Drone-as-a-Service Market Overview

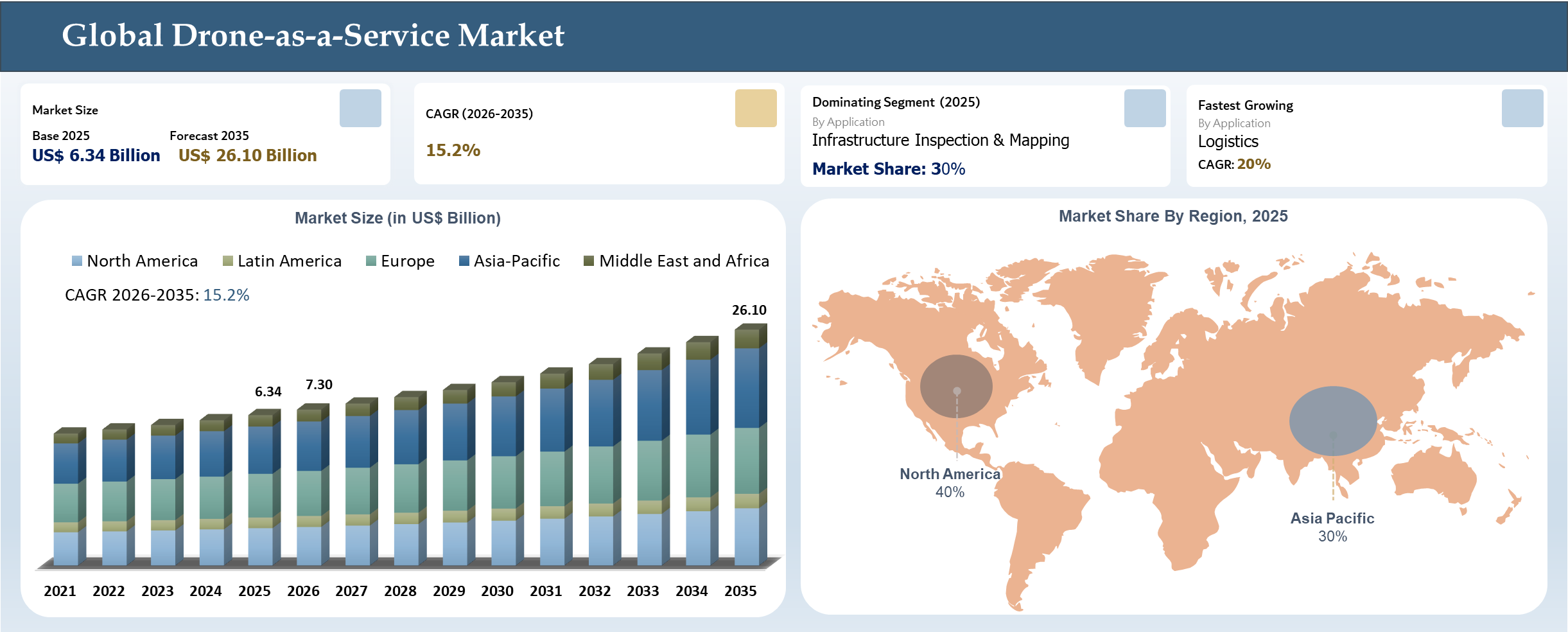

Global Drone-as-a-Service Market reached US$ 6.34 billion in 2025 and is expected to reach US$ 26.10 billion by 2035, growing with a CAGR of 15.2% during the forecast period 2026-2033. The global Drone-as-a-Service (DaaS) market is witnessing strong growth as enterprises increasingly rely on outsourced drone operations for faster data acquisition, improved operational safety, and cost-efficient asset monitoring. Industries such as energy, oil & gas, mining, and construction are shifting from manual inspections to autonomous drone services to enhance efficiency, reduce downtime, and enable predictive maintenance strategies.

Service providers are actively expanding international partnerships and large-scale deployments to capture this demand. For example, in 2025, Terra Drone Corporation strengthened its global infrastructure inspection presence by boosting cooperation with Saudi Aramco to conduct drone-based inspections of oil and gas facilities, marking a significant step toward full-scale industrial deployment. Such advancements highlight how DaaS companies are securing long-term industrial contracts and positioning drone services as a core component of modern infrastructure management.

Drone-as-a-Service Industry Trends and Strategic Insights

- The Drone-as-a-Service industry is fast evolving from the traditional model based on hardware procurement to one based on subscriptions involving autonomous flights mainly within infrastructure inspection, agriculture, mining, logistics, and public safety sectors.

