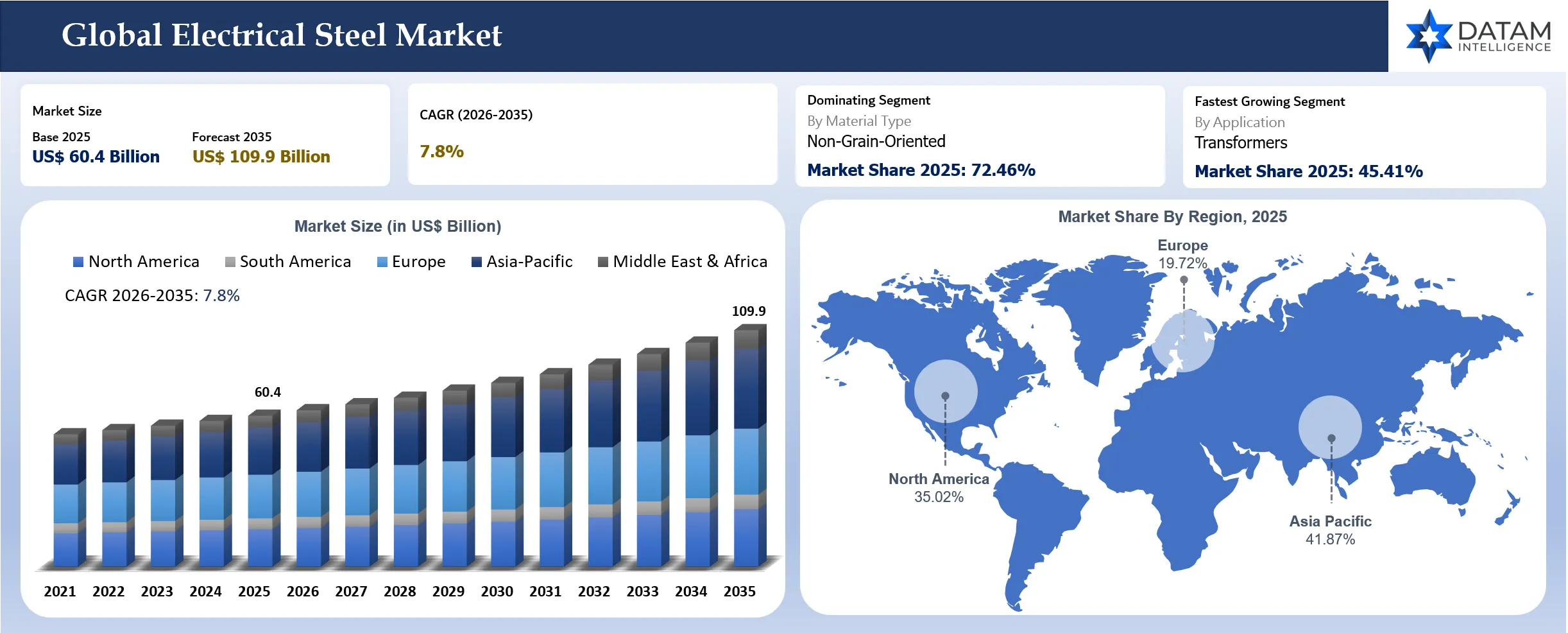

Electrical Steel Market Size

The global electrical steel market reached US$ 60.4 billion in 2025 and is expected to reach US$ 109.9 billion by 2035, growing with a CAGR of 7.8% during the forecast period 2026-2035. Electrical steel has become an important component in transformers, electric motors, generators, and other power equipment due to its good magnetic characteristics and energy savings potential. The fast development of power transmission lines has led to increased consumption of grain oriented electrical steel (GOES), while the transport electrification process results in growing consumption of non-grain oriented electrical steel (NGOES).

Countries such as China, India, the United States, Japan, and Germany, are increasing the production of transformers and developing their transmission grids in order to integrate renewable energy and increase electricity consumption. Manufacturers are making significant investments in securing the supply chain for electrical steel because demand is exceeding the current capacity of high-quality products.

On the other hand, there are still many infrastructure investments that involve steel-heavy projects, while increased industrial automation, data centers, more efficient electric motors, and electrification of transportation are driving the continuous need for more electrical steels. Thus, electrical steel becomes an important part of the steel group that plays a key role in the energy transition and electrification.

