Drilling Tools Market Overview

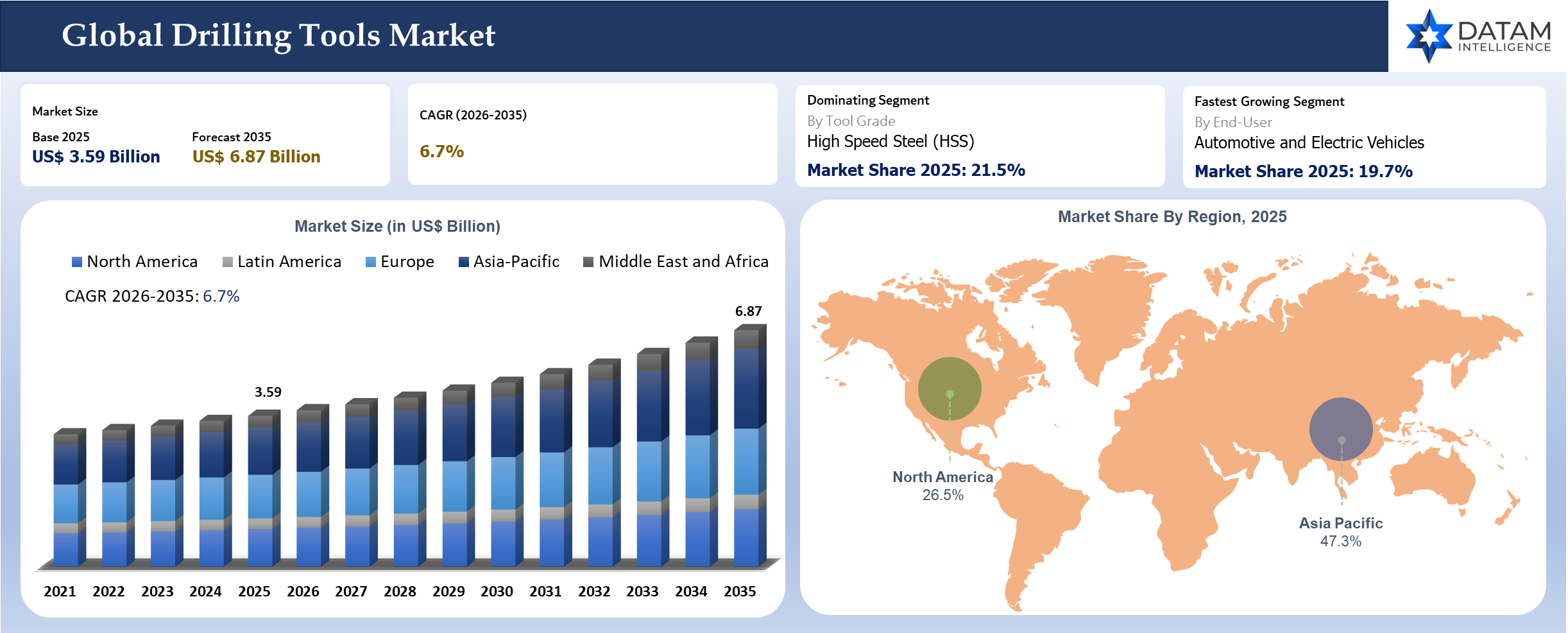

The global drilling tools market reached US$ 3.59 billion in 2025 and is expected to reach US$ 6.87 billion by 2035, growing with a CAGR of 6.7% during the forecast period 2026-2035. Drilling equipment is an important component in the process of material removal, precision hole-making and high speed machining in the industries of metal working and industrial production. Both the government and industries are heavily investing in machining processes for increased efficiency and precision of the parts being machined. As per International Energy Agency (IEA), energy investments reached over US$ 3 trillion in 2024 dedicated to upstream oil & gas production, geothermal drilling and mineral exploration all demanding drilling equipment and advanced cutting practices. Meanwhile, the manufacturing production in the world continues to grow because of industrial automation.

The increase in production of electric vehicles and renewable energy structures has also resulted in rising demand for drilling tools utilized in lightweight and composite materials, as well as high-strength alloys. Production of wind turbines, batteries, transmission lines and aerospace components requires extremely accurate drilling processes, leading to an increase in the application of carbide, coated and indexable drills. Moreover, smart factory systems and the concept of industry 4.0 promote the utilization of tooling systems that are digitally monitored and controlled.

Drilling Tools Industry Trends and Strategic Insights

- The increased adoption of high-efficiency carbide and coated drills in the production of titanium, aluminum and composites is gaining traction within the aerospace and electric vehicle manufacturing sectors, with the Asia-Pacific leading in industrial drilling applications in 2025.