- Commercial DaaS in North America and Europe is being driven by the increasing acceptance and implementation of autonomous drone corridors and industrial inspections due to the rising regulatory backing for such operations. In China, rapid expansion of low-altitude economic zone infrastructure, logistics operations and smart city aerial services have been fueled by changes in aviation regulations and government-led commercialization efforts.

- Competition has evolved to become more about AI fleet management, geospatial analytics and application-based service offerings rather than being solely focused on drone production. Leading companies are concentrating on building analytical platforms integrating autonomous operations, predictive maintenance intelligence, and cloud-edge management to win business contracts.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 6.34 Billion | |

| 2035 Projected Market Size | US$ 26.10 Billion | |

| CAGR (2026-2035) | 15.2% | |

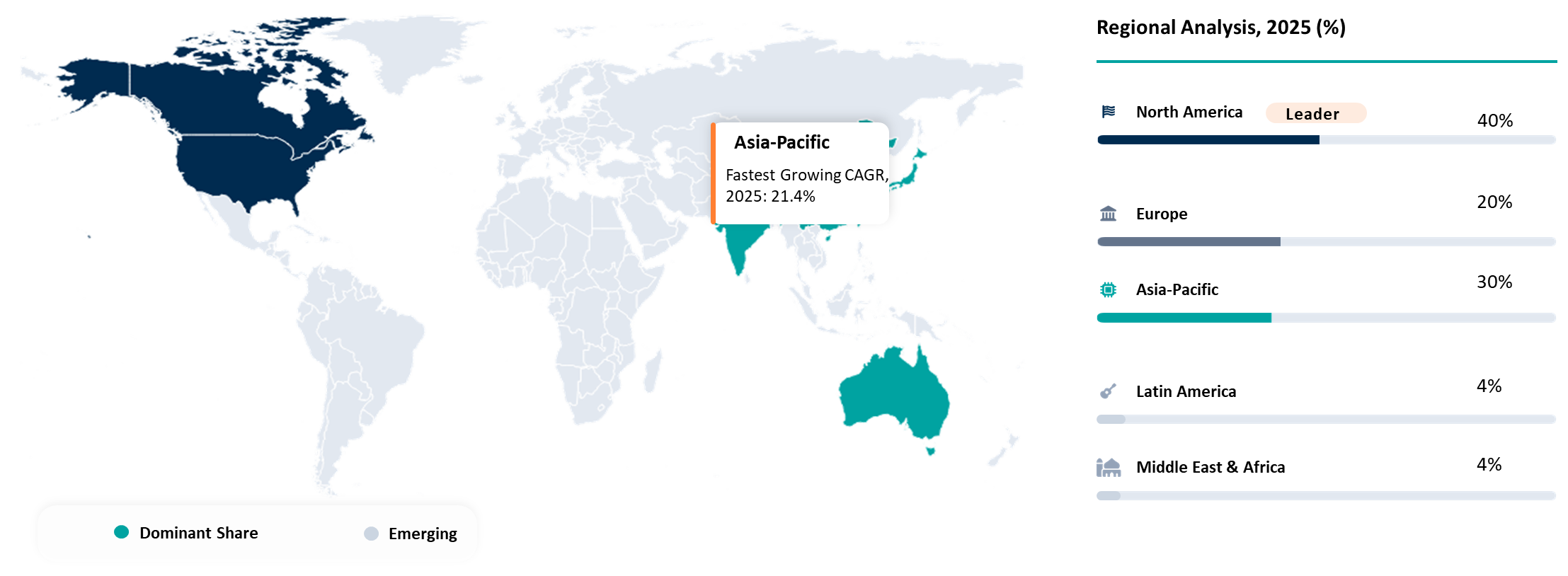

| Largest Market | North America | |

| Fastest Growing Market | Asia-Pacific | |

| By Business Model | Subscription-Based Access, Task-Based, Pay-Per-Use, Fully Managed Services | |

| By Application | Agriculture, Defense, Logistics, Infrastructure, Inspection and Mapping, Energy and Utilities, Public Safety and Security, Media and Entertainment, Others | |

| By Drone Type | Fixed-Wing Drones, Rotary-Wing Drones, Hybrid Drones | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Disruption Analysis

Shift Toward Autonomous Drone Networks Reshaping Service Delivery Models

A significant disruptor in the industry is the shift from manned drones to autonomous drone networks that can carry out operations on a massive scale without much human interference. The adoption of autonomous drone fleets integrated with AI and cloud technologies is changing the dynamics of service efficiency and effectiveness. In such cases, companies that do not have autonomy technology in their portfolio are likely to see their competitiveness eroded in high-demand use cases.