Key Takeaways

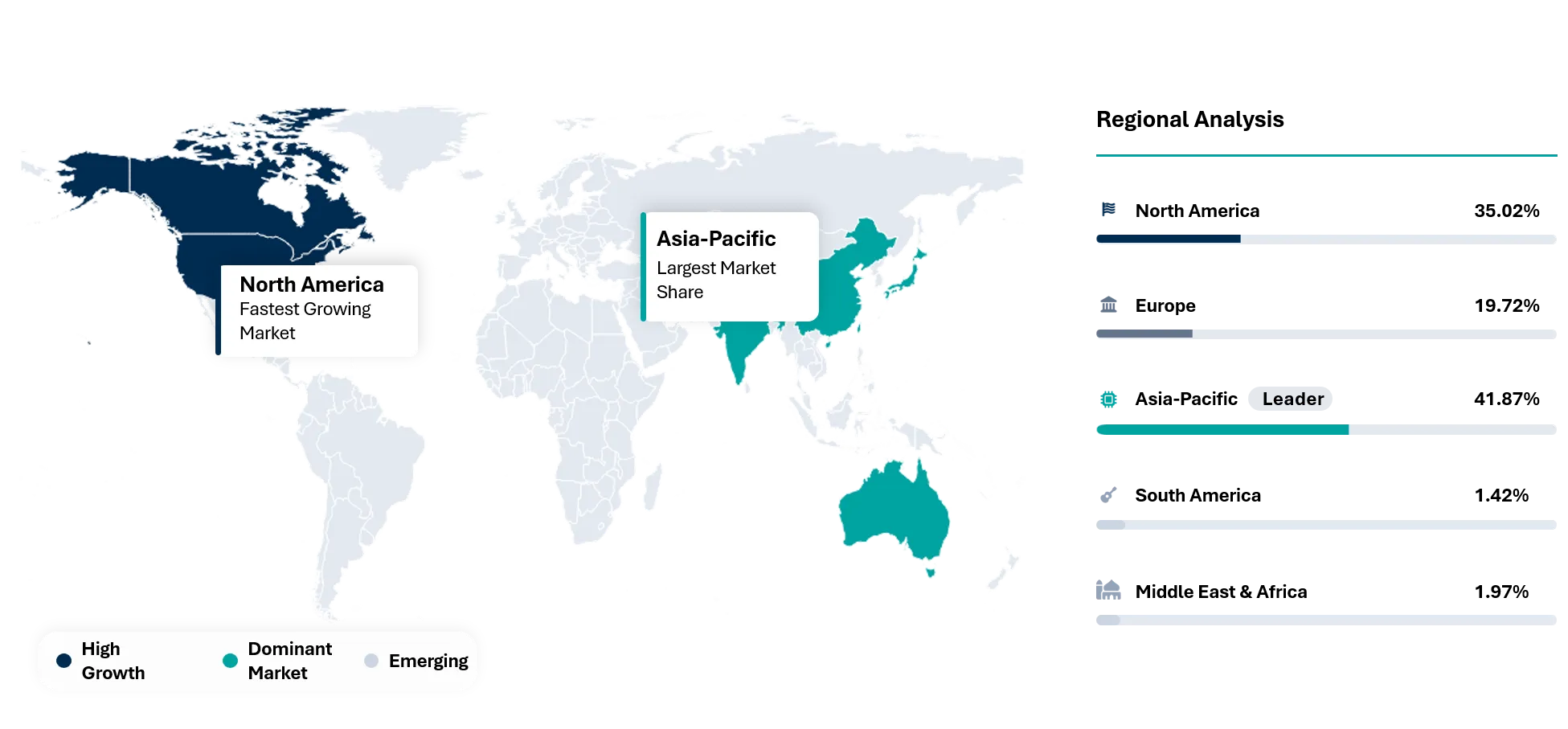

- Asia-Pacific is dominating the global electrical steel market, accounting 41.87% in 2025, driven by China, Japan, South Korea, and India’s expanding power transmission infrastructure, electric vehicle manufacturing, and transformer production capacity, while North America is projected to register one of the fastest growth rates through 2035 due to grid modernization investments and accelerating domestic EV supply chain development.

- In 2025, Non-Grain-Oriented Electrical Steel (NGOES) led the market with 72.46%, supported by strong demand from power transformers, smart grid projects, and high-voltage transmission networks worldwide.

- Growing need for high-end electrical steel due to accelerated electrification in transport industry in forms of thin gauge grain-oriented and non-grain-oriented electrical steel that improves efficiency, power density, and energy efficiency of EV motors.

- Grid evolution and deployment of renewables necessitates investment in high-end transformer-grade electrical steels, since utilities seek lower transmission losses, higher efficiency rates, and compliance with energy regulations.

- The accelerating global transition toward electrification, renewable energy integration, and grid modernization is a major driver fueling demand for high-performance electrical steel, particularly in transformers, EV traction motors, and energy-efficient industrial equipment.

- Leading manufacturers including Nippon Steel Corporation, POSCO, Baowu Steel Group, and thyssenkrupp Steel Europe have strengthened their market positions through capacity expansions, advanced low-loss electrical steel developments, EV-grade material innovation, and strategic partnerships with automotive and power equipment manufacturers.

Electrical Steel Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 60.4 Billion | |

| 2035 Projected Market Size | US$ 109.9 Billion | |

| CAGR (2026-2035) | 7.8% | |

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Material Type | Grain-Oriented, Non-Grain-Oriented | |

| By Silicon Content | Low Silicon (<2%), Medium Silicon (2-3%), High Silicon (3-6.5%) | |

| By Product Form | Sheets, Coils, Strips, Others | |

| By Manufacturing Technology | Cold Rolled, Hot Rolled | |

| By Power Rating | Low Power (<1 kW), Medium Power (1 kW – 100 kW), High Power (>100 kW) | |

| By Thickness | Thick gauge (>0.5 mm), Medium gauge (0.3-0.5 mm), Thin gauge (0.2-0.3 mm), Ultra-thin (<0.2 mm) | |

| By Application | Transformers, Motors, Generators, Inductors & Reactors | |

| By End-User | Energy & Power, Automotive, Industrial Manufacturing, Household Appliances, Construction & Infrastructure | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia, Vietnam, Thailand, Philippnes | |

| South America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye, Nigeria | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Why does this report matter in 2026?

The global market of electrical steel will witness a revolutionary stage of growth in 2026 owing to the increased efforts by governments, utility companies, automakers, and industries towards developing efficient electrification infrastructure. With increased adoption of EVs, renewable energy sources, smart grids, and highly efficient transformers, there is an increased demand for high-quality electrical steel materials in large economies such as China, USA, India, Japan, South Korea, and European Union. The change is transforming the global market for electrical steel from being a traditional steel market to an important part of the global energy transition.

Electrical steel suppliers find themselves under growing pressure to provide materials which are of top performance, low loss, and cost-competitive nature that could help in fulfilling the changing standards of efficiency and sustainability. Growing developments in the field of GOES, NGOES, ultra thin gauge, and high silicon steels are setting new benchmarks for competitive dynamics within the industry. It is imperative that buyers, investors, and technology stakeholders have insight on performance of magnetic flux density, ability to reduce core loss, growth in manufacturing capacity, securing of raw material supplies, incorporation in EV motors, transformation in transformers, partnerships, and electrification initiatives supported by the government.

White Space & Investment Opportunities

- The capacity for manufacturing high-quality grain oriented electrical steel (GOES) is underdeveloped as utilities push towards expanding their ultra-high voltage transmission networks.