- The implementation of IoT-powered drill tool management systems and predictive maintenance technology powered by artificial intelligence is revolutionizing industrial drilling operations by minimizing machine downtime and maximizing tool efficiency in large-scale manufacturing environments.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 3.59 Billion | |

| 2035 Projected Market Size | US$ 6.87 Billion | |

| CAGR (2026-2035) | 6.7% | |

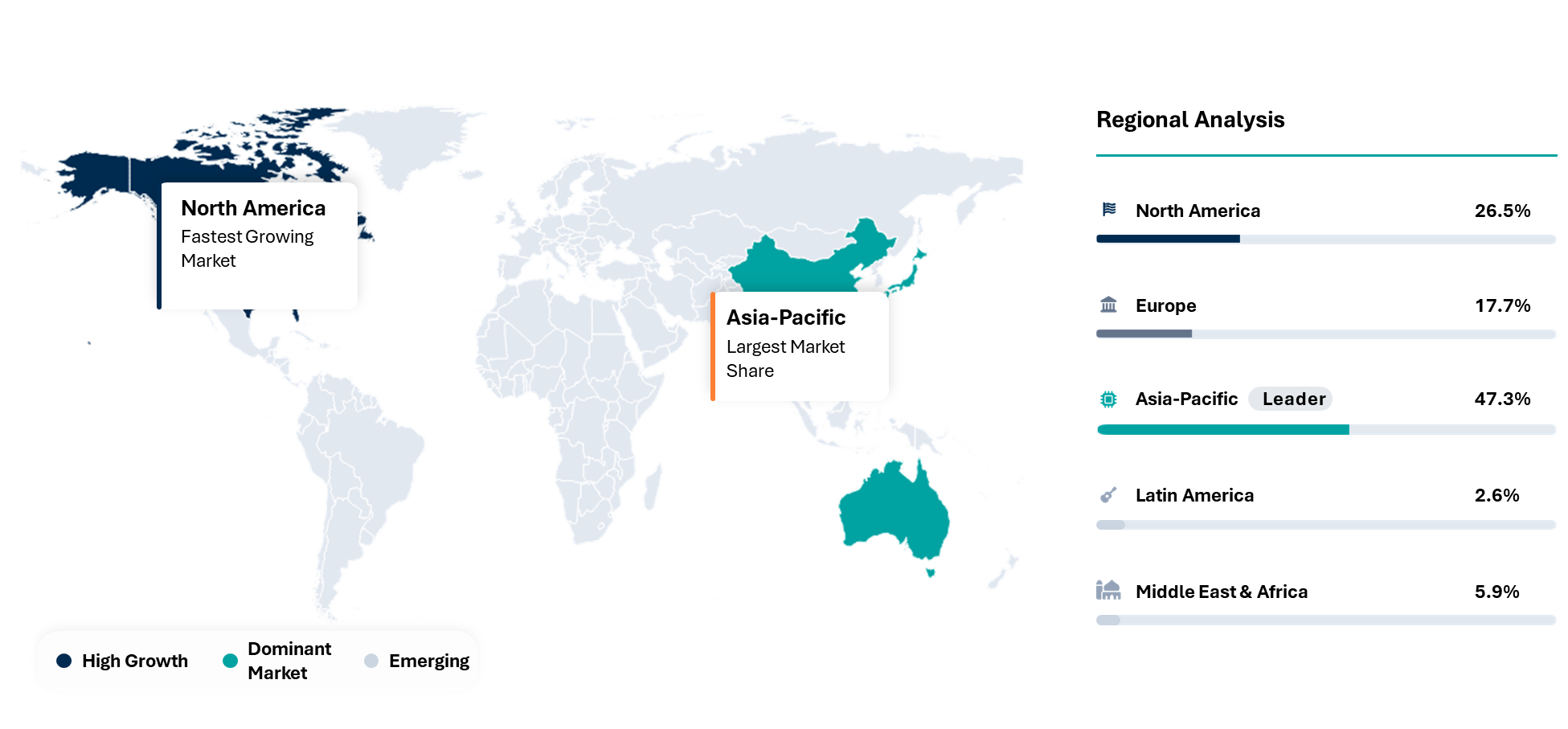

| Largest Market | Asia-Pacific | |

| Fastest Growing Market | Asia-Pacific | |

| By Tool Grade | High Speed Steel (HSS), Solid Carbide, Diamond Tools | |

| By Machine Type | 5-Axis Machining Center , Machining Center, CNC Turning Machines (Turning Center), Swiss Type Automatic Lathes (Sliding Head Lathes), Multi-Tasking Machines (Mill Turn Machines), Other | |

| By Workpiece Detail | P Steel, M Stainless Steel, K Cast Iron, N Non Ferrous Metals, S Super Alloys and Titanium, H Hardened Materials, Composites, Plastic, Wood | |

| By End-User | Automotive and Electric Vehicles, Aerospace and Defense, General Machining, Job Shops, Die and Mold, Industrial Machinery, Construction and Agriculture Equipment, Energy and Power Generation, Oil and Gas, Mining, Rail, Marine and Shipbuilding, Electronics and Consumer, Appliances, Semiconductor Equipment and Precision Parts, Medical Devices, Dental, Bearing Manufacturing, Others | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

Strategic Indicators For Drilling Tools

High Regulation Impact

Increasing regulations in USA, Saudi Arabia, Norway and Brazil are significantly changing the way drill tools are purchased. The EPA regulations on emissions in USA along with BSEE regulations on offshore drilling compliance are compelling companies to use low-emission rotary steerable systems and electronically controlled drill bits. The requirement for real-time reporting on well integrity by the Norwegian Petroleum Safety Authority is creating a greater need for sensors in drilling systems. In the Kingdom, the requirement by Saudi Aramco for localization for compliance is driving companies to procure tools made locally in approved facilities.

