Drone Insurance Market Definition & Overview

What is the Drone Insurance Market?

The Drone Insurance Market includes specialized aviation insurance products that protect commercial and recreational drone operators against liability, hull damage, payload loss, privacy claims, cyber exposure and operational interruption. The market entails annual policies, on demand flight coverage, fleet programs, broker led aviation policies and embedded digital insurance sold through drone management platforms. Demand is tied to the growth of commercial UAV operations in inspection, agriculture, construction, energy, media, public safety and logistics. The market also includes underwriting analytics, flight data based pricing, claims support, regulatory compliance assistance and risk engineering services that help buyers operate drones safely across regulated airspace.

Drone Insurance Industry Background & Evolution

Parent market background: The parent market is aviation insurance and specialty property and casualty coverage. Traditional aviation policies focused on aircraft hull and third party liability, then expanded into unmanned aircraft as drones moved from hobby use to commercial missions. Roadmap evolution: 2016 Part 107 accelerated US commercial drone adoption and created clearer underwriting triggers. 2018 to 2020 brought app based policies and hourly coverage. 2021 to 2024 shifted buyers toward annual fleet liability, payload cover and cyber add ons. 2025 introduced major BVLOS rulemaking momentum that raised demand for scalable risk models. From 2026 onward, the market is expected to move toward data driven pricing, automated compliance checks and integrated fleet insurance for logistics and infrastructure missions.