- The advanced production of non-grain oriented electrical steel (NGOES) will make for an attractive investment proposition as motor manufacturers aim to increase efficiency and reduce core losses.

- Local processing and slitting of electrical steel in India, Southeast Asia, the Middle East, and Latin America will assist in supply chain diversification and local manufacturing.

- Recycling or circular economy processes for recovering scrap electrical steel are also attractive options as regulatory and sustainability pressures continue to grow.

- Electrical steel manufacturing using decarbonized production processes such as green hydrogen and electricity from renewable sources in electric arc furnaces is becoming a premium investment area.

Future Market Transformation

By 2035, the market will mature to a strategic pillar of global electrification infrastructure. Suppliers will provide their customers with magnetic materials that are efficient in their use and come with quality certification, carbon footprint monitoring, metallurgy services, and specialized engineering solutions. It will focus on developing supply relationships with EV makers, transformers' OEMs, renewable energy generators, and grid operators in the long term. Electrical steel products will be made thinner and efficient at higher frequencies. The key players on the market will be those that can produce such products efficiently in large volumes while offering secure regional supply chains.

Buyer Decision-Making Criteria

Electrical steel suppliers for transformers and motors as well as OEMs normally consider their suppliers by examining magnetic properties, core loss features, supply continuity, cost effectiveness, and technical assistance provided. Energy efficiency is one major criterion used to qualify suppliers, but continuity of supply and consistency of products often influence decision-making. The increasing emphasis by customers on lower carbon content in electrical steel products as part of the sustainability efforts and compliance requirements. Collaboration of steelmakers and equipment manufacturers at an early stage may help in designing motors and transformers that will improve relationship with suppliers.

Economic & Investment Analysis

The macro factors that drive the electrical steel industry include grid modernization spending, renewable energy generation, EV penetration, steel production cost, energy cost, and industrial capital spending. High costs of electricity and materials could affect the business economics, whereas public spending on transmission facilities and clean energy will help increase demand. Inflation of iron ore, coking coal, alloying metals, and transport could strain margins unless there is some price contract in place. Currency exchange rate volatility affects international supply chains, especially since Asia continues to be a significant production region. Despite the cyclicality of industry production, the market is helped by structural electrification dynamics. Even a modest growth in the economy will help boost the demand for electrical steel via growing renewable energy capacities, transformers replacement programs, electric vehicle motors manufacture, and automation systems.

Investment Trends in the Market

- Advanced grain-oriented electrical steel (Hi-B GOES) production facilities.

- High-efficiency non-grain-oriented electrical steel lines for EV traction motors.

- Automated annealing, coating, laser-scribing, and quality-control technologies.

- Regional electrical steel manufacturing and processing capacity near EV and transformer manufacturing hubs.

- Green steel initiatives utilizing hydrogen-based ironmaking and renewable-energy-powered operations.

- Electrical steel recycling and closed-loop scrap recovery systems.

- Digital manufacturing, AI-driven process optimization, and real-time quality traceability platforms.

- R&D investments in ultra-thin gauges and low-core-loss electrical steel grades for next-generation energy applications.

Strategic Indicators For Electrical Steel

High Regulation Impact

The market for global electrical steel is currently undergoing an important regulatory transformation owing to transformer efficiency requirements, EV motor specifications, and industrial de-carbonization policies. In China, strict energy performance criteria continue to be set for distribution transformers, resulting in the increase in replacement needs for high-quality GOES. In the US, tougher transformer efficiency requirements under DOE standards generate an underlying demand for high-end magnetic steels. India's specialized steel program and localization policy reduce dependency on foreign inputs and encourage domestic CRGO developments. In the EU, the Ecodesign and carbon reduction directives prefer low loss electrical steels.

High Investment Activity

India has become a key country attracting investments in terms of CRGO electrical steel production for domestic transformers, thus minimizing the need for imports through expansions of their capacities by JSW Steel and JFE Steel. Many investments are being made in the manufacturing of advanced electrical steels in Europe, and one of such projects is an electrical steel plant of ArcelorMittal in France. Germany keeps building lines of NGO production intended for EV traction motors.

Supply Chain Disruption

The sourcing of electrical steel continues to be a challenge due to the localization of GOES and NGO production in China, Japan, South Korea, and some parts of Europe. The long lead time that many transformer producers in North America and Europe are experiencing is a result of the inadequate supply of electrical steel relative to the growing networks and renewable sources of power generation. India has been relying on premium-grade imports despite attempts at localization. Sourcing of raw material, energy consumption during processing, and annealing capacity are key chokepoints.

Pricing Volatility

Fluctuations will persist in the pricing of electrical steel because of varying costs of energy, capacity limitations of premium steel, and increasing demand for transformers. Pricing benchmarks of electrical steel will still be affected by Chinese production practices and costs associated with compliance. Higher production costs due to investments in green technology and carbon compliance affect prices for European manufacturers. The growing demand for transformers from utilities in North America has also made more competitive procurement of grain-oriented electrical steel. India will still experience volatility in its import costs due to dependency on foreign premium electrical steel producers.

Procurement Pressure

The procurement teams find it difficult to get long term procurement for the electrical steel because of the intense competition between the utility companies, electric vehicle manufacturers, transformers and renewable energy companies for their demand in the limited available premium grade production. The North America and European regions have seen more contractual sourcing in order to mitigate the risk of spot shortage. The Indian transformer manufacturers have started focusing on local supply contracts owing to the localization programs. China continues to dominate exports but due to quality concerns and trade limitations, there is more diversification in procurement.

New Technology Adoption

Adoption of technology is driven by ultra-thin gauge electrical steel, laser-domain refining, advanced coating techniques, AI-driven processing optimization, and low-carbon processing technologies. Germany and Japan continue to dominate in terms of advanced NGO production aimed at use in electric vehicles' traction motors. China is developing its capabilities in high-permeability GOES production aimed at ultra-high voltage transmission systems. Producers in Europe are scaling up their efforts to produce low-carbon electrical steel through decarbonized processing routes. Digital processing, predictive metallurgy, and automatic annealing technologies are resulting in improved magnetic properties' uniformity and minimizing manufacturing variability.