High Investment Activity

Rapid capital investment is currently underway in technologically sophisticated drilling equipment in United States, Saudi Arabia, UAE and China. The shale players in U.S. have ramped up their investment in durable PDC drill bits and automated drilling tools. In Saudi Arabia, there is consistent upstream investment through the Aramco drilling efficiency initiative, which focuses on unconventional reservoirs. In UAE, the oil companies, ADNOC, are moving into integrated drilling optimization deals and thereby requiring advanced bottom hole assemblies. In China, the state-run oil players are making investments in indigenous drilling tool technology.

Supply Chain Disruption

The supply chain uncertainty is escalating in light of titanium carbide, tungsten carbide and rare earth magnets supply issues located primarily within China, Russia and Vietnam. There is export limitations imposed on the supply of tungsten ore, which results in longer production cycles of drill bits. Sanctions were placed by US and EU countries in relation to industrial components from Russia that make the procurement process for high-quality steel problematic. The middle eastern countries that use drill bits will experience transportation problems through the Red Sea with the delivery of precision machinery.

Pricing Volatility

Fluctuations in drilling equipment pricing are caused by changes in the prices of tungsten carbide inputs, intensive forging procedures and shipping risks. American shale gas drillers witness irregular price changes in their drill bits by 8% to 14% during peak drilling seasons in the Permian Basin. Saudi Arabia retains a stable price structure owing to procurement deals for Aramco. China faces declining prices because of overproduction of drilling inputs in the country. Europe sees high prices due to energy prices impacting manufacturing of precise tools. Brazil and the offshore West African have premium prices because of import risks from deep-sea drilling.

Procurement Pressure

The pressure on procurement is growing with more E&P organizations applying performance-based contracting in North America, Middle East and Canada. The operators have started insisting that their drilling tools should be provided at an ROP improvement level. In addition, Saudi Aramco and ADNOC procurement policies have become focused on lifecycle cost management, rather than price. Shale players in USA have introduced vendor consolidation and limited the number of suppliers for drill bits and down-hole tools. E&P players in Europe have begun focusing on sustainable procurement and have restricted the use of uncertified suppliers. China insists on local content procurement as per energy security policy.

New Technology Adoption

Adoption of technologies is swiftly transitioning into AI-based drilling optimization systems in U.S., Norway and UAE. Telemetry sensors combined with machine learning are helping increase accuracy during directional drilling of shale formations. Digital twin technology is being applied in Saudi Arabia for pre-drilling of wells through reduced NPTs. Norway is ahead in autonomous offshore drilling equipment connected to subsea monitoring systems. The adoption rate of automated drilling rigs with predictive maintenance technologies is rising rapidly in China. The trend has led to less human involvement in hazardous drilling activities.

Regional Expansion Opportunity

North America - Digital Drilling Tool Scale-Up Hub

North America is still considered the most valuable area for expansion because of the high shale density in the Permian and Bakken basins. The OEMs are increasing their service centers in Texas and Oklahoma to facilitate quick replacement of tools and installation of AI-assisted drilling equipment.

Middle East - Integrated National Oil Company Contracts Hub

Expansion in the Middle East is being fueled by national oil companies of Saudi Arabia and UAE demanding that local manufacturing be done and complete drilling tool servicing agreements be in place.

Government Policy Support

The government policies have become an important factor affecting the demand for drilling tools in Saudi Arabia, United States, China and Brazil. Saudi Vision 2031 policy calls for localization in the upstream industry and thus increases the local production of drilling tools. The U.S. Inflation Reduction Act, on the other hand, indirectly boosts the demand for drilling tools through investment incentives in energy infrastructure. China's national energy security policy encourages domestic independence in the oilfield services industry. ANP's reforms in Brazil have been encouraging offshore exploration with high safety standards compliance.

Import Export And Pricing Intelligence

Global trade flows of drilling tools are dominated by oilfield service contractors sourcing rotary bits, downhole assemblies and precision cutting tools from manufacturing hubs in China, U.S. and Germany, while re-export hubs in the Middle East and Singapore facilitate redistribution, customs optimization and offshore procurement alignment across regions.

| HS Code | Reporter | Trade Flow | 2025 Trade Value (US$) | Interpretation |

| HS 820750 | Japan | Export | 204,693,400 | Global manufacturing hub; dominates low-cost & mass-market drilling tools supply chain |

| HS 820750 | USA | Export | 203,876,367 | High-precision engineering exports; strong industrial tooling leadership |

| HS 820750 | USA | Import | 611,458,302 | Aggregated intra-EU high-value machining tools exports |

| HS 820750 | UK | Import | 132,594,745 | Premium precision tooling exports, niche industrial applications |

| HS 820750 | China | Export | 18,281,300 | Advanced machining & oilfield tooling exports with strong domestic consumption linkage |

Pricing intelligence is characterized by heavy reliance on tungsten carbide inserts, premium alloy steel make-up, machining tolerances and certifications for oil field safety specifications, among others, with OEM contractual arrangements, replacement schedules and project-specific demand for drilling rigs shaping pricing agreements amid global dynamics.