Drone Insurance Market Snapshot

| Metric | Details |

| Market Report Name | Drone Insurance Market |

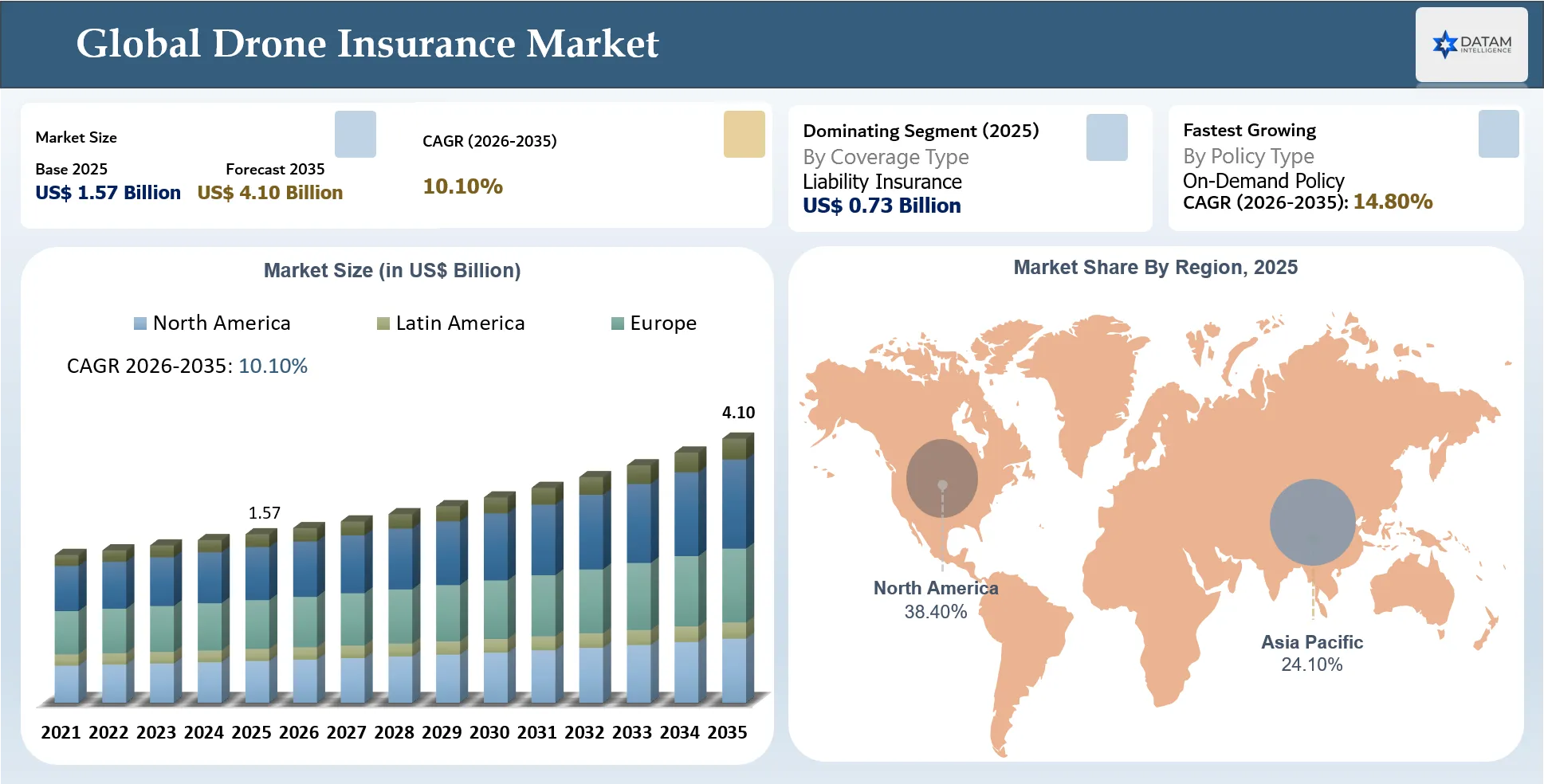

| Global Market Size 2025 | USD $1.57 Billion |

| Projected Market Size 2035 | USD $4.10 Billion |

| CAGR 2026-2035 | 10.10% |

| Largest Segment Name | Liability Insurance |

| Largest Segment Share | 46.20% |

| Fastest Growing Segment Name | On Demand Policy |

| Fastest Growing Segment Share/CAGR | 14.80% |

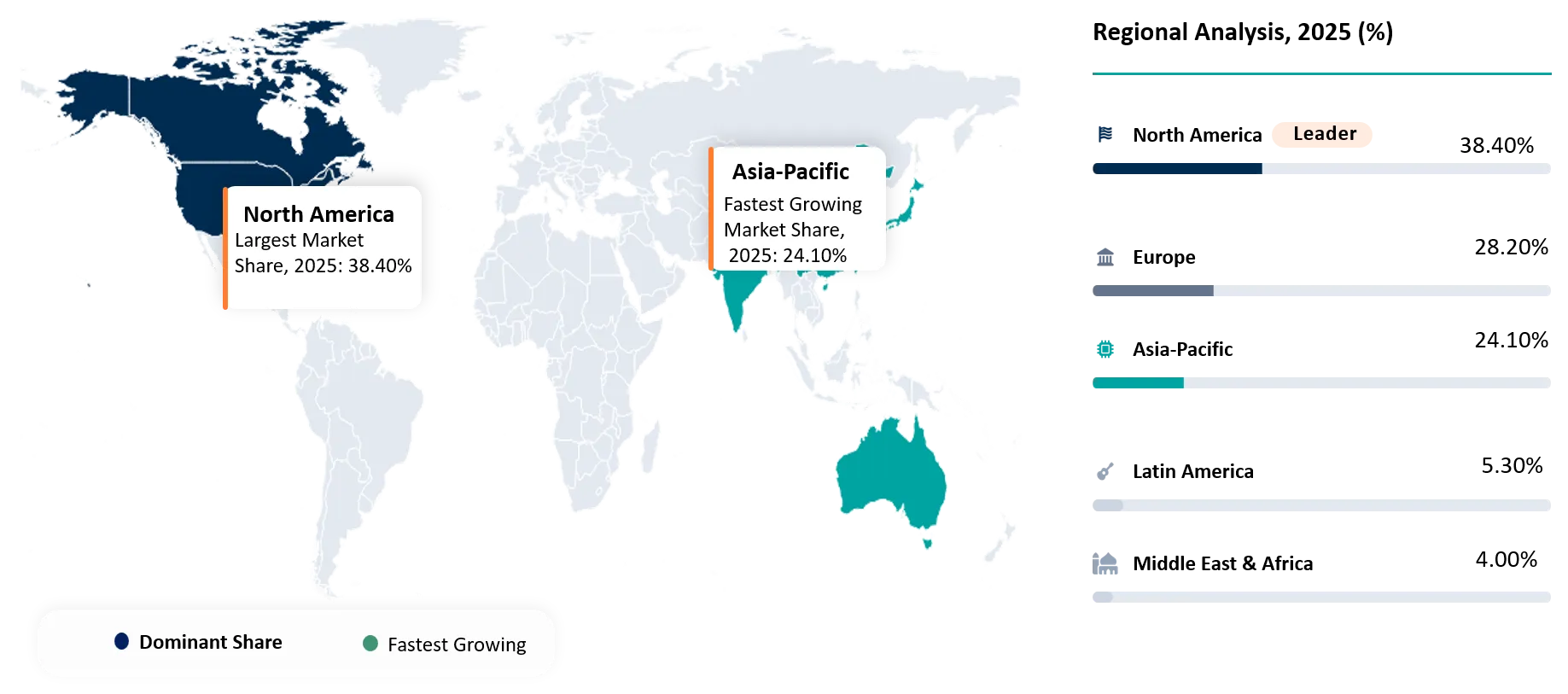

| Largest Region Name | North America |

| Largest Region Share | 38.40% |

| Fastest Growing Region Name | Asia Pacific |

| Fastest Growing Region Share/CAGR | 12.90% |

| Geographic Market Share for the 5 Regions | North America: 38.40% Europe: 28.20% Asia Pacific: 24.10% Latin America: 5.30% Middle East & Africa: 4.00% |

| Top Companies | Global Aerospace, SkyWatch.AI, Coverdrone, Allianz Commercial, AIG Aerospace, Avion Insurance, BWI Aviation Insurance, Thimble, Transport Risk Management, Flock |

Historical Drone Insurance Market Trend Analysis

During 2020 to 2025, the Drone Insurance Market moved from niche aviation coverage to a wider specialty insurance category. Early demand was led by photographers and small inspection pilots buying liability cover for project access. Over time, enterprises began requiring formal insurance certificates, named insured endorsements and hull cover before permitting drone work on construction sites, utilities and industrial assets. App based underwriting also improved market access by allowing hourly and monthly coverage for occasional pilots. The biggest historical shift was the rising role of regulatory compliance in purchasing decisions, as buyers increasingly connected insurance with operational authorization, flight logging and safety documentation. Claims patterns around crashes, privacy complaints, lost payloads and property damage pushed insurers to price policies by use case rather than drone value alone. By 2025, the market had become more data oriented, with telematics, operator history and mission type shaping both premium levels and underwriting appetite.

Drone Insurance Growth Outlook Summary

The short term outlook is shaped by commercial drone adoption in mapping, media, inspection and agriculture, where liability cover is becoming a routine procurement requirement. Buyers are increasingly selecting digital policies that allow fast proof of insurance, adjustable liability limits and easier coverage for rented or client owned drones. In the mid term, BVLOS operations, larger fleets and delivery pilots are expected to shift the market from single operator policies toward enterprise risk programs. This will increase demand for risk engineering, flight data based underwriting and cyber liability because autonomous missions create more complex exposure. In the long term, the Drone Insurance Market will likely resemble a hybrid of aviation insurance, technology liability and mobility risk management. Growth will come from high frequency drone operations across infrastructure, energy, emergency response and logistics. Insurers that integrate with fleet management software, use real flight telemetry and provide country specific compliance support will capture higher share.

Key Takeaways

- Liability insurance remains the largest coverage segment because enterprise clients require proof of third party protection before approving drone operations on job sites and public projects.

- North America is the largest region because FAA registration, commercial drone density and mature specialty aviation underwriting create stronger demand concentration than other regions.

- Asia Pacific is the fastest growing region as China, Japan, India and Australia increase drone use in agriculture, disaster response, inspection and delivery related pilots.

- On demand policy formats are the fastest growing segment because occasional pilots and small businesses want flexible coverage aligned with actual flight hours and mission risk.