Regional Expansion Opportunity

Asia-Pacific still continues to be the most appealing region of expansion in terms of the quick installation of transformers, increasing production of electric vehicles, adding renewable energy, and the localization of steel industry with government help. North America holds great potential because utilities are investing heavily in the modernization of grids and upgrading their transformers. The demand for electrical steel production is rising because of domestic manufacturing investments and reshoring activities.

Government Policy Support

Government backing has emerged as a key catalyst to the growth of electrical steel production. The PLI initiative of the Indian government is helping in the production of electrical steel within India. The industrial decarbonization initiatives of the EU help in encouraging investments in electrical steel plants that use lower carbon. Energy efficiency regulations of China related to transformers and electric motors keep pushing the demand for premium quality magnetic steel. Grid transformation, transformer production expansion, and industrial supply chain strengthening within the US are being encouraged by the US government.

Import Export and Pricing Intelligence

The flow of global trade in electrical steels has been becoming more affected by strategic localization and energy security considerations. India still remains a notable consumer of high quality grain-oriented electrical steel even with all domestic investments that have been made. China is the leading exporter country, whereas Japan and South Korea are leaders in manufacturing high quality specialty electrical steels.

Electrical steel price setting will be less dependent on raw materials cost and will become more dependent on the efficiency of the material. The high quality low loss electrical steel will have higher margins because of transformer deficit, increased demand for EV motors and regulations on efficiency improvement. The buyers prefer guaranteed supply and consistent magnetic performance.

| HS Code | Reporter | Trade Flow | 2025 Trade Value (US$) | Interpretation |

| 722519 | Italy | Import | 387.2 Million | Import-dependent hub supporting transformers, machinery, EVs, and grid modernization. |

| 722519 | Japan | Export | 359.2 Million | Premium GOES supplier with high permeability grades used in power transformers. |

| 722519 | Mexico | Import | 340.7 Million | Premium exporter supplying advanced electrical steel for transformers, EVs. |

| 722519 | Germany | Export | 161.2 Million | High-value electrical steel trade driven by automotive electrification. |

AI Impact Analysis

Artificial Intelligence (AI) has revolutionized the production process of electrical steels by employing predictive metallurgy, process optimization, defect detection, and energy management systems. The use of AI in quality control ensures consistency in magnetic property and reduced losses in the rolling and annealing processes. Machine learning has become common in optimizing grain orientation, coating and production scheduling. Countries including China, Japan, Germany, and South Korea have adopted the use of AI in order to enhance efficiency and reduce energy consumption and cost of production. AI-based demand forecast has helped manufacturers to manage capacity in line with transformer and electric vehicle demands.

Disruption Analysis

Traditional demand patterns centered on industrial motors and power transformers are rapidly evolving toward high-performance electrical steels capable of supporting next-generation energy-efficient systems. The accelerating expansion of EV manufacturing is reshaping product requirements, with automakers demanding thinner gauges, lower core losses, and higher magnetic flux density materials to improve motor efficiency and vehicle range. The transition is compelling steel producers to invest heavily in advanced non-grain-oriented electrical steel technologies and specialized processing capabilities.

Aging power grids in North America and Europe, coupled with large-scale renewable integration projects in Asia-Pacific, are increasing demand for premium grain-oriented electrical steel used in high-efficiency transformers. Supply chain dynamics are also changing as governments seek domestic manufacturing capabilities for strategic energy-transition materials, reducing dependence on imports and encouraging regional capacity additions. Simultaneously, environmental regulations and decarbonization commitments are pushing manufacturers toward low-carbon steelmaking technologies, creating competitive differentiation based on sustainability credentials rather than production scale alone.