Company Coverage Preview

Schlumberger holds a leadership role in drilling tools globally owing to its integrated portfolio for drilling wells and advanced digital drilling services. The includes the company’s usage of rotary steerable systems, AI-driven drilling optimization solutions and efficient drill bits. The competitive edge held by Schlumberger comes from offering drilling tools along with real-time data analysis services that facilitate improved rate of penetration and lower non-productive times. SLB enjoys a wide geographical presence including North America, Middle East and offshore Brazil, thus creating strong associations with national oil companies.

AI Impact Analysis

The application of AI is revolutionizing drilling tool performance and lifecycle optimization. Machine learning is facilitating accurate prediction of drill bit wear in order to avoid unexpected failures of the tools in shale oil reservoirs. Drill trajectory can be modeled beforehand through digital twin technologies in operations conducted by companies from Norway and Saudi Arabia. Advanced autonomous drilling is now possible through directional drilling systems in challenging terrains like deepwater Brazil and unconventional shale plays in United States. Autonomously operated drilling rigs have been employed in China where human interaction is minimized in hazardous environments.

Disruption Analysis

The most disruptive elements are the rapid adoption of AI, machine learning and drilling data analytics in the drilling industry. Large companies like SLB, Halliburton and Baker Hughes are using more and more smart drilling equipment, predictive maintenance technology and automated directional drilling systems in order to increase drilling performance and mitigate risks. Renewable energy and geothermal drilling have become an important trend that is impacting product innovations, going beyond traditional oil and gas drilling. The use of high-temperature drilling equipment, PDC bits and digitally-connected drilling systems is now required for geothermal and carbon capture projects.

Fluctuations in crude oil prices and a decrease in the number of North American drilling rigs have prompted manufacturers of drilling tools to expand into new areas. Mining and construction sector automated drilling rigs are causing a disruption to the industry through the use of autonomous drilling rigs and drilling optimization systems, which were developed by companies such as Atlas Copco and Epiroc. The growing demands for sustainable operations, decarbonization initiatives and decreased methane emissions are increasing the need for more efficient drilling systems.