- BVLOS regulation is a market catalyst because longer range operations increase exposure severity and push buyers toward higher liability limits, better safety documentation and fleet programs.

- Underwriting is shifting from asset value to mission risk, so insurers need data on flight conditions, pilot behavior, payload type and operating environment to price risk accurately.

- Drone insurance is becoming embedded in platforms, with quote and bind functions moving into fleet management tools, drone marketplaces and operator compliance software.

- Claims differentiation will become a competitive advantage because drone losses require aviation expertise, payload valuation knowledge and rapid support for commercial continuity.

Drone Insurance Market White Space & Investment Opportunities

White space opportunities highlight underpenetrated buyer groups coverage gaps and distribution models where insurers brokers and platforms can build differentiated products as drone adoption scales across industries globally through 2035.

- Cyber and privacy liability for drone data remains under served as many buyers still purchase physical risk coverage without fully protecting sensitive imagery, location records and platform access.

- Public safety fleet insurance is an attractive niche because police, fire, emergency medical and disaster response teams need tailored liability, hull, payload and volunteer operator coverage.

- Delivery corridor insurance will grow as autonomous logistics pilots require coverage linked to flight density, landing zones, route risk and third-party property exposure.

- SME embedded coverage through drone marketplaces can capture occasional operators who avoid broker based annual policies but need fast certificates for specific commercial projects.

Drone Insurance Market Procurement & Buyer Behavior Analysis

Drone Insurance Market Buyer Decision Making Criteria

Buyers evaluate drone insurance based on whether the policy satisfies client contracts, regulatory expectations and mission exposure. Procurement teams increasingly want fast certificates, clear exclusions and coverage that matches drone type, payload value and operating geography.

- Liability limit adequacy for client contracts, public operations and industrial site access.

- Coverage clarity for hull damage, payload loss, privacy claims, cyber exposure and non-owned drones.

- Certificate turnaround speed with additional insured wording and project specific documentation.

- Geographic scope and regulatory fit for operators flying across multiple jurisdictions.

- Claims support quality, including aviation adjuster expertise and fast response after incidents.

- Pricing flexibility through annual, monthly, daily or hourly options aligned with utilization.

Drone Insurance Market Economic & Investment Analysis

Drone Insurance Market Macroeconomic Impact Factors

Macroeconomic conditions affect drone insurance through capital spending, infrastructure activity, insurance pricing cycles and enterprise risk appetite. Higher interest rates and tighter budgets can make small operators more premium sensitive, reducing optional hull or payload purchases. At the same time, infrastructure, utilities and energy companies continue to use drones because aerial inspection reduces labor risk and improves asset visibility. Inflation in repair costs, sensors and replacement parts can lift hull premiums and make payload coverage more important. The broader property and casualty cycle also matters because reinsurers may adjust capacity for specialty aviation risks after large losses or uncertainty around autonomous operations. Government spending on infrastructure, public safety and drone integration supports market growth by creating more formal procurement requirements. By 2035, the strongest macroeconomic tailwind will be productivity pressure, as companies use drones to lower inspection costs and then purchase insurance to manage operational exposure.

Drone Insurance Investment Trends in the Market

Investment is shifting toward digital distribution, underwriting analytics and embedded insurance because these areas improve access and pricing accuracy. Investors are also watching drone fleet platforms that can monetize operational data through insurance partnerships.

- Usage based insurance platforms and digital quote engines.

- Telemetry analytics for safer underwriting and premium adjustment.

- Embedded insurance inside drone fleet management and marketplace platforms.

- Cyber and payload coverage modules for enterprise drone operations.

Drone Insurance Market Funding & M&A Activity

Funding and M&A activity is expected to focus on Insurtech distribution, aviation data platforms and specialty brokers that can aggregate drone operators. Direct drone insurance acquisitions are selective, yet strategic interest is increasing as autonomous operations grow.

- 2025 Skywatch and Global Aerospace carrier partnership continued to support digital drone insurance distribution with aviation backed capacity.

- 2025 to 2026 specialist drone insurers and brokers expanded platform features and broker engagement as enterprise procurement became more formalized.

- 2026 investors are expected to target UAS risk analytics, embedded insurance workflows and drone fleet data platforms rather than only traditional policy brokers.

- 2026 M&A focus is likely to include aviation brokers with UAV expertise, compliance software and platforms serving commercial drone fleets.

Drone Insurance Market Regulatory & Policy Analysis

Drone Insurance Regulatory Framework Overview

The regulatory framework for drone insurance is shaped by aviation rules, commercial drone operating permissions, privacy expectations and country specific liability requirements. In the US, Part 107 provides the operational foundation for commercial drone flights, while the FAA August 2025 BVLOS proposal may normalize longer range low altitude operations. In Europe, EASA rules classify drone operations and influence risk expectations across open, specific and certified categories. Insurance requirements vary by jurisdiction and customer contract, so market growth depends on clearer operating permissions and stronger compliance documentation.

- August 2025 FAA BVLOS NPRM may expand long range commercial operations, increasing demand for fleet liability and risk data-based underwriting.

- 2025 to 2026 EASA implementation of drone categories continues to influence insurance wording for European commercial operators.

- 2026 public event airspace restrictions around major events increase attention to drone liability, compliance and unauthorized flight risk.

Drone Insurance Policy Impact on Market Growth

Government policies affect drone insurance by changing where drones can fly, which operations need authorization and how buyers view liability. Supportive rules can expand insured missions, while complex requirements increase broker and compliance demand.

- BVLOS policy progress expands the addressable market for infrastructure inspection, delivery and remote monitoring insurance programs.

- Public safety drone funding supports fleet adoption by agencies that require formal liability and equipment coverage.

- Stronger privacy and data protection expectations increase demand for policies that address imagery, personal injury and cyber liability.

- Airspace integration policy encourages enterprise buyers to formalize risk transfer before scaling autonomous drone operations.