BCG Matrix: Company Evaluation

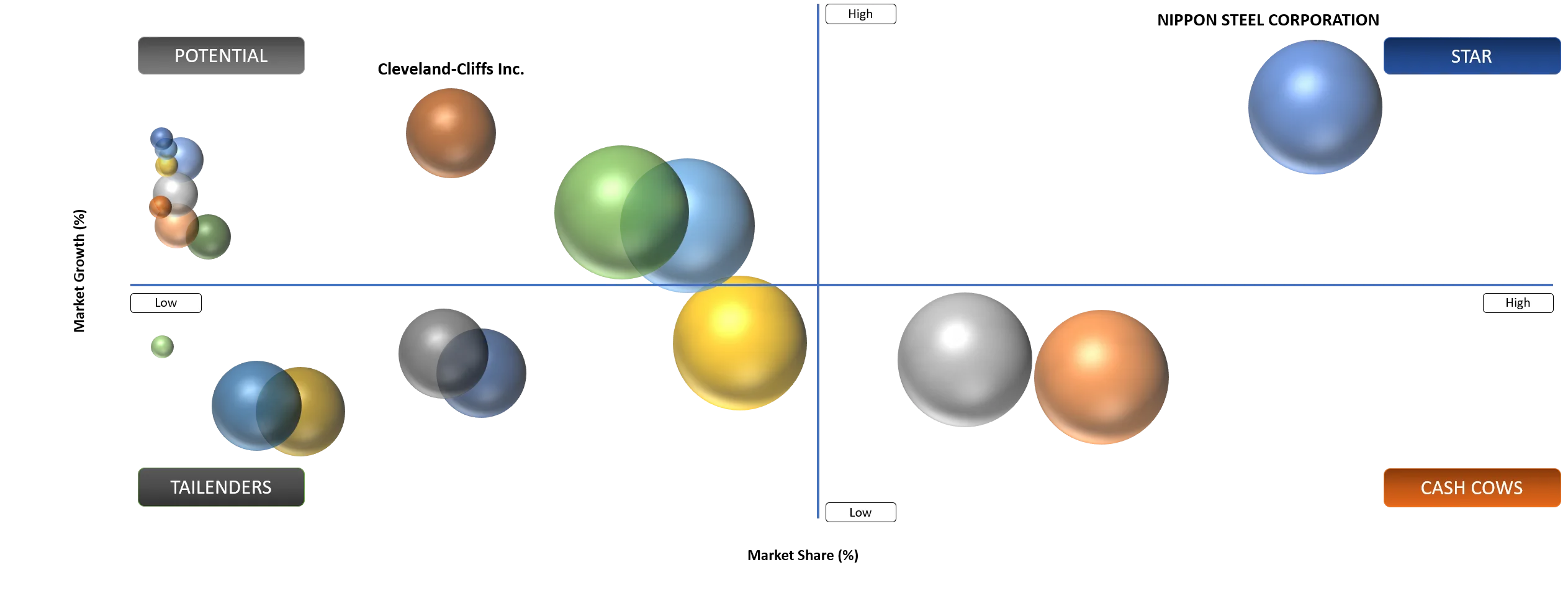

STAR

The star quadrant consists of players who have high market shares, sophisticated grain oriented electrical steels and non-grain oriented electrical steel technology, and are deeply integrated with trends like energy transition and electrification. Market players dominating this segment include the Nippon Steel Corporation, Baowu Steel Group, POSCO Holdings, and thyssenkrupp Steel Europe as they have been investing in high permeability electrical steel used in transformers and EV motors as well as renewable energy systems.

POTENTIAL

The potential competitors have been positioning themselves through capacity increases, technology improvements, and localized supply chain within regions. JFE Steel Corporation, ArcelorMittal, Voestalpine AG, and Shougang Group have been increasingly focusing on the production of premium quality electrical steel with specific uses such as the construction of traction motors and high efficiency transformers for electric vehicles (EVs).

Market Dynamics

Driver Impact Analysis

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

Rising Adoption of Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs) | 5.40% | China, Europe, North America, Japan, and South Korea automotive manufacturing hubs | EV traction motors, hybrid drivetrains, high-efficiency powertrain systems | Accelerates demand for high-grade non-grain-oriented electrical steel, improving motor efficiency and supporting vehicle electrification goals |

Expanding Investments in Renewable Energy Generation and Grid Modernization | 5.00% | China, India, Europe, North America, and Middle East energy infrastructure projects | Wind turbine generators, power transformers, smart grids, transmission networks | Strengthens consumption of grain-oriented electrical steel and supports development of efficient power transmission and renewable energy integration systems |

Increasing Deployment of Energy-Efficient Transformers and Distribution Infrastructure | 4.70% | Utility companies, transmission operators, and industrial power networks worldwide | Power transformers, distribution transformers, substations, grid expansion projects | Enhances demand for low-core-loss electrical steel, helping utilities reduce transmission losses and comply with energy efficiency regulations |

Driver: Rising Electric Vehicle Production Driving NGOES Demand

Increasing EV production is generating structural demand for non-grain-oriented electrical steel owing to its suitability for use in traction motors of EVs since it has high magnetic permeability, minimal iron losses, thin gauge and high stability of its magnetic properties at high rotational speed. Motor efficiency determines EV range, heat efficiency, battery efficiency and general energy consumption of the vehicle. China is still the biggest manufacturer and consumer of EVs; however, Europe, America, Japan, South Korea and India are increasing their production capacity for EVs.

In automotive OEMs, there is a trend from the traditional use of motor steel to thinner low-loss and specialized NGOES varieties to achieve higher torque densities and minimize core losses. There is particular need for ultra thin NGOES varieties in fast traction motors since heat dissipation, magnetic uniformity and lamination are important. The trends are reflected by capacity expansion for premium NGOES varieties, enhanced annealing facilities, isolation lines, advanced coating technology, and cooperation with motor and automotive suppliers regionally. Manufacturers that have good cold rolling, slitting, coating, magnetic testing and client qualification skills are best poised to benefit from the increasing use of electrical steel in electric vehicles.

Driver: Expansion of Power Grid Infrastructure Boosting GOES Consumption

Expansion of power grid infrastructure is strengthening demand for grain-oriented electrical steel, as GOES is a critical core material in power transformers, distribution transformers and high-efficiency grid equipment. Utilities are increasing investments to manage renewable power integration, industrial electrification, EV charging demand, data center loads and aging transmission assets. It is creating steady demand for low-loss transformer cores, where GOES helps improve magnetic efficiency, reduce technical losses and support reliable long-distance power transmission. China remains the largest grid-led opportunity, with IEA estimating US$ 88 billion in transmission and distribution investment in 2025, supported by renewable evacuation, ultra-high-voltage transmission and industrial power demand. In the U.S., transformer replacement and resilience upgrades are becoming more urgent, while DOE’s 2024 distribution transformer efficiency rule preserved the use of GOES and estimated US$ 824 million per year in electricity cost savings.

Europe is also moving toward large-scale grid modernization, as the European Commission notes that electricity consumption may rise around 60% by 2030 and about 40% of distribution grids are over 40 years old. India is another important opportunity, supported by Green Energy Corridor Phase II transmission and substation additions, along with JSW and JFE’s move to expand domestic GOES capacity. Power grid expansion is shifting GOES demand toward premium, low-loss and high-permeability grades used in modern transformers and energy-efficient grid infrastructure.

Restraint Impact Analysis

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

High Energy and Raw Material Costs (Iron Ore, Coking Coal & Electricity) | 4.60% | Production economics and profit margins | Grain-oriented (GOES) and non-grain-oriented electrical steel manufacturing | Increases production costs, reduces pricing competitiveness, and limits capacity expansion investments |

Stringent Environmental Regulations & Decarbonization Compliance Costs | 4.10% | Steelmaking operations and emissions management | Blast furnace-based electrical steel production and conventional processing facilities | Raises capital expenditure requirements and extends modernization timelines for steel manufacturers |

Restraints: High Capital Investment and Complex Manufacturing Processes

High capital requirement limits the growth in the electrical steel industry, where premium GOES and NGOES production requires specific technology of cold rolling, annealing, insulation coating, grain orientation, magnetic tests, and certification. The high set up costs, lengthy time required for installation, and technical complexity limit capacity expansion and make it difficult for newcomers. Production of premium electrical steel requires precision in thickness, core losses, permeability, quality of surface, and uniformity of coating. Any deviation will have a negative impact on transformer and EV motors and limit qualification of customers.

