Diesel Bus Market Overview

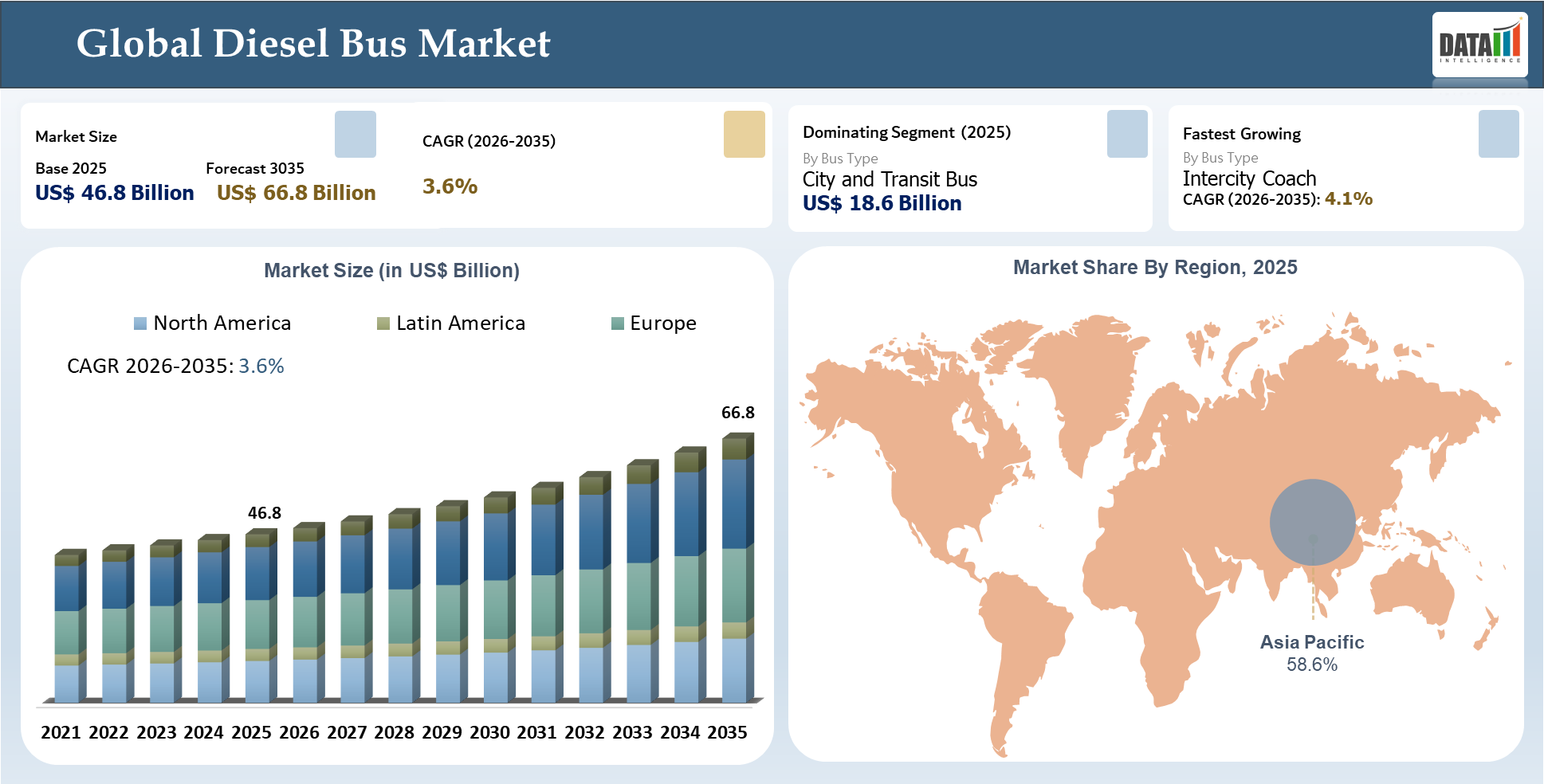

The Global Diesel Bus Market was valued at US$ 46.8 billion in 2025 and forecast to attain US$ 66.8 billion by 2035, growing at a compound annual growth rate (CAGR) of 3.6% during 2026-2035. The market encompasses diesel-fueled bus types, relevant components, and after-market services, covering categories of bus type, length, emission category, passenger carrying capability, usage type, ownership model, and engine power. Revenues depend on specifications of the product, alignment with regulations, supply chain preparedness, and supplier delivery against product requirements.

