardiac interventions to include real-time intracardiac visualization and AI-enabled imaging alongside integrated EP mapping. For instance, according to recent statistics, there were 919,032 deaths from cardiovascular disease in the U.S. alone in 2023, which equals 1 death out of 3 recorded cases. Additionally, the Center for Disease Control estimated that the costs associated with health care and medications for treating heart disease amounted to more than US$168 billion in 2021-2022.

Furthermore, several recently approved products provide evidence of increased uptake of endocardial diagnostic equipment in the country. Thus, Siemens Healthineers obtained FDA clearance for its products called ACUSON Origin and AcuNav Lumos 4D ICE Catheter in August 2024 and enhanced AI-based cardiovascular imaging along with 4D intracardiac echography. In May 2025, Johnson & Johnson MedTech launched SOUNDSTAR CRYSTAL Ultrasound Catheter that is characterized by an 88-element phased linear array and CARTO 3 integration for cardiac ablation. Clearly, the U.S. market will move towards advanced ICE platforms used for atrial fibrillation ablation, structural heart interventions, and minimally invasive operations.

Japan Endocardiography Market Outlook

Japan is likely to emerge as a strategically vital market for endocardiography owing to its aged populace and robust cardiovascular care system. As per estimates, more than 36.24 million people in Japan belonged to the ages of 65 and above accounting for nearly 29.3% of the population in the country as on October 2024. The demographic dynamics of Japan make the market relevant for endocardiology as the aging process is associated with an increase in conditions such as atrial fibrillation, valvular heart diseases and structural heart diseases.

Japan's cardiac diseases' burden augments the case for cardiac interventional procedures in the country. Vital statistics in the country track deaths, death rate and adjusted mortality rate from heart diseases, by disease type. Also, the Japanese ecosystem provides for a robust TAVR and valve procedures platform via its Japan Transcatheter Valve Therapies registry. Japan will continue to be an important market for intracardiac imaging in electrophysiology procedures, trans-septal access and valve interventional procedures owing to its well-developed infrastructure comprising of premier hospitals and cath laboratories along with physicians' expertise with regard to the usage of precision cardiac solutions.

Competitive Landscape

The Endocardiography market is moderately concentrated, where competition emanates from the direct intracardiac imaging sector and ICE players such as Siemens Healthineers, Johnson & Johnson MedTech, Abbott, Koninklijke Philips N.V., and Boston Scientific Corporation. The positioning of such firms is significantly boosted due to their direct involvement in intracardiac echocardiography catheters, imaging systems, guidance for electrophysiology procedures, and structural heart interventional solutions. GE Healthcare boosts competition due to its cardiological imaging ecosystem, and Stryker enhances competition through reprocessing of catheters, contributing towards cost-efficiency and sustainable practices in hospitals.

The competitive environment also encompasses companies like EnChannel Medical Ltd., Medtronic, Stereotaxis, Merit Medical Systems, Cook, Edwards Lifesciences Corporation, Atricure, Inc., and Baylis Medical Technologies Inc. Such companies may not necessarily be directly competing in endocardial imaging devices; however, they contribute to competition through mapping, ablation, transseptal access, left atrial appendage (LAA) treatments, valve interventions, robot guidance, and catheter solutions for cardiac procedures. Competing firms are gradually evolving from imaging-focused solutions towards integrated procedural environments that include navigation, mapping, imaging, and delivery of devices.

Recent Developments

- April 2026: Johnson & Johnson MedTech announced the CARTOSOUND SONATA Module, using AI with the CARTO System to transform ICE images into detailed heart-chamber maps and automatically label cardiac structures, strengthening AI-assisted endocardiography workflows.

- August 2025: Koninklijke Philips N.V. highlighted its VeriSight Pro 3D Intracardiac Echocardiography Catheter at ESC 2025, supporting real-time 2D and 3D intracardiac imaging for electrophysiology and structural heart procedures.

- June 2025: Koninklijke Philips N.V. completed the first European procedures using VeriSight Pro 3D ICE Catheter in Germany, strengthening real-time intracardiac imaging adoption in minimally invasive structural heart interventions.

- May 2025: Johnson & Johnson MedTech launched SOUNDSTAR CRYSTAL Ultrasound Catheter in the U.S., improving 2D intracardiac echocardiography image clarity for cardiac ablation procedures and integrated EP workflows.

- March 2025: LUMA Vision received FDA clearance for the VERAFEYE Imaging Catheter and VERAFEYE Imaging System, expanding intracardiac and intraluminal visualization capabilities for cardiac and great vessel anatomy.

- August 2024: Siemens Healthineers received FDA clearance for the ACUSON Origin cardiovascular ultrasound system and AcuNav Lumos 4D ICE Catheter, strengthening AI-enabled cardiovascular imaging and 4D ICE procedure guidance.

- June 2024: Johnson & Johnson MedTech received FDA clearance for NUVISION Ultrasound Catheter and NUVISION NAV Ultrasound Catheter, supporting intracardiac and intraluminal visualization during cardiac interventional percutaneous procedures.

AI Impact Analysis

AI is anticipated to greatly boost the Endocardiography Market by converting intracardiac imaging technology into a more intelligent solution for procedural navigation purposes. In complicated EP and structural heart cases, AI can help enhance image quality, automatically recognize cardiac anatomy, enable chamber mapping, and assist doctors during real-time decision-making. This is extremely important in cases like atrial fibrillation ablation, transseptal puncture, LAA closure, and heart valve interventions, when precise catheter placement and device delivery become crucial factors.