The regulatory framework that facilitates beyond visual line of sight operations and urban air mobility integration. Regulatory authorities are becoming more supportive towards the establishment of drone corridors and automated traffic management systems to unlock additional growth opportunities. These regulatory changes are opening new doors for companies looking to offer DaaS services by offering them access to new markets.

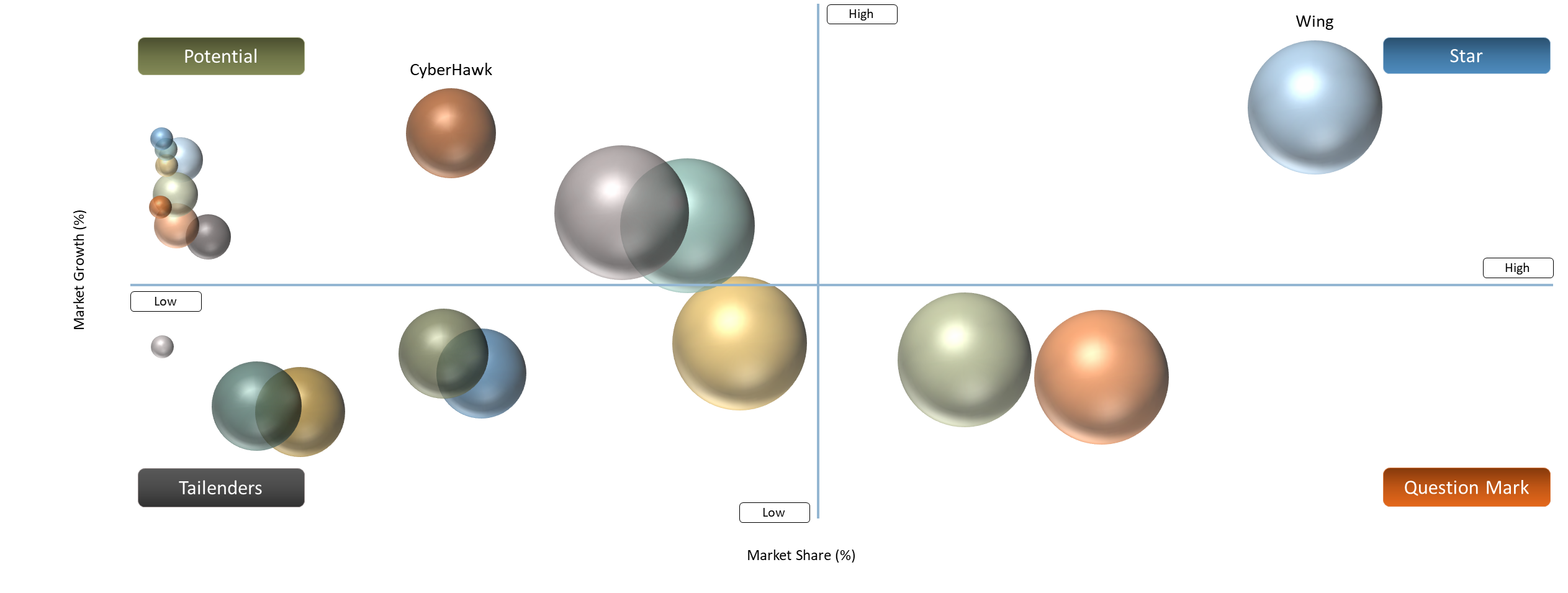

BCZ Matrix: Company Evaluation

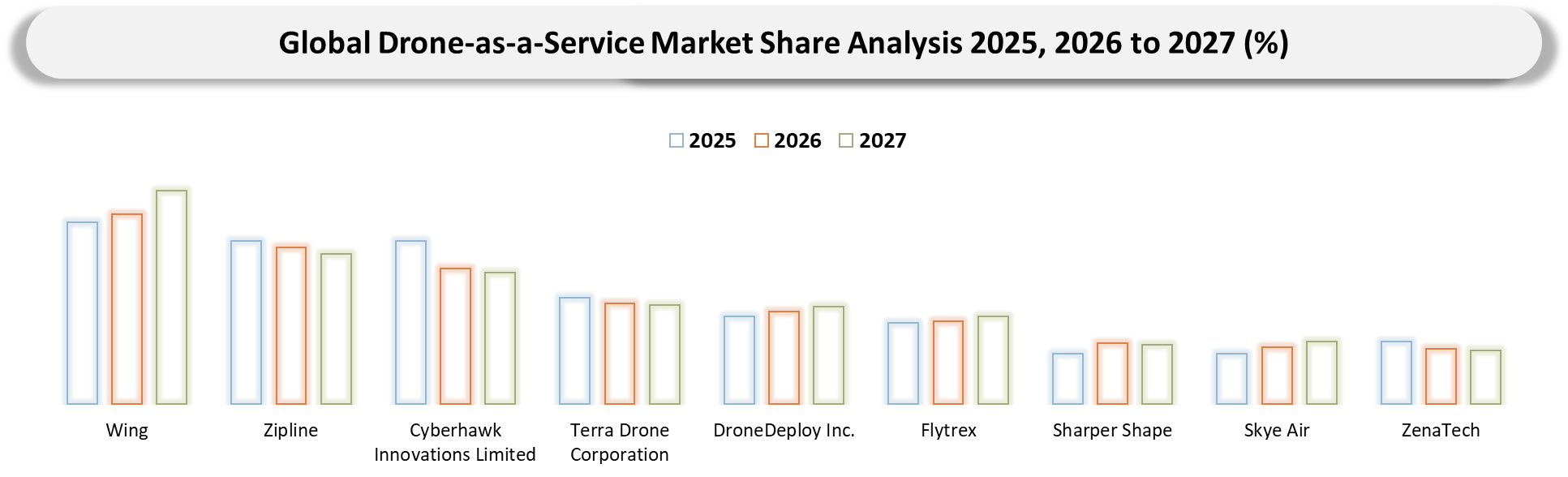

The Stars and Question Marks categories showcase firms that achieve scale through deployment coupled with complex regulatory and operational issues. Star category includes firms like Wing, Zipline, and Terra Drone Corporation which have established themselves through leadership roles in network deployment, infrastructure inspection, global expansion plans, solid financing, and strong partnerships. The fact that such firms can conduct operations in logistics and healthcare delivery makes them better at achieving revenues. The firms grouped in Question Mark category include DroneDeploy Inc., Flytrex, and Skye Air which, despite having robust platforms and local presence, are facing challenges in scalability and regulation issues in other markets.

The Potential Players and Tail Enders category includes niche players and emerging players with relatively poor global presence. Firms like Cyberhawk Innovations Limited, Sharper Shape, and ZenaTech, despite being involved in industrial inspection, data analytics, and artificial intelligence technology in drones respectively, belong to this category since their scaling is hampered by client dependence.

Market Dynamics

Rising Demand for Precision Agriculture and Crop Health Monitoring

The Drone-as-a-Service market is expanding rapidly as AI-driven precision agriculture solutions gain widespread adoption. Farms are increasingly using drones equipped with advanced sensors and machine-learning analytics to monitor crop health, optimize irrigation, and reduce fertilizer and pesticide usage. These technologies are improving productivity while significantly lowering operational costs.