Demand for the product continues to be driven mostly by replacement needs in applications like urban transit services, intercity transportation, school transportation, and employee transport services. Despite growing electrification trends, diesel buses still have commercial importance in areas where the necessary charging infrastructure and grids, financial constraints, and the extent of route operation are barriers to immediate transition to electric vehicles.

As a result, competition is shifting from broad product availability toward execution-led differentiation, where success depends on route-specific platforms, stronger aftermarket support, localized manufacturing, and tender responsiveness.

AI Impact Analysis

AI is now an integral value-adding component for the market for diesel buses compared to an independent growth story for the market. Businesses have been implementing AI tools to boost their ability to forecast demand, prioritize tenders, plan replacements, and develop product mixes such that they can match their buses' configurations to specific fleets' requirements. With unpredictable public procurement and regionalized operating conditions, such insights will help with better commercial planning.

In relation to products and operations, there has been the increasing implementation of AI technologies for purposes such as predictive maintenance, fuel efficiency improvements, performance tracking of vehicles on various routes, and even spare parts replacement. This analysis of the diagnostic and performance data of buses helps with lowering the time spent on maintenance and optimizing their life cycle.

Lastly, the use of AI also affects competitive advantages in the market. Those businesses whose products enjoy visibility in the installed base and who benefit from their connectedness with service providers and other parties that generate operating data gain a competitive edge over others. Over time, it will be the vendors who combine domain knowledge and fleet operating data who win.