ArcelorMittal, in February 2025, has committed an investment of approximately US$ 0.9 billion for a premium non-grain-oriented electrical steel plant in Calvert, Alabama, with an output expected by the second half of 2027, illustrating the lengthy process between investment and output.In January 2025, thyssenkrupp inaugurated its Bochum annealing and isolation line for non-grain-oriented electrical steel, capable of producing more than 200,000 metric tons per year, indicating the complexity and technological nature of advanced electrical steel production. The high capital expenditure, lengthy process of commissioning, qualification processes, and the lack of technical expertise limit faster expansion of the supply even with rising demand from transformers, EV traction motors, renewable energy generators, and grid equipment.

Segmentation Analysis

The global electrical steel market is segmented based on the material type, silicon content, product form, manufacturing technology, power rating, thickness, application, end-user and region.

By Application

Transformer Segment Leads Market Demand

With rising transmission network development and renewable energy projects in countries, there is growing installation of transformers. The International Energy Agency states that the world added around 700 gigawatts of renewable energy capacity in 2024, while renewables made up over 80% of global power generation capacity additions. The large installation of renewables would require efficient transformers to connect to the grid and transmit electricity.

The utilities are using grain-oriented electrical steels that lower no-load losses and increase the efficiency of transformers. Tight energy efficiency standards in North America, Europe, China, India, and Japan are further making rapid adoption of new high-efficiency transformers from old fleets, leading to higher demand for electrical steel.

By End-User

Electric Vehicle Applications Gain Momentum

The quick rise of the electric vehicle market has also become another demand driver for non-grain-oriented electrical steel. Electric vehicle traction motors need to have high magnetic permeability, low core loss, and efficiency properties, which make NGO electrical steel a vital material for today's EVs. China has made up almost 64% of the worldwide growth in electric vehicle sales, while Europe and North America kept on promoting the adoption of EVs through incentives and investments in manufacturing. The increased production of electric vehicles has thus resulted in a rise in the need for more efficient NGO electrical steel grades. Car manufacturers are now working closely together with steel suppliers to produce thinner electrical steel with higher silicon content in order to increase the range and efficiency of electric motors, making the EV market one of the most rapidly growing segments of the electrical steel market.

Market Segmentation

- By Material Type

- Grain-Oriented

- Conventional

- High Permeability

- Domain Refined

- Laser-scribed

- Non-Grain-Oriented

- Fully processed

- Semi processed

- Grain-Oriented

- By Silicon Content

- Low Silicon (<2%)

- Medium Silicon (2-3%)

- High Silicon (3-6.5%)

- By Product Form

- Sheets

- Coils

- Strips

- Others

- By Manufacturing Technology

- Cold Rolled

- Hot Rolled

- By Power Rating

- Low Power (<1 kW)

- Medium Power (1 kW – 100 kW)

- High Power (>100 kW)

- By Thickness

- Thick gauge (>0.5 mm)

- Medium gauge (0.3-0.5 mm)

- Thin gauge (0.2-0.3 mm)

- Ultra-thin (<0.2 mm)

- By Application

- Transformers

- Power Transformers

- Distribution Transformers

- Motors

- Induction Motors

- Permanent Magnet Synchronous Motors (PMSM)

- Switched Reluctance Motors (SRM)

- Brushless DC Motors (BLDC)

- Generators

- Inductors & Reactors

- Transformers

- By End-User

- Energy & Power

- Automotive

- Industrial Manufacturing

- Household Appliances

- Construction & Infrastructure

Geographical Penetration

U.S. Electrical Steel Market Landscape

U.S. demand for electrical steel is closely linked to transformer efficiency, grid reliability and the replacement cycle for distribution assets. DOE’s energy conservation standards for distribution transformers reinforce the importance of grain-oriented electrical steel in designs that lower no-load and load losses without creating avoidable supply risk. Utility customers and transformer OEMs are likely to place greater attention on conventional, high permeability and domain refined material choices where core loss performance affects lifetime cost.

Transmission system reinforcement also supports demand for high power applications. Large power transformers require long qualification cycles and customers often approve suppliers through detailed technical records rather than short-term pricing. Electrical steel suppliers able to provide sheets and coils with stable thickness, magnetic loss data and reliable delivery schedules will be better suited for utility procurement. High power transformers used in grid substations also create demand for thick gauge and medium gauge material where mechanical handling, core build quality and loss performance must be balanced.

Automotive electrification adds a second demand channel through non-grain-oriented material. PMSM, BLDC and induction motor designs use thin gauge and ultra-thin electrical steel to improve efficiency, reduce heat generation and support compact motor packaging. Motor producers serving EV platforms will value fully processed grades with tight dimensional tolerances, consistent punching behavior and validated magnetic properties.

Japan Electrical Steel Market Outlook

Japan’s electrical steel demand reflects a market where reliability, compact design, energy efficiency and manufacturing precision carry high commercial weight. The 7th Strategic Energy Plan and GX2040 Vision connect future electricity demand with decarbonized energy supply and industrial competitiveness. Energy and power customers therefore require power transformers, distribution transformers and reactors that can support stable grids, renewable integration and resilient electricity supply. Grain-oriented electrical steel is central to transformer efficiency and noise control.

Japanese transformer procurement often emphasizes quality consistency and long service performance. High permeability, domain refined and laser-scribed grain-oriented grades are relevant where transformer makers design compact, low-loss and low-noise equipment. Thin gauge and medium gauge selections depend on core architecture and efficiency requirements. Suppliers must meet strict documentation standards, batch consistency and process discipline because qualification is detailed and customer expectations are high.