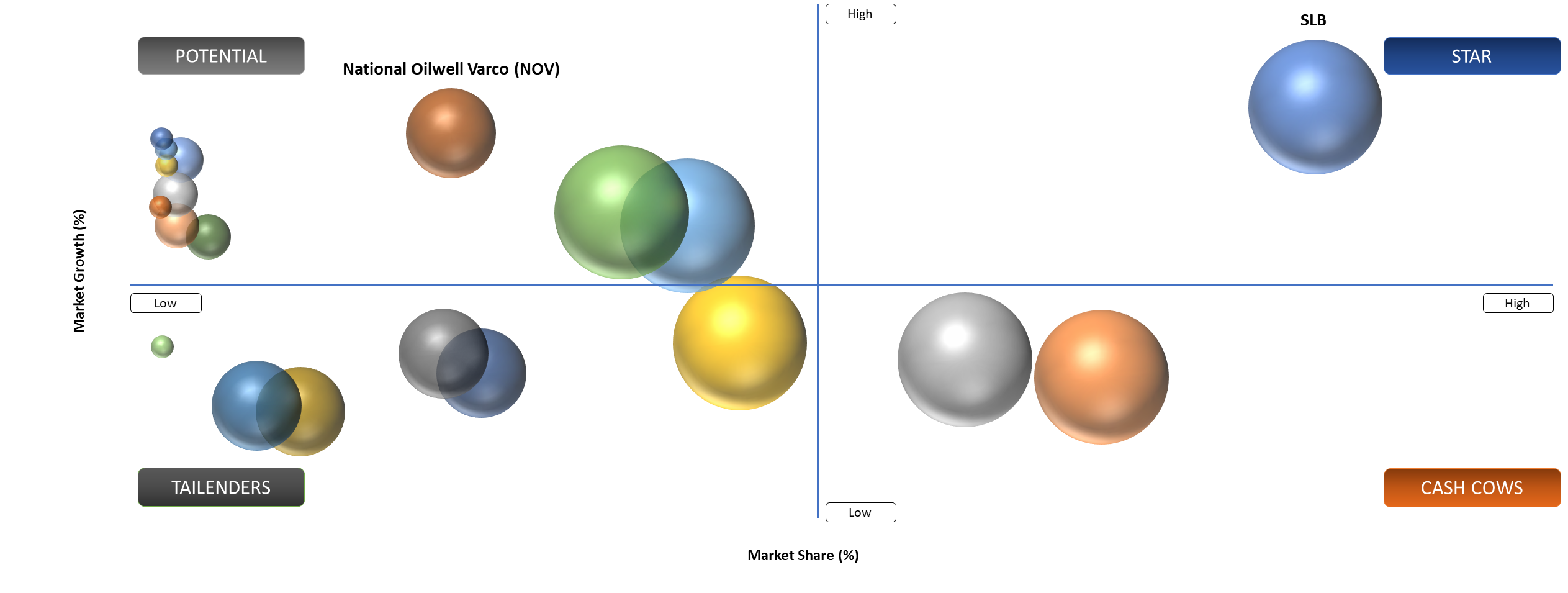

BCG Matrix: Company Evaluation

The market exhibits diversity among the competitive positions that the multinational oilfield service companies, mining equipment manufacturing firms and specialty downhole tool manufacturers occupy in the BCG Matrix. The stars of this market include SLB, Halliburton and Baker Hughes because of their significant market share, use of sophisticated digital drilling techniques and wide-ranging operations globally in the drill field. It is leading in the development and application of intelligent drilling systems, rotary steerable systems, AI drilling analytics and offshore drilling equipment.

The potentials are likely to be National Oilwell Varco and Weatherford International, who have the advantage of having a proven portfolio of drilling equipment, solid customer relationships that provide steady revenue even in conditions of modest market growth and after-sales support that earns them revenues. The Question Marks includes Drilling Tools International, Varel Energy Solutions and some rising regional firms who are building their businesses via acquisitions and new technologies but do not yet dominate globally.

Market Dynamics

Rising Investments in Industrial Manufacturing and Infrastructure Development

Economies with emergent status are allocating significant resources towards projects related to transport, intelligent city constructions, railway constructions, aerodrome developments and power plants. The projects involve vast use of metallic constructions and sophisticated drilling processes. The need for investments in infrastructure development in emerging economies is projected by the World Bank at US$ 4 trillion each year up to 2031. Metal fabrications, manufacture of heavy machinery and construction equipment manufacturing depend significantly on drilling equipment.

Demand is being created through the growth in the aerospace and defense industries. The aerospace industry demands very advanced drilling machines that can work with difficult machining materials such as titanium and carbon fibers. Aircraft manufacturing in US, Europe and Asia has increased capacity in manufacturing, thereby driving the demand higher.

Volatility in Raw Material Costs and Tool Wear Challenges

The critical problems facing the international drilling tools market is the fluctuation in prices of raw materials such as tungsten carbide, cobalt, high-speed steel and special coatings needed for the manufacture of cutting tools. Issues like interruptions in supply chains have continued to cause variations in prices of metals and increased production costs. Based on information from U.S. Geological Survey, China has been reported to account for more than 80% of tungsten capacity globally in 2024.

Drilling at high speeds in aerospace, mining and automotive industries causes drills to be exposed to severe temperatures, abrasions and wear. Manufacturers are under constant pressure to make the drills last longer without compromising the precision of machining processes and minimizing the number of replacements required. Regular drill wear causes machine downtime, inefficiencies during machining processes and high costs of operation for industry end-users. The problem is more acute in automated production systems, where minor tool wear could have a significant impact on the entire production process.

Segmentation Analysis

The global drilling tools market is segmented based on the tool grade, machine type, workpiece detail, end-user and region.

Automotive Manufacturing Segment Leads Market Demand

The automotive sector continues to be among the biggest users of drilling machines on a global scale, owing to significant demands from machining in engine blocks, transmissions, chassis parts, brakes and electric vehicle batteries. As per reports International Energy Agency (IEA), more than 17 million electric vehicles were sold globally in 2024, creating a huge demand for machining light materials such as aluminum and composites. Drilling is extensively applied in automation and high-speed machining in CNC centers.

Automotive companies are also making more investments in giga factories and manufacturing centers. In 2024, various automobile companies in Europe, China and North America have made investments of several billion dollars into their electric vehicle battery manufacturing facilities and automobile manufacturing plants. Such manufacturing plants need automated drilling and machining systems to be installed on a grand scale. In addition, stricter fuel consumption rules have encouraged automobile makers to use light materials in their products, leading to the adoption of drilling systems suitable for aluminum and composites.

Oil & Gas and Mining Applications Gain Momentum

An increasing demand is seen for heavy-duty drilling machinery in the oil and gas sector as well as mining. As per data from the International Energy Forum, investment in upstream oil and gas was in excess of US$ 600 billion globally in 2024. The rise is due to the fact that countries have undertaken measures for increasing energy security and exploration. The need for drill bits and hard rock drills is crucial for drilling in tough geological conditions.

The process of mining has also been expedited due to the growing requirement for strategic metals like lithium, copper, nickel and rare earth elements that can be utilized in electric cars and renewable energy sources. It has escalated exploration around the globe, including Australia, Chile, Canada and Africa, thereby promoting the usage of modern rotary drills and tungsten carbide drill bits in the mining sector.