Diesel Bus Market Key Takeaways

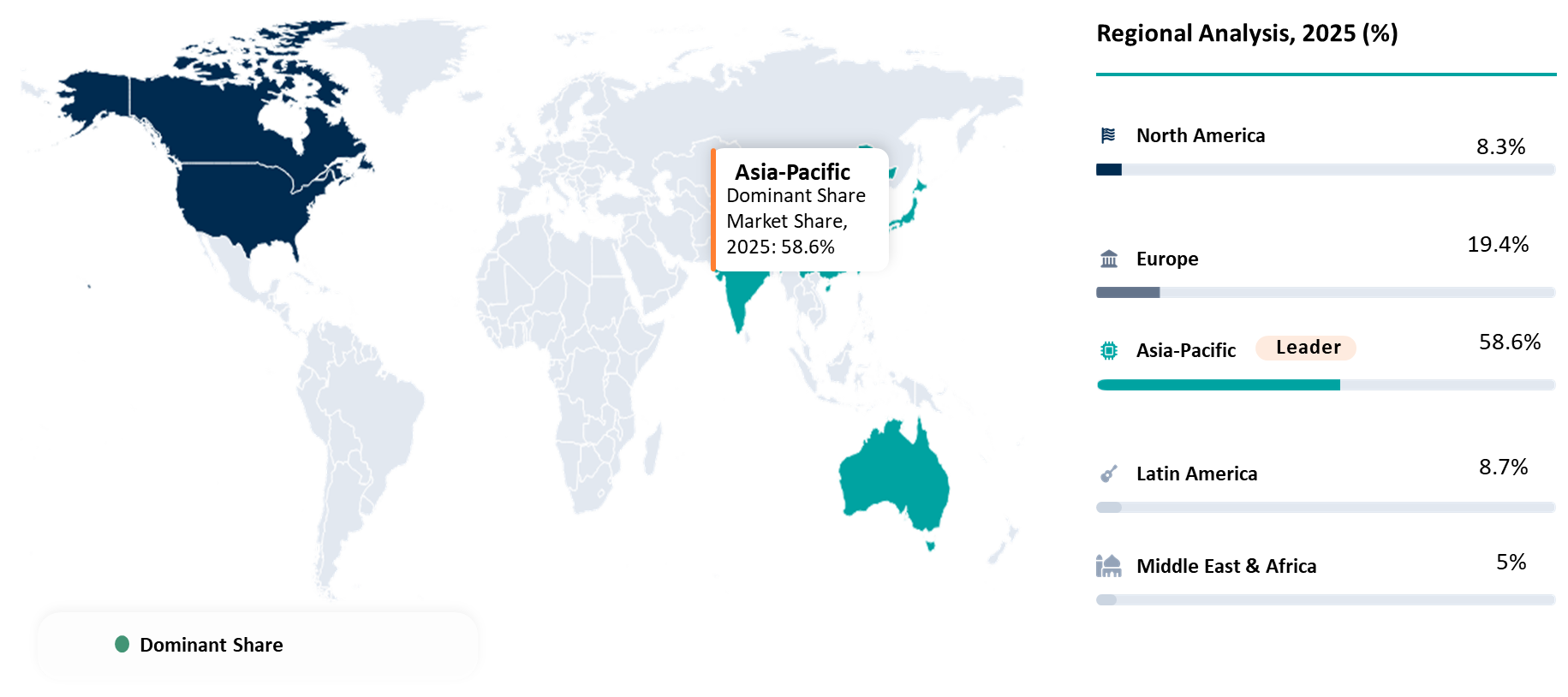

- The Asia-Pacific region will continue to dominate the global diesel bus market owing to its massive potential for fleet demand, replacements, and benchmarking in the context of competition between the OEMs.

- City & Transit Bus will continue to be the largest commercial segment owing to its closer link with the prevalent procurement trends and immediate deployability.

- Replacement of diesel buses in existing fleets operating in the public transport sector will remain the primary growth catalyst, while the execution risk will continue to lie in rapid adoption of electric and fuel-cell-powered buses in major urban fleets.

- Suppliers with product breadth and fast execution will be better suited to fend off competition and preserve their market position, especially in markets where execution is as important as product offerings.

Market Scope

| Metrics | Details | |

| 2025 Market Size | US$ 46.8 Billion | |

| 2035 Projected Market Size | US$ 66.8 Billion | |

| CAGR (2026-2035) | 3.6% | |

| Largest Market | Asia-Pacific | |

By Bus Type

| City and Transit Bus, Intercity Coach, School Bus, Tour and Charter Bus, and Special Purpose Bus | |

| By Length | Below 9 m, 9 m to 12 m, Above 12 m, and Articulated and Double Articulated | |

| By Emission Standard | Bharat Stage and Euro IV Equivalent, Euro V Equivalent, and Euro VI and Ultra Low Emission Diesel | |

| By Seating Capacity | Below 30 Seats, 30 to 50 Seats, and Above 50 Seats | |

| By Application | Public Transport, School Transport, Tourism and Charter, and Industrial and Employee Transport | |

| By Ownership | Public Fleet, Private Fleet, and Leased and Contract Fleet | |

| By Engine Power | Below 200 hp, 200 hp to 300 hp, and Above 300 hp | |

| By Region | North America | U.S., Canada, Mexico |

| Europe | Germany, UK, France, Spain, Italy, Poland | |

| Asia-Pacific | China, India, Japan, Australia, South Korea, Indonesia, Malaysia | |

| Latin America | Brazil, Argentina | |

| Middle East and Africa | UAE, Saudi Arabia, South Africa, Israel, Turkiye | |

| Report Insights Covered | Competitive Landscape Analysis, Company Profile Analysis, Market Size, Share, Growth | |