Japan’s automotive segment is a major route for non-grain-oriented electrical steel. Hybrid, plug-in hybrid and battery electric vehicles require PMSM, BLDC and auxiliary motor systems with compact cores and high efficiency. Thin gauge and ultra-thin fully processed material can support high-speed motor designs where iron loss, torque density and heat generation affect vehicle performance. Motor manufacturers will prioritize surface quality, thickness tolerance and magnetic property stability.

China Electrical Steel Market Trends

China represents one of the broadest demand bases for electrical steel because grid construction, renewable integration, EV production, appliance manufacturing and industrial equipment all pull material through different applications. The national action plan for a new electricity system emphasizes clean electricity transmission, advanced regulation and control technologies. High power transformers, distribution transformers and reactors therefore remain critical applications for grain-oriented electrical steel in the energy and power end-user segment.

Ultra-high-voltage transmission, large renewable bases and regional power transfer requirements support demand for high specification transformer cores. Grain-oriented grades such as high permeability, domain refined and laser-scribed material can be used where transformer makers pursue lower losses and performance stability in large assets. Product form demand spans sheets, coils and strips because China has extensive transformer, core processing and electrical equipment manufacturing capacity. Cold rolled technology is central to high-quality electrical steel production.

China’s automotive segment creates substantial demand for non-grain-oriented electrical steel. New energy vehicle platforms use PMSM, BLDC and induction motor systems that require thin gauge and ultra-thin material with low iron losses, high magnetic flux capability and stable stamping behavior. Motor makers also need reliable supply in high volumes because vehicle production schedules are sensitive to material qualification and coil availability.

Competitive Landscape

- The global electrical steel market is characterized by a concentrated competitive landscape where technological expertise, production scale, and advanced processing capabilities serve as key differentiators.

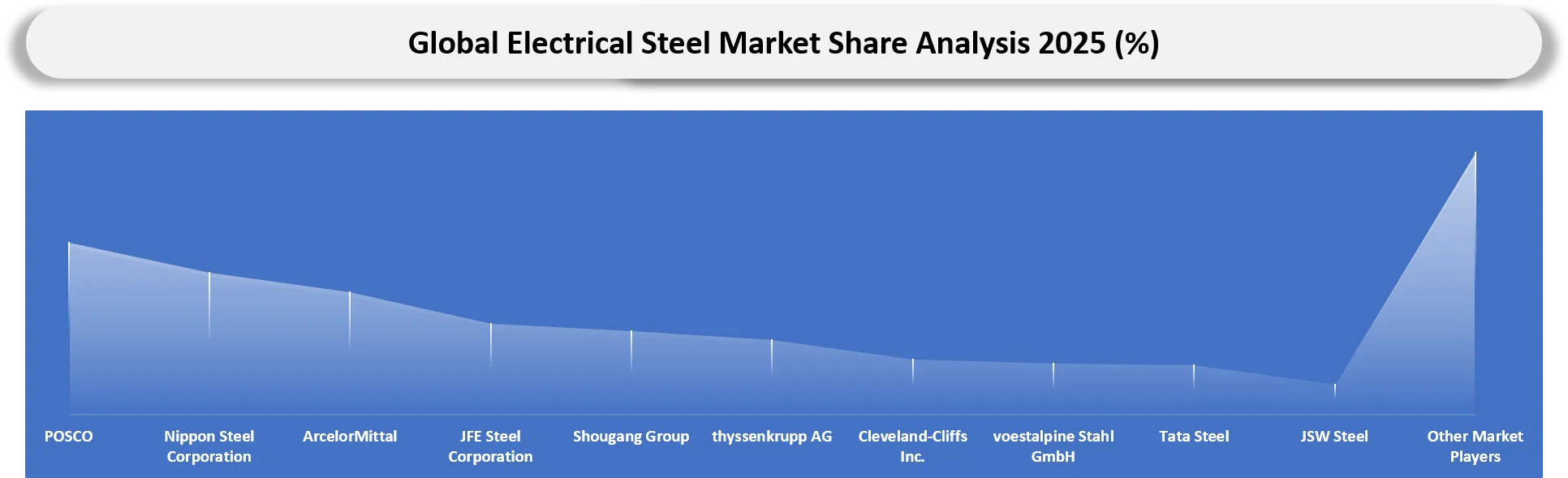

- Major participants include Nippon Steel Corporation, JFE Steel Corporation, POSCO, Baowu Steel Group, thyssenkrupp Steel, Voestalpine AG, ArcelorMittal, Cleveland-Cliffs Inc., Tata Steel, Shougang Group, and NLMK Group.

- Companies are increasingly investing in high-permeability grain-oriented electrical steel, ultra-thin NGO grades for EV motors, advanced coating technologies, and low-carbon steel production processes.

- Strategic capacity expansions, technology partnerships, and investments in energy-efficient manufacturing are becoming critical competitive factors as demand accelerates across power transmission, renewable energy, industrial automation, and electric mobility applications.

Company Coverage Preview

Nippon Steel is one of the leading players in electrical steel with a clear technological lead in grain-oriented and non-grain oriented electrical steel for use in transformers and electric vehicles. Nippon Steel is constantly working on securing their source of raw materials, international partnerships, and exposure to growth markets powered by electrification. Some of the latest steps taken by the company in this regard are investments in their supply chain, international acquisitions, and development of next generation low-carbon steel.

Key Companies

- ThyssenKrupp AG

- POSCO

- ArcelorMittal

- NIPPON STEEL CORPORATION.

- JFE Steel Corporation

- Tata Steel

- Voestalpine Stahl GmbH

- United States Steel Corporation

- Cleveland-Cliffs Inc.