Drone Insurance Market Trends & Innovation Landscape

Drone Insurance Key Market Trends

Digital underwriting is reshaping the market as buyers expect faster quote generation, flexible liability limits and instant certificates. The strongest trends are linked to commercial fleet use, regulatory visibility and the need for clearer coverage around data exposure.

- On demand coverage is growing because operators want policies that match specific flights, client projects and seasonal demand patterns.

- Fleet policies are replacing single drone cover for enterprise buyers that operate across many sites and require centralized compliance.

- Payload and cyber add ons are becoming more important as drones carry expensive sensors and collect sensitive operational data.

- Broker digitalization is expanding because aviation brokers are using online portals to reduce application friction and improve certificate turnaround.

Drone Insurance Market Technology Advancements

Technology changes are making drone insurance more data centric. The market is moving toward underwriting systems that evaluate mission context, operator behavior and aircraft utilization rather than relying only on drone purchase value.

- August 2025 BVLOS rulemaking is accelerating demand for insurance systems that can price longer range autonomous and remotely supervised missions using operational risk data.

- 2025 to 2026 telematics based underwriting platforms are increasingly linking flight logs, geofencing events and pilot history to premium adjustment and risk prevention.

- Digital quote and bind tools are reducing policy issuance time by connecting operator details, liability limits and certificate generation through online workflows.

- Cyber risk modules are being added to drone policies as connected drones, cloud controls and captured imagery increase data liability exposure.

Drone Insurance Industry Transformation Trends

- The market is shifting from manual aviation underwriting toward platform assisted pricing as insurers use digital data to serve smaller operators at scale.

- Enterprise buyers are consolidating drone insurance through master fleet policies that cover multiple aircraft, pilots, payloads and operating locations.

- Regulatory changes are moving insurance from optional protection toward a compliance linked procurement requirement for commercial missions.

- Specialized insurers are gaining influence because drone risks require aviation knowledge, fast certificates and clearer wording for privacy, cyber and payload exposure.

Drone Insurance Market Disruption Analysis

The main disruption in the Drone Insurance Market is the shift from static annual policies to data driven coverage linked to actual mission risk. Hourly coverage, platform-based purchase journeys and BVLOS operations are changing how insurers price and distribute protection. Traditional aviation insurers still provide capacity and claims expertise, while insurtech platforms control customer access and data. This creates a structural split between capital providers and digital distributors. As autonomous operations grow, underwriting will rely more on flight logs, operator history and airspace risk. Insurers that cannot integrate data or issue rapid certificates may lose share to digitally native platforms and embedded insurance partners.

Drone Insurance Market Disruption & Structural Shift Analysis

Drone Insurance Market Technology Disruption Impact

Technology disruption is shifting drone insurance from policy administration toward operational risk intelligence. Insurers increasingly need flight data, compliance records and software partnerships to underwrite future drone missions.

- BVLOS operations disrupt traditional underwriting because exposure is no longer limited to nearby piloted flights. Longer routes, remote supervision and higher mission frequency require fleet level pricing and stronger risk documentation.

- Embedded insurance disrupts broker led distribution because operators can buy coverage inside software workflows. This reduces friction for small buyers and gives platforms more control over customer relationships.

- Telemetry based underwriting disrupts flat rate pricing because flight logs can reveal real behavior and environment risk. Safer operators may receive better pricing while high risk missions become more expensive.

- Autonomous docking disrupts claims assumptions because drones can fly more frequently with less manual oversight. Higher utilization raises loss probability and increases demand for maintenance linked coverage.

Drone Insurance Future Market Transformation

By 2035, drone insurance will be transformed from a static annual policy product into an operational risk service. Policies will increasingly adjust to flight frequency, route type, payload value, pilot history and regulatory approval status. Enterprise buyers will expect dashboards showing coverage, incidents, compliance status and renewal exposure across fleets. Insurers will package liability, hull, payload, cyber and business interruption in modular structures. Distribution will shift toward embedded models inside flight planning and fleet software. The business model will also move from reactive claims payment to loss prevention, using telemetry and safety scoring to reduce incidents and improve premium accuracy.

Drone Insurance Market Growth Dynamics

Drone Insurance Market Drivers

- Commercial drone adoption is expanding insured exposure because construction, utility, agriculture and media users increasingly need liability cover before operating near people, assets or customer property. This raises recurring demand for annual and project specific policies.

- BVLOS regulation is accelerating market growth because longer range operations carry higher liability and operational risk. As approvals increase, fleet owners will need more sophisticated coverage for remote pilots, autonomous missions and third party services.

- Digital underwriting platforms are expanding access by offering hourly, daily and monthly policies. This lowers adoption friction for occasional pilots and turns insurance from a broker led purchase into a transaction embedded in flight planning.

- Enterprise procurement rules are raising insurance requirements because clients increasingly request certificates, additional insured status, hull cover and data liability terms before contracting drone service providers for sensitive site operations.

Driver Impact Assessment

| Driver | Market Growth Impact (%) | Demand Concentration | Impacted Use Case | Strategic Impact |

| Commercial drone adoption | 3.20% | Construction, utilities, agriculture, media operators | Liability coverage for job sites, aerial surveying, inspections, and imaging operations | Converts drone insurance from an optional expense into a standard operational requirement for commercial projects and contracts. |

| BVLOS regulatory normalization | 2.70% | North America, Europe, Australia, enterprise drone fleets | Long-range infrastructure inspection, delivery services, surveillance, and mapping | Increases insurance limits, encourages fleet-wide policies, and drives development of advanced risk assessment and enterprise coverage solutions. |

| Digital on-demand underwriting | 2.10% | Small businesses, recreational pilots, freelance operators, occasional commercial users | Hourly, daily, or mission-specific flight insurance | Expands the addressable customer base by reducing purchase friction, enabling flexible coverage, and supporting pay-per-flight insurance models. |

| Enterprise compliance requirements | 1.90% | Large enterprises, industrial asset owners, public agencies, infrastructure operators | Vendor qualification, contract compliance, named insured endorsements, certificate of insurance | Strengthens annual policy renewals, increases broker participation, and embeds insurance as a mandatory component of enterprise procurement and risk management. |

Drone Insurance Market Restraints

- Limited actuarial history restrains pricing confidence because many drone operations are new and claims data remains fragmented across payload types, pilot skill levels and operating environments.