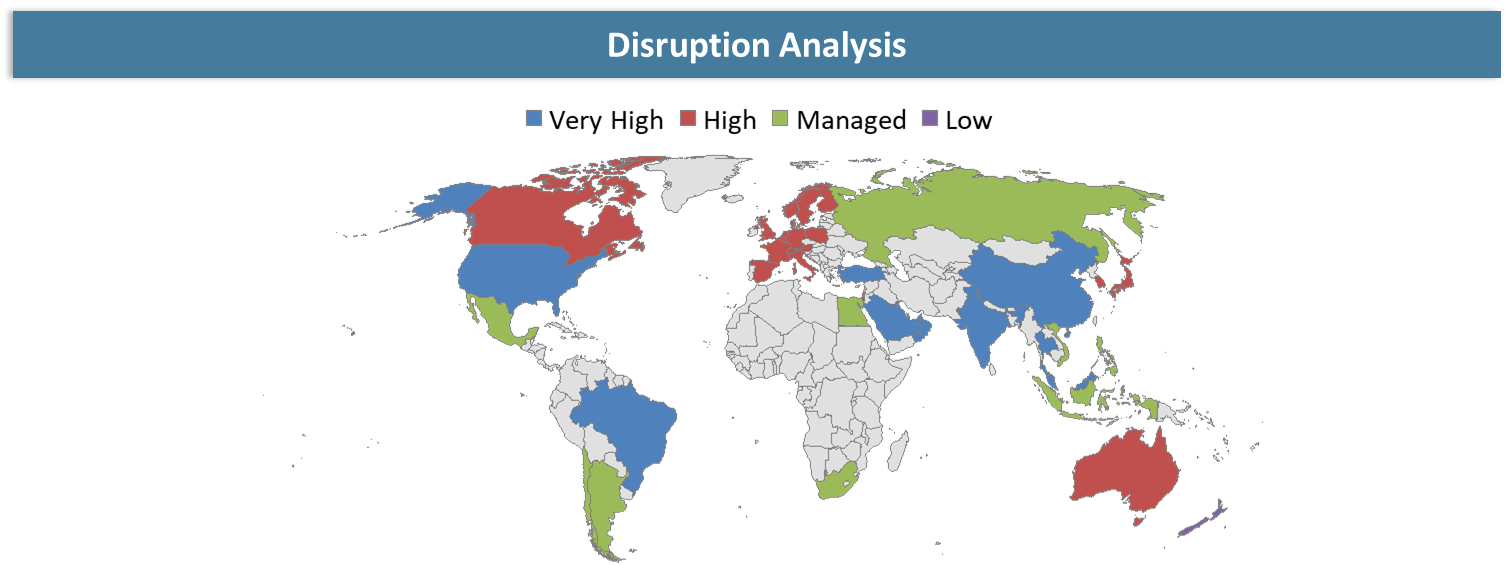

Disruption Analysis

Procurement-Led Disruption and Electrification Pressure Reshaping the Diesel Bus Market

The main disruption within the market of the diesel buses comes from being procurement driven rather than product driven, as customers change their focus from the initial cost of acquiring the vehicles to the total cost of ownership, emissions, and reliability. This is important because there is more and more pressure on the transport operators to prove that their investments are made based on sound business decisions, and not just based on the specifications of the bus itself.

The second structural disruption comes in the form of electrification, accelerated in the context of bus procurement, particularly city buses tendering in EU cities. According to the EU, in 2025, electrically chargeable buses made up 23.8% of total bus registrations against 62.1 percent for diesel buses, thus, the dominant fuel is still diesel, but not protected by policies going forward in critical city markets. The International Energy Agency reported that electric buses made up around 4.5% of total global bus sales in 2022, and the proportion exceeded 13% in Europe by 2024 and exceeded 40 percent in certain countries. Thus, we see that the disruption is happening, but is geographically and application-specific.

In terms of the competitive implication, being big is now becoming irrelevant to protecting your market share. Companies that manage to combine their compliant diesel platforms with aftersales support and tender performance have better chances to maintain their relevance through this period of change. On the other hand, it should be kept in mind that electric buses are still significantly more expensive than diesel buses in certain applications and geographical contexts.