Geographical Penetration

U.S. Drilling Tools Market Landscape

The U.S. drilling tool market is expected to remain highly driven by significant investment made by manufacturers in aerospace, defense, automotive, semiconductor and energy industries, all of which use drilling equipment extensively for producing complex components with greater precision. The rising utilization of CNC machining centers, automated drilling machines and multi-axis manufacturing machines is driving the growing need for carbide drills, indexable drilling tools and coated drilling tools that can withstand higher rotational speed and maintain dimensional accuracy while performing the drilling process. In particular, aerospace manufacturers and contract machining facilities witnessed a surge in purchases of advanced machining equipment in late 2024, thereby presenting new growth prospects for providers of drilling solutions.

Smart tooling systems equipped with tool condition monitoring and predictive maintenance technologies are gaining popularity among manufacturers seeking to increase efficiency by reducing machine downtime. Drilling processes that will allow lightweight composites and batteries to be manufactured without any damage as a result of thermal distortion are becoming ever more popular within aerospace and EV manufacturing industries. Moreover, American companies are focusing on automated drilling operations where drills with high tool life and efficient chip evacuation technology are becoming increasingly crucial. Investments in aircraft manufacturing and defense industries, as well as EV battery manufacturing facilities, are expected to stimulate the use of advanced solid carbide and diamond PCD drills in America.

Japan Drilling Tools Market Outlook

Japan continues to be one of the most technologically advanced centers for manufacture of drill bits, owing to its advanced automotive, electronic, robotic and industrial machinery industries. The precision manufacturing industry in Japan gives a lot of importance to the highest levels of accuracy, superior machining and finishing and durability of tools, which promotes technological advancements in coatings, geometry and substrates for drill bits. The well-established export-driven manufacturing industry in Japan also provides impetus to demand for advance drill bits for use in automotive powertrains, semiconductors and aerospace components manufacture.

The drilling tools market in Japan is being driven towards more automated and intelligent factory designs. Several prominent industrial firms are incorporating artificial intelligence-based machining analysis, robotic automation and IoT-connected CNC machines to enhance the effectiveness of the drilling process and minimize wastage. The ongoing transition into electric vehicle manufacturing within the country has spurred interest in drilling tools that can effectively machine materials such as aluminum, carbon fiber and battery casing with superior precision. Increased manufacturing of semiconductor components and devices in Japan has boosted the need for highly precise drills for wafer machinery and other electronic component production processes. Additionally, Japanese firms involved in drilling tool manufacturing remain dedicated to innovations in nano-coating technology, heat-resistant carbides and vibration damping solutions.

China Drilling Tools Market Trends

China is one of the most rapidly developing drilling tools markets globally as a result of a highly developed manufacturing sector that operates within the fields of automobiles, electronics, aviation, heavy machinery and renewable energy. An accelerated growth of the capabilities related to industrial automation and precision manufacturing has resulted in a heightened demand for drilling tools including CNC drilling equipment, carbide drills and high-speed machining technology. China’s leading position in EVs manufacturing industry drives additional demand for state-of-the-art drilling machines which are utilized in such areas as production of batteries, electric motors and light vehicle parts. China is actively investing into semiconductor manufacturing and robotics thus creating many opportunities for micro-drilling and ultra-precision machining processes. Recovery of Chinese machine tool demand has positively impacted Japan's foreign machine tool orders during 2024 period.

The drilling tool market in China is also experiencing strong growth due to the aggressive drive towards smart manufacturing and automation in large factories, which will result in increased productivity locally. The implementation of digital machining centers that are aided by process optimization and predictive maintenance with artificial intelligence technology is becoming more common among manufacturers. The aviation industry, driven by indigenous aircraft programs, creates increasing demand for drilling tools that can machine titanium and carbon fiber composite materials with utmost accuracy. Meanwhile, production of renewable energy equipment, such as wind turbines and solar manufacturing machinery, will see growing consumption of robust drilling tools for industrial applications. Moreover, manufacturers in China are investing in innovations within the field to minimize reliance on foreign high-tech cutting equipment, resulting in increased research and development in terms of advanced coatings, nano-carbide drilling materials and abrasion-resistant drilling tools.

Competitive Landscape

- The global drilling tools market is highly competitive, with major players focusing on advanced material technologies, tool durability, precision engineering and digital machining solutions to strengthen their market positions.

- Key players include Sandvik AB, Kennametal Inc., ISCAR Ltd., Mitsubishi Materials Corporation, Sumitomo Electric Industries Ltd., Seco Tools AB, Kyocera Corporation, Guhring KG, OSG Corporation and Walter AG.

- Companies are increasingly investing in nano-coated carbide drills, indexable drilling systems, additive manufacturing technologies and AI-driven tool monitoring platforms to improve machining efficiency and extend tool lifespan.

Strategic collaborations with automotive, aerospace, semiconductor and energy companies are accelerating product innovation, while sustainability initiatives are encouraging manufacturers to develop recyclable tooling materials and energy-efficient machining solutions.

MAJOR PAIN POINTS

- High Raw Material Price Volatility: Fluctuating prices of tungsten carbide, high-speed steel, cobalt and specialty alloys are increasing manufacturing costs and pressuring profit margins for drilling tool producers.