AI-driven analytics are projected to reduce agricultural input costs by 25% in 2025, while optimized irrigation models can cut water usage by up to 30%. Studies indicate a 15–20% increase in crop yields compared to conventional methods, with specialized drones reducing chemical usage by up to 35%. Over 70% of large-scale farms in developed countries are estimated to use at least one AI-based agricultural technology, highlighting strong adoption momentum. Drones can scan up to 1,000 acres per day, delivering real-time actionable insights for farmers. In the U.S., registered agricultural drones increased sharply from 1,000 in January 2024 to nearly 5,500 by July 2025, reflecting accelerating deployment. Overall, rising food security concerns, climate variability, and the need for cost-efficient farming practices are driving strong demand for drone-enabled crop monitoring services globally.

Data Security, Privacy, and Regulatory Compliance Challenges

The Drone-as-a-Service market faces growing concerns despite adoption, around data privacy, cybersecurity, and regulatory compliance. Drones capture high-resolution imagery, geospatial intelligence, and sensitive infrastructure data, raising risks related to unauthorized access, data breaches, and surveillance misuse. Enterprises operating in energy, defense, agriculture, and smart city projects are particularly cautious about how aerial data is stored, transmitted, and processed.

Cross-border data transfer restrictions and evolving aviation regulations further complicate compliance requirements for service providers. Concerns over cloud storage vulnerabilities and cyberattacks on drone communication networks add additional risk. Public perception issues surrounding surveillance and privacy rights also create adoption hesitations in urban environments. These challenges make enterprises more selective, often preferring providers with strong encryption, secure cloud partnerships, and regulatory certifications, increasing operational complexity for smaller DaaS vendors.