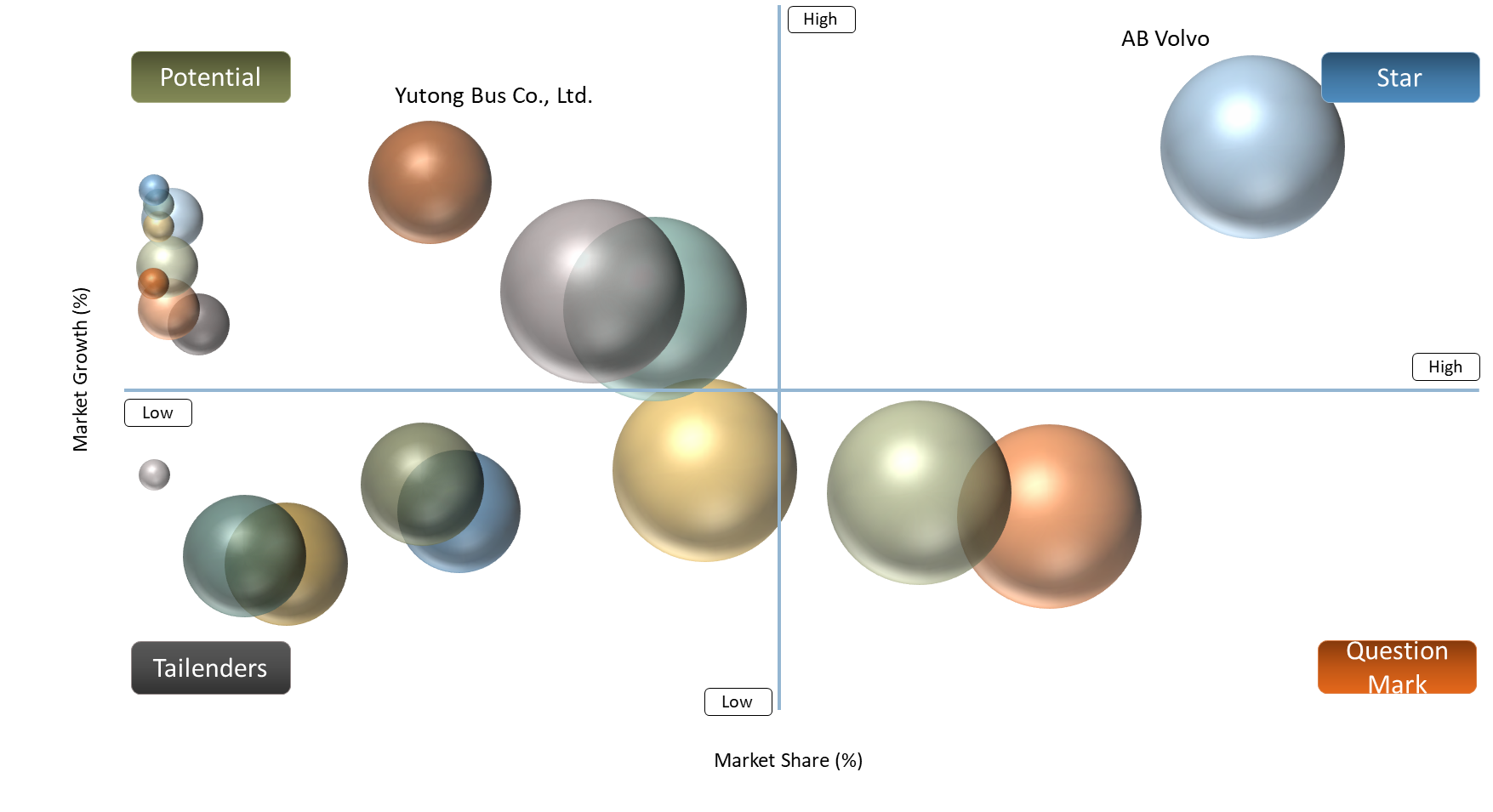

BCG Matrix: Company Evaluation

In the context of BCG analysis, the Stars within the diesel buses sector are located in areas and segments where there is still robust demand, especially in Asia-Pacific and infrastructure-deprived countries. Firms like Daimler Truck Holding AG, AB Volvo, and TRATON SE have maintained excellent positioning through their dominance in setting product specifications, worldwide logistics capabilities, and involvement in major tender bids. Nonetheless, their Star position is becoming more defined in specific segments rather than across the entire market due to the slow transition to electric mobility.

Cash Cows make up the heart of the diesel buses market because its dynamics revolve around replacement demand. Well-established vendors with extensive fleets, robust after-sales support, and sustained procurement relationships have continued to reap consistent incomes. Their competitive edge stems from the guaranteed nature of repeat sales, maintenance contracts, and fleet longevity, which renders them hard to unseat despite the lack of significant growth prospects.

Question Marks consist of local producers as well as new entrants which aim at addressing more profitable niches or regions, such as markets that have cost constraints, education transport services, or specific uses. This category of companies will grow rapidly, provided that it gets regulatory approval or tender wins but faces limitations in its ability to compete on an international level, reputation, and logistics.

Dogs are legacy diesel products that suffer from commoditization and substitution threats. In urban public transport segments where electric solutions are advancing, the inability of companies to adapt their emissions or increase cost efficiency leads to their irrelevance.

Market Dynamics

Diesel bus procurement remains relevant where charging infrastructure, route duty cycles, or grid readiness limit full electrification

The strategic relevance of diesel bus procurement is dictated by the uneven progress in the development of zero emission bus fleets in various geographies, duty cycles, and procurement financing climates. In Europe, in 2025, diesel buses accounted for 62.1% of all bus purchases, whereas electrically chargeable ones comprised just 23.8%, suggesting that the switch to electric power is ongoing; however, it has not yet managed to displace the traditional diesel engine from its leading position as a bus procurement option.