- Regulatory fragmentation raises compliance costs because operators face different insurance expectations across countries, states, cities and client contracts. This increases policy complexity and slows multinational fleet purchasing.

- Premium sensitivity limits uptake among recreational pilots and small operators, especially when liability coverage is perceived as optional for low frequency flights or low value drone assets.

- Exclusions and coverage gaps restrain buyer confidence when policies do not clearly address privacy, cyber, payload loss, autonomous operations or flights beyond standard regulatory permissions.

Drone Insurance Market Restraint Impact Assessment

| Restraint | Drag on Market Growth (%) | Primary Impact Area | Impacted Use Case | Strategic Impact |

| Limited actuarial data | 2.40% | Pricing accuracy and risk assessment | New commercial missions, autonomous operations, and advanced drone applications | Leads insurers to adopt conservative underwriting practices, resulting in higher premiums and slower policy innovation for emerging drone use cases. |

| Regulatory fragmentation | 2.10% | Cross-border compliance and policy standardization | Multinational drone fleet operations and international commercial deployments | Increases reliance on brokers and local insurers, complicates policy administration, and delays the rollout of standardized global insurance programs. |

| Premium sensitivity | 1.80% | Adoption among small operators | Recreational flying, startups, and occasional commercial drone missions | Discourages insurance purchases among cost-sensitive users, leaving a significant portion of operators uninsured or underinsured. |

| Coverage exclusions | 1.60% | Buyer confidence and claims certainty | Privacy liability, cyber risks, payload protection, and BVLOS operations | Drives demand for clearer, modular insurance products with customizable endorsements to address evolving operational and regulatory risks. |

Drone Insurance Market Emerging Drone Insurance Growth Factors

Emerging growth factors show where drone insurance demand is broadening beyond standard liability coverage as BVLOS operations fleet programs data analytics and commercial mission complexity reshape underwriting priorities globally today.

- Flight telemetry is becoming a pricing input because insurers can use mission records, route data and safety behavior to improve underwriting accuracy for both small operators and enterprise fleets.

- Drone fleet management platforms are becoming insurance distribution channels by connecting aircraft records, pilots, compliance checks and proof of insurance in one workflow.

- Autonomous docking stations are creating new recurring coverage needs because drones can operate repeatedly without manual launch, increasing utilization and raising equipment liability exposure.

- Payload value inflation is lifting premiums because advanced sensors, mapping tools and delivery modules often exceed the drone hull value and require separate coverage.

Drone Insurance Market Segmentation Analysis

Drone Insurance Market by Coverage Type Trends

Liability insurance is the major segment because most commercial customers require proof of third party liability before a pilot can operate near assets, workers or public spaces. The segment is being shaped by rising contract compliance, higher liability limits and growing concern around privacy claims. Hull and payload coverage are expanding as sensors become more expensive, yet liability remains the gateway policy for most buyers. The market is headed toward bundled coverage where liability, hull, payload and data risks are configured in modular packages for different mission categories.

Drone Insurance Market by Policy Type Trends

Annual policies currently account for the strongest premium base because commercial operators need continuous coverage for recurring contracts, fleet work and vendor approval. The major trend is the rise of flexible on demand policies that support occasional pilots and project based work. Monthly and hourly products are expanding market access, yet annual fleet programs are becoming more valuable for enterprises. The market is headed toward hybrid policy structures that combine annual base liability with mission based add ons for payload, BVLOS exposure and client specific requirements.

Drone Insurance Market by Application Trends

Construction and infrastructure inspection is a major application because drones are widely used for site monitoring, roof inspection, tower assessment and asset mapping. This segment is influenced by client procurement rules that require certificates before site entry. Energy, utilities and agriculture are also gaining momentum as inspection frequency rises. The market is headed toward application specific underwriting where premiums reflect operating height, people exposure, asset criticality and payload value rather than a generic drone category.

Drone Insurance Regional Market Analysis

North America Drone Insurance Market

North America leads the Drone Insurance Market because the US and Canada combine large commercial drone fleets, mature aviation insurance capacity and clear procurement standards for commercial UAV services. The US market is especially shaped by Part 107 operations, public safety drone adoption, infrastructure inspection and growing interest in BVLOS missions. The August 2025 FAA BVLOS proposal strengthens long term demand because utilities, rail operators, logistics firms and energy companies will require higher liability limits and better documentation for long range operations. Production capacity changes in the region are linked less to aircraft manufacturing and more to underwriting capacity, broker digitization and insurtech distribution. Demand is moving from one off photographer policies toward annual fleet programs with named insured endorsements, hull coverage and payload protection. The region also shows strong demand for on demand coverage because smaller operators want fast certificates for project access. By 2035, North America is expected to remain the largest market, with deeper integration between insurance, flight software and enterprise vendor compliance.

Europe Drone Insurance Market

Europe is a mature Drone Insurance Market with demand concentrated in the UK, Germany, France, Spain, Italy and the Nordics. The region is shaped by EASA drone categories, privacy requirements and strong aviation insurance traditions. Buyers often require compliant liability cover before commercial operation, especially for inspections, mapping and public sector work. Production capacity changes are reflected in growing broker specialization and pan European policy wording that supports cross border operations. Demand is increasing in energy inspection, construction, agriculture and media, while recreational coverage remains relevant in countries with active hobbyist communities. Europe is also seeing stronger appetite for privacy liability and cyber add ons because drone data collection intersects with strict data protection expectations. By 2035, market growth will depend on harmonized compliance support, scalable digital distribution and policies tailored for autonomous inspection and infrastructure monitoring.