- Rapid Tool Wear in High-Performance Machining: Increasing machining speeds and harder workpiece materials are accelerating tool wear, reducing operational efficiency and increasing replacement frequency.

- Supply Chain Disruptions for Precision Components: Delays in sourcing carbide inserts, coatings and precision-engineered tool components are impacting production timelines and delivery commitments.

- Growing Demand for Customized Tooling Solutions: End-users increasingly require application-specific drilling tools, creating challenges in design flexibility, inventory management and production scalability.

- Intense Competition from Low-Cost Manufacturers: Regional manufacturers offering lower-priced alternatives are intensifying pricing pressure and reducing market differentiation opportunities.

- Limited Tool Life in Composite and Advanced Materials: Drilling carbon fiber composites, titanium alloys and hardened steels causes excessive heat generation and rapid edge degradation.

- Shortage of Skilled Machining and Tooling Professionals: Lack of experienced CNC operators and tooling specialists is affecting optimal tool selection, performance and maintenance practices.

- Increasing Pressure for Sustainable Manufacturing: Manufacturers face rising demand for recyclable materials, energy-efficient production processes and reduced metalworking waste generation.

- Technological Complexity in Smart Tool Integration: Adoption of sensor-enabled and digitally connected drilling tools requires substantial investment in automation, IoT infrastructure and software compatibility.

Downtime and Productivity Loss in Industrial Operations: Frequent tool changes, unexpected breakage and maintenance interruptions are negatively impacting machining productivity and operational efficiency.

KEY DEVELOPMENTS

- May 2026 - SLB launched AlphaSight reservoir mapping solution, improving real-time drilling visibility, geosteering precision and autonomous drilling performance globally.

- February 2026 - SLB secured Mubadala Energy offshore drilling contracts in Indonesia, covering directional drilling, completions, wireline and well-testing services.

- October 2025 - Halliburton introduced StreamStar wired drill pipe interface system, enabling continuous downhole power and real-time drilling automation data transmission.

- July 2025 - Halliburton launched LOGIX automated geosteering technology, enhancing well placement accuracy through machine learning and advanced geological interpretation capabilities.

- May 2025 - Halliburton released EarthStar 3DX resistivity service, providing horizontal look-ahead geological insights up to fifty feet before drilling penetration.

- September 2025 - Baker Hughes joined California’s Hell’s Kitchen geothermal project, supplying advanced high-temperature drilling technologies for large-scale geothermal energy development.

November 2025 - Baker Hughes committed key drilling and compression equipment support for Alaska LNG infrastructure and gas treatment development project.

ANALYST VIEW / OPINION

- Rising offshore and unconventional hydrocarbon exploration activities continue accelerating advanced drilling tools demand globally.

- Automation-integrated drilling systems significantly improve operational efficiency, drilling accuracy and non-productive time reduction.

- Increasing geothermal energy investments are creating new long-term growth opportunities for drilling tool manufacturers.

- Demand for high-performance carbide and diamond-based drilling tools is rapidly increasing across harsh environments.

- Digital drilling analytics and real-time monitoring technologies are reshaping competitive differentiation among market participants.

- North America maintains market leadership due to shale drilling expansion and strong upstream investments.

- Asia-Pacific emerges as fastest-growing regional market supported by mining, infrastructure and energy development projects.

- Environmental regulations and sustainability targets are encouraging development of energy-efficient and low-emission drilling technologies.

- Tool wear, operational downtime and fluctuating raw material prices remain major profitability challenges across manufacturers.

- Strategic collaborations between oilfield service providers and drilling technology companies are intensifying global market consolidation.

TARGET AUDIENCE

| INDUSTRY | WHO SHOULD BUY THIS REPORT? | REASON TO BUY THIS REPORT |

| Oil & Gas Exploration Companies | Drilling Operations Managers, Well Engineering Teams, Procurement Heads | Analyze drilling tool demand, offshore and onshore drilling trends and advanced well construction technologies |

| Oilfield Service Providers | Directional Drilling Teams, Field Operations Managers, Technical Service Departments | Evaluate high-performance drilling tools for improved penetration rates and operational efficiency |

| Offshore Drilling Contractors | Offshore Project Managers, Rig Operations Teams, Supply Chain Departments | Assess deepwater and ultra-deepwater drilling tool requirements and technology advancements |

| Onshore Drilling Contractors | Drilling Supervisors, Asset Management Teams, Procurement Managers | Identify cost-efficient drilling solutions for shale, tight oil and conventional drilling operations |

Mining & Mineral Exploration Companies | Exploration Managers, Rock Drilling Engineers, Operations Teams | Evaluate drilling technologies for mineral exploration, core drilling and extraction efficiency |

| Geothermal Energy Companies | Geothermal Project Engineers, Drilling Program Managers, Technical Procurement Teams | Analyze specialized drilling tools for geothermal well development and sustainable energy projects |

Construction & Infrastructure Companies | Foundation Engineering Teams, Tunneling Managers, Project Procurement Departments | Understand drilling tool requirements for infrastructure, piling and tunneling applications |