From the perspective of a consultant working in the field, one can deduce that the demand for diesel buses persists due to operational feasibility and not technological superiority. The International Energy Agency notes that electric buses comprised only 3% of the global bus sales market share as of 2023, and their use was confined to specific countries driven by governmental policies and not an integral part of the general transition process towards zero-emission vehicle fleets around the globe.

Rapid policy shift toward battery electric and fuel cell buses in large urban fleets

The primary constraint in the diesel bus industry is the increasing pressure on governments to move toward battery electric and hydrogen buses, especially in large urban public transport systems where acquisition practices are becoming increasingly focused on meeting zero-emission aspirations. The International Energy Agency states that 11 nations had signed up to the Global Memorandum of Understanding on Zero-Emission Medium-and Heavy-Duty Vehicles by 2022, pledging to achieve 100% of zero-emissions for new trucks and buses by 2040. This becomes a fundamental constraint against the uptake of diesel buses in fleet replacements driven by urban municipalities.

In terms of sizing the market, this restraint acts to constrain the addressable market by diverting commercially viable demand away from policy-driven urban markets and towards those that have not yet found economic viability or charging infrastructure. It constrains visibility and future-proofing of the fleet and raises the possibility that technical demand will not result in actual demand. Companies addressing this constraint through improved diesel technologies, cost-effective life cycle economics, localization of services, and policy alignment will be most successful in navigating the transition period.

Segmentation Analysis

The global diesel bus market is segmented based on bus type, length, emission standard, seating capacity, application, ownership, engine power, and region.

City and Transit and Intercity Coach Segments Continue to Anchor Market Demand

Bus type is still the most significant commercial framework for understanding the dynamics of the global diesel bus industry, with the two sub-segments in focus being City and Transit Buses as well as Intercity Coaches, which can best reflect the areas where demand is currently being observed and monetization opportunities are available. Such segmentation is important given that there are significant differences when it comes to purchasing rationale, duty cycle, need for replacement, and compliance issues depending on the vehicle's mission and less on its engine specifications. Specifically, City and Transit Buses are predominantly procured via tenders aimed at ensuring continued service delivery and fleet renewal, whereas Intercity Coaches are usually procured on an economic basis with regards to route, uptime, fuel consumption, and consistency of operation. Even though electrification has become a key factor influencing the market, there is still a demand for diesel engines due to factors such as insufficient charging infrastructure, poor grid availability, budget limitations, and difficult operational conditions for charging.

This replacement need is further reinforced by fleet age, with the average age of buses operating in the EU standing at 12.2 years, highlighting the continued commercial importance of conventional fleet renewal. Hence, traditional buses and fleet renewal will always be a vital part of the commercial transport market. Buses and city vehicles remain key drivers of diesel demand in locations that require quick fleet replacement before the electrification of depots. Intercity coaches also favor diesel in cases that require route profitability and certainty.

Geographical Penetration

Asia-Pacific Remains the Core Demand and Supply Hub for the Diesel Bus Market

Asia-Pacific still stands out as the topmost strategic location in the diesel bus business segment due to a combination of high public transportation needs and an elaborate support network comprising manufacturing and services. The reason for Asia-Pacific's prominence in the sector does not lie in the use of diesel fuel itself, but rather in the combination of non-homogenous levels of electrification, large-scale vehicle turnover programs, and varied demands of different types of routes within urban and inter-city transportation systems.

Furthermore, there is an additional boost for Asia-Pacific in the shape of significant OEM presence and capacity for exporting products. As noted by Yutong Bus Co., Ltd., the company accounts for over 10% of global sales, making it one of the major bus manufacturers in the world. In addition to that, according to figures provided by Higer Bus Company Limited, the company had managed to sell more than 329891 units of its buses to over 150 countries around the globe. Together, these factors reinforce Asia-Pacific’s position as the central hub for both diesel bus demand and supply.