Asia Pacific Drone Insurance Market

Asia Pacific is the fastest growing Drone Insurance Market because drone deployment is accelerating in China, Japan, India, South Korea and Australia across agriculture, logistics, disaster response, inspection and public safety. The region has rising drone manufacturing capacity, expanding enterprise adoption and increasing regulatory attention to safe commercial operations. Demand changes are strongest in agriculture and infrastructure, where drone services are becoming more frequent and insurers are beginning to support commercial fleet coverage. Japan and Australia are developing advanced use cases around remote inspection and delivery pilots, while India is scaling drone services through manufacturing and agriculture programs. China has deep UAV production and enterprise usage, creating opportunities for hull, payload and liability cover. By 2035, Asia Pacific is expected to gain share as regulation matures and operators shift from informal risk acceptance to formal insurance procurement.

Drone Insurance Country-Level Market Analysis

United States Drone Insurance Market Size/Forecast

The United States is the largest country specific drone insurance market due to high commercial drone registrations, widespread enterprise adoption and mature specialty aviation carriers. Demand is strongest in construction, utilities, real estate, media, public safety and infrastructure inspection. The FAA BVLOS proposal in August 2025 is expected to accelerate demand for fleet policies, higher liability limits and underwriting based on safety documentation. Production capacity changes are seen in insurtech platforms, broker portals and aviation carrier capacity rather than physical drone manufacturing alone. The US market is forecast to remain the global anchor for usage based policies and embedded proof of insurance workflows through 2035.

Japan Drone Insurance Market Size/Forecast

Japan is a high potential drone insurance market because the country is using drones for infrastructure inspection, disaster response, agriculture and logistics in areas affected by labor shortages and aging infrastructure. Demand is rising for policies that support safe operations near public assets and remote regions. Japan is also an important market for structured regulatory frameworks and enterprise compliance. Insurance growth is expected to follow expansion in remote inspection, delivery pilots and municipal drone use. Production capacity changes are linked to domestic drone technology, robotics capabilities and service providers that need hull, liability and payload coverage for recurring missions.

China Drone Insurance Market Size/Forecast

China is one of the most important country specific drone insurance markets because it combines large UAV manufacturing capacity, strong enterprise adoption and expanding use in agriculture, logistics, infrastructure and public safety. Insurance penetration is still developing compared with drone deployment volume, which creates a large growth gap. Demand is expected to move from basic aircraft protection toward commercial liability, payload and fleet policies as drone services become more formalized. Domestic production scale lowers drone hardware cost, yet higher utilization increases accident and liability exposure. By 2035, China is expected to be one of the largest incremental growth contributors in Asia Pacific.

India Drone Insurance Market Size/Forecast

India is an emerging drone insurance market supported by policy focus on domestic drone manufacturing, agriculture services, infrastructure mapping and public sector use. Demand is moving from project level cover toward more formal risk transfer as drone service providers work with government agencies, enterprise clients and agricultural programs. Insurance penetration remains early because many operators are small and price sensitive, yet procurement requirements are improving awareness. Production capacity is rising through local UAV manufacturing and service ecosystems. By 2035, India could become a high growth market for low cost liability coverage, fleet insurance and embedded insurance sold through drone service platforms.

Drone Insurance Market Other Key Countries

- United Kingdom Drone Insurance Market: The UK has a mature insurance environment, strong commercial drone adoption and specialist providers such as Coverdrone. Demand is focused on liability, hull and compliant cover for commercial pilots working in media, inspection, surveying and public sector missions.

- Germany Drone Insurance Market: Germany is shaped by industrial inspection, energy infrastructure, logistics pilots and strict operational compliance. Buyers favor robust liability policies and broker supported coverage for enterprise drone use across manufacturing, utilities and engineering applications.

- Australia Drone Insurance Market: Australia is expanding drone use across mining, agriculture, energy and remote infrastructure. The country supports strong demand for fleet policies because operators often fly in remote areas with expensive payloads and critical asset inspection requirements.

- Brazil Drone Insurance Market: Brazil is the leading Latin American opportunity due to agriculture, mining, construction and environmental monitoring. Insurance demand is rising as commercial drone services mature and enterprise clients request liability coverage for field operations.

- United Arab Emirates Drone Insurance Market: The UAE is a premium opportunity due to smart city programs, construction, energy inspection and advanced aviation policy focus. Demand is strongest for professional liability cover, fleet operations and high value commercial missions.

Drone Insurance Market Competitive Landscape

Drone Insurance Market Competitive Benchmarking

Competitive benchmarking shows a split between aviation capacity providers and digital distribution platforms. The most successful players combine specialized claims expertise, flexible policy duration and strong access to commercial drone operators.

- Global Aerospace focuses on aviation backed capacity, fleet coverage and worldwide UAS experience, targeting commercial operators that need reliable claims support and scalable liability protection.

- SkyWatch.AI focuses on digital quote and bind, flexible hourly, monthly and annual plans, targeting small commercial pilots and operators that need fast certificates.

- Coverdrone focuses on specialist commercial and recreational drone insurance, with a strong European presence and coverage for liability, hull, equipment and privacy related exposures.

- Allianz Commercial targets larger aviation and enterprise accounts through global underwriting reach, specialist claims capability and integration with broader aviation risk programs.