Segmentation Analysis

The global drone-as-a-service market is segmented based on business model, application, drone type, and region.

AI-Driven Autonomous Infrastructure Inspection Solutions Strengthening Market Dominance

Infrastructure Inspection & Mapping is driving strong demand in the global Drone-as-a-Service (DaaS) market with 30% share, as enterprises and governments seek accurate, real-time aerial data for asset monitoring, predictive maintenance, and risk reduction. Drone-based inspection services provide high-resolution imaging, thermal scanning, and AI-powered analytics that significantly reduce manual inspection costs, improve worker safety, and enhance operational efficiency across utilities, construction, oil & gas, and transportation infrastructure. These advantages are a major reason why infrastructure-intensive industries increasingly rely on drone inspection services for performance-critical asset management.

Drone technology providers are actively advancing autonomous inspection platforms to meet this demand. For example, in 2025, Percepto launched an AI-powered solution for electric utilities, enabling continuous autonomous drone monitoring of grid infrastructure with real-time data analytics and automated anomaly detection. Such advancements demonstrate how intelligent, AI-driven drone inspection systems are strengthening the dominance of the Infrastructure Inspection & Mapping segment as organizations prioritize scalable, data-driven infrastructure management solutions.

Rapid Commercialization of Last-Mile Drone Delivery Accelerating Logistics Segment Growth

The logistics segment is emerging as the fastest-growing application with 15% share in the Drone-as-a-Service (DaaS) market, driven by expanding urban drone corridors, increasing BVLOS approvals, and rising demand for faster, cost-efficient last-mile fulfillment. Growing integration between drone operators and major delivery platforms is transforming aerial logistics from pilot programs into scalable commercial services.

For instance, in May 2025, Wing and DoorDash expanded drone delivery operations by launching commercial drone deliveries in Charlotte, North Carolina, demonstrating increasing real-world adoption of aerial logistics for last-mile services. Such deployments highlight how regulatory support and enterprise partnerships are accelerating commercial drone logistics adoption globally.

Geographical Penetration

Rapid Expansion Driven by Infrastructure Development and Aerial Data Demand

The Asia-Pacific Drone-as-a-Service (DaaS) market is the fastest-growing region in the global market, holding around 30% share in 2025, driven by rapid infrastructure investment, urbanization, and increasing demand for aerial data across agriculture, construction, energy, and logistics sectors. Governments and private enterprises in Asia-Pacific are actively supporting drone adoption through regulatory enhancements, industry events, and public-private collaborations that accelerate use cases for aerial inspection, delivery, and monitoring services.

For instance, in 2026, ST Engineering, a Singapore-based aerospace and technology company, unveiled the DrN-600 medium-lift cargo drone at the Singapore Airshow, showcasing advanced cargo and industrial UAV capabilities designed for logistics and infrastructure support across the region. Other regional developments include expanded commercial drone demonstrations at major trade shows and increased partnerships between local providers and government agencies to deploy drones for smart city applications, agriculture monitoring, and critical infrastructure inspection.

Japan Drone-as-a-Service Market Outlook

Japan’s Drone-as-a-Service (DaaS) industry strengthened its regional and international footprint through expanded infrastructure inspection partnerships and technology deployments. Japanese drone providers are leveraging advanced UAV platforms and aerial analytics to support industrial clients at home and abroad, particularly in energy and critical infrastructure sectors.

For instance, in April 2025, Terra Drone Corporation, a Japanese drone technology company, boosted cooperation with Saudi Aramco by signing an agreement to conduct drone-based inspections of oil and gas facilities, with pilot runs scheduled during 2025 and full-scale deployment expected thereafter. This collaboration illustrates how Japan’s drone services ecosystem is extending beyond domestic applications to high-value international infrastructure inspection contracts, reinforcing Asia-Pacific’s rapid DaaS market expansion.

China Drone-as-a-Service Market Trends

China continues to strengthen its position in the global Drone-as-a-Service (DaaS) market in 2025–2026, driven by aggressive international expansion and growing demand for industrial and emergency response UAV solutions. Domestic manufacturers are leveraging mature production capabilities and advanced drone technologies to capture export markets and infrastructure service contracts abroad.