India Diesel Bus Market Trends

India is still among the most economically significant markets for diesel buses, owing to the need for ongoing fleet renewal driven by the need for service recovery, financial prudence, and scalability of purchases in state transport undertakings. As a result, conventional buses remain economically feasible in scenarios that cannot afford to wait for depot electrification, chargers, and finance aligning for such projects. The scale of such replacements is not insignificant either. In March 2026, for example, Tata Motors reported cumulative orders of more than 5,000 buses and bus chassis placed with them by various state transport undertakings, which will be deployed in phases. Similarly, Ashok Leyland reported in October 2025 winning an order for 1,937 buses from Tamil Nadu State Transport Undertakings, including town buses, mofussil, and SETC types. Such results reiterate the significance of the Indian bus replacement market despite evolving powertrains becoming more route and regional in nature. There are developments toward bus electrification on selective routes in the region, yet there is no doubt about the continued practicality of diesel-powered buses in certain use cases.

China Diesel Bus Market Outlook

The influence of China in the global market for diesel buses has remained strong not due to the dominance of diesel buses in the bus fleets of major Chinese cities, but due to the fact that China plays an important role in shaping the supplies, export capabilities, and cost-efficiency of the production of conventional vehicles on both the domestic and foreign markets. Even though major cities in China have become aggressive supporters of new-energy buses, there is still a relevance of diesel in terms of intercity, heavy-duty use, and exports. Thus, the influence of China as a producer of diesel buses on the global market is related not to the domestic demands of the cities in China but to its production capacity. The relevance of Chinese producers of diesel buses is illustrated by the fact that in 2025, China exported 78,313 buses and coaches, among which 29,576 buses would be for city transportation. It shows that China is still a crucial element in the process of fleet modernization for countries that transition more slowly than the Chinese ones.

Competitive Landscape

The competitive environment for diesel buses involves a blend of international leaders and regional players, with Daimler Truck Holding AG, AB Volvo, TRATON SE, and Iveco Group N.V. taking a crucial part in defining the product standards, compliance requirements, and fleet procurement processes. Competitiveness in this particular industry involves not only the variety of the product portfolio offered, but also the match with the specific needs of the client, the distribution network capacity, the aftersales services provided, and the level of support during the whole lifecycle of the vehicle.

The most competitive players have been relying on platform improvements, local manufacturing capabilities, partner cooperation, and efficient tenders for their growth and development. The current market trend is shifting towards replacement-focused solutions and policies-based procurement. As a result, those players which have an advantage in their installed bases, service networks, and uptime record will be more competitive in the future. Eventually, the market leadership will consolidate around those companies with a higher level of technological expertise, faster commercialization, and lifecycle efficiency.

Key Developments

- March 2026: Tata Motors announced cumulative orders of more than 5,000 buses and bus chassis from multiple Indian state transport undertakings, reinforcing the continued scale of replacement-led bus procurement in a market where diesel remains operationally relevant.

- March 2026: TRATON reported that MAN Truck & Bus increased unit sales in 2025, driven in part by higher bus volumes, indicating continued commercial traction for conventional bus platforms within its portfolio.

- January 2026: Daimler Buses highlighted a major coach production milestone as the 40,000th Mercedes-Benz Tourismo rolled off the line, underscoring sustained demand for high-deck touring coach platforms in the conventional bus segment.

- October 2025: Ashok Leyland won an order for 1,937 buses from Tamil Nadu State Transport Undertakings, one of the clearest indicators of ongoing large-scale bus replacement demand in India.

- June 2025: Daimler Buses began delivering 111 Mercedes-Benz and Setra buses to Busitalia, including Mercedes-Benz Tourismo and Setra double-deck coaches, highlighting continued demand for premium conventional coach platforms in Europe.

- June 2025: Tata Motors launched the all-new LPO 1622 bus in Qatar, powered by a 220 hp Euro VI-compliant diesel engine, showing continued investment in export-ready diesel bus platforms for infrastructure-constrained markets.

- March 2025: Volvo Buses and UNVI announced the Volvo B13R UNVI XL for the UK and Ireland, a new full-size coach platform aimed at the touring and intercity segment, with deliveries planned from Summer 2026.

- March 2025: Ashok Leyland inaugurated a new bus manufacturing plant near Vijayawada with annual capacity of 4,800 buses, designed to produce the complete range of Ashok Leyland diesel buses alongside electric models.

- October 2025: Daimler’s Setra TopClass won Coach of the Year 2026, reinforcing the competitive importance of premium long-distance coach platforms in the conventional bus market.