Water Well & Environmental Drilling Companies | Hydrogeology Teams, Environmental Engineering Departments, Drilling Operations Managers | Assess drilling solutions for groundwater exploration and environmental remediation projects |

Heavy Equipment & Industrial Machinery Manufacturers | Industrial Engineering Teams, Manufacturing Operations Managers, Product Development Departments | Track demand for drilling components and precision-machined drilling equipment |

Drill Bit & Downhole Tool Manufacturers | Product Innovation Teams, R&D Departments, Competitive Intelligence Teams | Benchmark drilling technologies, cutter materials and product development strategies |

Carbide, Diamond & Advanced Material Suppliers | Material Science Teams, Technical Sales Departments, Strategic Business Units | Analyze future demand for PDC cutters, carbide inserts and wear-resistant materials |

Directional Drilling & Measurement Technology Companies | MWD/LWD Engineers, Automation Specialists, Technology Integration Teams | Evaluate demand for intelligent drilling systems and real-time drilling optimization tools |

Industrial Automation & Digital Oilfield Companies | Smart Drilling Teams, Industry 4.0 Engineers, Data Analytics Departments | Assess integration opportunities for automation, AI and predictive drilling technologies |

Industrial Distributors & Oilfield Equipment Suppliers | Category Managers, Regional Sales Teams, Inventory Planning Departments | Understand regional demand trends and optimize drilling tool product portfolios |

Aerospace & Defense Component Manufacturers | Precision Machining Teams, CNC Manufacturing Departments, Supply Chain Managers | Analyze drilling tool applications for high-strength alloy and aerospace material processing |

Energy & Power Generation Companies | Plant Engineering Teams, Turbine Manufacturing Departments, Procurement Teams | Evaluate drilling technologies used in energy infrastructure and equipment manufacturing |

Railway & Heavy Engineering Companies | Fabrication Managers, Manufacturing Engineers, Operations Departments | Assess drilling equipment demand for heavy engineering and industrial fabrication activities |

Research Institutions & Universities | Petroleum Engineering Departments, Mining Research Teams, Industrial Technology Centers | Study advancements in drilling efficiency, automation and next-generation drilling systems |

Government & Public Sector Energy Organizations | Energy Development Authorities, National Oil Agencies, Infrastructure Planning Teams | Support strategic planning for domestic energy exploration and drilling modernization initiatives |

Investors, Private Equity & Consulting Firms | Investment Analysts, Industrial Strategy Consultants, Market Intelligence Teams | Evaluate growth opportunities, competitive landscape and investment potential in drilling technologies |

WHY CHOOSE DATAM?

- Data-Driven insights: Dive into detailed analyses with granular insights such as pricing, market shares and value chain evaluations, enriched by interviews with industry leaders and disruptors.

- Post-Purchase Support and Expert Analyst Consultations: As a valued client, gain direct access to our expert analysts for personalized advice and strategic guidance, tailored to your specific needs and challenges.

- White Papers and Case Studies: Benefit quarterly from our in-depth studies related to your purchased titles, tailored to refine your operational and marketing strategies for maximum impact.

- Annual Updates on Purchased Reports: As an existing customer, enjoy the privilege of annual updates to your reports, ensuring you stay abreast of the latest market insights and technological advancements. Terms and conditions apply.

- Specialized Focus on Emerging Markets: DataM differentiates itself by delivering in-depth, specialized insights specifically for emerging markets, rather than offering generalized geographic overviews. The approach equips our clients with a nuanced understanding and actionable intelligence that are essential for navigating and succeeding in high-growth regions.

- Value of DataM Reports: Our reports offer specialized insights tailored to the latest trends and specific business inquiries. The personalized approach provides a deeper, strategic perspective, ensuring you receive the precise information necessary to make informed decisions. The insights complement and go beyond what is typically available in generic databases.

WHAT DATAM UNIQUELY PROVIDES

- Proprietary upstream drilling tool demand forecasting using rig-level activity mapping and basin-specific utilization intelligence models

- OEM-level margin benchmarking across drill bits, BHA systems and directional drilling tool categories globally

- Real-time CAPEX allocation tracking across national oil companies and independent exploration firms globally

- Granular HS-code trade flow reconstruction for drilling tools across 120+ importing and exporting countries

- Competitive intelligence on drilling tool innovation pipelines and field trial deployment cycles across major oilfield service firms

- AI-driven pricing elasticity modeling based on rig count fluctuations and crude price sensitivity correlations

- Contract-level procurement intelligence covering long-term drilling service agreements and vendor consolidation patterns

QUESTIONS THIS REPORT ANSWERS

- What is the current and forecast market size of the global drilling tools market through 2035?

- Which end-users are driving demand growth and why?

- Which regions and drilling tool types present the highest growth and investment opportunities?

- How are investments in automation, digital drilling technologies and AI-enabled monitoring reshaping ownership models and competitive dynamics?

- How do regulatory frameworks, environmental standards and geopolitical risks affect drilling operations and drilling tools deployment?

- Which technologies are shaping next-generation drilling tools manufacturing?