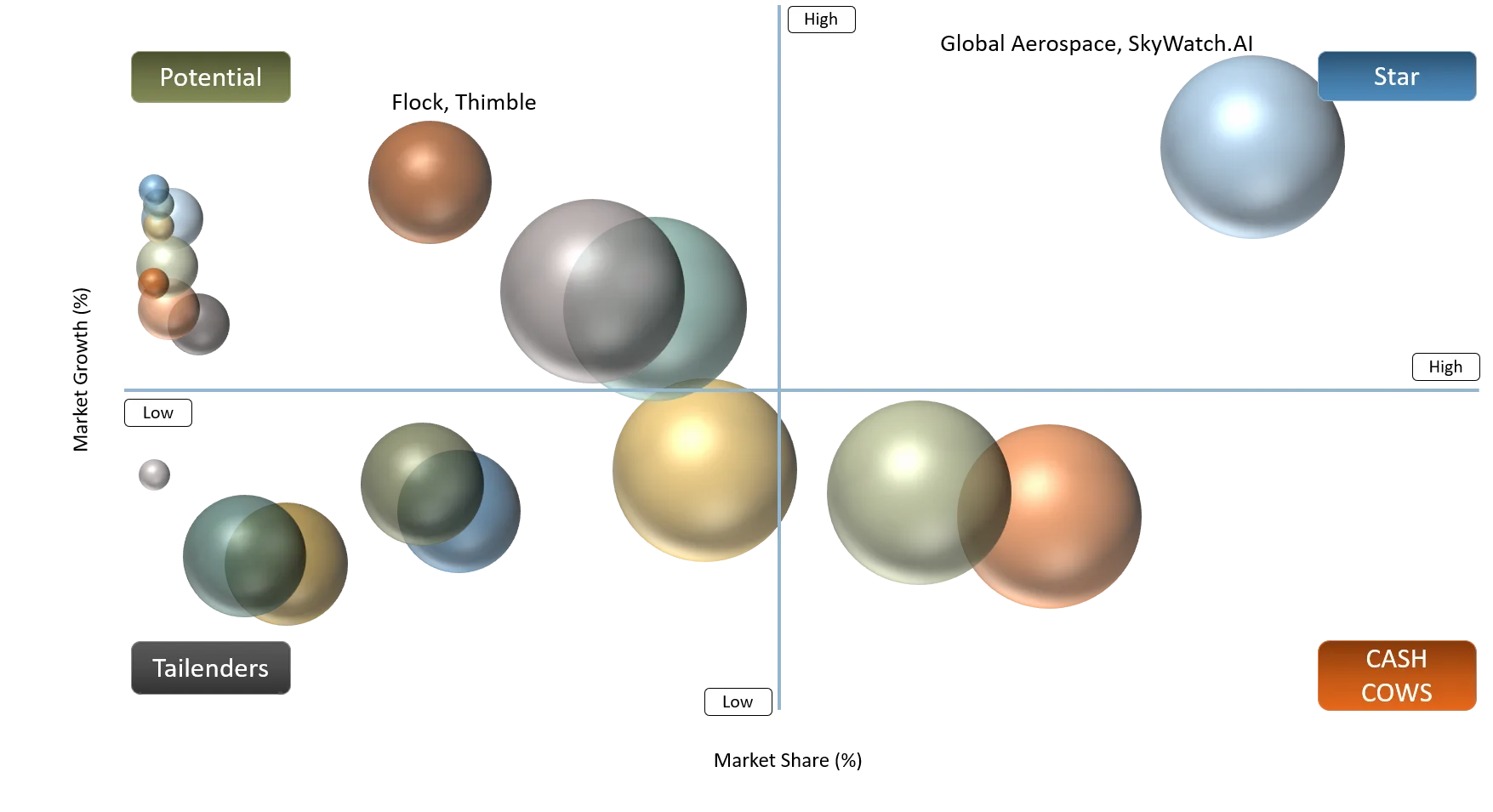

Drone Insurance Market BCG Matrix List

Stars: Global Aerospace, SkyWatch.AI

Question Marks: Flock, Thimble

Cash Cows: Allianz Commercial, AIG Aerospace

Niche Players: Coverdrone, BWI Aviation Insurance

Drone Insurance Market BCG Matrix Analysis

Stars such as Global Aerospace and SkyWatch.AI are positioned strongly because they combine high visibility in drone coverage with differentiated distribution models. Global Aerospace benefits from aviation capacity, claims depth and fleet programs, while SkyWatch.AI benefits from digital access and flexible policy formats. Cash Cows such as Allianz Commercial and AIG Aerospace have strong balance sheets, aviation expertise and enterprise broker relationships, yet drone insurance is one part of a wider aviation portfolio. Question Marks such as Flock and Thimble have digital strengths and brand relevance, although their long term drone insurance share depends on carrier partnerships and risk appetite. Niche Players such as Coverdrone and BWI Aviation Insurance retain strong specialist appeal because they understand pilot needs, compliance wording and equipment risks. Their challenge is scaling globally while maintaining specialist service quality.

Drone Insurance Market Company Profiles & Strategy Analysis

Drone Insurance Market Expansion & Partnership Strategy

- May 2026 Coverdrone strengthened broker engagement through a specialist appointment, signaling continued investment in broker relationships and distribution education for commercial and recreational drone insurance buyers.

- August 2025 FAA BVLOS rulemaking created a strategic catalyst for insurer partnerships with fleet software, UTM providers and enterprise drone operators that need compliance linked insurance programs.

- 2025 SkyWatch and Global Aerospace continued their carrier partnership model for on demand drone insurance, improving distribution reach and giving digital buyers access to aviation backed capacity.

- 2025 Allianz and Transport Risk continued promoting UAS safety technology partnerships, reinforcing the role of risk management data in insurance pricing and loss prevention.

Drone Insurance Market Major Industry Developments

Industry developments in 2025 and 2026 show that regulatory normalization, broker digitization and stronger distribution partnerships are shaping the market. These changes improve buyer confidence and expand the addressable market for higher value coverage.

- August 2025: The FAA released a proposed BVLOS rule, creating a path for more normalized long range drone operations and raising demand for enterprise fleet insurance.

- May 2026: Coverdrone strengthened broker engagement through a specialist appointment, supporting wider intermediary education and better distribution for drone insurance products.

- June 2026: Federal drone policy discussions in the US focused on BVLOS, public event restrictions and communication rules, keeping drone liability and compliance in the spotlight.

- 2025: SkyWatch and Global Aerospace continued promoting digital on demand drone insurance backed by aviation capacity, improving access for small commercial and recreational users.

Drone Insurance Recent Market Announcements

August 2025 FAA BVLOS proposal is the most important recent market announcement because it creates a regulatory pathway for normalized beyond visual line of sight drone operations in the US. This matters directly for drone insurance because BVLOS flights increase mission distance, operating complexity and third-party exposure. Utilities, logistics firms, rail operators and public agencies will need stronger liability protection, fleet documentation and underwriting data before scaling these operations. The announcement also encourages insurers to develop products for autonomous supervision, route risk, UTM services and enterprise fleet management. Its market impact is likely to be long term, especially for high value commercial use cases.