In terms of hospitals, AI-equipped endocardiography can assist them in decreasing procedure duration, ensuring workflow consistency, minimizing the need for manual image interpretation, and making minimally invasive procedures safer. As for manufacturers, AI offers differentiation potential via superior software solutions, mapping technologies, automation of anatomy recognition, and premium imaging platforms. Nevertheless, the implementation of AI will require clinical proof, regulatory approval, physician trust, proper data integration, and cath lab/EP lab compatibility. AI is set to change competition in the market towards more intelligent cardiac procedure ecosystems.

White Space Opportunities

There are numerous opportunities in the Endocardiography Market for white spaces as there is a shift towards real time, image-guided and minimally invasive cardiac procedures. There is huge potential in AI-assisted intracardiac imaging in which automation in recognizing heart anatomy, image enhancing capabilities and procedure guiding capabilities can enhance the confidence of cardiologists performing EP and structural heart interventions. 3D and 4D endocardiography has still not tapped the market in procedures like LAA closure, transseptal access, valve interventions and congenital heart defects. Cost efficient catheter designs is another lucrative area for companies to venture into, like making single-use catheters optimized and offering reprocessing services to hospitals that are struggling with high cost per catheter use. Developing countries present huge potential in developing premium cardiac centers with EP lab and structural heart intervention facilities in the APAC, LATAM and MEA regions. Differentiation can be made by offering an all-in-one package of ICE, Mapping and Navigation solutions to hospitals for fluoroscopy reduction and efficient workflows.

DMI Opinion

DMI sees that the Endocardiography Market will progress from an intracardiac visualization niche market to a procedural guidance market in advanced cardiology. The major growth in the market will be realized from EP and structural heart sites, where clinicians demand imaging in order to perform ablation, trans-septal access, left atrial appendage closure, and valve interventions. Although there has been penetration in top hospitals owing to the cost of catheters and systems, the clinical demand for safe, fast, and accurate minimal invasive procedures will drive further market growth. Manufacturers who develop ICE catheters integrated with AI visualization, 3D and 4D imaging capability, as well as mapping systems, will have more advantages in their competition. In addition, DMI predicts that cost-efficient catheters, reprocessing, and growth in emerging markets will generate growth prospects in the market.

Why This Report Matters in 2026?

In 2026, the global endocardiography market will be more strategic due to the evolution of the role of cardiac imaging from providing basic imaging support to enabling procedural guidance for procedures done using catheter. Growing number of electrophysiology cases, atrial fibrillation ablation, transseptal access, left atrial appendage closure, and structural heart interventions means hospitals, electrophysiology laboratories and cardiac centers have to invest in advanced catheter-based imaging tools to improve catheter navigation, device deployment, and complication detection as well as guide decision making.

Also, more buyers are demanding 3D and 4D intracardiac imaging, artificial intelligence-based visualization, comprehensive mapping system, and efficient catheter system. They now look for more visibility in the quality of imaging, usability of catheters, applicability to procedures, cost effectiveness, reimbursement capability, training needs and workflow efficiency in relation to EP procedures and structural heart interventions. This study will be useful in identifying trends in demand, technologies of high relevance, most promising applications, and leading companies in the evolving endocardiography market environment.

Why Choose DataM?

- Procedure-Level Market Intelligence: DataM provides detailed insights across EP procedures, structural heart interventions, transseptal access, ablation guidance and device deployment workflows, helping clients understand where endocardiography demand is actually scaling.

- Commercially Feasible Segmentation: Our segmentation is built around measurable revenue pools such as product type, imaging technology, clinical use cases, disease areas and end users, reducing overlap and improving market-sizing accuracy.

- Competitive and Ecosystem Mapping: DataM tracks both direct ICE/endocardiography players and adjacent cardiac intervention companies across imaging, mapping, navigation, ablation, access and structural heart ecosystems.

- Decision-Ready Strategic Add-Ons: Clients receive actionable insights such as BCG matrix, white space opportunities, AI impact analysis, recent developments, market dynamics and procurement priorities to support business planning.

- Client-Specific Growth Support: DataM helps companies identify high-growth procedure areas, priority geographies, potential partners, emerging technologies and commercialization opportunities across the evolving endocardiography market.

Key Procurement Priorities and Buyer Evaluation Criteria

- Buyers in the Global Endocardiography Market are increasingly prioritizing providers that can deliver high-resolution intracardiac imaging, real-time procedural guidance, reliable catheter performance and seamless integration across EP and structural heart workflows.

- Procurement decisions are shifting from standalone imaging catheters toward integrated cardiac procedure ecosystems that combine ICE catheters, imaging consoles, 3D and 4D visualization, electro-anatomical mapping, ablation guidance, navigation support and procedure documentation.

- Hospitals, EP labs, structural heart centers and specialty cardiology centers are evaluating vendors based on image clarity, catheter maneuverability, compatibility with existing cath lab infrastructure, procedure efficiency, physician usability, training support, reimbursement fit and total cost per procedure.

- Vendors with strong capabilities in AI-assisted imaging, 3D and 4D ICE, mapping integration, single-use catheter economics, workflow automation and procedure-specific cardiac guidance are better positioned to win long-term hospital contracts as buyers move toward precision-led minimally invasive cardiac interventions.