For instance, in early 2026, Aerospace Times Feipeng, a leading Chinese drone maker, ramped up its global expansion by entering markets in Southeast Asia, the Middle East, and Europe, showcasing high-end inspection, surveillance, and rescue drones and aiming to increase overseas sales amid fierce competition in its home market. These moves reflect China’s broader strategic push to export drone technology and establish regional partnerships that support infrastructure monitoring, public safety applications, and commercial aerial services across international markets.

Rising Commercial Drone Deployment and Regulatory Advancements in North America

North America is the dominant region with approximately 40% share in 2025 in the global Drone-as-a-Service (DaaS) market, driven by strong regulatory frameworks, early commercialization of drone delivery, and growing enterprise and defense adoption. The region benefits from advanced aviation infrastructure, increasing BVLOS approvals, and rapid expansion of last-mile delivery partnerships. For instance, Regulatory advancements led by the Federal Aviation Administration (FAA) and supportive state aviation authorities are significantly lowering operational barriers for commercial drone deployments across the United States. Increasing approvals for Beyond Visual Line of Sight (BVLOS) operations are enabling drone operators to conduct longer-range, autonomous flights without requiring direct visual monitoring, which is critical for scalable logistics and infrastructure inspection services.

U.S. Drone-as-a-Service Market Insights

The United States remains the largest contributor to regional revenue, supported by the rapid commercialization of drone deliveries, defense modernization programs, and smart city initiatives. For instance, in 2025, Uber Eats and Flytrex, U.S.–based companies, partnered to expand drone food delivery trials across select markets, marking a significant step in commercial drone delivery services and integrating autonomous aerial logistics with mainstream food delivery platforms. Strengthening last-mile delivery capabilities in select U.S. suburbs, accelerating enterprise confidence in scalable DaaS models across logistics and e-commerce sectors.

Canada Drone-as-a-Service Industry Growth

Canada is witnessing steady growth in Drone-as-a-Service adoption, particularly across defense, public safety, and government applications. For instance, in 2025, ZenaTech, a Canada–based drone technology company, launched its Drone-as-a-Service (DaaS) offerings for U.S. defense and government agencies through new strategic partnerships, accelerating the adoption of enterprise and public-sector drone applications. Canada’s strong aerospace ecosystem, supportive regulatory framework, and innovation-driven drone companies are positioning the country as a key contributor to North America’s DaaS market growth.

Sustainability Analysis

The Drone-as-a-Service (DaaS) market is shaped by aviation safety, airspace control, and data protection regulations worldwide. In the U.S., the Federal Aviation Administration enforces 14 CFR Part 107 and the Remote ID Rule (Part 89), mandating pilot certification, operational limits, and drone identification for commercial use. Waivers for Beyond Visual Line of Sight (BVLOS) operations are expanding commercial opportunities but increasing compliance and equipment costs.

In the EU, the European Union Aviation Safety Agency regulates drones under Regulations (EU) 2019/947 and 2019/945, categorizing operations by risk and standardizing cross-border services. The General Data Protection Regulation (GDPR) further restricts aerial data collection and processing, impacting surveillance-based DaaS models. In India, the Directorate General of Civil Aviation implements the Drone Rules, 2021, through the Digital Sky Platform, simplifying approvals while enforcing geofencing and registration norms. China’s Civil Aviation Administration mandates strict registration and cybersecurity compliance for commercial drone operations. Overall, these regulations enhance safety and transparency but increase operational costs while supporting structured long-term growth of the DaaS ecosystem.

Competitive Landscape

- The global drone-as-a-service market is characterized by a competitive landscape that includes both established and regional players.

- Key players include Wing Aviation LLC, Zipline International Inc., Cyberhawk Innovations Limited, Terra Drone Corporation, DroneDeploy Inc., Flytrex Inc., Sharper Shape Oy, Skye Air Inc., ZenaTech Inc.

Key Developments

- In 2025, AgEagle Aerial Systems, a U.S.-based drone and sensor technology company, advanced its global expansion by supporting Brazil’s sugarcane industry with enhanced unmanned aerial solutions, deploying high-resolution imaging and data analytics to improve crop management and operational efficiency.

- In 2025, Delair, a France-based enterprise drone manufacturer, unveiled its new DT61 drone at the Paris Air Show, showcasing advanced capabilities for industrial mapping and inspection applications that expand its service portfolio for commercial and infrastructure survey markets.

Why Choose DataM?

- Data-Driven Insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. This approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. This personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. These insights complement and go beyond what is typically available in generic databases.

Target Audience

- Manufacturers/ Buyers

- Industry Investors/Investment Bankers

- Research Professionals

- Emerging Companies