Drone Insurance Market Technology Launches & Partnerships

Technology launches and partnerships are making drone insurance more connected to digital aviation workflows. The most impactful moves link underwriting capacity, platform access and operational data so buyers can obtain coverage faster.

- 2025 SkyWatch and Global Aerospace partnership supported on demand drone insurance, linking digital distribution with aviation backed underwriting capacity.

- 2025 to 2026 UASidekick related insurance partnerships highlighted the role of safety technology and compliance data in reducing risk and supporting insurance discounts.

- May 2026 Coverdrone broker engagement expansion strengthened market education and improved access for intermediaries serving commercial drone operators.

- August 2025 FAA BVLOS rulemaking encouraged insurers and technology providers to prepare coverage models for long range autonomous operations.

Drone Insurance Market Strategic Insights & Analyst Perspective

Analyst Insights for Drone Insurance Market

From a DataM Intelligence perspective, the Drone Insurance Market is entering a more institutional phase. The first phase was driven by hobbyists and small commercial pilots buying basic liability or hull coverage. The next phase will be driven by enterprise fleets, BVLOS operations and platform based distribution. The market impact is significant because insurance will become a gatekeeper for drone adoption in high value sectors such as utilities, construction, logistics, public safety and energy. Operators will not be judged only on aircraft quality, they will also be judged on risk documentation, coverage adequacy and claims readiness. The most attractive growth will come from mission specific policies that address payload value, privacy exposure, cyber risk and long range operations. North America will retain the largest share because of FAA rulemaking and mature underwriting capacity, while Asia Pacific will deliver faster growth as drone use scales across agriculture, inspection and logistics. DataM expects the market to move toward fewer generic policies and more configurable coverage packages. Companies that combine aviation expertise with digital workflows will shape the future market. Insurers should prioritize partnerships with fleet management software, UTM providers and enterprise drone service firms. The winners will use data to reduce uncertainty while making coverage easier to buy.

Strategic Recommendations for Drone Insurance Market

Recommendation 1: Build mission specific coverage packages rather than selling generic drone policies. A company in the market should develop modular products for construction inspection, utility inspection, agriculture, media and public safety. Each package should define liability limits, hull cover, payload protection, privacy add ons and cyber coverage in clear terms. This approach improves buyer confidence because policy language matches the real use case. It also helps underwriters price more accurately by linking premiums to mission severity, site exposure and operating frequency. From a DataM Intelligence perspective, verticalized coverage will improve conversion, retention and premium per customer. Recommendation 2: Invest in embedded distribution and flight data partnerships. Drone operators increasingly manage flight planning, compliance records and equipment data inside digital platforms. Insurers should integrate quote and bind functions directly into these systems, allowing coverage to be activated when a mission is scheduled. This will reduce acquisition cost and give underwriters access to better risk signals such as route type, flight history, pilot credentials and aircraft utilization. From a DataM Intelligence perspective, embedded insurance will be especially important for small operators and enterprise fleets that need fast certificates. Companies that control workflow data will gain pricing advantage.

Drone Insurance Future Market Outlook (2035 Vision)

In 2025, the Drone Insurance Market is still weighted toward liability and hull policies for small commercial operators, recreational pilots and early enterprise fleets. Coverage is often purchased to satisfy project requirements, protect drone hardware or meet customer expectations. By 2035, the market will be more integrated, data driven and enterprise focused. BVLOS inspection, drone delivery, autonomous docking and public safety fleets will require higher liability limits, more sophisticated wording and stronger links between insurance and operational compliance. Digital platforms will become the main purchase point for small operators, while large enterprises will rely on fleet programs that combine liability, payload, cyber and business interruption protection. Regional differences will remain important, with North America leading in market share and Asia Pacific adding the most incremental demand. The major change will be that drone insurance will no longer be seen as a back office purchase. It will become a core operational enabler for autonomous aerial services.

Drone Insurance Market Target Audience

Target audience includes the value chain segments most likely to buy this report and use it for strategy, procurement, investment or market entry decisions.

- Aviation insurers and reinsurers that need market size, share, forecast and underwriting opportunity analysis for UAV risk products.

- Specialist brokers and agents that want to understand buyer priorities, competitive positioning and country specific market demand.

- Drone service providers and fleet operators that need insurance benchmarks for procurement, pricing and customer contract compliance.

- Drone software platforms that want to evaluate embedded insurance, telemetry underwriting and partnership opportunities.

- Investors and private equity firms assessing insurtech, drone services, aviation data and specialty broker acquisition targets.

- Government and public safety agencies evaluating liability exposure and procurement criteria for drone fleet programs.

- OEMs and payload manufacturers studying how insurance affects adoption of high value commercial drone equipment.

Who Should Buy this Report?

This report is designed for decision makers that need a practical view of the Drone Insurance Market, including market size, country specific market opportunity, competitive landscape, buyer behavior and growth forecast. It helps teams connect drone adoption trends with insurance demand, procurement criteria and investment priorities.

- Insurance carriers evaluating UAV product expansion.

- Reinsurers assessing specialty aviation exposure.

- Drone insurance brokers planning market entry or portfolio growth.

- Drone service providers negotiating client insurance requirements.

- Fleet management software firms exploring embedded insurance.

- Investors assessing insurtech and UAV risk platforms.

- Enterprise procurement teams setting drone vendor insurance standards.

Why Choose DataM Intelligence?

- Business outcome focus: DataM links market size, share and forecast analysis to procurement decisions, pricing strategy and market entry priorities.

- Segment depth: The report breaks down coverage type, policy type, application, region and country specific market opportunity for practical planning.

- Competitive intelligence: DataM evaluates major insurers, brokers and insurtech platforms based on portfolio, target strategy and use case focus.

- Buyer behavior insight: The analysis explains what customers prioritize when procuring drone insurance, including liability limits, certificates and claims support.

- Regulatory clarity: DataM tracks BVLOS, aviation compliance and privacy developments that directly influence market growth.

- Investment perspective: The report identifies white space areas such as embedded insurance, payload protection and telemetry based underwriting.