- November 2024: Wrightbus launched the next-generation StreetDeck Ultroliner diesel, powered by a Cummins B6.7 diesel engine and Voith DIWA.8 NXT transmission, showing that OEMs were still upgrading diesel bus efficiency and emissions performance.

White Space Opportunities

According to DataM, one of the more obvious examples of white space within the market for diesel-powered buses is actually beyond the scope of the most prominent large public tenders. As major vendors focus on supplying highly volume-driven urban tenders, underpenetrated demand may actually be found in peri-urban transportation, employee shuttles, school buses, and regional corridor services where the emphasis is not on technology transition but uptime and fleet deployment speed. Packaging offers from suppliers that are based on route-specific needs and support can yield much more sustainable business model.

The second whitespace opportunity relates to lifecycle-oriented business packaging beyond merely providing vehicles. Purchasers today favor providers who not only provide buses but also maintenance services, uptime guarantees, telematics solutions, and fuel consumption optimization services. In total-cost-of-ownership-driven procurement landscapes, vendors who mitigate implementation risks can scale at a much higher pace than those providing just a technologically viable product.

Moreover, there is scope in addressing the needs of medium-sized and regional bus fleets that have often been ignored but represent a regular demand base. This allows opportunities for strategic channel partnerships, localized service delivery, financial assistance, and aftermarket initiatives. According to DataM, the next phase of outperformance would be driven by companies that are able to find and leverage such white spaces early on.

DMI Opinion

According to the DataM report, while demand for diesel buses should not be in doubt, the key challenge in the segment is to identify how to capitalize on replacement demand without becoming overly exposed to sensitive areas of policy. Increasingly, success favors those businesses who manage to create commercially feasible models of diesel procurement by virtue of reliability, regulation compliance, aftersales, and lifecycle costs management. We believe diesel buses have continued to offer themselves as feasible options in contexts where route utilization, restrictions on charging capacity, budgetary constraints, and urgent deployments favor their usage over alternatives.

From our analysis of the DataM report, we find that many players continue to overestimate the role of broad portfolio narratives and downplay the relevance of commercial execution details. For this reason, tendering capabilities, aftersales, availability of spare parts, and route-specific product designs are critical to successful commercialization. This implies that suppliers who invest in localized solutions will fare better than those focused solely on leveraging their size and visibility in the market.

According to our analysis, the focus will move to more concentrated yet high-value pockets of opportunity. This means that the market is an execution opportunity and not an expansion one, where the outperformance will be driven by those suppliers who are able to mitigate risks and improve the economics for fleets.

Why Choose DataM?

- Diesel Bus Technologies and Innovations: Highlights important technological advancements in the field of diesel bus chassis, which include efficient engine performance, emissions compliance technology, exhaust treatments, telematics connectivity, and design optimization for different routes used in urban, intercity, school, and personnel transportation purposes.

- Performance of Leading Companies within Vehicle Chassis Applications and Positioning in the Market: Evaluates the relative performance of industry-leading companies within various diesel bus applications based on parameters such as reliability, fuel economy, route compatibility, emissions compliance, customer service, manufacturing capability, and aftermarket capabilities.

- Market Demand and Practical Uses of Diesel Buses: Specifies actual situations where diesel buses can still be used, namely in public transit, intercity transportation, school buses, and personnel buses.

- Industry Trends and Market News: Covers important industry trends like new bus introductions, fleet purchases, manufacturing capacity increases, localisation initiatives, regulations, and purchasing information from around the world, especially in Asia-Pacific, Europe, China, and India.

- Strategic Business Plan: Details how key competitors have used strategic moves to improve their standing by enhancing their products, expanding geographically, partnering, manufacturing locally, and growing their aftersales networks.

- Product Pricing and Marketing Strategy: Offers an understanding of diesel bus price competition, channel management, bidding activities, dealership effectiveness, and post-sales value creation in various geographic locations.

- Market Development Opportunities and Growth Strategy: Points out areas that are yet to be explored, covering peri-urban bus services, long-distance transportation, employee commuting, replacement business, and exports.

Target Audience

- OEMs and product developers active across the diesel bus value chain

- Distributors, channel partners, and regional aggregators

- Strategy teams, product managers, and corporate development leaders

- Procurement heads and technical buyers at key end users

- Investors, consultants, and market intelligence teams tracking emerging growth pockets