- Shougang

- JSW Steel

MAJOR PAIN POINTS

- Volatility in Raw Material Prices

- Supply-Demand Imbalance for Grain-Oriented Electrical Steel (GOES)

- High Energy and Manufacturing Costs

- Capacity Constraints Amid Growing EV Demand

- Stringent Environmental and Carbon Emission Regulations

- Technological Complexity in Producing High-Grade Electrical Steel

- Dependence on Power Infrastructure Investment Cycles

- Increasing Competition from Alternative Motor Technologies

- Customer Pressure for Higher Efficiency and Lower Core Losses

RECENT DEVELOPMENTS

| Company | Strategy | Date | Development | Strategic Implication |

NIPPON STEEL CORPORATION and United States Steel Corporation | Strategic acquisition | June 2025 | Nippon Steel finalized its acquisition of U. S. Steel through Nippon Steel North America. | Strengthens Nippon Steel’s North American platform and improves access to automotive, energy, industrial and electrical steel-linked customers in a protected U.S. steel market. |

JSW Steel and JFE Steel Corporation | Acquisition through joint venture | January 2025 | JSW Steel and JFE Steel completed the acquisition of thyssenkrupp Electrical Steel India through their joint venture. | Accelerates India’s domestic electrical steel capability and strengthens local supply for CRGO, transformer cores, grid expansion and power infrastructure demand. |

| ArcelorMittal | Strategic capacity investment | February 2025 | ArcelorMittal announced it would proceed with an advanced non-grain-oriented electrical steel manufacturing facility in Alabama with capacity of up to 150,000 metric tons annually. | Strengthens North American NGOES supply for EV motors, generators, renewable electricity production and industrial electrical applications. |

JSW Steel and JFE Steel Corporation | Greenfield joint venture | February 2024 | JSW and JFE established JSW JFE Electrical Steel Private Limited to manufacture grain-oriented electrical steel in India. | Builds India’s domestic GOES platform and reduces long-term import dependence for transformer manufacturers and grid infrastructure projects. |

ANALYST VIEW / OPINION

- Rising electrification of transportation is reshaping demand patterns, with high-grade grain-oriented and non-grain-oriented electrical steel becoming a critical material for EV motors, charging infrastructure, and next-generation mobility systems.

- Capacity expansions across Asia-Pacific are intensifying competitive dynamics, enabling regional manufacturers to strengthen export capabilities while addressing increasing domestic demand from power transmission and automotive sectors.

- Energy efficiency regulations are accelerating the replacement of conventional magnetic materials with advanced electrical steel grades, creating long-term growth opportunities across transformers, generators, and industrial motors.

- Transformer modernization programs and grid expansion investments are driving sustained consumption of grain-oriented electrical steel, particularly in economies prioritizing renewable energy integration and transmission network upgrades.

- Premium electrical steel grades with lower core losses are gaining market share as utilities and industrial users seek to reduce operational energy costs and improve overall system efficiency.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

Power Transformer Manufacturers | Transformer Design Engineers, Procurement Heads, Product Development Teams | Analyze demand trends for grain-oriented electrical steel (GOES), transformer efficiency requirements, grid modernization projects, and raw material sourcing strategies |

Electric Vehicle (EV) Manufacturers | E-Mobility Engineering Teams, Motor Design Engineers, EV Powertrain Specialists | Evaluate electrical steel requirements for traction motors, vehicle electrification trends, motor efficiency improvements, and next-generation EV technologies |

Industrial Motor Manufacturers | Motor Design Engineers, Manufacturing Heads, Product Strategy Teams | Assess demand for non-grain-oriented electrical steel (NGOES), energy-efficient motor production, industrial automation growth, and performance optimization opportunities |

Power Generation Equipment Manufacturers | Generator Engineering Teams, Plant Equipment Designers, Strategic Sourcing Departments | Understand electrical steel consumption in generators, turbines, renewable energy systems, and high-efficiency power equipment manufacturing |

Renewable Energy Equipment Manufacturers | Wind Turbine Engineering Teams, Renewable Technology Specialists, Procurement Managers | Analyze electrical steel demand driven by wind turbine generators, clean energy investments, and global renewable power expansion initiatives |

Transmission & Distribution (T&D) Equipment Manufacturers | Grid Infrastructure Teams, Transformer Production Managers, Utility Equipment Engineers | Evaluate opportunities arising from transmission network upgrades, smart grid deployment, and growing electricity demand worldwide |

Consumer Appliances Manufacturers | Product Development Teams, Electrical Component Engineers, Supply Chain Managers | Assess electrical steel demand for compressors, air conditioners, refrigerators, washing machines, and energy-efficient appliance production |

Electrical Equipment & Industrial Automation Companies | Industrial Automation Engineers, Product Innovation Teams, Manufacturing Operations Managers | Identify growth opportunities in automation systems, industrial drives, robotics, and high-performance electrical equipment applications |

Electrical Steel Producers & Raw Material Suppliers | Commercial Strategy Teams, Market Intelligence Departments, Capacity Planning Managers | Benchmark competitive positioning, production capacity expansions, technology advancements, pricing trends, and regional demand dynamics |

Investors, Private Equity Firms & Management Consultants | Investment Analysts, Corporate Strategy Teams, Market Research Consultants | Evaluate market growth opportunities, competitive landscape, electrification trends, energy transition investments, and long-term demand outlook for electrical steel |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- Electrical steel demand forecasting mapped directly to transformer, EV motor, and renewable energy deployment pipelines.

- Country-level GOES and NGO capacity benchmarking with operational, announced, and under-construction manufacturing facilities.

- Detailed transformer industry demand linkage model connecting grid investments with electrical steel consumption.

- Competitive intelligence covering technology leadership, magnetic performance benchmarking, and low-carbon product positioning.

- Trade-flow analysis identifying import dependency risks, sourcing vulnerabilities, and emerging export opportunities.

- Investment tracker covering electrical steel capacity expansions, acquisitions, partnerships, and greenfield manufacturing projects.

- AI-powered market outlook integrating policy changes, electrification trends, and infrastructure spending impacts